Taxation Case Study: TelDrop Partnership

VerifiedAdded on 2020/01/07

|12

|2522

|65

Case Study

AI Summary

This case study provides a detailed analysis of taxation principles applied to various business scenarios. It includes calculations of taxable income for an individual, a sole proprietorship (Second Chance), and a partnership (TelDrop). The study covers aspects such as salary deductions, business expenses, profit distribution, and trust income. It also addresses the Australian Taxation Office's regulations and guidelines for determining tax liabilities for different business structures. The report concludes with a summary of key findings and a list of references.

Taxation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

PART B...........................................................................................................................................4

PART C...........................................................................................................................................7

1. Calculating net income of TelDrop partnership firm for the year ended 30 June 2017..........7

2. Distributing the net income of the partnership for the year ended 30 June 2017....................9

PART D...........................................................................................................................................9

1. List any amounts for which there is no present entitlement as at 30 June 2017......................9

2 Amount retained by trust........................................................................................................10

(3) Taxable income....................................................................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

PART B...........................................................................................................................................4

PART C...........................................................................................................................................7

1. Calculating net income of TelDrop partnership firm for the year ended 30 June 2017..........7

2. Distributing the net income of the partnership for the year ended 30 June 2017....................9

PART D...........................................................................................................................................9

1. List any amounts for which there is no present entitlement as at 30 June 2017......................9

2 Amount retained by trust........................................................................................................10

(3) Taxable income....................................................................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

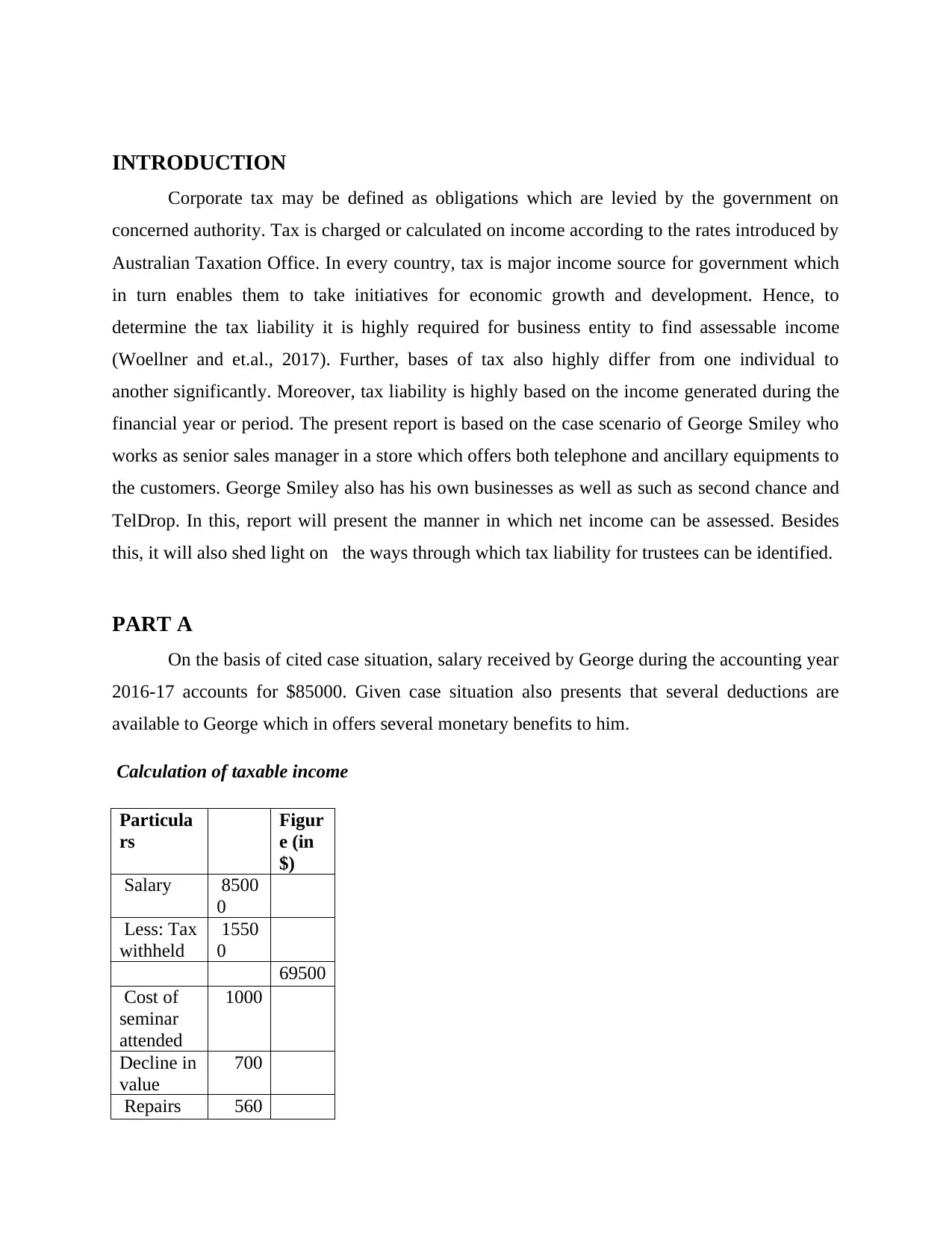

INTRODUCTION

Corporate tax may be defined as obligations which are levied by the government on

concerned authority. Tax is charged or calculated on income according to the rates introduced by

Australian Taxation Office. In every country, tax is major income source for government which

in turn enables them to take initiatives for economic growth and development. Hence, to

determine the tax liability it is highly required for business entity to find assessable income

(Woellner and et.al., 2017). Further, bases of tax also highly differ from one individual to

another significantly. Moreover, tax liability is highly based on the income generated during the

financial year or period. The present report is based on the case scenario of George Smiley who

works as senior sales manager in a store which offers both telephone and ancillary equipments to

the customers. George Smiley also has his own businesses as well as such as second chance and

TelDrop. In this, report will present the manner in which net income can be assessed. Besides

this, it will also shed light on the ways through which tax liability for trustees can be identified.

PART A

On the basis of cited case situation, salary received by George during the accounting year

2016-17 accounts for $85000. Given case situation also presents that several deductions are

available to George which in offers several monetary benefits to him.

Calculation of taxable income

Particula

rs

Figur

e (in

$)

Salary 8500

0

Less: Tax

withheld

1550

0

69500

Cost of

seminar

attended

1000

Decline in

value

700

Repairs 560

Corporate tax may be defined as obligations which are levied by the government on

concerned authority. Tax is charged or calculated on income according to the rates introduced by

Australian Taxation Office. In every country, tax is major income source for government which

in turn enables them to take initiatives for economic growth and development. Hence, to

determine the tax liability it is highly required for business entity to find assessable income

(Woellner and et.al., 2017). Further, bases of tax also highly differ from one individual to

another significantly. Moreover, tax liability is highly based on the income generated during the

financial year or period. The present report is based on the case scenario of George Smiley who

works as senior sales manager in a store which offers both telephone and ancillary equipments to

the customers. George Smiley also has his own businesses as well as such as second chance and

TelDrop. In this, report will present the manner in which net income can be assessed. Besides

this, it will also shed light on the ways through which tax liability for trustees can be identified.

PART A

On the basis of cited case situation, salary received by George during the accounting year

2016-17 accounts for $85000. Given case situation also presents that several deductions are

available to George which in offers several monetary benefits to him.

Calculation of taxable income

Particula

rs

Figur

e (in

$)

Salary 8500

0

Less: Tax

withheld

1550

0

69500

Cost of

seminar

attended

1000

Decline in

value

700

Repairs 560

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

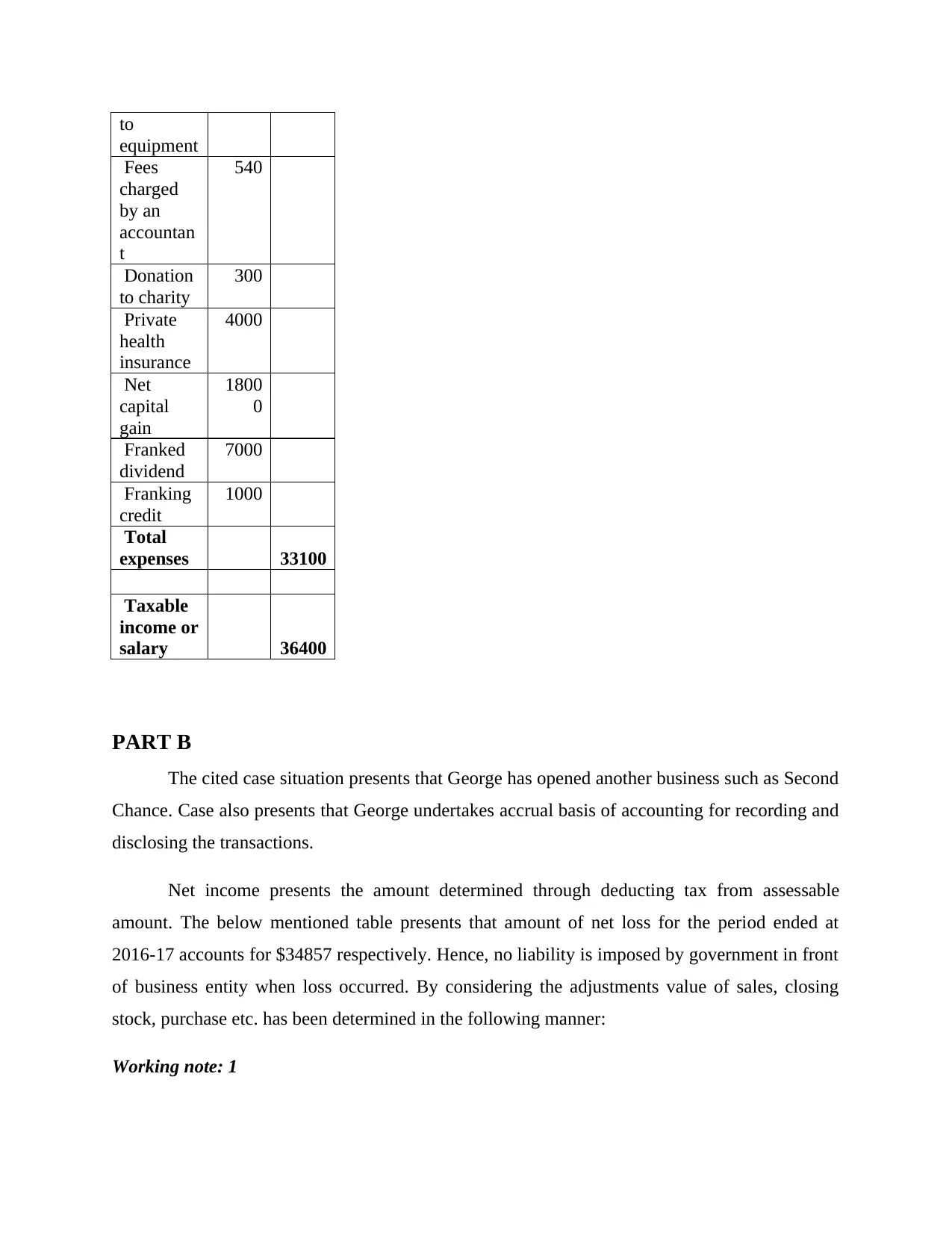

to

equipment

Fees

charged

by an

accountan

t

540

Donation

to charity

300

Private

health

insurance

4000

Net

capital

gain

1800

0

Franked

dividend

7000

Franking

credit

1000

Total

expenses 33100

Taxable

income or

salary 36400

PART B

The cited case situation presents that George has opened another business such as Second

Chance. Case also presents that George undertakes accrual basis of accounting for recording and

disclosing the transactions.

Net income presents the amount determined through deducting tax from assessable

amount. The below mentioned table presents that amount of net loss for the period ended at

2016-17 accounts for $34857 respectively. Hence, no liability is imposed by government in front

of business entity when loss occurred. By considering the adjustments value of sales, closing

stock, purchase etc. has been determined in the following manner:

Working note: 1

equipment

Fees

charged

by an

accountan

t

540

Donation

to charity

300

Private

health

insurance

4000

Net

capital

gain

1800

0

Franked

dividend

7000

Franking

credit

1000

Total

expenses 33100

Taxable

income or

salary 36400

PART B

The cited case situation presents that George has opened another business such as Second

Chance. Case also presents that George undertakes accrual basis of accounting for recording and

disclosing the transactions.

Net income presents the amount determined through deducting tax from assessable

amount. The below mentioned table presents that amount of net loss for the period ended at

2016-17 accounts for $34857 respectively. Hence, no liability is imposed by government in front

of business entity when loss occurred. By considering the adjustments value of sales, closing

stock, purchase etc. has been determined in the following manner:

Working note: 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

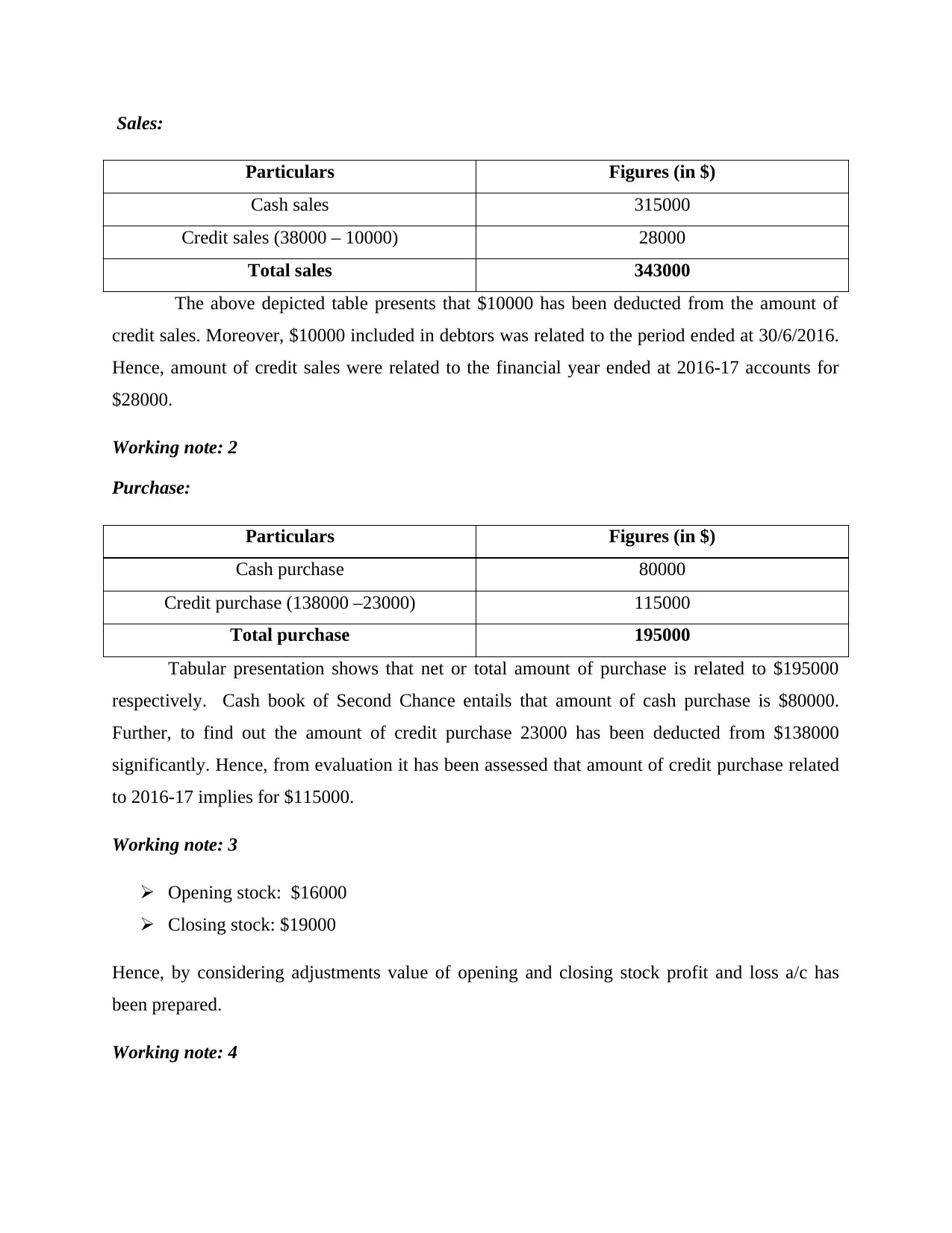

Sales:

Particulars Figures (in $)

Cash sales 315000

Credit sales (38000 – 10000) 28000

Total sales 343000

The above depicted table presents that $10000 has been deducted from the amount of

credit sales. Moreover, $10000 included in debtors was related to the period ended at 30/6/2016.

Hence, amount of credit sales were related to the financial year ended at 2016-17 accounts for

$28000.

Working note: 2

Purchase:

Particulars Figures (in $)

Cash purchase 80000

Credit purchase (138000 –23000) 115000

Total purchase 195000

Tabular presentation shows that net or total amount of purchase is related to $195000

respectively. Cash book of Second Chance entails that amount of cash purchase is $80000.

Further, to find out the amount of credit purchase 23000 has been deducted from $138000

significantly. Hence, from evaluation it has been assessed that amount of credit purchase related

to 2016-17 implies for $115000.

Working note: 3

Opening stock: $16000

Closing stock: $19000

Hence, by considering adjustments value of opening and closing stock profit and loss a/c has

been prepared.

Working note: 4

Particulars Figures (in $)

Cash sales 315000

Credit sales (38000 – 10000) 28000

Total sales 343000

The above depicted table presents that $10000 has been deducted from the amount of

credit sales. Moreover, $10000 included in debtors was related to the period ended at 30/6/2016.

Hence, amount of credit sales were related to the financial year ended at 2016-17 accounts for

$28000.

Working note: 2

Purchase:

Particulars Figures (in $)

Cash purchase 80000

Credit purchase (138000 –23000) 115000

Total purchase 195000

Tabular presentation shows that net or total amount of purchase is related to $195000

respectively. Cash book of Second Chance entails that amount of cash purchase is $80000.

Further, to find out the amount of credit purchase 23000 has been deducted from $138000

significantly. Hence, from evaluation it has been assessed that amount of credit purchase related

to 2016-17 implies for $115000.

Working note: 3

Opening stock: $16000

Closing stock: $19000

Hence, by considering adjustments value of opening and closing stock profit and loss a/c has

been prepared.

Working note: 4

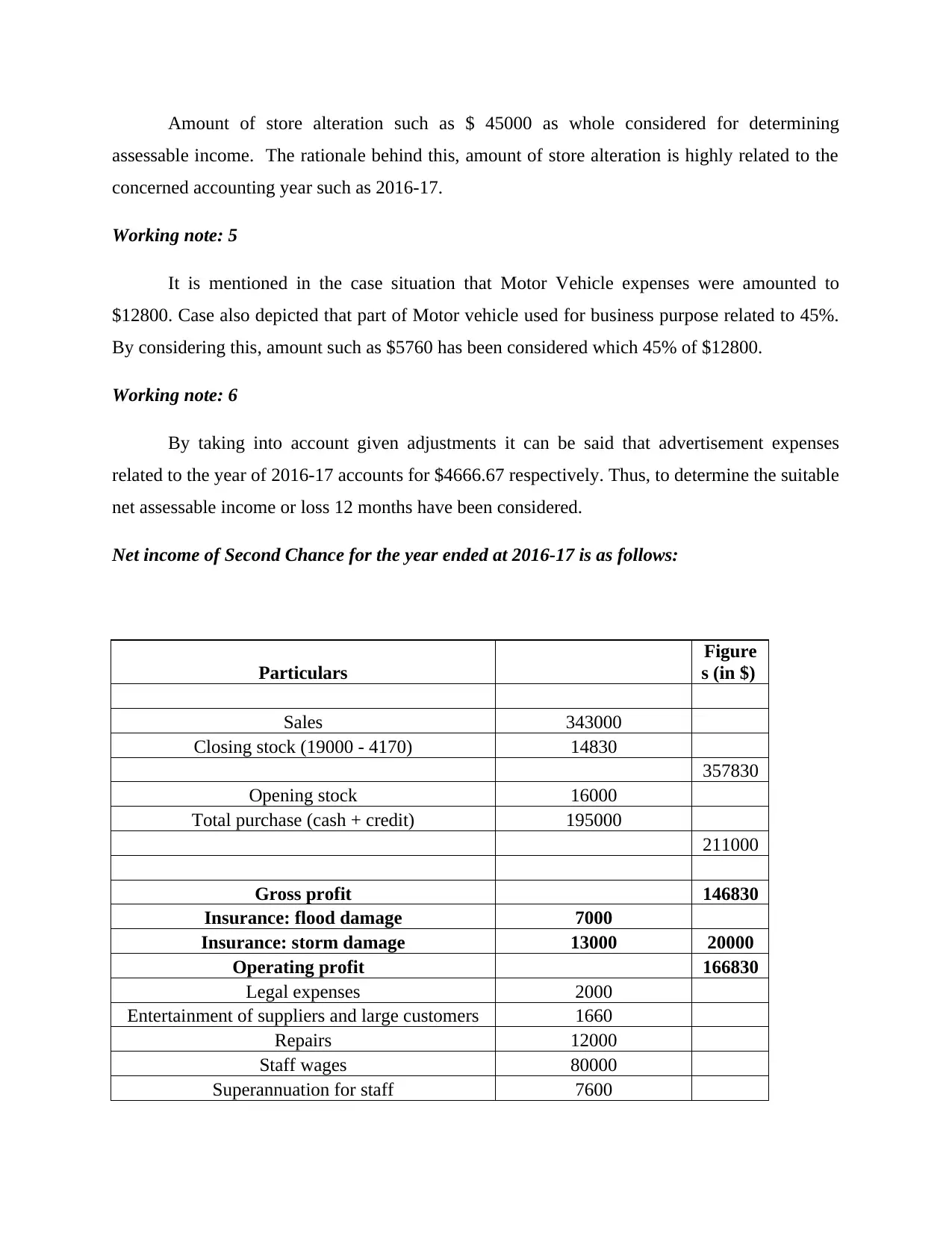

Amount of store alteration such as $ 45000 as whole considered for determining

assessable income. The rationale behind this, amount of store alteration is highly related to the

concerned accounting year such as 2016-17.

Working note: 5

It is mentioned in the case situation that Motor Vehicle expenses were amounted to

$12800. Case also depicted that part of Motor vehicle used for business purpose related to 45%.

By considering this, amount such as $5760 has been considered which 45% of $12800.

Working note: 6

By taking into account given adjustments it can be said that advertisement expenses

related to the year of 2016-17 accounts for $4666.67 respectively. Thus, to determine the suitable

net assessable income or loss 12 months have been considered.

Net income of Second Chance for the year ended at 2016-17 is as follows:

Particulars

Figure

s (in $)

Sales 343000

Closing stock (19000 - 4170) 14830

357830

Opening stock 16000

Total purchase (cash + credit) 195000

211000

Gross profit 146830

Insurance: flood damage 7000

Insurance: storm damage 13000 20000

Operating profit 166830

Legal expenses 2000

Entertainment of suppliers and large customers 1660

Repairs 12000

Staff wages 80000

Superannuation for staff 7600

assessable income. The rationale behind this, amount of store alteration is highly related to the

concerned accounting year such as 2016-17.

Working note: 5

It is mentioned in the case situation that Motor Vehicle expenses were amounted to

$12800. Case also depicted that part of Motor vehicle used for business purpose related to 45%.

By considering this, amount such as $5760 has been considered which 45% of $12800.

Working note: 6

By taking into account given adjustments it can be said that advertisement expenses

related to the year of 2016-17 accounts for $4666.67 respectively. Thus, to determine the suitable

net assessable income or loss 12 months have been considered.

Net income of Second Chance for the year ended at 2016-17 is as follows:

Particulars

Figure

s (in $)

Sales 343000

Closing stock (19000 - 4170) 14830

357830

Opening stock 16000

Total purchase (cash + credit) 195000

211000

Gross profit 146830

Insurance: flood damage 7000

Insurance: storm damage 13000 20000

Operating profit 166830

Legal expenses 2000

Entertainment of suppliers and large customers 1660

Repairs 12000

Staff wages 80000

Superannuation for staff 7600

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

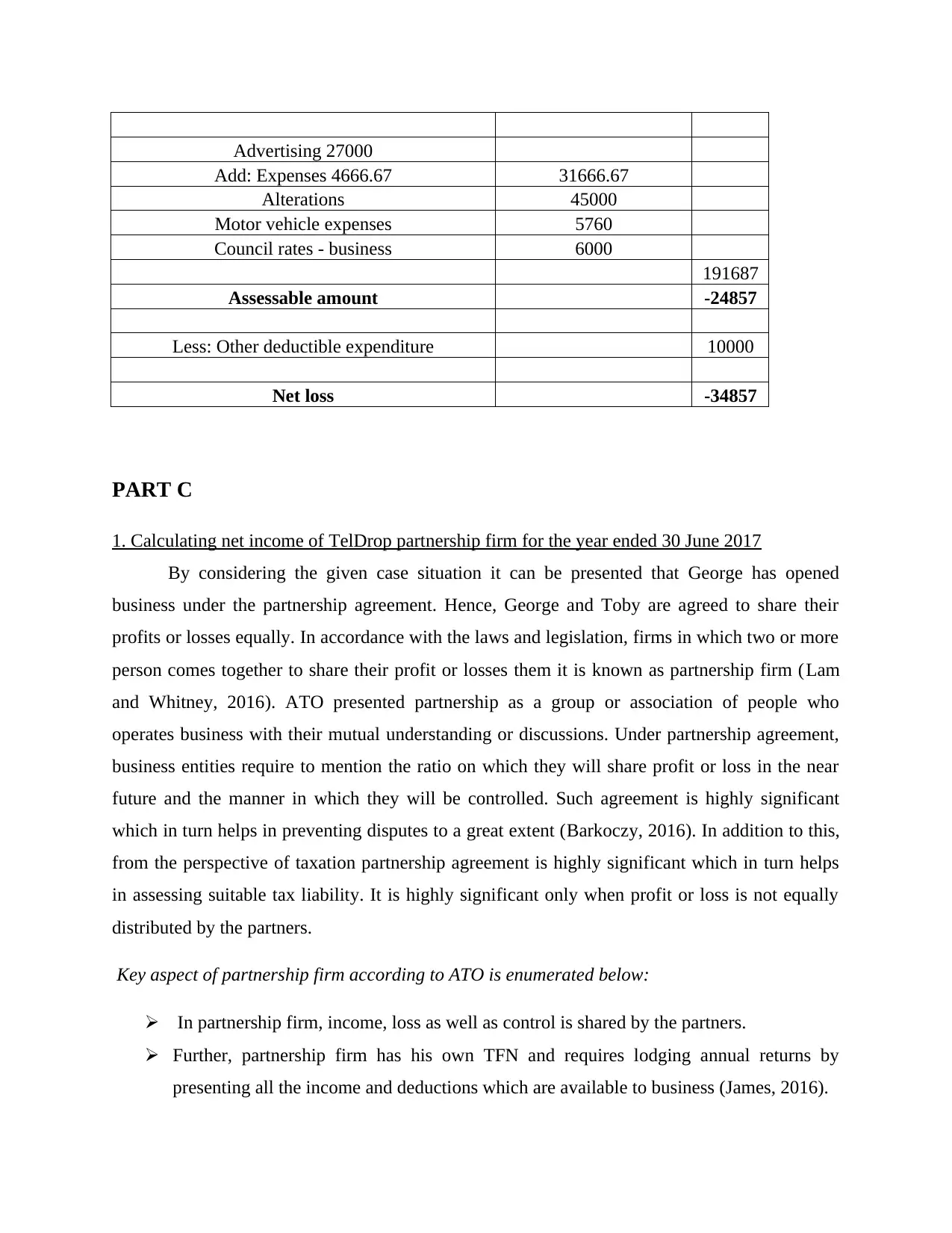

Advertising 27000

Add: Expenses 4666.67 31666.67

Alterations 45000

Motor vehicle expenses 5760

Council rates - business 6000

191687

Assessable amount -24857

Less: Other deductible expenditure 10000

Net loss -34857

PART C

1. Calculating net income of TelDrop partnership firm for the year ended 30 June 2017

By considering the given case situation it can be presented that George has opened

business under the partnership agreement. Hence, George and Toby are agreed to share their

profits or losses equally. In accordance with the laws and legislation, firms in which two or more

person comes together to share their profit or losses them it is known as partnership firm (Lam

and Whitney, 2016). ATO presented partnership as a group or association of people who

operates business with their mutual understanding or discussions. Under partnership agreement,

business entities require to mention the ratio on which they will share profit or loss in the near

future and the manner in which they will be controlled. Such agreement is highly significant

which in turn helps in preventing disputes to a great extent (Barkoczy, 2016). In addition to this,

from the perspective of taxation partnership agreement is highly significant which in turn helps

in assessing suitable tax liability. It is highly significant only when profit or loss is not equally

distributed by the partners.

Key aspect of partnership firm according to ATO is enumerated below:

In partnership firm, income, loss as well as control is shared by the partners.

Further, partnership firm has his own TFN and requires lodging annual returns by

presenting all the income and deductions which are available to business (James, 2016).

Add: Expenses 4666.67 31666.67

Alterations 45000

Motor vehicle expenses 5760

Council rates - business 6000

191687

Assessable amount -24857

Less: Other deductible expenditure 10000

Net loss -34857

PART C

1. Calculating net income of TelDrop partnership firm for the year ended 30 June 2017

By considering the given case situation it can be presented that George has opened

business under the partnership agreement. Hence, George and Toby are agreed to share their

profits or losses equally. In accordance with the laws and legislation, firms in which two or more

person comes together to share their profit or losses them it is known as partnership firm (Lam

and Whitney, 2016). ATO presented partnership as a group or association of people who

operates business with their mutual understanding or discussions. Under partnership agreement,

business entities require to mention the ratio on which they will share profit or loss in the near

future and the manner in which they will be controlled. Such agreement is highly significant

which in turn helps in preventing disputes to a great extent (Barkoczy, 2016). In addition to this,

from the perspective of taxation partnership agreement is highly significant which in turn helps

in assessing suitable tax liability. It is highly significant only when profit or loss is not equally

distributed by the partners.

Key aspect of partnership firm according to ATO is enumerated below:

In partnership firm, income, loss as well as control is shared by the partners.

Further, partnership firm has his own TFN and requires lodging annual returns by

presenting all the income and deductions which are available to business (James, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

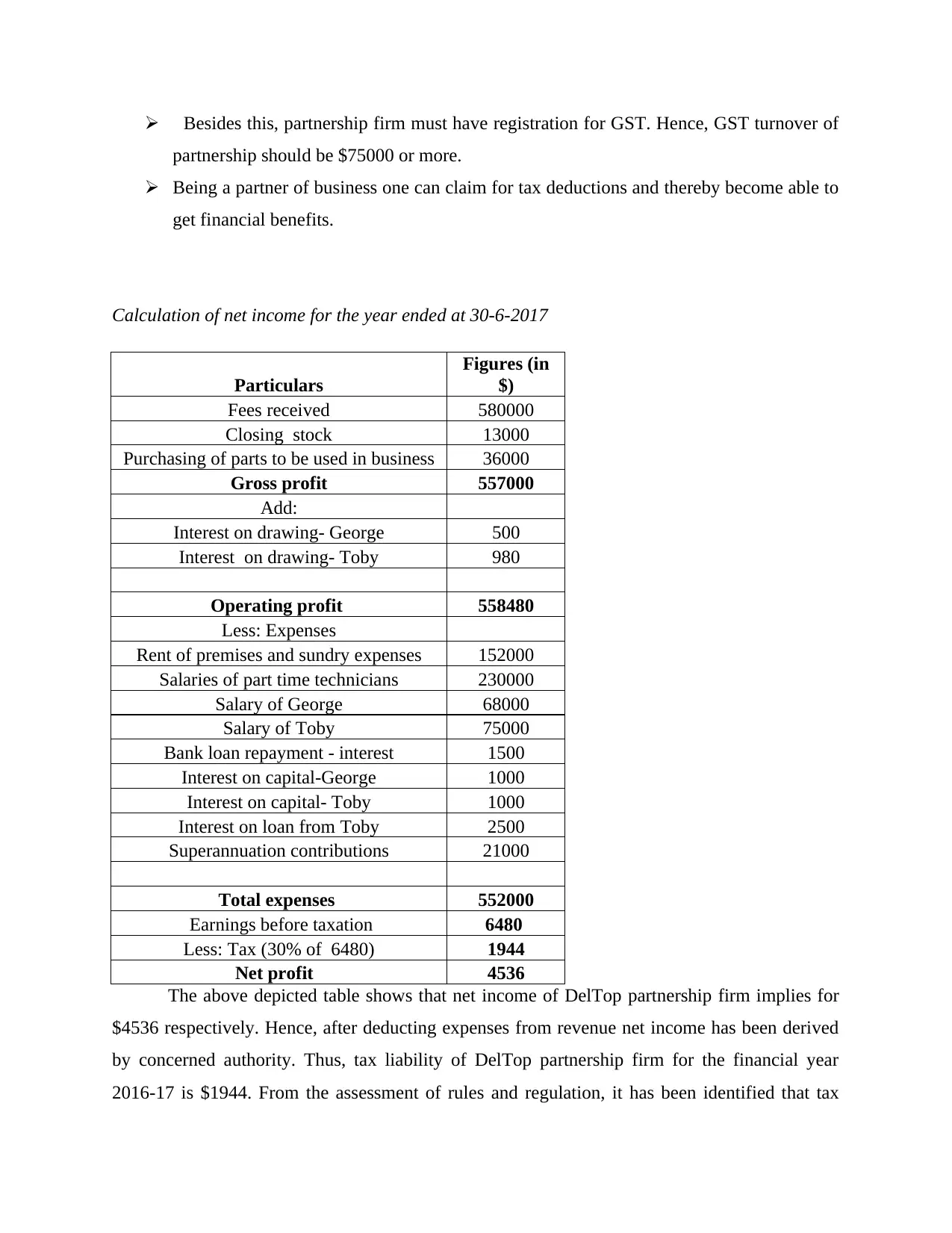

Besides this, partnership firm must have registration for GST. Hence, GST turnover of

partnership should be $75000 or more.

Being a partner of business one can claim for tax deductions and thereby become able to

get financial benefits.

Calculation of net income for the year ended at 30-6-2017

Particulars

Figures (in

$)

Fees received 580000

Closing stock 13000

Purchasing of parts to be used in business 36000

Gross profit 557000

Add:

Interest on drawing- George 500

Interest on drawing- Toby 980

Operating profit 558480

Less: Expenses

Rent of premises and sundry expenses 152000

Salaries of part time technicians 230000

Salary of George 68000

Salary of Toby 75000

Bank loan repayment - interest 1500

Interest on capital-George 1000

Interest on capital- Toby 1000

Interest on loan from Toby 2500

Superannuation contributions 21000

Total expenses 552000

Earnings before taxation 6480

Less: Tax (30% of 6480) 1944

Net profit 4536

The above depicted table shows that net income of DelTop partnership firm implies for

$4536 respectively. Hence, after deducting expenses from revenue net income has been derived

by concerned authority. Thus, tax liability of DelTop partnership firm for the financial year

2016-17 is $1944. From the assessment of rules and regulation, it has been identified that tax

partnership should be $75000 or more.

Being a partner of business one can claim for tax deductions and thereby become able to

get financial benefits.

Calculation of net income for the year ended at 30-6-2017

Particulars

Figures (in

$)

Fees received 580000

Closing stock 13000

Purchasing of parts to be used in business 36000

Gross profit 557000

Add:

Interest on drawing- George 500

Interest on drawing- Toby 980

Operating profit 558480

Less: Expenses

Rent of premises and sundry expenses 152000

Salaries of part time technicians 230000

Salary of George 68000

Salary of Toby 75000

Bank loan repayment - interest 1500

Interest on capital-George 1000

Interest on capital- Toby 1000

Interest on loan from Toby 2500

Superannuation contributions 21000

Total expenses 552000

Earnings before taxation 6480

Less: Tax (30% of 6480) 1944

Net profit 4536

The above depicted table shows that net income of DelTop partnership firm implies for

$4536 respectively. Hence, after deducting expenses from revenue net income has been derived

by concerned authority. Thus, tax liability of DelTop partnership firm for the financial year

2016-17 is $1944. From the assessment of rules and regulation, it has been identified that tax

rates for partnership firm is 30%. In the real life, partnership firm is recognized or treated as

separate entity. Company’s liability is not highly affected from the aspect whether it is

registered or not (Alghamdi and Rahim, 2016). Hence, partnership firm and partners come under

their respective slabs. Thus, by charging 30% tax rate on net profit tax liability has been

determined for DelTop such as $1944 respectively.

2. Distributing the net income of the partnership for the year ended 30 June 2017

Particulars

Figures (in

$)

Total Net income 4536

Part of Toby (50%) 2268

Part of George (50%) 2268

Tabular presentation shows that part of Toby and George implies for $2268 each

respectively. Moreover, it is presented in the case scenario that both the partners such as George

and Toby will share their profit equally. Hence, by taking into consideration such aspect equal

ratio has been considered to determine the level of net income for each partner. According to the

ratio of .5:.5 amounts has been allocated to each partner. Hence, at the time of allocation terms of

partnership agreement has been undertaken by the partners.

PART D

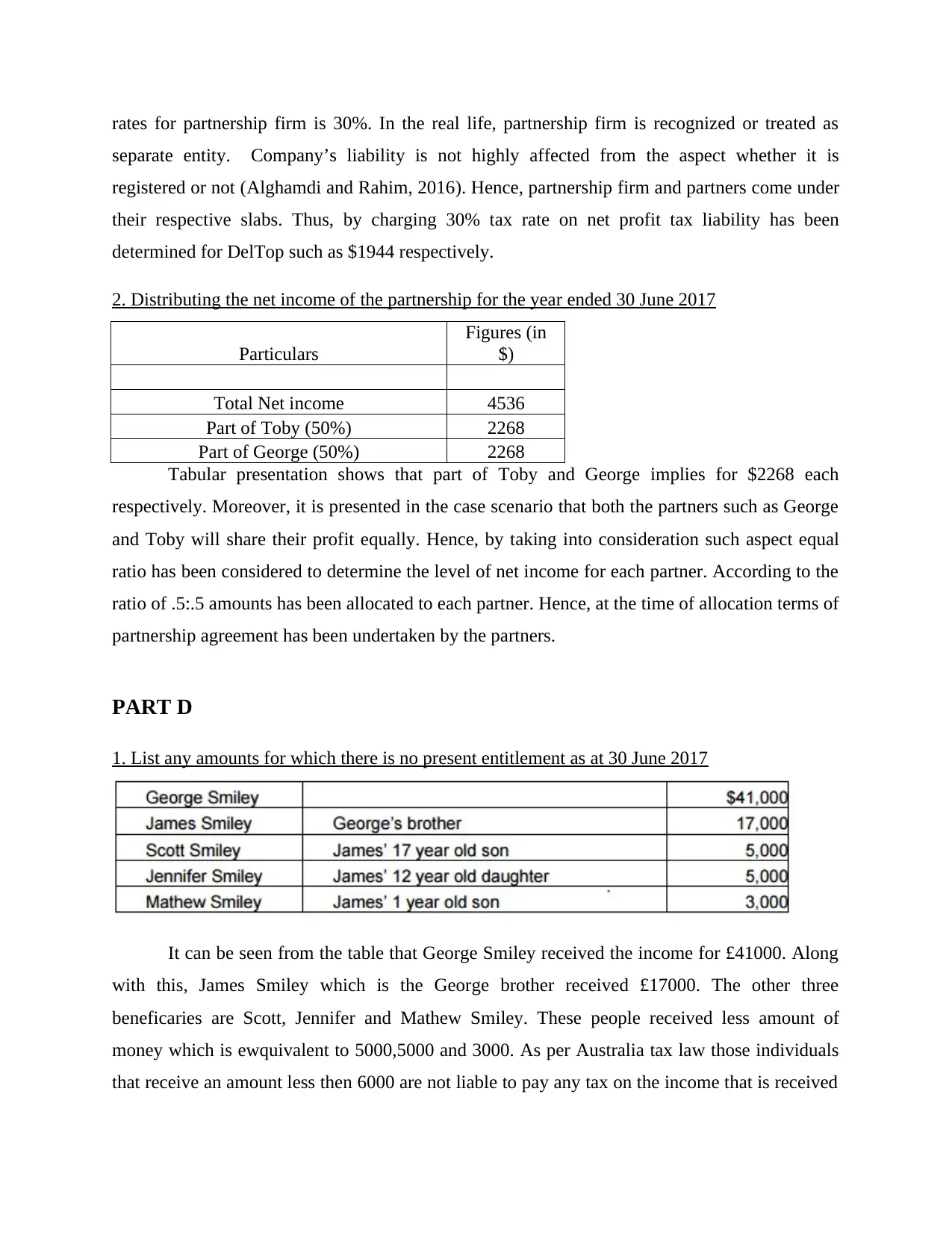

1. List any amounts for which there is no present entitlement as at 30 June 2017

It can be seen from the table that George Smiley received the income for £41000. Along

with this, James Smiley which is the George brother received £17000. The other three

beneficaries are Scott, Jennifer and Mathew Smiley. These people received less amount of

money which is ewquivalent to 5000,5000 and 3000. As per Australia tax law those individuals

that receive an amount less then 6000 are not liable to pay any tax on the income that is received

separate entity. Company’s liability is not highly affected from the aspect whether it is

registered or not (Alghamdi and Rahim, 2016). Hence, partnership firm and partners come under

their respective slabs. Thus, by charging 30% tax rate on net profit tax liability has been

determined for DelTop such as $1944 respectively.

2. Distributing the net income of the partnership for the year ended 30 June 2017

Particulars

Figures (in

$)

Total Net income 4536

Part of Toby (50%) 2268

Part of George (50%) 2268

Tabular presentation shows that part of Toby and George implies for $2268 each

respectively. Moreover, it is presented in the case scenario that both the partners such as George

and Toby will share their profit equally. Hence, by taking into consideration such aspect equal

ratio has been considered to determine the level of net income for each partner. According to the

ratio of .5:.5 amounts has been allocated to each partner. Hence, at the time of allocation terms of

partnership agreement has been undertaken by the partners.

PART D

1. List any amounts for which there is no present entitlement as at 30 June 2017

It can be seen from the table that George Smiley received the income for £41000. Along

with this, James Smiley which is the George brother received £17000. The other three

beneficaries are Scott, Jennifer and Mathew Smiley. These people received less amount of

money which is ewquivalent to 5000,5000 and 3000. As per Australia tax law those individuals

that receive an amount less then 6000 are not liable to pay any tax on the income that is received

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

from the trust. Thus, it can be said that in the present case Scott, Jennifer and Mathew are not

liable to pay tax and are entitled to obtain relaxation from the payment of tax or tax liability. This

means that other entities which are George and James Smiley are liable to pay tax to tax

department (An overview of trusts in Australia, 2017). It can be said that releaxation is given to

those in terms of payment of tax. It is very important to give relaxation in tax to the individuaals.

This is because by doing so it is ensured that those who have less income will not face shortage

of money due to payment of tax. Time to time many amendments are made in the law and by

doing so it is ensured that appropriate amount of tax is charged on the individuals. Usually

percentage of tax is very high on the income and due to this reason those that are liable to pay tax

have to pay heavy amount of cash inflow to the tax department of the nation. Thus, it can be said

that in order to ensure that low income individual will not face huge problem lots of relaxation is

given to them in terms of tax.

2 Amount retained by trust

No amount is retained by trust as it can be observed that in total amount of balance

retained by trustee is equal to zero. This is because entire amount of net income of trust is

£68000. If total of allocations will be done then it can be observed that allocation is higher than

net income of trust. This can be verified from the example that is given below.

Table 1Calculation of amount retained in the business

Net income of trust 68000

Allocation of fund

George Smiley 41000

James Smiley 17000

Scott Smiley 5000

Jennifer Smiley 5000

Mathew Smiley 3000

Total 71000

Value -3000

liable to pay tax and are entitled to obtain relaxation from the payment of tax or tax liability. This

means that other entities which are George and James Smiley are liable to pay tax to tax

department (An overview of trusts in Australia, 2017). It can be said that releaxation is given to

those in terms of payment of tax. It is very important to give relaxation in tax to the individuaals.

This is because by doing so it is ensured that those who have less income will not face shortage

of money due to payment of tax. Time to time many amendments are made in the law and by

doing so it is ensured that appropriate amount of tax is charged on the individuals. Usually

percentage of tax is very high on the income and due to this reason those that are liable to pay tax

have to pay heavy amount of cash inflow to the tax department of the nation. Thus, it can be said

that in order to ensure that low income individual will not face huge problem lots of relaxation is

given to them in terms of tax.

2 Amount retained by trust

No amount is retained by trust as it can be observed that in total amount of balance

retained by trustee is equal to zero. This is because entire amount of net income of trust is

£68000. If total of allocations will be done then it can be observed that allocation is higher than

net income of trust. This can be verified from the example that is given below.

Table 1Calculation of amount retained in the business

Net income of trust 68000

Allocation of fund

George Smiley 41000

James Smiley 17000

Scott Smiley 5000

Jennifer Smiley 5000

Mathew Smiley 3000

Total 71000

Value -3000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It can be seen from the table that from the net income of trust expenditures is 68000 and overall

expenditure amount is 71000. This reflects that more than net income of trust allocation is made

which means that nothing is retained in trust.

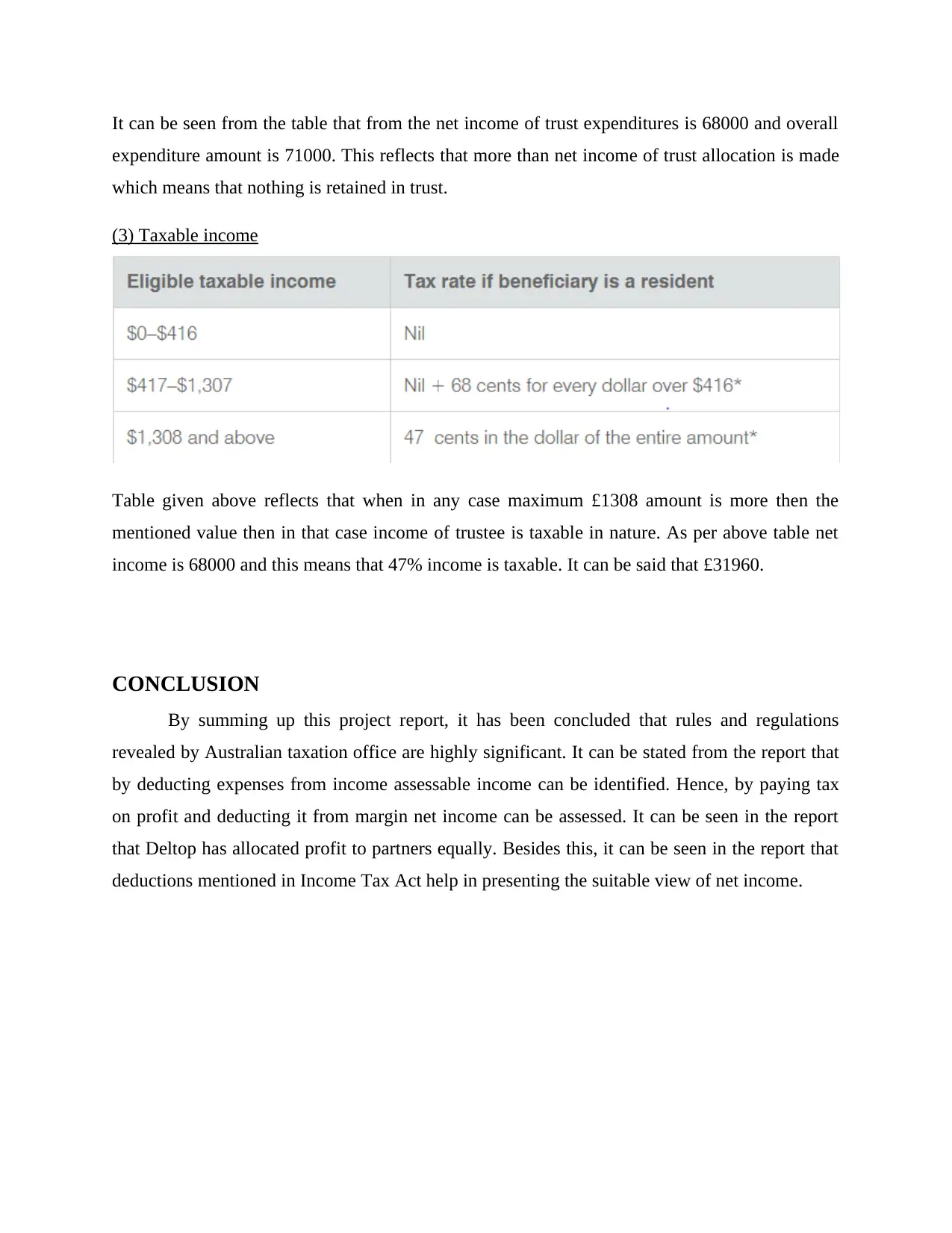

(3) Taxable income

Table given above reflects that when in any case maximum £1308 amount is more then the

mentioned value then in that case income of trustee is taxable in nature. As per above table net

income is 68000 and this means that 47% income is taxable. It can be said that £31960.

CONCLUSION

By summing up this project report, it has been concluded that rules and regulations

revealed by Australian taxation office are highly significant. It can be stated from the report that

by deducting expenses from income assessable income can be identified. Hence, by paying tax

on profit and deducting it from margin net income can be assessed. It can be seen in the report

that Deltop has allocated profit to partners equally. Besides this, it can be seen in the report that

deductions mentioned in Income Tax Act help in presenting the suitable view of net income.

expenditure amount is 71000. This reflects that more than net income of trust allocation is made

which means that nothing is retained in trust.

(3) Taxable income

Table given above reflects that when in any case maximum £1308 amount is more then the

mentioned value then in that case income of trustee is taxable in nature. As per above table net

income is 68000 and this means that 47% income is taxable. It can be said that £31960.

CONCLUSION

By summing up this project report, it has been concluded that rules and regulations

revealed by Australian taxation office are highly significant. It can be stated from the report that

by deducting expenses from income assessable income can be identified. Hence, by paying tax

on profit and deducting it from margin net income can be assessed. It can be seen in the report

that Deltop has allocated profit to partners equally. Besides this, it can be seen in the report that

deductions mentioned in Income Tax Act help in presenting the suitable view of net income.

REFERENCES

Books and Journals

Alghamdi, A. and Rahim, M., 2016. Development of a Measurement Scale for User Satisfaction

with E-tax Systems in Australia. In Transactions on Large-Scale Data-and Knowledge-

Centered Systems XXVII (pp. 64-83). Springer Berlin Heidelberg.

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

James, K., 2016. The Australian Taxation Office perspective on work-related travel expense

deductions for academics. International Journal of Critical Accounting. 8(5-6). pp.345-362

Lam, D. and Whitney, A., 2016. Taxation and property: Practical aspects of the new foreign

resident CGT witholding tax. LSJ: Law Society of NSW Journal. (21). p.84.

Woellner, R. and et.al., 2017. Australian Taxation Law 2017 27th edition. OUP Catalogue.

Online

An overview of trusts in Australia, 2017. [Online]. Available

through:<https://www.davidgarry.com.au/overview-of-trusts-in-australia.html>. [Accessed

on 12th May 2017].

Books and Journals

Alghamdi, A. and Rahim, M., 2016. Development of a Measurement Scale for User Satisfaction

with E-tax Systems in Australia. In Transactions on Large-Scale Data-and Knowledge-

Centered Systems XXVII (pp. 64-83). Springer Berlin Heidelberg.

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

James, K., 2016. The Australian Taxation Office perspective on work-related travel expense

deductions for academics. International Journal of Critical Accounting. 8(5-6). pp.345-362

Lam, D. and Whitney, A., 2016. Taxation and property: Practical aspects of the new foreign

resident CGT witholding tax. LSJ: Law Society of NSW Journal. (21). p.84.

Woellner, R. and et.al., 2017. Australian Taxation Law 2017 27th edition. OUP Catalogue.

Online

An overview of trusts in Australia, 2017. [Online]. Available

through:<https://www.davidgarry.com.au/overview-of-trusts-in-australia.html>. [Accessed

on 12th May 2017].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.