HI6028 Taxation Law Assignment: Creditable Acquisition Analysis

VerifiedAdded on 2022/11/09

|13

|2936

|449

Homework Assignment

AI Summary

This assignment solution for HI6028 Taxation Law delves into the intricacies of Australian taxation, focusing on creditable acquisition, GST, and CGT. The first part examines the determination of input tax credit claims related to creditable acquisitions, analyzing relevant laws like GSTR 2008/1 and the GST Act 1999, and applying these principles to a case study involving City Sky Co. The second part addresses capital gains tax (CGT), exploring deductions, cost base elements, and the CGT implications of selling a block of land, as well as the sale of shares and stamps, referencing relevant legislation such as the ITAA 1997. The assignment demonstrates an understanding of the Australian income tax system, applying taxation principles to real-life problems and interpreting relevant taxation legislations and case law.

Running Head: TAXATION LAW

TAXATION LAW

Name of the Student

Name of the University

Author Note

TAXATION LAW

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Response to requirement 1:........................................................................................................2

Response to requirement 2:........................................................................................................4

References:...............................................................................................................................11

Table of Contents

Response to requirement 1:........................................................................................................2

Response to requirement 2:........................................................................................................4

References:...............................................................................................................................11

2TAXATION LAW

Response to requirement 1:

Issues:

The issues of determination of claims related to input tax credit which originates from

the acquisition of credit is discussed in this case.

Laws:

The transactions of a business related to acquisition or importation of the goods either

completely or for the purpose of credit is mainly dealt by “GSTR 2008/1”. A taxpayer for

getting input tax credit is required here for making creditable acquisition. It is necessary for

the taxpayers to make importation or acquisition wholly or partly for creditable purpose for

making the transaction a creditable acquisition or importation (Brandon 2019). According to

the “GST Act 1999”, a creditable acquisition and creditable importation helps in certification

of input tax credit.

The explanation of creditable acquisition is mentioned in “Div 15”, it deals also with

creditable importations (Martin and O'Connell 2018). The situation where a business is

acquiring anything which is for creditable purpose either fully or partly and a business

supplied with things for taxable purpose is referred to as creditable acquisition according to

“s 11.5, GST Act 1999”. As per “S 11.15”, acquiring of a thing is done by a business for

creditable purpose to the extent the acquired thing is consumed entirely for the purpose of

carrying the enterprise.

A supplier who is manufacturing supplies which are assessable, according to the

“GSTR 2008/1” is to be considered liable to pay GST for those supplies. The supplier enjoys

entitlement of obtaining input tax credit for the acquisition which is made by him related to

the making of the making of the supplies (James 2018). As stated by the court of “CT v HP

Response to requirement 1:

Issues:

The issues of determination of claims related to input tax credit which originates from

the acquisition of credit is discussed in this case.

Laws:

The transactions of a business related to acquisition or importation of the goods either

completely or for the purpose of credit is mainly dealt by “GSTR 2008/1”. A taxpayer for

getting input tax credit is required here for making creditable acquisition. It is necessary for

the taxpayers to make importation or acquisition wholly or partly for creditable purpose for

making the transaction a creditable acquisition or importation (Brandon 2019). According to

the “GST Act 1999”, a creditable acquisition and creditable importation helps in certification

of input tax credit.

The explanation of creditable acquisition is mentioned in “Div 15”, it deals also with

creditable importations (Martin and O'Connell 2018). The situation where a business is

acquiring anything which is for creditable purpose either fully or partly and a business

supplied with things for taxable purpose is referred to as creditable acquisition according to

“s 11.5, GST Act 1999”. As per “S 11.15”, acquiring of a thing is done by a business for

creditable purpose to the extent the acquired thing is consumed entirely for the purpose of

carrying the enterprise.

A supplier who is manufacturing supplies which are assessable, according to the

“GSTR 2008/1” is to be considered liable to pay GST for those supplies. The supplier enjoys

entitlement of obtaining input tax credit for the acquisition which is made by him related to

the making of the making of the supplies (James 2018). As stated by the court of “CT v HP

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Mercantile Pty Ltd (2005)”, the input tax credit will be given to the taxpayer when it is

assured that the credit on the output tax which is to be paid by the taxpayer is not included on

the sum in which the taxpayer has already paid tax at certain levels. It is to be assured by the

input tax credits that the purchase price in which GST is included, for the acquisition purpose

provide the acquisition is done only for the purpose of the business. The supplier who is

engaged in making supplies which are taxable will be responsible for the GST as well (Zu

2018). The entitlement to claim input tax credit is given to the supplier related to the

acquisition for manufacturing the taxable supplies.

The entities which are registered under GST are eligible to acquire the entitlement of

input tax credit related to creditable acquisition. When a company has made a creditable

acquisition either completely or partly for the purpose of credit is referred to be a creditable

acquisition made by that company as per the “sec 11.5, ITAA 1997”. Mostly, it is important

to identify the things that are acquired, are acquired to carry on the activities of the business

or not. For example, a shoe has been acquired by a business and it is sold from its shop

(Black 2018). Thus, it is clear that the company has acquired the shoe during the time of its

business operations.

Application:

The company here in this paper is City Sky Co. It is a property development and

investment company. A vacant land has been acquired by the company with the intention of

building approximately 15 apartments for selling purpose. This acquisition of purchase of

land is treated as creditable acquisition. The reason for the same is due to the acquirement of

the land took place for creditable purpose only. As referred to “s11.5, GST Act 1999”, it can

be said the vacant land acquired by City Sky Co for the purpose related to creditable and the

Mercantile Pty Ltd (2005)”, the input tax credit will be given to the taxpayer when it is

assured that the credit on the output tax which is to be paid by the taxpayer is not included on

the sum in which the taxpayer has already paid tax at certain levels. It is to be assured by the

input tax credits that the purchase price in which GST is included, for the acquisition purpose

provide the acquisition is done only for the purpose of the business. The supplier who is

engaged in making supplies which are taxable will be responsible for the GST as well (Zu

2018). The entitlement to claim input tax credit is given to the supplier related to the

acquisition for manufacturing the taxable supplies.

The entities which are registered under GST are eligible to acquire the entitlement of

input tax credit related to creditable acquisition. When a company has made a creditable

acquisition either completely or partly for the purpose of credit is referred to be a creditable

acquisition made by that company as per the “sec 11.5, ITAA 1997”. Mostly, it is important

to identify the things that are acquired, are acquired to carry on the activities of the business

or not. For example, a shoe has been acquired by a business and it is sold from its shop

(Black 2018). Thus, it is clear that the company has acquired the shoe during the time of its

business operations.

Application:

The company here in this paper is City Sky Co. It is a property development and

investment company. A vacant land has been acquired by the company with the intention of

building approximately 15 apartments for selling purpose. This acquisition of purchase of

land is treated as creditable acquisition. The reason for the same is due to the acquirement of

the land took place for creditable purpose only. As referred to “s11.5, GST Act 1999”, it can

be said the vacant land acquired by City Sky Co for the purpose related to creditable and the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

apartment constructed on the same land is for sale which is to be treated as a taxable purpose

only (Hoseini 2018).

According to “s 11.15, GST Act 1999”, the business of City Sky Co usually deals

with acquirement of vacant land for the event of creditable purpose. It will be treated as

creditable purpose till the extent the acquired land is entirely used for the carrying the

business of the enterprise (Pesch and Bussiere 2018). As per the “GSTR 2008/1”, the

assessable supplies manufactured by City Sky Co will be assessed for GST. The supplies

include those supplies which are supplied to the apartments of the vacant land. Referred to

the circumstantial situation of “CT v HP Mercantile Pty Ltd (2005)”, City Sky Co has made

the acquisition entirely for the purpose of business so it will be eligible for receiving the input

tax credit for creditable acquisition (Ingles and Stewart 2018). Moreover, the company uses

the land acquired for creditable acquisition for creditable purpose either partly or fully. There

is also a relation of adequate between the acquired land of the company and the business

activities of the company. This is due to the acquisition of the vacant land was done by the

company for selling purposes for carrying its business.

Conclusion:

Supporting the above discussion, it can be concluded that City Sky Co is eligible for

claiming input tax credit for the purpose of creditable acquisition of the vacant land according

to “sec 11-15, GST Act 1999”. The company has acquired the vacant land for the business of

selling during the course of the business.

Response to requirement 2:

Sale of block of land $ 1,000,000:

The deduction related to some specific purposes is obtained by a taxpayer for the

property which is available for rent or has been rent out already. However, there are few

apartment constructed on the same land is for sale which is to be treated as a taxable purpose

only (Hoseini 2018).

According to “s 11.15, GST Act 1999”, the business of City Sky Co usually deals

with acquirement of vacant land for the event of creditable purpose. It will be treated as

creditable purpose till the extent the acquired land is entirely used for the carrying the

business of the enterprise (Pesch and Bussiere 2018). As per the “GSTR 2008/1”, the

assessable supplies manufactured by City Sky Co will be assessed for GST. The supplies

include those supplies which are supplied to the apartments of the vacant land. Referred to

the circumstantial situation of “CT v HP Mercantile Pty Ltd (2005)”, City Sky Co has made

the acquisition entirely for the purpose of business so it will be eligible for receiving the input

tax credit for creditable acquisition (Ingles and Stewart 2018). Moreover, the company uses

the land acquired for creditable acquisition for creditable purpose either partly or fully. There

is also a relation of adequate between the acquired land of the company and the business

activities of the company. This is due to the acquisition of the vacant land was done by the

company for selling purposes for carrying its business.

Conclusion:

Supporting the above discussion, it can be concluded that City Sky Co is eligible for

claiming input tax credit for the purpose of creditable acquisition of the vacant land according

to “sec 11-15, GST Act 1999”. The company has acquired the vacant land for the business of

selling during the course of the business.

Response to requirement 2:

Sale of block of land $ 1,000,000:

The deduction related to some specific purposes is obtained by a taxpayer for the

property which is available for rent or has been rent out already. However, there are few

5TAXATION LAW

expenses which are capital in nature are exempted from deductions (McCluskey and Franzsen

2017). Deductions like cost incurred for selling or acquiring the property of investment is

exempted from deduction and the taxpayer cannot claim for the deduction of the same. These

costs include advertisement costs, cost of conveyance and stamp duty. Nevertheless, in the

cost base of property these costs are added for CGT purpose.

The CGT provision is applicable on CGT assets which are purchased after 20th

September, 1985. Due to this reason the time of CGT asset is supposed to be utmost relevant.

Similarly, the acquisition date is also important for a taxpayer who is holding an asset for

more than a time period of 12 months before the assets are being sold under “CGT event A1”

(Gordon and Kopczuk 2014). A taxpayer holding a CGT asset is eligible for cost base

indexation or discount on capital gains if it is held for a time period of more than 12 months.

Tangible assets like land and building, intangible assets like goodwill and shares are certain

instances of the same.

Most of the events of CGT is related to the comparison between the receipts of capital

proceeds and the cost base. Computation of net capital gains is done with the help of cost

base. A capital gain is said to take place when the capital proceeds of assets exceed cost base

of assets. According to the “sec 116-20, ITA Act 1997”, the total money received by a

taxpayer or allowed with respect to an event of CGT to a taxpayer represents the capital

proceeds that took place due to CGT event (Harding 2014).

There are five elements of cost base assets. The total of these five base elements

forms the cost base assets. These five elements are discussed as per “sec 110-25 (1)” –

First Element- The purchase price of an item is included in this element.

Second Element- This includes the costs of lawyer fees, stamp duty, transfer fees. These are

known as incident costs of the asset (Mertens and Montiel Olea 2018).

expenses which are capital in nature are exempted from deductions (McCluskey and Franzsen

2017). Deductions like cost incurred for selling or acquiring the property of investment is

exempted from deduction and the taxpayer cannot claim for the deduction of the same. These

costs include advertisement costs, cost of conveyance and stamp duty. Nevertheless, in the

cost base of property these costs are added for CGT purpose.

The CGT provision is applicable on CGT assets which are purchased after 20th

September, 1985. Due to this reason the time of CGT asset is supposed to be utmost relevant.

Similarly, the acquisition date is also important for a taxpayer who is holding an asset for

more than a time period of 12 months before the assets are being sold under “CGT event A1”

(Gordon and Kopczuk 2014). A taxpayer holding a CGT asset is eligible for cost base

indexation or discount on capital gains if it is held for a time period of more than 12 months.

Tangible assets like land and building, intangible assets like goodwill and shares are certain

instances of the same.

Most of the events of CGT is related to the comparison between the receipts of capital

proceeds and the cost base. Computation of net capital gains is done with the help of cost

base. A capital gain is said to take place when the capital proceeds of assets exceed cost base

of assets. According to the “sec 116-20, ITA Act 1997”, the total money received by a

taxpayer or allowed with respect to an event of CGT to a taxpayer represents the capital

proceeds that took place due to CGT event (Harding 2014).

There are five elements of cost base assets. The total of these five base elements

forms the cost base assets. These five elements are discussed as per “sec 110-25 (1)” –

First Element- The purchase price of an item is included in this element.

Second Element- This includes the costs of lawyer fees, stamp duty, transfer fees. These are

known as incident costs of the asset (Mertens and Montiel Olea 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Third Element- These costs are non-capital cost of ownership of assets like repairs, land tax,

rates. The assets must have been purchased after 20/8/1991.

Fourth Element- This element comprises costs of capital improvement for improving the

value of the assets.

Fifth Element- This has the cost of capital expenses which is incurred for preserving or for

defending the title of the assets of the taxpayers.

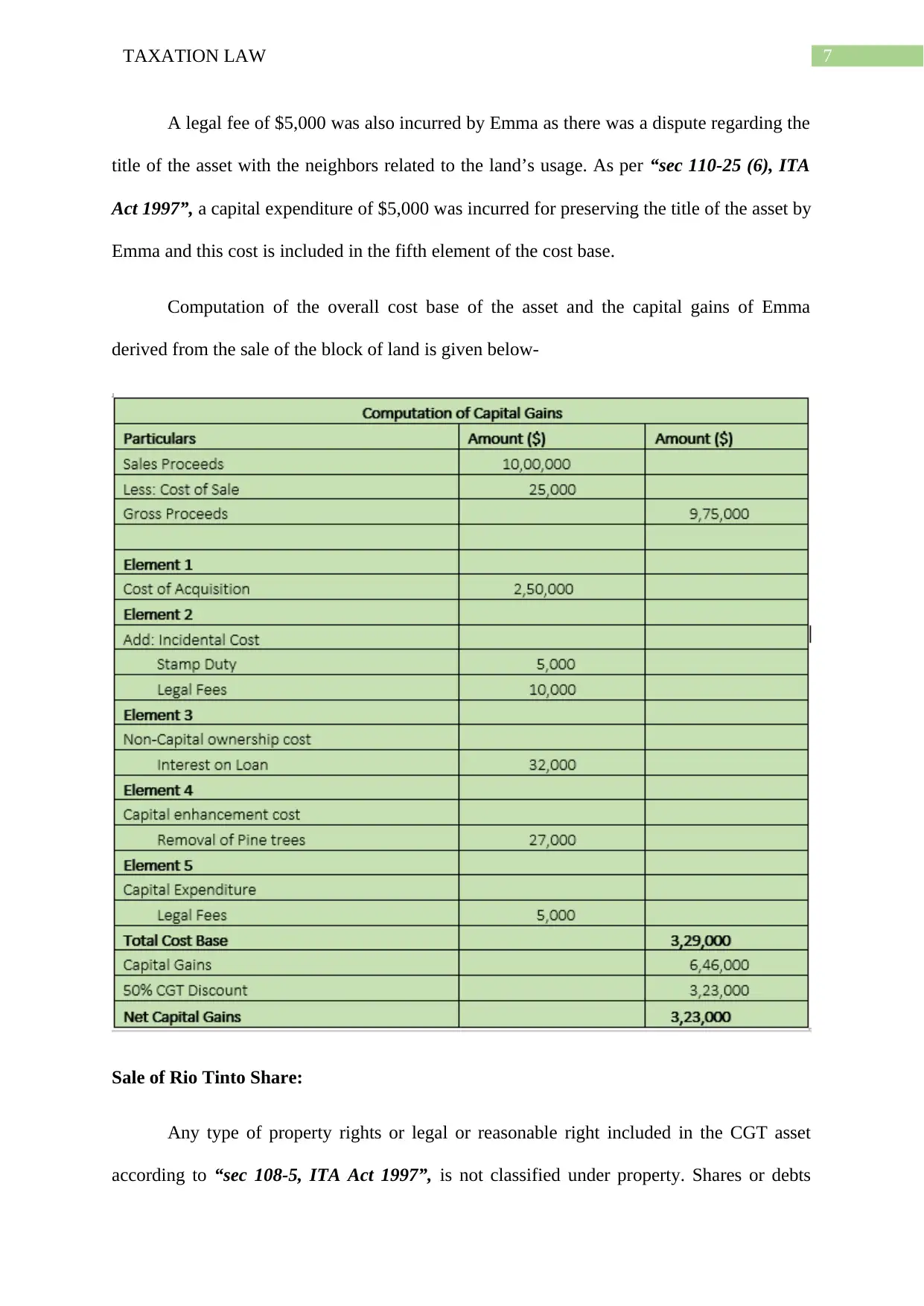

Emma owns a block of land which was purchased by her for $250,000. She has

decided to that block of land for $1,000,000. As per “sec 104-10 (1)”, this event is to be

considered as the “CGT event A1” (Choudhary, Koester and Shevlin 2016). The first element

is comprised of the purchase price which is the payment made for acquiring the asset and

under the first element comes the cost base cost of the asset. Similarly, the cost base item

comes under the second element under “sec 110-25 (1)”. The incidental cost is also included

in this element which includes legal fees costing $10,000 and stamp duty which costs $5,000.

During the ownership held by Emma related to the block of land, certain expenses

were made by Emma which are the incidental expenses like rates, council water expenses,

insurance and interest on land that amounted to $54,000. These are the cost of ownership and

it should be included in the third element of the cost base related to the block of land as it is

exempted from deduction under income.

Before the land was put on sale by Emma, she had to take out the pine trees which

were on the land and for that she had to incur expenses. The cost of taking out those trees

falls under capital enhancement cost and preservation cost which amounted $22,000. Emma

had to undertake the costs in order to preserve the value of the assets and it is included under

“sec 110-25 (5), ITA Act 1997” as well as the cost base fourth element (Santhanam 2016).

Third Element- These costs are non-capital cost of ownership of assets like repairs, land tax,

rates. The assets must have been purchased after 20/8/1991.

Fourth Element- This element comprises costs of capital improvement for improving the

value of the assets.

Fifth Element- This has the cost of capital expenses which is incurred for preserving or for

defending the title of the assets of the taxpayers.

Emma owns a block of land which was purchased by her for $250,000. She has

decided to that block of land for $1,000,000. As per “sec 104-10 (1)”, this event is to be

considered as the “CGT event A1” (Choudhary, Koester and Shevlin 2016). The first element

is comprised of the purchase price which is the payment made for acquiring the asset and

under the first element comes the cost base cost of the asset. Similarly, the cost base item

comes under the second element under “sec 110-25 (1)”. The incidental cost is also included

in this element which includes legal fees costing $10,000 and stamp duty which costs $5,000.

During the ownership held by Emma related to the block of land, certain expenses

were made by Emma which are the incidental expenses like rates, council water expenses,

insurance and interest on land that amounted to $54,000. These are the cost of ownership and

it should be included in the third element of the cost base related to the block of land as it is

exempted from deduction under income.

Before the land was put on sale by Emma, she had to take out the pine trees which

were on the land and for that she had to incur expenses. The cost of taking out those trees

falls under capital enhancement cost and preservation cost which amounted $22,000. Emma

had to undertake the costs in order to preserve the value of the assets and it is included under

“sec 110-25 (5), ITA Act 1997” as well as the cost base fourth element (Santhanam 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

A legal fee of $5,000 was also incurred by Emma as there was a dispute regarding the

title of the asset with the neighbors related to the land’s usage. As per “sec 110-25 (6), ITA

Act 1997”, a capital expenditure of $5,000 was incurred for preserving the title of the asset by

Emma and this cost is included in the fifth element of the cost base.

Computation of the overall cost base of the asset and the capital gains of Emma

derived from the sale of the block of land is given below-

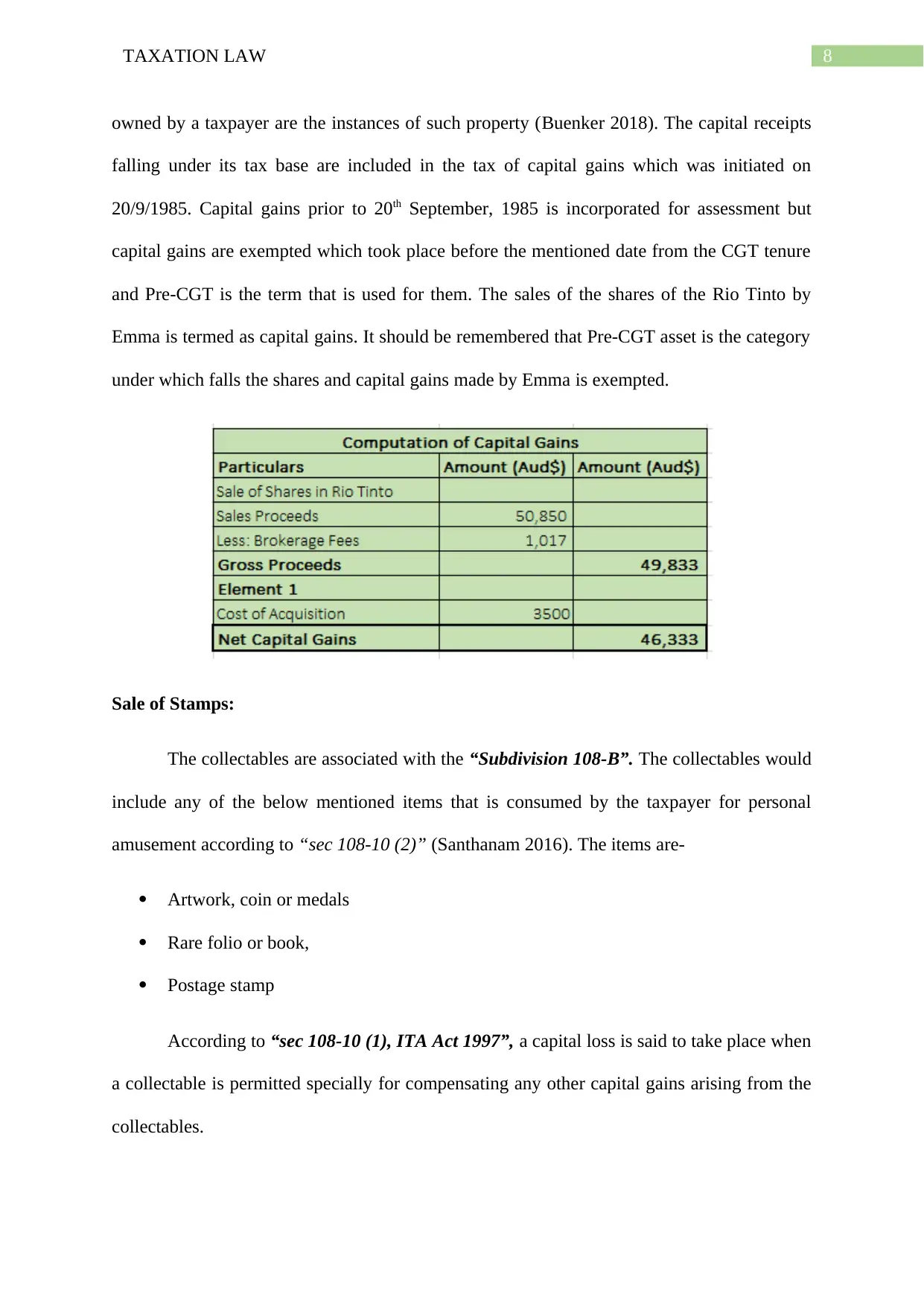

Sale of Rio Tinto Share:

Any type of property rights or legal or reasonable right included in the CGT asset

according to “sec 108-5, ITA Act 1997”, is not classified under property. Shares or debts

A legal fee of $5,000 was also incurred by Emma as there was a dispute regarding the

title of the asset with the neighbors related to the land’s usage. As per “sec 110-25 (6), ITA

Act 1997”, a capital expenditure of $5,000 was incurred for preserving the title of the asset by

Emma and this cost is included in the fifth element of the cost base.

Computation of the overall cost base of the asset and the capital gains of Emma

derived from the sale of the block of land is given below-

Sale of Rio Tinto Share:

Any type of property rights or legal or reasonable right included in the CGT asset

according to “sec 108-5, ITA Act 1997”, is not classified under property. Shares or debts

8TAXATION LAW

owned by a taxpayer are the instances of such property (Buenker 2018). The capital receipts

falling under its tax base are included in the tax of capital gains which was initiated on

20/9/1985. Capital gains prior to 20th September, 1985 is incorporated for assessment but

capital gains are exempted which took place before the mentioned date from the CGT tenure

and Pre-CGT is the term that is used for them. The sales of the shares of the Rio Tinto by

Emma is termed as capital gains. It should be remembered that Pre-CGT asset is the category

under which falls the shares and capital gains made by Emma is exempted.

Sale of Stamps:

The collectables are associated with the “Subdivision 108-B”. The collectables would

include any of the below mentioned items that is consumed by the taxpayer for personal

amusement according to “sec 108-10 (2)” (Santhanam 2016). The items are-

Artwork, coin or medals

Rare folio or book,

Postage stamp

According to “sec 108-10 (1), ITA Act 1997”, a capital loss is said to take place when

a collectable is permitted specially for compensating any other capital gains arising from the

collectables.

owned by a taxpayer are the instances of such property (Buenker 2018). The capital receipts

falling under its tax base are included in the tax of capital gains which was initiated on

20/9/1985. Capital gains prior to 20th September, 1985 is incorporated for assessment but

capital gains are exempted which took place before the mentioned date from the CGT tenure

and Pre-CGT is the term that is used for them. The sales of the shares of the Rio Tinto by

Emma is termed as capital gains. It should be remembered that Pre-CGT asset is the category

under which falls the shares and capital gains made by Emma is exempted.

Sale of Stamps:

The collectables are associated with the “Subdivision 108-B”. The collectables would

include any of the below mentioned items that is consumed by the taxpayer for personal

amusement according to “sec 108-10 (2)” (Santhanam 2016). The items are-

Artwork, coin or medals

Rare folio or book,

Postage stamp

According to “sec 108-10 (1), ITA Act 1997”, a capital loss is said to take place when

a collectable is permitted specially for compensating any other capital gains arising from the

collectables.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

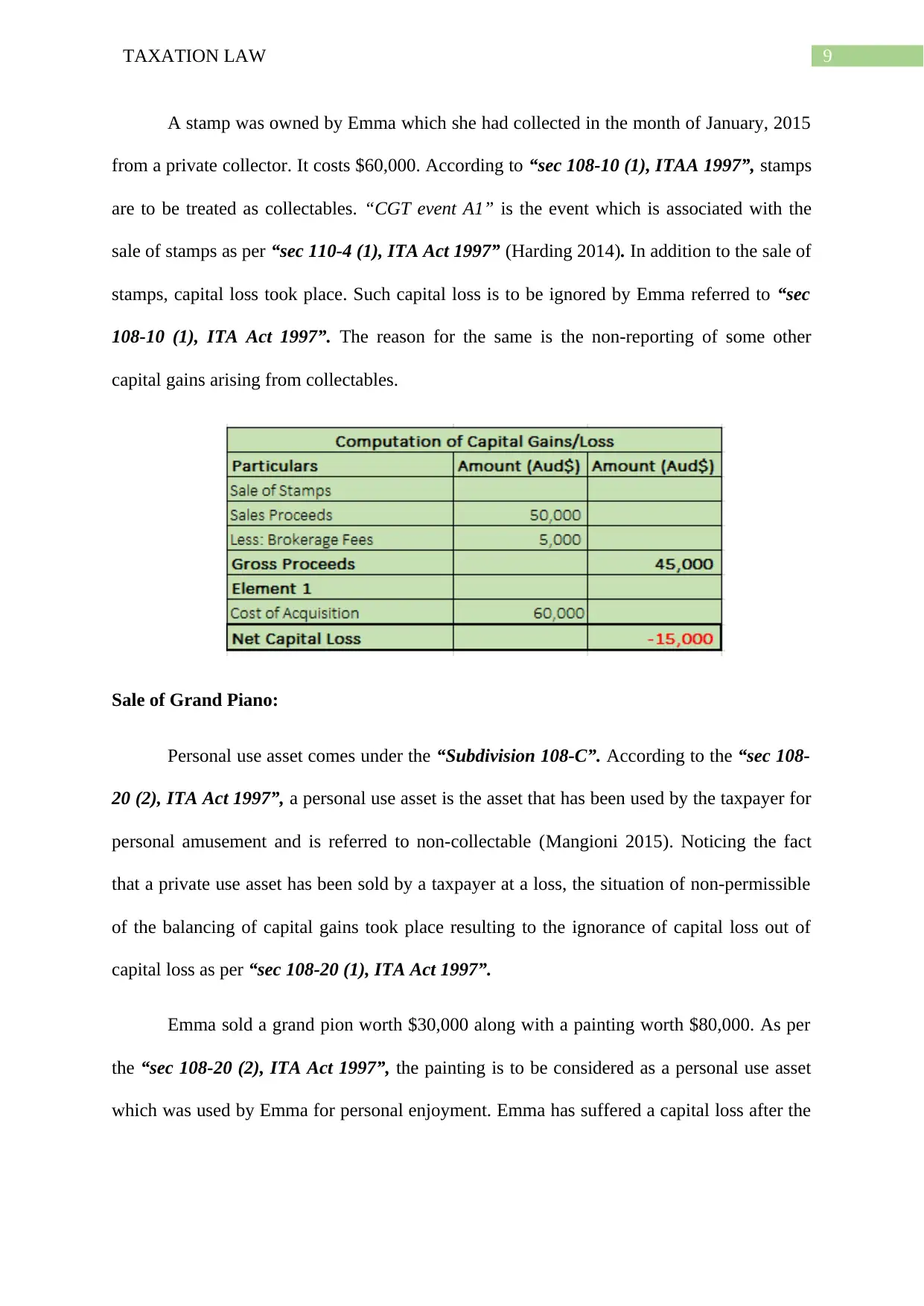

A stamp was owned by Emma which she had collected in the month of January, 2015

from a private collector. It costs $60,000. According to “sec 108-10 (1), ITAA 1997”, stamps

are to be treated as collectables. “CGT event A1” is the event which is associated with the

sale of stamps as per “sec 110-4 (1), ITA Act 1997” (Harding 2014). In addition to the sale of

stamps, capital loss took place. Such capital loss is to be ignored by Emma referred to “sec

108-10 (1), ITA Act 1997”. The reason for the same is the non-reporting of some other

capital gains arising from collectables.

Sale of Grand Piano:

Personal use asset comes under the “Subdivision 108-C”. According to the “sec 108-

20 (2), ITA Act 1997”, a personal use asset is the asset that has been used by the taxpayer for

personal amusement and is referred to non-collectable (Mangioni 2015). Noticing the fact

that a private use asset has been sold by a taxpayer at a loss, the situation of non-permissible

of the balancing of capital gains took place resulting to the ignorance of capital loss out of

capital loss as per “sec 108-20 (1), ITA Act 1997”.

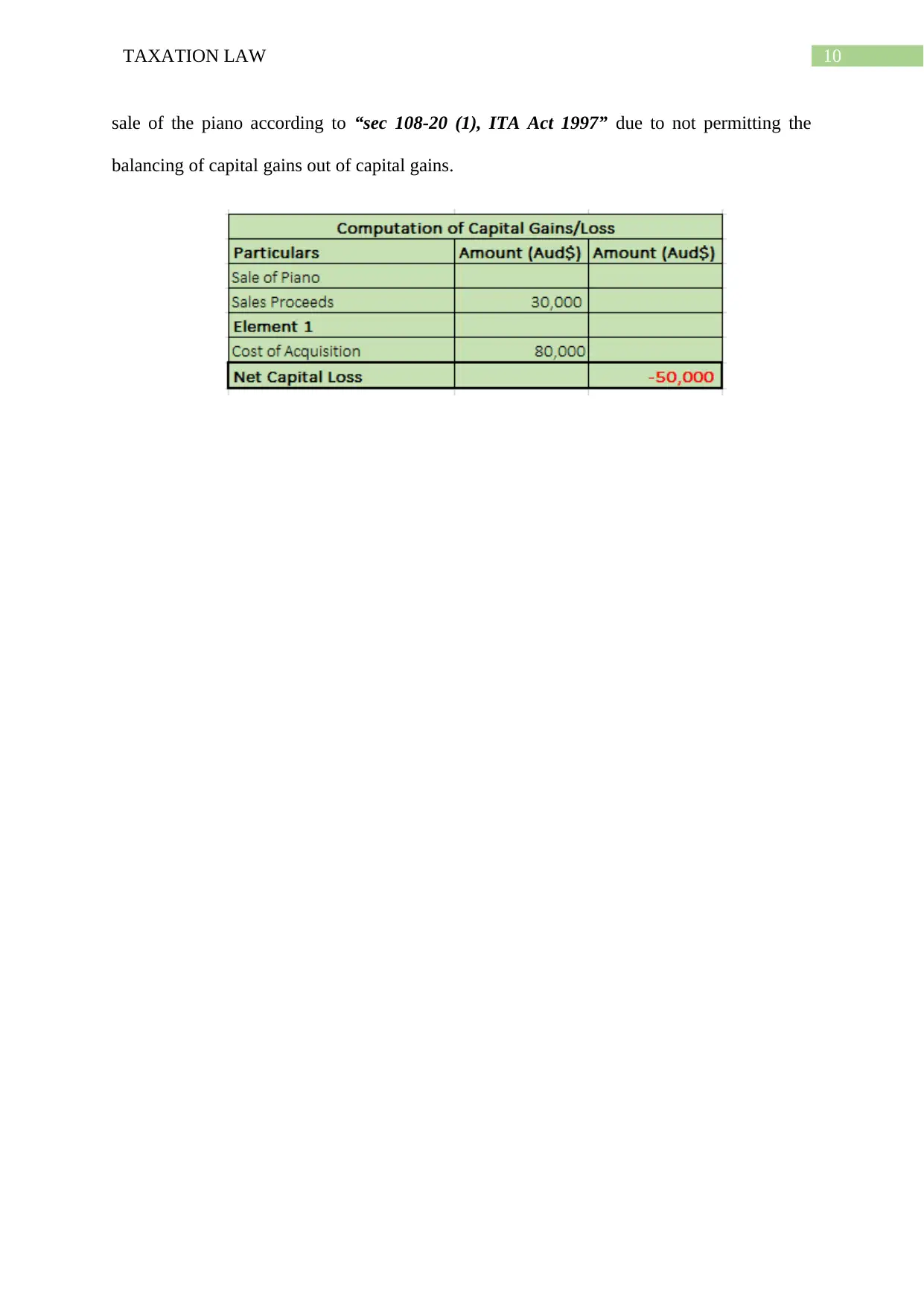

Emma sold a grand pion worth $30,000 along with a painting worth $80,000. As per

the “sec 108-20 (2), ITA Act 1997”, the painting is to be considered as a personal use asset

which was used by Emma for personal enjoyment. Emma has suffered a capital loss after the

A stamp was owned by Emma which she had collected in the month of January, 2015

from a private collector. It costs $60,000. According to “sec 108-10 (1), ITAA 1997”, stamps

are to be treated as collectables. “CGT event A1” is the event which is associated with the

sale of stamps as per “sec 110-4 (1), ITA Act 1997” (Harding 2014). In addition to the sale of

stamps, capital loss took place. Such capital loss is to be ignored by Emma referred to “sec

108-10 (1), ITA Act 1997”. The reason for the same is the non-reporting of some other

capital gains arising from collectables.

Sale of Grand Piano:

Personal use asset comes under the “Subdivision 108-C”. According to the “sec 108-

20 (2), ITA Act 1997”, a personal use asset is the asset that has been used by the taxpayer for

personal amusement and is referred to non-collectable (Mangioni 2015). Noticing the fact

that a private use asset has been sold by a taxpayer at a loss, the situation of non-permissible

of the balancing of capital gains took place resulting to the ignorance of capital loss out of

capital loss as per “sec 108-20 (1), ITA Act 1997”.

Emma sold a grand pion worth $30,000 along with a painting worth $80,000. As per

the “sec 108-20 (2), ITA Act 1997”, the painting is to be considered as a personal use asset

which was used by Emma for personal enjoyment. Emma has suffered a capital loss after the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

sale of the piano according to “sec 108-20 (1), ITA Act 1997” due to not permitting the

balancing of capital gains out of capital gains.

sale of the piano according to “sec 108-20 (1), ITA Act 1997” due to not permitting the

balancing of capital gains out of capital gains.

11TAXATION LAW

References:

Black, C., 2018. Taxation of Intellectual Property Under Domestic Law and Tax Treaties:

Australia. Taxation of Intellectual Property under Domestic Law, EU Law and Tax Treaties",

IBFD: Amsterdam.

Brandon, G., 2019. Who has a liability to pay GST?. Taxation in Australia, 53(7), p.357.

Buenker, J.D., 2018. The Income Tax and the Progressive Era. Routledge.

Choudhary, P., Koester, A. and Shevlin, T., 2016. Measuring income tax accrual

quality. Review of Accounting Studies, 21(1), pp.89-139.

Gordon, R.H. and Kopczuk, W., 2014. The choice of the personal income tax base. Journal

of Public Economics, 118, pp.97-110.

Harding, M., 2014. Personal tax treatment of company cars and commuting expenses.

Hoseini, M., 2018. Value‐Added Tax, Input–Output Linkages and Informality. Economical.

Ingles, D. and Stewart, M., 2018, October. Australia's company tax: Options for fiscally

sustainable reform. In Australian Tax Forum (Vol. 33, No. 1).

James, K., 2018. Applying the GST to imports of low-value goods in Australia. Applying the

GST to imports of low value goods in Australia,(2018), 47.

Mangioni, V., 2015. Land Tax in Australia: Fiscal reform of sub-national government.

Routledge.

Martin, F. and O'Connell, A., 2018. Crowdfunding: What Are the Tax Issues. J. Austl.

Tax'n, 20, p.16.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

References:

Black, C., 2018. Taxation of Intellectual Property Under Domestic Law and Tax Treaties:

Australia. Taxation of Intellectual Property under Domestic Law, EU Law and Tax Treaties",

IBFD: Amsterdam.

Brandon, G., 2019. Who has a liability to pay GST?. Taxation in Australia, 53(7), p.357.

Buenker, J.D., 2018. The Income Tax and the Progressive Era. Routledge.

Choudhary, P., Koester, A. and Shevlin, T., 2016. Measuring income tax accrual

quality. Review of Accounting Studies, 21(1), pp.89-139.

Gordon, R.H. and Kopczuk, W., 2014. The choice of the personal income tax base. Journal

of Public Economics, 118, pp.97-110.

Harding, M., 2014. Personal tax treatment of company cars and commuting expenses.

Hoseini, M., 2018. Value‐Added Tax, Input–Output Linkages and Informality. Economical.

Ingles, D. and Stewart, M., 2018, October. Australia's company tax: Options for fiscally

sustainable reform. In Australian Tax Forum (Vol. 33, No. 1).

James, K., 2018. Applying the GST to imports of low-value goods in Australia. Applying the

GST to imports of low value goods in Australia,(2018), 47.

Mangioni, V., 2015. Land Tax in Australia: Fiscal reform of sub-national government.

Routledge.

Martin, F. and O'Connell, A., 2018. Crowdfunding: What Are the Tax Issues. J. Austl.

Tax'n, 20, p.16.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.