Taxation Assignment: Residency, Business Income, and Tax Liabilities

VerifiedAdded on 2022/10/17

|11

|2357

|16

Case Study

AI Summary

This case study analyzes Australian taxation, focusing on residency, income, and business activities. Part A examines Rachel, a medical practitioner from London, and determines her tax residency status based on ATO guidelines, considering her family ties, bank accounts, and the 183-day test. It assesses her income from various sources, including foreign interest and Australian salary, to determine her tax liabilities. Part B analyzes John's residency status, comparing his situation to the Harding v Commissioner of Taxation case. Case study 2 explores the distinction between a hobby and a business for tax purposes, using Nadine's painting activity as an example. Case study 3 discusses the taxation of workers, including employees and contract workers, PAYG, payroll tax, and fringe benefits tax. Finally, the case study provides an accounting analysis of Sam's financial year, calculating his total liabilities based on his receipts and payments, and determining his taxable income.

Taxation

by [Name]

Course

Professor’s Name

Institution

Date

by [Name]

Course

Professor’s Name

Institution

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Taxation

The Australian Tax Office (ATO) on behalf of the federal government does taxation on

Income in Australia. Income tax is generally charged on the income of corporations and

individuals. With the increase in mobility of labor and capital, it becomes more challenging for a

government to tax income from foreign countries, and these calls for more clear criteria.

Part A

Rachel will be subjected to the residency for tax purposes tests as per the Australian Tax Office

(ATO). Taking the first as the ‘resides,' Rachel is in Australia, has family ties(spouse and two

children) in Australia, has bank accounts in her names and also has social and living provisions,

this qualifies her as a resident for tax purposes regarding this test.

Another test performed to determine an individual’s residence for tax purposes in Australia is the

Superannuation test, this calls for individuals who are employed by the Australian government

with duty stations abroad to be considered Australian residents for tax purposes1. This test does

not apply to Rachel since her duty station is in Australia.

Considering the 183-day test, this studies whether you have been staying in Australia for more

than half the financial year. It doesn’t matter whether daily or intermittently. Tests your usual

place of abode, and whether you intend to acquire a residence in the area. According to this test,

Rachel has stayed in Australia for more than 183 days, her usual place of abode is London

(outside Australia), has no intention of taking up residence in Australia since her and her family

plan going back to London and therefore her residence in Australia is not constructive as per the

183 days rule2. She will be considered a resident for tax purposes since she fulfills the test.

1 Mayo, Wayne, Time to Upgrade Australia’s Company Tax System From Imputation to Integration (July 31, 2018).

Australian Tax Forum, Vol. 33(4), 2018. Available at SSRN: https://ssrn.com/abstract=3311250

2 Australian Government. Residency-The The 183-day test. 2019. Available at https://www.investopedia.com

Taxation

The Australian Tax Office (ATO) on behalf of the federal government does taxation on

Income in Australia. Income tax is generally charged on the income of corporations and

individuals. With the increase in mobility of labor and capital, it becomes more challenging for a

government to tax income from foreign countries, and these calls for more clear criteria.

Part A

Rachel will be subjected to the residency for tax purposes tests as per the Australian Tax Office

(ATO). Taking the first as the ‘resides,' Rachel is in Australia, has family ties(spouse and two

children) in Australia, has bank accounts in her names and also has social and living provisions,

this qualifies her as a resident for tax purposes regarding this test.

Another test performed to determine an individual’s residence for tax purposes in Australia is the

Superannuation test, this calls for individuals who are employed by the Australian government

with duty stations abroad to be considered Australian residents for tax purposes1. This test does

not apply to Rachel since her duty station is in Australia.

Considering the 183-day test, this studies whether you have been staying in Australia for more

than half the financial year. It doesn’t matter whether daily or intermittently. Tests your usual

place of abode, and whether you intend to acquire a residence in the area. According to this test,

Rachel has stayed in Australia for more than 183 days, her usual place of abode is London

(outside Australia), has no intention of taking up residence in Australia since her and her family

plan going back to London and therefore her residence in Australia is not constructive as per the

183 days rule2. She will be considered a resident for tax purposes since she fulfills the test.

1 Mayo, Wayne, Time to Upgrade Australia’s Company Tax System From Imputation to Integration (July 31, 2018).

Australian Tax Forum, Vol. 33(4), 2018. Available at SSRN: https://ssrn.com/abstract=3311250

2 Australian Government. Residency-The The 183-day test. 2019. Available at https://www.investopedia.com

2

Australia's taxation of income from foreign countries exempts businesses from income for which

a tax has already been levied from the source country and encourages payment of tax for stable

income in the source country. Residents of Australia pay tax on their foreign income and also

income in their state which does not exclude capital gains3.

The source of income principles requires that Australian residents for tax purposes declare all

income earned both domestically and outside on their Australian tax profit regardless of whether

they have already paid tax on the income overseas.4 Rachel will be charged tax on her interest

earned on the bank account held in London $2500(EUR), salary and wages on her work before

going to Australia $45,000(EUR), salary and wage income from her Perth job $120,000(AUD).

A tax will also be levied on the Australian salary and her deductions relating to her job at the

hospital.

Part B

Taking into account John's purpose of presence in Australia, family and business ties, whether he

has open bank accounts, social and living arrangements that are the 'resides' test. He fulfills none

of these requirements, which leads us to test other tests on John.

Subjecting John to the 183-day test gives us the result that John is not considered a resident for

tax purposes for the years 2017/2018 and 2018/2019 as per the 183-day test since he was not in

Australia for those days.

The superannuation test requires that individuals employed by the Australian government

working overseas be considered Australian residents for tax purposes. John is not in this category

3 John, McLaren. Should the international income of an Australian resident be taxed on a worldwide or territorial

basis? 2006. Available at https://pdfs.semanticscholar.org/932c/caac062cdd28c1cc5e27fbad617e9345e63f.pdf

4 The Australian tax office, Work out your tax residency, the Australian government, 2018.

Australia's taxation of income from foreign countries exempts businesses from income for which

a tax has already been levied from the source country and encourages payment of tax for stable

income in the source country. Residents of Australia pay tax on their foreign income and also

income in their state which does not exclude capital gains3.

The source of income principles requires that Australian residents for tax purposes declare all

income earned both domestically and outside on their Australian tax profit regardless of whether

they have already paid tax on the income overseas.4 Rachel will be charged tax on her interest

earned on the bank account held in London $2500(EUR), salary and wages on her work before

going to Australia $45,000(EUR), salary and wage income from her Perth job $120,000(AUD).

A tax will also be levied on the Australian salary and her deductions relating to her job at the

hospital.

Part B

Taking into account John's purpose of presence in Australia, family and business ties, whether he

has open bank accounts, social and living arrangements that are the 'resides' test. He fulfills none

of these requirements, which leads us to test other tests on John.

Subjecting John to the 183-day test gives us the result that John is not considered a resident for

tax purposes for the years 2017/2018 and 2018/2019 as per the 183-day test since he was not in

Australia for those days.

The superannuation test requires that individuals employed by the Australian government

working overseas be considered Australian residents for tax purposes. John is not in this category

3 John, McLaren. Should the international income of an Australian resident be taxed on a worldwide or territorial

basis? 2006. Available at https://pdfs.semanticscholar.org/932c/caac062cdd28c1cc5e27fbad617e9345e63f.pdf

4 The Australian tax office, Work out your tax residency, the Australian government, 2018.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

and therefore, not considered a taxpayer to the Australian government all his time in Brunei

under the superannuation test.

John fulfills the domicile test with his permanent home is in Australia since he did not acquire

permanent residence in Brunei. He is considered an Australian resident for tax purposes. Since

John fulfills one of the tests, he will be considered a resident for tax purposes by the Australian

tax office.5

Relating John to the Harding v Commissioner of Taxation [2019] FCAFC 29, this is a

case where an individual was born in Australia, had not lived there for the previous 17years after

his move to work in Saudi Arabia. He was still considered a resident for tax purposes by the

Australian government after all this time. The Federal Court's first decision was that Harding was

a resident basing on the place of abode as a correct address. However, awakening the place of

abode to mean an individual's permanent address changed Harding's place of abode to Saudi

Arabia because he had permanently left Australia. Harding in this argues that the individuals the

financial connections left by an individual in Australia (the family house, investments, accounts

at the bank) have no much use where a person resides.6

The other aspects of the ‘resides’ test, such as the purpose of his visits to Australia

(visiting family) also disqualify Harding as a taxpayer to Australis. Subjecting Harding’s case to

the Australian 183 day test residence test for tax purposes revealed him as a none resident given

the fact that he would never spend half the financial in Australia. The fact that the Australian

5 Jacob, Joseph. Tax return for Australian residents. 2019. Available at https://www.finder.com.au/australian-

resident-for-tax-purposes,

6 Maja, Garaca Djurdjevic. Harding case: Full Federal Court clarifies the definition of ‘permanent abode.' 28th

February 2019. Available at https://www.publicaccountant.com.au/news/full-federal-court-clarifies-definition-

permanent-abode-harding-case

and therefore, not considered a taxpayer to the Australian government all his time in Brunei

under the superannuation test.

John fulfills the domicile test with his permanent home is in Australia since he did not acquire

permanent residence in Brunei. He is considered an Australian resident for tax purposes. Since

John fulfills one of the tests, he will be considered a resident for tax purposes by the Australian

tax office.5

Relating John to the Harding v Commissioner of Taxation [2019] FCAFC 29, this is a

case where an individual was born in Australia, had not lived there for the previous 17years after

his move to work in Saudi Arabia. He was still considered a resident for tax purposes by the

Australian government after all this time. The Federal Court's first decision was that Harding was

a resident basing on the place of abode as a correct address. However, awakening the place of

abode to mean an individual's permanent address changed Harding's place of abode to Saudi

Arabia because he had permanently left Australia. Harding in this argues that the individuals the

financial connections left by an individual in Australia (the family house, investments, accounts

at the bank) have no much use where a person resides.6

The other aspects of the ‘resides’ test, such as the purpose of his visits to Australia

(visiting family) also disqualify Harding as a taxpayer to Australis. Subjecting Harding’s case to

the Australian 183 day test residence test for tax purposes revealed him as a none resident given

the fact that he would never spend half the financial in Australia. The fact that the Australian

5 Jacob, Joseph. Tax return for Australian residents. 2019. Available at https://www.finder.com.au/australian-

resident-for-tax-purposes,

6 Maja, Garaca Djurdjevic. Harding case: Full Federal Court clarifies the definition of ‘permanent abode.' 28th

February 2019. Available at https://www.publicaccountant.com.au/news/full-federal-court-clarifies-definition-

permanent-abode-harding-case

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

government did not employ Harding at his job also justifies his appeal not to be taxed by the

Australian government at that time.

The court terminated the Commissioner's application on 13th September 2019 and this

confirmed that Australian nationals who are employed overseas but maintain family of financial

assets that fall under the Australia individual tax laws for residents, then the term 'permanent

place of abode' refers to the town where these assets or family are but not his specific address7

Case study 2

Comprehensiveness is one of the commonly known qualities of a good tax and

taxation of every income yielding entity is one way of ensuring comprehensiveness. There may

be no apparent difference between a business and a hobby for a layman however going on to

think about it. A hobby is one you spend on for enjoyment, but it turns into a business if the

individual manages to make money out of it raising the question of whether the activity should

be treated as a business for tax purposes8.

The first way to tell if it’s a business or a hobby is by identifying whether the

activity is being done for commercial purposes; however hard it may be to answer. Baldwin

gives an example of George Harrison's rock band project, not excluding the amazingly renowned

and financially progressing ones such as rolling stones and Beatles. This project went cross

border to France in just a few years. He goes on to state that there is a high chance for a hobby

that starts producing small and irregular returns to develop into a reliable source of income9.

7 Narelle McBride, Andrew Whit, Scott Luetjens and Millie Mavrodis. A permanent place of abode refers to a

country or town, not a specific address. 8th April 2019. Available at

http://www.greenwoods.com.au/insights/riposte/21-march-2019-permanent-place-of-abode-refers-to-country-or-

town-not-specific-address-harding-appeal-updated-8-april/

8 Geoff, Baldwin. Hobby or business? What's the difference? 2019. Available at

http://www.mondaq.com/australia/x/778260/Income+Tax/Hobby+or+business+What+is+the+difference

9 See 7 above

government did not employ Harding at his job also justifies his appeal not to be taxed by the

Australian government at that time.

The court terminated the Commissioner's application on 13th September 2019 and this

confirmed that Australian nationals who are employed overseas but maintain family of financial

assets that fall under the Australia individual tax laws for residents, then the term 'permanent

place of abode' refers to the town where these assets or family are but not his specific address7

Case study 2

Comprehensiveness is one of the commonly known qualities of a good tax and

taxation of every income yielding entity is one way of ensuring comprehensiveness. There may

be no apparent difference between a business and a hobby for a layman however going on to

think about it. A hobby is one you spend on for enjoyment, but it turns into a business if the

individual manages to make money out of it raising the question of whether the activity should

be treated as a business for tax purposes8.

The first way to tell if it’s a business or a hobby is by identifying whether the

activity is being done for commercial purposes; however hard it may be to answer. Baldwin

gives an example of George Harrison's rock band project, not excluding the amazingly renowned

and financially progressing ones such as rolling stones and Beatles. This project went cross

border to France in just a few years. He goes on to state that there is a high chance for a hobby

that starts producing small and irregular returns to develop into a reliable source of income9.

7 Narelle McBride, Andrew Whit, Scott Luetjens and Millie Mavrodis. A permanent place of abode refers to a

country or town, not a specific address. 8th April 2019. Available at

http://www.greenwoods.com.au/insights/riposte/21-march-2019-permanent-place-of-abode-refers-to-country-or-

town-not-specific-address-harding-appeal-updated-8-april/

8 Geoff, Baldwin. Hobby or business? What's the difference? 2019. Available at

http://www.mondaq.com/australia/x/778260/Income+Tax/Hobby+or+business+What+is+the+difference

9 See 7 above

5

Basing on the chance that Nadine will go on to do business, it can be considered a business for

taxation purposes.

The consideration of the Australian Tax Office for a leisure activity that has progressed to a

business are possession of a registered name for the business, a business number in Australia, the

main objective changing for profitability, repeated sales, expectation to increase the activity

securing the business its bank account and an online presence that looks like a shop10. Surveying

the position of Nadine’s paintings for the above answers, each of the above aspects yields

negative answers except for the fact that she enquires for a market stall (makes no effort to sale)

and continually goes to the market to sell. The view of Nadine’s painting activity can be

challenged by the fact that she does not tag prices on the paintings, does not advertise and

continues to state that to her the activity has not ceased from being a leisure time thing.

The writer goes on to support the view of Nadine’s painting activity as a business for tax

purposes standing with the point that it affects the creation and buildup of human capital11

Another case in point is where there occurs a business for tax purposes is where fringe benefits

provided by an employer to his employees turn into entertainment. These become entertainment

depending on the reason for their provision, time of provision, where provided, and what type is

provided.

Case study 3

There are several considerations on taxation of workers explained in this chapter

the first one being the status (whether an employee or contract worker) under which they

10 Allison and Jillian, When do you have to start paying tax on your hobby. 2018. Available at

https://www.smh.com.au/business/banking-and-finance/when-do-you-have-to-start-paying-tax-on-your-hobby-

20180420-p4zaph.html

11 Wei, X., QU, H., and Ma, E. How does Leisure Time Affect Production Efficiency? Evidence from China, Japan,

and the US. Social Indicators Research, 127(1): 2016, 101-122. DOI 10.1007/s11205-015-0962-1.

Basing on the chance that Nadine will go on to do business, it can be considered a business for

taxation purposes.

The consideration of the Australian Tax Office for a leisure activity that has progressed to a

business are possession of a registered name for the business, a business number in Australia, the

main objective changing for profitability, repeated sales, expectation to increase the activity

securing the business its bank account and an online presence that looks like a shop10. Surveying

the position of Nadine’s paintings for the above answers, each of the above aspects yields

negative answers except for the fact that she enquires for a market stall (makes no effort to sale)

and continually goes to the market to sell. The view of Nadine’s painting activity can be

challenged by the fact that she does not tag prices on the paintings, does not advertise and

continues to state that to her the activity has not ceased from being a leisure time thing.

The writer goes on to support the view of Nadine’s painting activity as a business for tax

purposes standing with the point that it affects the creation and buildup of human capital11

Another case in point is where there occurs a business for tax purposes is where fringe benefits

provided by an employer to his employees turn into entertainment. These become entertainment

depending on the reason for their provision, time of provision, where provided, and what type is

provided.

Case study 3

There are several considerations on taxation of workers explained in this chapter

the first one being the status (whether an employee or contract worker) under which they

10 Allison and Jillian, When do you have to start paying tax on your hobby. 2018. Available at

https://www.smh.com.au/business/banking-and-finance/when-do-you-have-to-start-paying-tax-on-your-hobby-

20180420-p4zaph.html

11 Wei, X., QU, H., and Ma, E. How does Leisure Time Affect Production Efficiency? Evidence from China, Japan,

and the US. Social Indicators Research, 127(1): 2016, 101-122. DOI 10.1007/s11205-015-0962-1.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

(workers) are classified according to the Australian tax office. An employee refers to a worker

employed in your business, and generally, a tax is withheld from the payments made to them. A

contract worker is one who has some other commitments other than work in your company but is

hired for a specific period to render you services to you. As an employer, you do not levy a tax

on this worker's income unless on the agreement between you (the employer) and him (the

contract worker). Another consideration when taxing a worker is the Pay As You Go (PAYG), a

requirement by law to withhold given amounts for income tax. Tax by the state levied on wages

paid by an employer every month.12

There is also the payroll tax which is a tax by the state levied on wages paid by an employer

every month. For an employee to ensure that the needs of his workers are being met, he/she

should consider the provision of fringe benefits instead of any other ways of payment. The tax on

fringe benefits is named fringe benefits tax (FBT), and it is paid to the employee or the people he

has to pay it for replacing the monthly or daily pay that the employee would have paid.

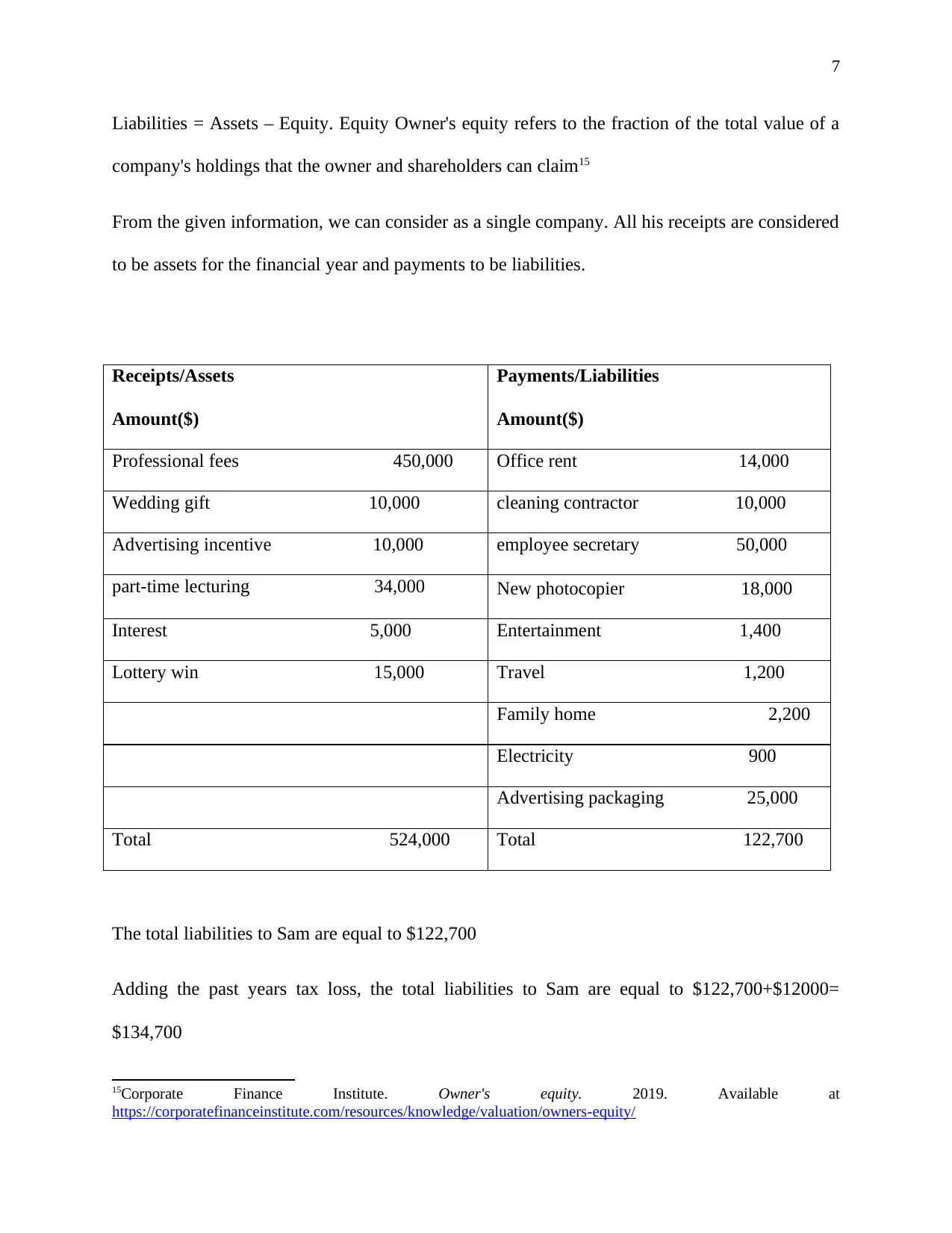

The simplest definition of a liability is anything that a company or business owes an individual

or another company. One classification of liabilities in accounting is accounts payables which

put all of the payments under liabilities. 13 Office rent is a liability because it is paid to the

landlord

From the accounting equation Assets, =Liabilities + Equity14. We get the financial year’s income

which will be subjected to the tax. Assets refer to Sam’s holdings throughout the year.

12 “Taxation.” Taxation and your employees. 2019 Available at https://www.business.gov.au/people/hiring/pay-and-

conditions/taxation-and-your-employees.

13 Australian Tax Office (ATO). How to calculate Liabilities: A step-by-step Guide for Small Business.2018

Available at https://www.freshbooks.com/hub/accounting/calculate-liabilities

14“Accounting Equation.” The basic accounting equation. 2019. Available at

https://courses.lumenlearning.com/sac-finaccounting/chapter/the-basic-accounting-equation/

(workers) are classified according to the Australian tax office. An employee refers to a worker

employed in your business, and generally, a tax is withheld from the payments made to them. A

contract worker is one who has some other commitments other than work in your company but is

hired for a specific period to render you services to you. As an employer, you do not levy a tax

on this worker's income unless on the agreement between you (the employer) and him (the

contract worker). Another consideration when taxing a worker is the Pay As You Go (PAYG), a

requirement by law to withhold given amounts for income tax. Tax by the state levied on wages

paid by an employer every month.12

There is also the payroll tax which is a tax by the state levied on wages paid by an employer

every month. For an employee to ensure that the needs of his workers are being met, he/she

should consider the provision of fringe benefits instead of any other ways of payment. The tax on

fringe benefits is named fringe benefits tax (FBT), and it is paid to the employee or the people he

has to pay it for replacing the monthly or daily pay that the employee would have paid.

The simplest definition of a liability is anything that a company or business owes an individual

or another company. One classification of liabilities in accounting is accounts payables which

put all of the payments under liabilities. 13 Office rent is a liability because it is paid to the

landlord

From the accounting equation Assets, =Liabilities + Equity14. We get the financial year’s income

which will be subjected to the tax. Assets refer to Sam’s holdings throughout the year.

12 “Taxation.” Taxation and your employees. 2019 Available at https://www.business.gov.au/people/hiring/pay-and-

conditions/taxation-and-your-employees.

13 Australian Tax Office (ATO). How to calculate Liabilities: A step-by-step Guide for Small Business.2018

Available at https://www.freshbooks.com/hub/accounting/calculate-liabilities

14“Accounting Equation.” The basic accounting equation. 2019. Available at

https://courses.lumenlearning.com/sac-finaccounting/chapter/the-basic-accounting-equation/

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Liabilities = Assets – Equity. Equity Owner's equity refers to the fraction of the total value of a

company's holdings that the owner and shareholders can claim15

From the given information, we can consider as a single company. All his receipts are considered

to be assets for the financial year and payments to be liabilities.

Receipts/Assets

Amount($)

Payments/Liabilities

Amount($)

Professional fees 450,000 Office rent 14,000

Wedding gift 10,000 cleaning contractor 10,000

Advertising incentive 10,000 employee secretary 50,000

part-time lecturing 34,000 New photocopier 18,000

Interest 5,000 Entertainment 1,400

Lottery win 15,000 Travel 1,200

Family home 2,200

Electricity 900

Advertising packaging 25,000

Total 524,000 Total 122,700

The total liabilities to Sam are equal to $122,700

Adding the past years tax loss, the total liabilities to Sam are equal to $122,700+$12000=

$134,700

15Corporate Finance Institute. Owner's equity. 2019. Available at

https://corporatefinanceinstitute.com/resources/knowledge/valuation/owners-equity/

Liabilities = Assets – Equity. Equity Owner's equity refers to the fraction of the total value of a

company's holdings that the owner and shareholders can claim15

From the given information, we can consider as a single company. All his receipts are considered

to be assets for the financial year and payments to be liabilities.

Receipts/Assets

Amount($)

Payments/Liabilities

Amount($)

Professional fees 450,000 Office rent 14,000

Wedding gift 10,000 cleaning contractor 10,000

Advertising incentive 10,000 employee secretary 50,000

part-time lecturing 34,000 New photocopier 18,000

Interest 5,000 Entertainment 1,400

Lottery win 15,000 Travel 1,200

Family home 2,200

Electricity 900

Advertising packaging 25,000

Total 524,000 Total 122,700

The total liabilities to Sam are equal to $122,700

Adding the past years tax loss, the total liabilities to Sam are equal to $122,700+$12000=

$134,700

15Corporate Finance Institute. Owner's equity. 2019. Available at

https://corporatefinanceinstitute.com/resources/knowledge/valuation/owners-equity/

8

From Liabilities= Assets- Equity

Total return from the year ending 30th June 2019 = 524,000-122,700= 401,300

From Liabilities= Assets- Equity

Total return from the year ending 30th June 2019 = 524,000-122,700= 401,300

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Bibliography

“Taxation.” Taxation and your employees. 2019 Available at

https://www.business.gov.au/people/hiring/pay-and-conditions/taxation-and-your-

employees.

Accounting Equation.” The basic accounting equation. 2019 Available at

https://courses.lumenlearning.com/sac-finaccounting/chapter/the-basic-accounting-

equation/

Allison and Jillian, When do you have to start paying tax on your hobby. 2018. Available at

https://www.smh.com.au/business/banking-and-finance/when-do-you-have-to-start-

paying-tax-on-your-hobby-20180420-p4zaph.html

Australian Government. Residency-The The 183-day test. 2019. Available at

https://www.investopedia.com

Australian Tax Office (ATO). How to calculate Liabilities: A step-by-step Guide for Small

Business.2018 Available at https://www.freshbooks.com/hub/accounting/calculate-

liabilities

Australian tax office. Work out your tax residency, the Australian government, 2018.

Corporate Finance Institute. Owner's equity. 2019. Available at

https://corporatefinanceinstitute.com/resources/knowledge/valuation/owners-equity/

Geoff, Baldwin. Hobby or business? what's the difference? 2019. Available at

http://www.mondaq.com/australia/x/778260/Income+Tax/Hobby+or+business+What+is+

the+difference

Bibliography

“Taxation.” Taxation and your employees. 2019 Available at

https://www.business.gov.au/people/hiring/pay-and-conditions/taxation-and-your-

employees.

Accounting Equation.” The basic accounting equation. 2019 Available at

https://courses.lumenlearning.com/sac-finaccounting/chapter/the-basic-accounting-

equation/

Allison and Jillian, When do you have to start paying tax on your hobby. 2018. Available at

https://www.smh.com.au/business/banking-and-finance/when-do-you-have-to-start-

paying-tax-on-your-hobby-20180420-p4zaph.html

Australian Government. Residency-The The 183-day test. 2019. Available at

https://www.investopedia.com

Australian Tax Office (ATO). How to calculate Liabilities: A step-by-step Guide for Small

Business.2018 Available at https://www.freshbooks.com/hub/accounting/calculate-

liabilities

Australian tax office. Work out your tax residency, the Australian government, 2018.

Corporate Finance Institute. Owner's equity. 2019. Available at

https://corporatefinanceinstitute.com/resources/knowledge/valuation/owners-equity/

Geoff, Baldwin. Hobby or business? what's the difference? 2019. Available at

http://www.mondaq.com/australia/x/778260/Income+Tax/Hobby+or+business+What+is+

the+difference

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Jacob, Joseph. Tax return for Australian residents. 2019. Available at

https://www.finder.com.au/australian-resident-for-tax-purposes,

John, McLaren. Should the international income of an Australian resident be taxed on a

worldwide or territorial basis? 2006. Available at

https://pdfs.semanticscholar.org/932c/caac062cdd28c1cc5e27fbad617e9345e63f.pdf Pg

75.

Maja, Garaca Djurdjevic. Harding case: Full Federal Court clarifies the definition of

‘permanent abode.' 28th February 2019. Available at

https://www.publicaccountant.com.au/news/full-federal-court-clarifies-definition-

permanent-abode-harding-case

Mayo, Wayne, Time to Upgrade Australia’s Company Tax System From Imputation to

Integration (July 31, 2018). Australian Tax Forum, Vol. 33(4), 2018. Available at SSRN:

https://ssrn.com/abstract=3311250

Narelle McBride, Andrew Whit, Scott Luetjens and Millie Mavrodis. A permanent place of

abode refers to a country or town, not a specific address. 8th April 2019. Available at

http://www.greenwoods.com.au/insights/riposte/21-march-2019-permanent-place-of-

abode-refers-to-country-or-town-not-specific-address-harding-appeal-updated-8-april/

Wei, X., QU, H., and Ma, E. How does Leisure Time Affect Production Efficiency? Evidence

from China, Japan, and the US. Social Indicators Research, 127(1): 2016, 101-122. DOI

10.1007/s11205-015-0962-1.

Jacob, Joseph. Tax return for Australian residents. 2019. Available at

https://www.finder.com.au/australian-resident-for-tax-purposes,

John, McLaren. Should the international income of an Australian resident be taxed on a

worldwide or territorial basis? 2006. Available at

https://pdfs.semanticscholar.org/932c/caac062cdd28c1cc5e27fbad617e9345e63f.pdf Pg

75.

Maja, Garaca Djurdjevic. Harding case: Full Federal Court clarifies the definition of

‘permanent abode.' 28th February 2019. Available at

https://www.publicaccountant.com.au/news/full-federal-court-clarifies-definition-

permanent-abode-harding-case

Mayo, Wayne, Time to Upgrade Australia’s Company Tax System From Imputation to

Integration (July 31, 2018). Australian Tax Forum, Vol. 33(4), 2018. Available at SSRN:

https://ssrn.com/abstract=3311250

Narelle McBride, Andrew Whit, Scott Luetjens and Millie Mavrodis. A permanent place of

abode refers to a country or town, not a specific address. 8th April 2019. Available at

http://www.greenwoods.com.au/insights/riposte/21-march-2019-permanent-place-of-

abode-refers-to-country-or-town-not-specific-address-harding-appeal-updated-8-april/

Wei, X., QU, H., and Ma, E. How does Leisure Time Affect Production Efficiency? Evidence

from China, Japan, and the US. Social Indicators Research, 127(1): 2016, 101-122. DOI

10.1007/s11205-015-0962-1.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.