Taxation Analysis: Capital Gains, Fringe Benefits, and Tax Avoidance

VerifiedAdded on 2020/07/23

|9

|2582

|65

Homework Assignment

AI Summary

This assignment delves into various aspects of taxation, commencing with an analysis of capital gains and losses derived from the sale of assets, including antiques and shares, and the implications of the Income Tax Assessment Act 1997. The assignment then explores fringe benefits provided by employers, such as low-interest loans, and calculates the taxable amounts based on statutory interest rates. Furthermore, the analysis extends to tax avoidance strategies, examining a case where a couple attempts to minimize tax liabilities through a specific income-sharing arrangement for a rental property, and the legal precedent set by the IRC vs Duke of Westminster case. Finally, the assignment assesses the tax implications of selling timber, differentiating between agricultural income and commercial revenue. The assignment provides detailed calculations, critical analyses, and supporting evidence from relevant tax policies and acts.

Taxation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Question 1........................................................................................................................................1

Introduction.................................................................................................................................1

Critical Analysis..........................................................................................................................1

Supporting Evidence...................................................................................................................2

Conclusion...................................................................................................................................2

Question 2........................................................................................................................................2

Introduction.................................................................................................................................2

Critical analysis...........................................................................................................................2

Supportive evidence: ..................................................................................................................4

Conclusion...................................................................................................................................4

Question 3........................................................................................................................................4

Introduction.................................................................................................................................4

Critical Evaluation......................................................................................................................4

Supportive Evidence...................................................................................................................5

Conclusion...................................................................................................................................5

Question 4........................................................................................................................................5

Introduction.................................................................................................................................5

Critical Analysis..........................................................................................................................5

Supporting Evidence...................................................................................................................5

Conclusion...................................................................................................................................6

Question 5........................................................................................................................................6

Introduction.................................................................................................................................6

Critical Analysis..........................................................................................................................6

Supporting Evidence:..................................................................................................................6

Conclusion...................................................................................................................................6

REFERENCES................................................................................................................................7

Question 1........................................................................................................................................1

Introduction.................................................................................................................................1

Critical Analysis..........................................................................................................................1

Supporting Evidence...................................................................................................................2

Conclusion...................................................................................................................................2

Question 2........................................................................................................................................2

Introduction.................................................................................................................................2

Critical analysis...........................................................................................................................2

Supportive evidence: ..................................................................................................................4

Conclusion...................................................................................................................................4

Question 3........................................................................................................................................4

Introduction.................................................................................................................................4

Critical Evaluation......................................................................................................................4

Supportive Evidence...................................................................................................................5

Conclusion...................................................................................................................................5

Question 4........................................................................................................................................5

Introduction.................................................................................................................................5

Critical Analysis..........................................................................................................................5

Supporting Evidence...................................................................................................................5

Conclusion...................................................................................................................................6

Question 5........................................................................................................................................6

Introduction.................................................................................................................................6

Critical Analysis..........................................................................................................................6

Supporting Evidence:..................................................................................................................6

Conclusion...................................................................................................................................6

REFERENCES................................................................................................................................7

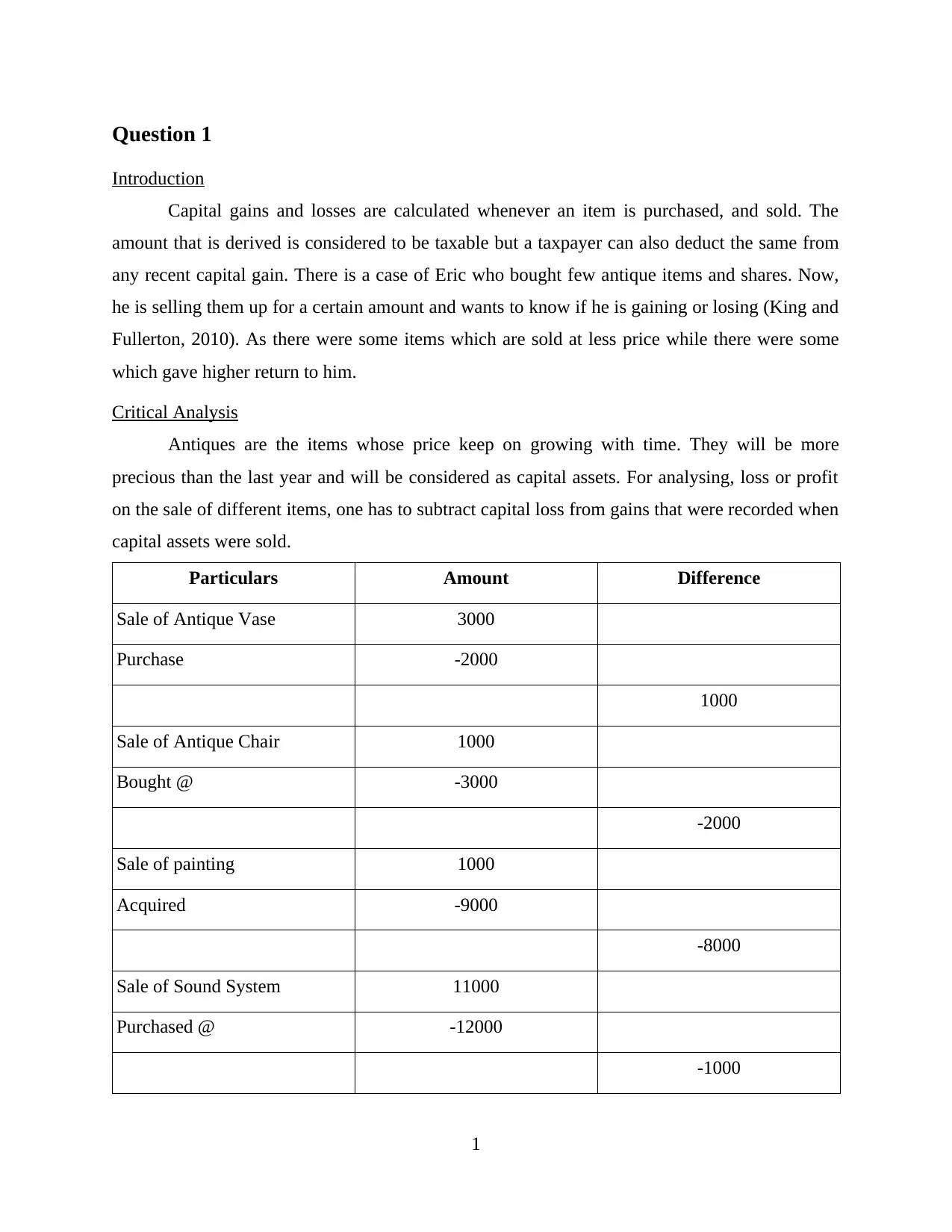

Question 1

Introduction

Capital gains and losses are calculated whenever an item is purchased, and sold. The

amount that is derived is considered to be taxable but a taxpayer can also deduct the same from

any recent capital gain. There is a case of Eric who bought few antique items and shares. Now,

he is selling them up for a certain amount and wants to know if he is gaining or losing (King and

Fullerton, 2010). As there were some items which are sold at less price while there were some

which gave higher return to him.

Critical Analysis

Antiques are the items whose price keep on growing with time. They will be more

precious than the last year and will be considered as capital assets. For analysing, loss or profit

on the sale of different items, one has to subtract capital loss from gains that were recorded when

capital assets were sold.

Particulars Amount Difference

Sale of Antique Vase 3000

Purchase -2000

1000

Sale of Antique Chair 1000

Bought @ -3000

-2000

Sale of painting 1000

Acquired -9000

-8000

Sale of Sound System 11000

Purchased @ -12000

-1000

1

Introduction

Capital gains and losses are calculated whenever an item is purchased, and sold. The

amount that is derived is considered to be taxable but a taxpayer can also deduct the same from

any recent capital gain. There is a case of Eric who bought few antique items and shares. Now,

he is selling them up for a certain amount and wants to know if he is gaining or losing (King and

Fullerton, 2010). As there were some items which are sold at less price while there were some

which gave higher return to him.

Critical Analysis

Antiques are the items whose price keep on growing with time. They will be more

precious than the last year and will be considered as capital assets. For analysing, loss or profit

on the sale of different items, one has to subtract capital loss from gains that were recorded when

capital assets were sold.

Particulars Amount Difference

Sale of Antique Vase 3000

Purchase -2000

1000

Sale of Antique Chair 1000

Bought @ -3000

-2000

Sale of painting 1000

Acquired -9000

-8000

Sale of Sound System 11000

Purchased @ -12000

-1000

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

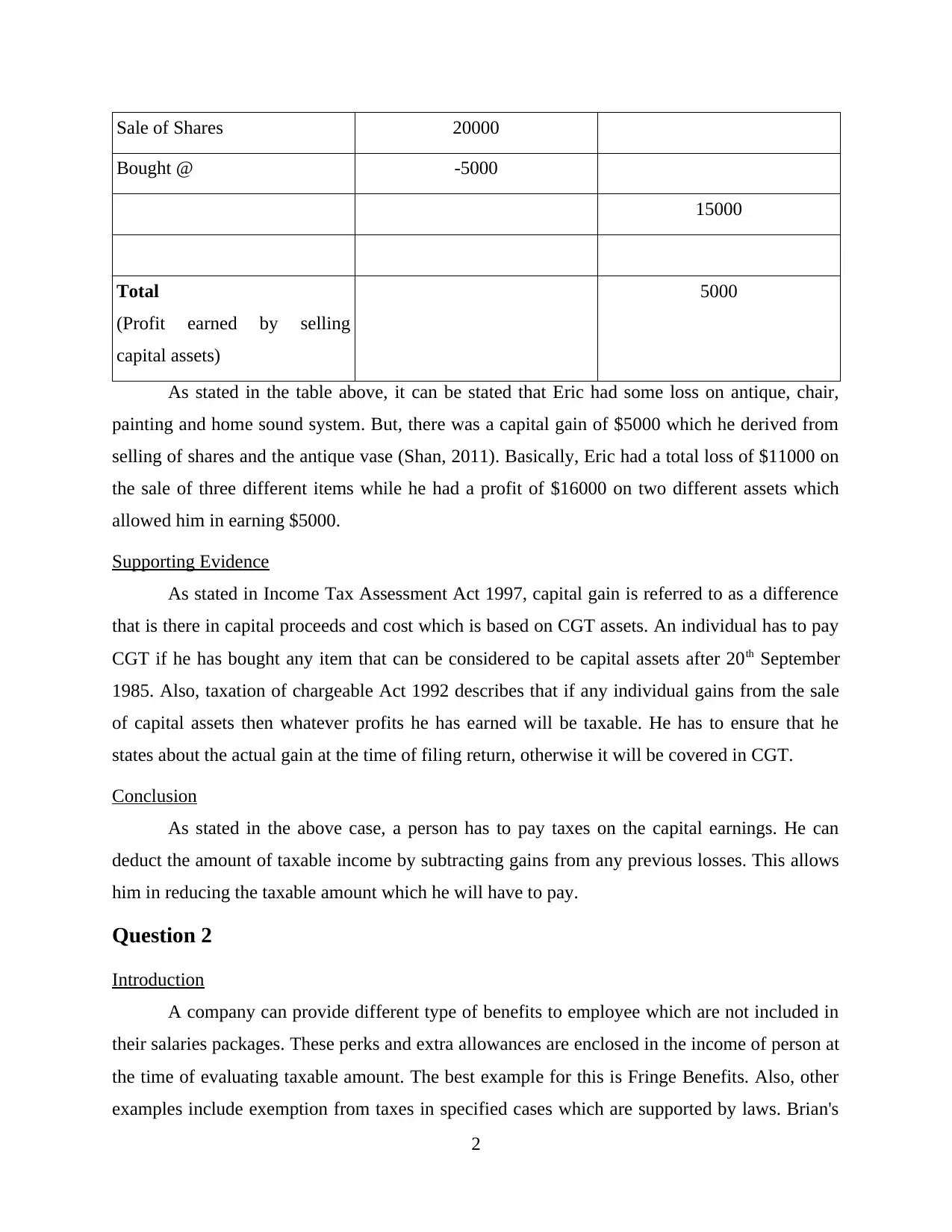

Sale of Shares 20000

Bought @ -5000

15000

Total

(Profit earned by selling

capital assets)

5000

As stated in the table above, it can be stated that Eric had some loss on antique, chair,

painting and home sound system. But, there was a capital gain of $5000 which he derived from

selling of shares and the antique vase (Shan, 2011). Basically, Eric had a total loss of $11000 on

the sale of three different items while he had a profit of $16000 on two different assets which

allowed him in earning $5000.

Supporting Evidence

As stated in Income Tax Assessment Act 1997, capital gain is referred to as a difference

that is there in capital proceeds and cost which is based on CGT assets. An individual has to pay

CGT if he has bought any item that can be considered to be capital assets after 20th September

1985. Also, taxation of chargeable Act 1992 describes that if any individual gains from the sale

of capital assets then whatever profits he has earned will be taxable. He has to ensure that he

states about the actual gain at the time of filing return, otherwise it will be covered in CGT.

Conclusion

As stated in the above case, a person has to pay taxes on the capital earnings. He can

deduct the amount of taxable income by subtracting gains from any previous losses. This allows

him in reducing the taxable amount which he will have to pay.

Question 2

Introduction

A company can provide different type of benefits to employee which are not included in

their salaries packages. These perks and extra allowances are enclosed in the income of person at

the time of evaluating taxable amount. The best example for this is Fringe Benefits. Also, other

examples include exemption from taxes in specified cases which are supported by laws. Brian's

2

Bought @ -5000

15000

Total

(Profit earned by selling

capital assets)

5000

As stated in the table above, it can be stated that Eric had some loss on antique, chair,

painting and home sound system. But, there was a capital gain of $5000 which he derived from

selling of shares and the antique vase (Shan, 2011). Basically, Eric had a total loss of $11000 on

the sale of three different items while he had a profit of $16000 on two different assets which

allowed him in earning $5000.

Supporting Evidence

As stated in Income Tax Assessment Act 1997, capital gain is referred to as a difference

that is there in capital proceeds and cost which is based on CGT assets. An individual has to pay

CGT if he has bought any item that can be considered to be capital assets after 20th September

1985. Also, taxation of chargeable Act 1992 describes that if any individual gains from the sale

of capital assets then whatever profits he has earned will be taxable. He has to ensure that he

states about the actual gain at the time of filing return, otherwise it will be covered in CGT.

Conclusion

As stated in the above case, a person has to pay taxes on the capital earnings. He can

deduct the amount of taxable income by subtracting gains from any previous losses. This allows

him in reducing the taxable amount which he will have to pay.

Question 2

Introduction

A company can provide different type of benefits to employee which are not included in

their salaries packages. These perks and extra allowances are enclosed in the income of person at

the time of evaluating taxable amount. The best example for this is Fringe Benefits. Also, other

examples include exemption from taxes in specified cases which are supported by laws. Brian's

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

employer provided him a loan of $1 million @ of interest of 1% per annum (Hopkins, 2011).

But, he utilised some of the amount which was borrowed from his employer for generating extra

income.

Critical analysis

Employer of Brian provided him with a loan of $1 million at the interest rate of 1%

which is far less than the prevailing market rate which can be considered to be a fringe benefit

for him. The statutory rate that is prevailing at present in the market is stated to be 5.65%. the

difference between offered interest rate and statutory is 4.65%.

The calculation of tax is evaluated as:

1) The amount of taxes which are payable on taxable benefit.

The initial interest rate is:

$1,000,000*1%=$10,000.

According to provisions and regulations are:

$1,000,000*5.65%=$56,500.

The total amount of Fringe benefits will be:

$56500-$10000=$46,500.

2) The taxable amount paid on different fringe benefits according to the given case the

benefits are charged without paying any type of interest rates.

$1,000,000*5.65%=$56,500.

3) If Brian is paying the interest rates according to the rates which are standard, then in this

case he is liable for $ 22600 amount will be deducted.

$56,500*40%=$22600

4) According to the case if the amount which had to be reduced from the total taxable amount

is $ 4000

$10,000*40%=$4000

5) The amount which is payable for taxes can be achieved if we subtract step 4 by step 3

$22600-$4000=$18600

In a scenario where monthly instalments are to be given, then total amount will be

divided by 12. The change in case (from annual to monthly) will not lead to change in amount

payable as a tax. In last case, if employer does not charge any amount as interest then there will

be different fringe benefit to Brian:

3

But, he utilised some of the amount which was borrowed from his employer for generating extra

income.

Critical analysis

Employer of Brian provided him with a loan of $1 million at the interest rate of 1%

which is far less than the prevailing market rate which can be considered to be a fringe benefit

for him. The statutory rate that is prevailing at present in the market is stated to be 5.65%. the

difference between offered interest rate and statutory is 4.65%.

The calculation of tax is evaluated as:

1) The amount of taxes which are payable on taxable benefit.

The initial interest rate is:

$1,000,000*1%=$10,000.

According to provisions and regulations are:

$1,000,000*5.65%=$56,500.

The total amount of Fringe benefits will be:

$56500-$10000=$46,500.

2) The taxable amount paid on different fringe benefits according to the given case the

benefits are charged without paying any type of interest rates.

$1,000,000*5.65%=$56,500.

3) If Brian is paying the interest rates according to the rates which are standard, then in this

case he is liable for $ 22600 amount will be deducted.

$56,500*40%=$22600

4) According to the case if the amount which had to be reduced from the total taxable amount

is $ 4000

$10,000*40%=$4000

5) The amount which is payable for taxes can be achieved if we subtract step 4 by step 3

$22600-$4000=$18600

In a scenario where monthly instalments are to be given, then total amount will be

divided by 12. The change in case (from annual to monthly) will not lead to change in amount

payable as a tax. In last case, if employer does not charge any amount as interest then there will

be different fringe benefit to Brian:

3

$ 1,000,000*5.65% = $56,500

$56,500*40% = $ 22,600

The total Fringe benefits from this scenario will be $22,600 to be precise.

Supportive evidence:

As stated in Fringe tax policy, the taxable amount will be the primary difference between

notional amount of interest and the actual rate that is applied on borrowed money. Under this

situation, each type of loan is considered to be independent (Rosenberg and Center, 2013). There

are different other benefits under this FBT policy, like exemption of not paying tax in certain

situations.

Conclusion

It is states that, in case that fringe benefits are the one which are given by employer to

employee. There are different employment taxes that are applicable on fringe benefits as a

taxable amount. It does not matter if the company provide payment method as monthly or yearly,

the rate of interest will remain same.

Question 3

Introduction

It is stated in the case that, Jack (an architect) and his wife Jill purchased a rental property

by borrowing a certain amount of money. Both of them formed a contract which was in written

form and the income would be divided on 1:9 ratios. Jack was liable for all the loss and liabilities

while Jill would gain 90% of income in case there is profit. This arrangement was made as to

avoid burden of tax. Also, there was loss of $10,000 in previous year which makes jack liable for

it.

Critical Evaluation

As described in the case, the contract was formed to reduce the burden of tax liabilities.

At present, Jill is working as a house maker. So, whatever her earnings are will be counted in

Jack account. Both, tax liabilities and income are categorised in his account as to make process

more fluid. If there is any loss, then financial loss will be carried out to the next year (Sammut

and Webb, 2011). Once there is a capital gain then loss of past will be managed. Jill is a

housewife, so she is not supposed to pay any liabilities, her husband will do so. Basically, both

of them clubbed together and made an agreement to save tax. At the time of selling property,

4

$56,500*40% = $ 22,600

The total Fringe benefits from this scenario will be $22,600 to be precise.

Supportive evidence:

As stated in Fringe tax policy, the taxable amount will be the primary difference between

notional amount of interest and the actual rate that is applied on borrowed money. Under this

situation, each type of loan is considered to be independent (Rosenberg and Center, 2013). There

are different other benefits under this FBT policy, like exemption of not paying tax in certain

situations.

Conclusion

It is states that, in case that fringe benefits are the one which are given by employer to

employee. There are different employment taxes that are applicable on fringe benefits as a

taxable amount. It does not matter if the company provide payment method as monthly or yearly,

the rate of interest will remain same.

Question 3

Introduction

It is stated in the case that, Jack (an architect) and his wife Jill purchased a rental property

by borrowing a certain amount of money. Both of them formed a contract which was in written

form and the income would be divided on 1:9 ratios. Jack was liable for all the loss and liabilities

while Jill would gain 90% of income in case there is profit. This arrangement was made as to

avoid burden of tax. Also, there was loss of $10,000 in previous year which makes jack liable for

it.

Critical Evaluation

As described in the case, the contract was formed to reduce the burden of tax liabilities.

At present, Jill is working as a house maker. So, whatever her earnings are will be counted in

Jack account. Both, tax liabilities and income are categorised in his account as to make process

more fluid. If there is any loss, then financial loss will be carried out to the next year (Sammut

and Webb, 2011). Once there is a capital gain then loss of past will be managed. Jill is a

housewife, so she is not supposed to pay any liabilities, her husband will do so. Basically, both

of them clubbed together and made an agreement to save tax. At the time of selling property,

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

whatever income will be made will be divided on the basis of 9(Jill): 1(Jack). If there is loss,

then they can carry it forwarded to next year and adjust it with capital gains.

Supportive Evidence

As stated by Australian Taxation Office, an individual will not get deduction on any

amount which is considered to be a non-essential thing. If there is capital loss than Jack can

deduct it from the earning that he made (Halabi, Barrett and Dyt, 2010). Also, as stated by

income tax department, any earning made by dependent individual will be considered in the

account of actual earner of house.

Conclusion

As explained above, it is stated that Jill will receive 90% of rental income while Jack will get

10%. He will be liable to pay all liabilities and adjust them with gains.

Question 4

Introduction

Everyone wants to save some amount in taxes and for that people use different methods.

The case of IRC vs Duke of Westminster, 1936, is based on related point of interest. There was a

deed which was formed between duke and his gardener, where he promised to pay the gardener

full amount equal to his wage one time in a year. The duke paid this amount from his post tax

income which allowed him to claim for deductions.

Critical Analysis

In IRC vs Duke of Westminster (1936), duke formed an agreement with his Gardner

where he would pay him complete amount in one go from his post tax income and claim for

relaxation in tax. It allowed him in exploiting the loopholes which were present in the case. IRC

filed a case against him when they found what was going on (Murphy, 2012). When asked in

court why he did so, Duke stated that if there is legal way to reduce tax burden then why not use

it. The Duke appointed Gardner and he was not paying him salary as mentioned in the

employment law.

Supporting Evidence

This is one of the most famous case in the history of tax and its avoidance. The statement

made by Lord Tomlin was more shocking as he stated that if there is a legal way to save tax then

5

then they can carry it forwarded to next year and adjust it with capital gains.

Supportive Evidence

As stated by Australian Taxation Office, an individual will not get deduction on any

amount which is considered to be a non-essential thing. If there is capital loss than Jack can

deduct it from the earning that he made (Halabi, Barrett and Dyt, 2010). Also, as stated by

income tax department, any earning made by dependent individual will be considered in the

account of actual earner of house.

Conclusion

As explained above, it is stated that Jill will receive 90% of rental income while Jack will get

10%. He will be liable to pay all liabilities and adjust them with gains.

Question 4

Introduction

Everyone wants to save some amount in taxes and for that people use different methods.

The case of IRC vs Duke of Westminster, 1936, is based on related point of interest. There was a

deed which was formed between duke and his gardener, where he promised to pay the gardener

full amount equal to his wage one time in a year. The duke paid this amount from his post tax

income which allowed him to claim for deductions.

Critical Analysis

In IRC vs Duke of Westminster (1936), duke formed an agreement with his Gardner

where he would pay him complete amount in one go from his post tax income and claim for

relaxation in tax. It allowed him in exploiting the loopholes which were present in the case. IRC

filed a case against him when they found what was going on (Murphy, 2012). When asked in

court why he did so, Duke stated that if there is legal way to reduce tax burden then why not use

it. The Duke appointed Gardner and he was not paying him salary as mentioned in the

employment law.

Supporting Evidence

This is one of the most famous case in the history of tax and its avoidance. The statement

made by Lord Tomlin was more shocking as he stated that if there is a legal way to save tax then

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

person should use it. As per the Principle of Ramsay, if a person is taking such steps which are

artificial in nature to save tax and not for commercial purpose then he has to pay tax. This is

implied in today's scenario.

Conclusion

At that point of time it was easy to avoid tax but today it is complex and next to

impossible for individual to use such way to save tax.

Question 5

Introduction

It is very hard to assess the taxable amount from sale of timber, as people had different

views regarding it. Some of them saw it as a agriculture income while some considered it as a

revenue. Bill is the owner of a land with a palm tree plantation, he wanted to use this place for

grazing his cattle for which he has to clean the area (Daniel, Keen and McPherson, 2010). For

this purpose, a logging company agreed to pay $1000 for 100 meters of area.

Critical Analysis

There will be income for bill which will be generated when tress will be cleared by

logging company. That income will fall under tax boundaries and bill will have to pay it. The

logging company is paying Bill a hefty amount of $50000 on whose basis whole situation will be

assessed. Also, he is allowing the company to take as much log they want for a sum of money

which creates a situation where he is dealing with them commercially. This is considered to be a

capital gain for which he has to pay taxes.

Supporting Evidence:

As stated in TR 95/6 any income which is generated by cutting and selling trees will be

assessed at the time of filing income tax. In this case if bill take money against the trees from

logging company then it will be considered as a commercial act which will make him liable to

pay taxes (Woellner and et. al., 2011).. If he does not charge company anything then it will

considered as a forest act where he won’t have to pay taxes.

Conclusion

As stated in the case study, it can be said that if a person charges money against timber

then he will have to pay taxes.

6

artificial in nature to save tax and not for commercial purpose then he has to pay tax. This is

implied in today's scenario.

Conclusion

At that point of time it was easy to avoid tax but today it is complex and next to

impossible for individual to use such way to save tax.

Question 5

Introduction

It is very hard to assess the taxable amount from sale of timber, as people had different

views regarding it. Some of them saw it as a agriculture income while some considered it as a

revenue. Bill is the owner of a land with a palm tree plantation, he wanted to use this place for

grazing his cattle for which he has to clean the area (Daniel, Keen and McPherson, 2010). For

this purpose, a logging company agreed to pay $1000 for 100 meters of area.

Critical Analysis

There will be income for bill which will be generated when tress will be cleared by

logging company. That income will fall under tax boundaries and bill will have to pay it. The

logging company is paying Bill a hefty amount of $50000 on whose basis whole situation will be

assessed. Also, he is allowing the company to take as much log they want for a sum of money

which creates a situation where he is dealing with them commercially. This is considered to be a

capital gain for which he has to pay taxes.

Supporting Evidence:

As stated in TR 95/6 any income which is generated by cutting and selling trees will be

assessed at the time of filing income tax. In this case if bill take money against the trees from

logging company then it will be considered as a commercial act which will make him liable to

pay taxes (Woellner and et. al., 2011).. If he does not charge company anything then it will

considered as a forest act where he won’t have to pay taxes.

Conclusion

As stated in the case study, it can be said that if a person charges money against timber

then he will have to pay taxes.

6

REFERENCES

Books and Journals

Daniel, P., Keen, M. and McPherson, C. eds., 2010. The taxation of petroleum and minerals:

principles, problems and practice. Routledge.

Halabi, A.K., Barrett, R. and Dyt, R., 2010. Understanding financial information used to assess

small firm performance: An Australian qualitative study. Qualitative Research in

Accounting & Management. 7(2). pp.163-179.

Hopkins, B.R., 2011. The law of tax-exempt organizations (Vol. 5). John Wiley & Sons.

King, M.A. and Fullerton, D., 2010. The taxation of income from capital: a comparative study of

the United States, the United Kingdom, Sweden and West Germany. University of

Chicago Press.

Rosenberg, J. and Center, U.B.T.P., 2013. Measuring income for distributional analysis.

Washington, DC.: Urban-Brookings Tax Policy Center. July, 25.

Sammut, C. and Webb, G.I. eds., 2011. Encyclopaedia of machine learning. Springer Science &

Business Media.

Shan, H., 2011. The effect of capital gains taxation on home sales: evidence from the Taxpayer

Relief Act of 1997. Journal of Public Economics. 95(1). pp.177-188.

Woellner, R. and et. al., 2011. Australian Taxation Law Select: legislation and commentary.

CCH Australia.

Online

Richard Murphy, 2012. The Duke of Westminster is Dead: Long Live the Duke of Westminster.

[Online]. Available through:<http://www.taxresearch.org.uk/Blog/2012/08/10/the-duke-

of-westminster-is-dead-long-live-the-duke-of-westminster/>. [Accessed on 19th

September 2017].

7

Books and Journals

Daniel, P., Keen, M. and McPherson, C. eds., 2010. The taxation of petroleum and minerals:

principles, problems and practice. Routledge.

Halabi, A.K., Barrett, R. and Dyt, R., 2010. Understanding financial information used to assess

small firm performance: An Australian qualitative study. Qualitative Research in

Accounting & Management. 7(2). pp.163-179.

Hopkins, B.R., 2011. The law of tax-exempt organizations (Vol. 5). John Wiley & Sons.

King, M.A. and Fullerton, D., 2010. The taxation of income from capital: a comparative study of

the United States, the United Kingdom, Sweden and West Germany. University of

Chicago Press.

Rosenberg, J. and Center, U.B.T.P., 2013. Measuring income for distributional analysis.

Washington, DC.: Urban-Brookings Tax Policy Center. July, 25.

Sammut, C. and Webb, G.I. eds., 2011. Encyclopaedia of machine learning. Springer Science &

Business Media.

Shan, H., 2011. The effect of capital gains taxation on home sales: evidence from the Taxpayer

Relief Act of 1997. Journal of Public Economics. 95(1). pp.177-188.

Woellner, R. and et. al., 2011. Australian Taxation Law Select: legislation and commentary.

CCH Australia.

Online

Richard Murphy, 2012. The Duke of Westminster is Dead: Long Live the Duke of Westminster.

[Online]. Available through:<http://www.taxresearch.org.uk/Blog/2012/08/10/the-duke-

of-westminster-is-dead-long-live-the-duke-of-westminster/>. [Accessed on 19th

September 2017].

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.