University Taxation Assignment: Fringe Benefits, Income Tax, and GST

VerifiedAdded on 2020/05/16

|10

|1733

|40

Homework Assignment

AI Summary

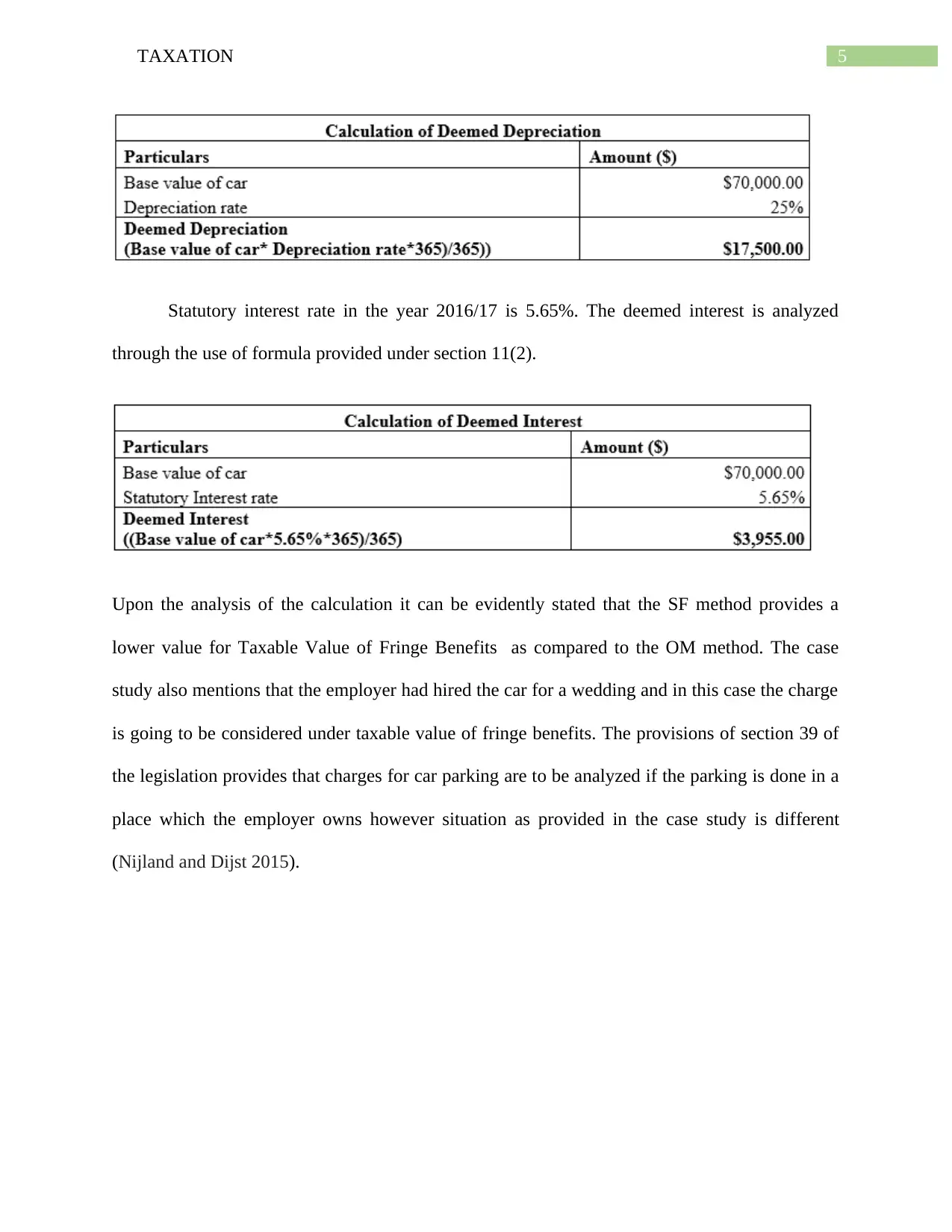

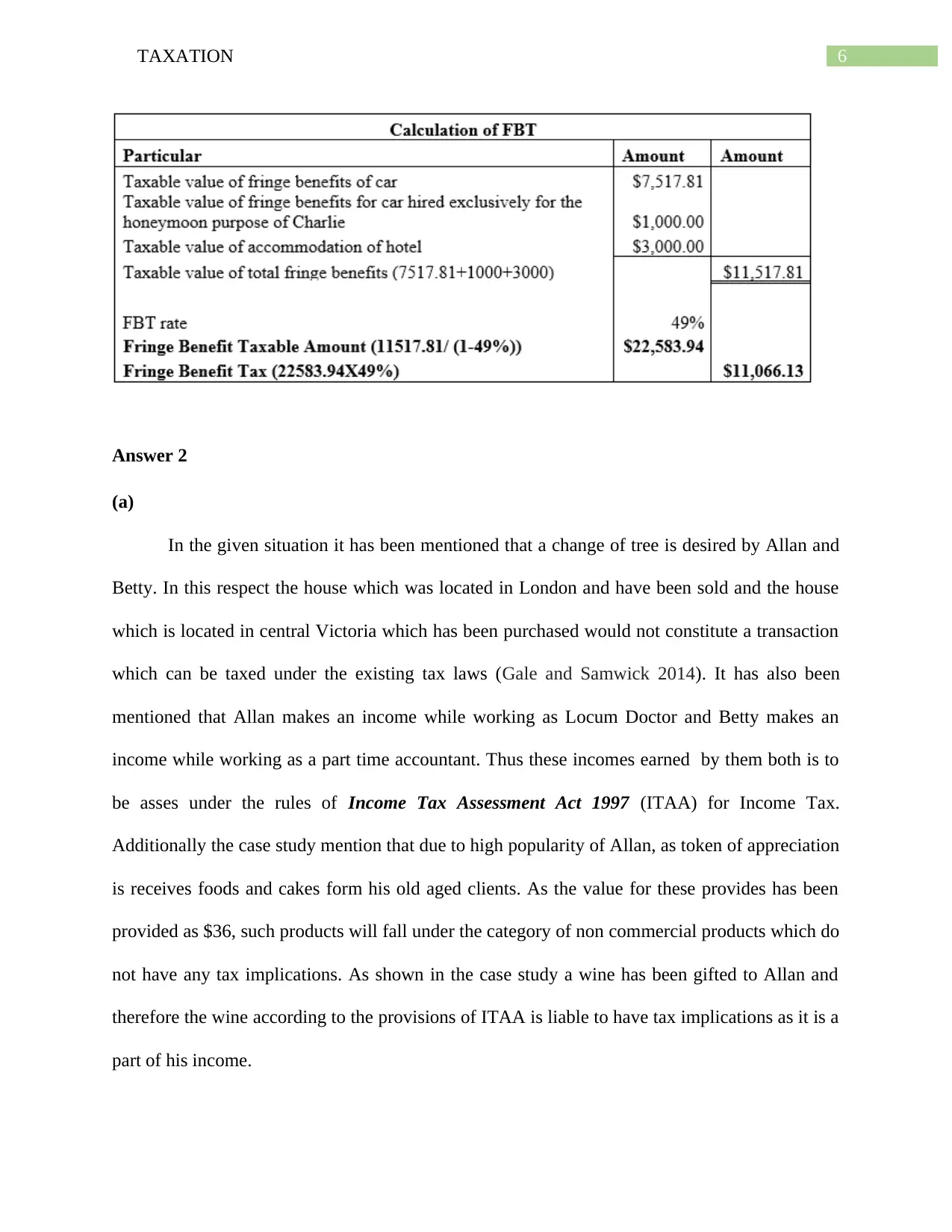

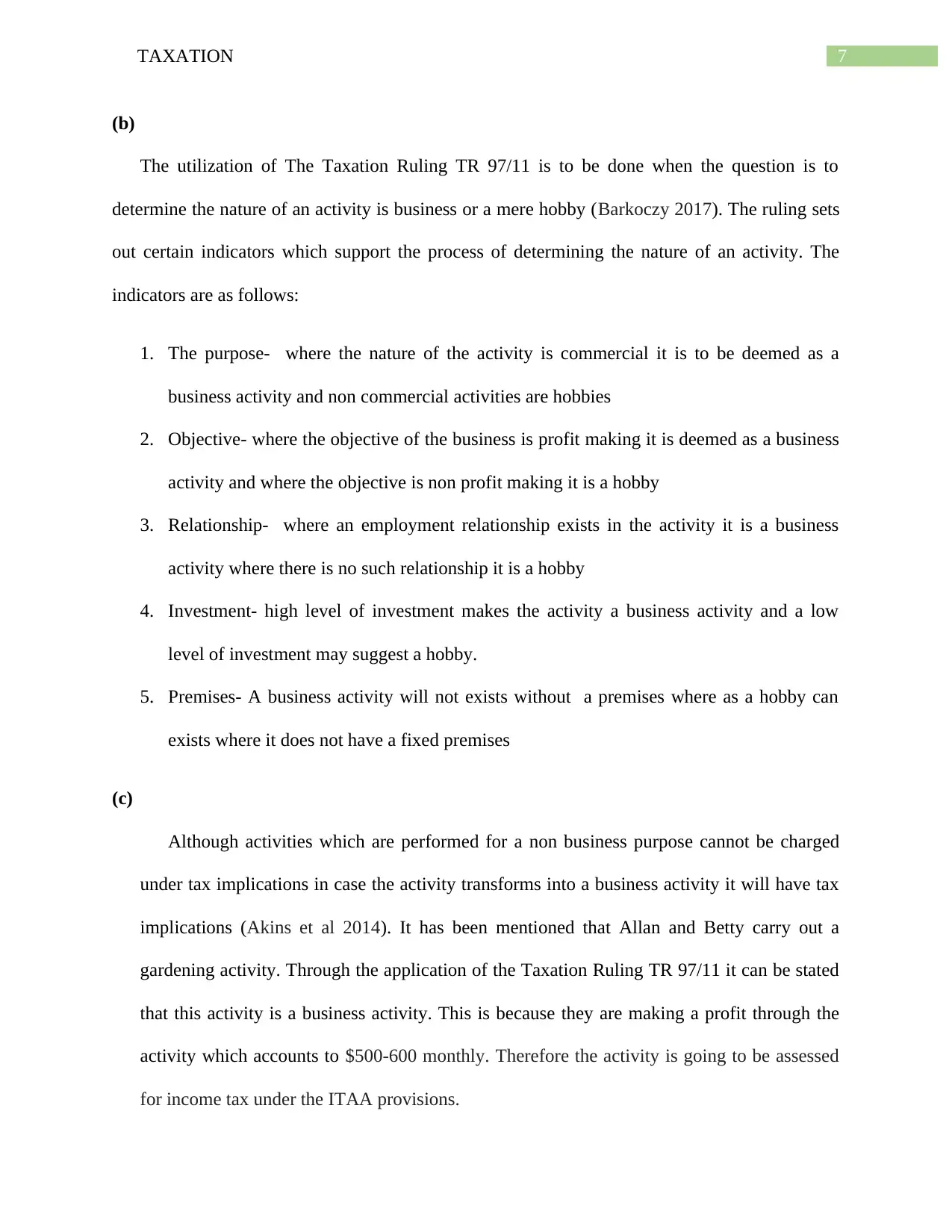

This assignment solution examines Australian taxation law, focusing on fringe benefits tax (FBTA) and income tax assessment. Answer 1 delves into fringe benefits, specifically those related to company cars, and explains the calculation of taxable value using both the statutory formula method (SFM) and the operating cost method (OCM). It analyzes case study facts, applying relevant sections of the FBTA. Answer 2 addresses income tax implications for individuals, including income from employment, gifts, and business activities. It explores the distinction between business and hobby activities using Taxation Ruling TR 97/11 and discusses the application of GST to transactions, including those conducted through a barter system. The solution references key legislation and rulings, providing a comprehensive overview of the taxation concepts.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.