Taxation Law Assessment 3: Letter of Advice and Partnership Analysis

VerifiedAdded on 2022/08/26

|7

|675

|23

Homework Assignment

AI Summary

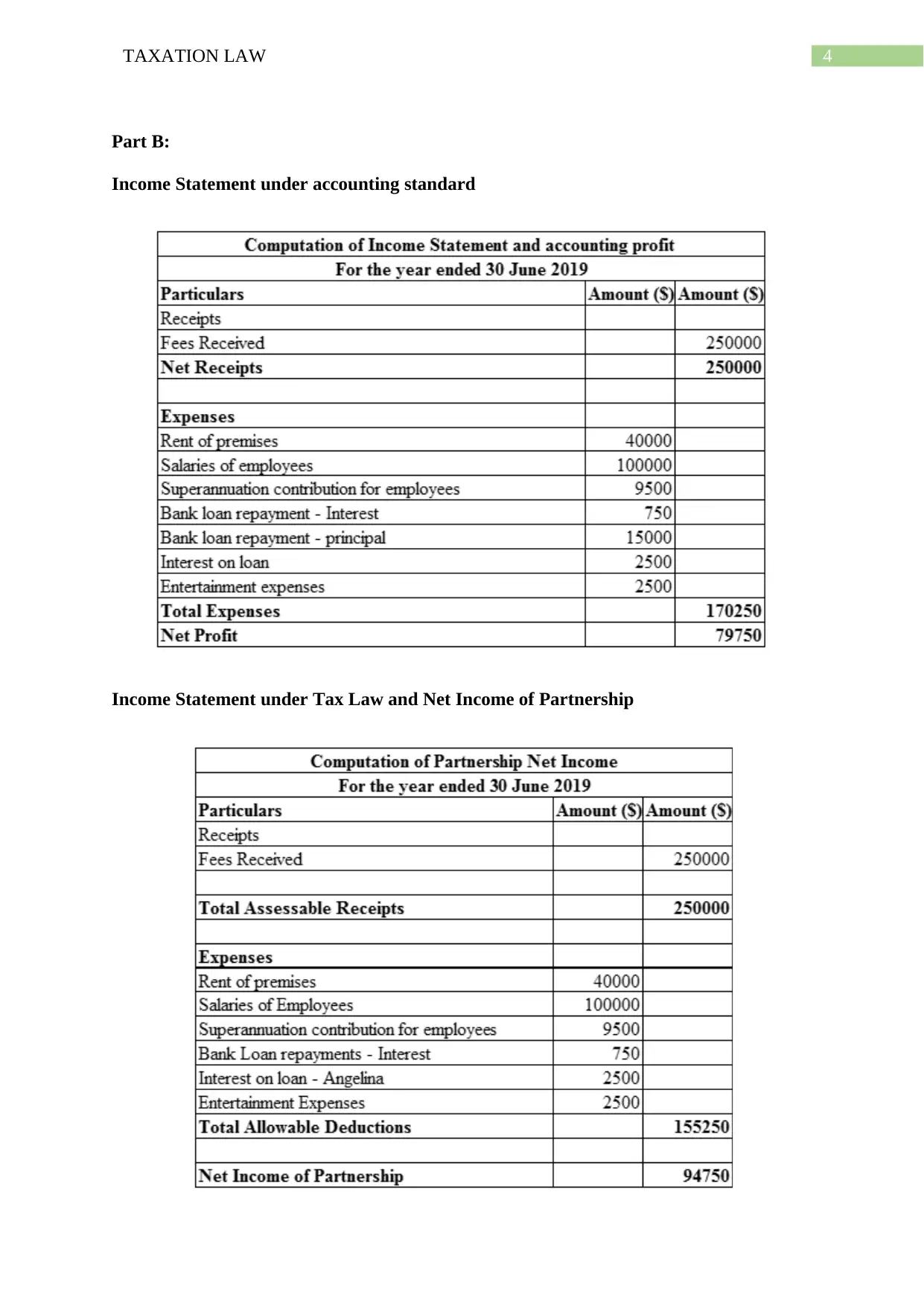

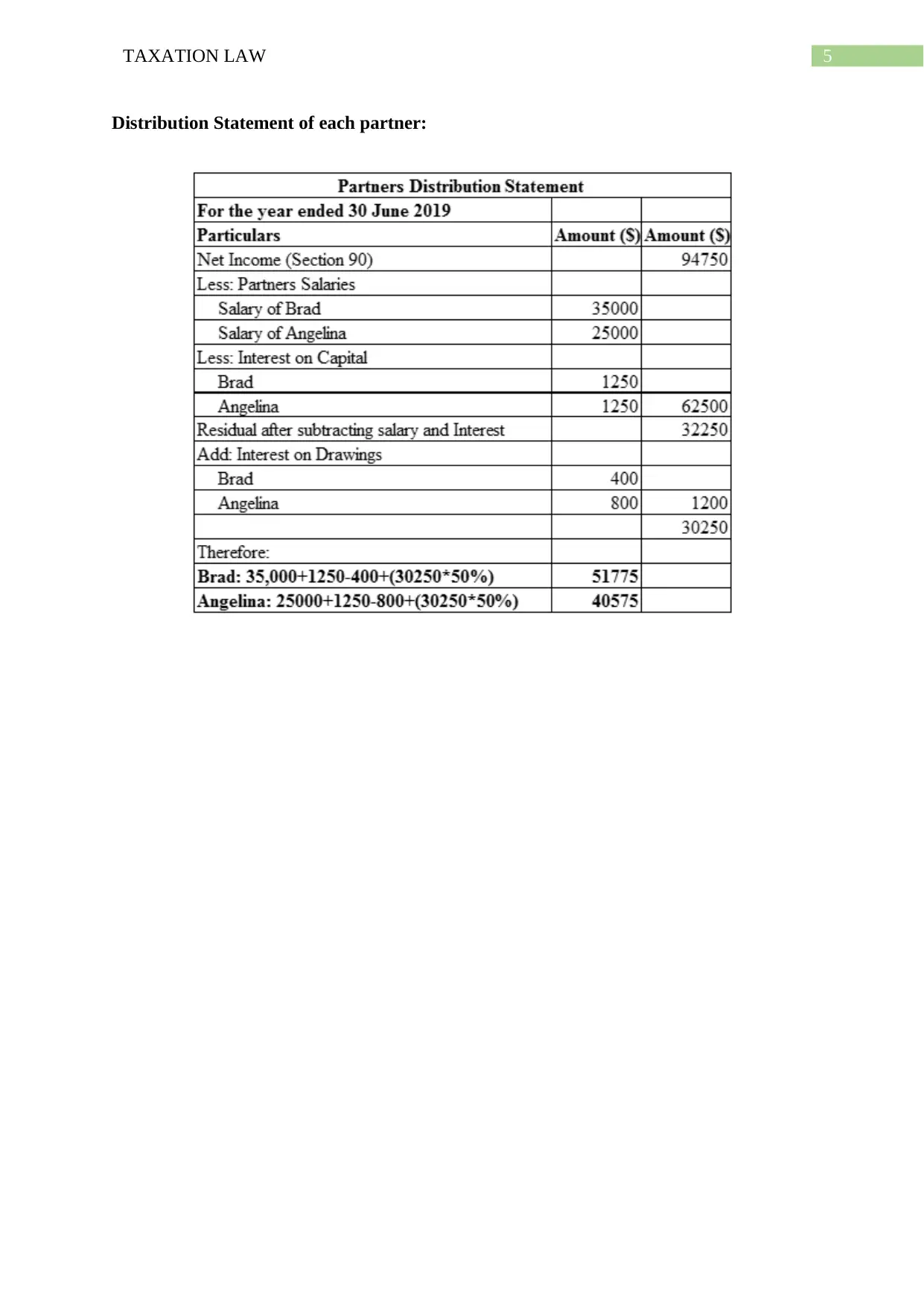

This assignment, completed for ACC304 Taxation Law, presents a comprehensive analysis of tax implications, particularly concerning cryptocurrencies and partnerships. Part A provides a detailed letter of advice addressing the tax treatment of cryptocurrencies, explaining capital gains tax and potential liabilities. It offers guidance on how profits from cryptocurrency trading are taxed either as income or as investments, depending on the portfolio size and the holding period. Part B includes an income statement under accounting standards and tax law, along with a distribution statement for each partner, illustrating the financial aspects. The assignment underscores the importance of understanding tax obligations related to digital assets and provides practical examples to clarify the tax implications of cryptocurrency transactions. References to relevant taxation law resources are also included.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.