Individual Assignment: Tax Treatment of Cryptocurrencies (ACC304)

VerifiedAdded on 2022/08/23

|7

|789

|16

Homework Assignment

AI Summary

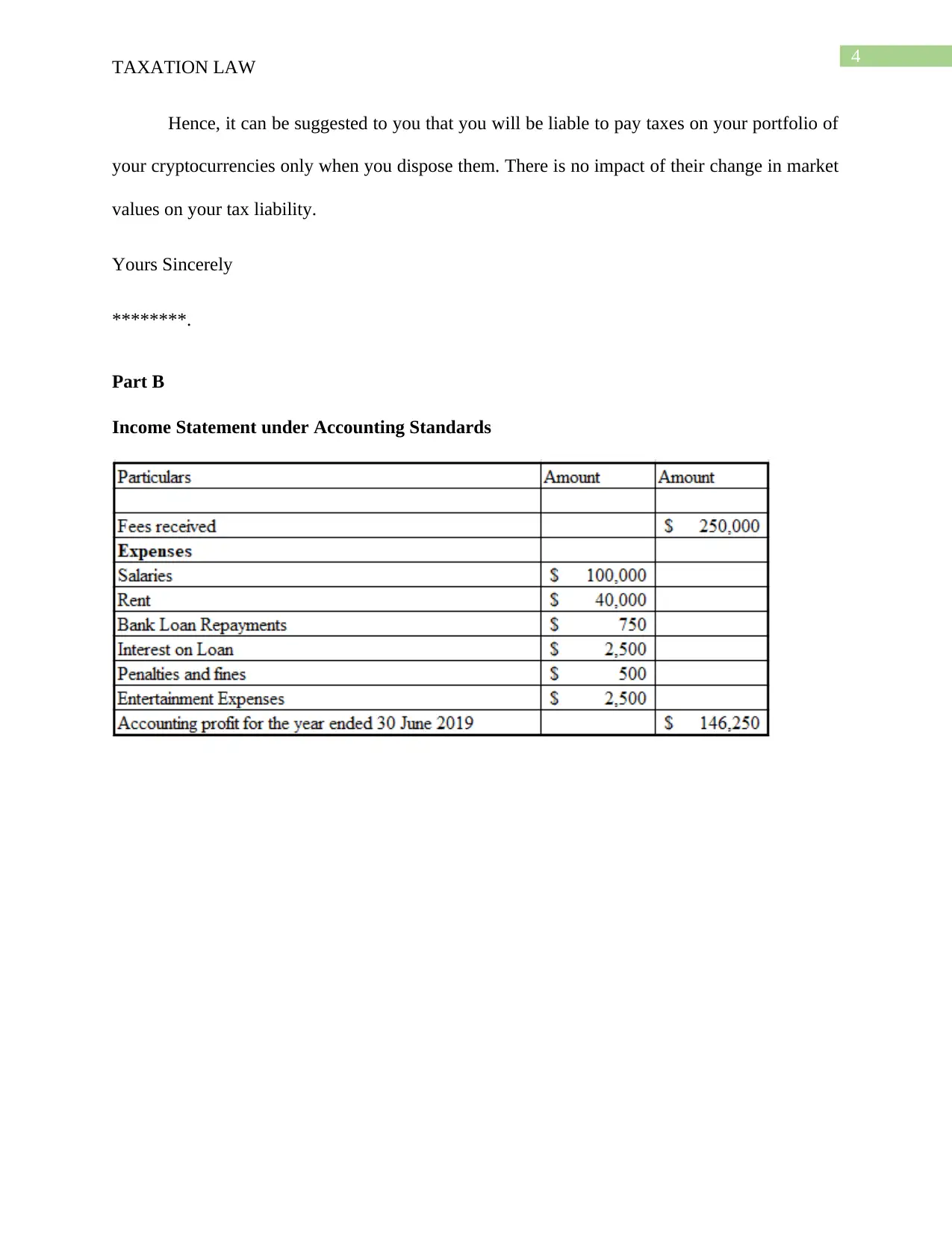

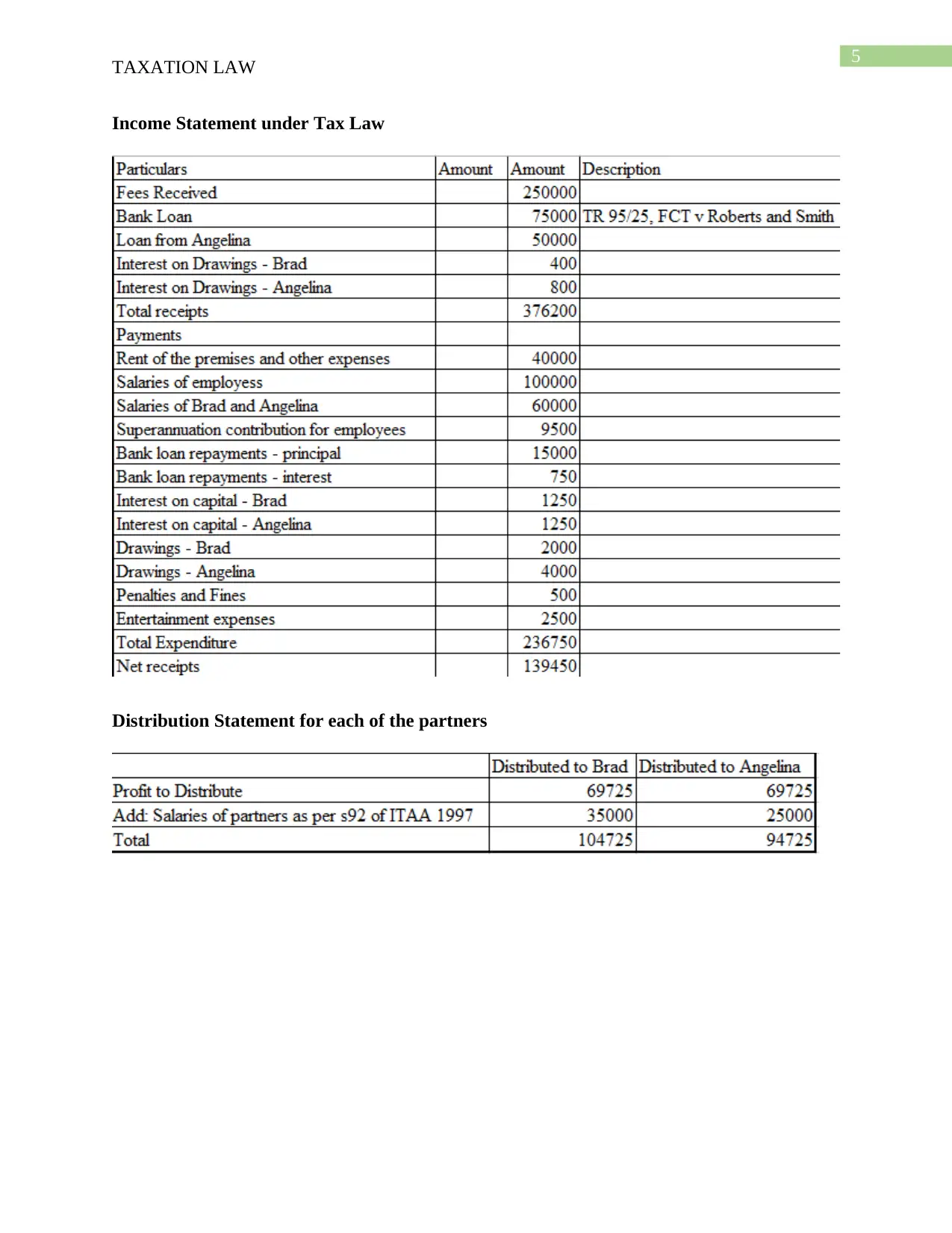

This assignment addresses the tax implications of cryptocurrencies in Australia, focusing on the guidelines provided by the Australian Taxation Office (ATO). It begins with a letter of advice to a client explaining how capital gains tax (CGT) applies to cryptocurrency transactions, including buying, selling, trading, and using cryptocurrencies to purchase goods and services. The letter differentiates between personal use assets and business transactions, clarifying when CGT is levied. The assignment then presents an income statement under accounting standards and tax law, followed by a distribution statement for partners. The provided references include relevant sources such as ATO guidelines and academic articles on cryptocurrency taxation. The assignment covers key aspects of cryptocurrency taxation, including the exchange of cryptocurrencies and the tax implications of holding cryptocurrencies as an investment portfolio. It emphasizes that tax liability arises upon disposal of the cryptocurrency, not from market value fluctuations. This assignment is a comprehensive analysis of cryptocurrency taxation within the Australian context.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.