Taxation Law Case Study: Gold Coast, QLD, Taxation Advice for Clients

VerifiedAdded on 2022/09/16

|10

|1431

|8

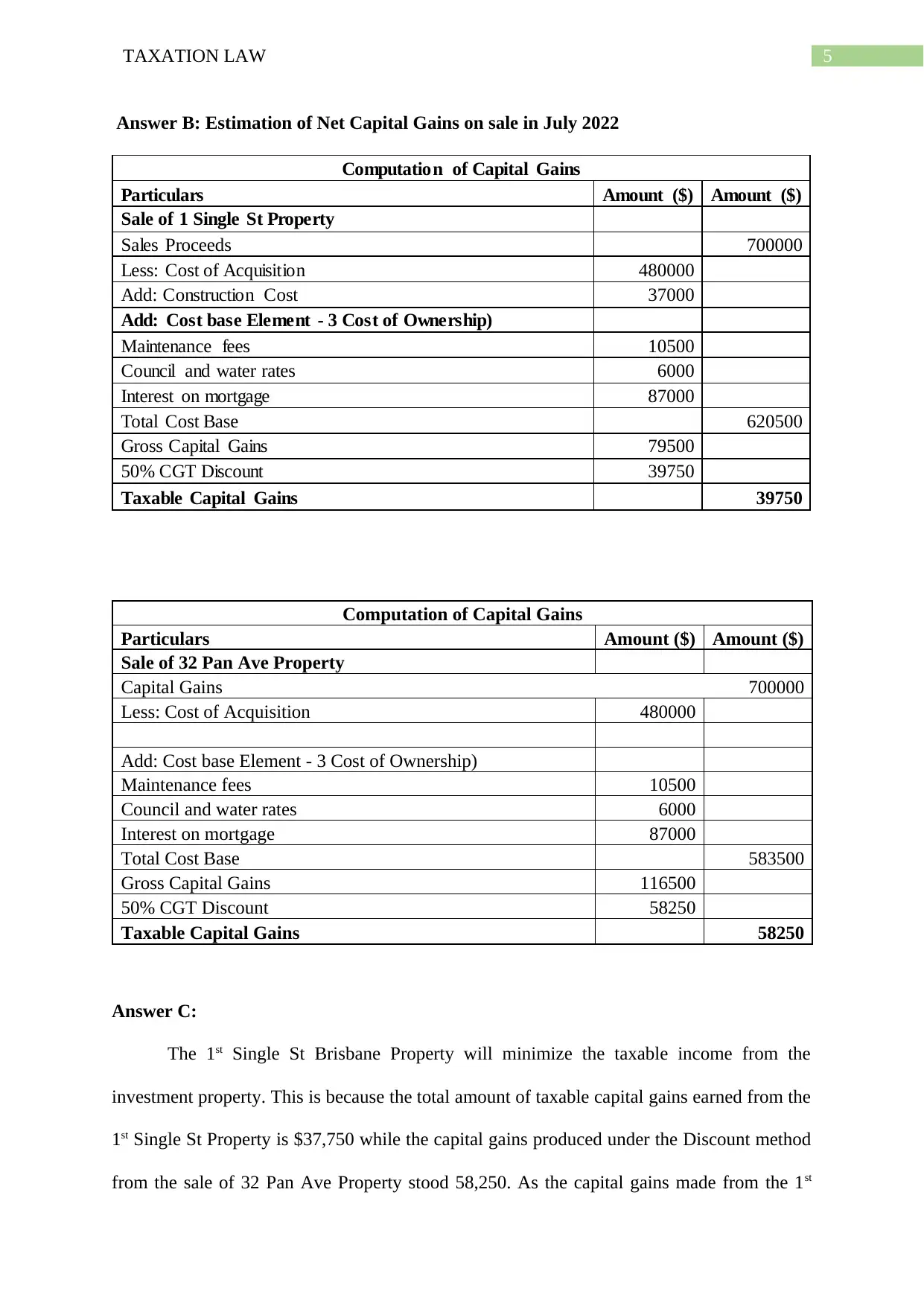

Case Study

AI Summary

This case study analyzes the taxation implications of various financial decisions for Matt and Miranda Murphy, an Australian married couple. The assignment delves into share investments, rental property income and losses, and the optimal business structure for their situation. It explores the computation of tax payable, net rental income, and capital gains, including the application of CGT discounts. The solution recommends strategies such as transferring share ownership to minimize tax liabilities and suggests the use of a discretionary family trust for asset protection and tax advantages. The analysis considers the tax implications of different business structures, including sole trader, Australian private company, and partnership, ultimately recommending the discretionary trust. Furthermore, it addresses asset distribution in the event of a marriage breakdown, including rollover relief for capital gains tax. The case study utilizes relevant Australian taxation law principles, providing practical advice based on the facts presented.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.