Taxation Theory, Practice & Law: Analysis of Tax Cases and Regulations

VerifiedAdded on 2019/10/31

|10

|2254

|159

Report

AI Summary

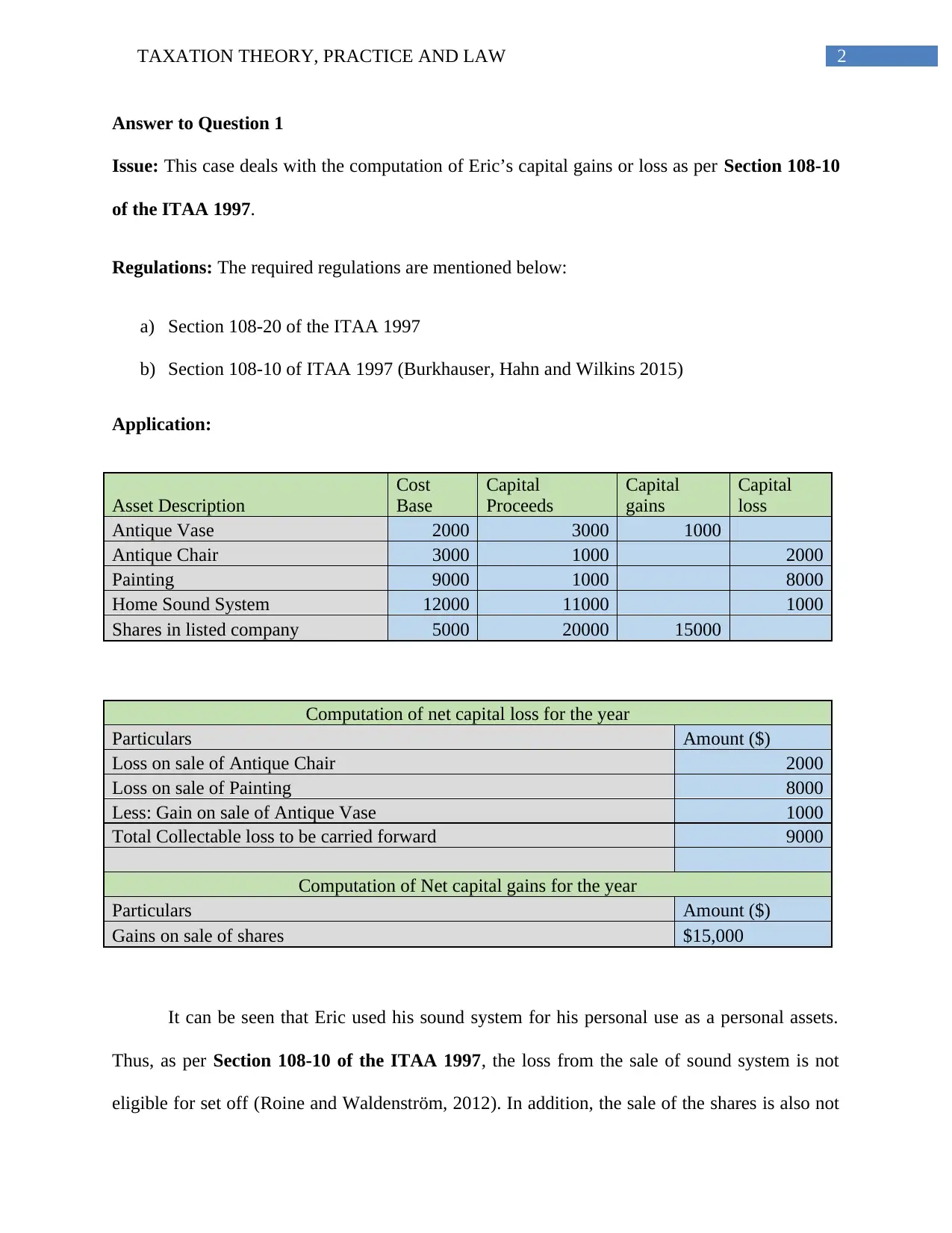

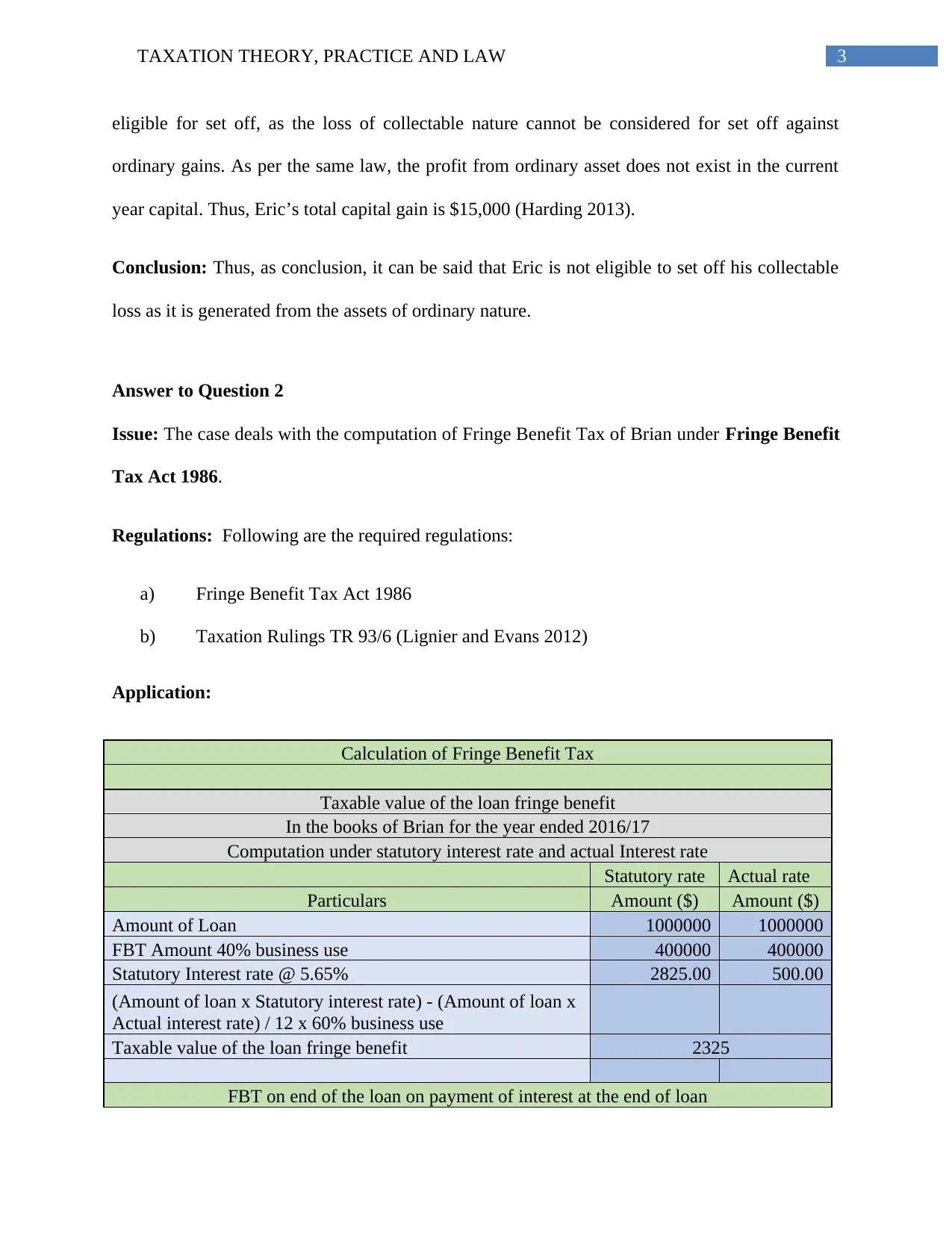

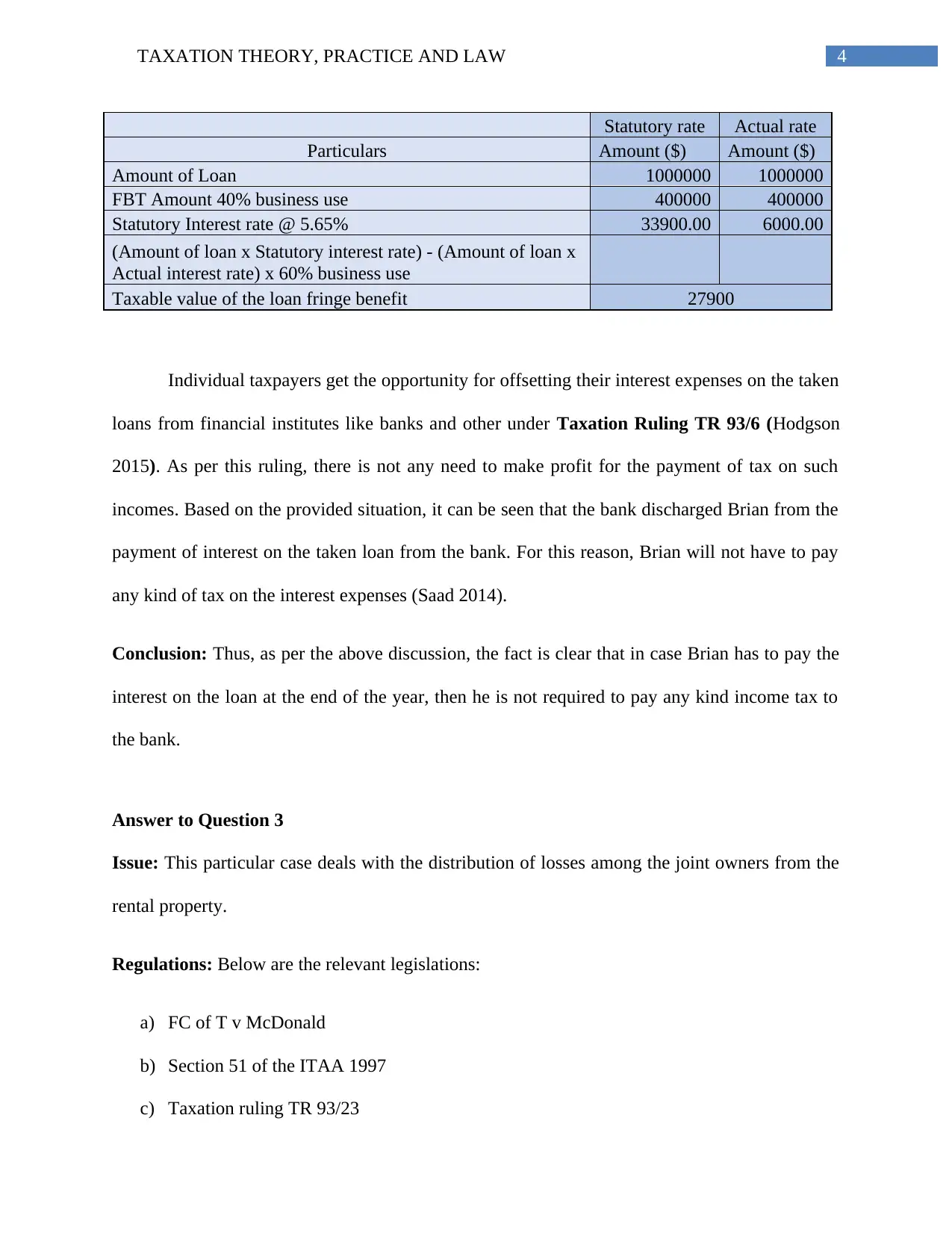

This report provides a detailed analysis of various taxation issues, including capital gains, fringe benefits tax, and tax assessment. It begins by examining the computation of capital gains and losses based on Section 108-10 of the ITAA 1997, including scenarios involving the sale of assets and the treatment of collectable losses. The report then delves into the computation of Fringe Benefit Tax (FBT) under the Fringe Benefit Tax Act 1986, specifically addressing the taxable value of loan fringe benefits and the impact of statutory and actual interest rates. Furthermore, it explores the distribution of losses among joint owners of rental properties, referencing relevant rulings and case law like FC of T v McDonald. The report also analyzes the case of IRC v Duke Westminster (1936), discussing the principles of tax avoidance and the rights of taxpayers. Finally, it assesses the tax implications of cutting timber, referencing Subsection 6 (1) of the ITAA 1936 and relevant rulings, determining whether income from forestry activities is considered primary production for tax purposes. The report concludes with comprehensive references to support the analysis.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.