TAXATION 3 Report: Detailed Analysis of Australian Taxation Law Cases

VerifiedAdded on 2020/03/28

|15

|2962

|32

Report

AI Summary

This report provides a comprehensive analysis of various taxation scenarios under Australian tax law. It begins by examining capital gains and losses, specifically addressing the offset of losses from collectibles against other gains, referencing relevant sections of the ITAA 1997. The report then delves into Fringe Benefit Tax (FBT), exploring the implications of loan interest offsets based on Taxation Ruling TR 93/6. The analysis extends to rental property taxation, focusing on the allocation of losses between co-owners, referencing Taxation Ruling TR 93/32 and the case of F.C of T.v Mc Donald (1987). The report also discusses tax avoidance, referencing TRC v Duke of Westminster [1936] AC 1 and WR Ramsey v.IRC principles. Finally, the report assesses the taxation of revenue generated from selling wood cut from land used for sheep grazing, referencing Subsection 6(1) of the Income Tax Assessment Act 1936 and Taxation Ruling 95/6, concluding that the revenue is considered disposable income from primary production.

Running head: TAXATION

Taxation

Name of the Student:

Name of the University:

Author’s Note:

Taxation

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

TAXATION

Table of Contents

Answer to Question No 1...........................................................................................................3

Issue:......................................................................................................................................3

Laws:......................................................................................................................................3

Calculations:...........................................................................................................................3

Applications:..........................................................................................................................3

Conclusion..............................................................................................................................4

Answer to Question No 2...........................................................................................................4

Issue:......................................................................................................................................4

Laws:......................................................................................................................................4

Calculations:...........................................................................................................................5

Applications:..........................................................................................................................5

Conclusion..............................................................................................................................6

Answer to Question No 3...........................................................................................................6

Issue:......................................................................................................................................6

Laws:......................................................................................................................................6

Applications:..........................................................................................................................6

Conclusion..............................................................................................................................8

Answer to Question No 4...........................................................................................................8

Answer to Question No 5...........................................................................................................9

Issue:......................................................................................................................................9

Laws.......................................................................................................................................9

TAXATION

Table of Contents

Answer to Question No 1...........................................................................................................3

Issue:......................................................................................................................................3

Laws:......................................................................................................................................3

Calculations:...........................................................................................................................3

Applications:..........................................................................................................................3

Conclusion..............................................................................................................................4

Answer to Question No 2...........................................................................................................4

Issue:......................................................................................................................................4

Laws:......................................................................................................................................4

Calculations:...........................................................................................................................5

Applications:..........................................................................................................................5

Conclusion..............................................................................................................................6

Answer to Question No 3...........................................................................................................6

Issue:......................................................................................................................................6

Laws:......................................................................................................................................6

Applications:..........................................................................................................................6

Conclusion..............................................................................................................................8

Answer to Question No 4...........................................................................................................8

Answer to Question No 5...........................................................................................................9

Issue:......................................................................................................................................9

Laws.......................................................................................................................................9

2

TAXATION

Applications:..........................................................................................................................9

Conclusion............................................................................................................................11

Reference List..........................................................................................................................12

TAXATION

Applications:..........................................................................................................................9

Conclusion............................................................................................................................11

Reference List..........................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

TAXATION

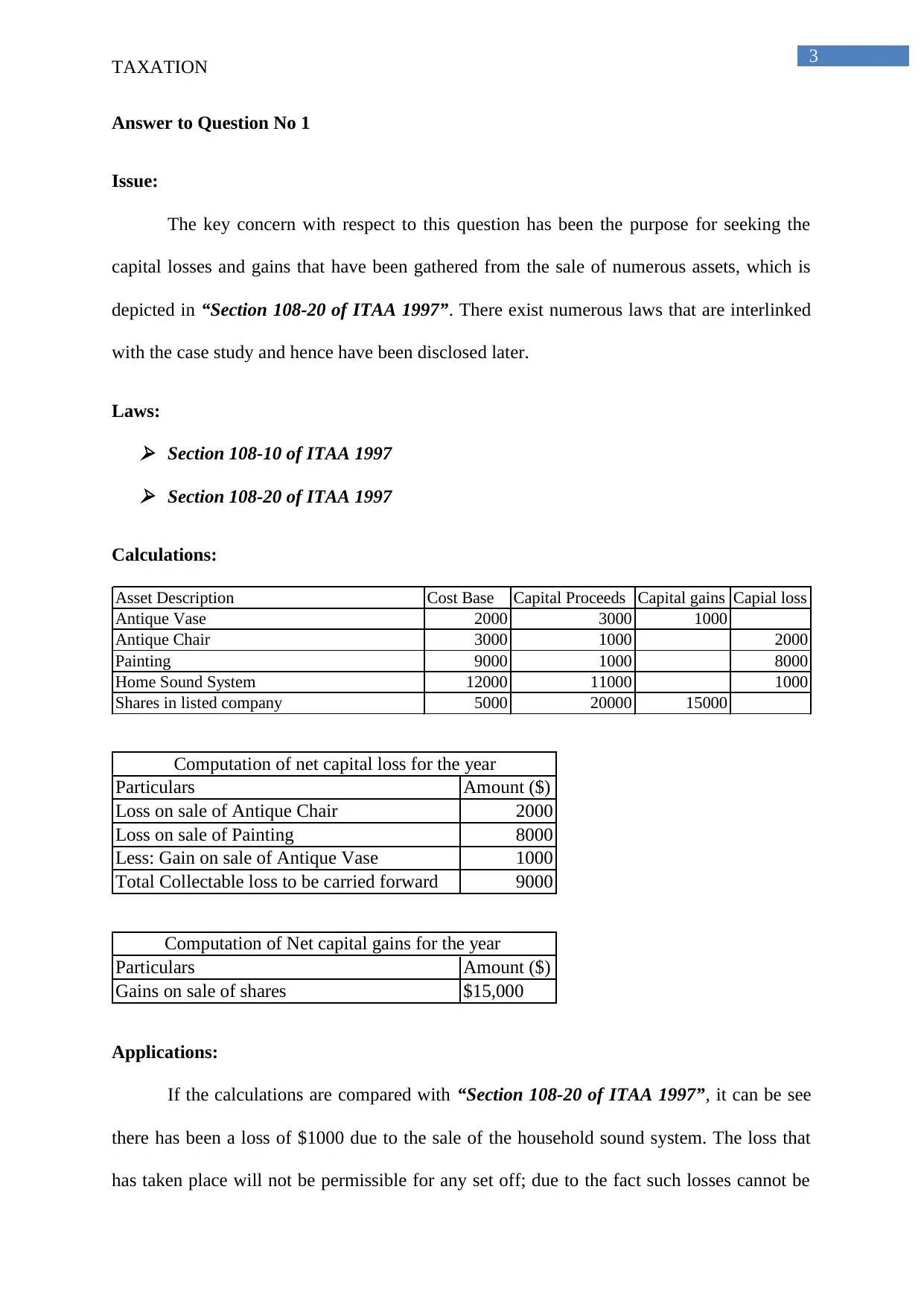

Answer to Question No 1

Issue:

The key concern with respect to this question has been the purpose for seeking the

capital losses and gains that have been gathered from the sale of numerous assets, which is

depicted in “Section 108-20 of ITAA 1997”. There exist numerous laws that are interlinked

with the case study and hence have been disclosed later.

Laws: Section 108-10 of ITAA 1997 Section 108-20 of ITAA 1997

Calculations:

Asset Description Cost Base Capital Proceeds Capital gains Capial loss

Antique Vase 2000 3000 1000

Antique Chair 3000 1000 2000

Painting 9000 1000 8000

Home Sound System 12000 11000 1000

Shares in listed company 5000 20000 15000

Particulars Amount ($)

Loss on sale of Antique Chair 2000

Loss on sale of Painting 8000

Less: Gain on sale of Antique Vase 1000

Total Collectable loss to be carried forward 9000

Computation of net capital loss for the year

Particulars Amount ($)

Gains on sale of shares $15,000

Computation of Net capital gains for the year

Applications:

If the calculations are compared with “Section 108-20 of ITAA 1997”, it can be see

there has been a loss of $1000 due to the sale of the household sound system. The loss that

has taken place will not be permissible for any set off; due to the fact such losses cannot be

TAXATION

Answer to Question No 1

Issue:

The key concern with respect to this question has been the purpose for seeking the

capital losses and gains that have been gathered from the sale of numerous assets, which is

depicted in “Section 108-20 of ITAA 1997”. There exist numerous laws that are interlinked

with the case study and hence have been disclosed later.

Laws: Section 108-10 of ITAA 1997 Section 108-20 of ITAA 1997

Calculations:

Asset Description Cost Base Capital Proceeds Capital gains Capial loss

Antique Vase 2000 3000 1000

Antique Chair 3000 1000 2000

Painting 9000 1000 8000

Home Sound System 12000 11000 1000

Shares in listed company 5000 20000 15000

Particulars Amount ($)

Loss on sale of Antique Chair 2000

Loss on sale of Painting 8000

Less: Gain on sale of Antique Vase 1000

Total Collectable loss to be carried forward 9000

Computation of net capital loss for the year

Particulars Amount ($)

Gains on sale of shares $15,000

Computation of Net capital gains for the year

Applications:

If the calculations are compared with “Section 108-20 of ITAA 1997”, it can be see

there has been a loss of $1000 due to the sale of the household sound system. The loss that

has taken place will not be permissible for any set off; due to the fact such losses cannot be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

TAXATION

permitted by relying on the disposal of the person making use of the assets. In conformity to

“Section 108-10 of ITAA 1997” the collectable losses may not be set off in regards to the

common gains that takes place from the selling off the shares (Petty et al., 2015).

Additionally, the offset can be considered in comparison to “Section 108-10 of ITAA 1997”.

As Eric has accomplished a profit by discarding the ordinary assets and there is no presence

of general capital or any other types that can be incorporated for deductions. Furthermore, the

capital gains for Eric have a current value of $15,000.

Conclusion

After observing the scenario of the question, it is concluded that Eric does not possess

the capacity to offset his losses that has been gathered from his collectibles as Eric has been

able to gain profit from the disposal of the general asset.

Answer to Question No 2

Issue:

The concern in this question has been to ascertain the Fringe Benefit Tax that is in

relation to “Taxation ruling of TR 93/6”. With respect to this question that rules and the

laws that are applicable are:

Laws: Taxation Rulings of TR 93/6

TAXATION

permitted by relying on the disposal of the person making use of the assets. In conformity to

“Section 108-10 of ITAA 1997” the collectable losses may not be set off in regards to the

common gains that takes place from the selling off the shares (Petty et al., 2015).

Additionally, the offset can be considered in comparison to “Section 108-10 of ITAA 1997”.

As Eric has accomplished a profit by discarding the ordinary assets and there is no presence

of general capital or any other types that can be incorporated for deductions. Furthermore, the

capital gains for Eric have a current value of $15,000.

Conclusion

After observing the scenario of the question, it is concluded that Eric does not possess

the capacity to offset his losses that has been gathered from his collectibles as Eric has been

able to gain profit from the disposal of the general asset.

Answer to Question No 2

Issue:

The concern in this question has been to ascertain the Fringe Benefit Tax that is in

relation to “Taxation ruling of TR 93/6”. With respect to this question that rules and the

laws that are applicable are:

Laws: Taxation Rulings of TR 93/6

5

TAXATION

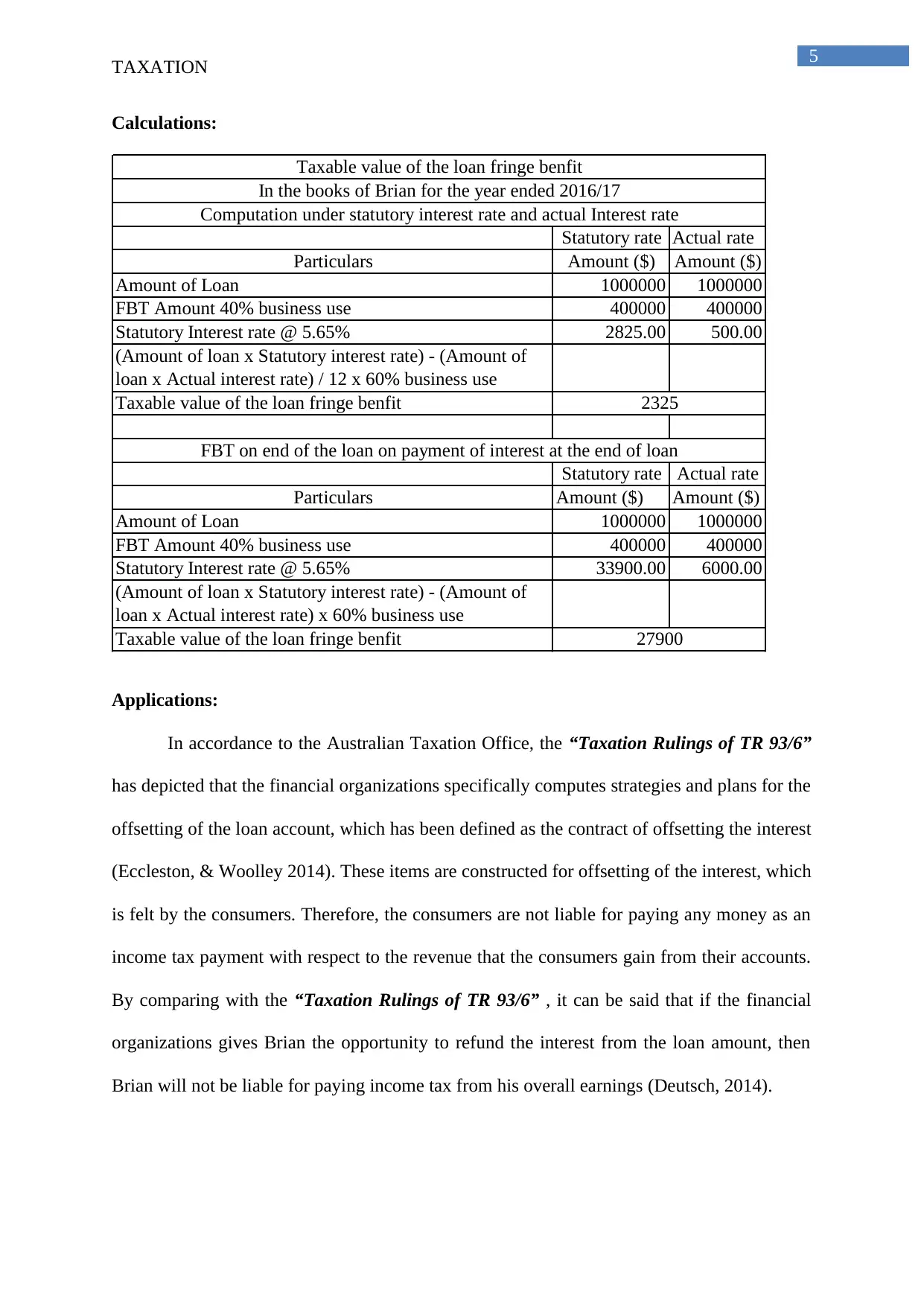

Calculations:

Statutory rate Actual rate

Particulars Amount ($) Amount ($)

Amount of Loan 1000000 1000000

FBT Amount 40% business use 400000 400000

Statutory Interest rate @ 5.65% 2825.00 500.00

(Amount of loan x Statutory interest rate) - (Amount of

loan x Actual interest rate) / 12 x 60% business use

Taxable value of the loan fringe benfit

Statutory rate Actual rate

Particulars Amount ($) Amount ($)

Amount of Loan 1000000 1000000

FBT Amount 40% business use 400000 400000

Statutory Interest rate @ 5.65% 33900.00 6000.00

(Amount of loan x Statutory interest rate) - (Amount of

loan x Actual interest rate) x 60% business use

Taxable value of the loan fringe benfit

2325

27900

FBT on end of the loan on payment of interest at the end of loan

Taxable value of the loan fringe benfit

In the books of Brian for the year ended 2016/17

Computation under statutory interest rate and actual Interest rate

Applications:

In accordance to the Australian Taxation Office, the “Taxation Rulings of TR 93/6”

has depicted that the financial organizations specifically computes strategies and plans for the

offsetting of the loan account, which has been defined as the contract of offsetting the interest

(Eccleston, & Woolley 2014). These items are constructed for offsetting of the interest, which

is felt by the consumers. Therefore, the consumers are not liable for paying any money as an

income tax payment with respect to the revenue that the consumers gain from their accounts.

By comparing with the “Taxation Rulings of TR 93/6” , it can be said that if the financial

organizations gives Brian the opportunity to refund the interest from the loan amount, then

Brian will not be liable for paying income tax from his overall earnings (Deutsch, 2014).

TAXATION

Calculations:

Statutory rate Actual rate

Particulars Amount ($) Amount ($)

Amount of Loan 1000000 1000000

FBT Amount 40% business use 400000 400000

Statutory Interest rate @ 5.65% 2825.00 500.00

(Amount of loan x Statutory interest rate) - (Amount of

loan x Actual interest rate) / 12 x 60% business use

Taxable value of the loan fringe benfit

Statutory rate Actual rate

Particulars Amount ($) Amount ($)

Amount of Loan 1000000 1000000

FBT Amount 40% business use 400000 400000

Statutory Interest rate @ 5.65% 33900.00 6000.00

(Amount of loan x Statutory interest rate) - (Amount of

loan x Actual interest rate) x 60% business use

Taxable value of the loan fringe benfit

2325

27900

FBT on end of the loan on payment of interest at the end of loan

Taxable value of the loan fringe benfit

In the books of Brian for the year ended 2016/17

Computation under statutory interest rate and actual Interest rate

Applications:

In accordance to the Australian Taxation Office, the “Taxation Rulings of TR 93/6”

has depicted that the financial organizations specifically computes strategies and plans for the

offsetting of the loan account, which has been defined as the contract of offsetting the interest

(Eccleston, & Woolley 2014). These items are constructed for offsetting of the interest, which

is felt by the consumers. Therefore, the consumers are not liable for paying any money as an

income tax payment with respect to the revenue that the consumers gain from their accounts.

By comparing with the “Taxation Rulings of TR 93/6” , it can be said that if the financial

organizations gives Brian the opportunity to refund the interest from the loan amount, then

Brian will not be liable for paying income tax from his overall earnings (Deutsch, 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

TAXATION

Conclusion

After the analysis of this question, it can be explained that Brian does not require to

pay any amount of money for the purpose of income tax if Brian is excused from any sort of

banking interest.

Answer to Question No 3

Issue:

The concern in this question has been determining the allocation of the losses that has

been faced from a property that is rented and is even under the co-ownership of Jack and Jill.

The rules ideal for this situation are:

Laws: Taxation Rulings of TR 93/32 FC of the T.v Mc Donald (1987) Section 51 of ITAA 1997

Applications:

“Taxation Rulings of TR 93/32” explains the depiction of the divisionary net losses

or income that is generated from the rental property between the co-owners of the land that

has been discussed in this question. Additionally, the rules for taxation have been essentially

considered for the examination of the taxable scenario of the dual owners who are liable for

transmitting their values into proceedings. The current scenario of Jack and Jill has the goal

of investigating the taxable scenario of the property that is rented in nature. It is being viewed

that Jack has been qualified for a percentage of 10% of the property and on the other hand Jill

has the eligibility of a percentage of 90% of the same property.

TAXATION

Conclusion

After the analysis of this question, it can be explained that Brian does not require to

pay any amount of money for the purpose of income tax if Brian is excused from any sort of

banking interest.

Answer to Question No 3

Issue:

The concern in this question has been determining the allocation of the losses that has

been faced from a property that is rented and is even under the co-ownership of Jack and Jill.

The rules ideal for this situation are:

Laws: Taxation Rulings of TR 93/32 FC of the T.v Mc Donald (1987) Section 51 of ITAA 1997

Applications:

“Taxation Rulings of TR 93/32” explains the depiction of the divisionary net losses

or income that is generated from the rental property between the co-owners of the land that

has been discussed in this question. Additionally, the rules for taxation have been essentially

considered for the examination of the taxable scenario of the dual owners who are liable for

transmitting their values into proceedings. The current scenario of Jack and Jill has the goal

of investigating the taxable scenario of the property that is rented in nature. It is being viewed

that Jack has been qualified for a percentage of 10% of the property and on the other hand Jill

has the eligibility of a percentage of 90% of the same property.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAXATION

By looking at “Taxation Ruling TR 93/32”, it can be said that the co-ownership of

the property that is rented is looked upon as a sort of partnership for the income tax purpose

but this has not been looked down as an personal partnership at the general law, in which the

co-partnership is looked down as a kind of partnership for satisfying the purpose of income

tax (Taylor, & Richardson 2014). The loss that has taken place from the income received

from the rental property is supervised and managed by taking help of the co-ownership of the

rental estate and also from the distribution of the profit and loss of the partnerships. The

current condition of Jack and Jill has depicted that the co-ownership of the rented estate

among each other, which is reliant on the rationale of the income tax and hence will be

regarded as a partnership in accordance to the general law.

The “Taxation Ruling of TR 93/32” has depicted that the co-owners of the estate that

is rented are distinctly not considered as partners if looked in the general. In this respect, the

contract of the partnership, which has been constructed in a written manner or verbally

becomes ineffective on the income shared value and the loss that is incurred from the rented

estate (Lee et al., 2016). Thus, the co-owners of the rented estate in this respect who are Jack

and Jill will hold the property as co-holders and renters due to personal common factor.

By looking at the case of “F.C of T.v Mc Donald (1987) 18 ATR 957”, Mr and Mrs

Mc Donald has the authority to hold two segments of the units of the titles as they have been

regarded as the co-renters. The agreement or the contract that has been prepared among them

has explained that the net profit that has incurred from the rented estate would comprise of

25% to Mr. Mc Donald and on the other hand Mrs Mc Donald would be liable for the rest

75% of the property. In this condition, the total loss value that has been faced is taken up by

Mr Mc Donald.

TAXATION

By looking at “Taxation Ruling TR 93/32”, it can be said that the co-ownership of

the property that is rented is looked upon as a sort of partnership for the income tax purpose

but this has not been looked down as an personal partnership at the general law, in which the

co-partnership is looked down as a kind of partnership for satisfying the purpose of income

tax (Taylor, & Richardson 2014). The loss that has taken place from the income received

from the rental property is supervised and managed by taking help of the co-ownership of the

rental estate and also from the distribution of the profit and loss of the partnerships. The

current condition of Jack and Jill has depicted that the co-ownership of the rented estate

among each other, which is reliant on the rationale of the income tax and hence will be

regarded as a partnership in accordance to the general law.

The “Taxation Ruling of TR 93/32” has depicted that the co-owners of the estate that

is rented are distinctly not considered as partners if looked in the general. In this respect, the

contract of the partnership, which has been constructed in a written manner or verbally

becomes ineffective on the income shared value and the loss that is incurred from the rented

estate (Lee et al., 2016). Thus, the co-owners of the rented estate in this respect who are Jack

and Jill will hold the property as co-holders and renters due to personal common factor.

By looking at the case of “F.C of T.v Mc Donald (1987) 18 ATR 957”, Mr and Mrs

Mc Donald has the authority to hold two segments of the units of the titles as they have been

regarded as the co-renters. The agreement or the contract that has been prepared among them

has explained that the net profit that has incurred from the rented estate would comprise of

25% to Mr. Mc Donald and on the other hand Mrs Mc Donald would be liable for the rest

75% of the property. In this condition, the total loss value that has been faced is taken up by

Mr Mc Donald.

8

TAXATION

Conclusion

The evaluation of the case background has established the solution that Jack and Jill

both requires to distribute the loss incurred equivalently and the co-ownership is not looked

upon as partnership venture.

Answer to Question No 4

The most commonly cited tax avoidance incident has been “TRC v Duke of

Westminster [1936] AC 1”. The case in this question has developed a principle that defines

that every individual is allowed to regulate their operations for granting the taxation

allocation, which has been framed within the Act that has been deemed appropriate. This

taxation allotment is very low with respect to before. Although, it can be said that this ruling

mechanism has been conspicuous for the other consumers who are seeking for the avoidance

of tax with respect to the complicated model of laws and they are moved by taking assistance

of the accomplished cases where the courts or the legal systems have experienced in the total

impact(Isa, 2014). By taking assistance of giving out an instance of the court for the future

aspects that has been much more restrictive and were implemented was in the “WR Ramsey

v.IRC principle”. In these circumstances, the transactions have been ordered at an initial

stage in a false process and this has not been helpful for any nature of commercial intentions.

The efficient rule has always been to charge the tax for broadening the transactions as an

entire proof.

In the scenario, which has been modern in this era, the principle and the rule within

the nation of Australia depicts that in the situation where a person achieves victory for

making sure that this result has been secured, the Inland Revenue has to be due to their

program and they may not be forced to pay for any extra amount of tax. Nevertheless, the

idea has has been incorporated is that this element grants the companies and persons for

TAXATION

Conclusion

The evaluation of the case background has established the solution that Jack and Jill

both requires to distribute the loss incurred equivalently and the co-ownership is not looked

upon as partnership venture.

Answer to Question No 4

The most commonly cited tax avoidance incident has been “TRC v Duke of

Westminster [1936] AC 1”. The case in this question has developed a principle that defines

that every individual is allowed to regulate their operations for granting the taxation

allocation, which has been framed within the Act that has been deemed appropriate. This

taxation allotment is very low with respect to before. Although, it can be said that this ruling

mechanism has been conspicuous for the other consumers who are seeking for the avoidance

of tax with respect to the complicated model of laws and they are moved by taking assistance

of the accomplished cases where the courts or the legal systems have experienced in the total

impact(Isa, 2014). By taking assistance of giving out an instance of the court for the future

aspects that has been much more restrictive and were implemented was in the “WR Ramsey

v.IRC principle”. In these circumstances, the transactions have been ordered at an initial

stage in a false process and this has not been helpful for any nature of commercial intentions.

The efficient rule has always been to charge the tax for broadening the transactions as an

entire proof.

In the scenario, which has been modern in this era, the principle and the rule within

the nation of Australia depicts that in the situation where a person achieves victory for

making sure that this result has been secured, the Inland Revenue has to be due to their

program and they may not be forced to pay for any extra amount of tax. Nevertheless, the

idea has has been incorporated is that this element grants the companies and persons for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

TAXATION

constructing financial agreement in accordance to the goals and objectives that have been set

for reducing the tax liabilities that is reliant on their models under numerous law models.

Answer to Question No 5

Issue:

In the present condition, the assessment of the sales revenue has been ascertained by

selling off the wood that has been cut down from the land in order to herd the sheep. This

scenario has been constructed by taking help of the “Subsection 6(1) of the Income tax

Assessment Act 1936”. The rules that are interlinked with this case are as follows:

Laws McCauley v. The Federal Commissioner of Taxation Subsection 6(1) of the Income tax Assessment Act 1936.

Applications:

With respect to the present business scenario, it is seen that Bill has been the owner of

a vast land where there is the presence of a number of pine trees. The intention of Bill has

been to make use of the land by grazing his sheep and in order to do so; he wants the land to

be cleared off. Bill has disclosed that there is a tree cutting company who have said that they

would be paying Bill $1000 for every 100 meters of the land clear off. The log cutting

company therefore has the opportunity to grasp the portion of Bill’s land. The “Taxation

Ruling of 95/6” has brought forward that the circumstances of income tax that is generated

from the activities of the primary forestry and manufacturing. This mechanism of ruling has

proposed a limitation of the earnings that is gained from the sale of wood. This element

consists of the revenues that is measurable and whether the person who are paying the taxes

are indulged in the activities of the forest business. “Subsection 6 (1) of the Income tax

TAXATION

constructing financial agreement in accordance to the goals and objectives that have been set

for reducing the tax liabilities that is reliant on their models under numerous law models.

Answer to Question No 5

Issue:

In the present condition, the assessment of the sales revenue has been ascertained by

selling off the wood that has been cut down from the land in order to herd the sheep. This

scenario has been constructed by taking help of the “Subsection 6(1) of the Income tax

Assessment Act 1936”. The rules that are interlinked with this case are as follows:

Laws McCauley v. The Federal Commissioner of Taxation Subsection 6(1) of the Income tax Assessment Act 1936.

Applications:

With respect to the present business scenario, it is seen that Bill has been the owner of

a vast land where there is the presence of a number of pine trees. The intention of Bill has

been to make use of the land by grazing his sheep and in order to do so; he wants the land to

be cleared off. Bill has disclosed that there is a tree cutting company who have said that they

would be paying Bill $1000 for every 100 meters of the land clear off. The log cutting

company therefore has the opportunity to grasp the portion of Bill’s land. The “Taxation

Ruling of 95/6” has brought forward that the circumstances of income tax that is generated

from the activities of the primary forestry and manufacturing. This mechanism of ruling has

proposed a limitation of the earnings that is gained from the sale of wood. This element

consists of the revenues that is measurable and whether the person who are paying the taxes

are indulged in the activities of the forest business. “Subsection 6 (1) of the Income tax

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

TAXATION

Assessment Act 1936”, the primary manufacturing is specifically defined as the tree

plantation with an area, which would be used later for the purpose of cutting. By observing

the present situation, Bill has been regarded as the basic producer as he has been busy in

process of primary production in accordance to “Subsection 6 (1) of the Income Tax

Assessment Act 1936”. The functions within the forest include cutting the trees down of a

wood or plantation even though the individuals paying tax are not concerned about the

planted trees.

Bill is the owner of a huge piece of land and in this land he has not planted any trees

but conversely, the total income generated from the land by Bill with the help of the sale of

woods has been identified as income that is disposable and therefore has focused for the aim

of sales that has been created as an income segment that is permissible (McCluskey, &

Franzsen 2017). In spite of these reasons, the sales has been looked upon as a mixture

permanently and partially for the individuals paying tax in accordance to “Subsection 6 (1) of

the Income Tax Assessment Act 1936”.

On the other hand, if the taxpaying personnel was paid an entire amount of 450,000

by proving the power to cut the amount of trees that are necessary, then in that case, the entire

amount that will be earned will be looked upon as the royalties. It is similar to “Section 26

(f)” where the earnings from the royalties by an individual for having the power to sell the

trees that has been logged from his land. In such situations, Bill will not be considered for

undertaking trading operations on the forest. in compliance, it has been considered that the

individual who pays tax did not plant the trees for the cutting purpose in order to gain benefit

out of the same. It has been observed that in “Mc Cauley v. The Federal Commissioner of

Tax”, the payments that are received by the lender come under the supremacy of undertaking

the same. The values that are similar and are gained by Bill as a form of royalty is mixed with

the earnings that is permissible in accordance to “Section 26(f)”.

TAXATION

Assessment Act 1936”, the primary manufacturing is specifically defined as the tree

plantation with an area, which would be used later for the purpose of cutting. By observing

the present situation, Bill has been regarded as the basic producer as he has been busy in

process of primary production in accordance to “Subsection 6 (1) of the Income Tax

Assessment Act 1936”. The functions within the forest include cutting the trees down of a

wood or plantation even though the individuals paying tax are not concerned about the

planted trees.

Bill is the owner of a huge piece of land and in this land he has not planted any trees

but conversely, the total income generated from the land by Bill with the help of the sale of

woods has been identified as income that is disposable and therefore has focused for the aim

of sales that has been created as an income segment that is permissible (McCluskey, &

Franzsen 2017). In spite of these reasons, the sales has been looked upon as a mixture

permanently and partially for the individuals paying tax in accordance to “Subsection 6 (1) of

the Income Tax Assessment Act 1936”.

On the other hand, if the taxpaying personnel was paid an entire amount of 450,000

by proving the power to cut the amount of trees that are necessary, then in that case, the entire

amount that will be earned will be looked upon as the royalties. It is similar to “Section 26

(f)” where the earnings from the royalties by an individual for having the power to sell the

trees that has been logged from his land. In such situations, Bill will not be considered for

undertaking trading operations on the forest. in compliance, it has been considered that the

individual who pays tax did not plant the trees for the cutting purpose in order to gain benefit

out of the same. It has been observed that in “Mc Cauley v. The Federal Commissioner of

Tax”, the payments that are received by the lender come under the supremacy of undertaking

the same. The values that are similar and are gained by Bill as a form of royalty is mixed with

the earnings that is permissible in accordance to “Section 26(f)”.

11

TAXATION

Conclusion

The examination of this case explains that income derived from the logging if the

tress would be looked upon as the earnings that are taxable in accordance to “Subsection 6(1)

of ITAA 1997”.

TAXATION

Conclusion

The examination of this case explains that income derived from the logging if the

tress would be looked upon as the earnings that are taxable in accordance to “Subsection 6(1)

of ITAA 1997”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.