Taxation Law Assignment: CGT, Depreciation and Business Assets

VerifiedAdded on 2022/10/18

|12

|2877

|15

Homework Assignment

AI Summary

This taxation law assignment solution addresses two key questions concerning Australian tax law. The first question analyzes various scenarios related to capital gains tax (CGT), including the sale of a primary residence, personal use assets like cars and furniture, small business CGT concessions, and the treatment of collectables. It explores relevant sections of the Income Tax Assessment Act 1997 (ITAA 1997) and explains how different assets are treated under CGT rules. The second question focuses on depreciation deductions for business assets, specifically examining the case of a manufacturing company owner who purchases a CNC machine. The solution outlines the relevant provisions of the ITAA 1997 regarding depreciating assets, including the definition of depreciating assets, the start time for depreciation, and the components of the asset's cost base. It applies these principles to the CNC machine scenario, determining the allowable depreciation deductions and the impact of additional expenses like installation and guiding rod costs. Overall, the assignment provides a comprehensive overview of CGT and depreciation rules in an Australian context.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................6

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................6

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Answer A:

A receipt received by the taxpayer regarding the sale of capital asset is known as

capital. Before 20 September 1985, the capital receipts were considered as non-taxable or tax

free until and unless the gains are derived from either from the disposal of asset acquired for

profit deriving purpose or a profit-deriving undertaking (Gordon 2017). Any assets purchased

before that date is exempted from capital gains and only real capital gains are considered

taxable following that date. The capital gains or loss that takes place to the house in which the

taxpayer is living is disregarded on the basis of the conditions that;

a. The taxpayer is an individual

b. The house was considered as the main dwelling all through the ownership period

c. The dwelling ownership was not passed to taxpayer as the beneficiary of the deceased

estate.

Jasmine being the Australian occupant is moving to UK and she is selling all her

Australian assets. She sells her home that has been her main dwelling from 1981. The home

was purchased by paying $40,000 and presently it was sold for $650,000. As it can be seen

that the house is her main dwelling and the capital gains that is made by her will be exempted

since the property is the pre-CGT asset (Bain and Boccabella 2019). She bought the house

prior to the introduction of CGT scheme and no tax is payable in this regard Jasmine.

Answer B:

As per the “sec 108-5, ITAA 97”, CGT asset comprises of any form of property

whether tangible or intangible. There are certain kinds of property that are dealt in special

manner. CGT is caused under “sec 104, ITAA 1997” on the occurrence of CGT event

Answer to question 1:

Answer A:

A receipt received by the taxpayer regarding the sale of capital asset is known as

capital. Before 20 September 1985, the capital receipts were considered as non-taxable or tax

free until and unless the gains are derived from either from the disposal of asset acquired for

profit deriving purpose or a profit-deriving undertaking (Gordon 2017). Any assets purchased

before that date is exempted from capital gains and only real capital gains are considered

taxable following that date. The capital gains or loss that takes place to the house in which the

taxpayer is living is disregarded on the basis of the conditions that;

a. The taxpayer is an individual

b. The house was considered as the main dwelling all through the ownership period

c. The dwelling ownership was not passed to taxpayer as the beneficiary of the deceased

estate.

Jasmine being the Australian occupant is moving to UK and she is selling all her

Australian assets. She sells her home that has been her main dwelling from 1981. The home

was purchased by paying $40,000 and presently it was sold for $650,000. As it can be seen

that the house is her main dwelling and the capital gains that is made by her will be exempted

since the property is the pre-CGT asset (Bain and Boccabella 2019). She bought the house

prior to the introduction of CGT scheme and no tax is payable in this regard Jasmine.

Answer B:

As per the “sec 108-5, ITAA 97”, CGT asset comprises of any form of property

whether tangible or intangible. There are certain kinds of property that are dealt in special

manner. CGT is caused under “sec 104, ITAA 1997” on the occurrence of CGT event

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

(Coates 2015). The main CGT event involves the “CGT event A1” which includes the

disposal of asset.

A personal use asset (PUA) is referred under “sec 108-20, ITAA 97” as those CGT

asset excluding the collectable which is kept for private usage and fun of the taxpayer (Lam

and Whitney 2016). Signifying “sec 108.20(1), ITAA 1997” capital loss instigating from the

sale of private usage asset is simply ignored notwithstanding of the acquisition price paid.

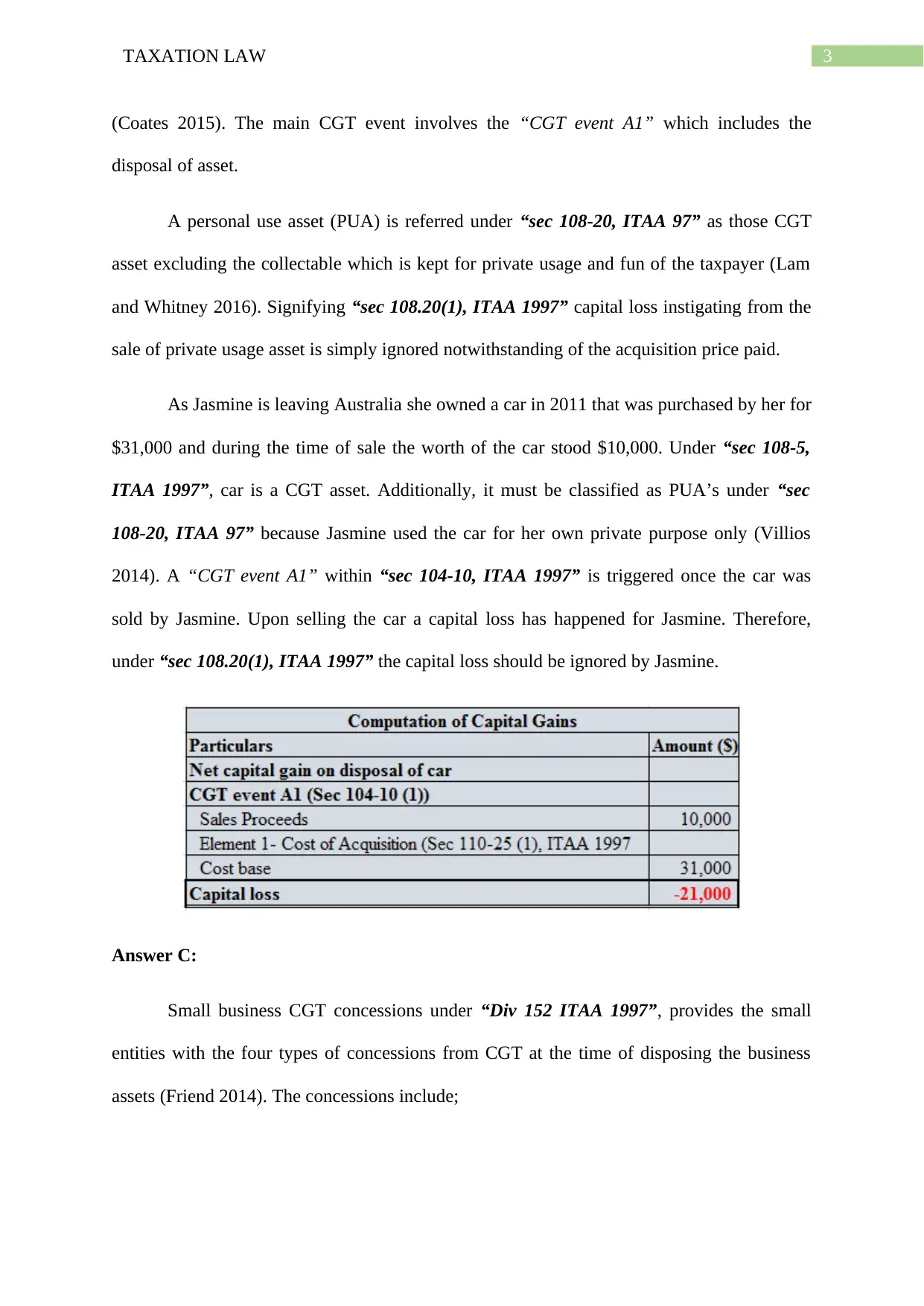

As Jasmine is leaving Australia she owned a car in 2011 that was purchased by her for

$31,000 and during the time of sale the worth of the car stood $10,000. Under “sec 108-5,

ITAA 1997”, car is a CGT asset. Additionally, it must be classified as PUA’s under “sec

108-20, ITAA 97” because Jasmine used the car for her own private purpose only (Villios

2014). A “CGT event A1” within “sec 104-10, ITAA 1997” is triggered once the car was

sold by Jasmine. Upon selling the car a capital loss has happened for Jasmine. Therefore,

under “sec 108.20(1), ITAA 1997” the capital loss should be ignored by Jasmine.

Answer C:

Small business CGT concessions under “Div 152 ITAA 1997”, provides the small

entities with the four types of concessions from CGT at the time of disposing the business

assets (Friend 2014). The concessions include;

(Coates 2015). The main CGT event involves the “CGT event A1” which includes the

disposal of asset.

A personal use asset (PUA) is referred under “sec 108-20, ITAA 97” as those CGT

asset excluding the collectable which is kept for private usage and fun of the taxpayer (Lam

and Whitney 2016). Signifying “sec 108.20(1), ITAA 1997” capital loss instigating from the

sale of private usage asset is simply ignored notwithstanding of the acquisition price paid.

As Jasmine is leaving Australia she owned a car in 2011 that was purchased by her for

$31,000 and during the time of sale the worth of the car stood $10,000. Under “sec 108-5,

ITAA 1997”, car is a CGT asset. Additionally, it must be classified as PUA’s under “sec

108-20, ITAA 97” because Jasmine used the car for her own private purpose only (Villios

2014). A “CGT event A1” within “sec 104-10, ITAA 1997” is triggered once the car was

sold by Jasmine. Upon selling the car a capital loss has happened for Jasmine. Therefore,

under “sec 108.20(1), ITAA 1997” the capital loss should be ignored by Jasmine.

Answer C:

Small business CGT concessions under “Div 152 ITAA 1997”, provides the small

entities with the four types of concessions from CGT at the time of disposing the business

assets (Friend 2014). The concessions include;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

a. The 15-year exemption for assets which the taxpayer has held under their ownership

for a minimum of 15 years.

b. The 50% reduction following the access of 50% discount if qualified

c. The retirement concession allows the taxpayer to disregard the capital gains by around

$500,000 given the proceeds are used in relation to the retirement of the taxpayer.

d. The rollover relief allows the taxpayer to defer the capital gain on small business

active asset when acquisition of replacement assets is made by the taxpayer.

To claim the above given relief the taxpayer is required to satisfy some important

conditions (Sadiq and Marsden 2014). Under “sub-div 152-A, ITAA 1997” the basic

conditions that must be met are as follows;

a. The business entity must be a small entity with turnover of lower than $2 million in

the previous year or the net value of assets should not be higher than $6 million.

b. The CGT asset is ought to be an active asset.

Jasmine is found to be retiring from her business because she is moving to UK on a

permanent basis. She sold all her business assets for $65,000 and her goodwill for $60,000.

Jasmine here should be considered eligible for small business CGT concession because she

has satisfied the basic conditions of SBE where all her business assets does not have worth

more than $6 million. Jasmine can obtain the 15-year exemption concession from the sale of

CGT asset. This is because the asset was under Jasmine ownership for 15-year and she also

aged more than 55 years. So she can avail the 15-year exemption from the capital gains made

from CGT asset disposal.

Answer D:

Jasmine owned a furniture that had the value of $2,000 however in the present year

she sold her furniture for $5,000. Notably, under “sec 118-10 (3), ITAA 1997” capital gains

a. The 15-year exemption for assets which the taxpayer has held under their ownership

for a minimum of 15 years.

b. The 50% reduction following the access of 50% discount if qualified

c. The retirement concession allows the taxpayer to disregard the capital gains by around

$500,000 given the proceeds are used in relation to the retirement of the taxpayer.

d. The rollover relief allows the taxpayer to defer the capital gain on small business

active asset when acquisition of replacement assets is made by the taxpayer.

To claim the above given relief the taxpayer is required to satisfy some important

conditions (Sadiq and Marsden 2014). Under “sub-div 152-A, ITAA 1997” the basic

conditions that must be met are as follows;

a. The business entity must be a small entity with turnover of lower than $2 million in

the previous year or the net value of assets should not be higher than $6 million.

b. The CGT asset is ought to be an active asset.

Jasmine is found to be retiring from her business because she is moving to UK on a

permanent basis. She sold all her business assets for $65,000 and her goodwill for $60,000.

Jasmine here should be considered eligible for small business CGT concession because she

has satisfied the basic conditions of SBE where all her business assets does not have worth

more than $6 million. Jasmine can obtain the 15-year exemption concession from the sale of

CGT asset. This is because the asset was under Jasmine ownership for 15-year and she also

aged more than 55 years. So she can avail the 15-year exemption from the capital gains made

from CGT asset disposal.

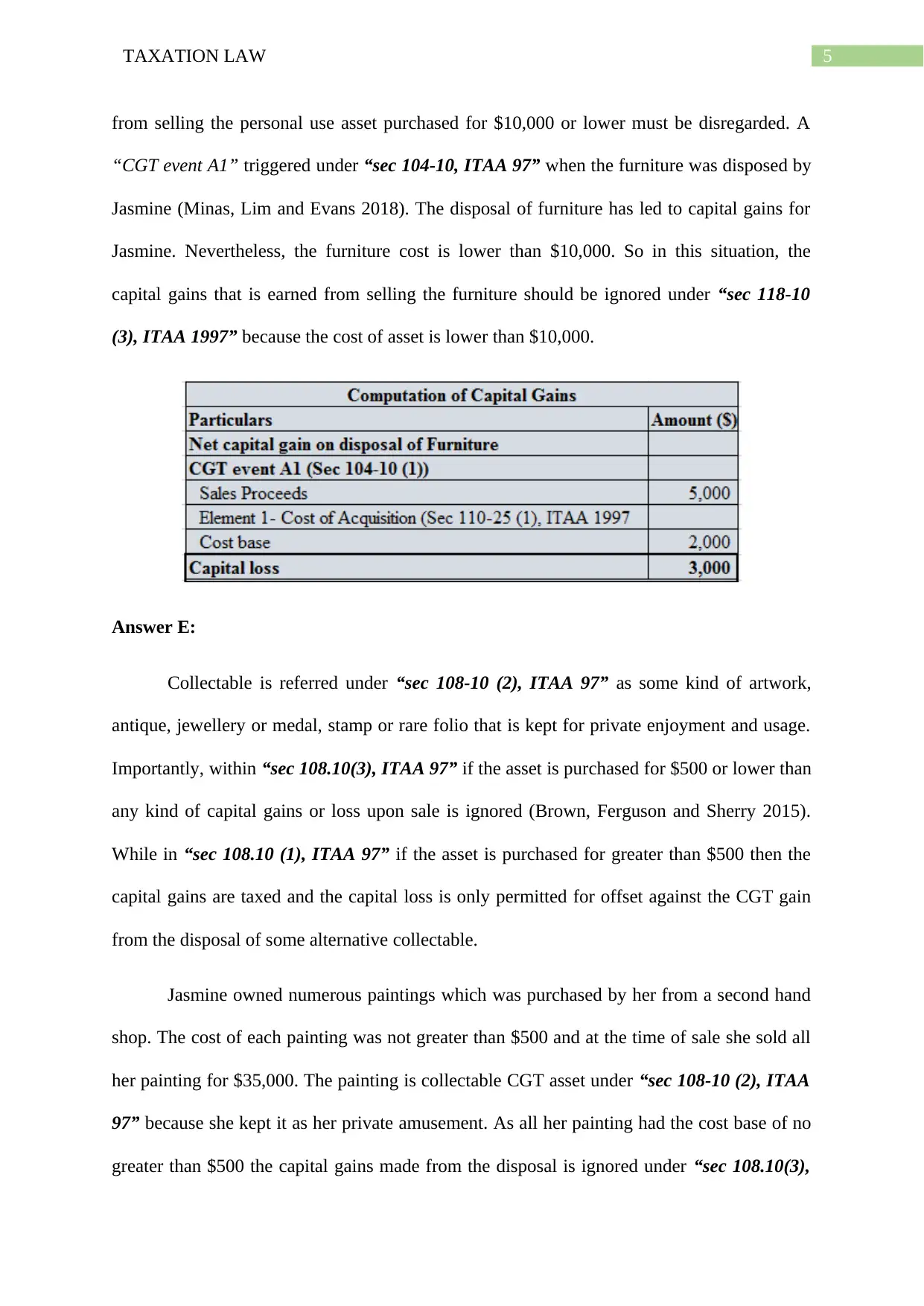

Answer D:

Jasmine owned a furniture that had the value of $2,000 however in the present year

she sold her furniture for $5,000. Notably, under “sec 118-10 (3), ITAA 1997” capital gains

5TAXATION LAW

from selling the personal use asset purchased for $10,000 or lower must be disregarded. A

“CGT event A1” triggered under “sec 104-10, ITAA 97” when the furniture was disposed by

Jasmine (Minas, Lim and Evans 2018). The disposal of furniture has led to capital gains for

Jasmine. Nevertheless, the furniture cost is lower than $10,000. So in this situation, the

capital gains that is earned from selling the furniture should be ignored under “sec 118-10

(3), ITAA 1997” because the cost of asset is lower than $10,000.

Answer E:

Collectable is referred under “sec 108-10 (2), ITAA 97” as some kind of artwork,

antique, jewellery or medal, stamp or rare folio that is kept for private enjoyment and usage.

Importantly, within “sec 108.10(3), ITAA 97” if the asset is purchased for $500 or lower than

any kind of capital gains or loss upon sale is ignored (Brown, Ferguson and Sherry 2015).

While in “sec 108.10 (1), ITAA 97” if the asset is purchased for greater than $500 then the

capital gains are taxed and the capital loss is only permitted for offset against the CGT gain

from the disposal of some alternative collectable.

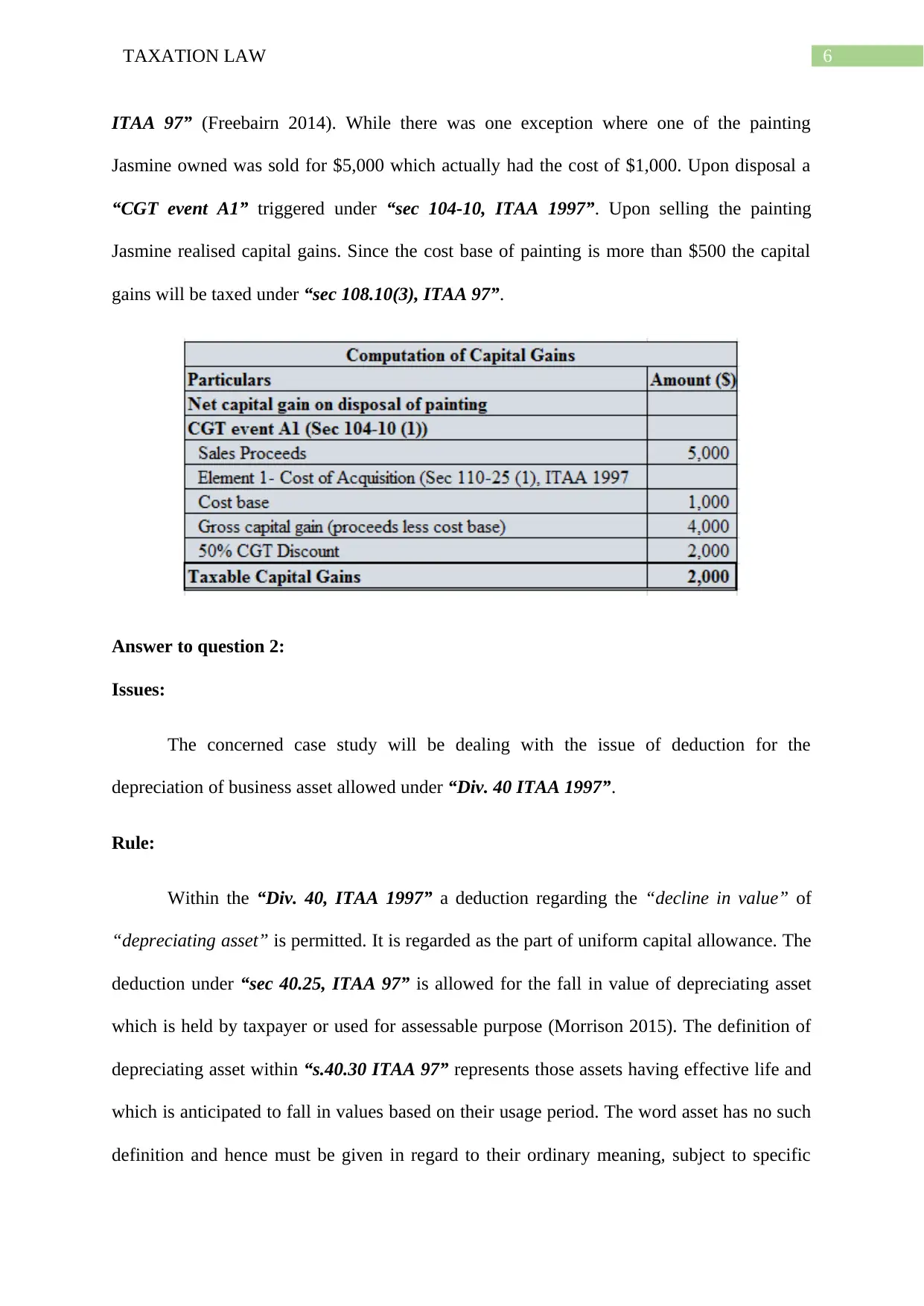

Jasmine owned numerous paintings which was purchased by her from a second hand

shop. The cost of each painting was not greater than $500 and at the time of sale she sold all

her painting for $35,000. The painting is collectable CGT asset under “sec 108-10 (2), ITAA

97” because she kept it as her private amusement. As all her painting had the cost base of no

greater than $500 the capital gains made from the disposal is ignored under “sec 108.10(3),

from selling the personal use asset purchased for $10,000 or lower must be disregarded. A

“CGT event A1” triggered under “sec 104-10, ITAA 97” when the furniture was disposed by

Jasmine (Minas, Lim and Evans 2018). The disposal of furniture has led to capital gains for

Jasmine. Nevertheless, the furniture cost is lower than $10,000. So in this situation, the

capital gains that is earned from selling the furniture should be ignored under “sec 118-10

(3), ITAA 1997” because the cost of asset is lower than $10,000.

Answer E:

Collectable is referred under “sec 108-10 (2), ITAA 97” as some kind of artwork,

antique, jewellery or medal, stamp or rare folio that is kept for private enjoyment and usage.

Importantly, within “sec 108.10(3), ITAA 97” if the asset is purchased for $500 or lower than

any kind of capital gains or loss upon sale is ignored (Brown, Ferguson and Sherry 2015).

While in “sec 108.10 (1), ITAA 97” if the asset is purchased for greater than $500 then the

capital gains are taxed and the capital loss is only permitted for offset against the CGT gain

from the disposal of some alternative collectable.

Jasmine owned numerous paintings which was purchased by her from a second hand

shop. The cost of each painting was not greater than $500 and at the time of sale she sold all

her painting for $35,000. The painting is collectable CGT asset under “sec 108-10 (2), ITAA

97” because she kept it as her private amusement. As all her painting had the cost base of no

greater than $500 the capital gains made from the disposal is ignored under “sec 108.10(3),

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

ITAA 97” (Freebairn 2014). While there was one exception where one of the painting

Jasmine owned was sold for $5,000 which actually had the cost of $1,000. Upon disposal a

“CGT event A1” triggered under “sec 104-10, ITAA 1997”. Upon selling the painting

Jasmine realised capital gains. Since the cost base of painting is more than $500 the capital

gains will be taxed under “sec 108.10(3), ITAA 97”.

Answer to question 2:

Issues:

The concerned case study will be dealing with the issue of deduction for the

depreciation of business asset allowed under “Div. 40 ITAA 1997”.

Rule:

Within the “Div. 40, ITAA 1997” a deduction regarding the “decline in value” of

“depreciating asset” is permitted. It is regarded as the part of uniform capital allowance. The

deduction under “sec 40.25, ITAA 97” is allowed for the fall in value of depreciating asset

which is held by taxpayer or used for assessable purpose (Morrison 2015). The definition of

depreciating asset within “s.40.30 ITAA 97” represents those assets having effective life and

which is anticipated to fall in values based on their usage period. The word asset has no such

definition and hence must be given in regard to their ordinary meaning, subject to specific

ITAA 97” (Freebairn 2014). While there was one exception where one of the painting

Jasmine owned was sold for $5,000 which actually had the cost of $1,000. Upon disposal a

“CGT event A1” triggered under “sec 104-10, ITAA 1997”. Upon selling the painting

Jasmine realised capital gains. Since the cost base of painting is more than $500 the capital

gains will be taxed under “sec 108.10(3), ITAA 97”.

Answer to question 2:

Issues:

The concerned case study will be dealing with the issue of deduction for the

depreciation of business asset allowed under “Div. 40 ITAA 1997”.

Rule:

Within the “Div. 40, ITAA 1997” a deduction regarding the “decline in value” of

“depreciating asset” is permitted. It is regarded as the part of uniform capital allowance. The

deduction under “sec 40.25, ITAA 97” is allowed for the fall in value of depreciating asset

which is held by taxpayer or used for assessable purpose (Morrison 2015). The definition of

depreciating asset within “s.40.30 ITAA 97” represents those assets having effective life and

which is anticipated to fall in values based on their usage period. The word asset has no such

definition and hence must be given in regard to their ordinary meaning, subject to specific

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

requirement of capital allowance provision. The ordinary definition of plant is considered in

“FCT v Wangaratta Woollen Mills Ltd (1969)” where a structure of dye house was held as

plant.

While “sec 40.40, ITAA 97” explains the rules that takes into the account holding of

asset under numerous situations. This includes that the asset should held by taxpayer for

assessable purpose and must be installed for set business use (Cook 2015). While “sec 40.25

(7), ITAA 97” explains that taxable purpose comprises of the use of machine for producing

business income, while the deduction is lowered based on the use of asset other than the

taxable purpose. Under the “s40.60 ITAA 97” the “decline in value” starts when the when

asset is first used or installed by the taxpayer for their business purpose. This is usually

known as the start time and the deduction for depreciation is generally on the basis of the

effective life as well as price paid to acquire the depreciating asset.

Under “Subdiv.40-C”, the deduction for the depreciation of the business use asset is

allowed to taxpayer on the basis of the cost of the asset (Smith 2015). The cost of the asset

normally includes two elements. The first element under “sec 40-180” includes the

following;

a. Working out initially the time when the taxpayer first used holds the assets

b. It commonly includes the amount that is paid for the assets

While “sec 40-190, ITAA 97” is associated with the second element cost base of

depreciating asset (Kenny 2015). This includes the amount which the taxpayer usually pays

to bring the asset in its current conditions and the location including the transportation cost

and cost incurred for installing the asset.

Application:

requirement of capital allowance provision. The ordinary definition of plant is considered in

“FCT v Wangaratta Woollen Mills Ltd (1969)” where a structure of dye house was held as

plant.

While “sec 40.40, ITAA 97” explains the rules that takes into the account holding of

asset under numerous situations. This includes that the asset should held by taxpayer for

assessable purpose and must be installed for set business use (Cook 2015). While “sec 40.25

(7), ITAA 97” explains that taxable purpose comprises of the use of machine for producing

business income, while the deduction is lowered based on the use of asset other than the

taxable purpose. Under the “s40.60 ITAA 97” the “decline in value” starts when the when

asset is first used or installed by the taxpayer for their business purpose. This is usually

known as the start time and the deduction for depreciation is generally on the basis of the

effective life as well as price paid to acquire the depreciating asset.

Under “Subdiv.40-C”, the deduction for the depreciation of the business use asset is

allowed to taxpayer on the basis of the cost of the asset (Smith 2015). The cost of the asset

normally includes two elements. The first element under “sec 40-180” includes the

following;

a. Working out initially the time when the taxpayer first used holds the assets

b. It commonly includes the amount that is paid for the assets

While “sec 40-190, ITAA 97” is associated with the second element cost base of

depreciating asset (Kenny 2015). This includes the amount which the taxpayer usually pays

to bring the asset in its current conditions and the location including the transportation cost

and cost incurred for installing the asset.

Application:

8TAXATION LAW

Evidently, John is the owner of manufacturing company. His company is mainly

dealing with the manufacturing of motor vehicle parts and produces. John was primarily

engaged in the production of BMW car parts. On 1st November 2014, John purchased a

numerical control machine (CNC) which he had imported from Germany. The acquisition

cost of the CNC machine stood $300,000. Citing the factual situation of “FCT v Wangaratta

Woollen Mills Ltd (1969)” in case of John the machine satisfies the definition of depreciating

asset under “sec 40.25 ITAA 97” (Khoury 2015). This is because the controlled numerical

computer has some reasonable effective life and it is also projected to “decline in value”

based on its usage over the time.

Denoting “sec 40.25 ITAA 97” the machine was held by John completely for the

taxable purpose. As a result, the deduction for the decline in value of the CNC machine is

permitted for claim under “sec 40.25, ITAA 1997”.

The CNC machine was finally installed by John on 15 January and he paid a total cost

of $25,000 for the installation of the machine. Once the installation of the machine was

completed, John began using the machine for his business purpose. Denoting “sec 40.60

ITAA 1997”, the start time is 15 January for computing the decline in value of the Machine

because the machine was installed for ready business usage from that onwards (Kenny 2015).

In other words, John first started using the machine for taxable business purpose from that

date onwards.

Additionally, on 1st February a guiding rod was added into the CNC machine by John.

He occurred a cost of $5,000 on installing a guiding rod. To compute the cost of the CNC

machine with the objective of computing the capital allowance under “Subdiv 40-C, ITAA

1997” it is necessary to take into the account the overall cost base of the machine (Cook

2015). Under “sec 40.180 ITAA 1997”, the first element cost base of CNC machine would

Evidently, John is the owner of manufacturing company. His company is mainly

dealing with the manufacturing of motor vehicle parts and produces. John was primarily

engaged in the production of BMW car parts. On 1st November 2014, John purchased a

numerical control machine (CNC) which he had imported from Germany. The acquisition

cost of the CNC machine stood $300,000. Citing the factual situation of “FCT v Wangaratta

Woollen Mills Ltd (1969)” in case of John the machine satisfies the definition of depreciating

asset under “sec 40.25 ITAA 97” (Khoury 2015). This is because the controlled numerical

computer has some reasonable effective life and it is also projected to “decline in value”

based on its usage over the time.

Denoting “sec 40.25 ITAA 97” the machine was held by John completely for the

taxable purpose. As a result, the deduction for the decline in value of the CNC machine is

permitted for claim under “sec 40.25, ITAA 1997”.

The CNC machine was finally installed by John on 15 January and he paid a total cost

of $25,000 for the installation of the machine. Once the installation of the machine was

completed, John began using the machine for his business purpose. Denoting “sec 40.60

ITAA 1997”, the start time is 15 January for computing the decline in value of the Machine

because the machine was installed for ready business usage from that onwards (Kenny 2015).

In other words, John first started using the machine for taxable business purpose from that

date onwards.

Additionally, on 1st February a guiding rod was added into the CNC machine by John.

He occurred a cost of $5,000 on installing a guiding rod. To compute the cost of the CNC

machine with the objective of computing the capital allowance under “Subdiv 40-C, ITAA

1997” it is necessary to take into the account the overall cost base of the machine (Cook

2015). Under “sec 40.180 ITAA 1997”, the first element cost base of CNC machine would

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

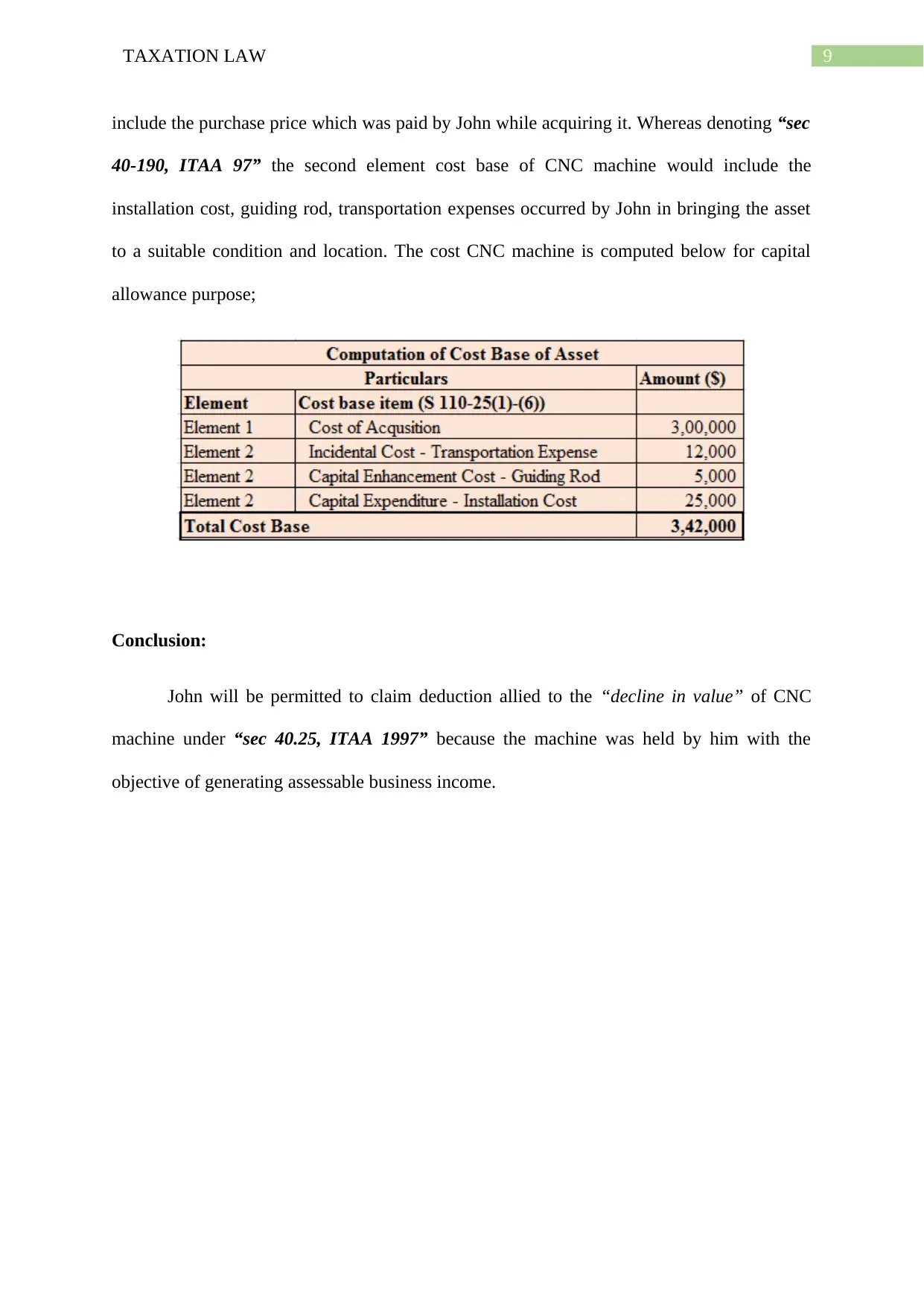

9TAXATION LAW

include the purchase price which was paid by John while acquiring it. Whereas denoting “sec

40-190, ITAA 97” the second element cost base of CNC machine would include the

installation cost, guiding rod, transportation expenses occurred by John in bringing the asset

to a suitable condition and location. The cost CNC machine is computed below for capital

allowance purpose;

Conclusion:

John will be permitted to claim deduction allied to the “decline in value” of CNC

machine under “sec 40.25, ITAA 1997” because the machine was held by him with the

objective of generating assessable business income.

include the purchase price which was paid by John while acquiring it. Whereas denoting “sec

40-190, ITAA 97” the second element cost base of CNC machine would include the

installation cost, guiding rod, transportation expenses occurred by John in bringing the asset

to a suitable condition and location. The cost CNC machine is computed below for capital

allowance purpose;

Conclusion:

John will be permitted to claim deduction allied to the “decline in value” of CNC

machine under “sec 40.25, ITAA 1997” because the machine was held by him with the

objective of generating assessable business income.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Bain, K and Boccabella, D, 2019. The age of the home worker - part 2: Calculation of home

occupancy expense deductions, deduction apportionment and partial loss of CGT main

residence exemption. Australian Tax Forum, 34(1), pp.65–93.

Brown, P., Ferguson, A. and Sherry, S., 2015. Investor behaviour in response to Australia’s

capital gains tax. Accounting & Finance, 50(4), pp.783–808.

Coates, M., 2015. Tax on property in deceased Estates - Part I: CGT. Mondaq Business

Briefing, pp.Mondaq Business Briefing, May 6, 2015.

Cook, K, 2015. Recent developments in administrative law. AIAL Forum, (81), pp.31–39.

Freebairn, J, 2014. A better and larger GST? Economic and Labour Relations Review, 22(3),

pp.85–100.

Friend, R, 2014. The CGT small business concessions: issues, anomalies and opportunities.

(capital gains tax) (Australia). Australian Tax Review, 40(2), pp.108–137.

Gordon, R., 2017. Proposed changes to CGT main residence exemption for foreign residents.

Mondaq Business Briefing, pp.Mondaq Business Briefing, August 22, 2017.

Kenny, P. et al., 2015. Australian tax 2015, Chatswood: LexisNexis Butterworths.

Khoury, D, 2015. Widening the availability of deductions under Australian taxation law. Tax

Specialist, 14(4), pp.207–211.

Lam, D. and Whitney, A., 2016. Practical aspects of the new foreign resident CGT

withholding tax. LSJ: Law Society of NSW Journal, (21), p.84.

Minas, J, Lim, Y and Evans, C, 2018. The impact of tax rate changes on capital gains

realisations: Evidence from Australia. Australian Tax Forum, 33(4), pp.635–666.

References:

Bain, K and Boccabella, D, 2019. The age of the home worker - part 2: Calculation of home

occupancy expense deductions, deduction apportionment and partial loss of CGT main

residence exemption. Australian Tax Forum, 34(1), pp.65–93.

Brown, P., Ferguson, A. and Sherry, S., 2015. Investor behaviour in response to Australia’s

capital gains tax. Accounting & Finance, 50(4), pp.783–808.

Coates, M., 2015. Tax on property in deceased Estates - Part I: CGT. Mondaq Business

Briefing, pp.Mondaq Business Briefing, May 6, 2015.

Cook, K, 2015. Recent developments in administrative law. AIAL Forum, (81), pp.31–39.

Freebairn, J, 2014. A better and larger GST? Economic and Labour Relations Review, 22(3),

pp.85–100.

Friend, R, 2014. The CGT small business concessions: issues, anomalies and opportunities.

(capital gains tax) (Australia). Australian Tax Review, 40(2), pp.108–137.

Gordon, R., 2017. Proposed changes to CGT main residence exemption for foreign residents.

Mondaq Business Briefing, pp.Mondaq Business Briefing, August 22, 2017.

Kenny, P. et al., 2015. Australian tax 2015, Chatswood: LexisNexis Butterworths.

Khoury, D, 2015. Widening the availability of deductions under Australian taxation law. Tax

Specialist, 14(4), pp.207–211.

Lam, D. and Whitney, A., 2016. Practical aspects of the new foreign resident CGT

withholding tax. LSJ: Law Society of NSW Journal, (21), p.84.

Minas, J, Lim, Y and Evans, C, 2018. The impact of tax rate changes on capital gains

realisations: Evidence from Australia. Australian Tax Forum, 33(4), pp.635–666.

11TAXATION LAW

Morrison, D., 2015. Never mind the law, just hurry up and collect more tax! The ATO

persists with unnecessary litigation. Insolvency Law Journal, 23(4), pp.196–208.

Sadiq, K. and Marsden, S., 2014. The small business CGT concessions: evidence from the

perspective of the tax practitioner. Revenue Law Journal, 24, pp.1–21.

Smith, J P, 2015. Australian state income taxation: A historical perspective. AUSTRALIAN

TAX FORUM, 30(4), pp.679–712.

Villios, Sylvia et al., 2014. The capital gains tax implications of buy-sell agreements.

(Australia). Australian Tax Review, 41(2), pp.100–112.

Morrison, D., 2015. Never mind the law, just hurry up and collect more tax! The ATO

persists with unnecessary litigation. Insolvency Law Journal, 23(4), pp.196–208.

Sadiq, K. and Marsden, S., 2014. The small business CGT concessions: evidence from the

perspective of the tax practitioner. Revenue Law Journal, 24, pp.1–21.

Smith, J P, 2015. Australian state income taxation: A historical perspective. AUSTRALIAN

TAX FORUM, 30(4), pp.679–712.

Villios, Sylvia et al., 2014. The capital gains tax implications of buy-sell agreements.

(Australia). Australian Tax Review, 41(2), pp.100–112.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.