Report: Taxation Fundamentals - Income, Benefits, and Tax Reducers

VerifiedAdded on 2023/01/19

|10

|2152

|97

Report

AI Summary

This report delves into the fundamentals of taxation, providing a comprehensive analysis of how taxable income is calculated, along with various tax reducers. Part 1 focuses on calculating Fiona's taxable income, considering her salary, benefits in kind (accommodation, car, and music system), pension contributions, and charitable donations. The report details the relevant tax legislation and rules applied in these calculations. Part 2 explores different types of tax reducers, including Married Couple's Allowance (MCA), Enterprise Investment Scheme (EIS) investments, Seed Enterprise Investment Scheme (SEIS) investments, Venture Capital Trusts (VCT) investments, maintenance payments, and loans used to purchase a life annuity. Each tax reducer is explained with its eligibility criteria and potential benefits. The report aims to provide a clear understanding of the UK tax system, encompassing both income assessment and strategies to minimize tax liability.

TAXATION

FUNDAMENTALS

FUNDAMENTALS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

PART 2............................................................................................................................................3

Tax Reducers..........................................................................................................................3

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

PART 2............................................................................................................................................3

Tax Reducers..........................................................................................................................3

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

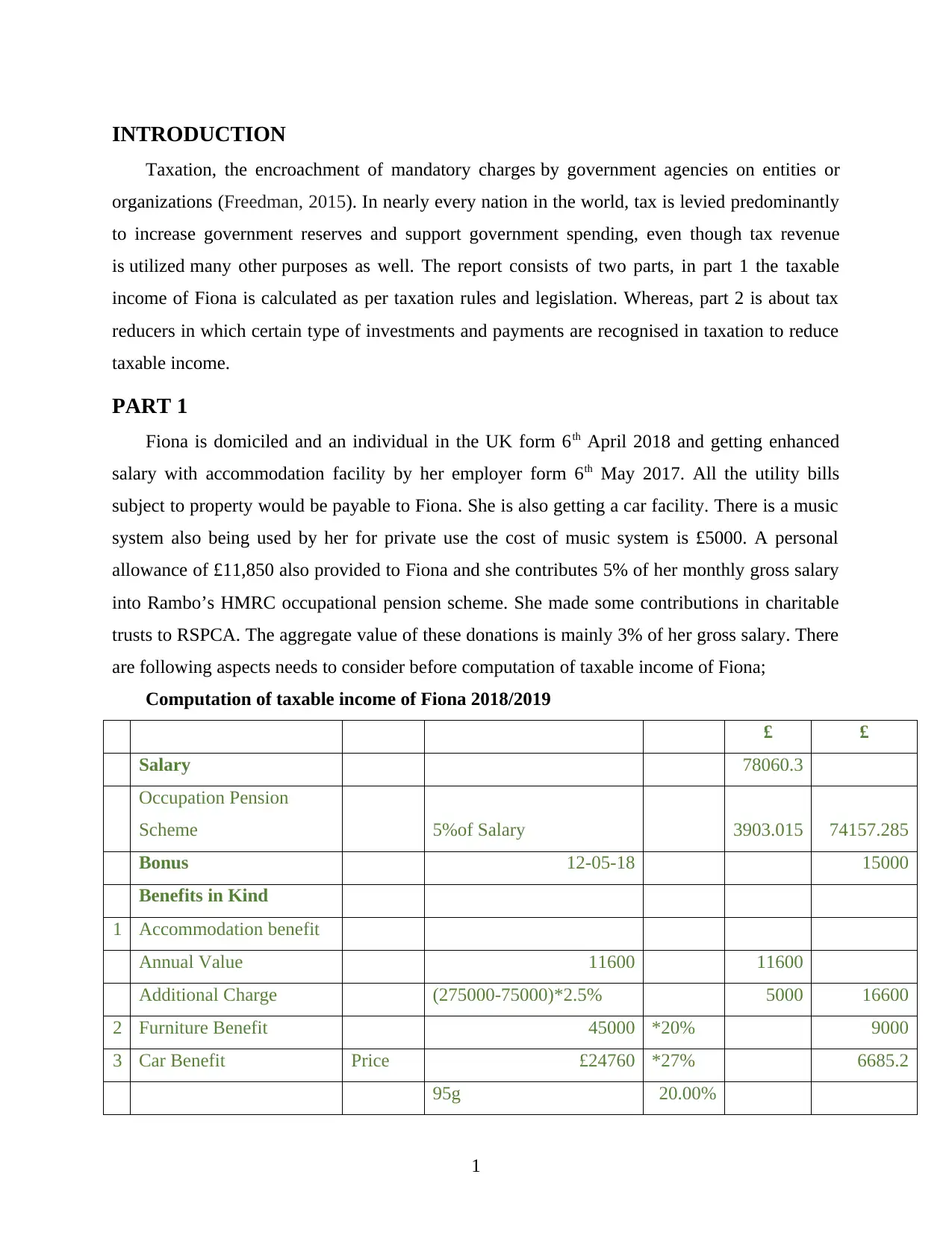

INTRODUCTION

Taxation, the encroachment of mandatory charges by government agencies on entities or

organizations (Freedman, 2015). In nearly every nation in the world, tax is levied predominantly

to increase government reserves and support government spending, even though tax revenue

is utilized many other purposes as well. The report consists of two parts, in part 1 the taxable

income of Fiona is calculated as per taxation rules and legislation. Whereas, part 2 is about tax

reducers in which certain type of investments and payments are recognised in taxation to reduce

taxable income.

PART 1

Fiona is domiciled and an individual in the UK form 6th April 2018 and getting enhanced

salary with accommodation facility by her employer form 6th May 2017. All the utility bills

subject to property would be payable to Fiona. She is also getting a car facility. There is a music

system also being used by her for private use the cost of music system is £5000. A personal

allowance of £11,850 also provided to Fiona and she contributes 5% of her monthly gross salary

into Rambo’s HMRC occupational pension scheme. She made some contributions in charitable

trusts to RSPCA. The aggregate value of these donations is mainly 3% of her gross salary. There

are following aspects needs to consider before computation of taxable income of Fiona;

Computation of taxable income of Fiona 2018/2019

£ £

Salary 78060.3

Occupation Pension

Scheme 5%of Salary 3903.015 74157.285

Bonus 12-05-18 15000

Benefits in Kind

1 Accommodation benefit

Annual Value 11600 11600

Additional Charge (275000-75000)*2.5% 5000 16600

2 Furniture Benefit 45000 *20% 9000

3 Car Benefit Price £24760 *27% 6685.2

95g 20.00%

1

Taxation, the encroachment of mandatory charges by government agencies on entities or

organizations (Freedman, 2015). In nearly every nation in the world, tax is levied predominantly

to increase government reserves and support government spending, even though tax revenue

is utilized many other purposes as well. The report consists of two parts, in part 1 the taxable

income of Fiona is calculated as per taxation rules and legislation. Whereas, part 2 is about tax

reducers in which certain type of investments and payments are recognised in taxation to reduce

taxable income.

PART 1

Fiona is domiciled and an individual in the UK form 6th April 2018 and getting enhanced

salary with accommodation facility by her employer form 6th May 2017. All the utility bills

subject to property would be payable to Fiona. She is also getting a car facility. There is a music

system also being used by her for private use the cost of music system is £5000. A personal

allowance of £11,850 also provided to Fiona and she contributes 5% of her monthly gross salary

into Rambo’s HMRC occupational pension scheme. She made some contributions in charitable

trusts to RSPCA. The aggregate value of these donations is mainly 3% of her gross salary. There

are following aspects needs to consider before computation of taxable income of Fiona;

Computation of taxable income of Fiona 2018/2019

£ £

Salary 78060.3

Occupation Pension

Scheme 5%of Salary 3903.015 74157.285

Bonus 12-05-18 15000

Benefits in Kind

1 Accommodation benefit

Annual Value 11600 11600

Additional Charge (275000-75000)*2.5% 5000 16600

2 Furniture Benefit 45000 *20% 9000

3 Car Benefit Price £24760 *27% 6685.2

95g 20.00%

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

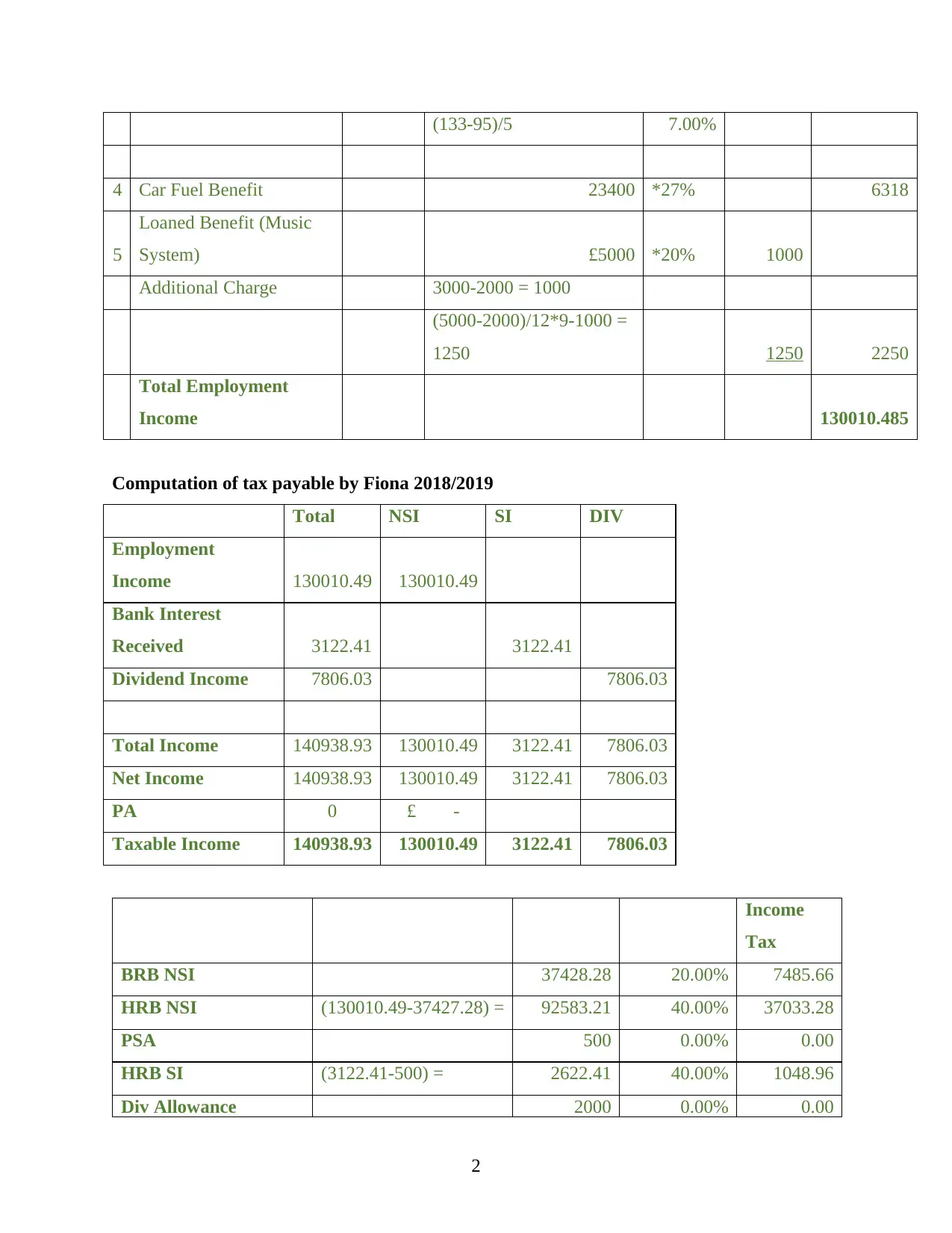

(133-95)/5 7.00%

4 Car Fuel Benefit 23400 *27% 6318

5

Loaned Benefit (Music

System) £5000 *20% 1000

Additional Charge 3000-2000 = 1000

(5000-2000)/12*9-1000 =

1250 1250 2250

Total Employment

Income 130010.485

Computation of tax payable by Fiona 2018/2019

Total NSI SI DIV

Employment

Income 130010.49 130010.49

Bank Interest

Received 3122.41 3122.41

Dividend Income 7806.03 7806.03

Total Income 140938.93 130010.49 3122.41 7806.03

Net Income 140938.93 130010.49 3122.41 7806.03

PA 0 £ -

Taxable Income 140938.93 130010.49 3122.41 7806.03

Income

Tax

BRB NSI 37428.28 20.00% 7485.66

HRB NSI (130010.49-37427.28) = 92583.21 40.00% 37033.28

PSA 500 0.00% 0.00

HRB SI (3122.41-500) = 2622.41 40.00% 1048.96

Div Allowance 2000 0.00% 0.00

2

4 Car Fuel Benefit 23400 *27% 6318

5

Loaned Benefit (Music

System) £5000 *20% 1000

Additional Charge 3000-2000 = 1000

(5000-2000)/12*9-1000 =

1250 1250 2250

Total Employment

Income 130010.485

Computation of tax payable by Fiona 2018/2019

Total NSI SI DIV

Employment

Income 130010.49 130010.49

Bank Interest

Received 3122.41 3122.41

Dividend Income 7806.03 7806.03

Total Income 140938.93 130010.49 3122.41 7806.03

Net Income 140938.93 130010.49 3122.41 7806.03

PA 0 £ -

Taxable Income 140938.93 130010.49 3122.41 7806.03

Income

Tax

BRB NSI 37428.28 20.00% 7485.66

HRB NSI (130010.49-37427.28) = 92583.21 40.00% 37033.28

PSA 500 0.00% 0.00

HRB SI (3122.41-500) = 2622.41 40.00% 1048.96

Div Allowance 2000 0.00% 0.00

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

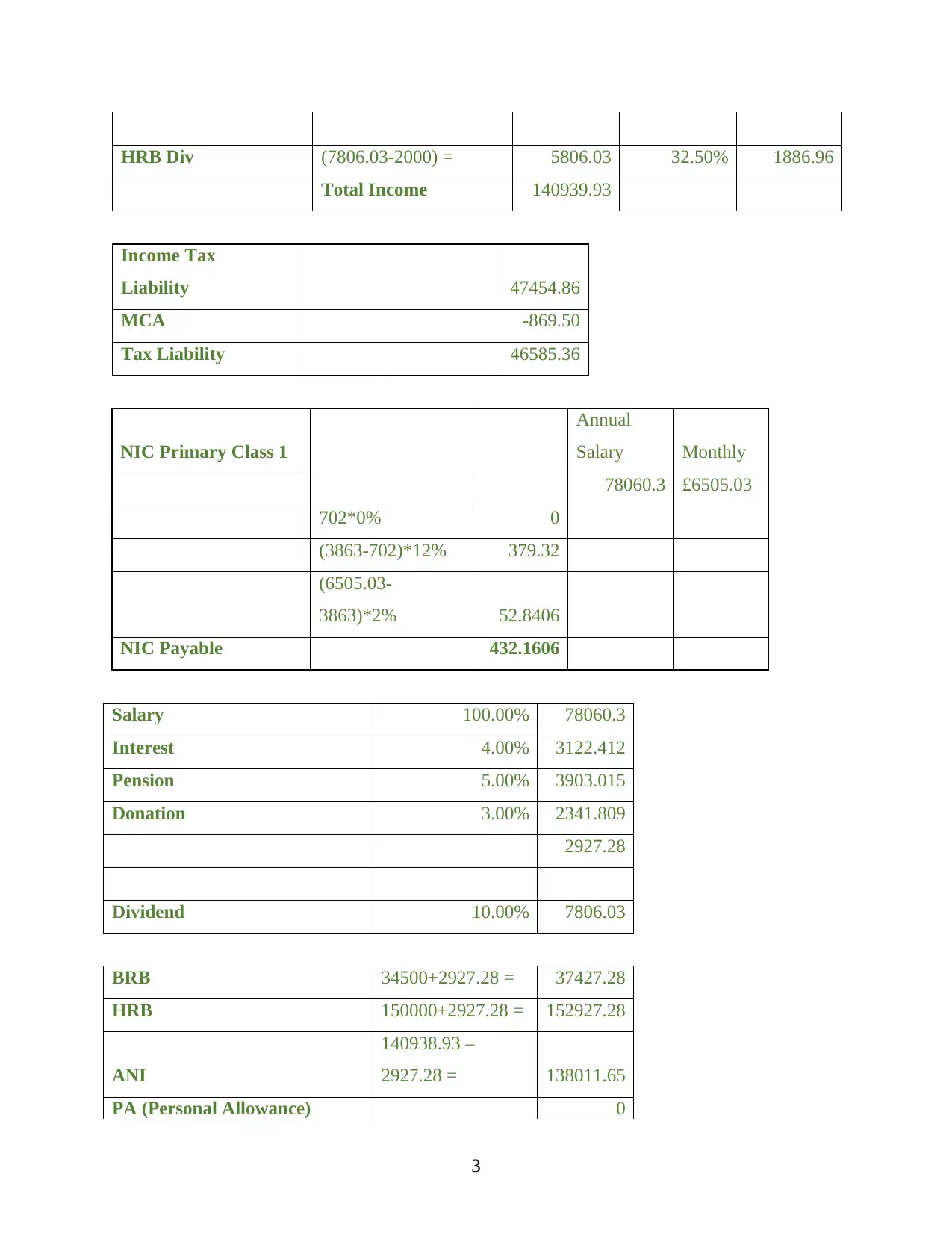

HRB Div (7806.03-2000) = 5806.03 32.50% 1886.96

Total Income 140939.93

Income Tax

Liability 47454.86

MCA -869.50

Tax Liability 46585.36

NIC Primary Class 1

Annual

Salary Monthly

78060.3 £6505.03

702*0% 0

(3863-702)*12% 379.32

(6505.03-

3863)*2% 52.8406

NIC Payable 432.1606

Salary 100.00% 78060.3

Interest 4.00% 3122.412

Pension 5.00% 3903.015

Donation 3.00% 2341.809

2927.28

Dividend 10.00% 7806.03

BRB 34500+2927.28 = 37427.28

HRB 150000+2927.28 = 152927.28

ANI

140938.93 –

2927.28 = 138011.65

PA (Personal Allowance) 0

3

Total Income 140939.93

Income Tax

Liability 47454.86

MCA -869.50

Tax Liability 46585.36

NIC Primary Class 1

Annual

Salary Monthly

78060.3 £6505.03

702*0% 0

(3863-702)*12% 379.32

(6505.03-

3863)*2% 52.8406

NIC Payable 432.1606

Salary 100.00% 78060.3

Interest 4.00% 3122.412

Pension 5.00% 3903.015

Donation 3.00% 2341.809

2927.28

Dividend 10.00% 7806.03

BRB 34500+2927.28 = 37427.28

HRB 150000+2927.28 = 152927.28

ANI

140938.93 –

2927.28 = 138011.65

PA (Personal Allowance) 0

3

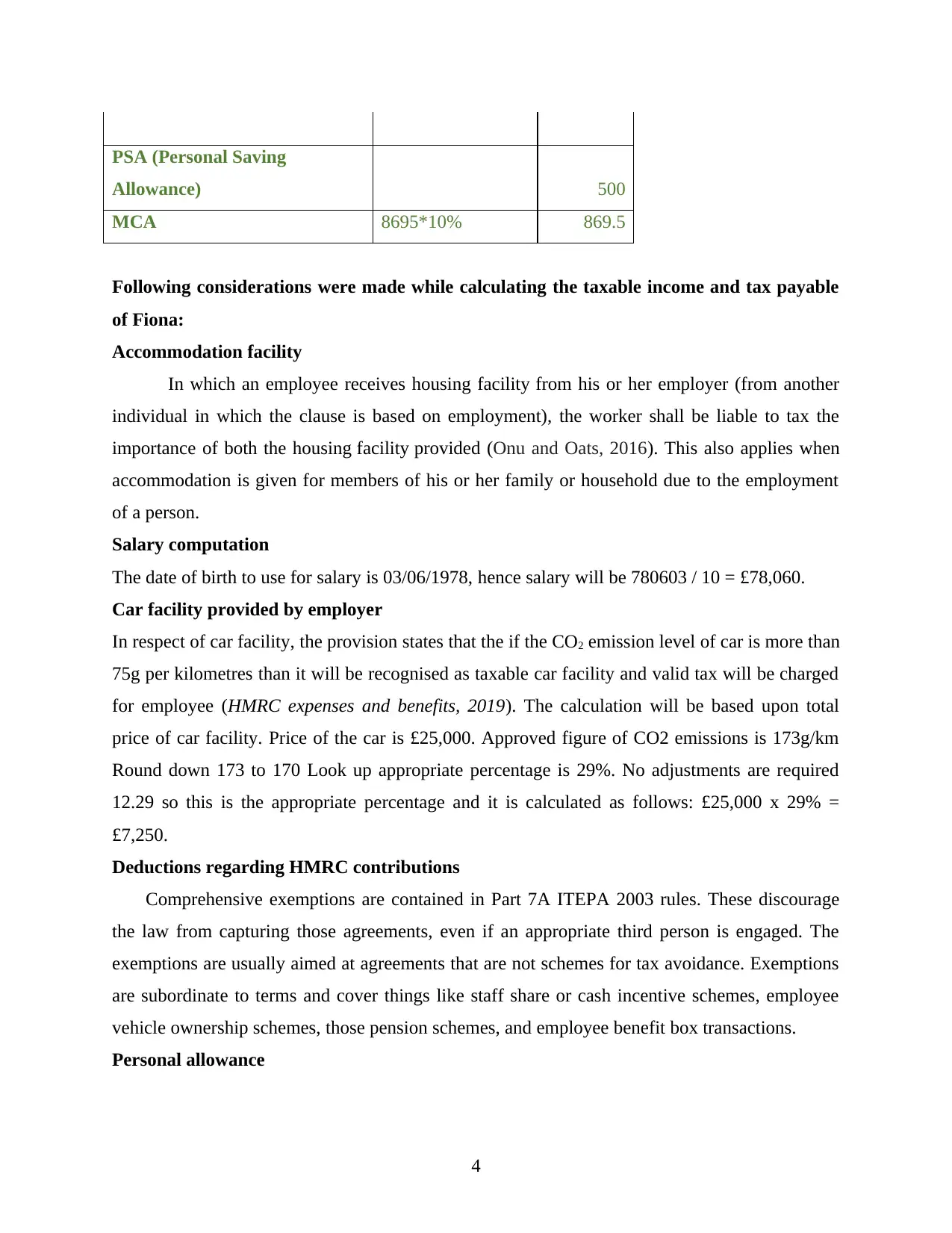

PSA (Personal Saving

Allowance) 500

MCA 8695*10% 869.5

Following considerations were made while calculating the taxable income and tax payable

of Fiona:

Accommodation facility

In which an employee receives housing facility from his or her employer (from another

individual in which the clause is based on employment), the worker shall be liable to tax the

importance of both the housing facility provided (Onu and Oats, 2016). This also applies when

accommodation is given for members of his or her family or household due to the employment

of a person.

Salary computation

The date of birth to use for salary is 03/06/1978, hence salary will be 780603 / 10 = £78,060.

Car facility provided by employer

In respect of car facility, the provision states that the if the CO2 emission level of car is more than

75g per kilometres than it will be recognised as taxable car facility and valid tax will be charged

for employee (HMRC expenses and benefits, 2019). The calculation will be based upon total

price of car facility. Price of the car is £25,000. Approved figure of CO2 emissions is 173g/km

Round down 173 to 170 Look up appropriate percentage is 29%. No adjustments are required

12.29 so this is the appropriate percentage and it is calculated as follows: £25,000 x 29% =

£7,250.

Deductions regarding HMRC contributions

Comprehensive exemptions are contained in Part 7A ITEPA 2003 rules. These discourage

the law from capturing those agreements, even if an appropriate third person is engaged. The

exemptions are usually aimed at agreements that are not schemes for tax avoidance. Exemptions

are subordinate to terms and cover things like staff share or cash incentive schemes, employee

vehicle ownership schemes, those pension schemes, and employee benefit box transactions.

Personal allowance

4

Allowance) 500

MCA 8695*10% 869.5

Following considerations were made while calculating the taxable income and tax payable

of Fiona:

Accommodation facility

In which an employee receives housing facility from his or her employer (from another

individual in which the clause is based on employment), the worker shall be liable to tax the

importance of both the housing facility provided (Onu and Oats, 2016). This also applies when

accommodation is given for members of his or her family or household due to the employment

of a person.

Salary computation

The date of birth to use for salary is 03/06/1978, hence salary will be 780603 / 10 = £78,060.

Car facility provided by employer

In respect of car facility, the provision states that the if the CO2 emission level of car is more than

75g per kilometres than it will be recognised as taxable car facility and valid tax will be charged

for employee (HMRC expenses and benefits, 2019). The calculation will be based upon total

price of car facility. Price of the car is £25,000. Approved figure of CO2 emissions is 173g/km

Round down 173 to 170 Look up appropriate percentage is 29%. No adjustments are required

12.29 so this is the appropriate percentage and it is calculated as follows: £25,000 x 29% =

£7,250.

Deductions regarding HMRC contributions

Comprehensive exemptions are contained in Part 7A ITEPA 2003 rules. These discourage

the law from capturing those agreements, even if an appropriate third person is engaged. The

exemptions are usually aimed at agreements that are not schemes for tax avoidance. Exemptions

are subordinate to terms and cover things like staff share or cash incentive schemes, employee

vehicle ownership schemes, those pension schemes, and employee benefit box transactions.

Personal allowance

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

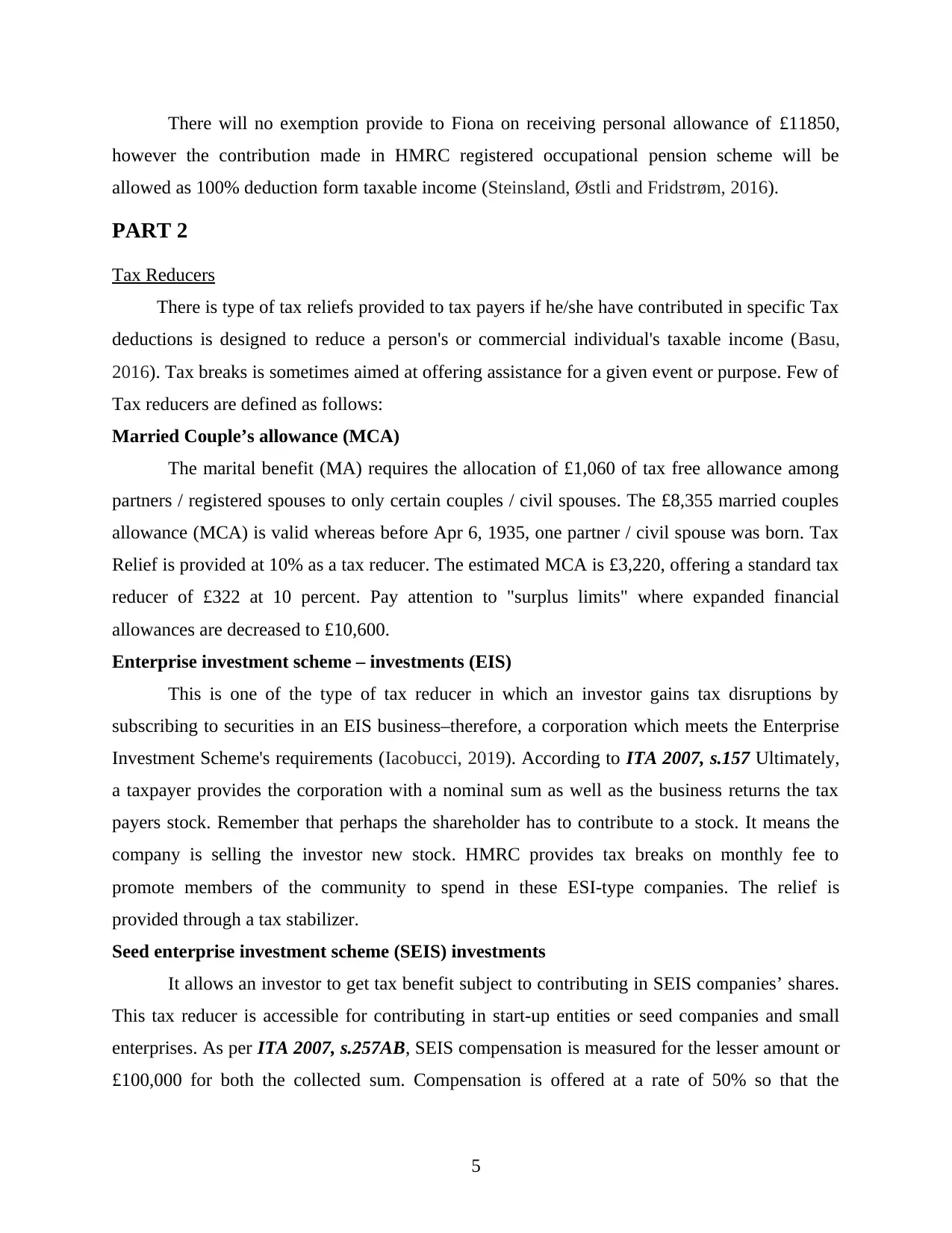

There will no exemption provide to Fiona on receiving personal allowance of £11850,

however the contribution made in HMRC registered occupational pension scheme will be

allowed as 100% deduction form taxable income (Steinsland, Østli and Fridstrøm, 2016).

PART 2

Tax Reducers

There is type of tax reliefs provided to tax payers if he/she have contributed in specific Tax

deductions is designed to reduce a person's or commercial individual's taxable income (Basu,

2016). Tax breaks is sometimes aimed at offering assistance for a given event or purpose. Few of

Tax reducers are defined as follows:

Married Couple’s allowance (MCA)

The marital benefit (MA) requires the allocation of £1,060 of tax free allowance among

partners / registered spouses to only certain couples / civil spouses. The £8,355 married couples

allowance (MCA) is valid whereas before Apr 6, 1935, one partner / civil spouse was born. Tax

Relief is provided at 10% as a tax reducer. The estimated MCA is £3,220, offering a standard tax

reducer of £322 at 10 percent. Pay attention to "surplus limits" where expanded financial

allowances are decreased to £10,600.

Enterprise investment scheme – investments (EIS)

This is one of the type of tax reducer in which an investor gains tax disruptions by

subscribing to securities in an EIS business–therefore, a corporation which meets the Enterprise

Investment Scheme's requirements (Iacobucci, 2019). According to ITA 2007, s.157 Ultimately,

a taxpayer provides the corporation with a nominal sum as well as the business returns the tax

payers stock. Remember that perhaps the shareholder has to contribute to a stock. It means the

company is selling the investor new stock. HMRC provides tax breaks on monthly fee to

promote members of the community to spend in these ESI-type companies. The relief is

provided through a tax stabilizer.

Seed enterprise investment scheme (SEIS) investments

It allows an investor to get tax benefit subject to contributing in SEIS companies’ shares.

This tax reducer is accessible for contributing in start-up entities or seed companies and small

enterprises. As per ITA 2007, s.257AB, SEIS compensation is measured for the lesser amount or

£100,000 for both the collected sum. Compensation is offered at a rate of 50% so that the

5

however the contribution made in HMRC registered occupational pension scheme will be

allowed as 100% deduction form taxable income (Steinsland, Østli and Fridstrøm, 2016).

PART 2

Tax Reducers

There is type of tax reliefs provided to tax payers if he/she have contributed in specific Tax

deductions is designed to reduce a person's or commercial individual's taxable income (Basu,

2016). Tax breaks is sometimes aimed at offering assistance for a given event or purpose. Few of

Tax reducers are defined as follows:

Married Couple’s allowance (MCA)

The marital benefit (MA) requires the allocation of £1,060 of tax free allowance among

partners / registered spouses to only certain couples / civil spouses. The £8,355 married couples

allowance (MCA) is valid whereas before Apr 6, 1935, one partner / civil spouse was born. Tax

Relief is provided at 10% as a tax reducer. The estimated MCA is £3,220, offering a standard tax

reducer of £322 at 10 percent. Pay attention to "surplus limits" where expanded financial

allowances are decreased to £10,600.

Enterprise investment scheme – investments (EIS)

This is one of the type of tax reducer in which an investor gains tax disruptions by

subscribing to securities in an EIS business–therefore, a corporation which meets the Enterprise

Investment Scheme's requirements (Iacobucci, 2019). According to ITA 2007, s.157 Ultimately,

a taxpayer provides the corporation with a nominal sum as well as the business returns the tax

payers stock. Remember that perhaps the shareholder has to contribute to a stock. It means the

company is selling the investor new stock. HMRC provides tax breaks on monthly fee to

promote members of the community to spend in these ESI-type companies. The relief is

provided through a tax stabilizer.

Seed enterprise investment scheme (SEIS) investments

It allows an investor to get tax benefit subject to contributing in SEIS companies’ shares.

This tax reducer is accessible for contributing in start-up entities or seed companies and small

enterprises. As per ITA 2007, s.257AB, SEIS compensation is measured for the lesser amount or

£100,000 for both the collected sum. Compensation is offered at a rate of 50% so that the

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

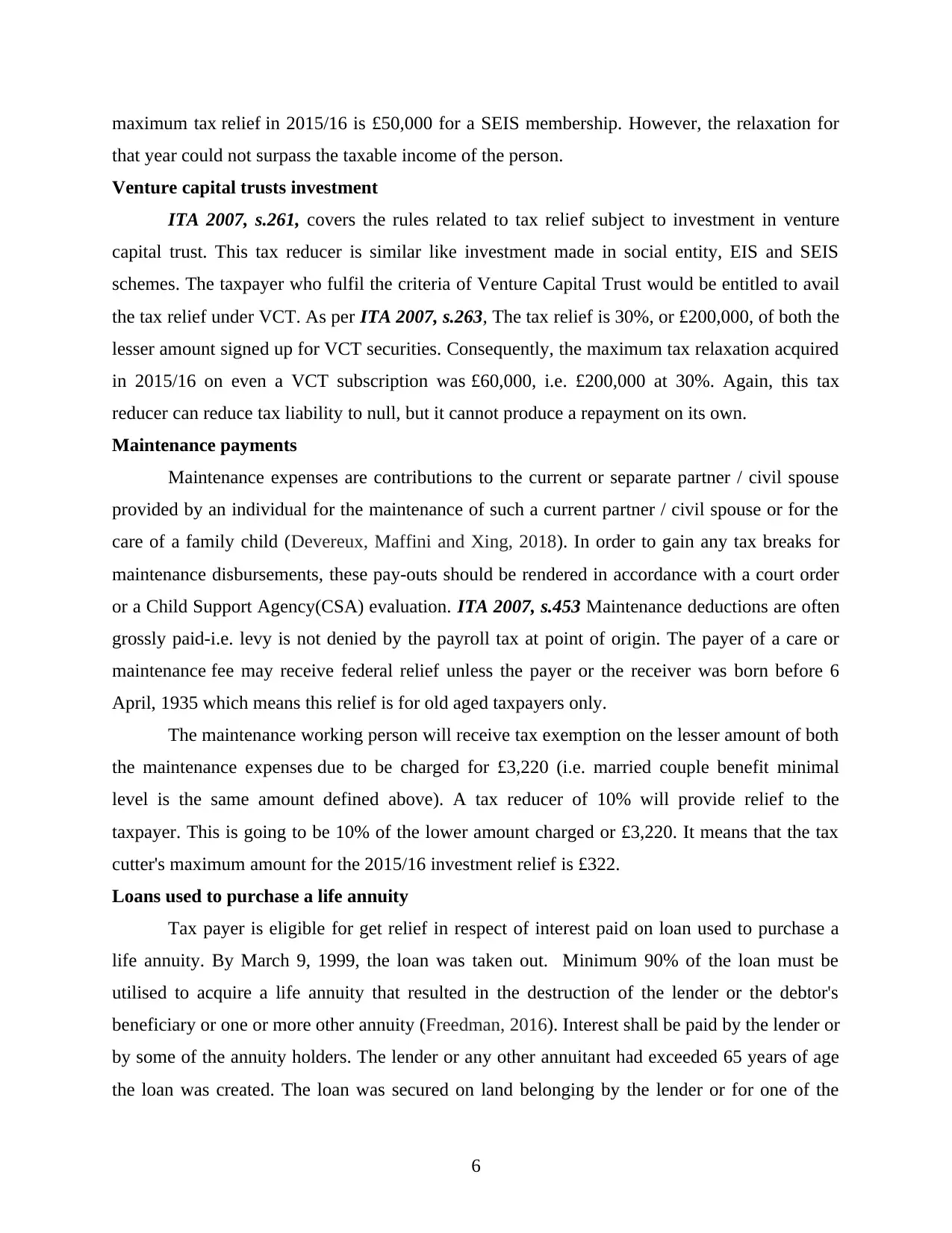

maximum tax relief in 2015/16 is £50,000 for a SEIS membership. However, the relaxation for

that year could not surpass the taxable income of the person.

Venture capital trusts investment

ITA 2007, s.261, covers the rules related to tax relief subject to investment in venture

capital trust. This tax reducer is similar like investment made in social entity, EIS and SEIS

schemes. The taxpayer who fulfil the criteria of Venture Capital Trust would be entitled to avail

the tax relief under VCT. As per ITA 2007, s.263, The tax relief is 30%, or £200,000, of both the

lesser amount signed up for VCT securities. Consequently, the maximum tax relaxation acquired

in 2015/16 on even a VCT subscription was £60,000, i.e. £200,000 at 30%. Again, this tax

reducer can reduce tax liability to null, but it cannot produce a repayment on its own.

Maintenance payments

Maintenance expenses are contributions to the current or separate partner / civil spouse

provided by an individual for the maintenance of such a current partner / civil spouse or for the

care of a family child (Devereux, Maffini and Xing, 2018). In order to gain any tax breaks for

maintenance disbursements, these pay-outs should be rendered in accordance with a court order

or a Child Support Agency(CSA) evaluation. ITA 2007, s.453 Maintenance deductions are often

grossly paid-i.e. levy is not denied by the payroll tax at point of origin. The payer of a care or

maintenance fee may receive federal relief unless the payer or the receiver was born before 6

April, 1935 which means this relief is for old aged taxpayers only.

The maintenance working person will receive tax exemption on the lesser amount of both

the maintenance expenses due to be charged for £3,220 (i.e. married couple benefit minimal

level is the same amount defined above). A tax reducer of 10% will provide relief to the

taxpayer. This is going to be 10% of the lower amount charged or £3,220. It means that the tax

cutter's maximum amount for the 2015/16 investment relief is £322.

Loans used to purchase a life annuity

Tax payer is eligible for get relief in respect of interest paid on loan used to purchase a

life annuity. By March 9, 1999, the loan was taken out. Minimum 90% of the loan must be

utilised to acquire a life annuity that resulted in the destruction of the lender or the debtor's

beneficiary or one or more other annuity (Freedman, 2016). Interest shall be paid by the lender or

by some of the annuity holders. The lender or any other annuitant had exceeded 65 years of age

the loan was created. The loan was secured on land belonging by the lender or for one of the

6

that year could not surpass the taxable income of the person.

Venture capital trusts investment

ITA 2007, s.261, covers the rules related to tax relief subject to investment in venture

capital trust. This tax reducer is similar like investment made in social entity, EIS and SEIS

schemes. The taxpayer who fulfil the criteria of Venture Capital Trust would be entitled to avail

the tax relief under VCT. As per ITA 2007, s.263, The tax relief is 30%, or £200,000, of both the

lesser amount signed up for VCT securities. Consequently, the maximum tax relaxation acquired

in 2015/16 on even a VCT subscription was £60,000, i.e. £200,000 at 30%. Again, this tax

reducer can reduce tax liability to null, but it cannot produce a repayment on its own.

Maintenance payments

Maintenance expenses are contributions to the current or separate partner / civil spouse

provided by an individual for the maintenance of such a current partner / civil spouse or for the

care of a family child (Devereux, Maffini and Xing, 2018). In order to gain any tax breaks for

maintenance disbursements, these pay-outs should be rendered in accordance with a court order

or a Child Support Agency(CSA) evaluation. ITA 2007, s.453 Maintenance deductions are often

grossly paid-i.e. levy is not denied by the payroll tax at point of origin. The payer of a care or

maintenance fee may receive federal relief unless the payer or the receiver was born before 6

April, 1935 which means this relief is for old aged taxpayers only.

The maintenance working person will receive tax exemption on the lesser amount of both

the maintenance expenses due to be charged for £3,220 (i.e. married couple benefit minimal

level is the same amount defined above). A tax reducer of 10% will provide relief to the

taxpayer. This is going to be 10% of the lower amount charged or £3,220. It means that the tax

cutter's maximum amount for the 2015/16 investment relief is £322.

Loans used to purchase a life annuity

Tax payer is eligible for get relief in respect of interest paid on loan used to purchase a

life annuity. By March 9, 1999, the loan was taken out. Minimum 90% of the loan must be

utilised to acquire a life annuity that resulted in the destruction of the lender or the debtor's

beneficiary or one or more other annuity (Freedman, 2016). Interest shall be paid by the lender or

by some of the annuity holders. The lender or any other annuitant had exceeded 65 years of age

the loan was created. The loan was secured on land belonging by the lender or for one of the

6

annuity holder. throughout the United Kingdom or even the Republic of Ireland and used as the

sole or principal property of annuitants immediately preceding 9 March 1999. The taxable relief

is entitled up to £30,000 of the loan.

CONCLUSION

The above report extract the concept of taxation fundamentals subject to assess the taxability

of taxpayer. First part conclude the exemptions and benefits provided to employee form the

employer and second part clearly extract the information related to tax reducers. The concept of

tax reducers in terms of reducing taxable income defined in effective manner.

7

sole or principal property of annuitants immediately preceding 9 March 1999. The taxable relief

is entitled up to £30,000 of the loan.

CONCLUSION

The above report extract the concept of taxation fundamentals subject to assess the taxability

of taxpayer. First part conclude the exemptions and benefits provided to employee form the

employer and second part clearly extract the information related to tax reducers. The concept of

tax reducers in terms of reducing taxable income defined in effective manner.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals:

Freedman, J., 2015. Managing tax complexity: the institutional framework for tax policy-making

and oversight.

Onu, D. and Oats, L., 2016. “Paying tax is part of life”: Social norms and social influence in tax

communications. Journal of Economic Behavior & Organization. 124. pp.29-42.

Steinsland, C., Østli, V. and Fridstrøm, L., 2016. Equity effects of automobile taxation. TØI

Report. 1463.

Basu, S., 2016. Global perspectives on e-commerce taxation law. Routledge.

Iacobucci, G., 2019. Workforce crisis:“punitive” cuts to pension tax relief must be reversed, say

consultants. BMJ: British Medical Journal (Online). 364.

Freedman, J., 2016. General Anti-Avoidance Rules (GAARs)–A Key Element of Tax Systems in

the Post-BEPS Tax World? The UK GAAR.

Devereux, M. P., Maffini, G. and Xing, J., 2018. Corporate tax incentives and capital structure:

New evidence from UK firm-level tax returns. Journal of Banking & Finance. 88.

pp.250-266.

Online

HMRC expenses and benefits, 2019. [online]. Available through:

<https://assets.publishing.service.gov.uk/government/uploads/system/uploads/

attachment_data/file/734647/480_2018_.pdf>

8

Books and Journals:

Freedman, J., 2015. Managing tax complexity: the institutional framework for tax policy-making

and oversight.

Onu, D. and Oats, L., 2016. “Paying tax is part of life”: Social norms and social influence in tax

communications. Journal of Economic Behavior & Organization. 124. pp.29-42.

Steinsland, C., Østli, V. and Fridstrøm, L., 2016. Equity effects of automobile taxation. TØI

Report. 1463.

Basu, S., 2016. Global perspectives on e-commerce taxation law. Routledge.

Iacobucci, G., 2019. Workforce crisis:“punitive” cuts to pension tax relief must be reversed, say

consultants. BMJ: British Medical Journal (Online). 364.

Freedman, J., 2016. General Anti-Avoidance Rules (GAARs)–A Key Element of Tax Systems in

the Post-BEPS Tax World? The UK GAAR.

Devereux, M. P., Maffini, G. and Xing, J., 2018. Corporate tax incentives and capital structure:

New evidence from UK firm-level tax returns. Journal of Banking & Finance. 88.

pp.250-266.

Online

HMRC expenses and benefits, 2019. [online]. Available through:

<https://assets.publishing.service.gov.uk/government/uploads/system/uploads/

attachment_data/file/734647/480_2018_.pdf>

8

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.