In-depth Analysis of Taxation: Capital Gains and Fringe Benefits Tax

VerifiedAdded on 2023/06/05

|13

|3388

|211

Report

AI Summary

This report provides a detailed analysis of Capital Gains Tax (CGT) and Fringe Benefits Tax (FBT) within the Australian taxation system. It addresses various scenarios involving the sale of assets such as vacant land, antiques, paintings, shares, and a violin, determining the applicability of CGT based on acquisition dates and personal use exemptions. The report includes a computation of net capital gains tax, considering proceeds, cost bases, ownership expenses, and CGT discounts. Furthermore, it examines issues related to Fringe Benefits Tax, focusing on the reimbursement of expenditures, the provision of company cars, and car parking benefits, referencing relevant sections of the Fringe Benefits Tax Assessment Act 1986 (FBTAA 1986) and case law to support its analysis. This student-contributed assignment is available on Desklib, a platform offering study tools and a wide range of academic resources for students.

Running head: TAXATION

Taxation

Name of the Student

Name of the University

Author’s Note

Taxation

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION

Table of Contents

Introduction......................................................................................................................................2

Answer 1..........................................................................................................................................2

Answer A:Block of Vacant Land................................................................................................2

Answer B: Antique Bed Sale.......................................................................................................3

Answer C: Painting......................................................................................................................3

Answer D: Shares........................................................................................................................4

Answer E: Violin.........................................................................................................................4

Answer 2..........................................................................................................................................6

Answer 2A:..................................................................................................................................6

Applications.................................................................................................................................9

Conclusion.....................................................................................................................................10

References..................................................................................................................................11

Table of Contents

Introduction......................................................................................................................................2

Answer 1..........................................................................................................................................2

Answer A:Block of Vacant Land................................................................................................2

Answer B: Antique Bed Sale.......................................................................................................3

Answer C: Painting......................................................................................................................3

Answer D: Shares........................................................................................................................4

Answer E: Violin.........................................................................................................................4

Answer 2..........................................................................................................................................6

Answer 2A:..................................................................................................................................6

Applications.................................................................................................................................9

Conclusion.....................................................................................................................................10

References..................................................................................................................................11

2TAXATION

Introduction

The theory of capital gains tax is mainly applied to assets that are attained or any other

event occurring after the year 1985. In context to this, the concept of pre- CGT as well as post-

CGT is especially used to refer as assets that are bought or the events occurring after the event

date of CGT. The capital gains tax system has been mainly applied on system of asset disposal or

any other form of particular events (Lang et al. 2018).

Answer 1

Answer A:Block of Vacant Land

If a taxpayer has attained vacant land to utilize it specially for investment or private

purpose, then the land is basically considered as the capital asset, which might be subjected to

capital gains tax when taxpayer sold this particular land. According to the statement published by

the taxation office of Australia, the vacant land is being held by taxpayer in form of capital asset

and thus might be treated equivalent to other assets mainly for the objective of the capital gains

(Ceriani, Fiorio and Gigliarano 2013). Moreover, the taxpayer is generally under compulsion of

keeping these records of date and the cost of attaining land as well as ongoing expenditure

specially interest on loan and council rates. However, this expenditure might not be claimed as

deductions of income tax but would be involved in cost base of land during estimation of capital

loss or capital gains when selling of land.

In this present scenario, the taxpayer is mainly contracted to sell vacant land block for the

amount of $320,000. The taxpayer has also reported the outgoings on council, sewerage rates,

land tax, water during the land ownership period. Moreover, the CGT event A1occurred under

the “section 104-10(1)” when the land is sold by the taxpayer. Under the “section 102-5,ITAA

Introduction

The theory of capital gains tax is mainly applied to assets that are attained or any other

event occurring after the year 1985. In context to this, the concept of pre- CGT as well as post-

CGT is especially used to refer as assets that are bought or the events occurring after the event

date of CGT. The capital gains tax system has been mainly applied on system of asset disposal or

any other form of particular events (Lang et al. 2018).

Answer 1

Answer A:Block of Vacant Land

If a taxpayer has attained vacant land to utilize it specially for investment or private

purpose, then the land is basically considered as the capital asset, which might be subjected to

capital gains tax when taxpayer sold this particular land. According to the statement published by

the taxation office of Australia, the vacant land is being held by taxpayer in form of capital asset

and thus might be treated equivalent to other assets mainly for the objective of the capital gains

(Ceriani, Fiorio and Gigliarano 2013). Moreover, the taxpayer is generally under compulsion of

keeping these records of date and the cost of attaining land as well as ongoing expenditure

specially interest on loan and council rates. However, this expenditure might not be claimed as

deductions of income tax but would be involved in cost base of land during estimation of capital

loss or capital gains when selling of land.

In this present scenario, the taxpayer is mainly contracted to sell vacant land block for the

amount of $320,000. The taxpayer has also reported the outgoings on council, sewerage rates,

land tax, water during the land ownership period. Moreover, the CGT event A1occurred under

the “section 104-10(1)” when the land is sold by the taxpayer. Under the “section 102-5,ITAA

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION

1997”, the taxpayer will be needed to involve the net addition of the capital gains in the taxable

income.

Answer B: Antique Bed Sale

The collectible theory has been given under the subdivision 108-B. Under this section

108-10(2), the collectable refers to the thing that is generally utilized by the taxpayer as well as

their associates for personal use. The section 118-10(1), ITAA 1997 states that the collectables

with buying value of about $500 will be eliminated from the CGT provision. The recent example

from the derived case recommend that this antique bed was stolen from the taxpayer’s premises.

Later it was found out that the antique bed had not been the part of list of taxpayer’s particular

matters in the insurance policy.

Apart from this, under the “section 104-25 (1)” CGT event C1 mainly occurs when the

asset is damaged or destroyed. In the present case, the compensation receipt for this stolen

antique bed led to the CGT event C1as the total compensation attained was mainly for the stolen

asset (Yagan 2015).

Answer C: Painting

The function of a CGT generally operates effectively and is only applicable if a CGT

event happens for those assets, which are bought after the date 20th September 1985. For

commonly the CGT events, there have been exceptions provided the CGT asset is attained before

20th September 2018. However, the assets that are purchased before this CGT event have been

held as excused CGT asset. It has been evident from the present situation that painting was

basically acquired on 2nd May 1985 by the taxpayer. The painting was sold by the taxpayer in the

present tax year for the amount of $125,000. Since this asset was attained before the CGT

1997”, the taxpayer will be needed to involve the net addition of the capital gains in the taxable

income.

Answer B: Antique Bed Sale

The collectible theory has been given under the subdivision 108-B. Under this section

108-10(2), the collectable refers to the thing that is generally utilized by the taxpayer as well as

their associates for personal use. The section 118-10(1), ITAA 1997 states that the collectables

with buying value of about $500 will be eliminated from the CGT provision. The recent example

from the derived case recommend that this antique bed was stolen from the taxpayer’s premises.

Later it was found out that the antique bed had not been the part of list of taxpayer’s particular

matters in the insurance policy.

Apart from this, under the “section 104-25 (1)” CGT event C1 mainly occurs when the

asset is damaged or destroyed. In the present case, the compensation receipt for this stolen

antique bed led to the CGT event C1as the total compensation attained was mainly for the stolen

asset (Yagan 2015).

Answer C: Painting

The function of a CGT generally operates effectively and is only applicable if a CGT

event happens for those assets, which are bought after the date 20th September 1985. For

commonly the CGT events, there have been exceptions provided the CGT asset is attained before

20th September 2018. However, the assets that are purchased before this CGT event have been

held as excused CGT asset. It has been evident from the present situation that painting was

basically acquired on 2nd May 1985 by the taxpayer. The painting was sold by the taxpayer in the

present tax year for the amount of $125,000. Since this asset was attained before the CGT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION

introduction before 20th September 1985, it will be taken into account as pre CGT asset which is

excluded from CGT event.

Answer D: Shares

For individual investors or taxpayers, CGT is generally applicable to profit that is

attained from units or shares when CGT event occurs specially during the selling of asset. It is

important to mention that the organization’s units or shares trust together with managed funds

are taken into account in the similar manner as other assets for the objective of capital gains tax

(Dai et al. 2015).

In the present circumstances, the taxpayer reports capital gains from units or shares that

were held in Common Ltd, Build Ltd and PHB. The taxpayers have also reported huge loss in

later events from sale of the kids learning shares. In the current situation, the taxpayers can set-

off capital loss from sale of kids learning shares against capital gains that is attained from sale of

Common Ltd, PHB, Build Ltd.

Answer E: Violin

Under the subdivision 108-C, the assets of personal use are mainly dealt. These assets

include- furniture, electrical items, boats and other household products. On the contrary, these

personal use assets do not involve land or buildings. Under the section 108-20(2), the asset of

personal use is defined as an asset which are mainly considered as non- collectable asset in

which the taxpayers hold these assets for personal enjoyment as well as utilization. On the other

hand, section 108-30 describes the ownership cost of the individual use asset. It has been stated

under the section 118-10(3) that the personal asset cost base which is lesser than the amount

$10,000 that might be ignored. It has been noted that the taxpayer is needed for keeping the asset

details that has been purchased for more than about $10,000 (Toder, Baneman and Center 2012).

introduction before 20th September 1985, it will be taken into account as pre CGT asset which is

excluded from CGT event.

Answer D: Shares

For individual investors or taxpayers, CGT is generally applicable to profit that is

attained from units or shares when CGT event occurs specially during the selling of asset. It is

important to mention that the organization’s units or shares trust together with managed funds

are taken into account in the similar manner as other assets for the objective of capital gains tax

(Dai et al. 2015).

In the present circumstances, the taxpayer reports capital gains from units or shares that

were held in Common Ltd, Build Ltd and PHB. The taxpayers have also reported huge loss in

later events from sale of the kids learning shares. In the current situation, the taxpayers can set-

off capital loss from sale of kids learning shares against capital gains that is attained from sale of

Common Ltd, PHB, Build Ltd.

Answer E: Violin

Under the subdivision 108-C, the assets of personal use are mainly dealt. These assets

include- furniture, electrical items, boats and other household products. On the contrary, these

personal use assets do not involve land or buildings. Under the section 108-20(2), the asset of

personal use is defined as an asset which are mainly considered as non- collectable asset in

which the taxpayers hold these assets for personal enjoyment as well as utilization. On the other

hand, section 108-30 describes the ownership cost of the individual use asset. It has been stated

under the section 118-10(3) that the personal asset cost base which is lesser than the amount

$10,000 that might be ignored. It has been noted that the taxpayer is needed for keeping the asset

details that has been purchased for more than about $10,000 (Toder, Baneman and Center 2012).

5TAXATION

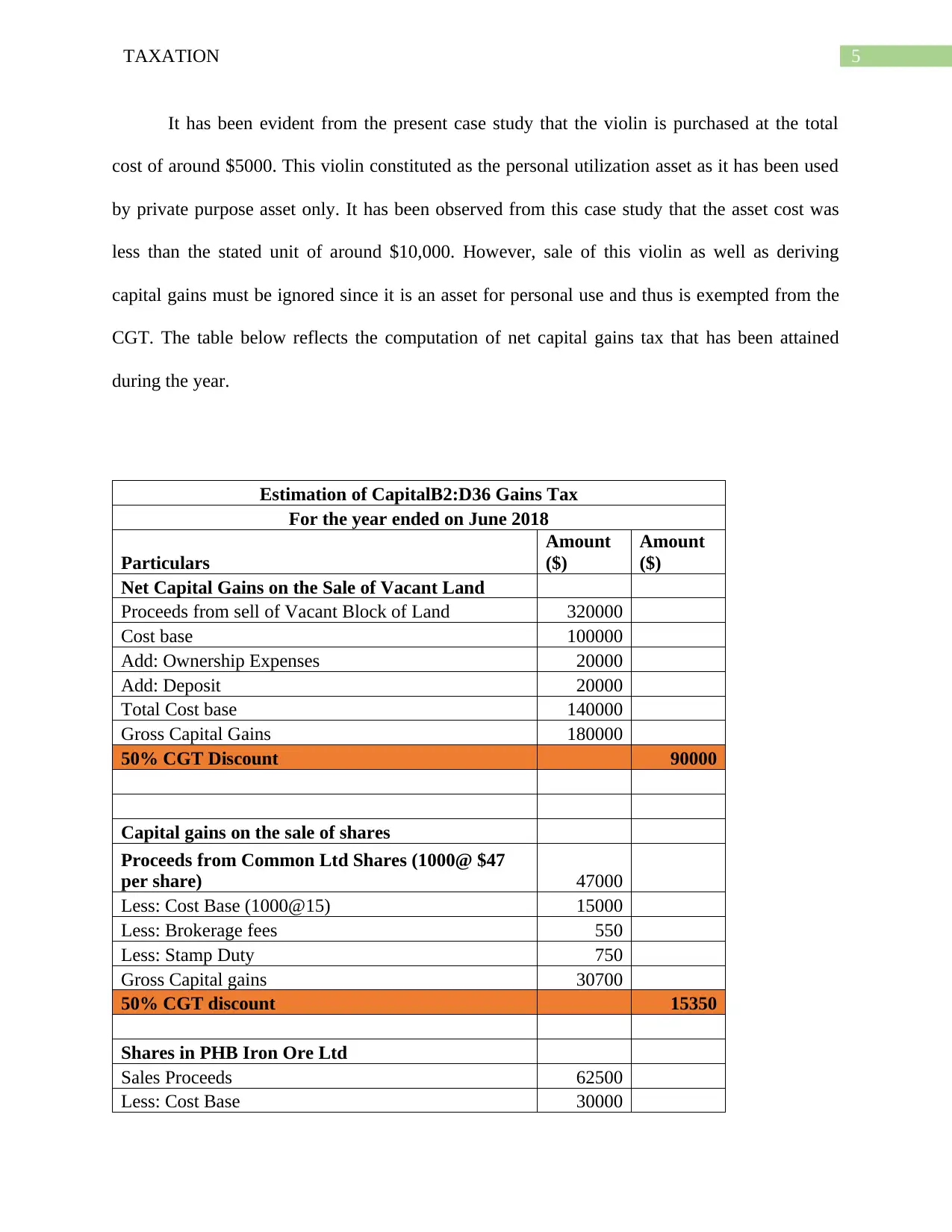

It has been evident from the present case study that the violin is purchased at the total

cost of around $5000. This violin constituted as the personal utilization asset as it has been used

by private purpose asset only. It has been observed from this case study that the asset cost was

less than the stated unit of around $10,000. However, sale of this violin as well as deriving

capital gains must be ignored since it is an asset for personal use and thus is exempted from the

CGT. The table below reflects the computation of net capital gains tax that has been attained

during the year.

Estimation of CapitalB2:D36 Gains Tax

For the year ended on June 2018

Particulars

Amount

($)

Amount

($)

Net Capital Gains on the Sale of Vacant Land

Proceeds from sell of Vacant Block of Land 320000

Cost base 100000

Add: Ownership Expenses 20000

Add: Deposit 20000

Total Cost base 140000

Gross Capital Gains 180000

50% CGT Discount 90000

Capital gains on the sale of shares

Proceeds from Common Ltd Shares (1000@ $47

per share) 47000

Less: Cost Base (1000@15) 15000

Less: Brokerage fees 550

Less: Stamp Duty 750

Gross Capital gains 30700

50% CGT discount 15350

Shares in PHB Iron Ore Ltd

Sales Proceeds 62500

Less: Cost Base 30000

It has been evident from the present case study that the violin is purchased at the total

cost of around $5000. This violin constituted as the personal utilization asset as it has been used

by private purpose asset only. It has been observed from this case study that the asset cost was

less than the stated unit of around $10,000. However, sale of this violin as well as deriving

capital gains must be ignored since it is an asset for personal use and thus is exempted from the

CGT. The table below reflects the computation of net capital gains tax that has been attained

during the year.

Estimation of CapitalB2:D36 Gains Tax

For the year ended on June 2018

Particulars

Amount

($)

Amount

($)

Net Capital Gains on the Sale of Vacant Land

Proceeds from sell of Vacant Block of Land 320000

Cost base 100000

Add: Ownership Expenses 20000

Add: Deposit 20000

Total Cost base 140000

Gross Capital Gains 180000

50% CGT Discount 90000

Capital gains on the sale of shares

Proceeds from Common Ltd Shares (1000@ $47

per share) 47000

Less: Cost Base (1000@15) 15000

Less: Brokerage fees 550

Less: Stamp Duty 750

Gross Capital gains 30700

50% CGT discount 15350

Shares in PHB Iron Ore Ltd

Sales Proceeds 62500

Less: Cost Base 30000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION

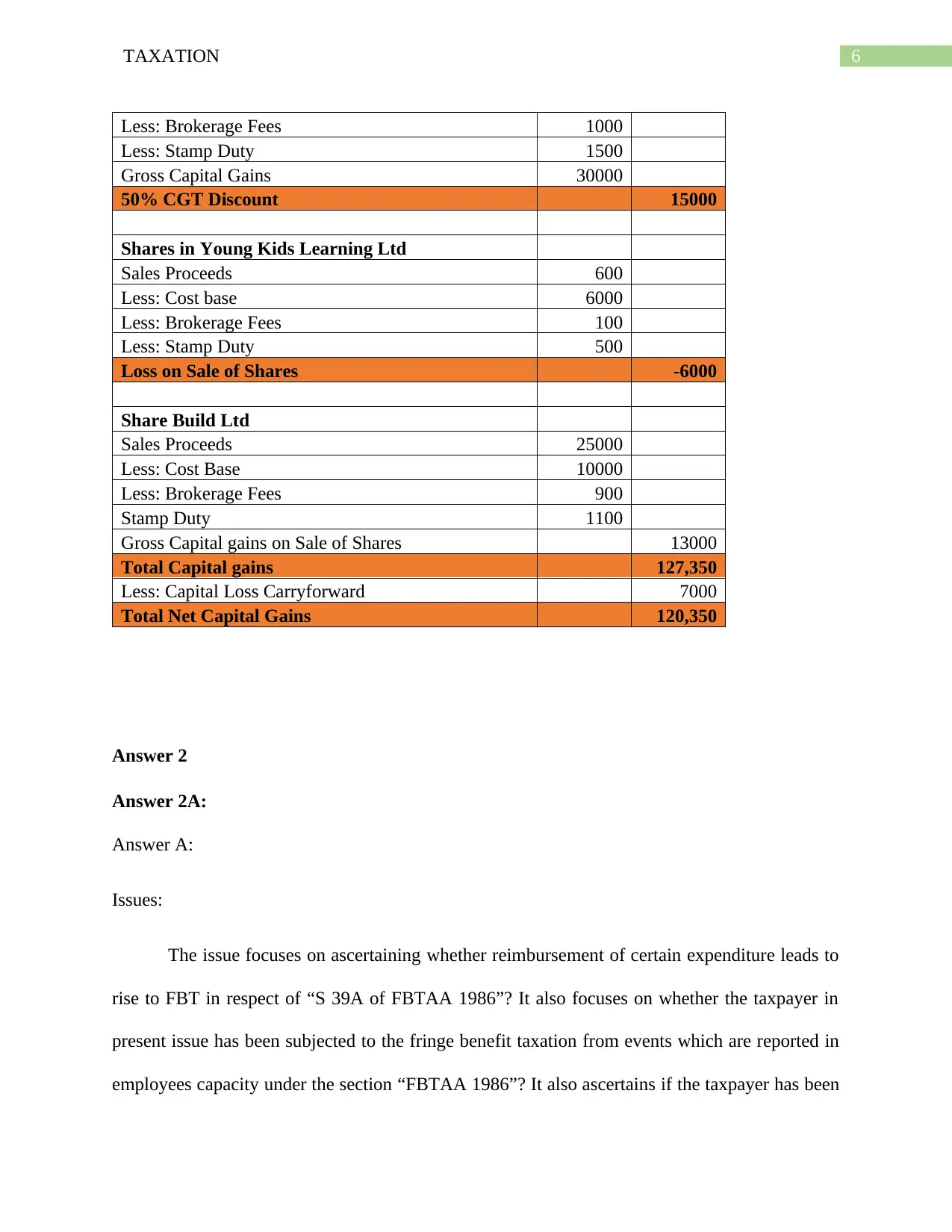

Less: Brokerage Fees 1000

Less: Stamp Duty 1500

Gross Capital Gains 30000

50% CGT Discount 15000

Shares in Young Kids Learning Ltd

Sales Proceeds 600

Less: Cost base 6000

Less: Brokerage Fees 100

Less: Stamp Duty 500

Loss on Sale of Shares -6000

Share Build Ltd

Sales Proceeds 25000

Less: Cost Base 10000

Less: Brokerage Fees 900

Stamp Duty 1100

Gross Capital gains on Sale of Shares 13000

Total Capital gains 127,350

Less: Capital Loss Carryforward 7000

Total Net Capital Gains 120,350

Answer 2

Answer 2A:

Answer A:

Issues:

The issue focuses on ascertaining whether reimbursement of certain expenditure leads to

rise to FBT in respect of “S 39A of FBTAA 1986”? It also focuses on whether the taxpayer in

present issue has been subjected to the fringe benefit taxation from events which are reported in

employees capacity under the section “FBTAA 1986”? It also ascertains if the taxpayer has been

Less: Brokerage Fees 1000

Less: Stamp Duty 1500

Gross Capital Gains 30000

50% CGT Discount 15000

Shares in Young Kids Learning Ltd

Sales Proceeds 600

Less: Cost base 6000

Less: Brokerage Fees 100

Less: Stamp Duty 500

Loss on Sale of Shares -6000

Share Build Ltd

Sales Proceeds 25000

Less: Cost Base 10000

Less: Brokerage Fees 900

Stamp Duty 1100

Gross Capital gains on Sale of Shares 13000

Total Capital gains 127,350

Less: Capital Loss Carryforward 7000

Total Net Capital Gains 120,350

Answer 2

Answer 2A:

Answer A:

Issues:

The issue focuses on ascertaining whether reimbursement of certain expenditure leads to

rise to FBT in respect of “S 39A of FBTAA 1986”? It also focuses on whether the taxpayer in

present issue has been subjected to the fringe benefit taxation from events which are reported in

employees capacity under the section “FBTAA 1986”? It also ascertains if the taxpayer has been

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION

accountable in paying FBT for car given with respect of employment? In addition to this, the

issue also provides the description relating to loan fringe benefits that has been provided to

employees under the “sub division A of FBTAA 1986”

Laws:

In respect of the “subsection ID of FBTAA 1986”, fringe benefits of an employer mainly

depicts assessable sum for a year commencing from Ist April 2000. The fringe benefits as well as

word benefit mainly holds better meanings for the objective of FBT. These fringe benefits

consists of privileges, services and the rights. According to the definition of FBT legislation, an

employer usually gives fringe benefit to their employees in respect of employment constitute

benefit. The fringe benefits is given only to those individuals who are employed as an employee

in an enterprise. An employee can be the person that ranges from former employee to future

employee. Moreover, the employee is an individual that might be entitled of receiving salary or

benefits in lieu of wages. An employer of the organization can be responsible for fringe benefit

tax provided that employer makes payment to their employee or the office holder that are mainly

subjected to any kind of withholding obligations or provides benefits in respect of payments. An

employer is also needed to pay fringe benefit tax despite certain condition if they are responsible

to pay other taxes specially the income tax (Shiftan, Albert and Keinan 2012).

Under the “section 7, FBTAA 1986” a car fringe benefit involves the benefit, which

occurs particularly under such condition where an employer uses the car mainly for the private

purpose (Scott, Currie and Tivendale 2012). The car that the employer generally holds is only

available for the usage of an employee. An employer usually makes a car available for personal

use of an employee when it is mainly used for the employers private purpose. In addition to this,

fringe benefit of a car arises only when it is available by an employee for private purpose

accountable in paying FBT for car given with respect of employment? In addition to this, the

issue also provides the description relating to loan fringe benefits that has been provided to

employees under the “sub division A of FBTAA 1986”

Laws:

In respect of the “subsection ID of FBTAA 1986”, fringe benefits of an employer mainly

depicts assessable sum for a year commencing from Ist April 2000. The fringe benefits as well as

word benefit mainly holds better meanings for the objective of FBT. These fringe benefits

consists of privileges, services and the rights. According to the definition of FBT legislation, an

employer usually gives fringe benefit to their employees in respect of employment constitute

benefit. The fringe benefits is given only to those individuals who are employed as an employee

in an enterprise. An employee can be the person that ranges from former employee to future

employee. Moreover, the employee is an individual that might be entitled of receiving salary or

benefits in lieu of wages. An employer of the organization can be responsible for fringe benefit

tax provided that employer makes payment to their employee or the office holder that are mainly

subjected to any kind of withholding obligations or provides benefits in respect of payments. An

employer is also needed to pay fringe benefit tax despite certain condition if they are responsible

to pay other taxes specially the income tax (Shiftan, Albert and Keinan 2012).

Under the “section 7, FBTAA 1986” a car fringe benefit involves the benefit, which

occurs particularly under such condition where an employer uses the car mainly for the private

purpose (Scott, Currie and Tivendale 2012). The car that the employer generally holds is only

available for the usage of an employee. An employer usually makes a car available for personal

use of an employee when it is mainly used for the employers private purpose. In addition to this,

fringe benefit of a car arises only when it is available by an employee for private purpose

8TAXATION

specially during when it is not within premise of the employer or garaged at the employee’s

residence.

As per the “FBTAA 1986”, the common rule is that travelling to or from the workplace

might be considered as private usage of this car. The car might be taken into account as private

utilization of an employee when this car goes in workshop for maintenance or routine services.

The taxation commission in the “Lunney v FCT (1958)”gave a description that travelling to the

workplace from the residence gives rise to personal usage of car for an employee (Barry and

Caron 2015).

The “ Division 5 of the FBTAA 1986” refers to a description in relation to the

expenditure payment fringe benefit, which can originate in certain situation if an employer

makes any kind of reimbursement for that expenditure incurred by an employee. On the other

hand, the fringe benefit for expenses occurs when an employee pays to the third parties due to

satisfaction from expenditure occurred by an employee. In any of the above mentioned cases, the

expense can be outgoings of business or private outgoings or the combination of these two cases.

The expense fringe benefit chargeable value basically represents those value, which is repaid by

an employer. In addition to this, in house expenditure payment fringe benefit generally occurs

when that expenditure is attained by an employee after reimbursement from an employer.

The fringe benefit of car parking under the “division10A of the FBTAA 1986” occurs for

all employee when an employer gives an employee with enough space for car parking, which is

utilized by an employee. The “division 10A FBTAA 1986” describes that the fringe benefit of

car parking occurs when the following conditions are given below-

specially during when it is not within premise of the employer or garaged at the employee’s

residence.

As per the “FBTAA 1986”, the common rule is that travelling to or from the workplace

might be considered as private usage of this car. The car might be taken into account as private

utilization of an employee when this car goes in workshop for maintenance or routine services.

The taxation commission in the “Lunney v FCT (1958)”gave a description that travelling to the

workplace from the residence gives rise to personal usage of car for an employee (Barry and

Caron 2015).

The “ Division 5 of the FBTAA 1986” refers to a description in relation to the

expenditure payment fringe benefit, which can originate in certain situation if an employer

makes any kind of reimbursement for that expenditure incurred by an employee. On the other

hand, the fringe benefit for expenses occurs when an employee pays to the third parties due to

satisfaction from expenditure occurred by an employee. In any of the above mentioned cases, the

expense can be outgoings of business or private outgoings or the combination of these two cases.

The expense fringe benefit chargeable value basically represents those value, which is repaid by

an employer. In addition to this, in house expenditure payment fringe benefit generally occurs

when that expenditure is attained by an employee after reimbursement from an employer.

The fringe benefit of car parking under the “division10A of the FBTAA 1986” occurs for

all employee when an employer gives an employee with enough space for car parking, which is

utilized by an employee. The “division 10A FBTAA 1986” describes that the fringe benefit of

car parking occurs when the following conditions are given below-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION

The parking of car is done inside the area of one kilometer where commercial parking

facilities is available and also charge fees for parking the car for the whole day.

The car parking is done at premises where an employer leases or owns

The car is given relating to employment of an employee

The parking of car is done for four hours during a specific day

Under the “division 4 of the FTBAA 1986” explains about the debt waiver and loan

fringe benefit. The fringe benefit for loan occurs when an employer gives loan to an

employee and thereby charges lower interest rate amount over the FBT year. It can be

mentioned from the case study that low interest rate is the amount that is lower than statutory

interest rate (Shiftan, Albert and Keinan 2012).

Applications

The present study reflects on the description of Jasmine as an employee of the Rapid

Heat Pvt Ltd selling electric heaters. Being a part of employment, Jasmine needed to travel more

owing to the purpose of work. In such circumstances, rapid gave Jasmine with a car for the

purpose of work. Jasmine was also allowed to use this car mainly for the private purpose. In this

condition, “section 7 FTBAA 1986” can be applied generally for Rapid Heat as an employer

gave this car to Jasmine for personal use and also for job purpose during the employment course.

The judgment done by “Lunney v FCT (1958)” highlights that the car that is used by Jasmine for

private purpose indicates the fringe benefit. However, the Rapid Heat Pvt Ltd would have the

liability for fringe benefit tax in order to give car to Jasmine (Marr, Huang and Friedman 2013).

The later segment of the case study highlights that Jasmine had used the car for travelling

10,000 kilometer and this created expenditure for around $550 on small repairs, which is repaid

by Rapid Heat. It has been observed that the employer had repaid Jasmine with the total amount

The parking of car is done inside the area of one kilometer where commercial parking

facilities is available and also charge fees for parking the car for the whole day.

The car parking is done at premises where an employer leases or owns

The car is given relating to employment of an employee

The parking of car is done for four hours during a specific day

Under the “division 4 of the FTBAA 1986” explains about the debt waiver and loan

fringe benefit. The fringe benefit for loan occurs when an employer gives loan to an

employee and thereby charges lower interest rate amount over the FBT year. It can be

mentioned from the case study that low interest rate is the amount that is lower than statutory

interest rate (Shiftan, Albert and Keinan 2012).

Applications

The present study reflects on the description of Jasmine as an employee of the Rapid

Heat Pvt Ltd selling electric heaters. Being a part of employment, Jasmine needed to travel more

owing to the purpose of work. In such circumstances, rapid gave Jasmine with a car for the

purpose of work. Jasmine was also allowed to use this car mainly for the private purpose. In this

condition, “section 7 FTBAA 1986” can be applied generally for Rapid Heat as an employer

gave this car to Jasmine for personal use and also for job purpose during the employment course.

The judgment done by “Lunney v FCT (1958)” highlights that the car that is used by Jasmine for

private purpose indicates the fringe benefit. However, the Rapid Heat Pvt Ltd would have the

liability for fringe benefit tax in order to give car to Jasmine (Marr, Huang and Friedman 2013).

The later segment of the case study highlights that Jasmine had used the car for travelling

10,000 kilometer and this created expenditure for around $550 on small repairs, which is repaid

by Rapid Heat. It has been observed that the employer had repaid Jasmine with the total amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION

of the repair expenditure, which was incurred for this small repair. Under the “division 5 of the

FBTAA 1986”, the fringe benefit of expenditure payment had arose for the Rapid Heat Pvt Ltd

in such condition (Ahmad, Etp and Bujan 2013). The main reason behind this is that an employer

Rapid Heat has disbursed an employee with expense repayment that Jasmine obtained for small

car repairs. Thus, the value of fringe benefit of such expenditure for Rapid Heat signifies the

value that can be repaid to Jasmine.

The events that took place later reflects that Jasmine had not used a car during her

interstate, parked her car at airport and parking of car at workstation for objective of planned

repair (Van Ommeren and Wentink 2012). Even though a car was given by Rapid Heat to

Jasmine with respect to employment but parking of car was not inside one kilometer. The present

study describes that Jasmine has been given loan of about $500,000 by the Rapid Heat Pvt Ltd at

the yearly interest rate of around 4.25%. However, in these circumstances fringe benefit for loan

occurred for the Rapid Heat Pvt Ltd as the loan has been given with respect of employment.

Answer 2B

Under the “section 8-1 of the ITAA 1997”, a taxpayer is allowed to claim for allowable

deductions specially under common provision when expenditure has incurred to gain taxable

income. Likewise, if Jasmine has used the total amount of around $50,000 for buying shares

herself despite providing loan to her husband without any interest in hypothetical condition, then

Jasmine can be permitted to claim allowable deductions for interest on the loan amount. Thus,

Jasmine has lent the total loan amount to her husband based on interest. Hence, no deductions

can be allowed under the common provision of “ section 8-1 ITAA 1997”.

of the repair expenditure, which was incurred for this small repair. Under the “division 5 of the

FBTAA 1986”, the fringe benefit of expenditure payment had arose for the Rapid Heat Pvt Ltd

in such condition (Ahmad, Etp and Bujan 2013). The main reason behind this is that an employer

Rapid Heat has disbursed an employee with expense repayment that Jasmine obtained for small

car repairs. Thus, the value of fringe benefit of such expenditure for Rapid Heat signifies the

value that can be repaid to Jasmine.

The events that took place later reflects that Jasmine had not used a car during her

interstate, parked her car at airport and parking of car at workstation for objective of planned

repair (Van Ommeren and Wentink 2012). Even though a car was given by Rapid Heat to

Jasmine with respect to employment but parking of car was not inside one kilometer. The present

study describes that Jasmine has been given loan of about $500,000 by the Rapid Heat Pvt Ltd at

the yearly interest rate of around 4.25%. However, in these circumstances fringe benefit for loan

occurred for the Rapid Heat Pvt Ltd as the loan has been given with respect of employment.

Answer 2B

Under the “section 8-1 of the ITAA 1997”, a taxpayer is allowed to claim for allowable

deductions specially under common provision when expenditure has incurred to gain taxable

income. Likewise, if Jasmine has used the total amount of around $50,000 for buying shares

herself despite providing loan to her husband without any interest in hypothetical condition, then

Jasmine can be permitted to claim allowable deductions for interest on the loan amount. Thus,

Jasmine has lent the total loan amount to her husband based on interest. Hence, no deductions

can be allowed under the common provision of “ section 8-1 ITAA 1997”.

11TAXATION

Conclusion

It has been evident from the above discussion that Rapid Heat Pvt Ltd might be held

accountable for fringe benefit taxation for loan during the FBT year. Thus, Rapid Heat Pvt Ltd

might claim allowable deduction for similar causes as the expenditure had been incurred during

course of an employees engagement

References

Ahmad, R., Etp, Y. and Bujan, S., 2013. Relationship between Types of Benefit (leave, loan and

retirement plan) and Employees’ Retention. International Journal of Education Research, 1(8).

Barry, J.M. and Caron, P.L., 2015. Tax regulation, transportation innovation, and the sharing

economy. U. Chi. L. Rev. Dialogue, 82, p.69.

Becker, J., Reimer, E. and Rust, A., 2015. Klaus Vogel on Double Taxation Conventions. Kluwer

Law International.

Ceriani, L., Fiorio, C.V. and Gigliarano, C., 2013. The importance of choosing the data set for

tax-benefit analysis (No. EM5/13). EUROMOD Working Paper.

Dai, M., Liu, H., Yang, C. and Zhong, Y., 2015. Optimal tax timing with asymmetric

long-term/short-term capital gains tax. The Review of Financial Studies, 28(9), pp.2687-2721.

Lang, M., Pistone, P., Schuch, J. and Staringer, C. eds., 2018. Introduction to European tax law

on direct taxation. Linde Verlag GmbH.

Marr, C., Huang, C.C. and Friedman, J., 2013. Tax expenditure reform: an essential ingredient of

needed deficit reduction. Center on Budget and Policy Priorities.

Conclusion

It has been evident from the above discussion that Rapid Heat Pvt Ltd might be held

accountable for fringe benefit taxation for loan during the FBT year. Thus, Rapid Heat Pvt Ltd

might claim allowable deduction for similar causes as the expenditure had been incurred during

course of an employees engagement

References

Ahmad, R., Etp, Y. and Bujan, S., 2013. Relationship between Types of Benefit (leave, loan and

retirement plan) and Employees’ Retention. International Journal of Education Research, 1(8).

Barry, J.M. and Caron, P.L., 2015. Tax regulation, transportation innovation, and the sharing

economy. U. Chi. L. Rev. Dialogue, 82, p.69.

Becker, J., Reimer, E. and Rust, A., 2015. Klaus Vogel on Double Taxation Conventions. Kluwer

Law International.

Ceriani, L., Fiorio, C.V. and Gigliarano, C., 2013. The importance of choosing the data set for

tax-benefit analysis (No. EM5/13). EUROMOD Working Paper.

Dai, M., Liu, H., Yang, C. and Zhong, Y., 2015. Optimal tax timing with asymmetric

long-term/short-term capital gains tax. The Review of Financial Studies, 28(9), pp.2687-2721.

Lang, M., Pistone, P., Schuch, J. and Staringer, C. eds., 2018. Introduction to European tax law

on direct taxation. Linde Verlag GmbH.

Marr, C., Huang, C.C. and Friedman, J., 2013. Tax expenditure reform: an essential ingredient of

needed deficit reduction. Center on Budget and Policy Priorities.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.