Taxation Theory, Practice & Law Report: Capital Gains and FBT Analysis

VerifiedAdded on 2020/10/22

|21

|3480

|181

Report

AI Summary

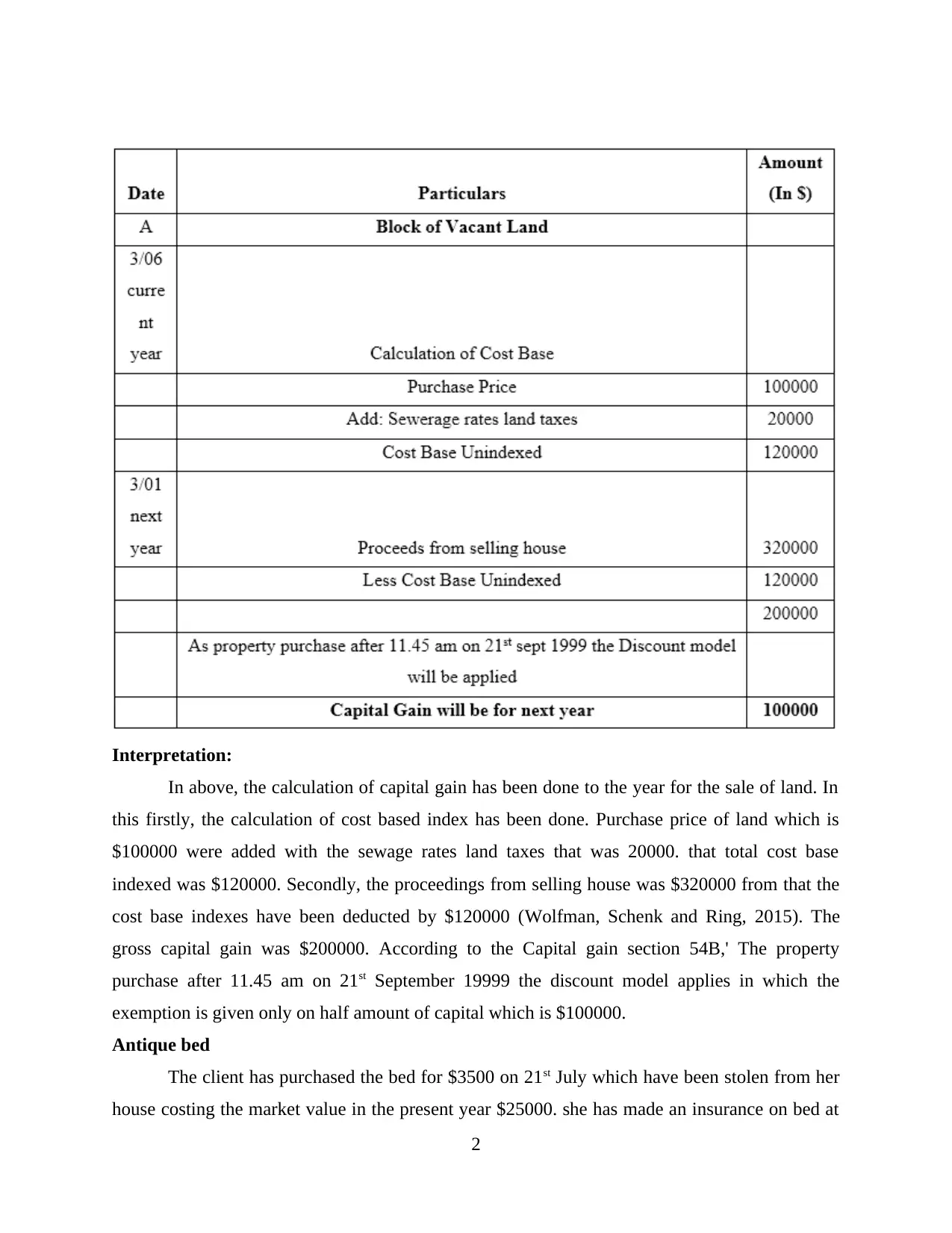

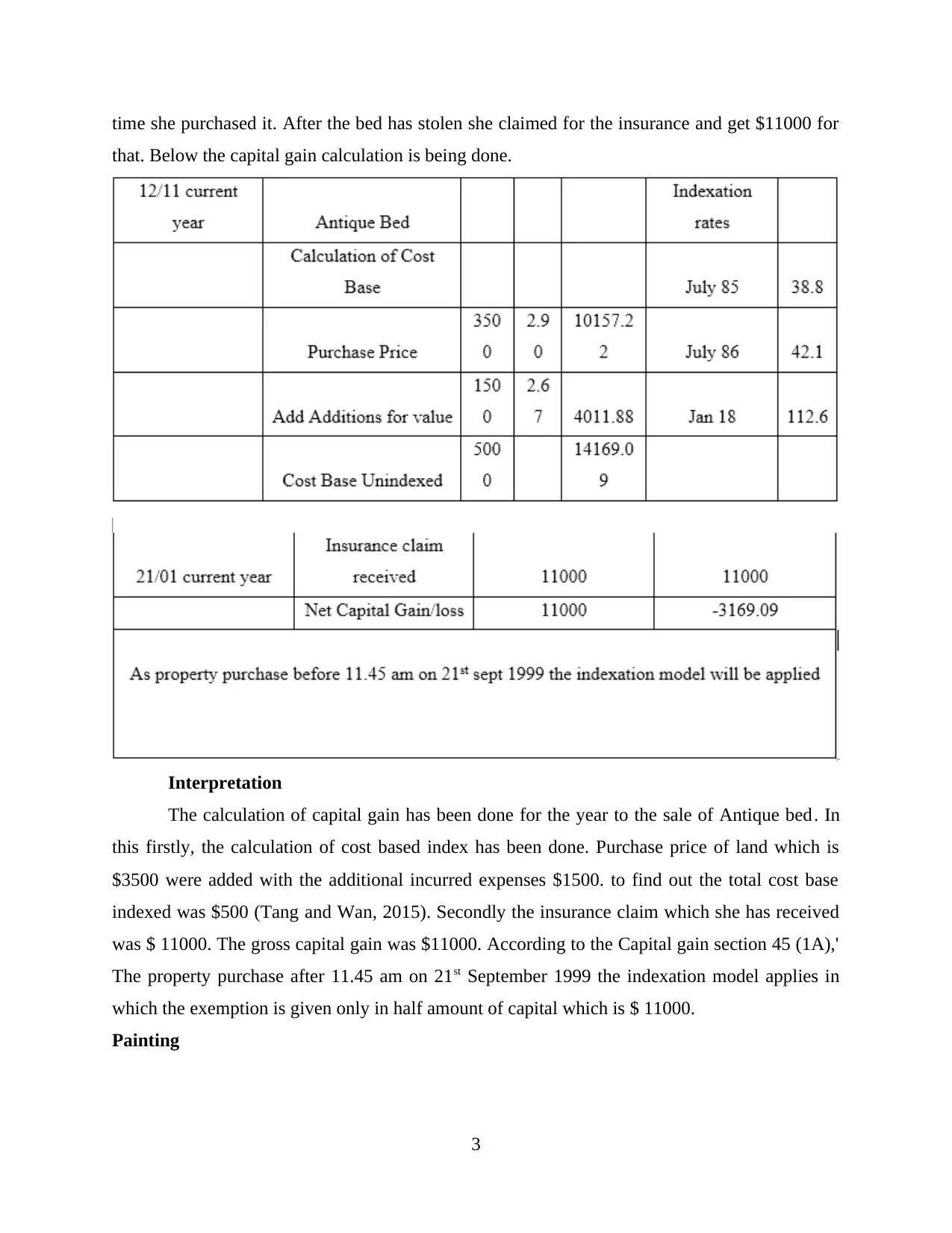

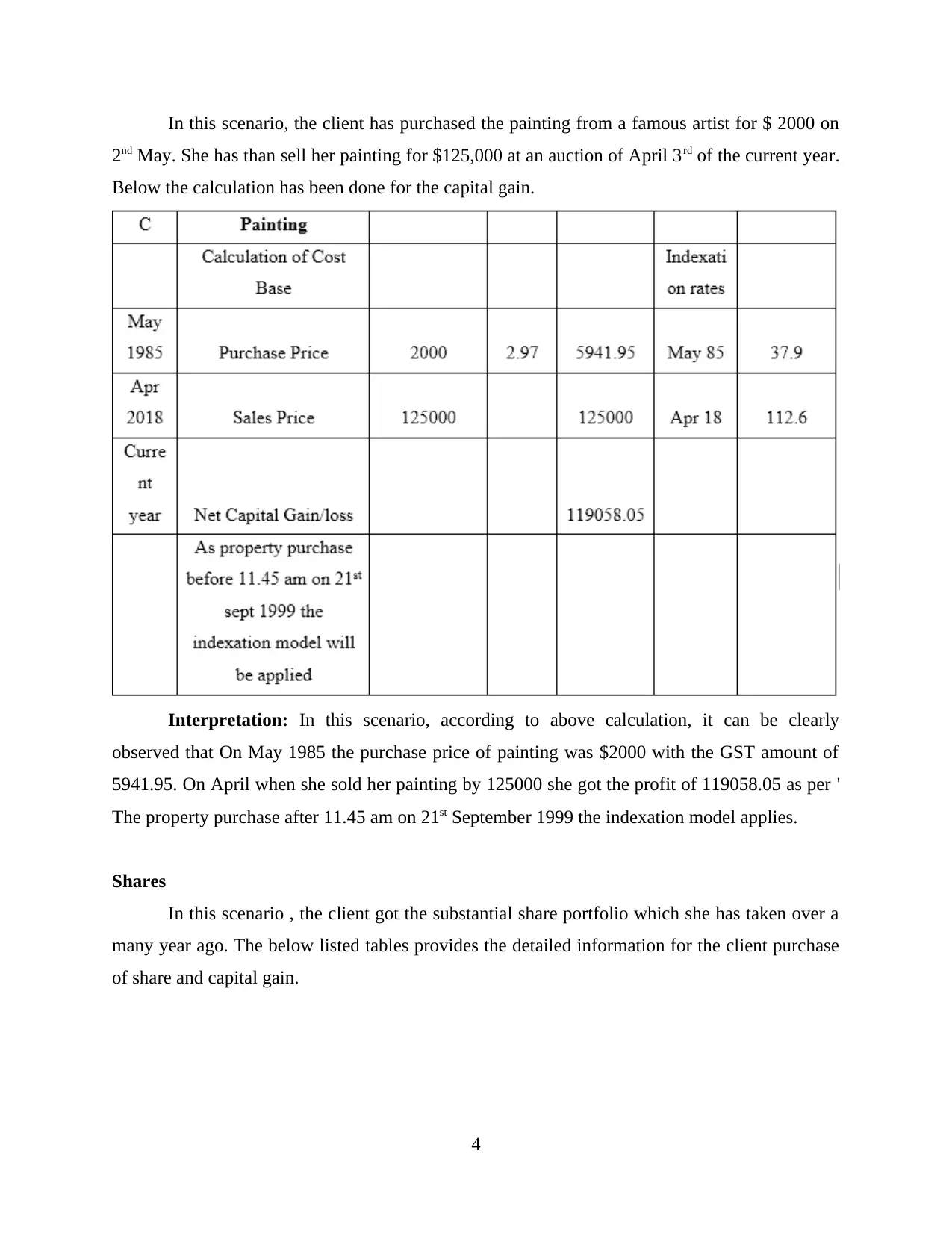

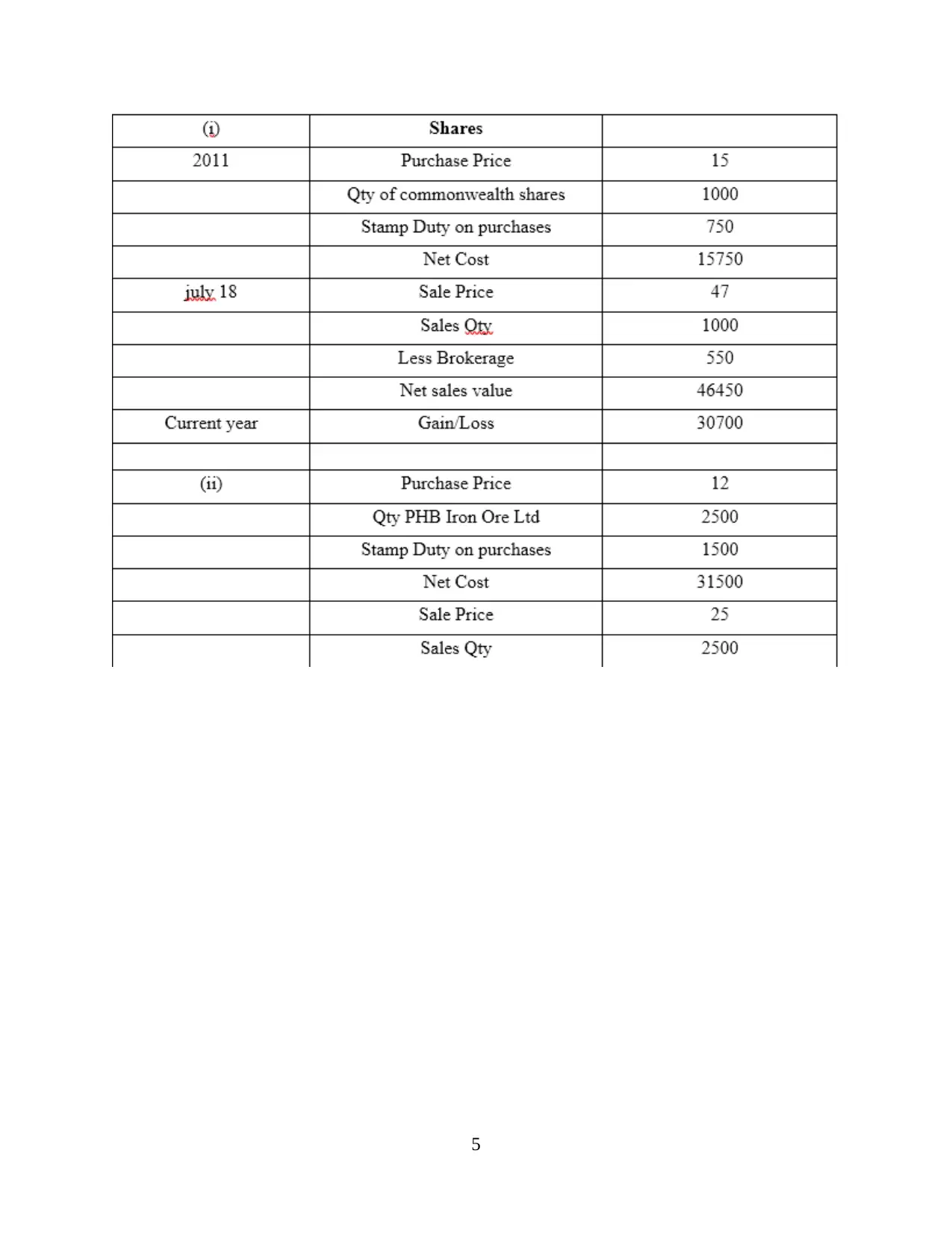

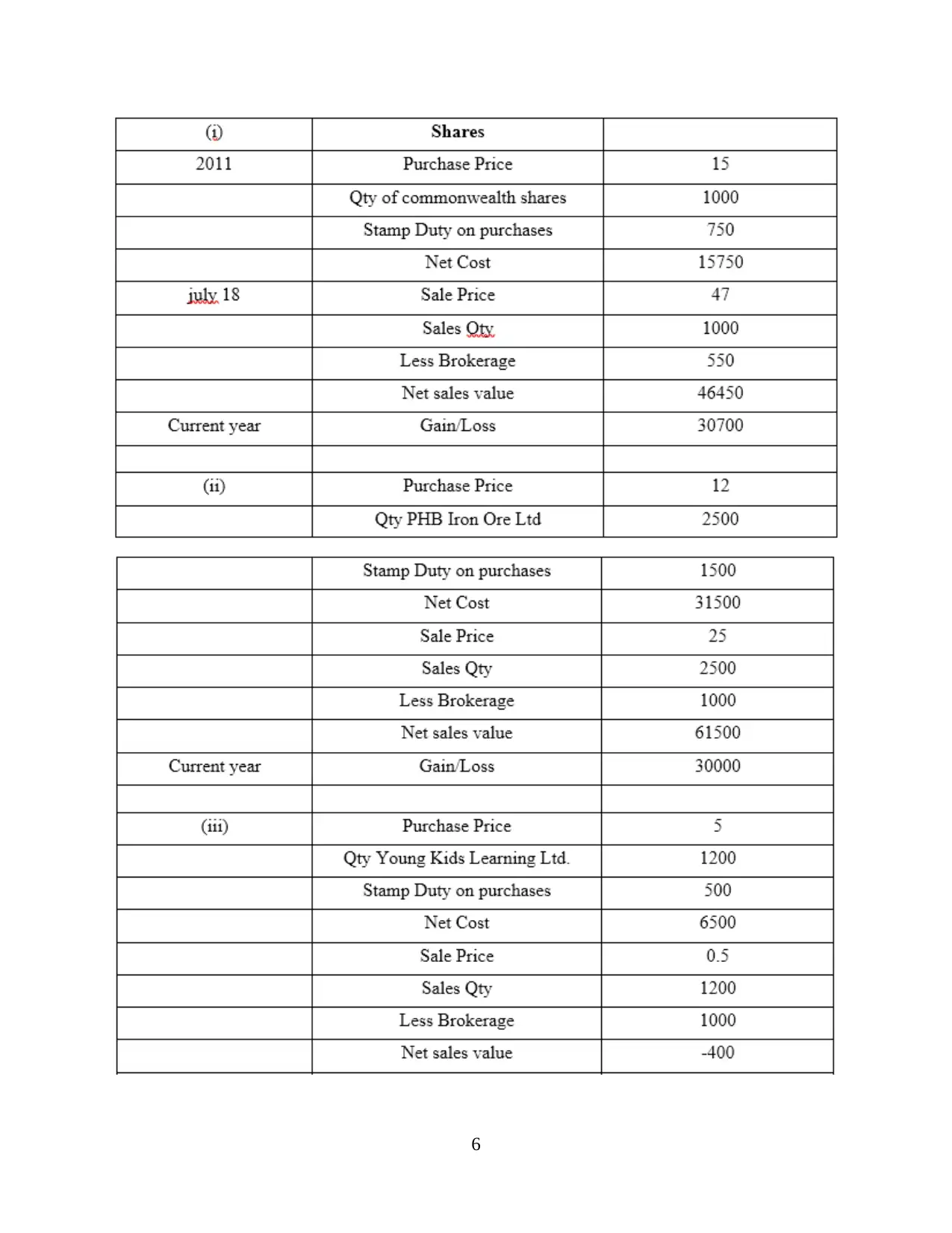

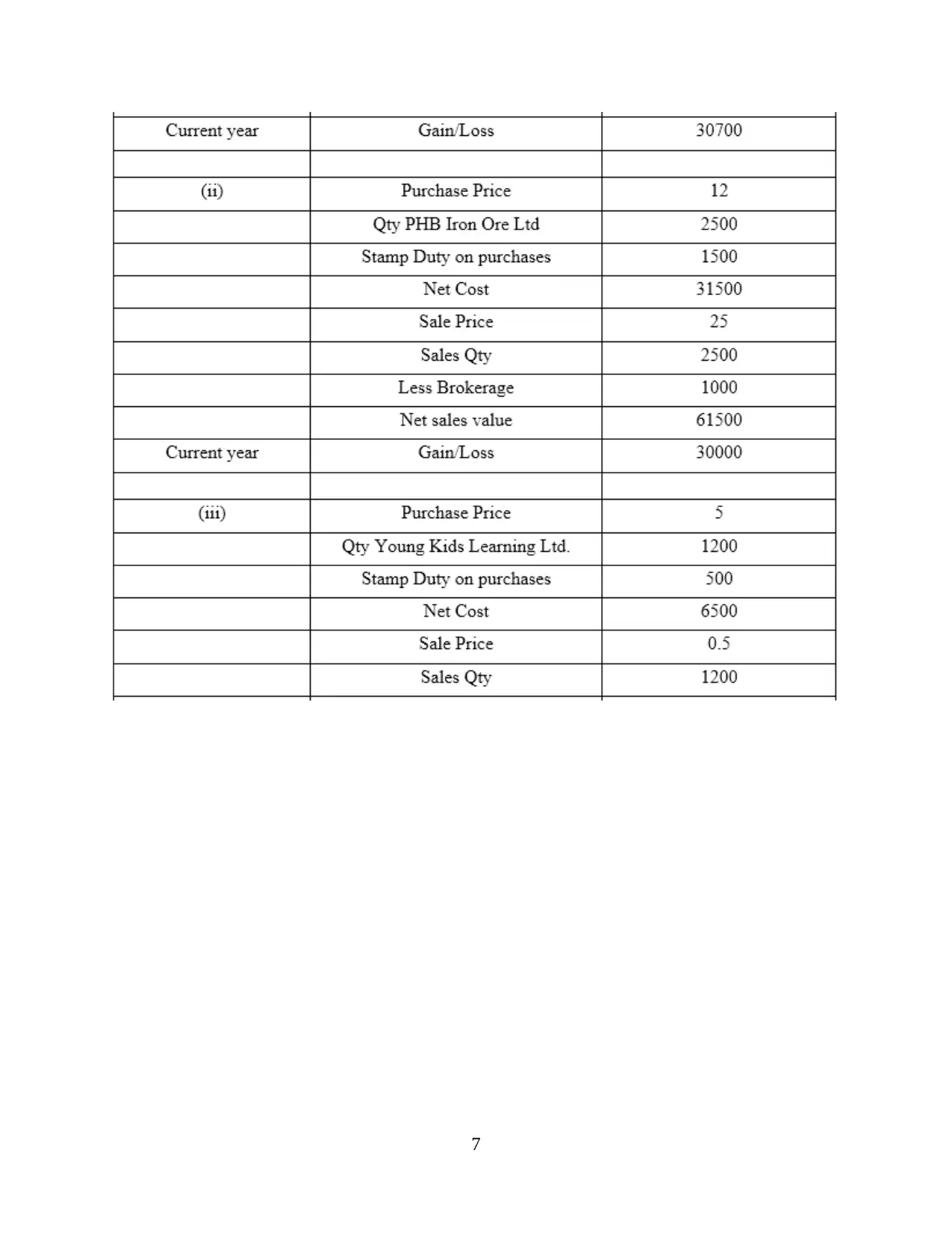

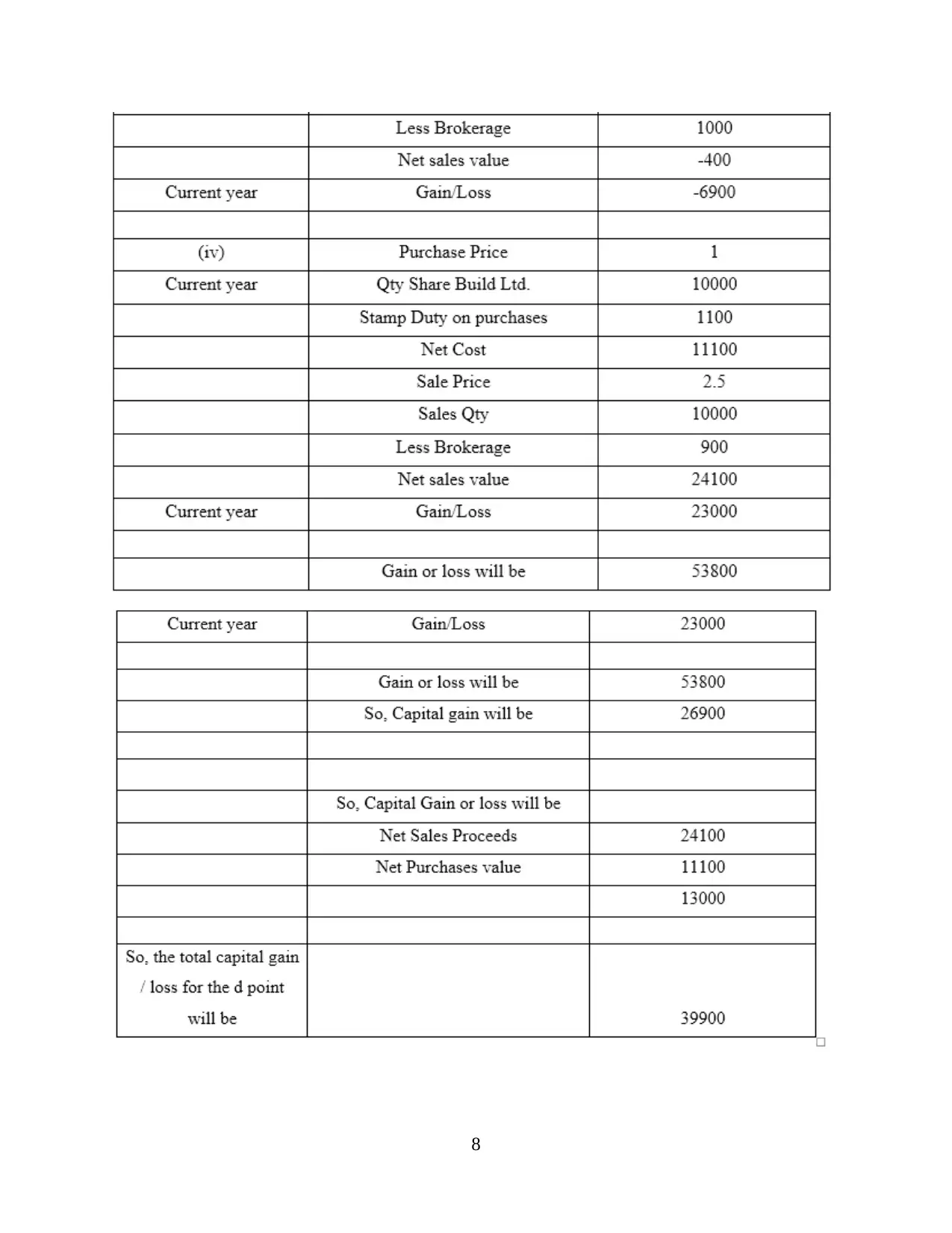

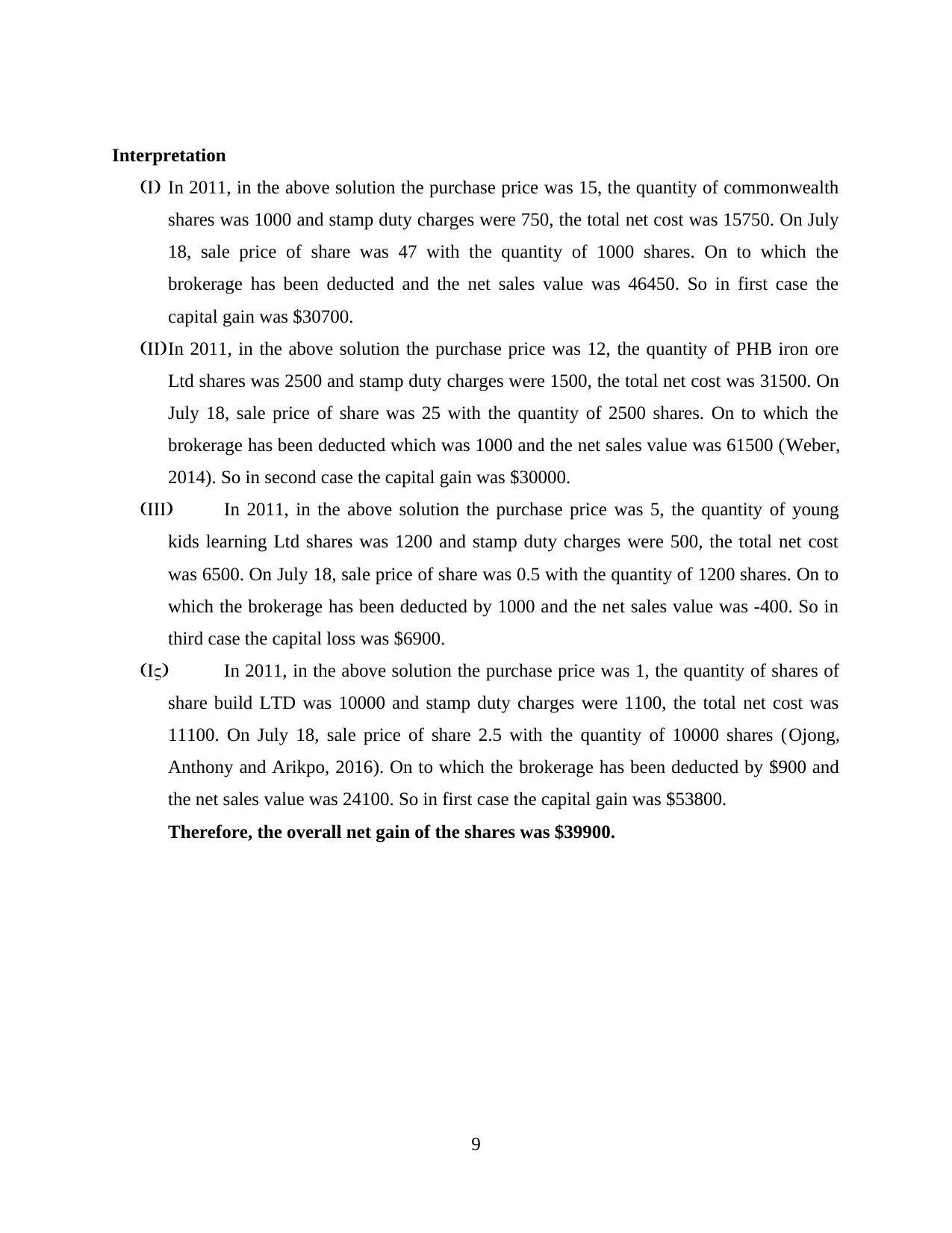

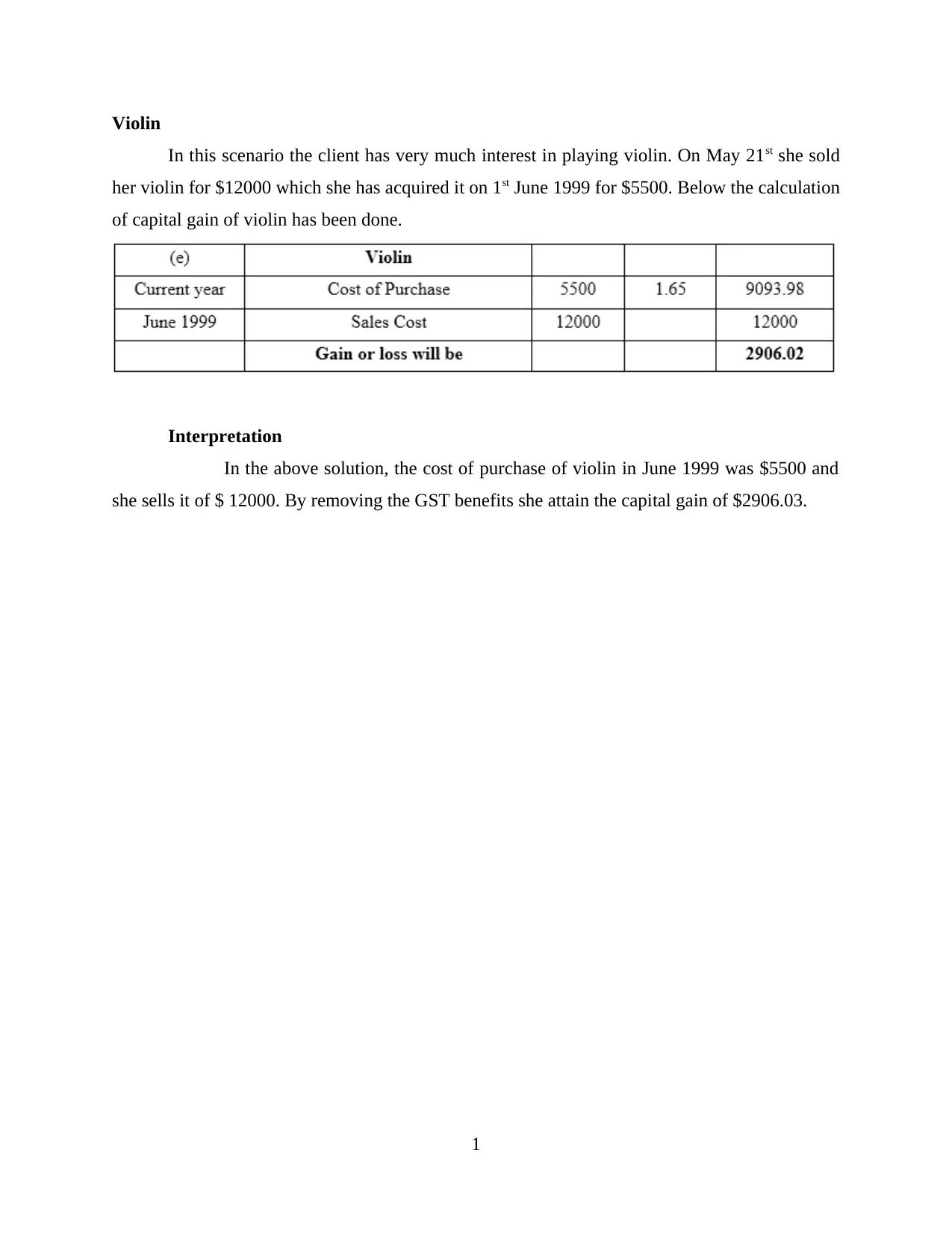

This report delves into taxation theory, practice, and law, providing a comprehensive analysis of capital gains, fringe benefits tax (FBT), and loan benefits. The report begins by determining the net capital gain of a client as of June 30, 2018, detailing calculations for various assets including vacant land, an antique bed, a painting, shares, and a violin. The report then advises on analyzing FBT on various assets, explaining the concept and calculation steps, including pros and cons. Finally, it analyzes the tax consequences when a loan amount is used to purchase securities, offering a complete overview of taxation concepts and their practical application. The analysis includes detailed calculations and interpretations for each scenario, offering insights into tax liabilities and financial planning.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.