CLWM4100 Taxation Law Assessment 3: CGT Event Timing & Capital Gains

VerifiedAdded on 2022/09/06

|7

|480

|24

Report

AI Summary

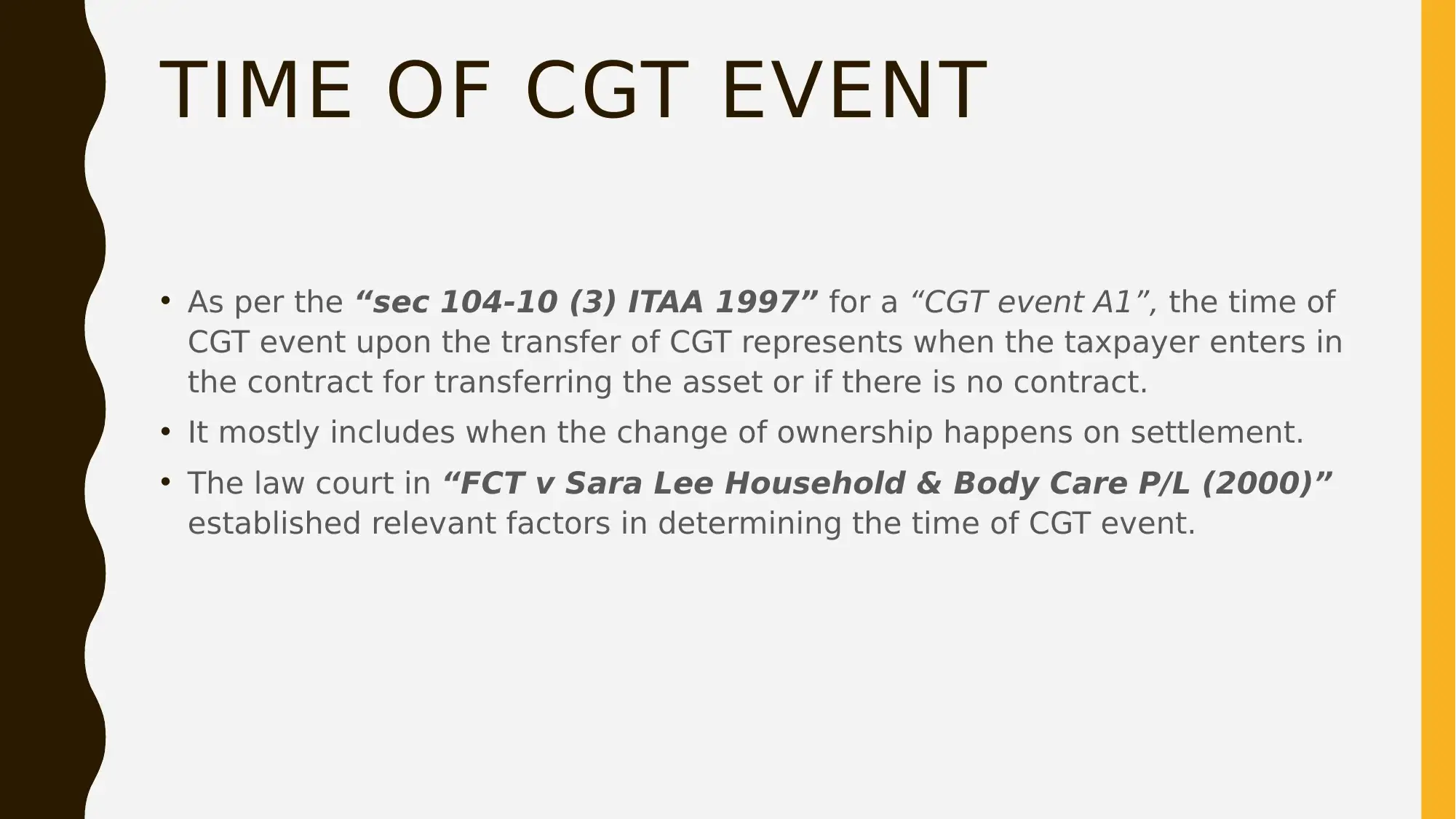

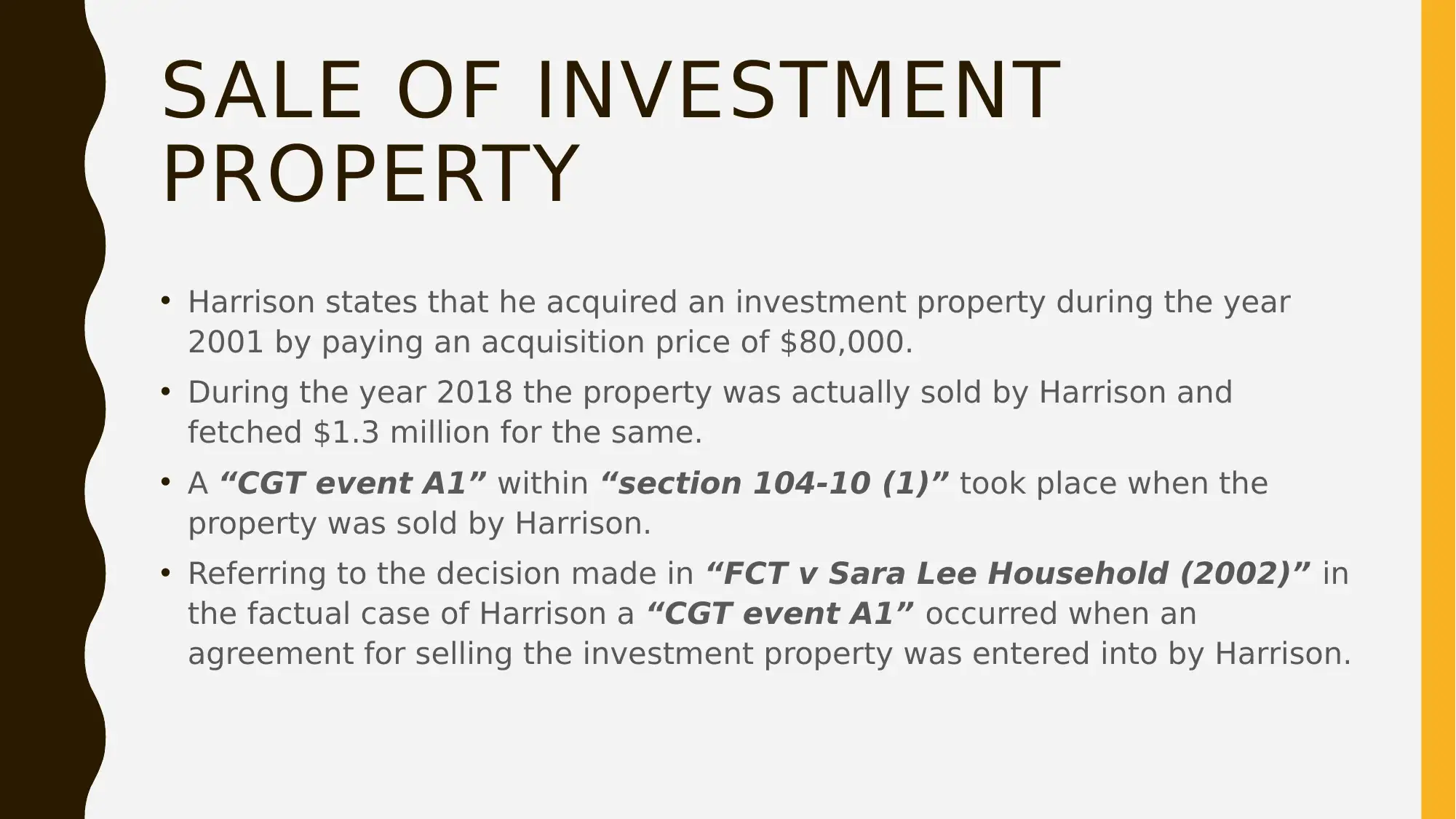

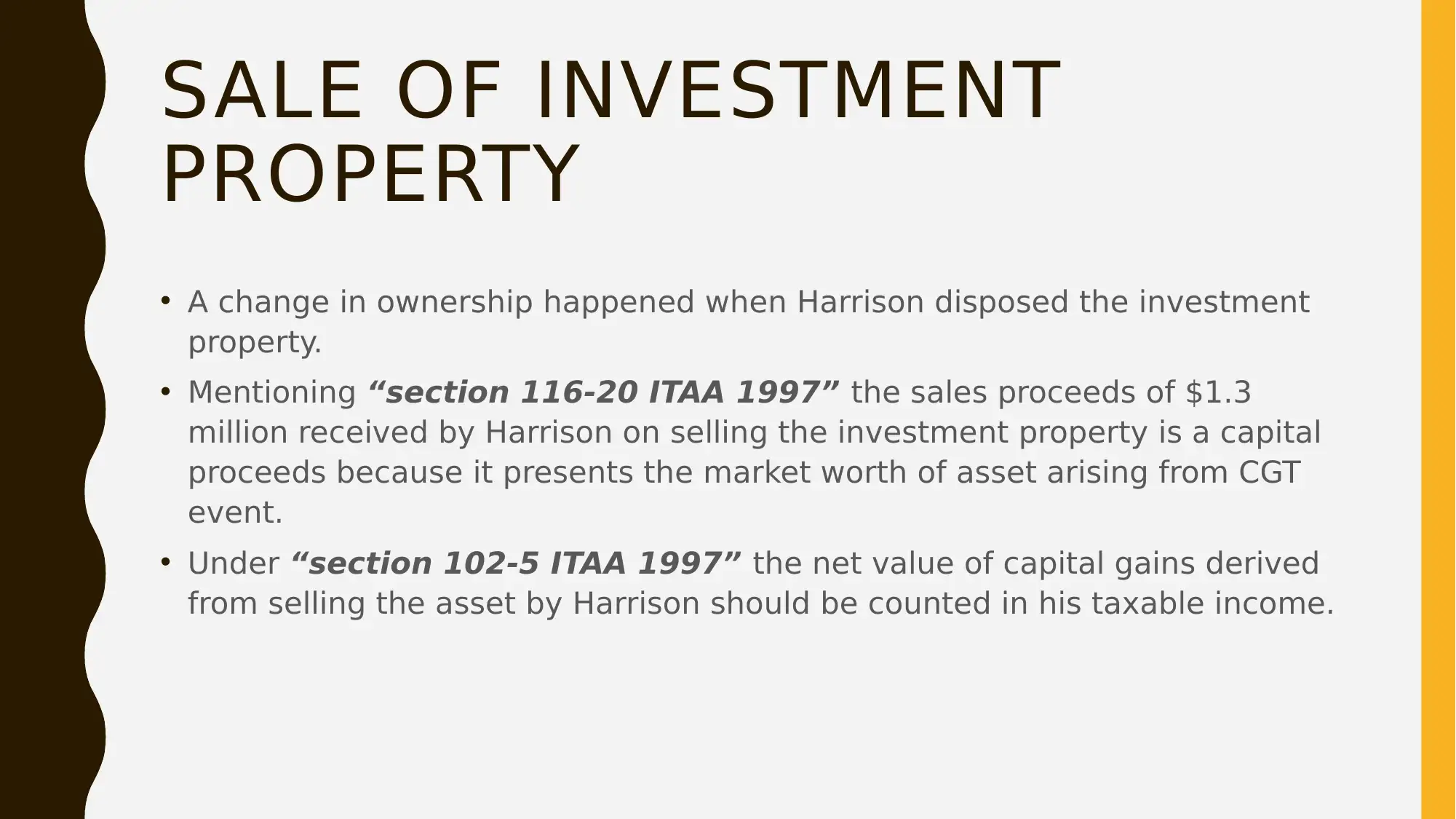

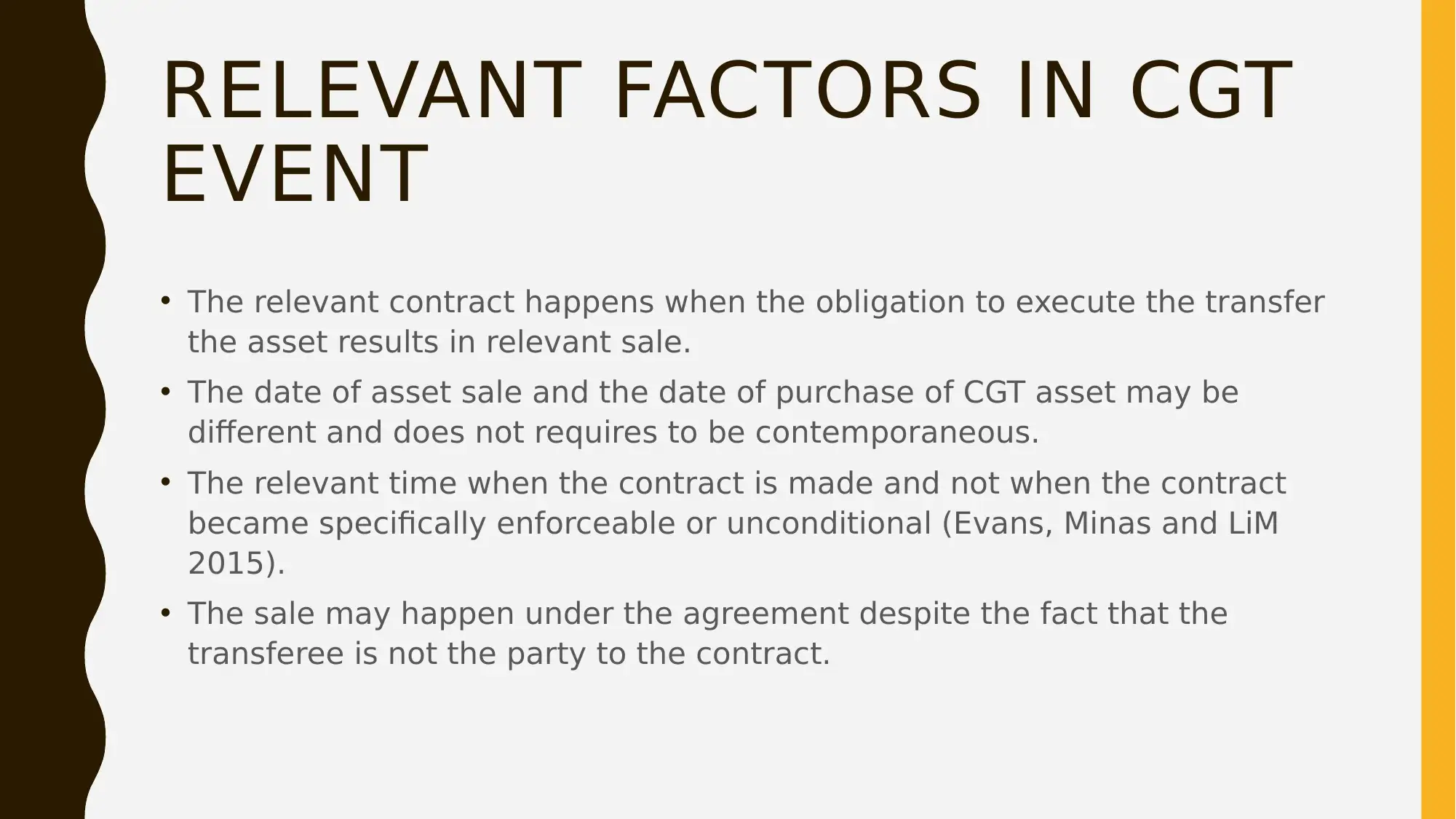

This report addresses a taxation law case study concerning CGT event timing and capital gains calculations for Harrison Carter. It begins by explaining the timing of a CGT event, referencing "sec 104-10 (3) ITAA 1997" and the "FCT v Sara Lee Household & Body Care P/L (2000)" case. The report then analyzes the sale of an investment property acquired in 2001 and sold in 2018, calculating capital gains and applying "section 116-20 ITAA 1997" and "section 102-5 ITAA 1997". It also considers the sale of shares acquired in 1985, classifying them as post-CGT assets and referencing "section 108-5 ITAA 1997". The report highlights relevant factors in determining CGT events and provides a detailed analysis of the tax implications for Harrison Carter, including the inclusion of capital gains in his taxable income. The report uses relevant case laws and sections to support the findings.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.