Taxation Law Assignment: Taxation of Compensation, CGT, and Income

VerifiedAdded on 2022/12/05

|15

|4080

|309

Homework Assignment

AI Summary

This taxation law assignment addresses two key questions. The first question examines the tax consequences of compensation received by a company for patent infringement and loss of revenue, analyzing whether the amounts are considered ordinary income or capital receipts under ITAA 1997 and relevant case law. The second question focuses on capital gains tax (CGT) implications arising from the sale of land, differentiating between pre-CGT and post-CGT assets and determining whether profits from the sale of subdivided land are taxable under section 25(1) or section 26(a). The assignment applies relevant legislation and case law to determine the assessable income and CGT liability. It covers issues related to compensation for business losses, interest, and legal fees, as well as the implications of land subdivision for tax purposes. The assignment concludes with calculations of assessable income and a discussion of the tax treatment of different income components.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.....................................................................................................................................2

Laws:......................................................................................................................................2

Application:............................................................................................................................4

Conclusion:............................................................................................................................6

Answer to question 2:.................................................................................................................6

Issues:.....................................................................................................................................6

Laws:......................................................................................................................................6

Application.............................................................................................................................8

Conclusion:..........................................................................................................................10

References:...............................................................................................................................11

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.....................................................................................................................................2

Laws:......................................................................................................................................2

Application:............................................................................................................................4

Conclusion:............................................................................................................................6

Answer to question 2:.................................................................................................................6

Issues:.....................................................................................................................................6

Laws:......................................................................................................................................6

Application.............................................................................................................................8

Conclusion:..........................................................................................................................10

References:...............................................................................................................................11

2TAXATION LAW

Answer to question 1:

Issues:

The issue here is associated to the tax consequences of the compensation amount that

is received by Our Earth Pty Ltd under “Division 6” or “subsection 25 (1) of the ITAA

1936”?

Laws:

Where the taxpayers receive the compensation payment on the basis of right of

seeking compensation or due to cause of action or because of any kind of legal actions taken

by the taxpayer in respect of right of taxpayers or arising because of the legal actions of law

court or comprises of any dissected sum (Evans et al., 2015). Where the taxpayers receive

any kind of compensation for damages, the such kind of compensatory damages are held as

assessable ordinary income within “Division 6 of the ITAA 1997” or it may be considered as

statutory income.

In order to establish whether or not the damages relating to compensation are treated

as ordinary income or capital amount, it is completely dependent on the nature of receipts.

When a taxpayer receives the compensation damages that is associated to income in relation

to the ordinary meaning then the legislative provision of “section 6-5, of the ITAA 1997” is

implemented (Chardon et al., 2016). For example, the compensatory damages are only treated

as income if the damages are received as the series of recurrent, periodic payments cannot be

categorized as instalment of lump sum.

The decision made in “Californian Oil Products Ltd v FCT (1934)” the

compensation damages that are paid or the compensation to insure the taxpayer for the loss of

profit that would originate in the ordinary business course will be treated as income

(Woellner et al., 2016). The reason for this is that it amounts to a part of profit that are gained

Answer to question 1:

Issues:

The issue here is associated to the tax consequences of the compensation amount that

is received by Our Earth Pty Ltd under “Division 6” or “subsection 25 (1) of the ITAA

1936”?

Laws:

Where the taxpayers receive the compensation payment on the basis of right of

seeking compensation or due to cause of action or because of any kind of legal actions taken

by the taxpayer in respect of right of taxpayers or arising because of the legal actions of law

court or comprises of any dissected sum (Evans et al., 2015). Where the taxpayers receive

any kind of compensation for damages, the such kind of compensatory damages are held as

assessable ordinary income within “Division 6 of the ITAA 1997” or it may be considered as

statutory income.

In order to establish whether or not the damages relating to compensation are treated

as ordinary income or capital amount, it is completely dependent on the nature of receipts.

When a taxpayer receives the compensation damages that is associated to income in relation

to the ordinary meaning then the legislative provision of “section 6-5, of the ITAA 1997” is

implemented (Chardon et al., 2016). For example, the compensatory damages are only treated

as income if the damages are received as the series of recurrent, periodic payments cannot be

categorized as instalment of lump sum.

The decision made in “Californian Oil Products Ltd v FCT (1934)” the

compensation damages that are paid or the compensation to insure the taxpayer for the loss of

profit that would originate in the ordinary business course will be treated as income

(Woellner et al., 2016). The reason for this is that it amounts to a part of profit that are gained

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

from the business activities even though they are triggered by uncommon or exceptional

events or situations.

The verdict given in the case of “CT (Vic) v Phillips (1936)” explained that if the

compensation that are paid for the loss of business or associated to the loss of basis or basis

of business then the compensation that is received will be considered as the loss of capital

asset (Ingles, 2015). because of absence of countervailing observation, the receipts take the

nature of capital. While in another case of “FCT v Spedley Securities Ltd (1988)” the court

of law in its decision explained that the sum received in the form of damage to goodwill is

viewed as capital in nature. On receiving a compensation amount for injury to the capital

asset is regarded as capital in nature.

Where the taxpayers are given interest for the part of compensation sum then the

amount will be considered as taxable income for the taxpayer on the basis of the ordinary

concept of income. The decision given by court in “Whitaker v FCT (1998)” explained that

post judgement interest has the nature of interest is treated as ordinary income (Duncan et al.,

2018). Where it is noticed that the compensation for lost income is related then the interest

that is paid will be considered income, if the claimant has not suffered damage then the

claimant has received the interest that is awarded.

When it is noted that the taxpayer is permitted to claim deduction for the legal

outgoings which is available under the legislative provision of “section 8-1, ITAA 1997”

then the payment in respect of the legal expenditure will be included into the assessable

income as the taxable recoupment within the “subdivision 20-A”. The legal expenses that is

awarded is usually paid to indemnify the recipient as the successful party for the expense of

bringing lawsuit. The amount is not held as income within ordinary meaning (Svetalekth,

2016). The amount is regarded as the assessable recoupment within the “subsection 20-20

from the business activities even though they are triggered by uncommon or exceptional

events or situations.

The verdict given in the case of “CT (Vic) v Phillips (1936)” explained that if the

compensation that are paid for the loss of business or associated to the loss of basis or basis

of business then the compensation that is received will be considered as the loss of capital

asset (Ingles, 2015). because of absence of countervailing observation, the receipts take the

nature of capital. While in another case of “FCT v Spedley Securities Ltd (1988)” the court

of law in its decision explained that the sum received in the form of damage to goodwill is

viewed as capital in nature. On receiving a compensation amount for injury to the capital

asset is regarded as capital in nature.

Where the taxpayers are given interest for the part of compensation sum then the

amount will be considered as taxable income for the taxpayer on the basis of the ordinary

concept of income. The decision given by court in “Whitaker v FCT (1998)” explained that

post judgement interest has the nature of interest is treated as ordinary income (Duncan et al.,

2018). Where it is noticed that the compensation for lost income is related then the interest

that is paid will be considered income, if the claimant has not suffered damage then the

claimant has received the interest that is awarded.

When it is noted that the taxpayer is permitted to claim deduction for the legal

outgoings which is available under the legislative provision of “section 8-1, ITAA 1997”

then the payment in respect of the legal expenditure will be included into the assessable

income as the taxable recoupment within the “subdivision 20-A”. The legal expenses that is

awarded is usually paid to indemnify the recipient as the successful party for the expense of

bringing lawsuit. The amount is not held as income within ordinary meaning (Svetalekth,

2016). The amount is regarded as the assessable recoupment within the “subsection 20-20

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

(2)”, that the amount that is received is regarded as the recoupment of expenses or losses that

are taxable as the recoupment provided the taxpayer received the amount as to indemnify and

the amount will be considered tax deductible under the “ITAA 1936 or ITAA 1997” (Kudrna,

2016).

Application:

The issue that is bought forward here is of Our Earth Pty Ltd which produces bio-

degradable coffee cups for which the company has patent. One of its rival Coffee Bean Pty

Ltd stole the design of coffee cups and sold overseas to the customers for a very cheap price.

This resulted the company to bring the lawsuit against the Coffee Bean Pty Ltd and the

company was successful in obtaining award for damages caused to the design of patent. The

compensation payment that is received is an infringement to the patent and the amount is

received as the right for seeking compensation for causing an illegal breach to the design of

coffee cups.

To take into the account whether the compensatory damages are treated as ordinary

income or capital receipts, the answer is dependent on the character of receipts that is

received by Our Earth Pty Ltd. Mentioning the decision in “CT (Vic) v Phillips (1936)” the

compensatory damages of $300,000 that is paid to the Our Earth Pty Ltd is associated to the

business loss or base of business activities (Long et al., 2016). Because of this, the amount of

$300,000 is regarded as the compensation to the loss of capital asset. In addition to this,

because of the non-existence of countervailing examination, the compensation receipts

constitute a capital amount.

Another instance of judgement made in “FC of T v Spedley Securities Ltd (1988)” is

applied in the current case and it can be stated that the sum of $300,000 that is received by

the taxpayer to recompense for the damages caused to patent that itself forms the item of

(2)”, that the amount that is received is regarded as the recoupment of expenses or losses that

are taxable as the recoupment provided the taxpayer received the amount as to indemnify and

the amount will be considered tax deductible under the “ITAA 1936 or ITAA 1997” (Kudrna,

2016).

Application:

The issue that is bought forward here is of Our Earth Pty Ltd which produces bio-

degradable coffee cups for which the company has patent. One of its rival Coffee Bean Pty

Ltd stole the design of coffee cups and sold overseas to the customers for a very cheap price.

This resulted the company to bring the lawsuit against the Coffee Bean Pty Ltd and the

company was successful in obtaining award for damages caused to the design of patent. The

compensation payment that is received is an infringement to the patent and the amount is

received as the right for seeking compensation for causing an illegal breach to the design of

coffee cups.

To take into the account whether the compensatory damages are treated as ordinary

income or capital receipts, the answer is dependent on the character of receipts that is

received by Our Earth Pty Ltd. Mentioning the decision in “CT (Vic) v Phillips (1936)” the

compensatory damages of $300,000 that is paid to the Our Earth Pty Ltd is associated to the

business loss or base of business activities (Long et al., 2016). Because of this, the amount of

$300,000 is regarded as the compensation to the loss of capital asset. In addition to this,

because of the non-existence of countervailing examination, the compensation receipts

constitute a capital amount.

Another instance of judgement made in “FC of T v Spedley Securities Ltd (1988)” is

applied in the current case and it can be stated that the sum of $300,000 that is received by

the taxpayer to recompense for the damages caused to patent that itself forms the item of

5TAXATION LAW

capital (Campbell, 2018). The amount will not be considered taxable as ordinary income

since it is a compensation for injury to the capital asset.

Later, it is noticed that Our Earth Pty Ltd was compensated with the sum of $200,000

by Coffee Bean Pty Ltd for causing an anticipated loss to the revenue during the last 12

months. Referring to the judgement made in “Californian Oil Products Ltd v FCT (1934)”

the compensation amount of $200,000 that is paid as the damages or to compensate for

causing a loss to business revenues is received during the ordinary business course of Our

Earth Pty Ltd (King, 2016). The sum of $200,000 is an income under the ordinary concepts

of “section 6-5, of the ITAA 1997”.

Our Earth Pty Ltd also received an interest fees of $15,000. The amount of interest

received by Our Earth Pty Ltd amounts to a part of compensation which will be considered

taxable income for the company under the common rules of income. By citing the judgement

made in “Whitaker v FCT (1998)” the interest amount of $15,000 should be viewed as post-

judgement interest and will be considered taxable income under ordinary meaning of

“section 6-5, ITAA 1997” (Yuan, 2016).

It is noted that Our Earth Pty Ltd was also reimbursed the amount of $40,000 that was

incurred as legal fees. The award of legal expenses is paid to compensating the Our Earth Pty

Ltd for being the successful party to have incurred the legal cost of lawsuit. Therefore, the

reimbursement of legal expenditure should not be viewed as ordinary income. The

reimbursement of legal expenditure amounts to payment that is awarded in respect of the

legal expenditure and the same must be included in Our Earth Pty Ltd taxable earnings as a

recoupment within the “subdivision 20-A”. The amount of legal fees paid to Our Earth Pty

Ltd should be considered as recoupment of loss or outgoings that are considered taxable

recoupment (Braithwaite & Reinhart, 2019).

capital (Campbell, 2018). The amount will not be considered taxable as ordinary income

since it is a compensation for injury to the capital asset.

Later, it is noticed that Our Earth Pty Ltd was compensated with the sum of $200,000

by Coffee Bean Pty Ltd for causing an anticipated loss to the revenue during the last 12

months. Referring to the judgement made in “Californian Oil Products Ltd v FCT (1934)”

the compensation amount of $200,000 that is paid as the damages or to compensate for

causing a loss to business revenues is received during the ordinary business course of Our

Earth Pty Ltd (King, 2016). The sum of $200,000 is an income under the ordinary concepts

of “section 6-5, of the ITAA 1997”.

Our Earth Pty Ltd also received an interest fees of $15,000. The amount of interest

received by Our Earth Pty Ltd amounts to a part of compensation which will be considered

taxable income for the company under the common rules of income. By citing the judgement

made in “Whitaker v FCT (1998)” the interest amount of $15,000 should be viewed as post-

judgement interest and will be considered taxable income under ordinary meaning of

“section 6-5, ITAA 1997” (Yuan, 2016).

It is noted that Our Earth Pty Ltd was also reimbursed the amount of $40,000 that was

incurred as legal fees. The award of legal expenses is paid to compensating the Our Earth Pty

Ltd for being the successful party to have incurred the legal cost of lawsuit. Therefore, the

reimbursement of legal expenditure should not be viewed as ordinary income. The

reimbursement of legal expenditure amounts to payment that is awarded in respect of the

legal expenditure and the same must be included in Our Earth Pty Ltd taxable earnings as a

recoupment within the “subdivision 20-A”. The amount of legal fees paid to Our Earth Pty

Ltd should be considered as recoupment of loss or outgoings that are considered taxable

recoupment (Braithwaite & Reinhart, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

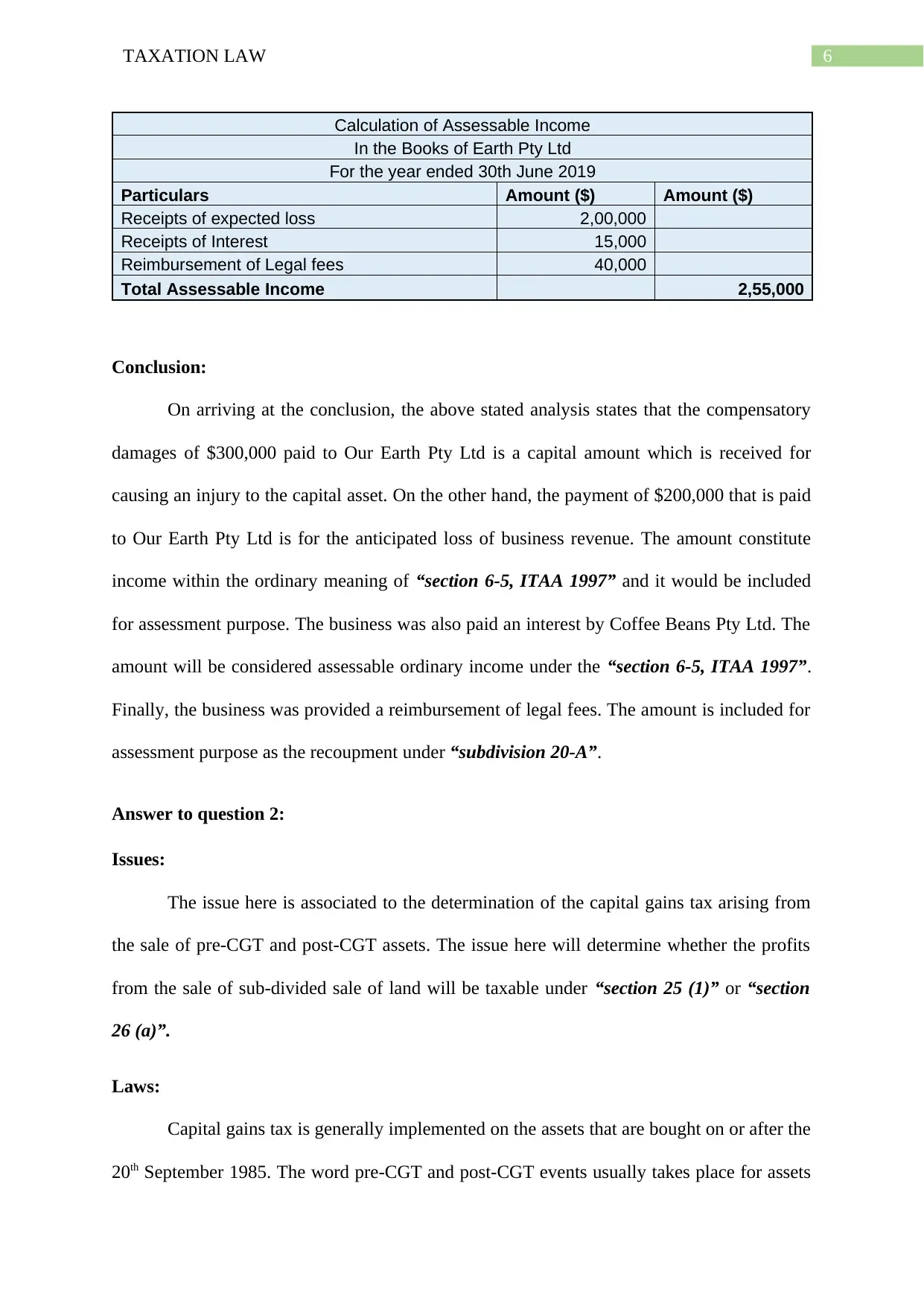

Calculation of Assessable Income

In the Books of Earth Pty Ltd

For the year ended 30th June 2019

Particulars Amount ($) Amount ($)

Receipts of expected loss 2,00,000

Receipts of Interest 15,000

Reimbursement of Legal fees 40,000

Total Assessable Income 2,55,000

Conclusion:

On arriving at the conclusion, the above stated analysis states that the compensatory

damages of $300,000 paid to Our Earth Pty Ltd is a capital amount which is received for

causing an injury to the capital asset. On the other hand, the payment of $200,000 that is paid

to Our Earth Pty Ltd is for the anticipated loss of business revenue. The amount constitute

income within the ordinary meaning of “section 6-5, ITAA 1997” and it would be included

for assessment purpose. The business was also paid an interest by Coffee Beans Pty Ltd. The

amount will be considered assessable ordinary income under the “section 6-5, ITAA 1997”.

Finally, the business was provided a reimbursement of legal fees. The amount is included for

assessment purpose as the recoupment under “subdivision 20-A”.

Answer to question 2:

Issues:

The issue here is associated to the determination of the capital gains tax arising from

the sale of pre-CGT and post-CGT assets. The issue here will determine whether the profits

from the sale of sub-divided sale of land will be taxable under “section 25 (1)” or “section

26 (a)”.

Laws:

Capital gains tax is generally implemented on the assets that are bought on or after the

20th September 1985. The word pre-CGT and post-CGT events usually takes place for assets

Calculation of Assessable Income

In the Books of Earth Pty Ltd

For the year ended 30th June 2019

Particulars Amount ($) Amount ($)

Receipts of expected loss 2,00,000

Receipts of Interest 15,000

Reimbursement of Legal fees 40,000

Total Assessable Income 2,55,000

Conclusion:

On arriving at the conclusion, the above stated analysis states that the compensatory

damages of $300,000 paid to Our Earth Pty Ltd is a capital amount which is received for

causing an injury to the capital asset. On the other hand, the payment of $200,000 that is paid

to Our Earth Pty Ltd is for the anticipated loss of business revenue. The amount constitute

income within the ordinary meaning of “section 6-5, ITAA 1997” and it would be included

for assessment purpose. The business was also paid an interest by Coffee Beans Pty Ltd. The

amount will be considered assessable ordinary income under the “section 6-5, ITAA 1997”.

Finally, the business was provided a reimbursement of legal fees. The amount is included for

assessment purpose as the recoupment under “subdivision 20-A”.

Answer to question 2:

Issues:

The issue here is associated to the determination of the capital gains tax arising from

the sale of pre-CGT and post-CGT assets. The issue here will determine whether the profits

from the sale of sub-divided sale of land will be taxable under “section 25 (1)” or “section

26 (a)”.

Laws:

Capital gains tax is generally implemented on the assets that are bought on or after the

20th September 1985. The word pre-CGT and post-CGT events usually takes place for assets

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

that are purchased prior to or following the commencement of CGT. Assets which are

purchased prior to 20th September 1985 are excluded from capital gains tax. The summary

relating to the CGT events is explained in “section 104-5, ITAA 1997”. A CGT event A1

happens within “section 104-10 (1)” when the asset is sold by the taxpayer. CGT asset can be

defined as any kind of property or legal or equal rights which is not regarded as property

(Johnson & Breunig, 2016).

There are several instances where the owners of land have the chance of subdivision

and selling of land that are that are primarily kept for the long time period. This usually takes

place where the owners of land are the primary producers at outskirts and considers the

construction of residential property as the best possible use of land rather than using the land

for the purpose of agriculture (Dixon & Nassios, 2016). Property development might turn

into substantial part where the taxpayer has the profit making motive from the land. This

brings forward the question as how the profits should be treated. The alternatives include the

following;

a. The subdivision and sale of land may be regarded as the simple realisation of the

capital asset.

b. The degree of land development might be in such manner that it constitutes

performing the business of land development.

c. The property development might be more than a simple realisation of land but may

fall short of requirements associated to conducting business (Torgler, 2016). Then in

such situations it amounts to carrying the business of profit making.

As defined in “Taxation Determination TD 97/3” normal subdividing the land

cannot be held as sale of land under “section 104-10, ITAA 1997”. As per this ruling, it helps

in ascertaining whether the profits made from the isolated transactions should be considered

that are purchased prior to or following the commencement of CGT. Assets which are

purchased prior to 20th September 1985 are excluded from capital gains tax. The summary

relating to the CGT events is explained in “section 104-5, ITAA 1997”. A CGT event A1

happens within “section 104-10 (1)” when the asset is sold by the taxpayer. CGT asset can be

defined as any kind of property or legal or equal rights which is not regarded as property

(Johnson & Breunig, 2016).

There are several instances where the owners of land have the chance of subdivision

and selling of land that are that are primarily kept for the long time period. This usually takes

place where the owners of land are the primary producers at outskirts and considers the

construction of residential property as the best possible use of land rather than using the land

for the purpose of agriculture (Dixon & Nassios, 2016). Property development might turn

into substantial part where the taxpayer has the profit making motive from the land. This

brings forward the question as how the profits should be treated. The alternatives include the

following;

a. The subdivision and sale of land may be regarded as the simple realisation of the

capital asset.

b. The degree of land development might be in such manner that it constitutes

performing the business of land development.

c. The property development might be more than a simple realisation of land but may

fall short of requirements associated to conducting business (Torgler, 2016). Then in

such situations it amounts to carrying the business of profit making.

As defined in “Taxation Determination TD 97/3” normal subdividing the land

cannot be held as sale of land under “section 104-10, ITAA 1997”. As per this ruling, it helps

in ascertaining whether the profits made from the isolated transactions should be considered

8TAXATION LAW

as gains and hence taxable under the “subsection 25 (1), ITAA 1936” (McGee et al., 2016). It

is necessary to understand that before entering in the detailed analysis it is vital to ascertain

that development of land constitutes simple realisation of asset. nevertheless, it is necessary

to understand that if the taxpayer bought the land actually for the resale purpose and

developmental purpose, then the profits that arise from the sale of land maybe treated taxable

as ordinary income irrespective of the sale of land.

Profits originating from the carrying the income deriving activity or in relation to the

land that is purchased prior to introduction of CGT or Pre-CGT assets is mainly included for

assessment purpose under “section 15-15, ITAA 1997” (Bankman et al., 2018). Making any

kind of capital improvements on the pre-CGT asset attracts capital gains tax.

The law court in “Scottish Australian Mining Co Ltd v FC of T (1950)” held that the

taxpayer derived significant amount of profit from the sale of subdivided lots (Schmalbeck et

al., 2015). The commissioner held that taxpayer taxable relating to the profits derived from

sale of several lots of land. The commissioner stated that the profits were considered taxable

as income each under “section 25 (1), ITAA 1936” as income earned from business of land

development and under “section 26 (a)” as profits arising from profit making structure.

In another instance of “FCT v Whitfords Beach Pty Ltd (1982)” the taxpayer was

considered taxable for the income made following the sale of several plots (Buenker, 2018).

The commissioner considered the taxpayer taxable under the “section 25 (1), ITAA 1936” as

the profits arising from profit deriving venture.

Once it is established that the activity of purchasing and sale of land gives rise to

profit that is not earned in the ordinary business course, then the income which is in question

will be considered as taxable income under ordinary concepts provided the taxpayer has the

purpose of making profit at the time of acquisition (Mertens & Montiel Olea, 2018).

as gains and hence taxable under the “subsection 25 (1), ITAA 1936” (McGee et al., 2016). It

is necessary to understand that before entering in the detailed analysis it is vital to ascertain

that development of land constitutes simple realisation of asset. nevertheless, it is necessary

to understand that if the taxpayer bought the land actually for the resale purpose and

developmental purpose, then the profits that arise from the sale of land maybe treated taxable

as ordinary income irrespective of the sale of land.

Profits originating from the carrying the income deriving activity or in relation to the

land that is purchased prior to introduction of CGT or Pre-CGT assets is mainly included for

assessment purpose under “section 15-15, ITAA 1997” (Bankman et al., 2018). Making any

kind of capital improvements on the pre-CGT asset attracts capital gains tax.

The law court in “Scottish Australian Mining Co Ltd v FC of T (1950)” held that the

taxpayer derived significant amount of profit from the sale of subdivided lots (Schmalbeck et

al., 2015). The commissioner held that taxpayer taxable relating to the profits derived from

sale of several lots of land. The commissioner stated that the profits were considered taxable

as income each under “section 25 (1), ITAA 1936” as income earned from business of land

development and under “section 26 (a)” as profits arising from profit making structure.

In another instance of “FCT v Whitfords Beach Pty Ltd (1982)” the taxpayer was

considered taxable for the income made following the sale of several plots (Buenker, 2018).

The commissioner considered the taxpayer taxable under the “section 25 (1), ITAA 1936” as

the profits arising from profit deriving venture.

Once it is established that the activity of purchasing and sale of land gives rise to

profit that is not earned in the ordinary business course, then the income which is in question

will be considered as taxable income under ordinary concepts provided the taxpayer has the

purpose of making profit at the time of acquisition (Mertens & Montiel Olea, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Application

Sam purchased 80 acres of land in 1984 while in 1995 an additional 20 acres of land

was bought by Sam. The land was initially bought for agricultural purpose however after

engaging the real estate agent Sam decided to subdivide the land for residential expansion.

The concept of pre-CGT and post-CGT can be implemented in the case of Sam by stating that

the 80 acres of land that was bought on 1984 will be considered as pre-CGT asset. Any kind

of capital gains made from the sale of 80 acres of land will be exempted from capital gains

tax purpose. While the 20 acres of land was purchased by Sam on February 1995. This

implies that the property is a post-CGT asset and any capital gains made thereon will be

subjected to capital gains tax.

Sam indulged in the property development by rezoning the land in order to fetch the

possible price. These kinds of property development are considered substantial in nature

because it involves the prospect of obtaining large sum of profits from the land. With regard

to the “Taxation Determination TD 97/3” it is necessary to ascertain whether or not the

profits that are derived from the sale of subdivided land constitutes taxable gains under

“subsection 25 (1), ITAA 1936” (Sadiq, 2019). Sam originally bought the land for

agricultural purpose however the motive of deriving profit originated in the later points.

Citing the case of Scottish Australian Mining Co Ltd v FC of T (1950)” a significant

amount of profit has been made by Sam from the disposal of subdivided lots (Schenk, 2017).

Sam will be considered for assessment purpose for the profits that are made from the sale of

land several plots land. Referring to the situation of Sam, the profits will be considered

assessable profits under either the “section 25 (1), ITAA 1936” in the form of income that is

earned from carrying the business of land development or under the “section 26 (a)” in the

form of profits that derived from profit making structure.

Application

Sam purchased 80 acres of land in 1984 while in 1995 an additional 20 acres of land

was bought by Sam. The land was initially bought for agricultural purpose however after

engaging the real estate agent Sam decided to subdivide the land for residential expansion.

The concept of pre-CGT and post-CGT can be implemented in the case of Sam by stating that

the 80 acres of land that was bought on 1984 will be considered as pre-CGT asset. Any kind

of capital gains made from the sale of 80 acres of land will be exempted from capital gains

tax purpose. While the 20 acres of land was purchased by Sam on February 1995. This

implies that the property is a post-CGT asset and any capital gains made thereon will be

subjected to capital gains tax.

Sam indulged in the property development by rezoning the land in order to fetch the

possible price. These kinds of property development are considered substantial in nature

because it involves the prospect of obtaining large sum of profits from the land. With regard

to the “Taxation Determination TD 97/3” it is necessary to ascertain whether or not the

profits that are derived from the sale of subdivided land constitutes taxable gains under

“subsection 25 (1), ITAA 1936” (Sadiq, 2019). Sam originally bought the land for

agricultural purpose however the motive of deriving profit originated in the later points.

Citing the case of Scottish Australian Mining Co Ltd v FC of T (1950)” a significant

amount of profit has been made by Sam from the disposal of subdivided lots (Schenk, 2017).

Sam will be considered for assessment purpose for the profits that are made from the sale of

land several plots land. Referring to the situation of Sam, the profits will be considered

assessable profits under either the “section 25 (1), ITAA 1936” in the form of income that is

earned from carrying the business of land development or under the “section 26 (a)” in the

form of profits that derived from profit making structure.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

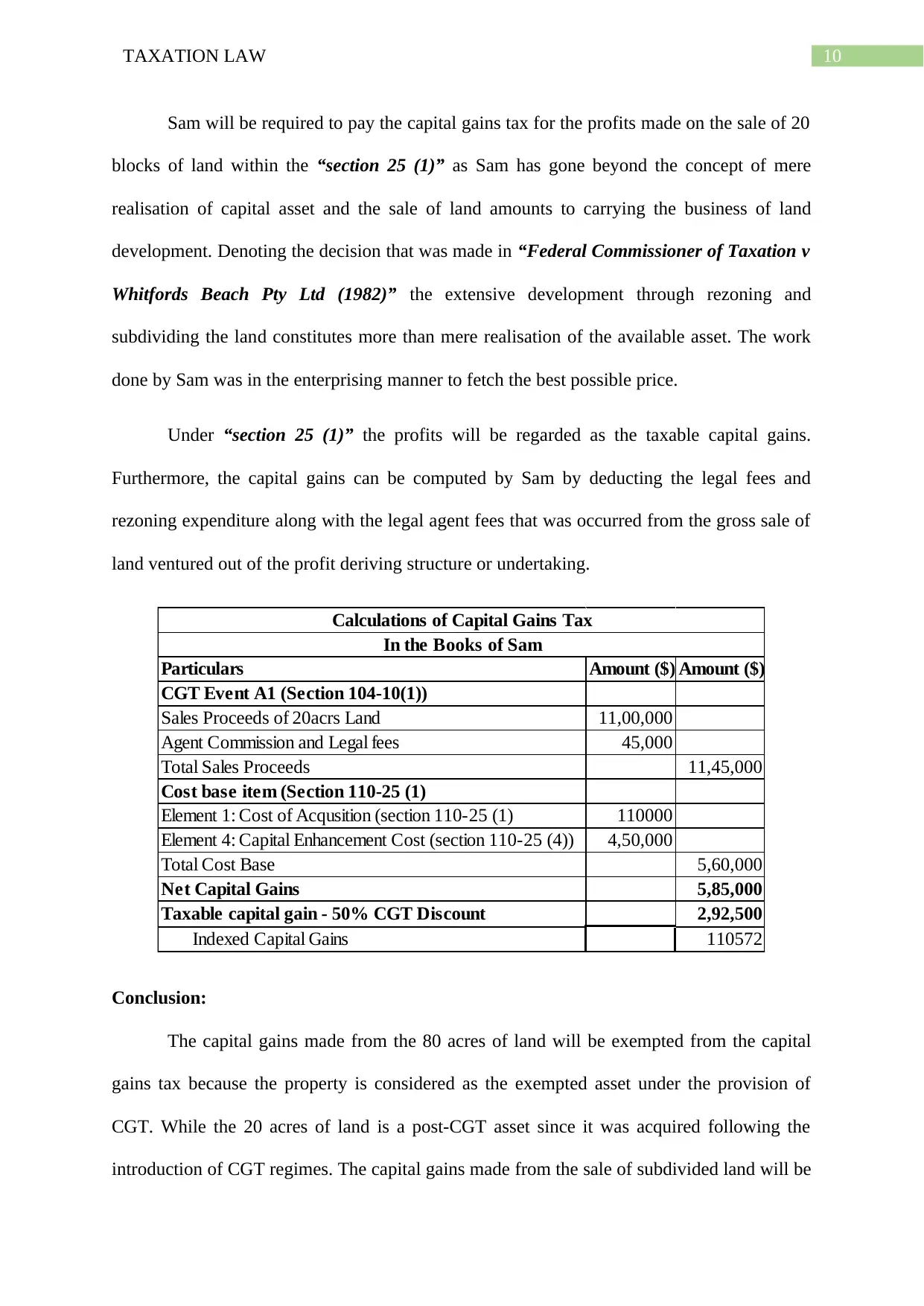

Sam will be required to pay the capital gains tax for the profits made on the sale of 20

blocks of land within the “section 25 (1)” as Sam has gone beyond the concept of mere

realisation of capital asset and the sale of land amounts to carrying the business of land

development. Denoting the decision that was made in “Federal Commissioner of Taxation v

Whitfords Beach Pty Ltd (1982)” the extensive development through rezoning and

subdividing the land constitutes more than mere realisation of the available asset. The work

done by Sam was in the enterprising manner to fetch the best possible price.

Under “section 25 (1)” the profits will be regarded as the taxable capital gains.

Furthermore, the capital gains can be computed by Sam by deducting the legal fees and

rezoning expenditure along with the legal agent fees that was occurred from the gross sale of

land ventured out of the profit deriving structure or undertaking.

Particulars Amount ($) Amount ($)

CGT Event A1 (Section 104-10(1))

Sales Proceeds of 20acrs Land 11,00,000

Agent Commission and Legal fees 45,000

Total Sales Proceeds 11,45,000

Cost base item (Section 110-25 (1)

Element 1: Cost of Acqusition (section 110-25 (1) 110000

Element 4: Capital Enhancement Cost (section 110-25 (4)) 4,50,000

Total Cost Base 5,60,000

Net Capital Gains 5,85,000

Taxable capital gain - 50% CGT Discount 2,92,500

Indexed Capital Gains 110572

Calculations of Capital Gains Tax

In the Books of Sam

Conclusion:

The capital gains made from the 80 acres of land will be exempted from the capital

gains tax because the property is considered as the exempted asset under the provision of

CGT. While the 20 acres of land is a post-CGT asset since it was acquired following the

introduction of CGT regimes. The capital gains made from the sale of subdivided land will be

Sam will be required to pay the capital gains tax for the profits made on the sale of 20

blocks of land within the “section 25 (1)” as Sam has gone beyond the concept of mere

realisation of capital asset and the sale of land amounts to carrying the business of land

development. Denoting the decision that was made in “Federal Commissioner of Taxation v

Whitfords Beach Pty Ltd (1982)” the extensive development through rezoning and

subdividing the land constitutes more than mere realisation of the available asset. The work

done by Sam was in the enterprising manner to fetch the best possible price.

Under “section 25 (1)” the profits will be regarded as the taxable capital gains.

Furthermore, the capital gains can be computed by Sam by deducting the legal fees and

rezoning expenditure along with the legal agent fees that was occurred from the gross sale of

land ventured out of the profit deriving structure or undertaking.

Particulars Amount ($) Amount ($)

CGT Event A1 (Section 104-10(1))

Sales Proceeds of 20acrs Land 11,00,000

Agent Commission and Legal fees 45,000

Total Sales Proceeds 11,45,000

Cost base item (Section 110-25 (1)

Element 1: Cost of Acqusition (section 110-25 (1) 110000

Element 4: Capital Enhancement Cost (section 110-25 (4)) 4,50,000

Total Cost Base 5,60,000

Net Capital Gains 5,85,000

Taxable capital gain - 50% CGT Discount 2,92,500

Indexed Capital Gains 110572

Calculations of Capital Gains Tax

In the Books of Sam

Conclusion:

The capital gains made from the 80 acres of land will be exempted from the capital

gains tax because the property is considered as the exempted asset under the provision of

CGT. While the 20 acres of land is a post-CGT asset since it was acquired following the

introduction of CGT regimes. The capital gains made from the sale of subdivided land will be

11TAXATION LAW

considered taxable under the legislative provision of “section 25 (1) of the ITAA 1936” as

the income derived from carrying the business of land development or within the “section 26

(a)” as gains resulting from carrying the profit making venture.

considered taxable under the legislative provision of “section 25 (1) of the ITAA 1936” as

the income derived from carrying the business of land development or within the “section 26

(a)” as gains resulting from carrying the profit making venture.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.