Taxation Report: Analysis of Daniel's Tax Liabilities and Implications

VerifiedAdded on 2020/03/16

|16

|2780

|99

Report

AI Summary

This report provides a detailed analysis of taxation principles, focusing on the Australian tax system. The first part of the report examines the residential status of an individual, Daniel, an employee of a multinational company, based on the 183-day test and other relevant criteria. It calculates his assessable income, deductions, and total tax payable, including income tax and medical levy. The second part of the report delves into fringe benefits tax (FBT) implications for an employee, Joyce, working for a holiday destination company. It analyzes various transactions, such as salary, superannuation, school fees, traveling expenses, car benefits, gym memberships, phone bills, iPads, airline lounges, and loans, determining their tax implications under the Income Tax Assessment Act and the Fringe Benefits Tax Assessment Act. The report provides calculations for car fringe benefits using both statutory formula and operating cost methods and discusses the FBT treatment of each benefit, offering a comprehensive overview of taxation in the context of employment and fringe benefits.

Running head: TAXATION

Taxation

Name of the Student:

Name of the University:

Authors Note:

Taxation

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2TAXATION

Table of Contents

Answer to Question 1......................................................................................................................3

i).......................................................................................................................................................3

ii)......................................................................................................................................................6

iii).....................................................................................................................................................7

Answer to Question 2......................................................................................................................8

a)......................................................................................................................................................8

i)...................................................................................................................................................8

Travelling expenses.........................................................................................................................9

ii)................................................................................................................................................12

b)....................................................................................................................................................13

i).................................................................................................................................................13

ii)................................................................................................................................................13

iii)...............................................................................................................................................14

Reference.......................................................................................................................................15

Table of Contents

Answer to Question 1......................................................................................................................3

i).......................................................................................................................................................3

ii)......................................................................................................................................................6

iii).....................................................................................................................................................7

Answer to Question 2......................................................................................................................8

a)......................................................................................................................................................8

i)...................................................................................................................................................8

Travelling expenses.........................................................................................................................9

ii)................................................................................................................................................12

b)....................................................................................................................................................13

i).................................................................................................................................................13

ii)................................................................................................................................................13

iii)...............................................................................................................................................14

Reference.......................................................................................................................................15

3TAXATION

Answer to Question 1

i)

The primary issue of this question is to determine the residential status for the year 2016-

2017 of Daniel who is an employee of Mining Capital Corporation, an America based

Multinational Company, whose permanent place of stay is in Malaysia but came in Australia for

the purpose of employment1.

In Australia, an individual is liable to pay tax is the person is a resident of Australia.

Thus, it is very much essential to determine the residential status of an individual in order to

compute his or her taxable income or tax liability. Taxation Ruling TR 98/17 defines the

meaning of resident that states that this rule is applicable to those individuals that falls under the

following category2:

Individuals who are migrants

Individuals associated with teaching profession

Students who came to Australia for the purpose of education

Individuals who comes to visit Australia

Employees or working profession of any foreign country who come to Australia for

employment purpose in Australia.

1 Howard, Steven J., Ross Gordon, and Sandra C. Jones. "Australian alcohol policy 2001–2013 and implications for

public health." BMC public health 14, no. 1 (2014): 848.

2 Saad, Natrah. "Tax knowledge, tax complexity and tax compliance: Taxpayers’ view." Procedia-Social and

Behavioral Sciences 109 (2014): 1069-1075.

Answer to Question 1

i)

The primary issue of this question is to determine the residential status for the year 2016-

2017 of Daniel who is an employee of Mining Capital Corporation, an America based

Multinational Company, whose permanent place of stay is in Malaysia but came in Australia for

the purpose of employment1.

In Australia, an individual is liable to pay tax is the person is a resident of Australia.

Thus, it is very much essential to determine the residential status of an individual in order to

compute his or her taxable income or tax liability. Taxation Ruling TR 98/17 defines the

meaning of resident that states that this rule is applicable to those individuals that falls under the

following category2:

Individuals who are migrants

Individuals associated with teaching profession

Students who came to Australia for the purpose of education

Individuals who comes to visit Australia

Employees or working profession of any foreign country who come to Australia for

employment purpose in Australia.

1 Howard, Steven J., Ross Gordon, and Sandra C. Jones. "Australian alcohol policy 2001–2013 and implications for

public health." BMC public health 14, no. 1 (2014): 848.

2 Saad, Natrah. "Tax knowledge, tax complexity and tax compliance: Taxpayers’ view." Procedia-Social and

Behavioral Sciences 109 (2014): 1069-1075.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4TAXATION

However, the above-mentioned category of individual in order to be declared as a resident of

Australia is subject to fulfilment of certain provisions or conditions.

In order to assess the residential status of an individual in Australia, there are four test

based on which the residential status of an individual is declared3. The four test or methods are

listed below:

1. Primary or Ordinary Test

2. Domicile Test

3. Superannuation Test

4. 183 Days Test

If the individual who is undergoing the test is satisfying any one of the following test then he/

she shall be eligible to be declared as a resident of Australia. Each of the following tests are

discussed in brief below:

1. Primary Test or Ordinary Test.

If the case is such that the individual is born in Australia and he/ she resides in Australia

since the time of birth then as per instructions provided under Australian Taxation Office the

individual is considered as an Australian resident by default and the person does not need to

apply for any further test or what so ever4.

3 Cao, Liangyue, Amanda Hosking, Michael Kouparitsas, Damian Mullaly, Xavier Rimmer, Qun Shi, Wallace Stark,

and Sebastian Wende. "Understanding the economy-wide efficiency and incidence of major Australian

taxes." Treasury WP 1 (2015).

4 Becker, Johannes, E. Reimer, and A. Rust. Klaus Vogel on Double Taxation Conventions. Kluwer Law

International, 2015.

However, the above-mentioned category of individual in order to be declared as a resident of

Australia is subject to fulfilment of certain provisions or conditions.

In order to assess the residential status of an individual in Australia, there are four test

based on which the residential status of an individual is declared3. The four test or methods are

listed below:

1. Primary or Ordinary Test

2. Domicile Test

3. Superannuation Test

4. 183 Days Test

If the individual who is undergoing the test is satisfying any one of the following test then he/

she shall be eligible to be declared as a resident of Australia. Each of the following tests are

discussed in brief below:

1. Primary Test or Ordinary Test.

If the case is such that the individual is born in Australia and he/ she resides in Australia

since the time of birth then as per instructions provided under Australian Taxation Office the

individual is considered as an Australian resident by default and the person does not need to

apply for any further test or what so ever4.

3 Cao, Liangyue, Amanda Hosking, Michael Kouparitsas, Damian Mullaly, Xavier Rimmer, Qun Shi, Wallace Stark,

and Sebastian Wende. "Understanding the economy-wide efficiency and incidence of major Australian

taxes." Treasury WP 1 (2015).

4 Becker, Johannes, E. Reimer, and A. Rust. Klaus Vogel on Double Taxation Conventions. Kluwer Law

International, 2015.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5TAXATION

2. Domicile Test.

The meaning of the word domicile is permanent place or stay or place of abode. According to

the Australian Taxation Office, an individual can be regarded as a resident of Australia, an

Australian Domicile is the individual’s permanent place of abode, or stay is in Australia.

Nevertheless if the fact is proved at any point of time by the Australian Commissioner of

Taxation that the person who is a resident of Australia resides in any other foreign country and

has a place of abode in that particular country then the individual will not have the rights to be

considered as an Australian resident5.

3. Superannuation Test.

The Superannuation Test is only applicable to the employees of the Australian Government

as per the Australian Taxation Office. The ATO confirms that government employees of

Australia those are held outside the country for the purpose of employment, they will be

considered as the resident of Australia.

4. 183 Days Test.

The last test to be performed in the process of determination of the residential status in Australia

is the 183 Days Test. The Australian Taxation Office states that any individual who come to

Australia forstaying in Australia for a period of 183 days or more, that may be with breaks or

continuously, then the person is automatically considered as a resident of Australia since the time

of his/ her arrival in Australia.

5 Petty, J. William, Sheridan Titman, Arthur J. Keown, Peter Martin, John D. Martin, and Michael

Burrow. Financial management: Principles and applications. Pearson Higher Education AU, 2015.

2. Domicile Test.

The meaning of the word domicile is permanent place or stay or place of abode. According to

the Australian Taxation Office, an individual can be regarded as a resident of Australia, an

Australian Domicile is the individual’s permanent place of abode, or stay is in Australia.

Nevertheless if the fact is proved at any point of time by the Australian Commissioner of

Taxation that the person who is a resident of Australia resides in any other foreign country and

has a place of abode in that particular country then the individual will not have the rights to be

considered as an Australian resident5.

3. Superannuation Test.

The Superannuation Test is only applicable to the employees of the Australian Government

as per the Australian Taxation Office. The ATO confirms that government employees of

Australia those are held outside the country for the purpose of employment, they will be

considered as the resident of Australia.

4. 183 Days Test.

The last test to be performed in the process of determination of the residential status in Australia

is the 183 Days Test. The Australian Taxation Office states that any individual who come to

Australia forstaying in Australia for a period of 183 days or more, that may be with breaks or

continuously, then the person is automatically considered as a resident of Australia since the time

of his/ her arrival in Australia.

5 Petty, J. William, Sheridan Titman, Arthur J. Keown, Peter Martin, John D. Martin, and Michael

Burrow. Financial management: Principles and applications. Pearson Higher Education AU, 2015.

6TAXATION

Now, as it is said in the case study that Daniel is an employee of Mining Capital

Corporation, which is an America based MNC and came to Australia for the growth of an

operation of the company located in Australia on November 1, 2016. His permanent place of

abode is in Malaysia that is his home countryand his tenure of stay is also tentative. In such

situation, it is not easy to determine his residential status for the year 2016-2017.

However, it is clear from the above discussion that Daniel cannot satisfy the ordinary test

and the domicile test. From the above discussion, it is clear that neither Daniel have born in

Australian not he is a domicile of Australia as his home country is Malaysia and used to stay

over there before entering Australia. Thus, in such case Daniel have to undergo superannuation

test and the 183 days test to be declared as an Australian resident6.

It is evident after analysing the case study that in July 2017, Daniel and his family

decided to buy a property in Perth due to the present market conditions and hence from this it can

be concluded that since November 1, 2016 till July 2017 Daniel was present in Australia which

more than 183 days. Hence as per the guidelines laid under 183 Days Test by ATO, Daniel will

be considered as a resident of Australia for the year 2016-2017 for the purpose of taxation.

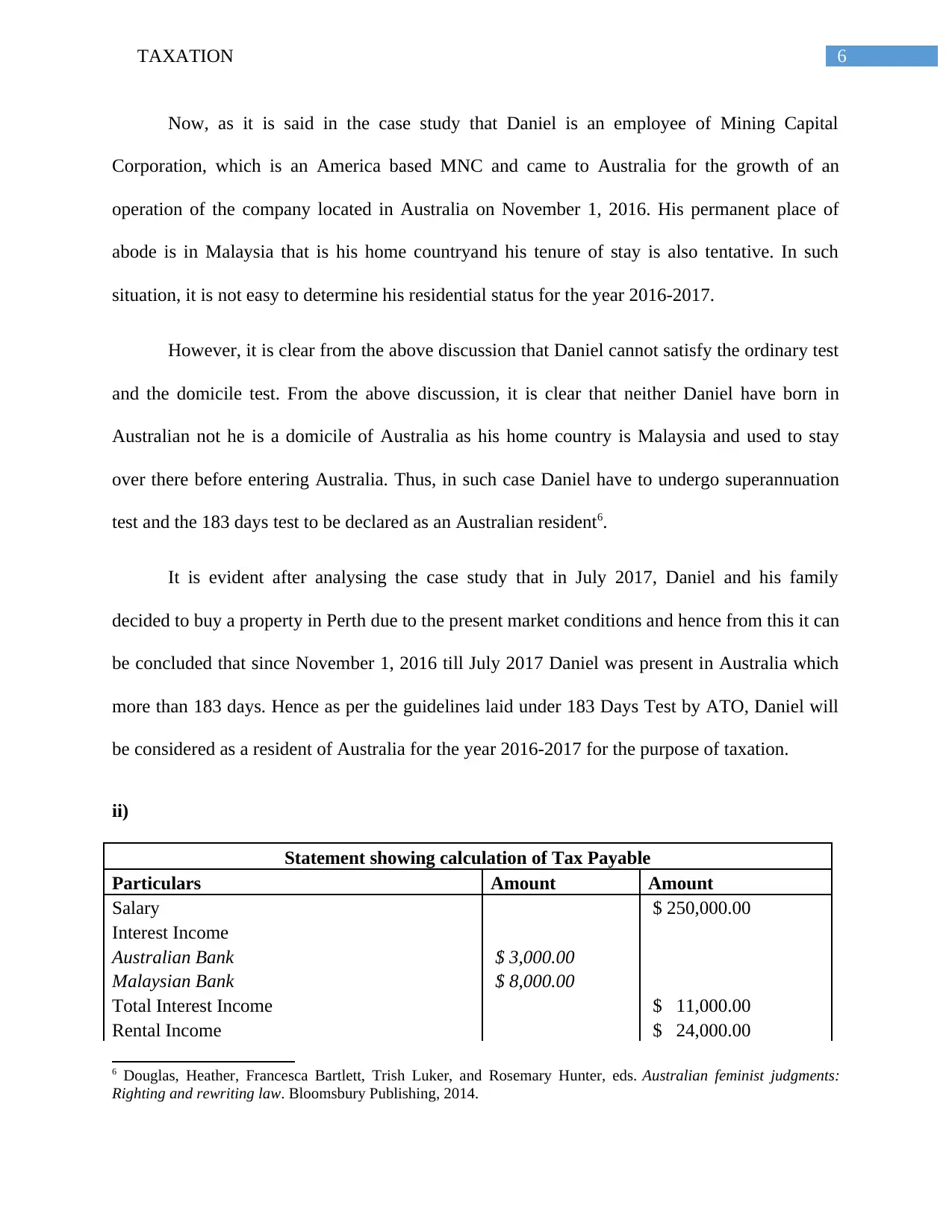

ii)

Statement showing calculation of Tax Payable

Particulars Amount Amount

Salary $ 250,000.00

Interest Income

Australian Bank $ 3,000.00

Malaysian Bank $ 8,000.00

Total Interest Income $ 11,000.00

Rental Income $ 24,000.00

6 Douglas, Heather, Francesca Bartlett, Trish Luker, and Rosemary Hunter, eds. Australian feminist judgments:

Righting and rewriting law. Bloomsbury Publishing, 2014.

Now, as it is said in the case study that Daniel is an employee of Mining Capital

Corporation, which is an America based MNC and came to Australia for the growth of an

operation of the company located in Australia on November 1, 2016. His permanent place of

abode is in Malaysia that is his home countryand his tenure of stay is also tentative. In such

situation, it is not easy to determine his residential status for the year 2016-2017.

However, it is clear from the above discussion that Daniel cannot satisfy the ordinary test

and the domicile test. From the above discussion, it is clear that neither Daniel have born in

Australian not he is a domicile of Australia as his home country is Malaysia and used to stay

over there before entering Australia. Thus, in such case Daniel have to undergo superannuation

test and the 183 days test to be declared as an Australian resident6.

It is evident after analysing the case study that in July 2017, Daniel and his family

decided to buy a property in Perth due to the present market conditions and hence from this it can

be concluded that since November 1, 2016 till July 2017 Daniel was present in Australia which

more than 183 days. Hence as per the guidelines laid under 183 Days Test by ATO, Daniel will

be considered as a resident of Australia for the year 2016-2017 for the purpose of taxation.

ii)

Statement showing calculation of Tax Payable

Particulars Amount Amount

Salary $ 250,000.00

Interest Income

Australian Bank $ 3,000.00

Malaysian Bank $ 8,000.00

Total Interest Income $ 11,000.00

Rental Income $ 24,000.00

6 Douglas, Heather, Francesca Bartlett, Trish Luker, and Rosemary Hunter, eds. Australian feminist judgments:

Righting and rewriting law. Bloomsbury Publishing, 2014.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7TAXATION

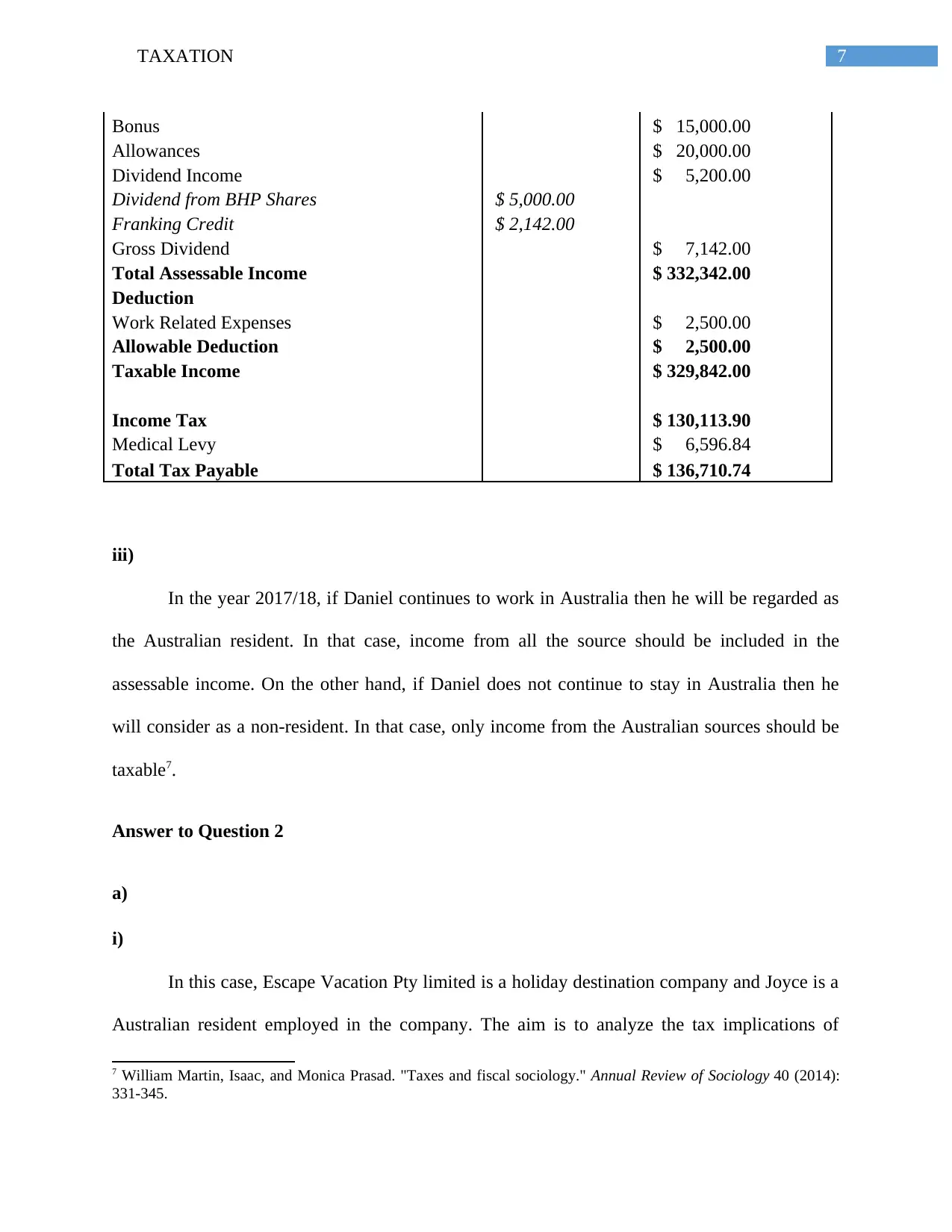

Bonus $ 15,000.00

Allowances $ 20,000.00

Dividend Income $ 5,200.00

Dividend from BHP Shares $ 5,000.00

Franking Credit $ 2,142.00

Gross Dividend $ 7,142.00

Total Assessable Income $ 332,342.00

Deduction

Work Related Expenses $ 2,500.00

Allowable Deduction $ 2,500.00

Taxable Income $ 329,842.00

Income Tax $ 130,113.90

Medical Levy $ 6,596.84

Total Tax Payable $ 136,710.74

iii)

In the year 2017/18, if Daniel continues to work in Australia then he will be regarded as

the Australian resident. In that case, income from all the source should be included in the

assessable income. On the other hand, if Daniel does not continue to stay in Australia then he

will consider as a non-resident. In that case, only income from the Australian sources should be

taxable7.

Answer to Question 2

a)

i)

In this case, Escape Vacation Pty limited is a holiday destination company and Joyce is a

Australian resident employed in the company. The aim is to analyze the tax implications of

7 William Martin, Isaac, and Monica Prasad. "Taxes and fiscal sociology." Annual Review of Sociology 40 (2014):

331-345.

Bonus $ 15,000.00

Allowances $ 20,000.00

Dividend Income $ 5,200.00

Dividend from BHP Shares $ 5,000.00

Franking Credit $ 2,142.00

Gross Dividend $ 7,142.00

Total Assessable Income $ 332,342.00

Deduction

Work Related Expenses $ 2,500.00

Allowable Deduction $ 2,500.00

Taxable Income $ 329,842.00

Income Tax $ 130,113.90

Medical Levy $ 6,596.84

Total Tax Payable $ 136,710.74

iii)

In the year 2017/18, if Daniel continues to work in Australia then he will be regarded as

the Australian resident. In that case, income from all the source should be included in the

assessable income. On the other hand, if Daniel does not continue to stay in Australia then he

will consider as a non-resident. In that case, only income from the Australian sources should be

taxable7.

Answer to Question 2

a)

i)

In this case, Escape Vacation Pty limited is a holiday destination company and Joyce is a

Australian resident employed in the company. The aim is to analyze the tax implications of

7 William Martin, Isaac, and Monica Prasad. "Taxes and fiscal sociology." Annual Review of Sociology 40 (2014):

331-345.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8TAXATION

various transactions that have been discussed in the case. The income tax implications of the

transactions are analyzed based on the Income Tax Assessment act 1936, 1997. The taxation

rulings, case laws and ATO interpretive decisions also plays an important role in the

determination of the tax implication of various transaction. The FBT implication is analyzed

based on the Fringe benefit Tax Assessment Act 19868.

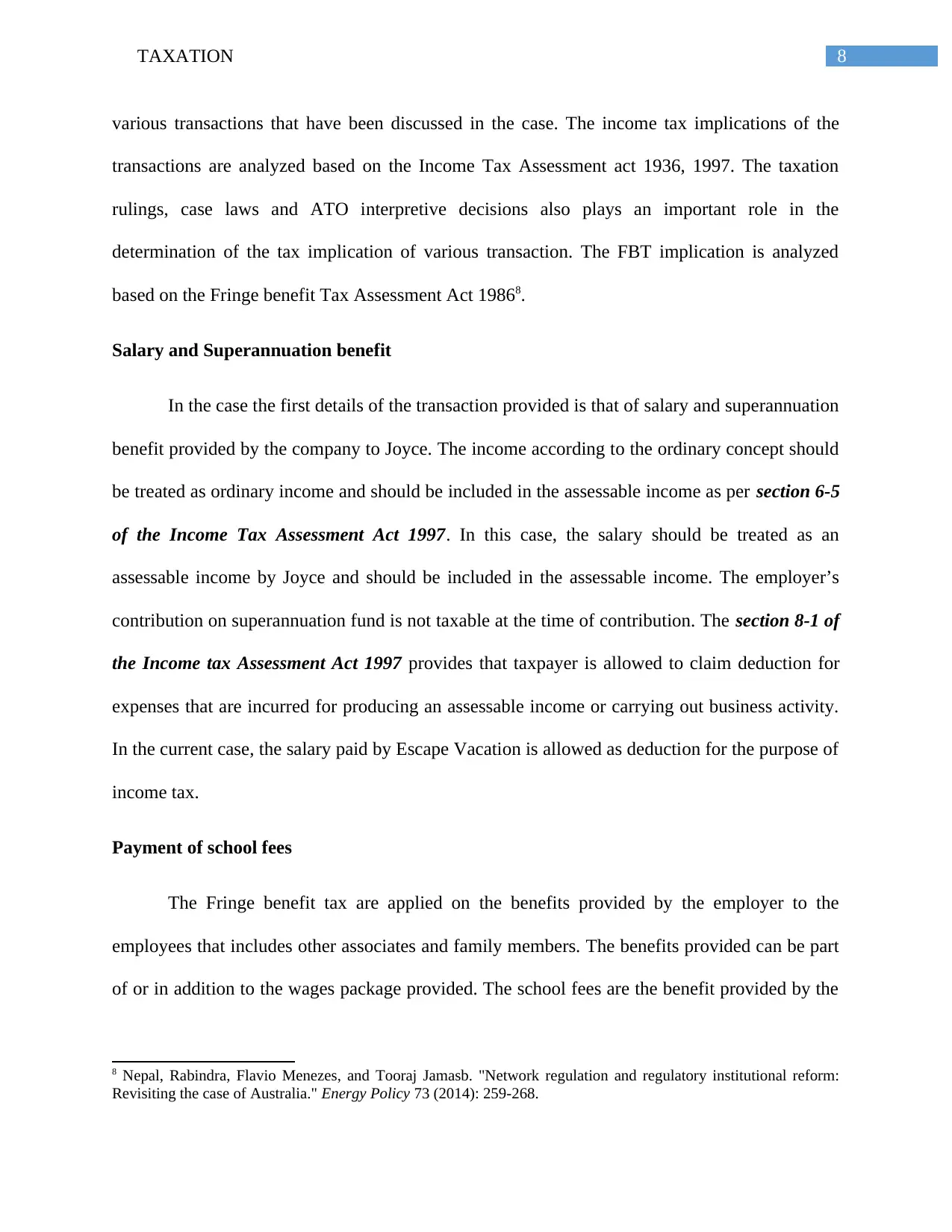

Salary and Superannuation benefit

In the case the first details of the transaction provided is that of salary and superannuation

benefit provided by the company to Joyce. The income according to the ordinary concept should

be treated as ordinary income and should be included in the assessable income as per section 6-5

of the Income Tax Assessment Act 1997. In this case, the salary should be treated as an

assessable income by Joyce and should be included in the assessable income. The employer’s

contribution on superannuation fund is not taxable at the time of contribution. The section 8-1 of

the Income tax Assessment Act 1997 provides that taxpayer is allowed to claim deduction for

expenses that are incurred for producing an assessable income or carrying out business activity.

In the current case, the salary paid by Escape Vacation is allowed as deduction for the purpose of

income tax.

Payment of school fees

The Fringe benefit tax are applied on the benefits provided by the employer to the

employees that includes other associates and family members. The benefits provided can be part

of or in addition to the wages package provided. The school fees are the benefit provided by the

8 Nepal, Rabindra, Flavio Menezes, and Tooraj Jamasb. "Network regulation and regulatory institutional reform:

Revisiting the case of Australia." Energy Policy 73 (2014): 259-268.

various transactions that have been discussed in the case. The income tax implications of the

transactions are analyzed based on the Income Tax Assessment act 1936, 1997. The taxation

rulings, case laws and ATO interpretive decisions also plays an important role in the

determination of the tax implication of various transaction. The FBT implication is analyzed

based on the Fringe benefit Tax Assessment Act 19868.

Salary and Superannuation benefit

In the case the first details of the transaction provided is that of salary and superannuation

benefit provided by the company to Joyce. The income according to the ordinary concept should

be treated as ordinary income and should be included in the assessable income as per section 6-5

of the Income Tax Assessment Act 1997. In this case, the salary should be treated as an

assessable income by Joyce and should be included in the assessable income. The employer’s

contribution on superannuation fund is not taxable at the time of contribution. The section 8-1 of

the Income tax Assessment Act 1997 provides that taxpayer is allowed to claim deduction for

expenses that are incurred for producing an assessable income or carrying out business activity.

In the current case, the salary paid by Escape Vacation is allowed as deduction for the purpose of

income tax.

Payment of school fees

The Fringe benefit tax are applied on the benefits provided by the employer to the

employees that includes other associates and family members. The benefits provided can be part

of or in addition to the wages package provided. The school fees are the benefit provided by the

8 Nepal, Rabindra, Flavio Menezes, and Tooraj Jamasb. "Network regulation and regulatory institutional reform:

Revisiting the case of Australia." Energy Policy 73 (2014): 259-268.

9TAXATION

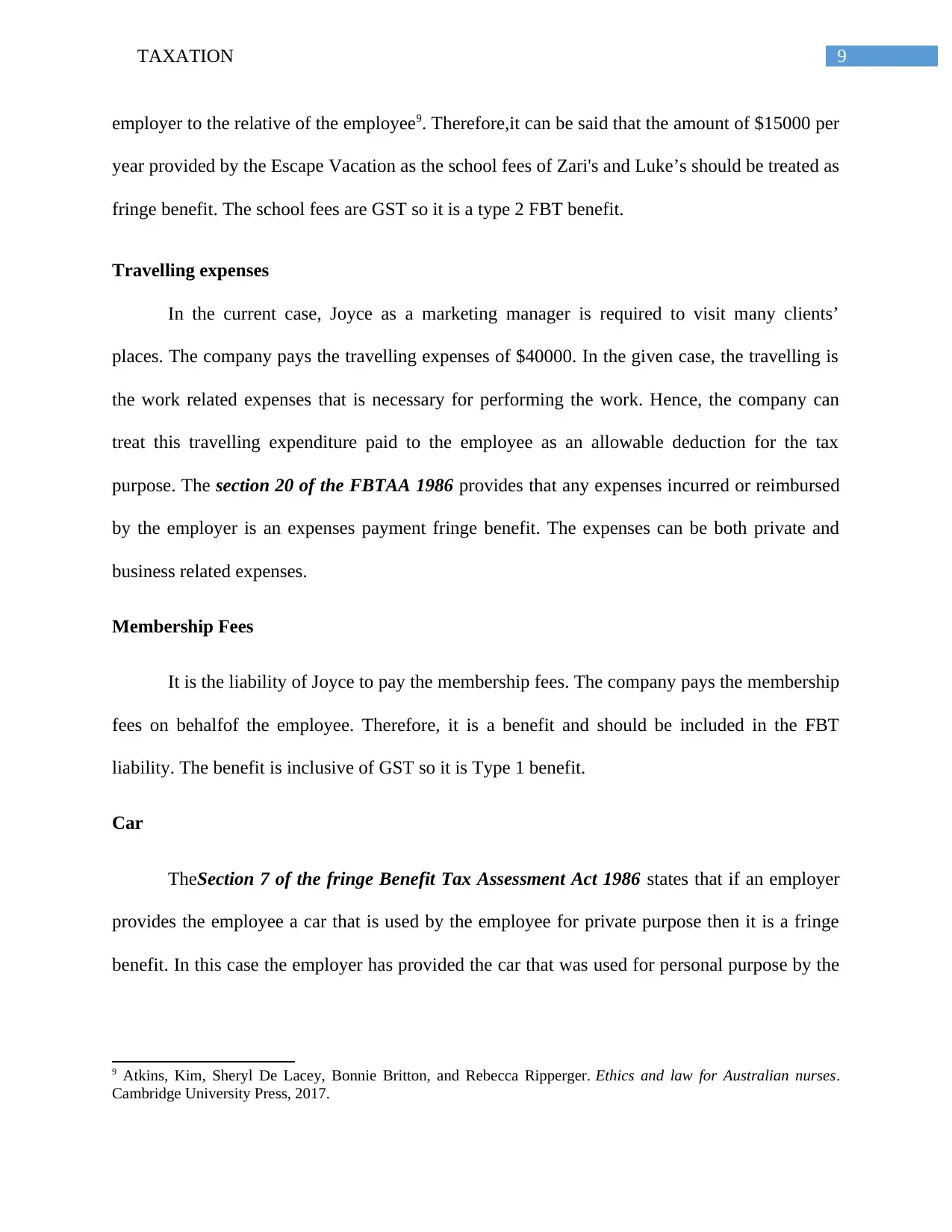

employer to the relative of the employee9. Therefore,it can be said that the amount of $15000 per

year provided by the Escape Vacation as the school fees of Zari's and Luke’s should be treated as

fringe benefit. The school fees are GST so it is a type 2 FBT benefit.

Travelling expenses

In the current case, Joyce as a marketing manager is required to visit many clients’

places. The company pays the travelling expenses of $40000. In the given case, the travelling is

the work related expenses that is necessary for performing the work. Hence, the company can

treat this travelling expenditure paid to the employee as an allowable deduction for the tax

purpose. The section 20 of the FBTAA 1986 provides that any expenses incurred or reimbursed

by the employer is an expenses payment fringe benefit. The expenses can be both private and

business related expenses.

Membership Fees

It is the liability of Joyce to pay the membership fees. The company pays the membership

fees on behalfof the employee. Therefore, it is a benefit and should be included in the FBT

liability. The benefit is inclusive of GST so it is Type 1 benefit.

Car

TheSection 7 of the fringe Benefit Tax Assessment Act 1986 states that if an employer

provides the employee a car that is used by the employee for private purpose then it is a fringe

benefit. In this case the employer has provided the car that was used for personal purpose by the

9 Atkins, Kim, Sheryl De Lacey, Bonnie Britton, and Rebecca Ripperger. Ethics and law for Australian nurses.

Cambridge University Press, 2017.

employer to the relative of the employee9. Therefore,it can be said that the amount of $15000 per

year provided by the Escape Vacation as the school fees of Zari's and Luke’s should be treated as

fringe benefit. The school fees are GST so it is a type 2 FBT benefit.

Travelling expenses

In the current case, Joyce as a marketing manager is required to visit many clients’

places. The company pays the travelling expenses of $40000. In the given case, the travelling is

the work related expenses that is necessary for performing the work. Hence, the company can

treat this travelling expenditure paid to the employee as an allowable deduction for the tax

purpose. The section 20 of the FBTAA 1986 provides that any expenses incurred or reimbursed

by the employer is an expenses payment fringe benefit. The expenses can be both private and

business related expenses.

Membership Fees

It is the liability of Joyce to pay the membership fees. The company pays the membership

fees on behalfof the employee. Therefore, it is a benefit and should be included in the FBT

liability. The benefit is inclusive of GST so it is Type 1 benefit.

Car

TheSection 7 of the fringe Benefit Tax Assessment Act 1986 states that if an employer

provides the employee a car that is used by the employee for private purpose then it is a fringe

benefit. In this case the employer has provided the car that was used for personal purpose by the

9 Atkins, Kim, Sheryl De Lacey, Bonnie Britton, and Rebecca Ripperger. Ethics and law for Australian nurses.

Cambridge University Press, 2017.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10TAXATION

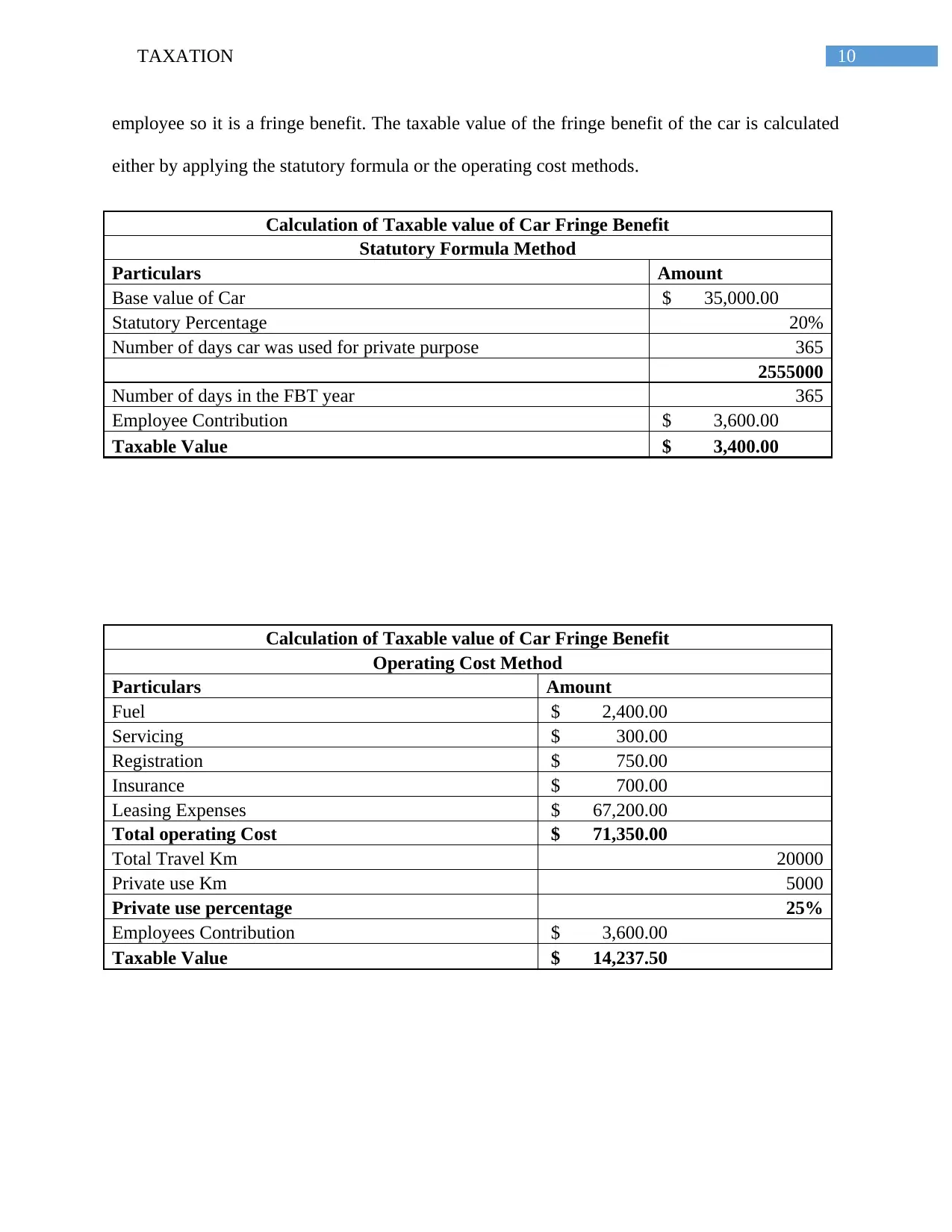

employee so it is a fringe benefit. The taxable value of the fringe benefit of the car is calculated

either by applying the statutory formula or the operating cost methods.

Calculation of Taxable value of Car Fringe Benefit

Statutory Formula Method

Particulars Amount

Base value of Car $ 35,000.00

Statutory Percentage 20%

Number of days car was used for private purpose 365

2555000

Number of days in the FBT year 365

Employee Contribution $ 3,600.00

Taxable Value $ 3,400.00

Calculation of Taxable value of Car Fringe Benefit

Operating Cost Method

Particulars Amount

Fuel $ 2,400.00

Servicing $ 300.00

Registration $ 750.00

Insurance $ 700.00

Leasing Expenses $ 67,200.00

Total operating Cost $ 71,350.00

Total Travel Km 20000

Private use Km 5000

Private use percentage 25%

Employees Contribution $ 3,600.00

Taxable Value $ 14,237.50

employee so it is a fringe benefit. The taxable value of the fringe benefit of the car is calculated

either by applying the statutory formula or the operating cost methods.

Calculation of Taxable value of Car Fringe Benefit

Statutory Formula Method

Particulars Amount

Base value of Car $ 35,000.00

Statutory Percentage 20%

Number of days car was used for private purpose 365

2555000

Number of days in the FBT year 365

Employee Contribution $ 3,600.00

Taxable Value $ 3,400.00

Calculation of Taxable value of Car Fringe Benefit

Operating Cost Method

Particulars Amount

Fuel $ 2,400.00

Servicing $ 300.00

Registration $ 750.00

Insurance $ 700.00

Leasing Expenses $ 67,200.00

Total operating Cost $ 71,350.00

Total Travel Km 20000

Private use Km 5000

Private use percentage 25%

Employees Contribution $ 3,600.00

Taxable Value $ 14,237.50

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11TAXATION

The calculation above shows that the taxable value of fringe benefit is less by using the

statutory formula method. Therefore, it can be said that the $3400 should be taken as taxable

fringe benefit.

Gym membership

The Gym membership fees paid by the employer are a benefit so FBT should be paid on

that amount. This should be treated as expense payment fringe benefit.

Phone bill

The section 20 of the Fringe Benefit Tax Assessment Act 1986 provides that if an

expense is reimbursed or paid to third party then the expenses payment should be treated as

fringe benefit.Joyce uses the mobile phone only for the purpose of business. The phone bill paid

by the company is a reimbursement of work related expenses but expenses reimbursement is

treated as fringe benefit irrespective of the fact whether it is incurred for business or private

purpose. Therefore, the phone bill paid should be treated as fringe benefit. The employer can

claim deduction for the phone bill expenses10.

IPad

The salary package can include the cost of iPad if it is primarily used for the work related

purpose. It should be noted that this benefit is an exempted Fringe benefit tax and hence FBT is

not payable.

Airline lounge

10 Atkins, Kim, Sheryl De Lacey, Bonnie Britton, and Rebecca Ripperger. Ethics and law for Australian nurses.

Cambridge University Press, 2017.

The calculation above shows that the taxable value of fringe benefit is less by using the

statutory formula method. Therefore, it can be said that the $3400 should be taken as taxable

fringe benefit.

Gym membership

The Gym membership fees paid by the employer are a benefit so FBT should be paid on

that amount. This should be treated as expense payment fringe benefit.

Phone bill

The section 20 of the Fringe Benefit Tax Assessment Act 1986 provides that if an

expense is reimbursed or paid to third party then the expenses payment should be treated as

fringe benefit.Joyce uses the mobile phone only for the purpose of business. The phone bill paid

by the company is a reimbursement of work related expenses but expenses reimbursement is

treated as fringe benefit irrespective of the fact whether it is incurred for business or private

purpose. Therefore, the phone bill paid should be treated as fringe benefit. The employer can

claim deduction for the phone bill expenses10.

IPad

The salary package can include the cost of iPad if it is primarily used for the work related

purpose. It should be noted that this benefit is an exempted Fringe benefit tax and hence FBT is

not payable.

Airline lounge

10 Atkins, Kim, Sheryl De Lacey, Bonnie Britton, and Rebecca Ripperger. Ethics and law for Australian nurses.

Cambridge University Press, 2017.

12TAXATION

In the case it is provided that Joyce is entitled to gold membership lounge of value $550.

It is furtherprovided that 20% of her trip is of private nature. Therefore,benefit that is receivedfor

private purpose should be regarded as fringe benefit and the fringe benefit tax should be applied.

. Loan

The Division 4 of the FBTAA 1986 deals with the loan fringe benefit. The interest free

loan is a fringe benefit and the company is required to pay fringe benefit tax on the amount of

taxable benefit. In order to calculate the value of benefit the current benchmark interest rate is

used for calculation.

Loan waiver benefit

If the company waive the loan of an employee then it is a loan waiver benefit. Therefore

the company is required to pay waive fringe benefit tax on that amount.

ii)

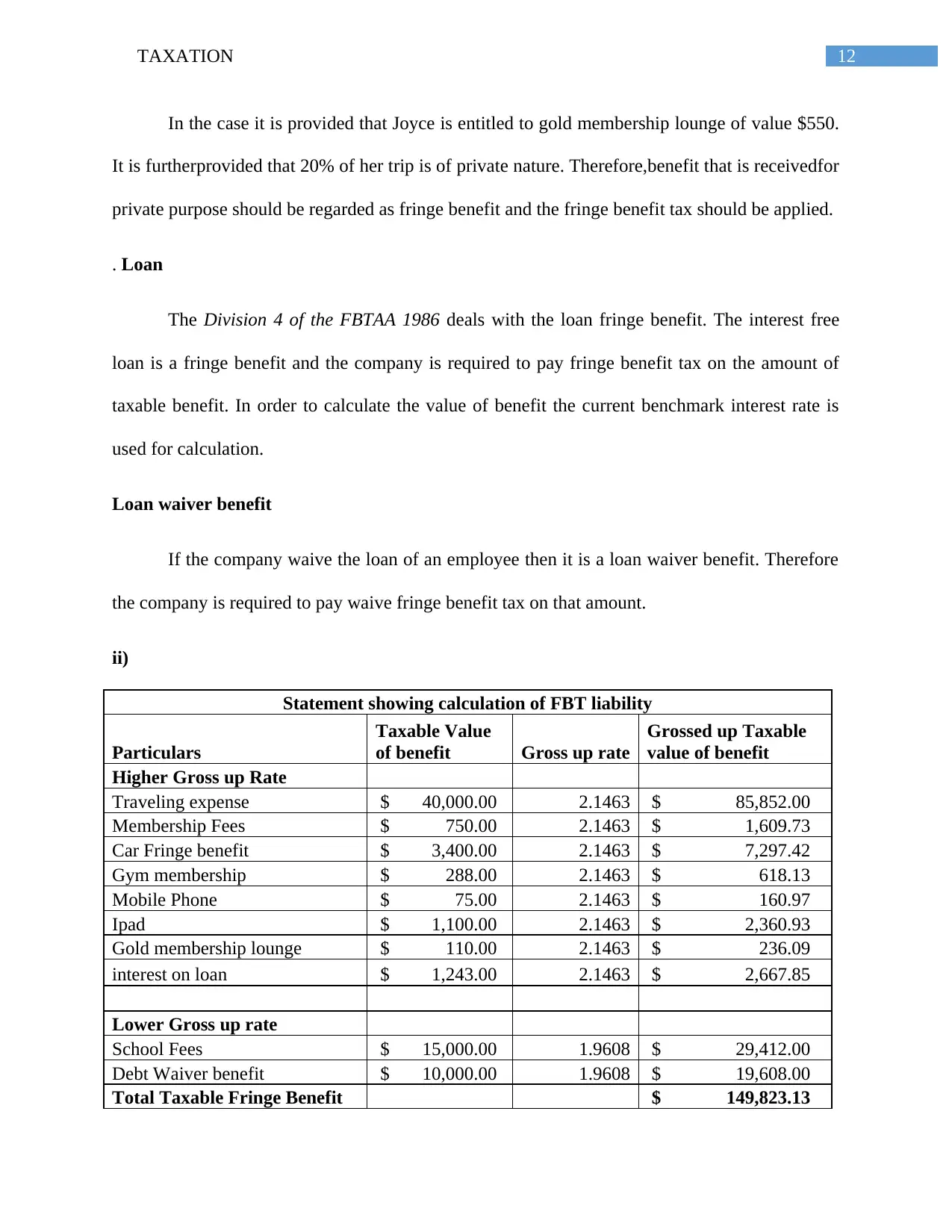

Statement showing calculation of FBT liability

Particulars

Taxable Value

of benefit Gross up rate

Grossed up Taxable

value of benefit

Higher Gross up Rate

Traveling expense $ 40,000.00 2.1463 $ 85,852.00

Membership Fees $ 750.00 2.1463 $ 1,609.73

Car Fringe benefit $ 3,400.00 2.1463 $ 7,297.42

Gym membership $ 288.00 2.1463 $ 618.13

Mobile Phone $ 75.00 2.1463 $ 160.97

Ipad $ 1,100.00 2.1463 $ 2,360.93

Gold membership lounge $ 110.00 2.1463 $ 236.09

interest on loan $ 1,243.00 2.1463 $ 2,667.85

Lower Gross up rate

School Fees $ 15,000.00 1.9608 $ 29,412.00

Debt Waiver benefit $ 10,000.00 1.9608 $ 19,608.00

Total Taxable Fringe Benefit $ 149,823.13

In the case it is provided that Joyce is entitled to gold membership lounge of value $550.

It is furtherprovided that 20% of her trip is of private nature. Therefore,benefit that is receivedfor

private purpose should be regarded as fringe benefit and the fringe benefit tax should be applied.

. Loan

The Division 4 of the FBTAA 1986 deals with the loan fringe benefit. The interest free

loan is a fringe benefit and the company is required to pay fringe benefit tax on the amount of

taxable benefit. In order to calculate the value of benefit the current benchmark interest rate is

used for calculation.

Loan waiver benefit

If the company waive the loan of an employee then it is a loan waiver benefit. Therefore

the company is required to pay waive fringe benefit tax on that amount.

ii)

Statement showing calculation of FBT liability

Particulars

Taxable Value

of benefit Gross up rate

Grossed up Taxable

value of benefit

Higher Gross up Rate

Traveling expense $ 40,000.00 2.1463 $ 85,852.00

Membership Fees $ 750.00 2.1463 $ 1,609.73

Car Fringe benefit $ 3,400.00 2.1463 $ 7,297.42

Gym membership $ 288.00 2.1463 $ 618.13

Mobile Phone $ 75.00 2.1463 $ 160.97

Ipad $ 1,100.00 2.1463 $ 2,360.93

Gold membership lounge $ 110.00 2.1463 $ 236.09

interest on loan $ 1,243.00 2.1463 $ 2,667.85

Lower Gross up rate

School Fees $ 15,000.00 1.9608 $ 29,412.00

Debt Waiver benefit $ 10,000.00 1.9608 $ 19,608.00

Total Taxable Fringe Benefit $ 149,823.13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.