Taxation Theory, Practice & Law Assignment: CGT and FBT Analysis

VerifiedAdded on 2023/06/07

|10

|2334

|86

Homework Assignment

AI Summary

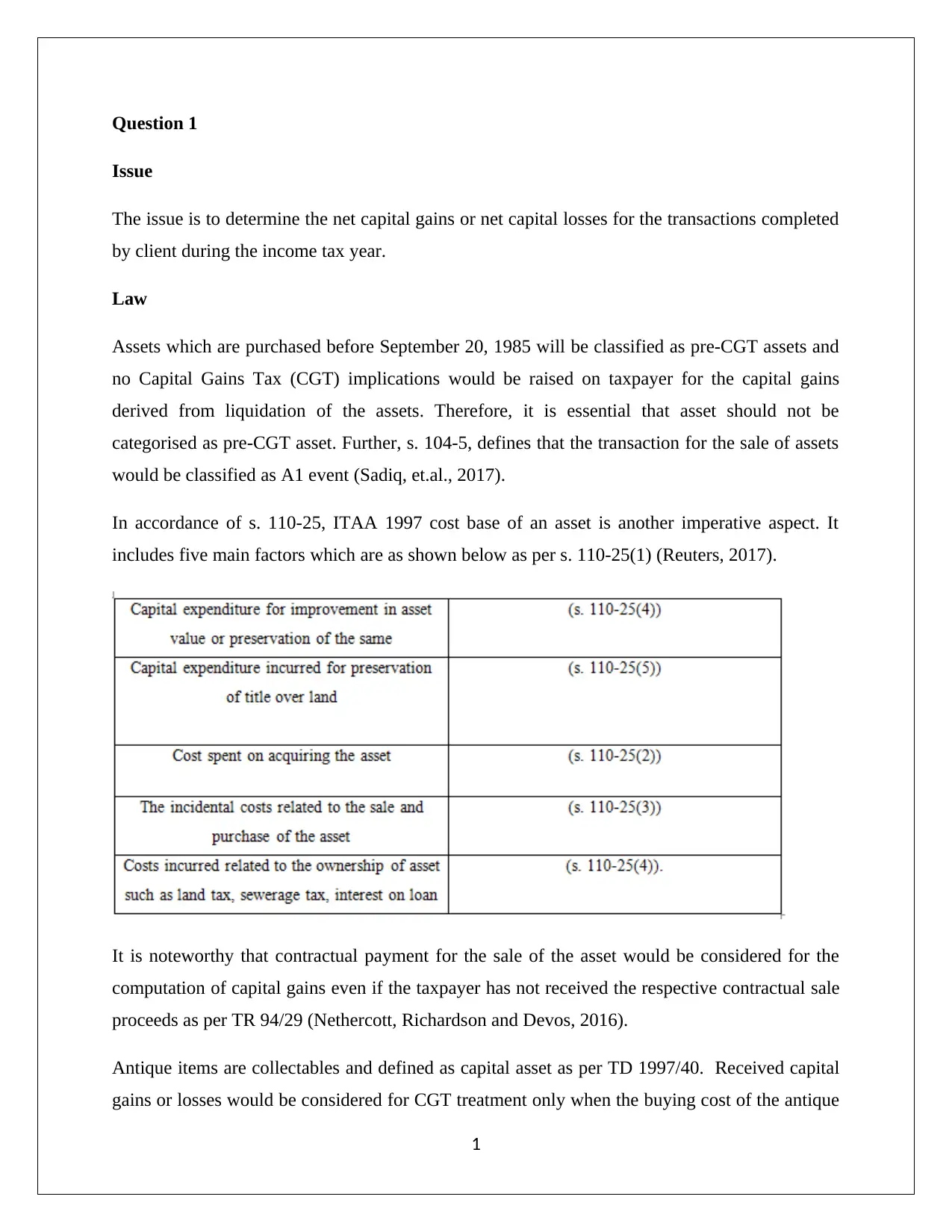

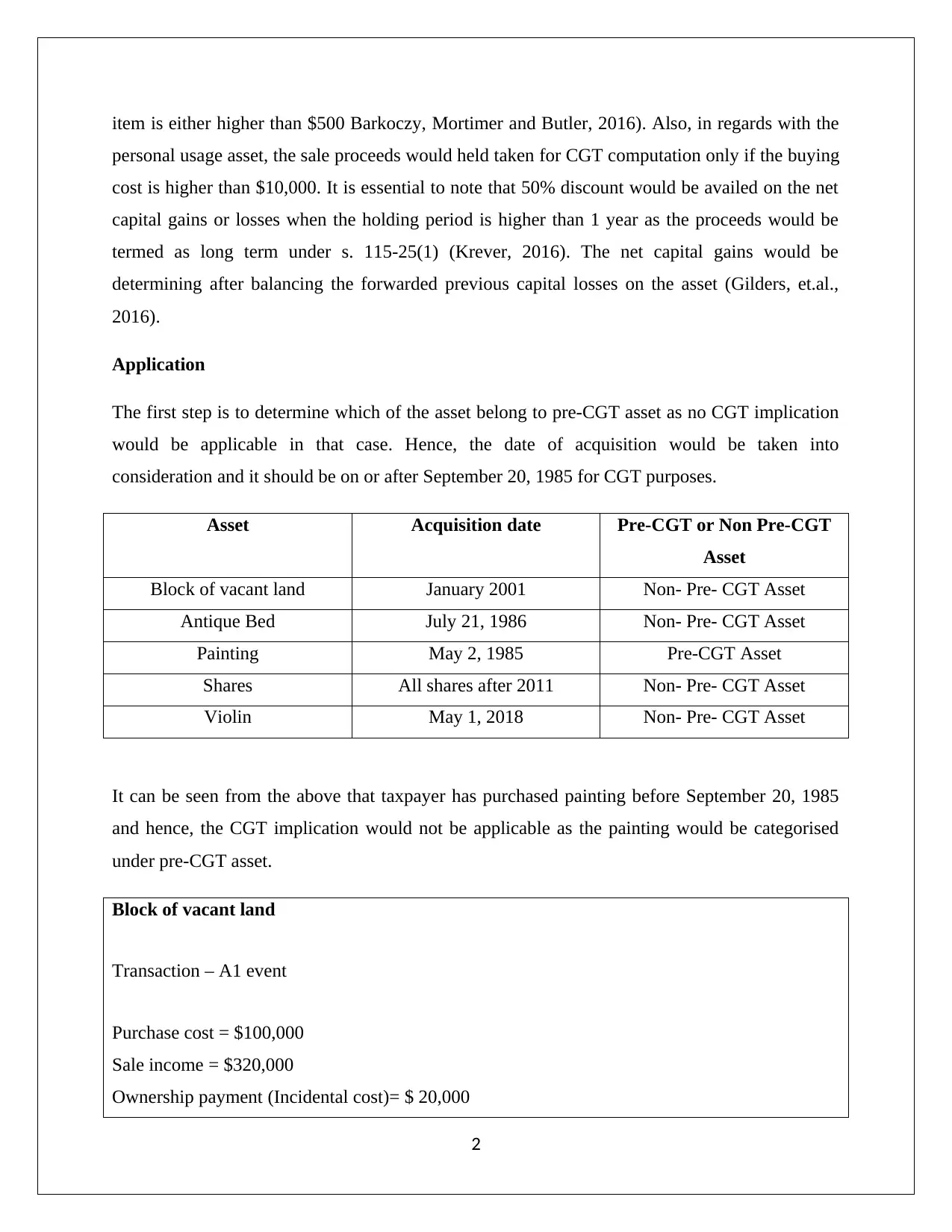

This assignment solution addresses two main issues in taxation law: calculating net capital gains or losses and commenting on fringe benefit tax (FBT) liabilities. The first part analyzes capital gains tax implications for various assets, determining whether they are pre-CGT assets and calculating capital gains based on acquisition dates, cost bases, sale incomes, and previous capital losses. The analysis includes assets like vacant land, antique beds, shares, and violins, applying relevant tax laws to determine the final capital gains subject to CGT. The second part examines FBT liabilities for an employer, Rapid Heat, who provides fringe benefits to an employee, Jasmine. It covers car fringe benefits, loan fringe benefits, and internal expense fringe benefits (electric heaters). The solution calculates the taxable value and FBT liability for each benefit, considering factors like car availability, loan interest rates, and the value of internal expenses. The solution also explores tax deductions for the employer based on the employee's actions, and the conclusion summarizes the tax liabilities for both CGT and FBT.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.