Taxation Law Assignment: Depreciation, CGT, Deductions and Taxation

VerifiedAdded on 2021/04/17

|4

|438

|28

Homework Assignment

AI Summary

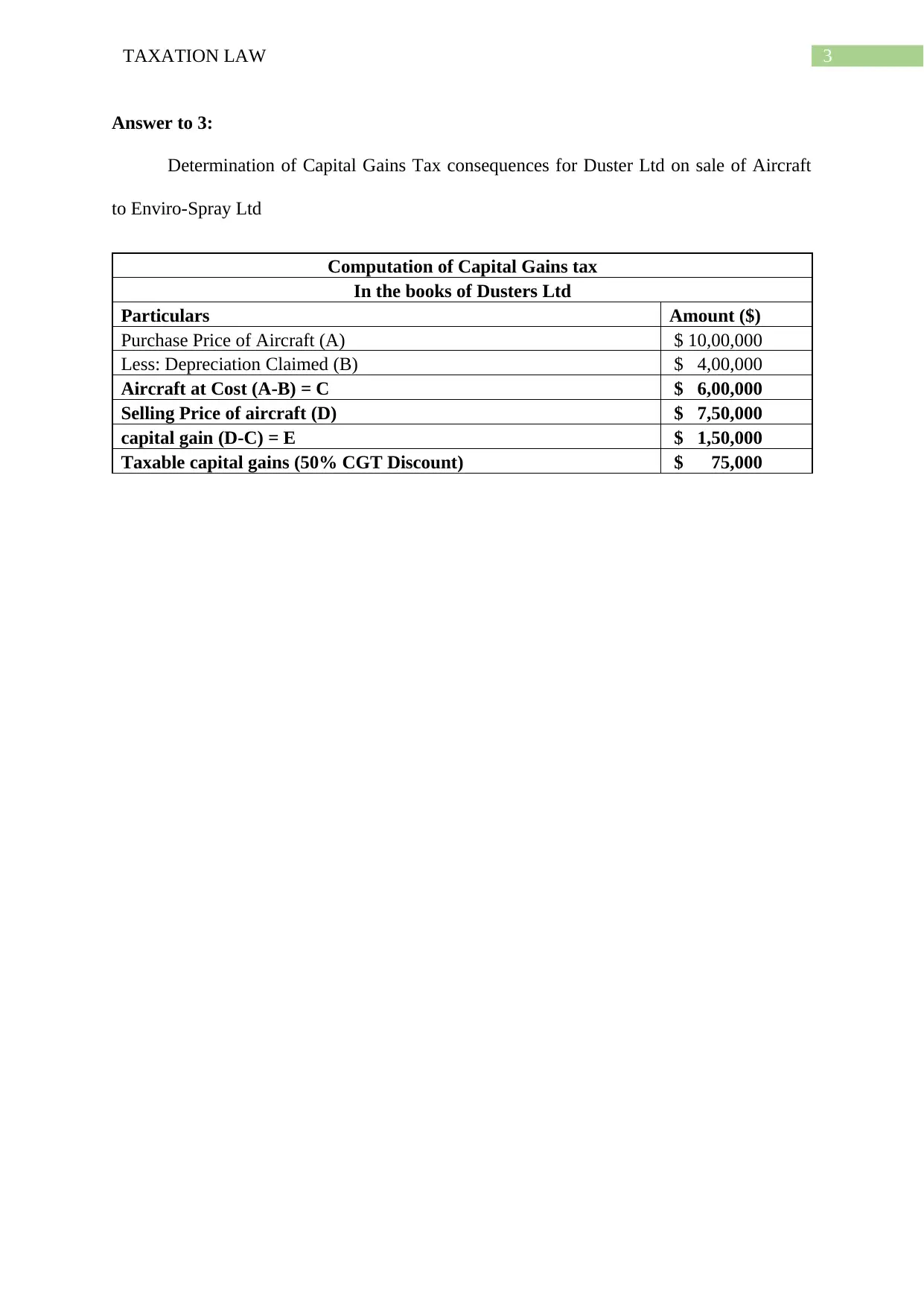

This assignment focuses on taxation law, specifically addressing depreciation, capital gains tax (CGT), and deductions. It analyzes scenarios involving Enviro-Spray Ltd and Duster Ltd, examining the application of relevant sections of the Income Tax Assessment Act 1997 (ITAA 1997). The assignment delves into the deductibility of expenses related to repairs and the implications of replacing equipment. Furthermore, it calculates the CGT consequences for Duster Ltd following the sale of an aircraft, including the determination of capital gains, depreciation, and taxable capital gains, with consideration for the 50% CGT discount. The assignment references legal precedents such as "FC of T v Western Suburbs Cinemas Ltd (1952)" to support its arguments and calculations.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.