Taxation Law Assignment: Capital Gains, Income, and Interest, HI6028

VerifiedAdded on 2022/11/23

|8

|2557

|396

Homework Assignment

AI Summary

This document presents a comprehensive solution to a taxation law assignment, addressing three key questions. The first question focuses on capital gains tax (CGT), analyzing the tax implications of selling various assets, including an antique impression, a historical sculpture, antique jewelry, and a picture. The analysis considers pre-CGT assets, collectibles, and personal use assets, applying relevant legislative provisions. The second question examines income from personal exertion, specifically the taxability of income earned by an economist who wrote a book, assigned copyright, and sold manuscripts and interview scripts, referencing relevant case law like Eisner v Macomber and Brent v FC of T. The third question addresses the tax treatment of interest payments received from a loan agreement, clarifying whether the interest constitutes ordinary income and should be assessed under the relevant legislation, citing Sec 6-5, ITA Act 1997.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:...................................................................................................2

Answer to question 2:...................................................................................................3

Answer to question 3:...................................................................................................4

References:..................................................................................................................7

Table of Contents

Answer to question 1:...................................................................................................2

Answer to question 2:...................................................................................................3

Answer to question 3:...................................................................................................4

References:..................................................................................................................7

2TAXATION LAW

Answer to question 1:

Capital gains from Antique impression:

The regime of capital gains tax is integrated into the regimes of income tax.

The capital gains tax cannot be viewed as the separate tax. The legislative provision

of “s102-5, ITAA 1997” explains that an individual net capital gains that is made in

the income year is considered for taxable purpose (Richardson and Lanis 2017).

Most notably the capital loss should be offset against the capital gains that are not

held deductible. Capital gains is only allowed to be imposed on the assets that are

purchased on or after the 20th sept 1985.

Helen in an effort to fund the retirement fund sold the antique impression that

she bought in February 1985. The disposal of antique painting led to capital gains for

Helen. But it must be noted that the painting is the pre-CGT asset as it is bought

before 20/9/2018. Similarly, the capital gains that is made is excluded from the CGT

regime.

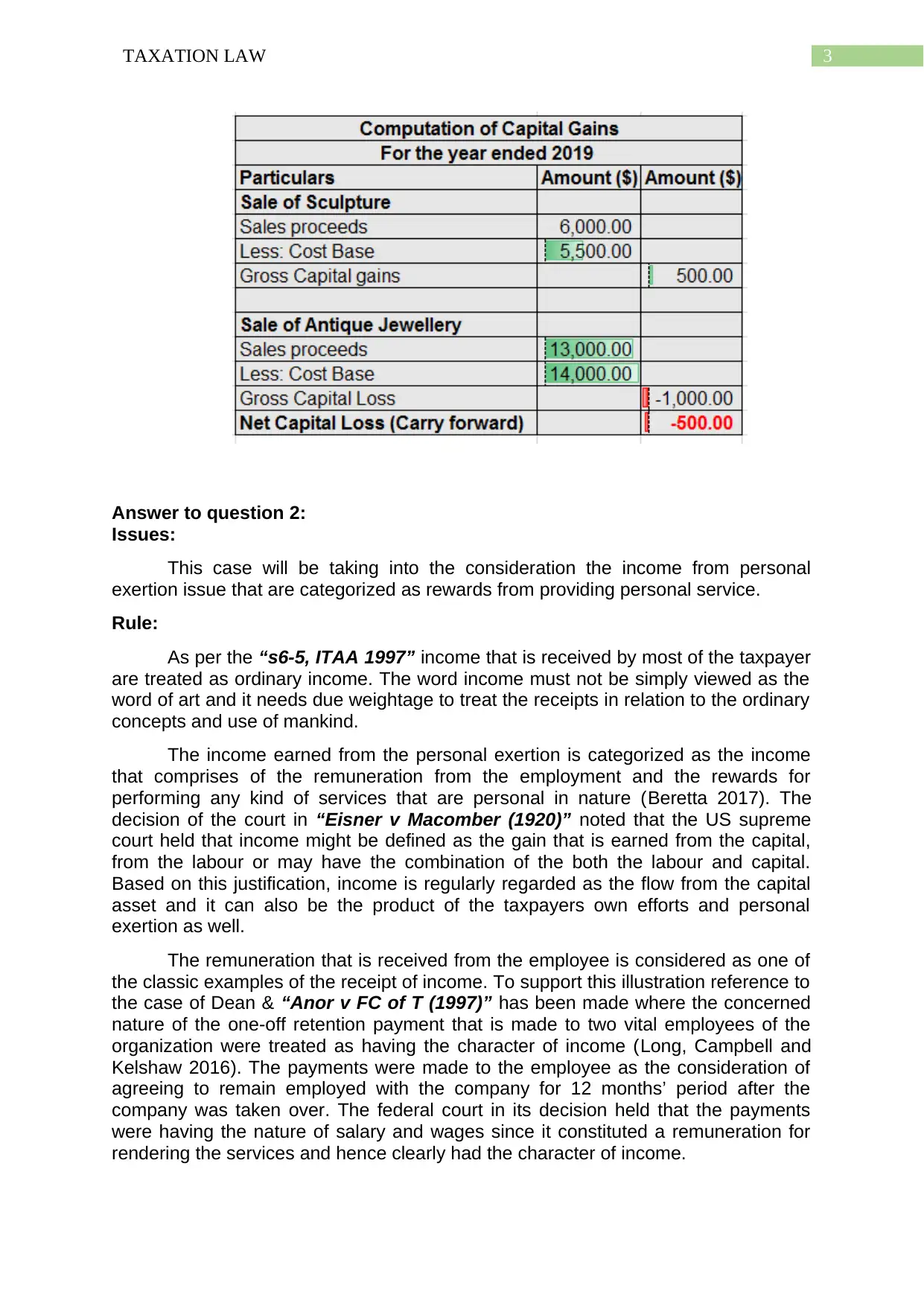

Capital gains from historical sculpture:

A CGT event A1 incurs upon disposing the CGT asset under “s104-10(1)”.

Referring “s108-10(2)” the artwork, jewellery, postage stamp, antiques is regarded

as collectibles. This is generally under the ownership of taxpayer for private

enjoyment purpose (Cunningham and Engelhardt 2018). Helen in a bid to start her

new fashion designer business sold the historical sculpture. The sales raise $6000

for Helen while the purchase value was $5,500. It can be said that CGT event A1

happened when Helen sold the sculpture. The capital gains that is made from

sculpture is taxable under legislative provision of “s102-5, ITAA 1997”.

Capital gains from jewellery:

Apart from defining the collectables it is necessary that some important rules

are applied on the collectables (Barkoczy and Wilkinson 2019). the capital gains and

capital loss must be ignored when the first element of the cost base relating to

collectables is not met and the cost of asset is below $500. Similarly, the

quarantining rule also makes it clear for the taxpayer that the capital loss from the

collectable must be used to offset the capital gains from collectables.

The antique jewellery purchased in October 1987 by paying a sum of $14,000

only fetched Helen $13,000 when it was sold. The jewellery should be treated as

collectables under “s-108-10(2)”. The quarantining rule must be applied by Helen

since the antique jewellery has led to loss for Helen. She is here recommended that

capital loss can be reduced from the capital gains made from historical sculpture and

the quarantining rules must be applied by Helen.

Capital gains from picture:

Accordingly, in the “s-108-20” personal use assets involve the TV at home,

bicycle, mobile phone etc. are usually kept by taxpayer for their own enjoyment and

usage. The capital loss or gains must be ignored if the asset cost is less than $10k

(Braithwaite 2019). Helen sold the picture that was purchased for $470. The sale of

picture resulted in capital gains. However, Helen under the special rules relating to

the personal use asset should ignore the capital gains made from picture because it

is personal use asset and the cost base of picture is lower than 10k.

Answer to question 1:

Capital gains from Antique impression:

The regime of capital gains tax is integrated into the regimes of income tax.

The capital gains tax cannot be viewed as the separate tax. The legislative provision

of “s102-5, ITAA 1997” explains that an individual net capital gains that is made in

the income year is considered for taxable purpose (Richardson and Lanis 2017).

Most notably the capital loss should be offset against the capital gains that are not

held deductible. Capital gains is only allowed to be imposed on the assets that are

purchased on or after the 20th sept 1985.

Helen in an effort to fund the retirement fund sold the antique impression that

she bought in February 1985. The disposal of antique painting led to capital gains for

Helen. But it must be noted that the painting is the pre-CGT asset as it is bought

before 20/9/2018. Similarly, the capital gains that is made is excluded from the CGT

regime.

Capital gains from historical sculpture:

A CGT event A1 incurs upon disposing the CGT asset under “s104-10(1)”.

Referring “s108-10(2)” the artwork, jewellery, postage stamp, antiques is regarded

as collectibles. This is generally under the ownership of taxpayer for private

enjoyment purpose (Cunningham and Engelhardt 2018). Helen in a bid to start her

new fashion designer business sold the historical sculpture. The sales raise $6000

for Helen while the purchase value was $5,500. It can be said that CGT event A1

happened when Helen sold the sculpture. The capital gains that is made from

sculpture is taxable under legislative provision of “s102-5, ITAA 1997”.

Capital gains from jewellery:

Apart from defining the collectables it is necessary that some important rules

are applied on the collectables (Barkoczy and Wilkinson 2019). the capital gains and

capital loss must be ignored when the first element of the cost base relating to

collectables is not met and the cost of asset is below $500. Similarly, the

quarantining rule also makes it clear for the taxpayer that the capital loss from the

collectable must be used to offset the capital gains from collectables.

The antique jewellery purchased in October 1987 by paying a sum of $14,000

only fetched Helen $13,000 when it was sold. The jewellery should be treated as

collectables under “s-108-10(2)”. The quarantining rule must be applied by Helen

since the antique jewellery has led to loss for Helen. She is here recommended that

capital loss can be reduced from the capital gains made from historical sculpture and

the quarantining rules must be applied by Helen.

Capital gains from picture:

Accordingly, in the “s-108-20” personal use assets involve the TV at home,

bicycle, mobile phone etc. are usually kept by taxpayer for their own enjoyment and

usage. The capital loss or gains must be ignored if the asset cost is less than $10k

(Braithwaite 2019). Helen sold the picture that was purchased for $470. The sale of

picture resulted in capital gains. However, Helen under the special rules relating to

the personal use asset should ignore the capital gains made from picture because it

is personal use asset and the cost base of picture is lower than 10k.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer to question 2:

Issues:

This case will be taking into the consideration the income from personal

exertion issue that are categorized as rewards from providing personal service.

Rule:

As per the “s6-5, ITAA 1997” income that is received by most of the taxpayer

are treated as ordinary income. The word income must not be simply viewed as the

word of art and it needs due weightage to treat the receipts in relation to the ordinary

concepts and use of mankind.

The income earned from the personal exertion is categorized as the income

that comprises of the remuneration from the employment and the rewards for

performing any kind of services that are personal in nature (Beretta 2017). The

decision of the court in “Eisner v Macomber (1920)” noted that the US supreme

court held that income might be defined as the gain that is earned from the capital,

from the labour or may have the combination of the both the labour and capital.

Based on this justification, income is regularly regarded as the flow from the capital

asset and it can also be the product of the taxpayers own efforts and personal

exertion as well.

The remuneration that is received from the employee is considered as one of

the classic examples of the receipt of income. To support this illustration reference to

the case of Dean & “Anor v FC of T (1997)” has been made where the concerned

nature of the one-off retention payment that is made to two vital employees of the

organization were treated as having the character of income (Long, Campbell and

Kelshaw 2016). The payments were made to the employee as the consideration of

agreeing to remain employed with the company for 12 months’ period after the

company was taken over. The federal court in its decision held that the payments

were having the nature of salary and wages since it constituted a remuneration for

rendering the services and hence clearly had the character of income.

Answer to question 2:

Issues:

This case will be taking into the consideration the income from personal

exertion issue that are categorized as rewards from providing personal service.

Rule:

As per the “s6-5, ITAA 1997” income that is received by most of the taxpayer

are treated as ordinary income. The word income must not be simply viewed as the

word of art and it needs due weightage to treat the receipts in relation to the ordinary

concepts and use of mankind.

The income earned from the personal exertion is categorized as the income

that comprises of the remuneration from the employment and the rewards for

performing any kind of services that are personal in nature (Beretta 2017). The

decision of the court in “Eisner v Macomber (1920)” noted that the US supreme

court held that income might be defined as the gain that is earned from the capital,

from the labour or may have the combination of the both the labour and capital.

Based on this justification, income is regularly regarded as the flow from the capital

asset and it can also be the product of the taxpayers own efforts and personal

exertion as well.

The remuneration that is received from the employee is considered as one of

the classic examples of the receipt of income. To support this illustration reference to

the case of Dean & “Anor v FC of T (1997)” has been made where the concerned

nature of the one-off retention payment that is made to two vital employees of the

organization were treated as having the character of income (Long, Campbell and

Kelshaw 2016). The payments were made to the employee as the consideration of

agreeing to remain employed with the company for 12 months’ period after the

company was taken over. The federal court in its decision held that the payments

were having the nature of salary and wages since it constituted a remuneration for

rendering the services and hence clearly had the character of income.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

The fact that the receipt of reward is a product of service rendered is also

referred in the case of “Brent v FC of T (1971)” that were having the nature of

income. The case comprised of the payments that were received by the wife of the

convicted train robber for allowing the exclusive publication of her story to the media

company (Kennedy et al. 2017). The court of law in its verdict stated that the amount

that were received by the taxpayer for granting the right was considered as having

the character of income and purely constituted the product of personal service

income.

Application:

On the basis of the above stated rules, the gathered circumstances of

Barbara can be considered where she is by profession an economist. She is majorly

engaged in the research work but she was once offered a sum of $13,000 for

scripting a book on economics. Persuaded by the publishers offer of writing the book

she simply began to use her effort and knowledge. Barbara successfully wrote down

the book named Principles of Economics. She was duly paid the amount of $13,000.

By referring to the case of “Brent v FC of T (1971)” it can be explained that rewards

that was received by Barbara was simply for the services rendered (Guo and Krause

2017). The amount will be considered as having the nature of income and the

concerned payment is related to making herself available for rendering the service.

Barbara in later stages is found to be assigning the copyright of the books that

was written by her on economics for its exclusive publications. The payment that she

received for assigning the copyright of her literary works stood $13,400. Citing the

case of “Anor v FC of T (1997)” the amount will be considered as income for the

services rendered and it is clearly having the nature of income which should be

taxable under the ordinary meaning of “s6-5, ITAA 1997”.

As the case unfolds, Barbara also sold the manuscripts of the books and the

interview scripts to the library. She was given a sum of $4,350 and $3,200

separately.

Citing the case of “Eisner v Macomber (1920)” the amount will be

considered as income and should be defined as gain that is derived from the capital

and labor as well. On the basis of this justification the payment of $4,350 and $3,200

separately should be considered as the flow from a capital asset and it is the product

of Barbara’s personal effort and exertion.

In the turn of events if the books are simply written by Barbara during the

leisure time and she decides to sell it later in exchange of payment, then the amount

that will be received will be considered as the product of Barbara’s personal exertion

and efforts. The amount will be considered as gain that will be having the

combination of both the labor and capital of Barbara.

Conclusion:

On the basis of the explanation above it can be stated that, Barbara has been

simply rewarded for the services that were performed by her and she should be held

for taxation accordingly under the ordinary meaning of “sec6-5, ITAA 1997”.

Answer to question 3:

Issue:

The fact that the receipt of reward is a product of service rendered is also

referred in the case of “Brent v FC of T (1971)” that were having the nature of

income. The case comprised of the payments that were received by the wife of the

convicted train robber for allowing the exclusive publication of her story to the media

company (Kennedy et al. 2017). The court of law in its verdict stated that the amount

that were received by the taxpayer for granting the right was considered as having

the character of income and purely constituted the product of personal service

income.

Application:

On the basis of the above stated rules, the gathered circumstances of

Barbara can be considered where she is by profession an economist. She is majorly

engaged in the research work but she was once offered a sum of $13,000 for

scripting a book on economics. Persuaded by the publishers offer of writing the book

she simply began to use her effort and knowledge. Barbara successfully wrote down

the book named Principles of Economics. She was duly paid the amount of $13,000.

By referring to the case of “Brent v FC of T (1971)” it can be explained that rewards

that was received by Barbara was simply for the services rendered (Guo and Krause

2017). The amount will be considered as having the nature of income and the

concerned payment is related to making herself available for rendering the service.

Barbara in later stages is found to be assigning the copyright of the books that

was written by her on economics for its exclusive publications. The payment that she

received for assigning the copyright of her literary works stood $13,400. Citing the

case of “Anor v FC of T (1997)” the amount will be considered as income for the

services rendered and it is clearly having the nature of income which should be

taxable under the ordinary meaning of “s6-5, ITAA 1997”.

As the case unfolds, Barbara also sold the manuscripts of the books and the

interview scripts to the library. She was given a sum of $4,350 and $3,200

separately.

Citing the case of “Eisner v Macomber (1920)” the amount will be

considered as income and should be defined as gain that is derived from the capital

and labor as well. On the basis of this justification the payment of $4,350 and $3,200

separately should be considered as the flow from a capital asset and it is the product

of Barbara’s personal effort and exertion.

In the turn of events if the books are simply written by Barbara during the

leisure time and she decides to sell it later in exchange of payment, then the amount

that will be received will be considered as the product of Barbara’s personal exertion

and efforts. The amount will be considered as gain that will be having the

combination of both the labor and capital of Barbara.

Conclusion:

On the basis of the explanation above it can be stated that, Barbara has been

simply rewarded for the services that were performed by her and she should be held

for taxation accordingly under the ordinary meaning of “sec6-5, ITAA 1997”.

Answer to question 3:

Issue:

5TAXATION LAW

The centre of focus here in this case is the interest payment received by

taxpayer from the loan made under the loan agreement.

Rule:

“Sec 6-5, ITA Act 1997” explains that the ordinary income with respect to the

ordinary meaning is considered under this legislation. It is worth mentioning that the

income in respect of the ordinary concepts means the gains that needs the

characterisation by the court to ascertain if the gains possess the character of

income. In the same way the assessable earnings comprise of the ordinary earnings

and the statutory earnings (Bishop and Plumb 2016). The ordinary income is usually

held as income by the court and usually requires the application of the definite

principles to treat the income under the concepts of ordinary income. The statutory

income is considered taxable under the numerous provisions in the taxation acts

particularly the net amount of capital gains.

“Sec6-25(2)” clearly states that statutory income must be first considered prior to

making the application of the ordinary income as the amount must be held for

assessment under the most specific provision. While for the taxpayers it is also

necessary to denote that receipts cannot be held as the ordinary income if the

receipts fails to meet the two perquisites. This includes;

a. Cash or convertible to cash

b. Real gain to the taxpayer

In order to consider tax liability of the receipts it is necessary to apply the pre-

requisite of the ordinary income. It is noticed that the both the prerequisite of the

income is met, then in such a situation the ordinary income will be showing the

satisfactory characteristics of income. A gain that is having the nature of periodic or

regularity is more probably going to have the nature of ordinary income than the

gains those are paid as lump sum (Pinto and Evans 2018). There are some

important consideration relating to the lump sum gains as well that may be having

the characteristics of ordinary income. such as one-off receipt of interest within the

arrangement of loan.

Application:

Gathered circumstances from the case study suggest that Patrick the

concerned taxpayer here has received an interest from the loan that he has made to

his son. The loan amount comprised of $52,000 that was given by Patrick to his son

David. The loan agreement involved the repayment of principle loan amount with the

interest of $6,000 to the father in five-year span. The principle amount of loan and an

amount of 5% on the loan value was returned by David to his father Patrick through

a single mode cheque.

It can be stated that the interest that is received by father from his son is a

gain from the loan agreement. The amount was paid to Patrick in lump sum through

cheque that also accompanied interest amount. The amount can be categorized as

one-off receipt of interest under the loan agreement which is having the

characteristics of ordinary income. Patrick will be considered taxable under “sec 6-

5, ITAA 1997” for the interest on loan that is received since both the perquisite of the

ordinary income is satisfied in this situation.

Conclusion:

The centre of focus here in this case is the interest payment received by

taxpayer from the loan made under the loan agreement.

Rule:

“Sec 6-5, ITA Act 1997” explains that the ordinary income with respect to the

ordinary meaning is considered under this legislation. It is worth mentioning that the

income in respect of the ordinary concepts means the gains that needs the

characterisation by the court to ascertain if the gains possess the character of

income. In the same way the assessable earnings comprise of the ordinary earnings

and the statutory earnings (Bishop and Plumb 2016). The ordinary income is usually

held as income by the court and usually requires the application of the definite

principles to treat the income under the concepts of ordinary income. The statutory

income is considered taxable under the numerous provisions in the taxation acts

particularly the net amount of capital gains.

“Sec6-25(2)” clearly states that statutory income must be first considered prior to

making the application of the ordinary income as the amount must be held for

assessment under the most specific provision. While for the taxpayers it is also

necessary to denote that receipts cannot be held as the ordinary income if the

receipts fails to meet the two perquisites. This includes;

a. Cash or convertible to cash

b. Real gain to the taxpayer

In order to consider tax liability of the receipts it is necessary to apply the pre-

requisite of the ordinary income. It is noticed that the both the prerequisite of the

income is met, then in such a situation the ordinary income will be showing the

satisfactory characteristics of income. A gain that is having the nature of periodic or

regularity is more probably going to have the nature of ordinary income than the

gains those are paid as lump sum (Pinto and Evans 2018). There are some

important consideration relating to the lump sum gains as well that may be having

the characteristics of ordinary income. such as one-off receipt of interest within the

arrangement of loan.

Application:

Gathered circumstances from the case study suggest that Patrick the

concerned taxpayer here has received an interest from the loan that he has made to

his son. The loan amount comprised of $52,000 that was given by Patrick to his son

David. The loan agreement involved the repayment of principle loan amount with the

interest of $6,000 to the father in five-year span. The principle amount of loan and an

amount of 5% on the loan value was returned by David to his father Patrick through

a single mode cheque.

It can be stated that the interest that is received by father from his son is a

gain from the loan agreement. The amount was paid to Patrick in lump sum through

cheque that also accompanied interest amount. The amount can be categorized as

one-off receipt of interest under the loan agreement which is having the

characteristics of ordinary income. Patrick will be considered taxable under “sec 6-

5, ITAA 1997” for the interest on loan that is received since both the perquisite of the

ordinary income is satisfied in this situation.

Conclusion:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

The interest that is in question is having the characteristics of ordinary

income. Even though the amount was paid in lump-sum but it is a real gain for the

Patrick and should accordingly assessed under “sec 6-5, ITAA 1997”.

The interest that is in question is having the characteristics of ordinary

income. Even though the amount was paid in lump-sum but it is a real gain for the

Patrick and should accordingly assessed under “sec 6-5, ITAA 1997”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

References:

Barkoczy, S. and Wilkinson, T., 2019. Australia’s Formal Venture Capital Tax

Incentive Programs. In Incentivising Angels (pp. 29-39). Springer, Singapore.

Beretta, G., 2017. Taxation of individuals in the sharing economy. Intertax, 45(1),

pp.2-11.

Bishop, J. and Plumb, M., 2016. Cyclical Labour Market Adjustment in

Australia. RBA Bulletin, March, pp.11-20.

Braithwaite, V., 2019. Tensions between the citizen taxpaying role and compliance

practices. Centre for Tax System Integrity (CTSI), Research School of Social

Sciences, The Australian National University.

Cunningham, C.R. and Engelhardt, G.V., 2018. Housing capital-gains taxation and

homeowner mobility: evidence from the Taxpayer Relief Act of 1997. Journal of

urban Economics, 63(3), pp.803-815.

Guo, J.T. and Krause, A., 2017. Changing social preferences and optimal

redistributive taxation. Oxford Economic Papers, 70(1), pp.73-92.

Kennedy, T., Smyth, R., Valadkhani, A. and Chen, G., 2017. Does income inequality

hinder economic growth? New evidence using Australian taxation

statistics. Economic Modelling, 65, pp.119-128.

Long, B., Campbell, J. and Kelshaw, C., 2016. The justice lens on taxation policy in

Australia. St Mark's Review, (235), p.94.

Pinto, D. and Evans, M., 2018. Returning income taxation revenue to the states:

back to the future.

Richardson, G. and Lanis, R., 2017. Determinants of the variability in corporate

effective tax rates and tax reform: Evidence from Australia. Journal of accounting

and public policy, 26(6), pp.689-704.

References:

Barkoczy, S. and Wilkinson, T., 2019. Australia’s Formal Venture Capital Tax

Incentive Programs. In Incentivising Angels (pp. 29-39). Springer, Singapore.

Beretta, G., 2017. Taxation of individuals in the sharing economy. Intertax, 45(1),

pp.2-11.

Bishop, J. and Plumb, M., 2016. Cyclical Labour Market Adjustment in

Australia. RBA Bulletin, March, pp.11-20.

Braithwaite, V., 2019. Tensions between the citizen taxpaying role and compliance

practices. Centre for Tax System Integrity (CTSI), Research School of Social

Sciences, The Australian National University.

Cunningham, C.R. and Engelhardt, G.V., 2018. Housing capital-gains taxation and

homeowner mobility: evidence from the Taxpayer Relief Act of 1997. Journal of

urban Economics, 63(3), pp.803-815.

Guo, J.T. and Krause, A., 2017. Changing social preferences and optimal

redistributive taxation. Oxford Economic Papers, 70(1), pp.73-92.

Kennedy, T., Smyth, R., Valadkhani, A. and Chen, G., 2017. Does income inequality

hinder economic growth? New evidence using Australian taxation

statistics. Economic Modelling, 65, pp.119-128.

Long, B., Campbell, J. and Kelshaw, C., 2016. The justice lens on taxation policy in

Australia. St Mark's Review, (235), p.94.

Pinto, D. and Evans, M., 2018. Returning income taxation revenue to the states:

back to the future.

Richardson, G. and Lanis, R., 2017. Determinants of the variability in corporate

effective tax rates and tax reform: Evidence from Australia. Journal of accounting

and public policy, 26(6), pp.689-704.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.