HI6028 Taxation: Capital Gains Tax, Fringe Benefits Tax & Implications

VerifiedAdded on 2023/06/04

|14

|3587

|238

Report

AI Summary

This report provides a detailed analysis of capital gains tax (CGT) and fringe benefit tax (FBT) under Australian law. It begins by assessing the net capital gain or loss of a client based on asset sales, including vacant land, stolen antiques, paintings, and shares, referencing relevant sections of the ITAA 1997. The report then calculates the CGT liability arising from these transactions. The second part focuses on fringe benefits, specifically the provision of a car to an employee, and evaluates the FBT implications for the employer, referencing the FBTAA 1986. The analysis covers the determination of taxable values and potential exemptions, offering a comprehensive overview of the tax consequences for both the client and Rapid Heat.

Running head: TAXATION THEORY, PRACTICE AND LAW

Taxation theory, practice and law

Name of the Student:

Name of the University:

Author Note

Taxation theory, practice and law

Name of the Student:

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION THEORY, PRACTICE AND LAW

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................7

Requirement a).................................................................................................................................7

Requirement b)..............................................................................................................................10

Reference and bibliography list:....................................................................................................13

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................7

Requirement a).................................................................................................................................7

Requirement b)..............................................................................................................................10

Reference and bibliography list:....................................................................................................13

2TAXATION THEORY, PRACTICE AND LAW

Answer to Question 1:

The first requirement seeks to assess the net capital loss or net capital gain of the client

based on the information provided about its various assets during the present financial year. In

addition to this, the first requirement also addresses the consequence of income tax due to

occurrence of transactions during the particular financial year. The client provides information

about tax that a capital loss of amount $ 8500 has been carried forward from the previous year.

Sculpture sale has also resulted in a loss that is attributable from previous tax of amount $ 1500.

The section 102-20 of ITAA 1997 takes into account the fact that any capital loss or gains

arises due to happening of any transactions, activities or any capital gain tax (CGT) event.

Events concerning capital gain tax can occur in multiple occasions. The provisions for capital

gain tax are triggered by the events that lead to incurring of such taxation. There exist

considerable number of events that is common to making provisions of CGT. This involves

disposing any assets related to CGT. According to section 104-10(1) of ITAA 1997, disposition

of CGT assets results in concurrence of CGT event and such event might result in capital gain or

capital loss. Capital loss occurs when the proceeds from capital is more than the reduced cost

base of assets. Capital gain, on other hand occurs when the disposal results in lower capital

proceeds that the cost base of assets. It is said that entering into contact generates placing

importance on the CGT event in accordance with the decision of the case “Sara Lee household v

FCT (2000)”. There is no separate provision for taxing the event resulting in capital gain; instead

they are taxed with the sequence of ordinary taxation.

During a particular financial year, it is required to take into account total capital for

paying tax according to section 102-5 of ITAA 1997. The capital gains can be used by tax payer

Answer to Question 1:

The first requirement seeks to assess the net capital loss or net capital gain of the client

based on the information provided about its various assets during the present financial year. In

addition to this, the first requirement also addresses the consequence of income tax due to

occurrence of transactions during the particular financial year. The client provides information

about tax that a capital loss of amount $ 8500 has been carried forward from the previous year.

Sculpture sale has also resulted in a loss that is attributable from previous tax of amount $ 1500.

The section 102-20 of ITAA 1997 takes into account the fact that any capital loss or gains

arises due to happening of any transactions, activities or any capital gain tax (CGT) event.

Events concerning capital gain tax can occur in multiple occasions. The provisions for capital

gain tax are triggered by the events that lead to incurring of such taxation. There exist

considerable number of events that is common to making provisions of CGT. This involves

disposing any assets related to CGT. According to section 104-10(1) of ITAA 1997, disposition

of CGT assets results in concurrence of CGT event and such event might result in capital gain or

capital loss. Capital loss occurs when the proceeds from capital is more than the reduced cost

base of assets. Capital gain, on other hand occurs when the disposal results in lower capital

proceeds that the cost base of assets. It is said that entering into contact generates placing

importance on the CGT event in accordance with the decision of the case “Sara Lee household v

FCT (2000)”. There is no separate provision for taxing the event resulting in capital gain; instead

they are taxed with the sequence of ordinary taxation.

During a particular financial year, it is required to take into account total capital for

paying tax according to section 102-5 of ITAA 1997. The capital gains can be used by tax payer

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION THEORY, PRACTICE AND LAW

to offset the amount of capital loss incurred due to such event. Such capital loss resulting from

events is to be carried forward instead of deducting it in the current year. Occurrence of capital

gain tax happens when the tax payer disposes off or destroys the assets as per the section 102-20

of ITAA 1997and it is applicable on the assets that have been acquired after 20th September in

year 1985.

Sale of a block of vacant land:

One of the events that lead to happening of the capital gain tax events is selling or

acquiring a block of vacant land. Acquisition or selling of land is treated as capital assets because

it can be used for any investment or private purpose by the owner. In addition to this, disposal of

such assets results in occurrence of CGT event. Such happens when the owner enters into the

disposal contract and the owner of assets is no long in the hand of entity. In this case, selling of

block of vacant land results into disposing of such CGT assets (Yagan 2015). The land was

acquired by the clients at $ 100000 and additional expenses has been incurred of amount $ 20000

in the form of land tax, local council, sewerage and water rates during the period of land

ownership. In respect of sale of any capital assets, the owner of such assets is accounted for gain

in capital tax in accordance with the rules of Australian taxation. In this particular case, it can be

seen that owning of tax has not generated any income to taxpayer and has resulted in incurring of

expenses in the form of water and sewerage waste and municipality taxation. In addition to this,

income was generated only at the time of selling the land for amount $ 320000 and additional

amount of $ 20000 for registering the ownership change. Therefore, tax payer cannot claim any

deductions on this. Moreover, for determining the capital gain tax amount, it is required to take

into account net property cost that is arrived by incorporating the amount of expense that has

been incurred.

to offset the amount of capital loss incurred due to such event. Such capital loss resulting from

events is to be carried forward instead of deducting it in the current year. Occurrence of capital

gain tax happens when the tax payer disposes off or destroys the assets as per the section 102-20

of ITAA 1997and it is applicable on the assets that have been acquired after 20th September in

year 1985.

Sale of a block of vacant land:

One of the events that lead to happening of the capital gain tax events is selling or

acquiring a block of vacant land. Acquisition or selling of land is treated as capital assets because

it can be used for any investment or private purpose by the owner. In addition to this, disposal of

such assets results in occurrence of CGT event. Such happens when the owner enters into the

disposal contract and the owner of assets is no long in the hand of entity. In this case, selling of

block of vacant land results into disposing of such CGT assets (Yagan 2015). The land was

acquired by the clients at $ 100000 and additional expenses has been incurred of amount $ 20000

in the form of land tax, local council, sewerage and water rates during the period of land

ownership. In respect of sale of any capital assets, the owner of such assets is accounted for gain

in capital tax in accordance with the rules of Australian taxation. In this particular case, it can be

seen that owning of tax has not generated any income to taxpayer and has resulted in incurring of

expenses in the form of water and sewerage waste and municipality taxation. In addition to this,

income was generated only at the time of selling the land for amount $ 320000 and additional

amount of $ 20000 for registering the ownership change. Therefore, tax payer cannot claim any

deductions on this. Moreover, for determining the capital gain tax amount, it is required to take

into account net property cost that is arrived by incorporating the amount of expense that has

been incurred.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION THEORY, PRACTICE AND LAW

Stealing of antique bed:

The case is about loss of antique item and accounting of this rare item has been presented

under the section 108-10(2) of ITAA 1997. As per this section, losses generated from

collectables should not be used for reducing the capital gain of $ 500 and collectable is any

antique, jewellery, manuscript, artwork, rare folio and postage stamp (Butler and Calcott 2018).

For any financial year, any net capital loss or net capital gain from collectables can be used to

reduce the capital gains only from collectables. Therefore, the loss or gain from capital assets

cannot be accounted for when the collectables base price is less than $ 500.

Since, the insurance policy does not take into account antique bed as specific item and

therefore under the content policy of household, client is entitled to receive amount $ 11000.

Since the assets under this case is neither sold nor acquired, it is stolen and was not recovered

under the insurance policy.

Acquisition of painting:

Any capital loss arising from the assets for personal usage is disregarded according to

section 108-20(1) of ITAA 1997. Any capital loss arising from selling of assets for personal use

should not be accounted for computing the tax liability of client. In addition to this, any personal

asset that is acquired at a price of less than $ 10000 should be exempted from any capital gains

(Scheuer and Wolitzky 2016). Since the painting has been acquired on 21st July, 1986 that is after

1985, the painting is to be incorporated in CGT assets and moreover, such items should not be

accounted for capital gain.

Acquisition of shares:

Stealing of antique bed:

The case is about loss of antique item and accounting of this rare item has been presented

under the section 108-10(2) of ITAA 1997. As per this section, losses generated from

collectables should not be used for reducing the capital gain of $ 500 and collectable is any

antique, jewellery, manuscript, artwork, rare folio and postage stamp (Butler and Calcott 2018).

For any financial year, any net capital loss or net capital gain from collectables can be used to

reduce the capital gains only from collectables. Therefore, the loss or gain from capital assets

cannot be accounted for when the collectables base price is less than $ 500.

Since, the insurance policy does not take into account antique bed as specific item and

therefore under the content policy of household, client is entitled to receive amount $ 11000.

Since the assets under this case is neither sold nor acquired, it is stolen and was not recovered

under the insurance policy.

Acquisition of painting:

Any capital loss arising from the assets for personal usage is disregarded according to

section 108-20(1) of ITAA 1997. Any capital loss arising from selling of assets for personal use

should not be accounted for computing the tax liability of client. In addition to this, any personal

asset that is acquired at a price of less than $ 10000 should be exempted from any capital gains

(Scheuer and Wolitzky 2016). Since the painting has been acquired on 21st July, 1986 that is after

1985, the painting is to be incorporated in CGT assets and moreover, such items should not be

accounted for capital gain.

Acquisition of shares:

5TAXATION THEORY, PRACTICE AND LAW

In terms of acquisition of shares, the occurrence of CGT event arises in the event of

capital payment for shares or when it is declared that the financial instrument or shares are

worthless. Also, in event of selling of shares, there is occurrence of capital gain tax. Sale of

shares will give direct rise to capital gain and relate directly to capital receipt (Martin 2014).

Disposing or selling of shares held by client in all the organization such as Common Bank ltd,

PHB Iron ore limited, Share Bid ltd and Young Kids learning limited would give rise to capital

gain or capital loss. There is no capital loss in event of capital payment. However, capital gain

arises when the cost base of shares is more than the payment.

Violin:

An asset for personal use or that are kept for personal enjoyment is considered as capital

gain tax asset as per section 108-20(2). It does not include any structure, building and stratum

unit and is considered separately due to sub division 108-D. when the cost of acquiring the assets

for personal use is lower than $ 10000, then the taxable income does not incorporate the capital

gains that has resulted from sale of such assets. In the given case, the cost of acquiring the violin

stood at $ 5500 which is less than $ 10000. Since the selling value of violin is less than the cost

base, it is not required to take into account the capital gain in determining the tax liability (Soled

and Thomas 2016).

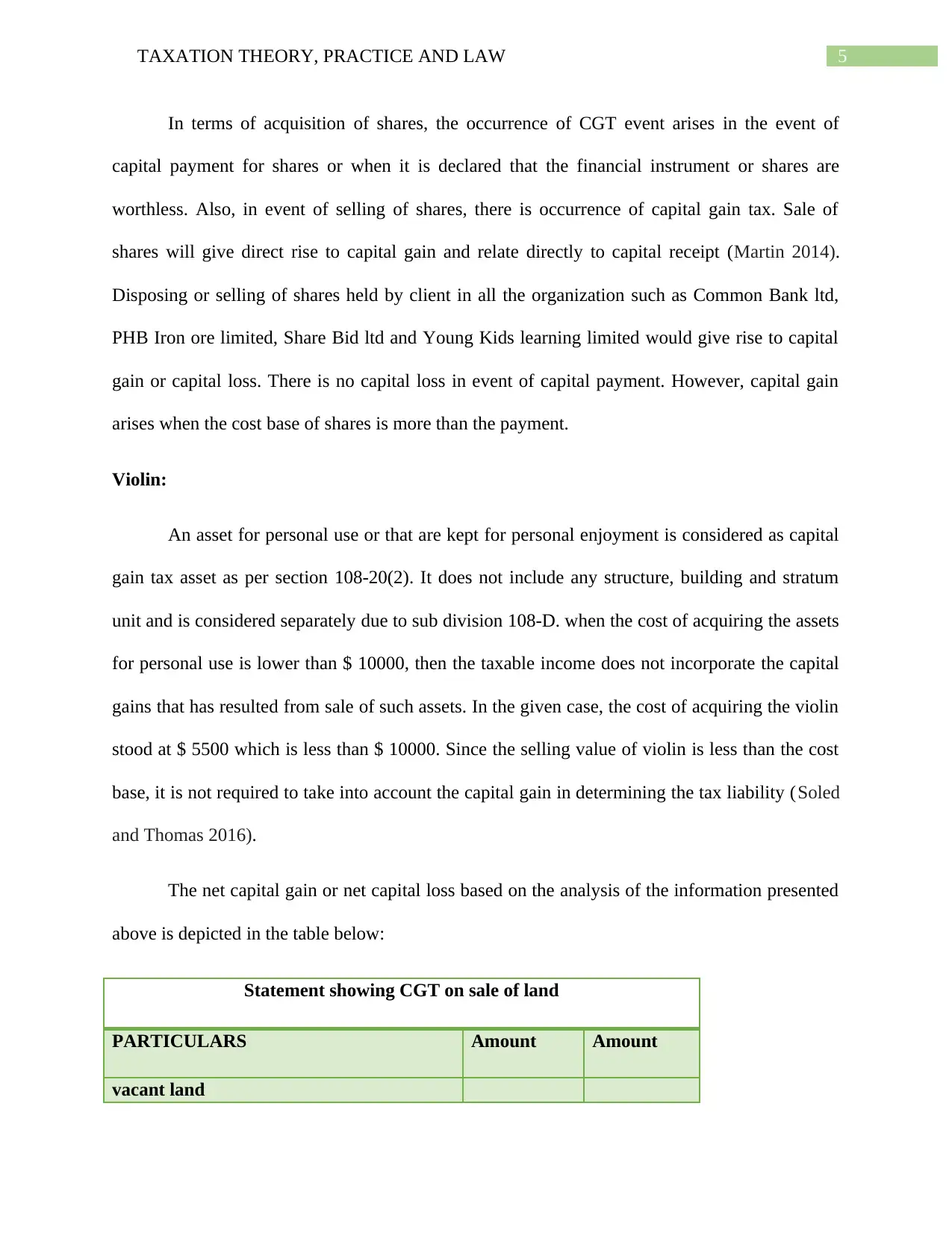

The net capital gain or net capital loss based on the analysis of the information presented

above is depicted in the table below:

Statement showing CGT on sale of land

PARTICULARS Amount Amount

vacant land

In terms of acquisition of shares, the occurrence of CGT event arises in the event of

capital payment for shares or when it is declared that the financial instrument or shares are

worthless. Also, in event of selling of shares, there is occurrence of capital gain tax. Sale of

shares will give direct rise to capital gain and relate directly to capital receipt (Martin 2014).

Disposing or selling of shares held by client in all the organization such as Common Bank ltd,

PHB Iron ore limited, Share Bid ltd and Young Kids learning limited would give rise to capital

gain or capital loss. There is no capital loss in event of capital payment. However, capital gain

arises when the cost base of shares is more than the payment.

Violin:

An asset for personal use or that are kept for personal enjoyment is considered as capital

gain tax asset as per section 108-20(2). It does not include any structure, building and stratum

unit and is considered separately due to sub division 108-D. when the cost of acquiring the assets

for personal use is lower than $ 10000, then the taxable income does not incorporate the capital

gains that has resulted from sale of such assets. In the given case, the cost of acquiring the violin

stood at $ 5500 which is less than $ 10000. Since the selling value of violin is less than the cost

base, it is not required to take into account the capital gain in determining the tax liability (Soled

and Thomas 2016).

The net capital gain or net capital loss based on the analysis of the information presented

above is depicted in the table below:

Statement showing CGT on sale of land

PARTICULARS Amount Amount

vacant land

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION THEORY, PRACTICE AND LAW

Amount received from sale of vacant land $320,000.00

Cost Base $100,000.00

Add: Ownership Expense $20,000.00

Add: Deposit $20,000.00

Total Cost Base $140,000.00

Gross Capital gain $180,000.00

50% CGT discount $90,000.00

Statement showing CGT on sale of Shares of Common Ltd

PARTICULARS Amount Amount

Proceed from Common Ltd shares

(1000@$47 per share)

$47,000.00

Less: Cost base (1000@15) $15,000.00

Less: Brokerage Fee $550.00

Less: Stamp Duty $750.00

Gross Capital gain $30,700.00

50% CGT discount $15,350.00

PARTICULARS Amount Amount

Sale proceeds $62,500.00

Less: Cost base $30,000.00

Less: Brokerage fees $1,000.00

Less: Stamp Duty $1,500.00

Gross Capital gain $30,000.00

50% CGT discount $15,000.00

Statement showing CGT on sale of Shares of Young Kids Ltd

PARTICULARS Amount Amount

Sale Proceeds $600.00

Less: Cost base $6,000.00

Less: brokerage fees $100.00

Less: stamp duty $500.00

Loss on sale of shares -$6,000.00

Amount received from sale of vacant land $320,000.00

Cost Base $100,000.00

Add: Ownership Expense $20,000.00

Add: Deposit $20,000.00

Total Cost Base $140,000.00

Gross Capital gain $180,000.00

50% CGT discount $90,000.00

Statement showing CGT on sale of Shares of Common Ltd

PARTICULARS Amount Amount

Proceed from Common Ltd shares

(1000@$47 per share)

$47,000.00

Less: Cost base (1000@15) $15,000.00

Less: Brokerage Fee $550.00

Less: Stamp Duty $750.00

Gross Capital gain $30,700.00

50% CGT discount $15,350.00

PARTICULARS Amount Amount

Sale proceeds $62,500.00

Less: Cost base $30,000.00

Less: Brokerage fees $1,000.00

Less: Stamp Duty $1,500.00

Gross Capital gain $30,000.00

50% CGT discount $15,000.00

Statement showing CGT on sale of Shares of Young Kids Ltd

PARTICULARS Amount Amount

Sale Proceeds $600.00

Less: Cost base $6,000.00

Less: brokerage fees $100.00

Less: stamp duty $500.00

Loss on sale of shares -$6,000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION THEORY, PRACTICE AND LAW

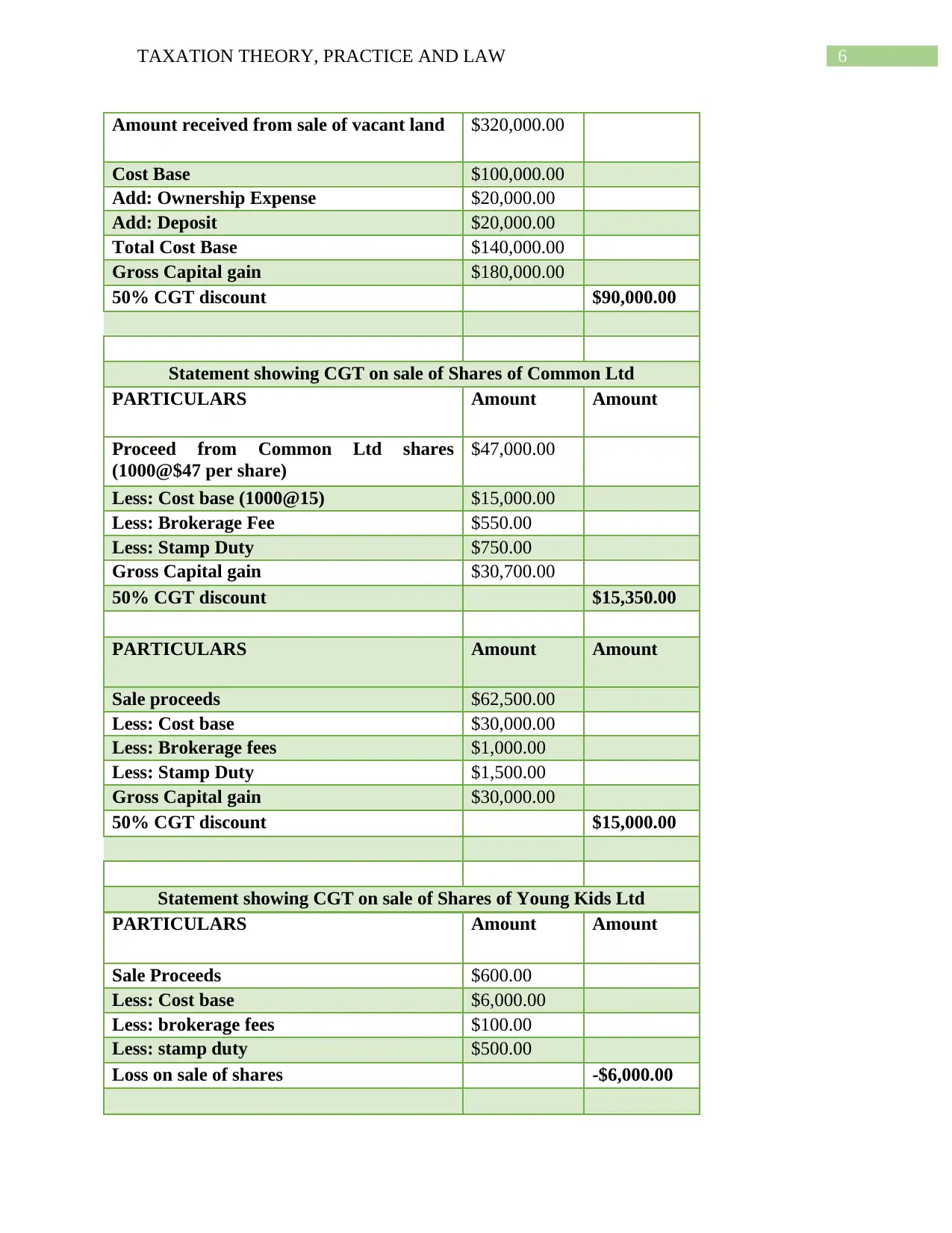

PARTICULARS Amount Amount

Sale proceeds 25000

Less: cost base 10000

Less: Brokerage fee 900

Less: Stamp duty 1100

Gross capital gain on sale of shares 13000

Statement showing total Net capital Gain

PARTICULARS Amount

CG from Vacant Land $90,000.00

CG from share of common ltd $15,350.00

CG from share of PHP Iron ore ltd $15,000.00

CG from share of Young Kid ltd -$6,000.00

CG from shares of Build Ltd $13,000.00

Total Capital Gain $127,350.00

Less: loss carry forward $7,000.00

Net Capital Gain $120,350.00

Answer to Question 2:

Requirement a)

In the given case, computation of liability of fringe benefit tax and the consequences of

the same is to be determined for advising Rapid heat. Under the Fringe benefit Income tax

assessment act 1986, assessment of the given car by company to its employee is required to be

done as she is required to a lot of travelling. Providing of car to company should be treated as

fringe benefit under the section 7 of the FBTAA 1986. Moreover, it is also required to assess that

whether the person to whom the fringe benefit is provided should bear the expense that is

incurred for parking of car. Determination of such facts under subsection A of FBTAA 1986 also

intends to identify the evaluation of the loan fringe benefits consequences (Chardon et al. 2016).

PARTICULARS Amount Amount

Sale proceeds 25000

Less: cost base 10000

Less: Brokerage fee 900

Less: Stamp duty 1100

Gross capital gain on sale of shares 13000

Statement showing total Net capital Gain

PARTICULARS Amount

CG from Vacant Land $90,000.00

CG from share of common ltd $15,350.00

CG from share of PHP Iron ore ltd $15,000.00

CG from share of Young Kid ltd -$6,000.00

CG from shares of Build Ltd $13,000.00

Total Capital Gain $127,350.00

Less: loss carry forward $7,000.00

Net Capital Gain $120,350.00

Answer to Question 2:

Requirement a)

In the given case, computation of liability of fringe benefit tax and the consequences of

the same is to be determined for advising Rapid heat. Under the Fringe benefit Income tax

assessment act 1986, assessment of the given car by company to its employee is required to be

done as she is required to a lot of travelling. Providing of car to company should be treated as

fringe benefit under the section 7 of the FBTAA 1986. Moreover, it is also required to assess that

whether the person to whom the fringe benefit is provided should bear the expense that is

incurred for parking of car. Determination of such facts under subsection A of FBTAA 1986 also

intends to identify the evaluation of the loan fringe benefits consequences (Chardon et al. 2016).

8TAXATION THEORY, PRACTICE AND LAW

Fringe benefits can be defined as the benefits that arise on part of obligations of

employees toward his or job and is provided in addition to the salaries or ordinary wages given.

The amount of individual fringe benefit provided by employer is the addition of all the taxation

values for fringe benefits in relation to taxation year. The law says that such benefit arises due to

the result of job entitlement and as a result of job of employees. The section 7 of the FBTAA

1986 says that such fringe benefit arises due to the employer and employees relationship

(Auerbach and Hassett 2015). In the given case, employer has provided car to its employee

where the benefits are held by employee in relation to its job obligations. Under the given case,

providing of car by employer is treated as fringe benefit. It is provided under the subsection

136(1) of the FBTAA 1986 that usage of car by employee or any of the associated will be

considered as fringe benefits. However, if the employee is using the car for his personal use and

no such assessable income is gained by employees, then there will be application of fringe tax of

such benefits derived. Benefits derived from using car are considered as an exempt benefit in the

year of tax in respect to the current employee employment. However, the section 86-60 of the

ITAA Act, 1997 says that such amount cannot be deducted by the person providing benefits for

the benefits being provided (Ato.gov.au 2018).

The subsection B 22A of FBTAA 1986 takes into account the fringe benefits expenses.

Expenses on the fringe benefits are the amount which the employees incur and the employer

should make the reimbursement of such amount. Such costs can be incurred on part of both

official and private reasons which might not incorporate any activities relating to official purpose

(Heathcote and Perri 2016). Therefore, the rule concerning the fringe benefits says that an

employee incurring expenses in terms of such benefit, it is entitled by employer under the title

Fringe benefits can be defined as the benefits that arise on part of obligations of

employees toward his or job and is provided in addition to the salaries or ordinary wages given.

The amount of individual fringe benefit provided by employer is the addition of all the taxation

values for fringe benefits in relation to taxation year. The law says that such benefit arises due to

the result of job entitlement and as a result of job of employees. The section 7 of the FBTAA

1986 says that such fringe benefit arises due to the employer and employees relationship

(Auerbach and Hassett 2015). In the given case, employer has provided car to its employee

where the benefits are held by employee in relation to its job obligations. Under the given case,

providing of car by employer is treated as fringe benefit. It is provided under the subsection

136(1) of the FBTAA 1986 that usage of car by employee or any of the associated will be

considered as fringe benefits. However, if the employee is using the car for his personal use and

no such assessable income is gained by employees, then there will be application of fringe tax of

such benefits derived. Benefits derived from using car are considered as an exempt benefit in the

year of tax in respect to the current employee employment. However, the section 86-60 of the

ITAA Act, 1997 says that such amount cannot be deducted by the person providing benefits for

the benefits being provided (Ato.gov.au 2018).

The subsection B 22A of FBTAA 1986 takes into account the fringe benefits expenses.

Expenses on the fringe benefits are the amount which the employees incur and the employer

should make the reimbursement of such amount. Such costs can be incurred on part of both

official and private reasons which might not incorporate any activities relating to official purpose

(Heathcote and Perri 2016). Therefore, the rule concerning the fringe benefits says that an

employee incurring expenses in terms of such benefit, it is entitled by employer under the title

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION THEORY, PRACTICE AND LAW

expense fringe benefit to reimburse the amount. Therefore, it is required to tax the amount that is

reimbursed by the employer.

The subsection B 39C of FBTAA 1986 takes into account the taxable value attributable

from car fringe benefits. The fringe benefit of car in relation to particular taxation year is held by

person receiving the benefits. Initiation of car fringe benefits arises in association with the

premises that are arranged within one kilometer or for lowering down the cost (Bhaduri et al.

2015). There are some additional circumstances when the fringe benefits can happen and they

are as follows:

During employment course, employer has taken the car

Car parking is done in a day for more than four hours.

Car is used by employer for travelling to office from home at least in a day.

Car parking within the company premises

Jasmine is provided with the car because of her job demand and she can use the car for

private reasons. Holding of such car for both private and official purpose is giving rise to fringe

benefits according to the subsection 136(1) of FBTAA 1986. Using of private car has resulted in

fringe benefits according to FBTAA 1986 in the case of “FCT v Lunney (1958). In addition to

this, expenses incurred by Jasmine of amount $ 550 is reimbursed by Rapid heat private limited.

However, the parking cost is not meant to be reimbursed by employer because car has not been

parked within radius of one kilometer and not within the premise of company. Furthermore, the

loan amount given to Jasmine is taken into account for the consideration of benefits.

It can therefore be concluded that the benefits received by Jasmine is accounted under "section 7

of the FBTAA 1986".

expense fringe benefit to reimburse the amount. Therefore, it is required to tax the amount that is

reimbursed by the employer.

The subsection B 39C of FBTAA 1986 takes into account the taxable value attributable

from car fringe benefits. The fringe benefit of car in relation to particular taxation year is held by

person receiving the benefits. Initiation of car fringe benefits arises in association with the

premises that are arranged within one kilometer or for lowering down the cost (Bhaduri et al.

2015). There are some additional circumstances when the fringe benefits can happen and they

are as follows:

During employment course, employer has taken the car

Car parking is done in a day for more than four hours.

Car is used by employer for travelling to office from home at least in a day.

Car parking within the company premises

Jasmine is provided with the car because of her job demand and she can use the car for

private reasons. Holding of such car for both private and official purpose is giving rise to fringe

benefits according to the subsection 136(1) of FBTAA 1986. Using of private car has resulted in

fringe benefits according to FBTAA 1986 in the case of “FCT v Lunney (1958). In addition to

this, expenses incurred by Jasmine of amount $ 550 is reimbursed by Rapid heat private limited.

However, the parking cost is not meant to be reimbursed by employer because car has not been

parked within radius of one kilometer and not within the premise of company. Furthermore, the

loan amount given to Jasmine is taken into account for the consideration of benefits.

It can therefore be concluded that the benefits received by Jasmine is accounted under "section 7

of the FBTAA 1986".

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION THEORY, PRACTICE AND LAW

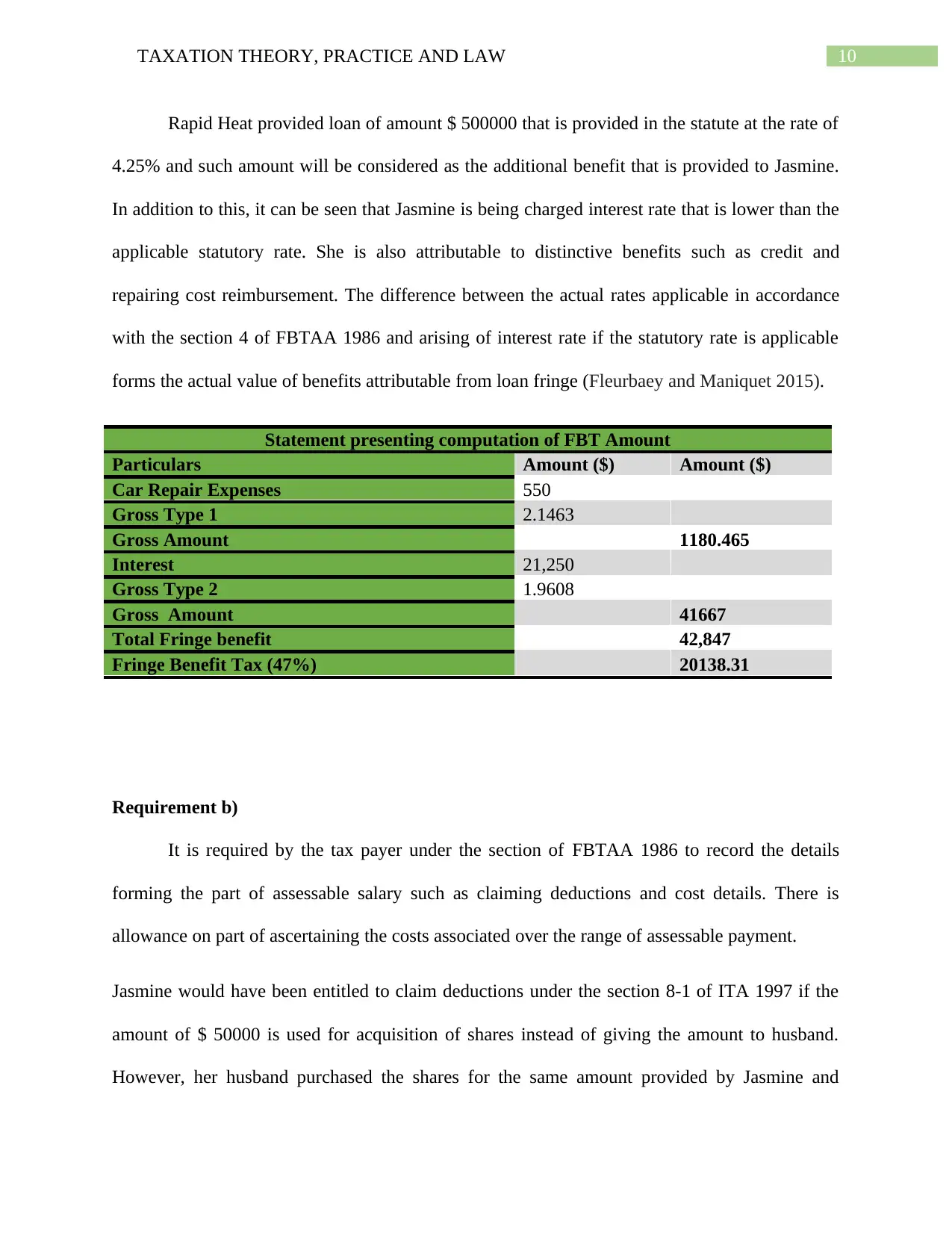

Rapid Heat provided loan of amount $ 500000 that is provided in the statute at the rate of

4.25% and such amount will be considered as the additional benefit that is provided to Jasmine.

In addition to this, it can be seen that Jasmine is being charged interest rate that is lower than the

applicable statutory rate. She is also attributable to distinctive benefits such as credit and

repairing cost reimbursement. The difference between the actual rates applicable in accordance

with the section 4 of FBTAA 1986 and arising of interest rate if the statutory rate is applicable

forms the actual value of benefits attributable from loan fringe (Fleurbaey and Maniquet 2015).

Statement presenting computation of FBT Amount

Particulars Amount ($) Amount ($)

Car Repair Expenses 550

Gross Type 1 2.1463

Gross Amount 1180.465

Interest 21,250

Gross Type 2 1.9608

Gross Amount 41667

Total Fringe benefit 42,847

Fringe Benefit Tax (47%) 20138.31

Requirement b)

It is required by the tax payer under the section of FBTAA 1986 to record the details

forming the part of assessable salary such as claiming deductions and cost details. There is

allowance on part of ascertaining the costs associated over the range of assessable payment.

Jasmine would have been entitled to claim deductions under the section 8-1 of ITA 1997 if the

amount of $ 50000 is used for acquisition of shares instead of giving the amount to husband.

However, her husband purchased the shares for the same amount provided by Jasmine and

Rapid Heat provided loan of amount $ 500000 that is provided in the statute at the rate of

4.25% and such amount will be considered as the additional benefit that is provided to Jasmine.

In addition to this, it can be seen that Jasmine is being charged interest rate that is lower than the

applicable statutory rate. She is also attributable to distinctive benefits such as credit and

repairing cost reimbursement. The difference between the actual rates applicable in accordance

with the section 4 of FBTAA 1986 and arising of interest rate if the statutory rate is applicable

forms the actual value of benefits attributable from loan fringe (Fleurbaey and Maniquet 2015).

Statement presenting computation of FBT Amount

Particulars Amount ($) Amount ($)

Car Repair Expenses 550

Gross Type 1 2.1463

Gross Amount 1180.465

Interest 21,250

Gross Type 2 1.9608

Gross Amount 41667

Total Fringe benefit 42,847

Fringe Benefit Tax (47%) 20138.31

Requirement b)

It is required by the tax payer under the section of FBTAA 1986 to record the details

forming the part of assessable salary such as claiming deductions and cost details. There is

allowance on part of ascertaining the costs associated over the range of assessable payment.

Jasmine would have been entitled to claim deductions under the section 8-1 of ITA 1997 if the

amount of $ 50000 is used for acquisition of shares instead of giving the amount to husband.

However, her husband purchased the shares for the same amount provided by Jasmine and

11TAXATION THEORY, PRACTICE AND LAW

therefore in relation to the amount of loan, jasmine is entitled to claim deductions according to

section 8-1 of ITAA 1997.

Reference and bibliography list:

Ato.gov.au. (2018). Types of CGT events. [online] Available at:

https://www.ato.gov.au/General/Capital-gains-tax/Selling-an-asset-and-other-CGT-events/

Types-of-CGT-events/#SharesG [Accessed 27 Sep. 2018].

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. American

Economic Review, 105(5), pp.38-42.

therefore in relation to the amount of loan, jasmine is entitled to claim deductions according to

section 8-1 of ITAA 1997.

Reference and bibliography list:

Ato.gov.au. (2018). Types of CGT events. [online] Available at:

https://www.ato.gov.au/General/Capital-gains-tax/Selling-an-asset-and-other-CGT-events/

Types-of-CGT-events/#SharesG [Accessed 27 Sep. 2018].

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. American

Economic Review, 105(5), pp.38-42.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.