Taxation Implications: Capital Gains, FBT and Tax Analysis

VerifiedAdded on 2023/06/05

|13

|2887

|302

Homework Assignment

AI Summary

This assignment delves into the intricacies of Australian taxation law, focusing on two key areas: capital gains tax (CGT) and fringe benefit tax (FBT). The first part of the assignment analyzes a client's tax implications resulting from the liquidation of various assets, determining whether the proceeds are revenue or capital, and subsequently, the application of CGT. It examines pre-CGT assets, collectables, and personal use items, calculating CGT liabilities, and considering the timing of CGT application. The second part shifts focus to fringe benefits provided by an employer (Rapid Heat) to an employee (Jasmine), specifically car fringe benefits, loan fringe benefits, and internal expense fringe benefits. The assignment outlines the relevant computations for determining FBT liabilities for the employer, referencing the Fringe Benefits Tax Assessment Act 1986 (FBTAA 1986) and considering deduction rules for loan benefits. The assignment provides a comprehensive overview of taxation principles and their practical application in real-world scenarios.

Taxation Theory, Practice & Law

Student Name

[Pick the date]

Student Name

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

Issue

The client in the given scenario has got some proceeds from liquidation od selected assets in the

current tax year. The purpose of the given analysis is to provide advice to the client in relation to

potential taxation implications of the provided transactions.

Law

Proceeds Nature

The pivotal question which assumes relevance in proceeds being derived by a taxpayer is to

ascertain the underlying nature of these proceeds. Two essential choices are presented for

proceeds being revenue or capital. Each of these possibilities could be possible based on the the

underlying case facts (Coleman, 2016). For instance, a real estate company involved in selling of

property would assume the proceeds as revenue as property is trading stock from the perspective

of the company. In contrast, if there is an individual who had purchased vacant land a decade

back and has now liquidated the same, the proceeds would be capital since there is no business

involving real estate and thereby the land would be a capital asset leading to obtaining capital

proceeds. This differentiation assumes importance owing to difference in tax treatment being

given to the two types of proceeds. In case of deriving capital proceeds, no tax is levied on the

proceeds but tax is possible on the capital gains in the process (Barkoczy, 2017).

CGT Relief

Section 149-10 has defined an asset class which is immune from CGT impact and is named as

pre-CGT asset. For an asset to be included within the ambit of this class, there is a basic

requirement of the asset purchase of being made at the time when the capital gains were ignored

from taxation fold. The requisite time period in order to ensure that above would be any time

prior to 20th September, 1985. If the purchase date of the asset belongs to this period, then CGT

liability would not arise (Coleman, 2016).

A blanket exemption is provided by the above asset category. However, there are certain other

provisions which provide exemption for certain specified assets and therefore are not so broad in

1

Issue

The client in the given scenario has got some proceeds from liquidation od selected assets in the

current tax year. The purpose of the given analysis is to provide advice to the client in relation to

potential taxation implications of the provided transactions.

Law

Proceeds Nature

The pivotal question which assumes relevance in proceeds being derived by a taxpayer is to

ascertain the underlying nature of these proceeds. Two essential choices are presented for

proceeds being revenue or capital. Each of these possibilities could be possible based on the the

underlying case facts (Coleman, 2016). For instance, a real estate company involved in selling of

property would assume the proceeds as revenue as property is trading stock from the perspective

of the company. In contrast, if there is an individual who had purchased vacant land a decade

back and has now liquidated the same, the proceeds would be capital since there is no business

involving real estate and thereby the land would be a capital asset leading to obtaining capital

proceeds. This differentiation assumes importance owing to difference in tax treatment being

given to the two types of proceeds. In case of deriving capital proceeds, no tax is levied on the

proceeds but tax is possible on the capital gains in the process (Barkoczy, 2017).

CGT Relief

Section 149-10 has defined an asset class which is immune from CGT impact and is named as

pre-CGT asset. For an asset to be included within the ambit of this class, there is a basic

requirement of the asset purchase of being made at the time when the capital gains were ignored

from taxation fold. The requisite time period in order to ensure that above would be any time

prior to 20th September, 1985. If the purchase date of the asset belongs to this period, then CGT

liability would not arise (Coleman, 2016).

A blanket exemption is provided by the above asset category. However, there are certain other

provisions which provide exemption for certain specified assets and therefore are not so broad in

1

coverage as the pre-CGT asset clause. As per s. 118-19, for a collectable to be qualified for

application of CGT on the capital gains produced, the price of asset acquisition must necessarily

be above $ 500 (Barkoczy, 2017). The corresponding minimum purchase price in case of items

meant for personal use is $ 10,000 so that CGT may be levied and if the above threshold is not

met, then no CGT is levied irrespective of the underlying capital gains realised from sale

(Wilmot, 2014).

CGT calculation

The process of CGT liability determination involves quite a few steps. The process begins when

a CGT event highlighted in s. 104-5 tends to take place. Although there is a variety of these CGT

events but the relevant CGT event from the perspective of the given scenario would be A1

considering that the client has sold several assets. Also, the underlying CGT event also

communicates the relevant methodology for deriving the potential gains or losses form asset

liquidation (Woellner, 2017).

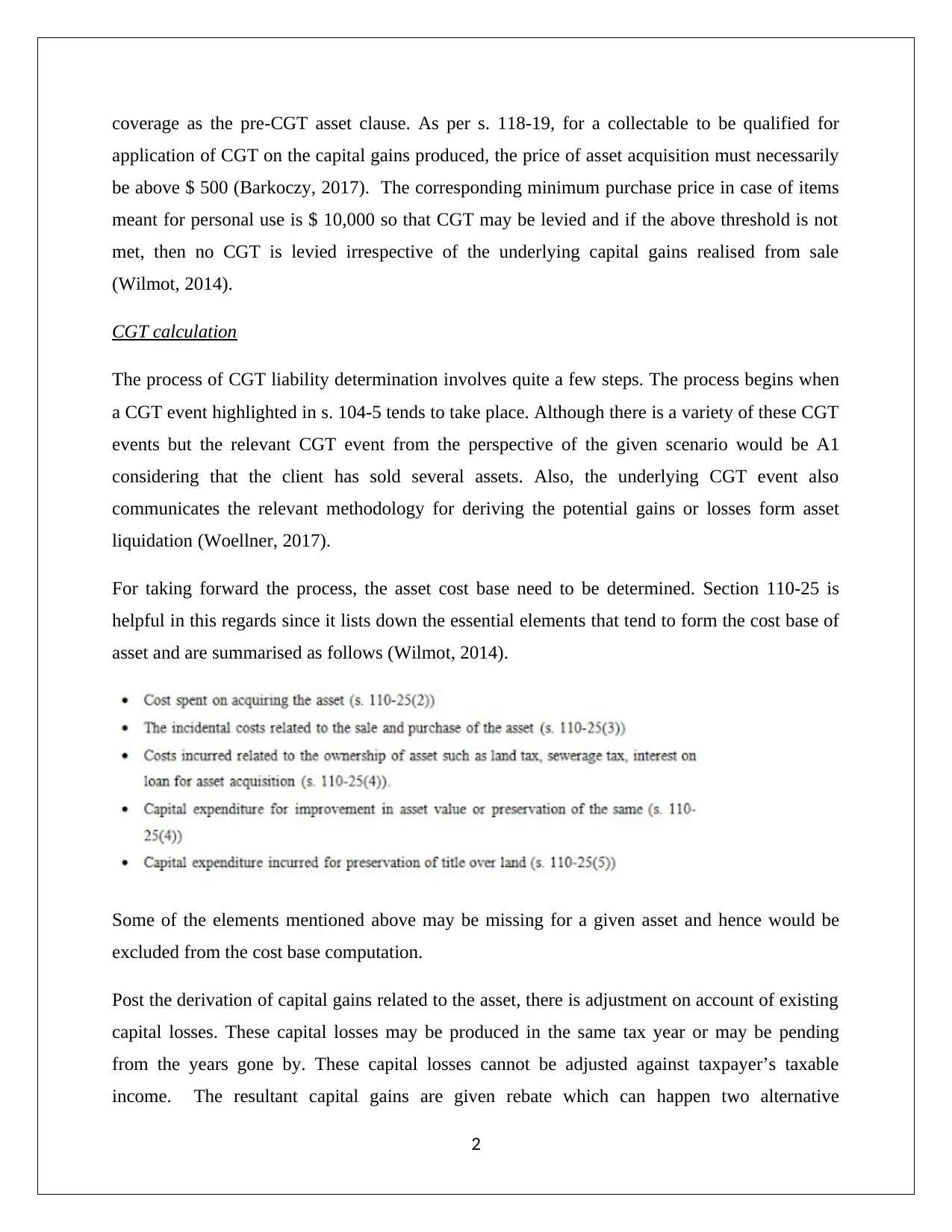

For taking forward the process, the asset cost base need to be determined. Section 110-25 is

helpful in this regards since it lists down the essential elements that tend to form the cost base of

asset and are summarised as follows (Wilmot, 2014).

Some of the elements mentioned above may be missing for a given asset and hence would be

excluded from the cost base computation.

Post the derivation of capital gains related to the asset, there is adjustment on account of existing

capital losses. These capital losses may be produced in the same tax year or may be pending

from the years gone by. These capital losses cannot be adjusted against taxpayer’s taxable

income. The resultant capital gains are given rebate which can happen two alternative

2

application of CGT on the capital gains produced, the price of asset acquisition must necessarily

be above $ 500 (Barkoczy, 2017). The corresponding minimum purchase price in case of items

meant for personal use is $ 10,000 so that CGT may be levied and if the above threshold is not

met, then no CGT is levied irrespective of the underlying capital gains realised from sale

(Wilmot, 2014).

CGT calculation

The process of CGT liability determination involves quite a few steps. The process begins when

a CGT event highlighted in s. 104-5 tends to take place. Although there is a variety of these CGT

events but the relevant CGT event from the perspective of the given scenario would be A1

considering that the client has sold several assets. Also, the underlying CGT event also

communicates the relevant methodology for deriving the potential gains or losses form asset

liquidation (Woellner, 2017).

For taking forward the process, the asset cost base need to be determined. Section 110-25 is

helpful in this regards since it lists down the essential elements that tend to form the cost base of

asset and are summarised as follows (Wilmot, 2014).

Some of the elements mentioned above may be missing for a given asset and hence would be

excluded from the cost base computation.

Post the derivation of capital gains related to the asset, there is adjustment on account of existing

capital losses. These capital losses may be produced in the same tax year or may be pending

from the years gone by. These capital losses cannot be adjusted against taxpayer’s taxable

income. The resultant capital gains are given rebate which can happen two alternative

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

mechanisms namely indexation and discount (Hodgson, Mortimer and Butler, 2016). The

application of these methods is driven by the satisfaction of the underlying conditions. For

instances, for the application of indexation method, a necessary condition is that the purchase of

asset ought to have been prior to September 1999 (Reuters, 2017). The indexation method true to

its name allows indexing the cost base to the change in the inflation rate so as to ensure that the

nominal gains are not taxed and CGT is limited to only real gains. Usually a more effective

method is discount method which has been outlined in s. 115-25 ITAA 1997 (Nethercott,

Richardson and Devos, 2016). This method allows for rebate on long term gains whereby only

50% of the gains would be considered taxable while the remaining would be ignored. The

necessary condition however, are gains being long term which can be ensured by asset holding

period to be in excess of one year (Gilders, et. al., 2015).

Timing of CGT Application

The capital asset liquidation may present a unique problem owing to the time difference between

the sale contract enactment and the proceeds being actually paid by the buyer. Due to this time

difference, a situation may arise where the above mentioned events tend to occur in two different

tax years. This presents a problem for the taxpayer in deciding as to whether the underlying CGT

implications tend to be reflected in the year of contract enactment or when the eventual proceeds

are received (Deutsch, et. al., 2015). This problem can be resolved by referring to TR 94/29

which provides clarity in this aspect by highlighting that CGT implications tend to be reported in

the same year as the asset sale contract is enacted. The proceeds may be received later.

Application

Proceeds Nature

Based on the given information, it is known that the client is not engaged in business with

regards to the given assets that have been liquidated. She is instead an investor along with being

a collector. The evidence presented clearly suggests that capital nature of the proceeds derived

from sale of assets as the client does not run any trading business. As the proceeds would be

termed as capital, therefore no tax would be attracted on these proceeds. However, any increase

or decrease in the proceeds derived when compared to the cost base would lead to the application

of CGT and resultant tax outflow.

3

application of these methods is driven by the satisfaction of the underlying conditions. For

instances, for the application of indexation method, a necessary condition is that the purchase of

asset ought to have been prior to September 1999 (Reuters, 2017). The indexation method true to

its name allows indexing the cost base to the change in the inflation rate so as to ensure that the

nominal gains are not taxed and CGT is limited to only real gains. Usually a more effective

method is discount method which has been outlined in s. 115-25 ITAA 1997 (Nethercott,

Richardson and Devos, 2016). This method allows for rebate on long term gains whereby only

50% of the gains would be considered taxable while the remaining would be ignored. The

necessary condition however, are gains being long term which can be ensured by asset holding

period to be in excess of one year (Gilders, et. al., 2015).

Timing of CGT Application

The capital asset liquidation may present a unique problem owing to the time difference between

the sale contract enactment and the proceeds being actually paid by the buyer. Due to this time

difference, a situation may arise where the above mentioned events tend to occur in two different

tax years. This presents a problem for the taxpayer in deciding as to whether the underlying CGT

implications tend to be reflected in the year of contract enactment or when the eventual proceeds

are received (Deutsch, et. al., 2015). This problem can be resolved by referring to TR 94/29

which provides clarity in this aspect by highlighting that CGT implications tend to be reported in

the same year as the asset sale contract is enacted. The proceeds may be received later.

Application

Proceeds Nature

Based on the given information, it is known that the client is not engaged in business with

regards to the given assets that have been liquidated. She is instead an investor along with being

a collector. The evidence presented clearly suggests that capital nature of the proceeds derived

from sale of assets as the client does not run any trading business. As the proceeds would be

termed as capital, therefore no tax would be attracted on these proceeds. However, any increase

or decrease in the proceeds derived when compared to the cost base would lead to the application

of CGT and resultant tax outflow.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CGT Relief

In line with the discussion in previous section, it is essential to consider the respective

acquisition date of various assets. This would lead to conclusion if any of the assets sold are pre-

CGT assets. After taking into consideration the buying data attached with the various assets, it

may be concluded that painting is that one asset which falls within the pre-CGT asset category.

Other assets in fray have their acquisition dates in a period where CGT was already applicable.

The net result is that there is no CGT burden with regards to the painting asset (Sadiq, et.al.,

2015).

In relation to the collectables, the only asset is antique bed which is successful in meeting with

the threshold value in excess of $ 500 as the underlying price paid to buy this bed was $ 3,500. In

relation to personal use item, a suitable choice would be violin. This has the features of a

collectable but the regular usage of this by client with the underlying intent to entertain herself

would imply the asset being for personal use. The acquisition of violin has been done at $ 5,500

which fails to cross the minimum threshold level in excess of $ 10,000 and the result is that

violin would have CGT exemption.

CGT calculation

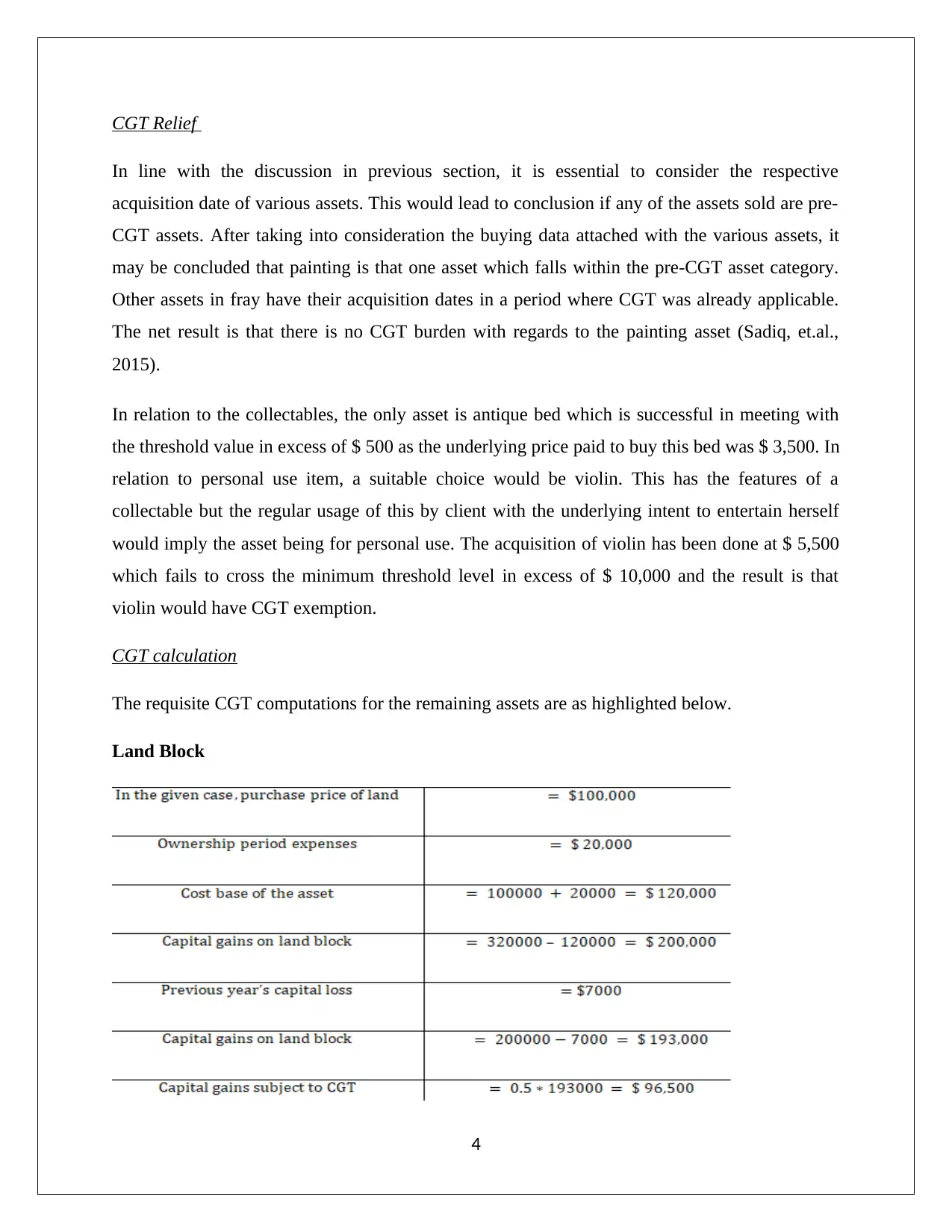

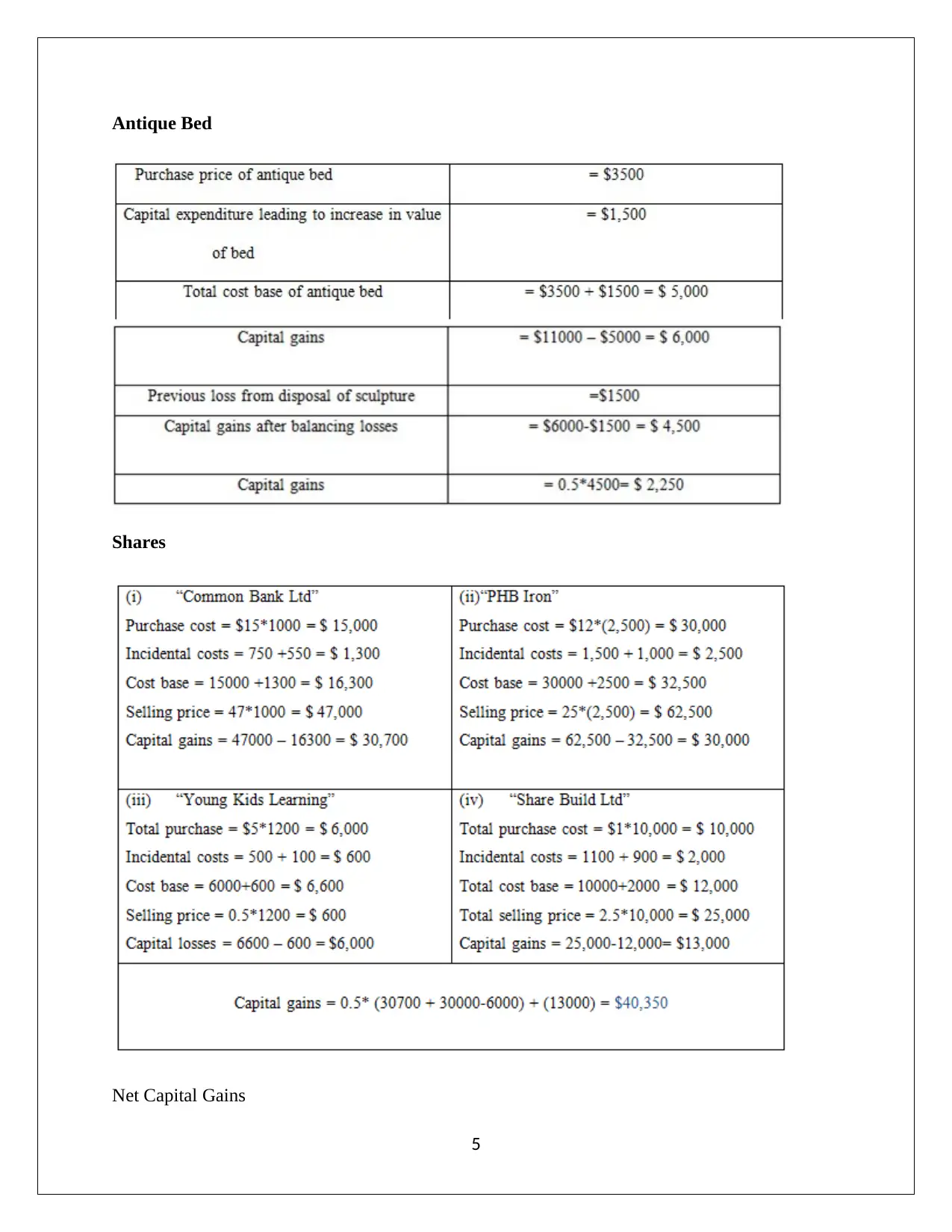

The requisite CGT computations for the remaining assets are as highlighted below.

Land Block

4

In line with the discussion in previous section, it is essential to consider the respective

acquisition date of various assets. This would lead to conclusion if any of the assets sold are pre-

CGT assets. After taking into consideration the buying data attached with the various assets, it

may be concluded that painting is that one asset which falls within the pre-CGT asset category.

Other assets in fray have their acquisition dates in a period where CGT was already applicable.

The net result is that there is no CGT burden with regards to the painting asset (Sadiq, et.al.,

2015).

In relation to the collectables, the only asset is antique bed which is successful in meeting with

the threshold value in excess of $ 500 as the underlying price paid to buy this bed was $ 3,500. In

relation to personal use item, a suitable choice would be violin. This has the features of a

collectable but the regular usage of this by client with the underlying intent to entertain herself

would imply the asset being for personal use. The acquisition of violin has been done at $ 5,500

which fails to cross the minimum threshold level in excess of $ 10,000 and the result is that

violin would have CGT exemption.

CGT calculation

The requisite CGT computations for the remaining assets are as highlighted below.

Land Block

4

Antique Bed

Shares

Net Capital Gains

5

Shares

Net Capital Gains

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

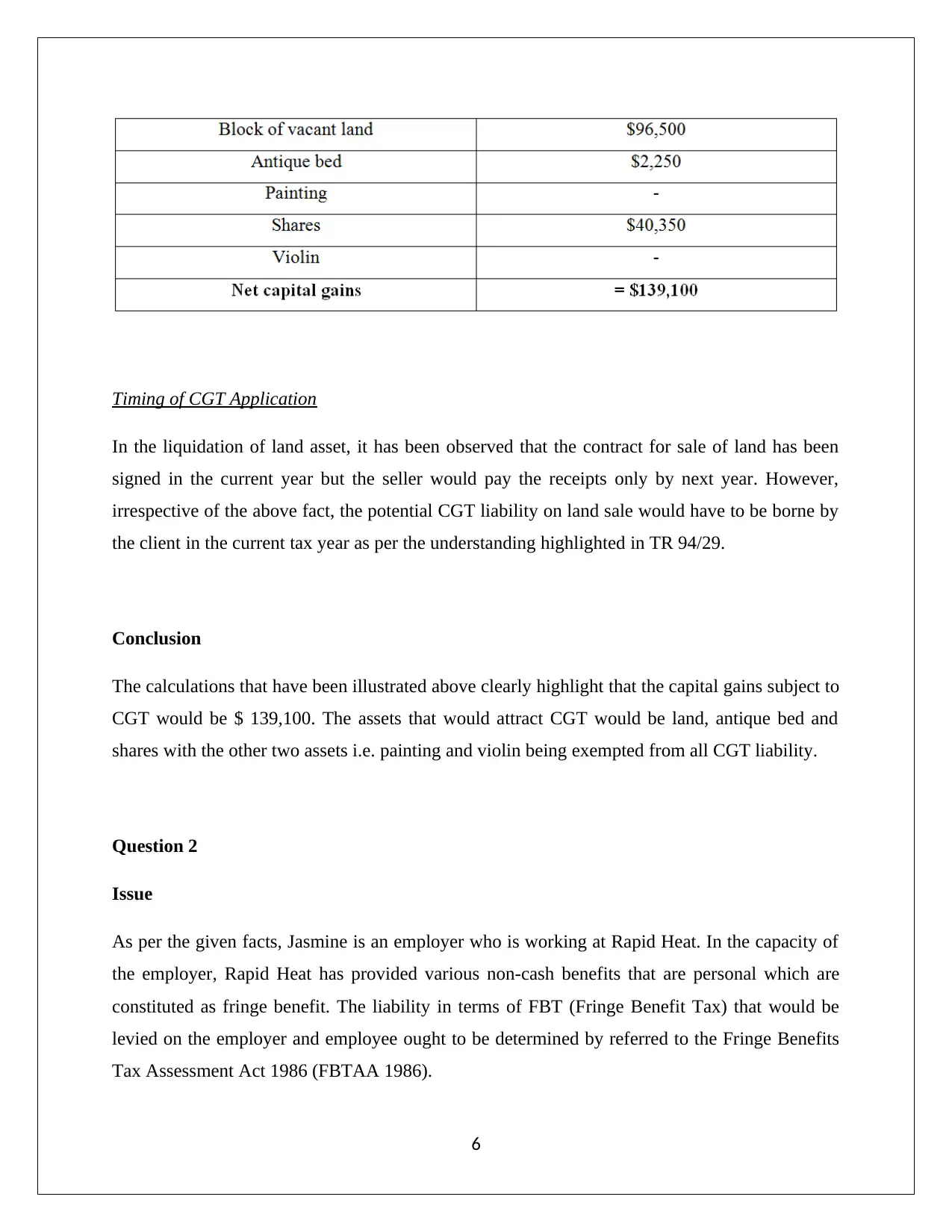

Timing of CGT Application

In the liquidation of land asset, it has been observed that the contract for sale of land has been

signed in the current year but the seller would pay the receipts only by next year. However,

irrespective of the above fact, the potential CGT liability on land sale would have to be borne by

the client in the current tax year as per the understanding highlighted in TR 94/29.

Conclusion

The calculations that have been illustrated above clearly highlight that the capital gains subject to

CGT would be $ 139,100. The assets that would attract CGT would be land, antique bed and

shares with the other two assets i.e. painting and violin being exempted from all CGT liability.

Question 2

Issue

As per the given facts, Jasmine is an employer who is working at Rapid Heat. In the capacity of

the employer, Rapid Heat has provided various non-cash benefits that are personal which are

constituted as fringe benefit. The liability in terms of FBT (Fringe Benefit Tax) that would be

levied on the employer and employee ought to be determined by referred to the Fringe Benefits

Tax Assessment Act 1986 (FBTAA 1986).

6

In the liquidation of land asset, it has been observed that the contract for sale of land has been

signed in the current year but the seller would pay the receipts only by next year. However,

irrespective of the above fact, the potential CGT liability on land sale would have to be borne by

the client in the current tax year as per the understanding highlighted in TR 94/29.

Conclusion

The calculations that have been illustrated above clearly highlight that the capital gains subject to

CGT would be $ 139,100. The assets that would attract CGT would be land, antique bed and

shares with the other two assets i.e. painting and violin being exempted from all CGT liability.

Question 2

Issue

As per the given facts, Jasmine is an employer who is working at Rapid Heat. In the capacity of

the employer, Rapid Heat has provided various non-cash benefits that are personal which are

constituted as fringe benefit. The liability in terms of FBT (Fringe Benefit Tax) that would be

levied on the employer and employee ought to be determined by referred to the Fringe Benefits

Tax Assessment Act 1986 (FBTAA 1986).

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Law

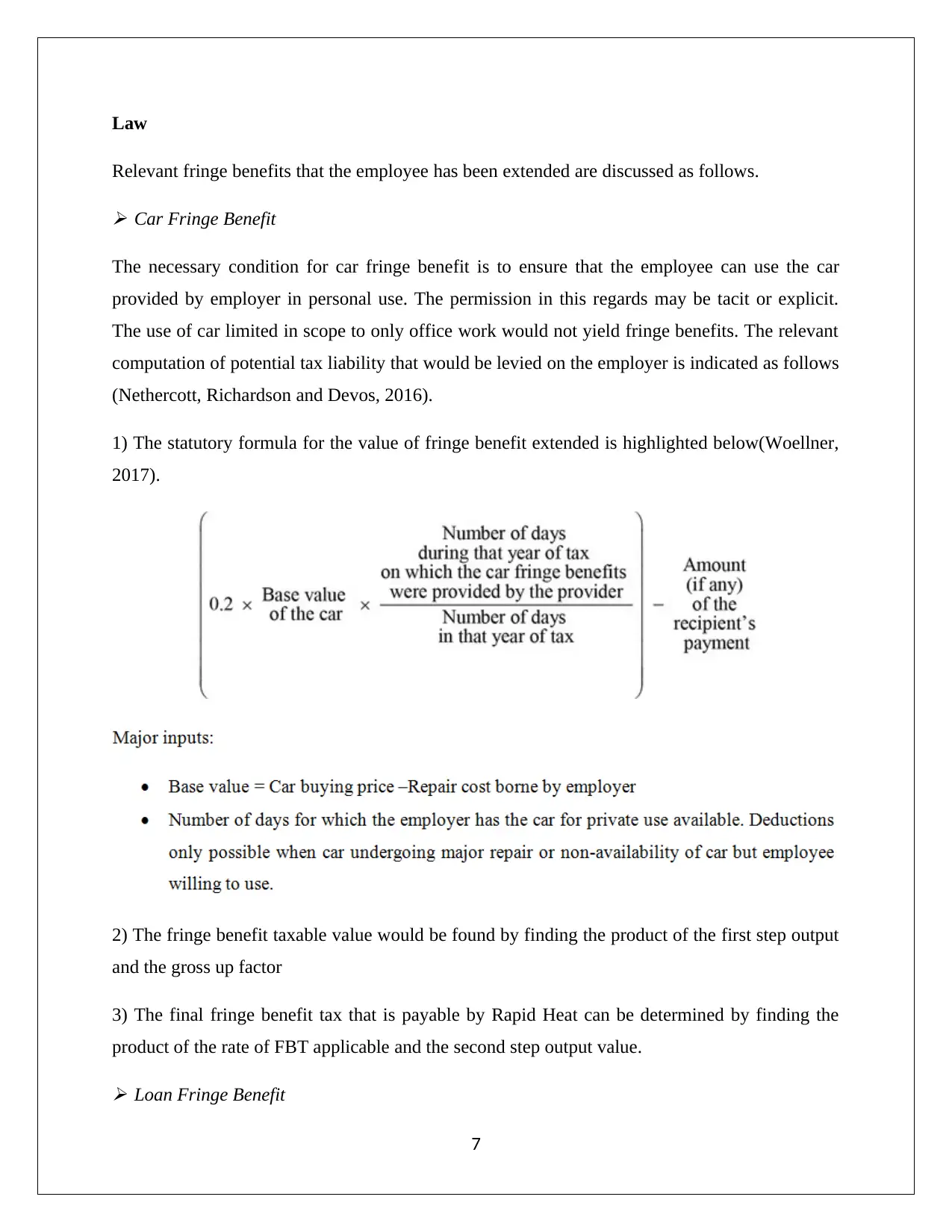

Relevant fringe benefits that the employee has been extended are discussed as follows.

Car Fringe Benefit

The necessary condition for car fringe benefit is to ensure that the employee can use the car

provided by employer in personal use. The permission in this regards may be tacit or explicit.

The use of car limited in scope to only office work would not yield fringe benefits. The relevant

computation of potential tax liability that would be levied on the employer is indicated as follows

(Nethercott, Richardson and Devos, 2016).

1) The statutory formula for the value of fringe benefit extended is highlighted below(Woellner,

2017).

2) The fringe benefit taxable value would be found by finding the product of the first step output

and the gross up factor

3) The final fringe benefit tax that is payable by Rapid Heat can be determined by finding the

product of the rate of FBT applicable and the second step output value.

Loan Fringe Benefit

7

Relevant fringe benefits that the employee has been extended are discussed as follows.

Car Fringe Benefit

The necessary condition for car fringe benefit is to ensure that the employee can use the car

provided by employer in personal use. The permission in this regards may be tacit or explicit.

The use of car limited in scope to only office work would not yield fringe benefits. The relevant

computation of potential tax liability that would be levied on the employer is indicated as follows

(Nethercott, Richardson and Devos, 2016).

1) The statutory formula for the value of fringe benefit extended is highlighted below(Woellner,

2017).

2) The fringe benefit taxable value would be found by finding the product of the first step output

and the gross up factor

3) The final fringe benefit tax that is payable by Rapid Heat can be determined by finding the

product of the rate of FBT applicable and the second step output value.

Loan Fringe Benefit

7

An essential condition for the employee to be able to avail this benefit is that the loan should be

provided to employee at low cost. This would help the employee to have savings related to

interest cost. The interest rate that the lending should be done by employer is RBA benchmark

rate. Any discount on this rate would imply that the employer has provided employees with

fringe benefits related to loan. The relevant computation of potential tax liability that would be

levied on the employer is indicated as follows (Woellner, 2017).

1) The key starting point of loan fringe benefit computation is the underlying interest savings

that employee has realised on the concessional rate considering the period for which loan has

been availed during the assessment year (Wilmot, 2014).

2) The fringe benefit taxable value would be found by finding the product of the first step output

and the gross up factor

3) The final fringe benefit tax that is payable by Rapid Heat can be determined by finding the

product of the rate of FBT applicable and the second step output value (Woellner, 2017).

Deduction Rule (s. 18) – Production of taxable income using the loan amount by employee (not

relatives or associates) would provide rebate in FBT liability to the underlying employer

(Coleman, 2016).

Internal expense fringe benefit

The help in non-cash form that employer may extend in regards to enabling meeting the

employer personal expenses are referred to expense fringe benefit. This may be carried out by

paying for any of the personal expenses of employee. One of these would be by paying the

partial amount for the purchase of good that employee is interested in purchasing from the

employer. The relevant computation of potential tax liability that would be levied on the

employer is indicated as follows (Barkoczy, 2017).

2) The fringe benefit taxable value would be found by finding the product of the first step output

and the gross up factor

8

provided to employee at low cost. This would help the employee to have savings related to

interest cost. The interest rate that the lending should be done by employer is RBA benchmark

rate. Any discount on this rate would imply that the employer has provided employees with

fringe benefits related to loan. The relevant computation of potential tax liability that would be

levied on the employer is indicated as follows (Woellner, 2017).

1) The key starting point of loan fringe benefit computation is the underlying interest savings

that employee has realised on the concessional rate considering the period for which loan has

been availed during the assessment year (Wilmot, 2014).

2) The fringe benefit taxable value would be found by finding the product of the first step output

and the gross up factor

3) The final fringe benefit tax that is payable by Rapid Heat can be determined by finding the

product of the rate of FBT applicable and the second step output value (Woellner, 2017).

Deduction Rule (s. 18) – Production of taxable income using the loan amount by employee (not

relatives or associates) would provide rebate in FBT liability to the underlying employer

(Coleman, 2016).

Internal expense fringe benefit

The help in non-cash form that employer may extend in regards to enabling meeting the

employer personal expenses are referred to expense fringe benefit. This may be carried out by

paying for any of the personal expenses of employee. One of these would be by paying the

partial amount for the purchase of good that employee is interested in purchasing from the

employer. The relevant computation of potential tax liability that would be levied on the

employer is indicated as follows (Barkoczy, 2017).

2) The fringe benefit taxable value would be found by finding the product of the first step output

and the gross up factor

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3) The final fringe benefit tax that is payable by Rapid Heat can be determined by finding the

product of the rate of FBT applicable and the second step output value (Deutsch, et.al., 2015).

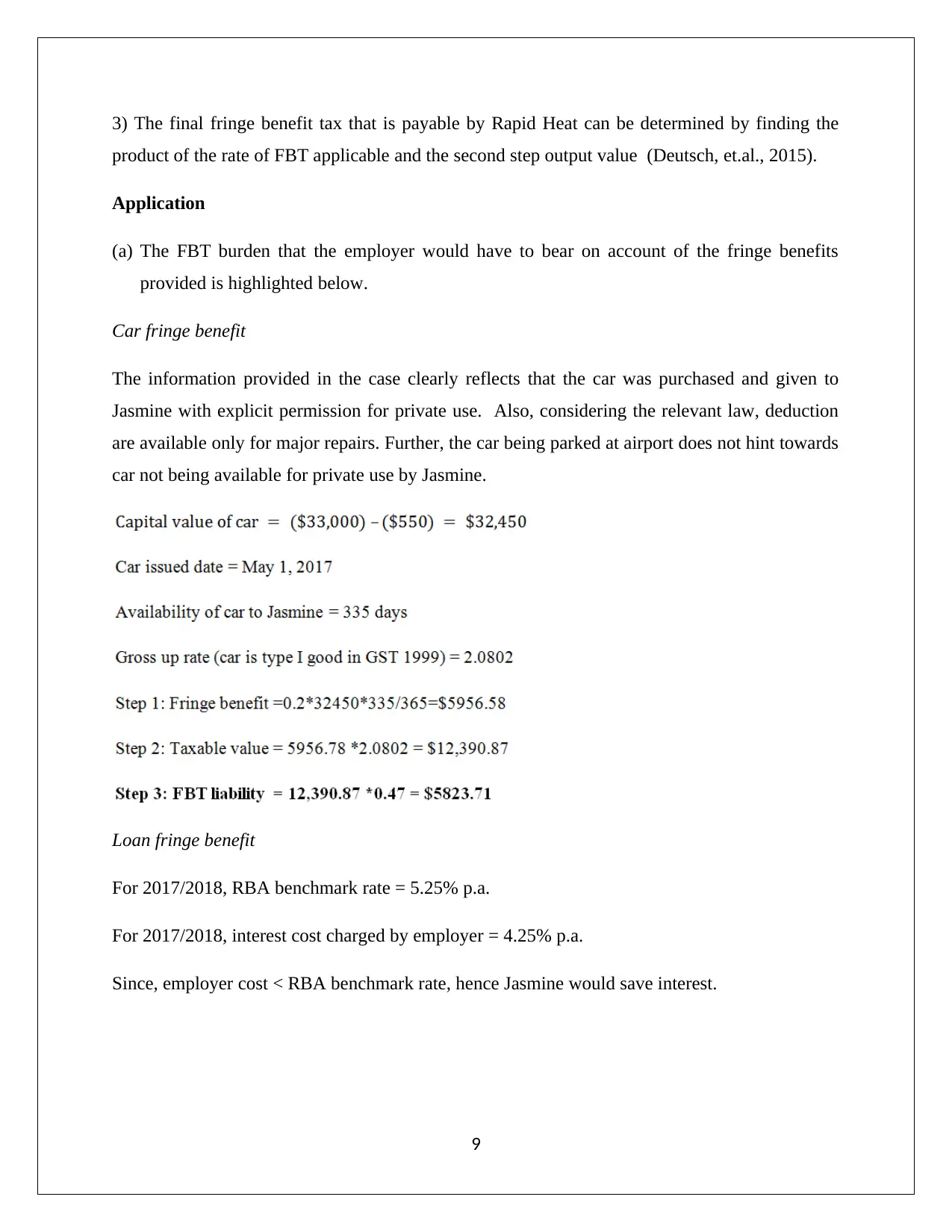

Application

(a) The FBT burden that the employer would have to bear on account of the fringe benefits

provided is highlighted below.

Car fringe benefit

The information provided in the case clearly reflects that the car was purchased and given to

Jasmine with explicit permission for private use. Also, considering the relevant law, deduction

are available only for major repairs. Further, the car being parked at airport does not hint towards

car not being available for private use by Jasmine.

Loan fringe benefit

For 2017/2018, RBA benchmark rate = 5.25% p.a.

For 2017/2018, interest cost charged by employer = 4.25% p.a.

Since, employer cost < RBA benchmark rate, hence Jasmine would save interest.

9

product of the rate of FBT applicable and the second step output value (Deutsch, et.al., 2015).

Application

(a) The FBT burden that the employer would have to bear on account of the fringe benefits

provided is highlighted below.

Car fringe benefit

The information provided in the case clearly reflects that the car was purchased and given to

Jasmine with explicit permission for private use. Also, considering the relevant law, deduction

are available only for major repairs. Further, the car being parked at airport does not hint towards

car not being available for private use by Jasmine.

Loan fringe benefit

For 2017/2018, RBA benchmark rate = 5.25% p.a.

For 2017/2018, interest cost charged by employer = 4.25% p.a.

Since, employer cost < RBA benchmark rate, hence Jasmine would save interest.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

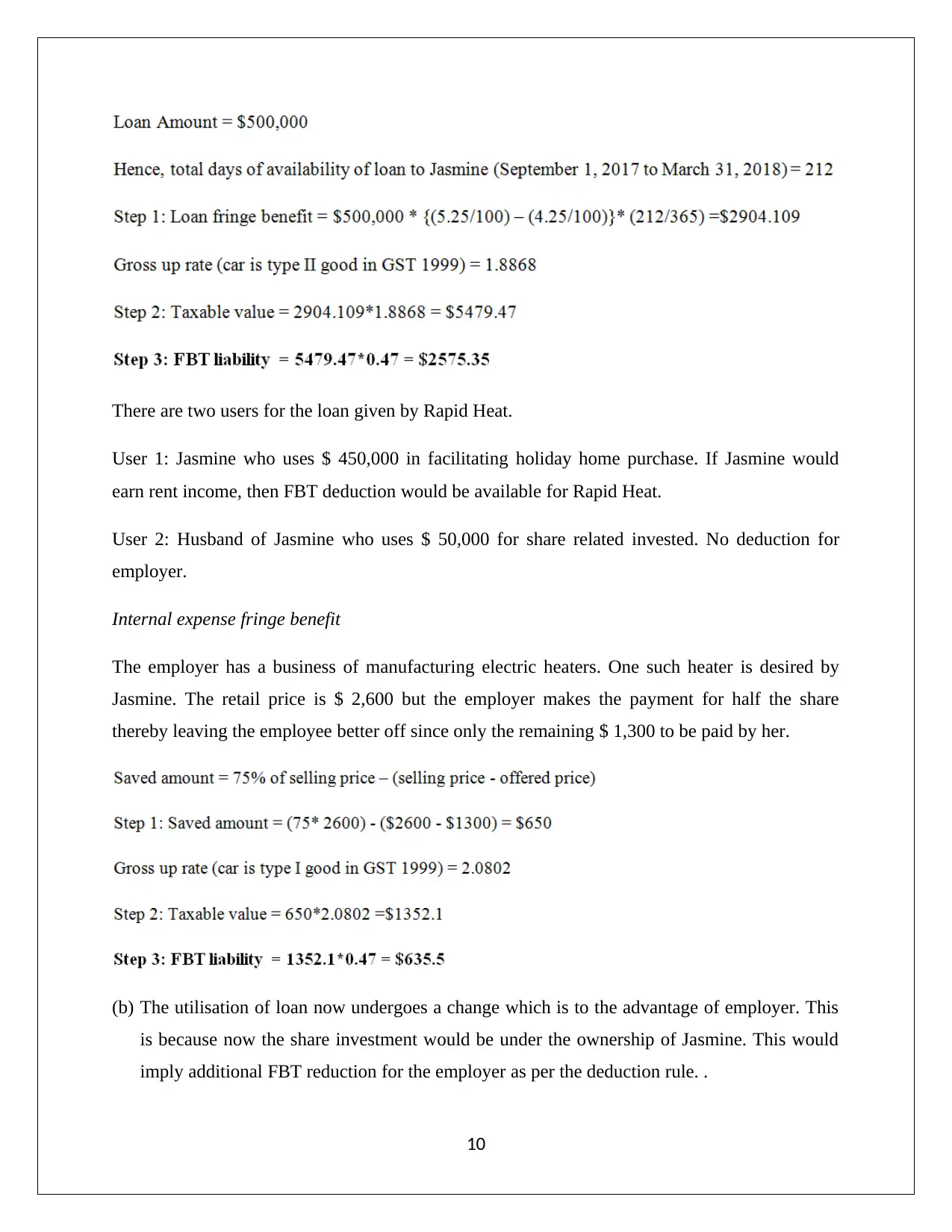

There are two users for the loan given by Rapid Heat.

User 1: Jasmine who uses $ 450,000 in facilitating holiday home purchase. If Jasmine would

earn rent income, then FBT deduction would be available for Rapid Heat.

User 2: Husband of Jasmine who uses $ 50,000 for share related invested. No deduction for

employer.

Internal expense fringe benefit

The employer has a business of manufacturing electric heaters. One such heater is desired by

Jasmine. The retail price is $ 2,600 but the employer makes the payment for half the share

thereby leaving the employee better off since only the remaining $ 1,300 to be paid by her.

(b) The utilisation of loan now undergoes a change which is to the advantage of employer. This

is because now the share investment would be under the ownership of Jasmine. This would

imply additional FBT reduction for the employer as per the deduction rule. .

10

User 1: Jasmine who uses $ 450,000 in facilitating holiday home purchase. If Jasmine would

earn rent income, then FBT deduction would be available for Rapid Heat.

User 2: Husband of Jasmine who uses $ 50,000 for share related invested. No deduction for

employer.

Internal expense fringe benefit

The employer has a business of manufacturing electric heaters. One such heater is desired by

Jasmine. The retail price is $ 2,600 but the employer makes the payment for half the share

thereby leaving the employee better off since only the remaining $ 1,300 to be paid by her.

(b) The utilisation of loan now undergoes a change which is to the advantage of employer. This

is because now the share investment would be under the ownership of Jasmine. This would

imply additional FBT reduction for the employer as per the deduction rule. .

10

Conclusion

The above analysis of the various fringe benefits provided to employee clearly highlights that all

the FBT liability would be borne by the employer and no portion of this falls on the employee.

However, possible relief for the employer can come from loan related FBT rebate provided

assessable income is produced using loan by employee.

11

The above analysis of the various fringe benefits provided to employee clearly highlights that all

the FBT liability would be borne by the employer and no portion of this falls on the employee.

However, possible relief for the employer can come from loan related FBT rebate provided

assessable income is produced using loan by employee.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.