Taxation Law Assignment: GST, CGT Implications for City Sky and Emma

VerifiedAdded on 2022/11/07

|11

|2167

|480

Homework Assignment

AI Summary

This document provides a detailed analysis of two taxation law scenarios. The first part addresses whether City Sky Co, a property investment and development company, can claim Input Tax Credit (ITC) for legal services related to a property development, considering GST regulations. The second part examines the Capital Gains Tax (CGT) implications for Emma, analyzing the tax consequences of selling land, shares, and a piano, considering the Income Tax Assessment Act 1997. The assignment calculates the ITC amount for City Sky Co and determines Emma's CGT gain, including the application of relevant provisions and elements of cost base and capital proceeds.

Running head: TAXATION LAW

TAXATION LAW

Name of the Student:

Name of the University:

Author Note:

TAXATION LAW

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Answer 1:

Issue

The matter of dispute arising out of the cases scenario weather ITC can be claimed by

City Sky Company presuming that the concerned company is registered under the GST scheme.

Rules

One can claim INPUT TAX CREDIT only on some specific type of goods or services

upon which GST is permissible to be imposed. This has been provided in the provisions

contained in s7.1 of the Goods and Services Tax Act 1999 or GSTA. In order to claim for

INPUT TAX CREDIT, GST must be applied on the services or goods in concern. However there

lie two criteria which were to be satisfied in order to impose GST. The two conditions are

taxable supplies along with taxable importations.

The first condition to be satisfied in order to impose GST is that creditable imposition or

creditable acquisition must occur.

Under section 7.1 of the GSTA, GST is generally paid on supplies and importation that

are taxable. Under section 9.5 of GSTA taxable supplies are defined which provides that a

taxable supply is made and when the making of such supply is during the course of transaction

carried out by an enterprise and such supply is in relation with Australia and the enterprise has

been registered or will be registered.

Under section 9.70 the GST amount on any taxable supply is given and GST amount is

calculated as:

Answer 1:

Issue

The matter of dispute arising out of the cases scenario weather ITC can be claimed by

City Sky Company presuming that the concerned company is registered under the GST scheme.

Rules

One can claim INPUT TAX CREDIT only on some specific type of goods or services

upon which GST is permissible to be imposed. This has been provided in the provisions

contained in s7.1 of the Goods and Services Tax Act 1999 or GSTA. In order to claim for

INPUT TAX CREDIT, GST must be applied on the services or goods in concern. However there

lie two criteria which were to be satisfied in order to impose GST. The two conditions are

taxable supplies along with taxable importations.

The first condition to be satisfied in order to impose GST is that creditable imposition or

creditable acquisition must occur.

Under section 7.1 of the GSTA, GST is generally paid on supplies and importation that

are taxable. Under section 9.5 of GSTA taxable supplies are defined which provides that a

taxable supply is made and when the making of such supply is during the course of transaction

carried out by an enterprise and such supply is in relation with Australia and the enterprise has

been registered or will be registered.

Under section 9.70 the GST amount on any taxable supply is given and GST amount is

calculated as:

2TAXATION LAW

Taxable supply= 10 percent of taxable supply value.

The formula for determining the taxable supply value is given under section 9.75 of the

GSTA , is equal to price*(10/11).

Where price equal to total consideration in respect of the supply without GST being

applied on it.

On the other hand section 11.5 of GSTA numerous that are creditable acquisition is made

when anything is acquired only or partly for creditable purpose and the supply in respect of that

thing can be regarded as a taxable supply and consideration for such supply is required to be paid

and the company has to be undergone registration.

Section 11.20 of GSTA provides that input tax credit is entitled to any credible

acquisition that has been made.

Moreover section 11.25 of GSTA provides that the input tax credit amount in respect of a

credible acquisition is equal to the amount of GST that is required to be paid regarding the

supply of the entity which is acquired. But this input tax credit amount is decreased incase

acquisition is creditable partly.

Generally the taxable supplies or the taxable importations are considered when the

company in this regard has provisions related to GST or such company can be registered as a

company on which GST can be imposed.

Any company or organization which has been registered or has been incorporated under

the GST scheme has the right to avail ITC for their editable acquisitions and also in respect of

taxable importation. The companies are the organizations that can claim ITC must be registered

Taxable supply= 10 percent of taxable supply value.

The formula for determining the taxable supply value is given under section 9.75 of the

GSTA , is equal to price*(10/11).

Where price equal to total consideration in respect of the supply without GST being

applied on it.

On the other hand section 11.5 of GSTA numerous that are creditable acquisition is made

when anything is acquired only or partly for creditable purpose and the supply in respect of that

thing can be regarded as a taxable supply and consideration for such supply is required to be paid

and the company has to be undergone registration.

Section 11.20 of GSTA provides that input tax credit is entitled to any credible

acquisition that has been made.

Moreover section 11.25 of GSTA provides that the input tax credit amount in respect of a

credible acquisition is equal to the amount of GST that is required to be paid regarding the

supply of the entity which is acquired. But this input tax credit amount is decreased incase

acquisition is creditable partly.

Generally the taxable supplies or the taxable importations are considered when the

company in this regard has provisions related to GST or such company can be registered as a

company on which GST can be imposed.

Any company or organization which has been registered or has been incorporated under

the GST scheme has the right to avail ITC for their editable acquisitions and also in respect of

taxable importation. The companies are the organizations that can claim ITC must be registered

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

under the GST regime. In order to fulfill such Condition the concerned company or organization

is required to carry out transactions that can be considered as a part of business activities.

Moreover such companies or organizations shall not be excluded from GST imposition. Hence

any organization or company has the right to claim ITC provided it has made business related

services in order to result a supply which is taxable and such Company or organization has not

availed it as an end consumer.

Application

In the present case scenario it has been seen that City Sky Company has been established

for carrying out investment and development of property. It bought a piece of vacant land located

in Brisbane’s southern part with the aim of building about 15 apartments for resulting their sale.

In this regard the company had taken services from a local lawyer and paid around

$33,000 to such lawyer. The lawyer named as Maurice Blackburn has a sole trading business and

its turnover revenue every year is around 300000 dollars. Any company or organization which

has been registered or has been incorporated under the scheme of GST has the right to claim

Input Tax Credt in respect of their editable acquisitions and also in respect of taxable

importation. The companies are the organizations that can claim ITC must be registered under

the GST regime. In order to fulfill such Condition the concerned company or organization is

required to carry out transactions that can be considered as a part of business activities. Moreover

such companies or organizations shall not be e excluded from GST imposition. Hence any

organization or company has the right to claim ITC provided it has made business related

services in order to result a supply which is taxable and such Company or organization has not

availed it as an end consumer.

under the GST regime. In order to fulfill such Condition the concerned company or organization

is required to carry out transactions that can be considered as a part of business activities.

Moreover such companies or organizations shall not be excluded from GST imposition. Hence

any organization or company has the right to claim ITC provided it has made business related

services in order to result a supply which is taxable and such Company or organization has not

availed it as an end consumer.

Application

In the present case scenario it has been seen that City Sky Company has been established

for carrying out investment and development of property. It bought a piece of vacant land located

in Brisbane’s southern part with the aim of building about 15 apartments for resulting their sale.

In this regard the company had taken services from a local lawyer and paid around

$33,000 to such lawyer. The lawyer named as Maurice Blackburn has a sole trading business and

its turnover revenue every year is around 300000 dollars. Any company or organization which

has been registered or has been incorporated under the scheme of GST has the right to claim

Input Tax Credt in respect of their editable acquisitions and also in respect of taxable

importation. The companies are the organizations that can claim ITC must be registered under

the GST regime. In order to fulfill such Condition the concerned company or organization is

required to carry out transactions that can be considered as a part of business activities. Moreover

such companies or organizations shall not be e excluded from GST imposition. Hence any

organization or company has the right to claim ITC provided it has made business related

services in order to result a supply which is taxable and such Company or organization has not

availed it as an end consumer.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

It is to be determined whether the City Sky Company can claim ITC in respect of the

creditable importations and creditable acquisitions for which GST is imposed on it.

Hence, input tax credit can be claimed by City Sky Co for its transaction made with the

lawyer and it can be computed in the following way by applying the following provisions.

Under section 9.70 the GST amount on any taxable supply is given and GST amount is

calculated as:

Taxable supply= 10 percent of taxable supply value.

The formula for determining the taxable supply value is given under section 9.75 of the

Act, is equal to price*(10/11).

Taxation value= (10*33000)/11= $30000

Value of input tax credit=10 percent of $ 30000= 3000 dollars.

Conclusion:

The company can claim 3000 $ as the input tax credit.

Answer to 2

Issue

The issue arising in the scenario is determining the cgt resulting out of the transactions

made by Emma.

Rules

It is to be determined whether the City Sky Company can claim ITC in respect of the

creditable importations and creditable acquisitions for which GST is imposed on it.

Hence, input tax credit can be claimed by City Sky Co for its transaction made with the

lawyer and it can be computed in the following way by applying the following provisions.

Under section 9.70 the GST amount on any taxable supply is given and GST amount is

calculated as:

Taxable supply= 10 percent of taxable supply value.

The formula for determining the taxable supply value is given under section 9.75 of the

Act, is equal to price*(10/11).

Taxation value= (10*33000)/11= $30000

Value of input tax credit=10 percent of $ 30000= 3000 dollars.

Conclusion:

The company can claim 3000 $ as the input tax credit.

Answer to 2

Issue

The issue arising in the scenario is determining the cgt resulting out of the transactions

made by Emma.

Rules

5TAXATION LAW

In case capital property is being disposed by its owner by causing its sale then this

transaction is regarded as a CGT A 1 event and this is provided under section 104.10 of the

Income Tax assessment act 1997 (Cth) or ITAA 1997.

A CGT A 1 event takes place when ownership in absolute form is transferred one party to

other by the transfer of property act by the concerned parties or by the order of court. However

this transfer must involve absolute transfer, mere change of nature of title will not attract a CGT

A 1 event.

A CGT event includes an asset of CGT. However an asset which was brought into

acquisition will not be considered as CGT asset if the same was acquired prior to 20th September

of 1985.

According to section 110.25 of ITAA 1997, the general rules of Cost Base are provided

which includes mainly five types of elements. Element 1 includes the money paid or is needed to

pay for acquiring the asset. In case a transaction involves exchange of one property with another,

then in such situation market value of the property is taken into consideration.

Element 2 involves the incidental costs incurred.

Element 3 refers to the cost incurred in order to own such CGT asset provided the asset is

acquired post 20th August 1991. This element includes costs for maintaining, insuring or even

repairing the asset, the interest required to be paid for the money borrowed for acquiring the

asset. However as per sections 118.17 of ITAA 1997and 108.30 of ITAA 1997, element 3 is not

applicable on collectables or assets for personal usage.

In case capital property is being disposed by its owner by causing its sale then this

transaction is regarded as a CGT A 1 event and this is provided under section 104.10 of the

Income Tax assessment act 1997 (Cth) or ITAA 1997.

A CGT A 1 event takes place when ownership in absolute form is transferred one party to

other by the transfer of property act by the concerned parties or by the order of court. However

this transfer must involve absolute transfer, mere change of nature of title will not attract a CGT

A 1 event.

A CGT event includes an asset of CGT. However an asset which was brought into

acquisition will not be considered as CGT asset if the same was acquired prior to 20th September

of 1985.

According to section 110.25 of ITAA 1997, the general rules of Cost Base are provided

which includes mainly five types of elements. Element 1 includes the money paid or is needed to

pay for acquiring the asset. In case a transaction involves exchange of one property with another,

then in such situation market value of the property is taken into consideration.

Element 2 involves the incidental costs incurred.

Element 3 refers to the cost incurred in order to own such CGT asset provided the asset is

acquired post 20th August 1991. This element includes costs for maintaining, insuring or even

repairing the asset, the interest required to be paid for the money borrowed for acquiring the

asset. However as per sections 118.17 of ITAA 1997and 108.30 of ITAA 1997, element 3 is not

applicable on collectables or assets for personal usage.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

The Element 4 includes the capital expenses incurred for the reason of effecting measures

that can increase or hold the present value of the asset. It includes the cost of moving as well as

installing an asset also.

Element 5 includes the capital expenses which is incurred for proving, establishing,

defending or even holding the title of the asset or right of such asset.

In this regard, capital proceeds in relation to a CGT event must be considered too. This

has been provided u/s 116.20 of the ITAA 1997. CP or the capital proceeds is the sum of the

money which is received or will be received related to the event occurring. It also includes the

market price of the property received or is entitled to get it related to the CGT event. Moreover,

in case an asset is held by a taxpayer for a period of more than 12 moths then a discount of 50

percent is applied on the capital gain resulting from the disposal of the said asset.

Application:

Here in order to determine the CGT consequences the transactions made by Emma are

required to be considered.

Selling of land @ 1,000,000 dollars:

According to section 110.25 of ITAA 1997, the general rules of Cost Base are

provided which includes mainly five types of elements. Element 1 includes the money paid or is

needed to pay for acquiring the asset. In case a transaction involves exchange of one property

with another, then in such situation market value of the property is taken into consideration. here

Emma bought a block of land on 1991 for 250000 dollars (this is element 1).

The Element 4 includes the capital expenses incurred for the reason of effecting measures

that can increase or hold the present value of the asset. It includes the cost of moving as well as

installing an asset also.

Element 5 includes the capital expenses which is incurred for proving, establishing,

defending or even holding the title of the asset or right of such asset.

In this regard, capital proceeds in relation to a CGT event must be considered too. This

has been provided u/s 116.20 of the ITAA 1997. CP or the capital proceeds is the sum of the

money which is received or will be received related to the event occurring. It also includes the

market price of the property received or is entitled to get it related to the CGT event. Moreover,

in case an asset is held by a taxpayer for a period of more than 12 moths then a discount of 50

percent is applied on the capital gain resulting from the disposal of the said asset.

Application:

Here in order to determine the CGT consequences the transactions made by Emma are

required to be considered.

Selling of land @ 1,000,000 dollars:

According to section 110.25 of ITAA 1997, the general rules of Cost Base are

provided which includes mainly five types of elements. Element 1 includes the money paid or is

needed to pay for acquiring the asset. In case a transaction involves exchange of one property

with another, then in such situation market value of the property is taken into consideration. here

Emma bought a block of land on 1991 for 250000 dollars (this is element 1).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

According to section 110.25 of ITAA 1997 Element 2 involves the incidental costs

incurred. She further spent 5000 for stamp duty, 10000 $ for legal fees. Therefore, 15000 $=

element 2.

According to section 110.25 of ITAA, Element 3 refers to the cost incurred in order to

own such CGT asset provided the asset is acquired post 20th August 1991. This element includes

costs for maintaining, insuring or even repairing the asset, the interest required to be paid for the

money borrowed for acquiring the asset. However as per sections 118.17 of ITAA 1997and

108.30 of ITAA 1997, element 3 is not applicable on collectables or assets for personal usage.

To accumulate the purchase price, she took a loan on which she paid interest of about 32000 $.

While the land was under her ownership, she paid 22000 $ as water rate, council rate and

insurance. This is element 3.

According to section 110.25 of ITAA, Element 4 includes the capital expenses incurred for the

reason of effecting measures that can increase or hold the present value of the asset. It includes

the cost of moving as well as installing an asset also. Fees paid in relation to legal proceedings=

5000 $ (this is Element 4).

According to section 110.25 of ITAA, Element 5 includes the capital expenses which are

incurred for proving, establishing, defending or even holding the title of the asset or right of such

asset. Thus, She spent 27500 $ for removing pine trees. This is Element 5.

Advertising+ legal fees+ agent’s fees on the sale of the land= 25,000 (not taken into

account).

Therefore, Sale proceeds= 1,000,000- 25000=975000.

Selling of shares:

According to section 110.25 of ITAA 1997 Element 2 involves the incidental costs

incurred. She further spent 5000 for stamp duty, 10000 $ for legal fees. Therefore, 15000 $=

element 2.

According to section 110.25 of ITAA, Element 3 refers to the cost incurred in order to

own such CGT asset provided the asset is acquired post 20th August 1991. This element includes

costs for maintaining, insuring or even repairing the asset, the interest required to be paid for the

money borrowed for acquiring the asset. However as per sections 118.17 of ITAA 1997and

108.30 of ITAA 1997, element 3 is not applicable on collectables or assets for personal usage.

To accumulate the purchase price, she took a loan on which she paid interest of about 32000 $.

While the land was under her ownership, she paid 22000 $ as water rate, council rate and

insurance. This is element 3.

According to section 110.25 of ITAA, Element 4 includes the capital expenses incurred for the

reason of effecting measures that can increase or hold the present value of the asset. It includes

the cost of moving as well as installing an asset also. Fees paid in relation to legal proceedings=

5000 $ (this is Element 4).

According to section 110.25 of ITAA, Element 5 includes the capital expenses which are

incurred for proving, establishing, defending or even holding the title of the asset or right of such

asset. Thus, She spent 27500 $ for removing pine trees. This is Element 5.

Advertising+ legal fees+ agent’s fees on the sale of the land= 25,000 (not taken into

account).

Therefore, Sale proceeds= 1,000,000- 25000=975000.

Selling of shares:

8TAXATION LAW

Shares were purchased for 3.5$ per share. Total purchasing price= 3.5 * 1000= 3500 $.

Selling price= 50.85 * 10000= 50,850 $.

Selling of stamp:

Selling price= 50000 $.

Sale proceeds= 50000- 5000=45000 $.

Purchasing cost= 60000 $.

Loss= Purchasing cost- Sale proceeds= 60000 $- 45000 $=15000$. This amount of 15000

$ will be carried to the coming year.

Sale of piano:

Selling price= 30000 $.

Buying price= 80000 $

Loss= 80000- 30000= 50000$. This amount of 50000 $ will be carried to the coming

year.

CGT consequences in respect of the transactions made by Emma:

CGT Gain

Amount in

dollars

Amount in

dollars

Amount in

dollars

Amount

in dollars

Amount in

dollars

Amount

in dollars

For the sale

of Land block

Cost Proceeds 975,000

1st element 25,0000

Shares were purchased for 3.5$ per share. Total purchasing price= 3.5 * 1000= 3500 $.

Selling price= 50.85 * 10000= 50,850 $.

Selling of stamp:

Selling price= 50000 $.

Sale proceeds= 50000- 5000=45000 $.

Purchasing cost= 60000 $.

Loss= Purchasing cost- Sale proceeds= 60000 $- 45000 $=15000$. This amount of 15000

$ will be carried to the coming year.

Sale of piano:

Selling price= 30000 $.

Buying price= 80000 $

Loss= 80000- 30000= 50000$. This amount of 50000 $ will be carried to the coming

year.

CGT consequences in respect of the transactions made by Emma:

CGT Gain

Amount in

dollars

Amount in

dollars

Amount in

dollars

Amount

in dollars

Amount in

dollars

Amount

in dollars

For the sale

of Land block

Cost Proceeds 975,000

1st element 25,0000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

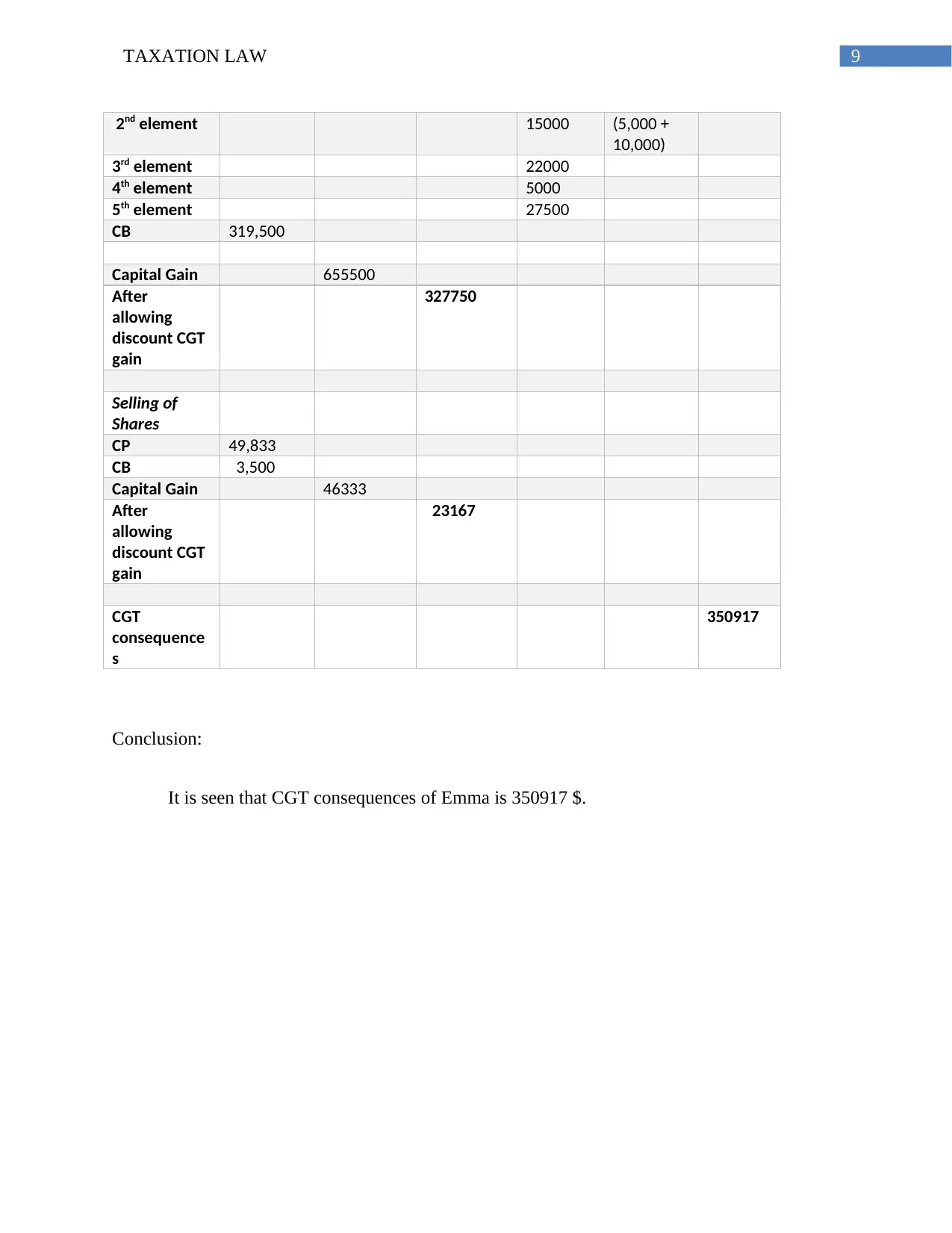

9TAXATION LAW

2nd element 15000 (5,000 +

10,000)

3rd element 22000

4th element 5000

5th element 27500

CB 319,500

Capital Gain 655500

After

allowing

discount CGT

gain

327750

Selling of

Shares

CP 49,833

CB 3,500

Capital Gain 46333

After

allowing

discount CGT

gain

23167

CGT

consequence

s

350917

Conclusion:

It is seen that CGT consequences of Emma is 350917 $.

2nd element 15000 (5,000 +

10,000)

3rd element 22000

4th element 5000

5th element 27500

CB 319,500

Capital Gain 655500

After

allowing

discount CGT

gain

327750

Selling of

Shares

CP 49,833

CB 3,500

Capital Gain 46333

After

allowing

discount CGT

gain

23167

CGT

consequence

s

350917

Conclusion:

It is seen that CGT consequences of Emma is 350917 $.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

The Goods and Services Tax 1999

The Income Tax Assessment Act 1997 (Cth)

References:

The Goods and Services Tax 1999

The Income Tax Assessment Act 1997 (Cth)

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.