Taxation Theory and Practice Law Report - Finance Module, Semester 1

VerifiedAdded on 2020/10/22

|8

|2616

|190

Report

AI Summary

This report delves into the intricacies of taxation law and practice, addressing key aspects such as capital gains, royalty income, and income tax assessment within the Australian context. The report analyzes three distinct scenarios involving capital gains tax on asset disposals, the tax treatment of royalty income derived from intellectual property, and the implications of personal loans between family members. The analysis references the Income Tax Assessment Act 1997 and other relevant regulations, providing detailed calculations and explanations to determine tax liabilities. The report considers exemptions, indexation methods, and the classification of income sources to offer a comprehensive understanding of taxation principles and their practical application in various financial situations.

Taxation theory and

practice law

practice law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

Question 1...................................................................................................................................3

Question 2 ..................................................................................................................................5

Question 3...................................................................................................................................7

CONCLUSION ...............................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................3

Question 1...................................................................................................................................3

Question 2 ..................................................................................................................................5

Question 3...................................................................................................................................7

CONCLUSION ...............................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Taxation refers to a term wherein the government levies or impose a tax on the income of

a person or an organisation. It is a wide concept which comprises rules, regulations and laws

which are to be complied with by a taxpayer (Oats, 2012). Government earn significant amount

through taxation which is further applicable for the betterment of the society. It is of two types

viz. Direct and indirect. Taxation laws provide legal provisions regarding which income to be

taxed, what rate should be applicable, what all deduction can a person or entity avail, what would

be the consequences if a person fails to abide by or contravenes any provision. The main element

of this report is taxation laws which has been defined by solving some questions in order to have

better idea about how tax laws are applicable in different situations.

MAIN BODY

Question 1

In this question Helen is a fashion designer who has disposed of some of her assets which

falls under “Capital Gain” head. Australian government has enacted Income Tax Assessment

Act, 1997 which governs the taxation of income arising from different sources which falls under

different heads. According to section 100-50, any income or loss on selling of an asset which

was acquired by an individual including acquisition through inheritance, then such gain or loss is

termed as capital gain or loss (Woellner and et. al., 2014).

There are two categories of assets such as long term and short term depending on the

holding period. If an asset is sold within 36 months from the date of acquisition, the it will be a

short term capital gain or loss on the other hand if yes it is held for more than 36 months, and any

loss or gain arising on disposing of such asset will be termed as long-term capital gain or loss.

Treatment for both holding period is different. In addition to this, capital gain tax is applicable to

real state, shares, units, leases, goodwill, collectibles, personal use assets which are above the

prescribed limit and many other things (Meaning of personal income, 2019). Also, there are

Somerset which are exempted from capital gain tax such as main residence, car on motorcycle,

depreciating assets and any asset purchased before 20th September, 1985.

The capital gain or loss is calculated in the following ways:

Sale price > Cost of acquisition = Capital gain

Sale price < Cost of acquisition = Capital loss

Taxation refers to a term wherein the government levies or impose a tax on the income of

a person or an organisation. It is a wide concept which comprises rules, regulations and laws

which are to be complied with by a taxpayer (Oats, 2012). Government earn significant amount

through taxation which is further applicable for the betterment of the society. It is of two types

viz. Direct and indirect. Taxation laws provide legal provisions regarding which income to be

taxed, what rate should be applicable, what all deduction can a person or entity avail, what would

be the consequences if a person fails to abide by or contravenes any provision. The main element

of this report is taxation laws which has been defined by solving some questions in order to have

better idea about how tax laws are applicable in different situations.

MAIN BODY

Question 1

In this question Helen is a fashion designer who has disposed of some of her assets which

falls under “Capital Gain” head. Australian government has enacted Income Tax Assessment

Act, 1997 which governs the taxation of income arising from different sources which falls under

different heads. According to section 100-50, any income or loss on selling of an asset which

was acquired by an individual including acquisition through inheritance, then such gain or loss is

termed as capital gain or loss (Woellner and et. al., 2014).

There are two categories of assets such as long term and short term depending on the

holding period. If an asset is sold within 36 months from the date of acquisition, the it will be a

short term capital gain or loss on the other hand if yes it is held for more than 36 months, and any

loss or gain arising on disposing of such asset will be termed as long-term capital gain or loss.

Treatment for both holding period is different. In addition to this, capital gain tax is applicable to

real state, shares, units, leases, goodwill, collectibles, personal use assets which are above the

prescribed limit and many other things (Meaning of personal income, 2019). Also, there are

Somerset which are exempted from capital gain tax such as main residence, car on motorcycle,

depreciating assets and any asset purchased before 20th September, 1985.

The capital gain or loss is calculated in the following ways:

Sale price > Cost of acquisition = Capital gain

Sale price < Cost of acquisition = Capital loss

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

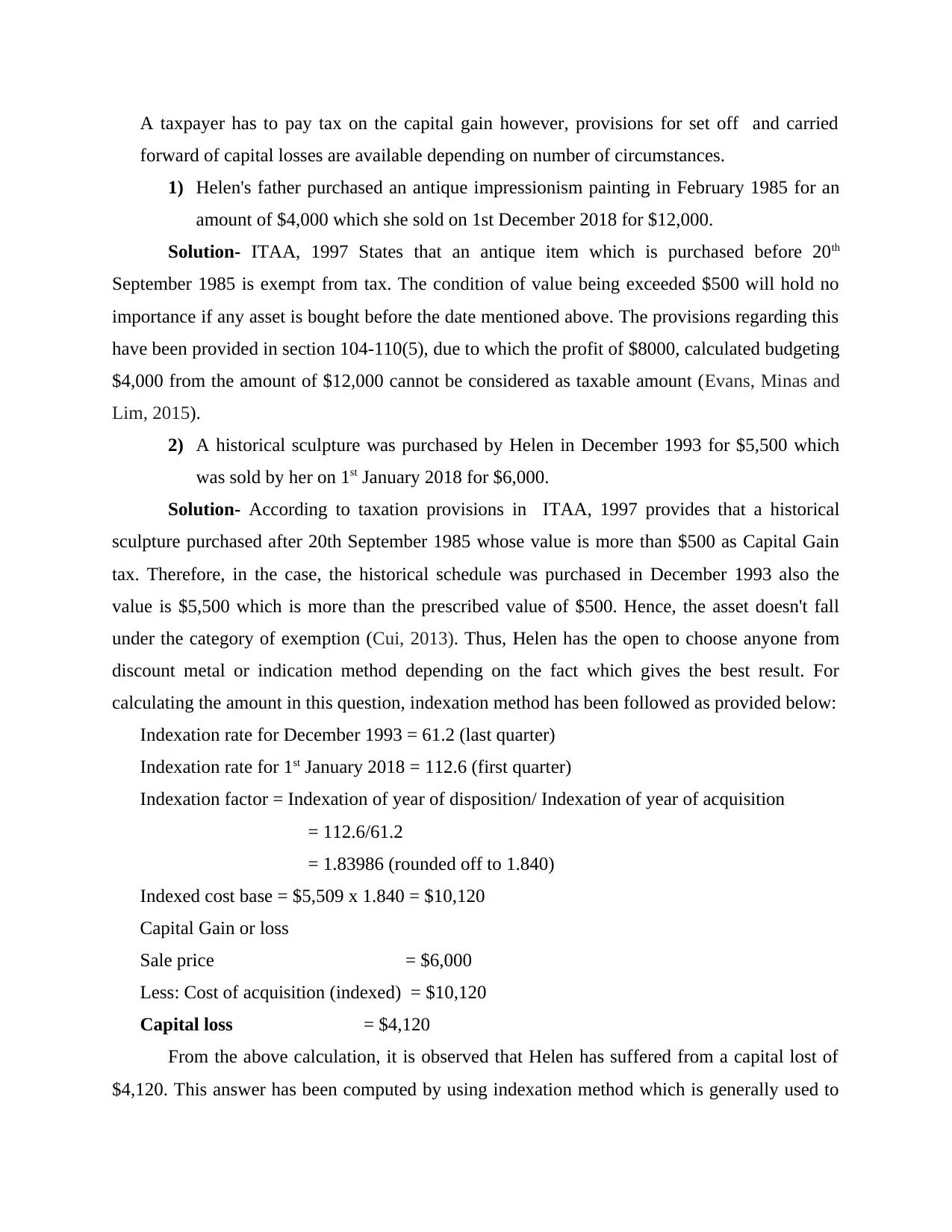

A taxpayer has to pay tax on the capital gain however, provisions for set off and carried

forward of capital losses are available depending on number of circumstances.

1) Helen's father purchased an antique impressionism painting in February 1985 for an

amount of $4,000 which she sold on 1st December 2018 for $12,000.

Solution- ITAA, 1997 States that an antique item which is purchased before 20th

September 1985 is exempt from tax. The condition of value being exceeded $500 will hold no

importance if any asset is bought before the date mentioned above. The provisions regarding this

have been provided in section 104-110(5), due to which the profit of $8000, calculated budgeting

$4,000 from the amount of $12,000 cannot be considered as taxable amount (Evans, Minas and

Lim, 2015).

2) A historical sculpture was purchased by Helen in December 1993 for $5,500 which

was sold by her on 1st January 2018 for $6,000.

Solution- According to taxation provisions in ITAA, 1997 provides that a historical

sculpture purchased after 20th September 1985 whose value is more than $500 as Capital Gain

tax. Therefore, in the case, the historical schedule was purchased in December 1993 also the

value is $5,500 which is more than the prescribed value of $500. Hence, the asset doesn't fall

under the category of exemption (Cui, 2013). Thus, Helen has the open to choose anyone from

discount metal or indication method depending on the fact which gives the best result. For

calculating the amount in this question, indexation method has been followed as provided below:

Indexation rate for December 1993 = 61.2 (last quarter)

Indexation rate for 1st January 2018 = 112.6 (first quarter)

Indexation factor = Indexation of year of disposition/ Indexation of year of acquisition

= 112.6/61.2

= 1.83986 (rounded off to 1.840)

Indexed cost base = $5,509 x 1.840 = $10,120

Capital Gain or loss

Sale price = $6,000

Less: Cost of acquisition (indexed) = $10,120

Capital loss = $4,120

From the above calculation, it is observed that Helen has suffered from a capital lost of

$4,120. This answer has been computed by using indexation method which is generally used to

forward of capital losses are available depending on number of circumstances.

1) Helen's father purchased an antique impressionism painting in February 1985 for an

amount of $4,000 which she sold on 1st December 2018 for $12,000.

Solution- ITAA, 1997 States that an antique item which is purchased before 20th

September 1985 is exempt from tax. The condition of value being exceeded $500 will hold no

importance if any asset is bought before the date mentioned above. The provisions regarding this

have been provided in section 104-110(5), due to which the profit of $8000, calculated budgeting

$4,000 from the amount of $12,000 cannot be considered as taxable amount (Evans, Minas and

Lim, 2015).

2) A historical sculpture was purchased by Helen in December 1993 for $5,500 which

was sold by her on 1st January 2018 for $6,000.

Solution- According to taxation provisions in ITAA, 1997 provides that a historical

sculpture purchased after 20th September 1985 whose value is more than $500 as Capital Gain

tax. Therefore, in the case, the historical schedule was purchased in December 1993 also the

value is $5,500 which is more than the prescribed value of $500. Hence, the asset doesn't fall

under the category of exemption (Cui, 2013). Thus, Helen has the open to choose anyone from

discount metal or indication method depending on the fact which gives the best result. For

calculating the amount in this question, indexation method has been followed as provided below:

Indexation rate for December 1993 = 61.2 (last quarter)

Indexation rate for 1st January 2018 = 112.6 (first quarter)

Indexation factor = Indexation of year of disposition/ Indexation of year of acquisition

= 112.6/61.2

= 1.83986 (rounded off to 1.840)

Indexed cost base = $5,509 x 1.840 = $10,120

Capital Gain or loss

Sale price = $6,000

Less: Cost of acquisition (indexed) = $10,120

Capital loss = $4,120

From the above calculation, it is observed that Helen has suffered from a capital lost of

$4,120. This answer has been computed by using indexation method which is generally used to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

get a capital profit. Hence, in this scenario, it is completely on Helen which method she chooses

to calculate the amount on disposing off the asset. Also, she will have to taken into account all

the exemption and select the method which will give the expected outcome.

3) An antique jewellery piece bought on 1987 for $14,000 which was sold by Helen on

20th March 2018 for $13,000.

Solution- The asset held by Helen is long-term asset on which the capital gain or loss is

calculated as follows:

Sale price = $13,000

Less: Cost of acquisition = $14,000

Capital loss = $1,000

Indexation method can be only be used in case of gain and not in loss. In this event,

Helen has incurred a loss of $1,000, hence, she can not use indexation method (Faccio and Xu,

2015). The loss can be set from the income of assets falling in the same category. However, there

is no such income, which mandates Helen to carry forward it in future and set off against the

gain from similar assets. This provision is mentioned in section 118-10(1), according to which,

loss from collectables can be set off against a collectables only.

4) A picture was purchased by Helen's mother in March 1978 for $470 which was sold

by Helen on 1st July 2018 for $5,000.

Solution- the purchase value of the picture was $470 which is below $500 to be able to

liable for tax under this head. Therefore, capital gain by deducting the indexed value from the

sale will not be charge to text as it does not exceed $500.

Hence, from all the Helen should carry forward the loss of $1,000 and set off in future you when

there is income from same asset. This will reduces the overall income chargeable to taxation.

Question 2

Barbara who is an economist research and commenter has been approached by Eco books

limited for writing a book on economics principles however, she has never written a book about

economics principles. The offer was made by the company at $13000 which was accepted by

Barbara. After writing the book, she assigned book’s copyright for $13400 dollar to Eco Books

Ltd. She was paid when the book was published altogether, she also sold books manuscript for

$4,350 and interview manuscripts for $3,200 to Eco Books Ltd. The manuscripts are has been

to calculate the amount on disposing off the asset. Also, she will have to taken into account all

the exemption and select the method which will give the expected outcome.

3) An antique jewellery piece bought on 1987 for $14,000 which was sold by Helen on

20th March 2018 for $13,000.

Solution- The asset held by Helen is long-term asset on which the capital gain or loss is

calculated as follows:

Sale price = $13,000

Less: Cost of acquisition = $14,000

Capital loss = $1,000

Indexation method can be only be used in case of gain and not in loss. In this event,

Helen has incurred a loss of $1,000, hence, she can not use indexation method (Faccio and Xu,

2015). The loss can be set from the income of assets falling in the same category. However, there

is no such income, which mandates Helen to carry forward it in future and set off against the

gain from similar assets. This provision is mentioned in section 118-10(1), according to which,

loss from collectables can be set off against a collectables only.

4) A picture was purchased by Helen's mother in March 1978 for $470 which was sold

by Helen on 1st July 2018 for $5,000.

Solution- the purchase value of the picture was $470 which is below $500 to be able to

liable for tax under this head. Therefore, capital gain by deducting the indexed value from the

sale will not be charge to text as it does not exceed $500.

Hence, from all the Helen should carry forward the loss of $1,000 and set off in future you when

there is income from same asset. This will reduces the overall income chargeable to taxation.

Question 2

Barbara who is an economist research and commenter has been approached by Eco books

limited for writing a book on economics principles however, she has never written a book about

economics principles. The offer was made by the company at $13000 which was accepted by

Barbara. After writing the book, she assigned book’s copyright for $13400 dollar to Eco Books

Ltd. She was paid when the book was published altogether, she also sold books manuscript for

$4,350 and interview manuscripts for $3,200 to Eco Books Ltd. The manuscripts are has been

collected when she was writing the book on economics principle (Burns, Le Leuch and Sunley,

2016).

Solution- Copyright is the exclusive right of the author to give right to publication,

distributors for our other authors to use the work or content which has been written. It is an

intellectual property which requires registration so as to protect it from fraud or theft. Work of

literary nature, photographs, live performance, films, paintings and work of similar nature has

been covered under the definition of copyright. The fees charged for providing copyright is

called royalty. Royalty is treated as an income under ITAA, 1997 which is chargeable to tax.

Section 6-5 of Income Tax Assessment Act, 1997 provide start if royalty has been received in the

nature of income then it is liable to be taxed. Whereas, if it has included in the nature of capital

then and the provisions provided under section 15 to 20 of ITAA 1997 will be applicable.

Each case in this question have different treatment which are as follows:

1. the amount of $13,000 which has been offered to Barbara buy Eco books limited for

writing the book name principles of economics will be treated as her personal income.

The reason being she has never written a book on the subject and was only engaged in

research and commentator work. According to the legal provisions in provided under

ITAA 1997, an income is treated under business and profession head if it is being

conducted in the nature of business. Hence, there seems no connection of $13,000 with

business and profession income (Green, 2016).

2. The value of copyright stood at $13400 should be treated as income from other sources

due to the fact that it does not pertain to business and profession head. Author has right to

sell the right to use the content written by him/her. the income source charged for giving

the right is called royalty. In this case Barbara giving copyright to Eco Books Ltd. Should

be charged at 30%. This rate is applicable on such case it shall be included in the head

business and profession.

3. Sale of books manuscripts for $4,350 is absolutely Barbara’s personal income as she sold

it from her own wish how to make more income. No law provides that manuscript should

be sold along with copyright as it is considered as the work of personal nature which has

been carried by the author for putting right amount of work in the book. Also there is no

requirement to sell such manuscript at all, therefore, Barbara made the sale for making

personal income.

2016).

Solution- Copyright is the exclusive right of the author to give right to publication,

distributors for our other authors to use the work or content which has been written. It is an

intellectual property which requires registration so as to protect it from fraud or theft. Work of

literary nature, photographs, live performance, films, paintings and work of similar nature has

been covered under the definition of copyright. The fees charged for providing copyright is

called royalty. Royalty is treated as an income under ITAA, 1997 which is chargeable to tax.

Section 6-5 of Income Tax Assessment Act, 1997 provide start if royalty has been received in the

nature of income then it is liable to be taxed. Whereas, if it has included in the nature of capital

then and the provisions provided under section 15 to 20 of ITAA 1997 will be applicable.

Each case in this question have different treatment which are as follows:

1. the amount of $13,000 which has been offered to Barbara buy Eco books limited for

writing the book name principles of economics will be treated as her personal income.

The reason being she has never written a book on the subject and was only engaged in

research and commentator work. According to the legal provisions in provided under

ITAA 1997, an income is treated under business and profession head if it is being

conducted in the nature of business. Hence, there seems no connection of $13,000 with

business and profession income (Green, 2016).

2. The value of copyright stood at $13400 should be treated as income from other sources

due to the fact that it does not pertain to business and profession head. Author has right to

sell the right to use the content written by him/her. the income source charged for giving

the right is called royalty. In this case Barbara giving copyright to Eco Books Ltd. Should

be charged at 30%. This rate is applicable on such case it shall be included in the head

business and profession.

3. Sale of books manuscripts for $4,350 is absolutely Barbara’s personal income as she sold

it from her own wish how to make more income. No law provides that manuscript should

be sold along with copyright as it is considered as the work of personal nature which has

been carried by the author for putting right amount of work in the book. Also there is no

requirement to sell such manuscript at all, therefore, Barbara made the sale for making

personal income.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. The income of $3,200 made by selling interviews' manuscripts is again her personal

income. There was no such compulsion of conducting interview, however, Barbara did so

to make the book more efficient. Hence, income earned by selling such manuscripts will

be treated as her personal income on which the rate as given in ITAA, 1997 will be

applicable (Tran, 2015).

Question 3

In this question Patrick given his son an amount of $52,000 for seeking assistance in his

newly started business. Both were agreed that David is liable to repay his father an amount of

$58,000 at the end of 5 years. There was no formal agreement for security deposit for the sum

lent by Patrick to David. Also, Patrick told his son that there is no requirement to pay interest.

However, the full amount was paid after 2 years through a check by David. This amount

included and additional amount equal to 5% on the principal amount so borrowed (Meaning of

royalty, 2019).

Solution – An income lent a family member, relative or friend to another person who

falls in the same category and also where no such formal agreement has been made, in such case

any such transaction will be treated as personal income and to be included under the head income

from other source. In the above case, the loan which was given by Patrick to David on the basis

of repayment after expiry of 5 years. The amount was $52,000. However, David paid the amount

within 2 years from the date of lending the amount. He paid $58,000 along with the interest of

5% included in the amount. On the application of provisions provided by ITAA, 1997, the

income of $58,000 will make a part of taxable income of Patrick which will be taxed by applying

the rates of individual's income (Individual tax rates, 2019).

CONCLUSION

From the above report, it has been analyse that tax is an important factor of an economy

and a significant source of government. For proper implementation of taxation system in a

country, various laws, rules, and legislations are enacted. It is a wider in nature which comprises

of five different heads pertaining to salary, income from house property, business and profession,

capital gain and income from other sources. Also, there are deductions which gives benefit to the

taxpayer as it reduces the amount on which tax is to be calculated. Furthermore, there are

different tax slabs which applies individuals, companies and other entities.

income. There was no such compulsion of conducting interview, however, Barbara did so

to make the book more efficient. Hence, income earned by selling such manuscripts will

be treated as her personal income on which the rate as given in ITAA, 1997 will be

applicable (Tran, 2015).

Question 3

In this question Patrick given his son an amount of $52,000 for seeking assistance in his

newly started business. Both were agreed that David is liable to repay his father an amount of

$58,000 at the end of 5 years. There was no formal agreement for security deposit for the sum

lent by Patrick to David. Also, Patrick told his son that there is no requirement to pay interest.

However, the full amount was paid after 2 years through a check by David. This amount

included and additional amount equal to 5% on the principal amount so borrowed (Meaning of

royalty, 2019).

Solution – An income lent a family member, relative or friend to another person who

falls in the same category and also where no such formal agreement has been made, in such case

any such transaction will be treated as personal income and to be included under the head income

from other source. In the above case, the loan which was given by Patrick to David on the basis

of repayment after expiry of 5 years. The amount was $52,000. However, David paid the amount

within 2 years from the date of lending the amount. He paid $58,000 along with the interest of

5% included in the amount. On the application of provisions provided by ITAA, 1997, the

income of $58,000 will make a part of taxable income of Patrick which will be taxed by applying

the rates of individual's income (Individual tax rates, 2019).

CONCLUSION

From the above report, it has been analyse that tax is an important factor of an economy

and a significant source of government. For proper implementation of taxation system in a

country, various laws, rules, and legislations are enacted. It is a wider in nature which comprises

of five different heads pertaining to salary, income from house property, business and profession,

capital gain and income from other sources. Also, there are deductions which gives benefit to the

taxpayer as it reduces the amount on which tax is to be calculated. Furthermore, there are

different tax slabs which applies individuals, companies and other entities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books & Journals:

Oats, L. (Ed.). (2012). Taxation: a fieldwork research handbook. Routledge.

Woellner, R., and et. al., (2014). Australian Taxation Law 2014 (pp. 1-81).

Evans, C., Minas, J., & Lim, Y. (2015). Taxing personal capital gains in Australia: an alternative

way forward. Austl. Tax F., 30, 735.

Cui, W. (2013). Taxing indirect transfers: Improving an instrument for stemming tax and legal

base erosion. Va. Tax Rev., 33, 653.

Faccio, M., & Xu, J. (2015). Taxes and capital structure. Journal of Financial and Quantitative

Analysis, 50(3), 277-300.

Burns, L., Le Leuch, H., & Sunley, E. M. (2016). Taxing gains on transfer of interest.

In International Taxation and the Extractive Industries (pp. 176-205). Routledge.

Green, J. (2016). Australia. In Angels without Borders: Trends and Policies Shaping Angel

Investment Worldwide (pp. 163-175).

Tran, A. (2015). Can taxable income be estimated from financial reports of listed companies in

Australia. Austl. Tax F., 30, 569.

Online:

Meaning of royalty. 2019. [Online]. Available through:

<https://www.ato.gov.au/law/view/document?docid=ITR/IT2660/NAT/ATO/00001>.

Individual tax rates. 2019. [Online]. Available through:

<https://www.ato.gov.au/Rates/Individual-income-tax-rates/>.

Meaning of personal income. 2019. [Online]. Available through:

<https://www.ato.gov.au/Individuals/Tax-Return/2017/Supplementary-tax-return/

Income-questions-13-24/14-Personal-services-income-(PSI)-2017/>.

Books & Journals:

Oats, L. (Ed.). (2012). Taxation: a fieldwork research handbook. Routledge.

Woellner, R., and et. al., (2014). Australian Taxation Law 2014 (pp. 1-81).

Evans, C., Minas, J., & Lim, Y. (2015). Taxing personal capital gains in Australia: an alternative

way forward. Austl. Tax F., 30, 735.

Cui, W. (2013). Taxing indirect transfers: Improving an instrument for stemming tax and legal

base erosion. Va. Tax Rev., 33, 653.

Faccio, M., & Xu, J. (2015). Taxes and capital structure. Journal of Financial and Quantitative

Analysis, 50(3), 277-300.

Burns, L., Le Leuch, H., & Sunley, E. M. (2016). Taxing gains on transfer of interest.

In International Taxation and the Extractive Industries (pp. 176-205). Routledge.

Green, J. (2016). Australia. In Angels without Borders: Trends and Policies Shaping Angel

Investment Worldwide (pp. 163-175).

Tran, A. (2015). Can taxable income be estimated from financial reports of listed companies in

Australia. Austl. Tax F., 30, 569.

Online:

Meaning of royalty. 2019. [Online]. Available through:

<https://www.ato.gov.au/law/view/document?docid=ITR/IT2660/NAT/ATO/00001>.

Individual tax rates. 2019. [Online]. Available through:

<https://www.ato.gov.au/Rates/Individual-income-tax-rates/>.

Meaning of personal income. 2019. [Online]. Available through:

<https://www.ato.gov.au/Individuals/Tax-Return/2017/Supplementary-tax-return/

Income-questions-13-24/14-Personal-services-income-(PSI)-2017/>.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.