Taxation Law Assignment: Finance, Capital Gains, and GST Analysis

VerifiedAdded on 2023/01/05

|13

|3025

|42

Homework Assignment

AI Summary

This taxation law assignment addresses two key questions. The first question analyzes the case of City Sky Co, focusing on the issue of input tax credit claims related to a land purchase for apartment construction, referencing relevant GST rulings and legislation like the "GSTR 2008/1" and various sections of the "GST Act 1999". The analysis determines whether the acquisition qualifies as a creditable acquisition, considering the company's GST registration and the intended use of the land. The second question examines the capital gains tax (CGT) implications of various transactions by Emma, including the sale of a block of land, shares in Rio Tinto, and a collection of stamps. It applies relevant sections of the "ITAA 1997", such as "sec 6-10", "sec 102-5 (1)", "sec 104-10", and "sec 110-25", to calculate capital gains, considering cost bases, incidental costs, capital enhancements, and the impact of pre-CGT assets and collectibles. The assignment demonstrates the application of taxation principles to real-world financial scenarios.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................4

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................4

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Issue:

The main issue that is related to the case of City Sky Co is regarding the claim for

input tax credit originating from the creditable transaction under “sec 11-5, GSTR 1999”.

Rule:

The goods and service tax ruling of “GSTR 2008/1” provides the guidelines regarding

the input tax credit originating from the creditable transaction. The ruling is largely related to

the GST that is payable or the input tax credits under the “GST Act of 1999” (Kraal and

Kasipillai 2016). The ruling also provides the explanation when the taxpayer should maintain

their books of accounts for the GST payable or the input tax credit regarding the sale of land

under the standard agreement of land.

According to this ruling, to claim the input tax credit the taxpayer should make the

creditable acquisition or the importation. As stated under this ruling, to make the creditable

acquisition or the import the taxpayers should make the acquisition or import completely or

partially for the creditable purpose only (Ramli et al., 2015). The general claims relating to

the tax credit originates from making the creditable acquisition and creditable import. A

supplier who makes the chargeable supplies will be accountable for the GST on the supplies.

Furthermore, the supplier is also permitted to get the input tax credit for acquisition it makes

that is associated to those supplies.

Under the “sec 11-20, GST Act 1999”, a company which is registered for the GST

purpose will be permitted to obtain the input tax credit for the creditable acquisition the

business during their business course (Tran-Nam, 2019). According to the “section 11-5,

GST Act 1999” a creditable acquisition generally happens if the business makes the

Answer to question 1:

Issue:

The main issue that is related to the case of City Sky Co is regarding the claim for

input tax credit originating from the creditable transaction under “sec 11-5, GSTR 1999”.

Rule:

The goods and service tax ruling of “GSTR 2008/1” provides the guidelines regarding

the input tax credit originating from the creditable transaction. The ruling is largely related to

the GST that is payable or the input tax credits under the “GST Act of 1999” (Kraal and

Kasipillai 2016). The ruling also provides the explanation when the taxpayer should maintain

their books of accounts for the GST payable or the input tax credit regarding the sale of land

under the standard agreement of land.

According to this ruling, to claim the input tax credit the taxpayer should make the

creditable acquisition or the importation. As stated under this ruling, to make the creditable

acquisition or the import the taxpayers should make the acquisition or import completely or

partially for the creditable purpose only (Ramli et al., 2015). The general claims relating to

the tax credit originates from making the creditable acquisition and creditable import. A

supplier who makes the chargeable supplies will be accountable for the GST on the supplies.

Furthermore, the supplier is also permitted to get the input tax credit for acquisition it makes

that is associated to those supplies.

Under the “sec 11-20, GST Act 1999”, a company which is registered for the GST

purpose will be permitted to obtain the input tax credit for the creditable acquisition the

business during their business course (Tran-Nam, 2019). According to the “section 11-5,

GST Act 1999” a creditable acquisition generally happens if the business makes the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

acquisition completely or partly for the creditable purpose and other related requirements of

the “section 11-5, GST Act 1999” are satisfied. As per the “section 11-15, GST Act 1999” a

business that purchases or acquires a thing for the creditable purpose up to the level that the

company acquires the item in conducting its business activities.

There are also rules regarding the reverse charge mechanism where the purchaser is

required to pay the GST. The reverse charge rules are applicable when the purchaser buys a

thing that is completely for the business purpose. The circumstances where the reverse charge

mechanism is applicable denotes that the supply is connected with Australia and the purchase

done or performed is within Australia.

Application:

The case facts obtained suggest that City Sky Co is property development and

investment company that has purchased a vacant land in Brisbane. The company bought the

land for the purpose of building 15 apartments for sale. With regard to the “section 11-5,

GST Act 1999” the acquisition of land by City Sky Co cannot be regarded as the creditable

acquisition since it is a capital asset and it amounts to an immovable property because the

land was acquired completely for constructing apartment (Verikios, Patron and Gharibnavaz

2017). Furthermore, the company is also registered for the GST purpose.

As noted under “sec 11-15, GST Act 1999”, Sky City Co acquired the land for

creditable purpose up to the level that it is carrying on its enterprise for making taxable

supplies in future (Ranjan, 2018). As eminent, Sky City Co prepares to make the taxable

supply by building 15 apartments on the land and the same will not be considered liable for

GST. Sky City Co would not be permitted to obtain the input tax credit relating to the

acquisition associated to the supplies.

acquisition completely or partly for the creditable purpose and other related requirements of

the “section 11-5, GST Act 1999” are satisfied. As per the “section 11-15, GST Act 1999” a

business that purchases or acquires a thing for the creditable purpose up to the level that the

company acquires the item in conducting its business activities.

There are also rules regarding the reverse charge mechanism where the purchaser is

required to pay the GST. The reverse charge rules are applicable when the purchaser buys a

thing that is completely for the business purpose. The circumstances where the reverse charge

mechanism is applicable denotes that the supply is connected with Australia and the purchase

done or performed is within Australia.

Application:

The case facts obtained suggest that City Sky Co is property development and

investment company that has purchased a vacant land in Brisbane. The company bought the

land for the purpose of building 15 apartments for sale. With regard to the “section 11-5,

GST Act 1999” the acquisition of land by City Sky Co cannot be regarded as the creditable

acquisition since it is a capital asset and it amounts to an immovable property because the

land was acquired completely for constructing apartment (Verikios, Patron and Gharibnavaz

2017). Furthermore, the company is also registered for the GST purpose.

As noted under “sec 11-15, GST Act 1999”, Sky City Co acquired the land for

creditable purpose up to the level that it is carrying on its enterprise for making taxable

supplies in future (Ranjan, 2018). As eminent, Sky City Co prepares to make the taxable

supply by building 15 apartments on the land and the same will not be considered liable for

GST. Sky City Co would not be permitted to obtain the input tax credit relating to the

acquisition associated to the supplies.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

The case study evidently provides the company Sky City Co is registered for the GST

purpose. The company cannot obtain the GST credit nor will it be allowed to obtain the input

tax credit for the creditable purpose regarding the acquisition of land that is made by the

company. The company here Sky City Co has made the creditable purchase of land since the

company has bought the land in conducting its business activities (Schenk, Thuronyi and Cui

2016).

Additionally, the company will only be permitted to claim input tax credit for the

legal services sought from the Maurice Blackburn since it is a taxable supply “sec 11-15,

GST Act 1999”. The legal services sought is falling inside the mechanism of reverse charge

and as a result City Sky Co being the service receiver will be liable for paying GST. The

company will be held eligible for claiming the input tax credit regarding the GST that is paid

to avail the services from the advocate.

Conclusion:

The above stated analysis can have concluded by stating that the company here Sky

City Co will be permitted to obtain the input tax credit under the “sec 11-15, GST Act 1999”

for the legal services sought from Maurice Blackburn. This is because the creditable

acquisition that is made by the company is entirely or completely for the use in business.

Answer to question 2:

Sale of a block of land for $1,000,000:

The provision of capital gains is applied on all the actual or realised gains. Under the

“sec 6-10, ITAA 1997” the capital gains are considered taxable as statutory income and it is

included into the assessable earnings of the taxpayer. Accordingly, “sec 102-5 (1)” is

regarded as the main operational provision of the CGT regime it comprises of the net capital

gains in the chargeable earnings (Hickman 2018). Capital gains are usually held taxable on

The case study evidently provides the company Sky City Co is registered for the GST

purpose. The company cannot obtain the GST credit nor will it be allowed to obtain the input

tax credit for the creditable purpose regarding the acquisition of land that is made by the

company. The company here Sky City Co has made the creditable purchase of land since the

company has bought the land in conducting its business activities (Schenk, Thuronyi and Cui

2016).

Additionally, the company will only be permitted to claim input tax credit for the

legal services sought from the Maurice Blackburn since it is a taxable supply “sec 11-15,

GST Act 1999”. The legal services sought is falling inside the mechanism of reverse charge

and as a result City Sky Co being the service receiver will be liable for paying GST. The

company will be held eligible for claiming the input tax credit regarding the GST that is paid

to avail the services from the advocate.

Conclusion:

The above stated analysis can have concluded by stating that the company here Sky

City Co will be permitted to obtain the input tax credit under the “sec 11-15, GST Act 1999”

for the legal services sought from Maurice Blackburn. This is because the creditable

acquisition that is made by the company is entirely or completely for the use in business.

Answer to question 2:

Sale of a block of land for $1,000,000:

The provision of capital gains is applied on all the actual or realised gains. Under the

“sec 6-10, ITAA 1997” the capital gains are considered taxable as statutory income and it is

included into the assessable earnings of the taxpayer. Accordingly, “sec 102-5 (1)” is

regarded as the main operational provision of the CGT regime it comprises of the net capital

gains in the chargeable earnings (Hickman 2018). Capital gains are usually held taxable on

5TAXATION LAW

the basis of the individual marginal rate however discount implies that only 50% of the

capital gains are taxed.

Whereas, “sec 104-10, ITAA 1997” is associated with the CGT event A1 that mainly

deals with the sale of the CGT asset (Krever and Sadiq 2019). This is applied on the CGT

asset that is bought following 19/9/85. As defined in the “sec 110-25, ITAA 1997” the cost

base of the CGT asset is generally made up of five elements. This comprises of the following;

Element 1: Money that is paid and the market value of the property that is needed to be paid

for purchasing the asset.

Element 2: This includes the incidental cost that has occurred for the acquisition of the asset.

Element 3: The cost involved in the ownership of the asset such as the loan interest, repairs

and insurance.

Element 4: The capital expenses occurred in increasing the value of the asset or which is

associated to the installation of the asset.

Element 5: The capital expenses that is occurred while maintaining the assets title and rights.

The taxpayer should denote that they are not permitted to obtain deduction for the

costs that are occurred in acquiring or selling the property. These costs are added into the cost

base of the property for the purpose of CGT.

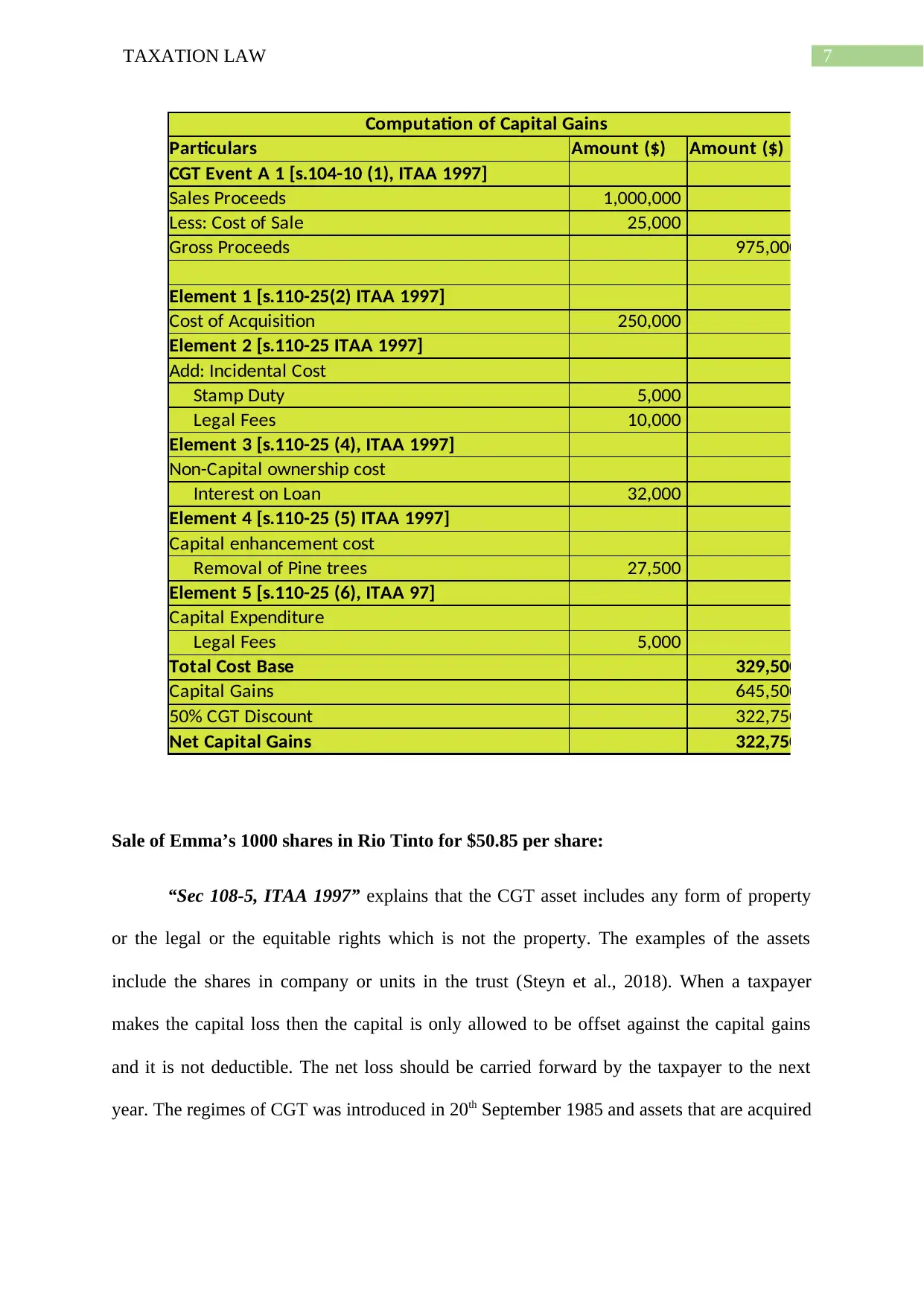

Emma here sells the block of land for $1,000,000. The sale of land has resulted in the

CGT event A1 under “sec 104-10, ITAA 1997” (Bentley 2019). The acquisition price that

was paid for acquiring the land by Emma was $250,000. The cost that is occurred in

acquisition should be viewed as the cost paid to acquire the property based on the available

market value. The sum of $250,000 will be included in the first element of the cost base of

the land for CGT purpose.

the basis of the individual marginal rate however discount implies that only 50% of the

capital gains are taxed.

Whereas, “sec 104-10, ITAA 1997” is associated with the CGT event A1 that mainly

deals with the sale of the CGT asset (Krever and Sadiq 2019). This is applied on the CGT

asset that is bought following 19/9/85. As defined in the “sec 110-25, ITAA 1997” the cost

base of the CGT asset is generally made up of five elements. This comprises of the following;

Element 1: Money that is paid and the market value of the property that is needed to be paid

for purchasing the asset.

Element 2: This includes the incidental cost that has occurred for the acquisition of the asset.

Element 3: The cost involved in the ownership of the asset such as the loan interest, repairs

and insurance.

Element 4: The capital expenses occurred in increasing the value of the asset or which is

associated to the installation of the asset.

Element 5: The capital expenses that is occurred while maintaining the assets title and rights.

The taxpayer should denote that they are not permitted to obtain deduction for the

costs that are occurred in acquiring or selling the property. These costs are added into the cost

base of the property for the purpose of CGT.

Emma here sells the block of land for $1,000,000. The sale of land has resulted in the

CGT event A1 under “sec 104-10, ITAA 1997” (Bentley 2019). The acquisition price that

was paid for acquiring the land by Emma was $250,000. The cost that is occurred in

acquisition should be viewed as the cost paid to acquire the property based on the available

market value. The sum of $250,000 will be included in the first element of the cost base of

the land for CGT purpose.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Emma is also seen to have paid a sum of $5000 in the stamp duty and $10,000 as the

legal fees to acquire the property. Neither of the above listed expenditure can be considered a

tax deductible. Nevertheless. Along with the purchase price of $250,000, these expenses will

be included under the second element of the cost base as the incidental cost of the property.

Emma paid a council fees, insurance, rates and water charges that totalled $22,000.

These expenses are non-capital ownership expenditure and these costs have not been claimed

by Emma as tax deduction. Under the third element of the cost base and reduced cost of the

land it will be added for CGT purpose.

She later reports that she had paid a sum of $5000 as the legal expenditure for solving

the dispute with the neighbours. These cost will be identified as the capital expenses that

Emma has incurred in maintaining the rights of the title to the asset. Hence, as the cost is non-

deductible it would be added into the cost base of the asset under the fifth element.

Emma also incurred an expense of $27,500 for removing the pine trees that were on

the property. The expenses incurred should be viewed as the capital expenditure that is

occurred in increasing the value of the asset. Under the fourth element of the cost base it

would be added for the CGT purpose. The overall cost base for the CGT purpose is computed

below;

Emma is also seen to have paid a sum of $5000 in the stamp duty and $10,000 as the

legal fees to acquire the property. Neither of the above listed expenditure can be considered a

tax deductible. Nevertheless. Along with the purchase price of $250,000, these expenses will

be included under the second element of the cost base as the incidental cost of the property.

Emma paid a council fees, insurance, rates and water charges that totalled $22,000.

These expenses are non-capital ownership expenditure and these costs have not been claimed

by Emma as tax deduction. Under the third element of the cost base and reduced cost of the

land it will be added for CGT purpose.

She later reports that she had paid a sum of $5000 as the legal expenditure for solving

the dispute with the neighbours. These cost will be identified as the capital expenses that

Emma has incurred in maintaining the rights of the title to the asset. Hence, as the cost is non-

deductible it would be added into the cost base of the asset under the fifth element.

Emma also incurred an expense of $27,500 for removing the pine trees that were on

the property. The expenses incurred should be viewed as the capital expenditure that is

occurred in increasing the value of the asset. Under the fourth element of the cost base it

would be added for the CGT purpose. The overall cost base for the CGT purpose is computed

below;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Computation of Capital Gains

Particulars Amount ($) Amount ($)

CGT Event A 1 [s.104-10 (1), ITAA 1997]

Sales Proceeds 1,000,000

Less: Cost of Sale 25,000

Gross Proceeds 975,000

Element 1 [s.110-25(2) ITAA 1997]

Cost of Acquisition 250,000

Element 2 [s.110-25 ITAA 1997]

Add: Incidental Cost

Stamp Duty 5,000

Legal Fees 10,000

Element 3 [s.110-25 (4), ITAA 1997]

Non-Capital ownership cost

Interest on Loan 32,000

Element 4 [s.110-25 (5) ITAA 1997]

Capital enhancement cost

Removal of Pine trees 27,500

Element 5 [s.110-25 (6), ITAA 97]

Capital Expenditure

Legal Fees 5,000

Total Cost Base 329,500

Capital Gains 645,500

50% CGT Discount 322,750

Net Capital Gains 322,750

Sale of Emma’s 1000 shares in Rio Tinto for $50.85 per share:

“Sec 108-5, ITAA 1997” explains that the CGT asset includes any form of property

or the legal or the equitable rights which is not the property. The examples of the assets

include the shares in company or units in the trust (Steyn et al., 2018). When a taxpayer

makes the capital loss then the capital is only allowed to be offset against the capital gains

and it is not deductible. The net loss should be carried forward by the taxpayer to the next

year. The regimes of CGT was introduced in 20th September 1985 and assets that are acquired

Computation of Capital Gains

Particulars Amount ($) Amount ($)

CGT Event A 1 [s.104-10 (1), ITAA 1997]

Sales Proceeds 1,000,000

Less: Cost of Sale 25,000

Gross Proceeds 975,000

Element 1 [s.110-25(2) ITAA 1997]

Cost of Acquisition 250,000

Element 2 [s.110-25 ITAA 1997]

Add: Incidental Cost

Stamp Duty 5,000

Legal Fees 10,000

Element 3 [s.110-25 (4), ITAA 1997]

Non-Capital ownership cost

Interest on Loan 32,000

Element 4 [s.110-25 (5) ITAA 1997]

Capital enhancement cost

Removal of Pine trees 27,500

Element 5 [s.110-25 (6), ITAA 97]

Capital Expenditure

Legal Fees 5,000

Total Cost Base 329,500

Capital Gains 645,500

50% CGT Discount 322,750

Net Capital Gains 322,750

Sale of Emma’s 1000 shares in Rio Tinto for $50.85 per share:

“Sec 108-5, ITAA 1997” explains that the CGT asset includes any form of property

or the legal or the equitable rights which is not the property. The examples of the assets

include the shares in company or units in the trust (Steyn et al., 2018). When a taxpayer

makes the capital loss then the capital is only allowed to be offset against the capital gains

and it is not deductible. The net loss should be carried forward by the taxpayer to the next

year. The regimes of CGT was introduced in 20th September 1985 and assets that are acquired

8TAXATION LAW

after that date are taken into the consideration only while assets that are purchased before that

date are exempted from capital gains tax and classified as pre-CGT asset.

Emma here purchased shares in the Rio Tinto for $3.5 in 1982 while she sold it for

$50.85 per share in the present tax year.

Computation of Capital Gains

Particulars Amount ($) Amount ($)

CGT Event A 1 [s.104-10 (1), ITAA 1997]

Sale of Shares in Rio Tinto

Sales Proceeds 50,850

Less: Brokerage Fees 1,017

Gross Proceeds 49,833

Element 1 [s.110-25(2) ITAA 1997]

Cost of Acquisition 3500

Net Capital Gains (Exempted) 46,333

The sale of shares has resulted in the CGT event A1 under “sec 104-10, ITAA 1997”.

The shares were bought by Emma before the introduction of the CGT regimes hence the asset

will be classified as the pre-CGT asset. The capital gains that are made from the shares will

be exempted from the CGT purpose because the shares are pre-CGT asset.

Sale of stamps for $60,000:

As noted in “sec 108-10 (2)” collectibles represent the items that kept by taxpayer for

their own personal enjoyment and usage (He et al., 2019). The examples of the collectables

include the following;

a. Antiques

b. Artwork involving paintings, sculptures

c. Jewellery

d. Rare stamps and coins

after that date are taken into the consideration only while assets that are purchased before that

date are exempted from capital gains tax and classified as pre-CGT asset.

Emma here purchased shares in the Rio Tinto for $3.5 in 1982 while she sold it for

$50.85 per share in the present tax year.

Computation of Capital Gains

Particulars Amount ($) Amount ($)

CGT Event A 1 [s.104-10 (1), ITAA 1997]

Sale of Shares in Rio Tinto

Sales Proceeds 50,850

Less: Brokerage Fees 1,017

Gross Proceeds 49,833

Element 1 [s.110-25(2) ITAA 1997]

Cost of Acquisition 3500

Net Capital Gains (Exempted) 46,333

The sale of shares has resulted in the CGT event A1 under “sec 104-10, ITAA 1997”.

The shares were bought by Emma before the introduction of the CGT regimes hence the asset

will be classified as the pre-CGT asset. The capital gains that are made from the shares will

be exempted from the CGT purpose because the shares are pre-CGT asset.

Sale of stamps for $60,000:

As noted in “sec 108-10 (2)” collectibles represent the items that kept by taxpayer for

their own personal enjoyment and usage (He et al., 2019). The examples of the collectables

include the following;

a. Antiques

b. Artwork involving paintings, sculptures

c. Jewellery

d. Rare stamps and coins

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

The capital loss that is produced from the collectables must be disregarded and it is only

allowable to be offset alongside to the capital gains made from the collectables.

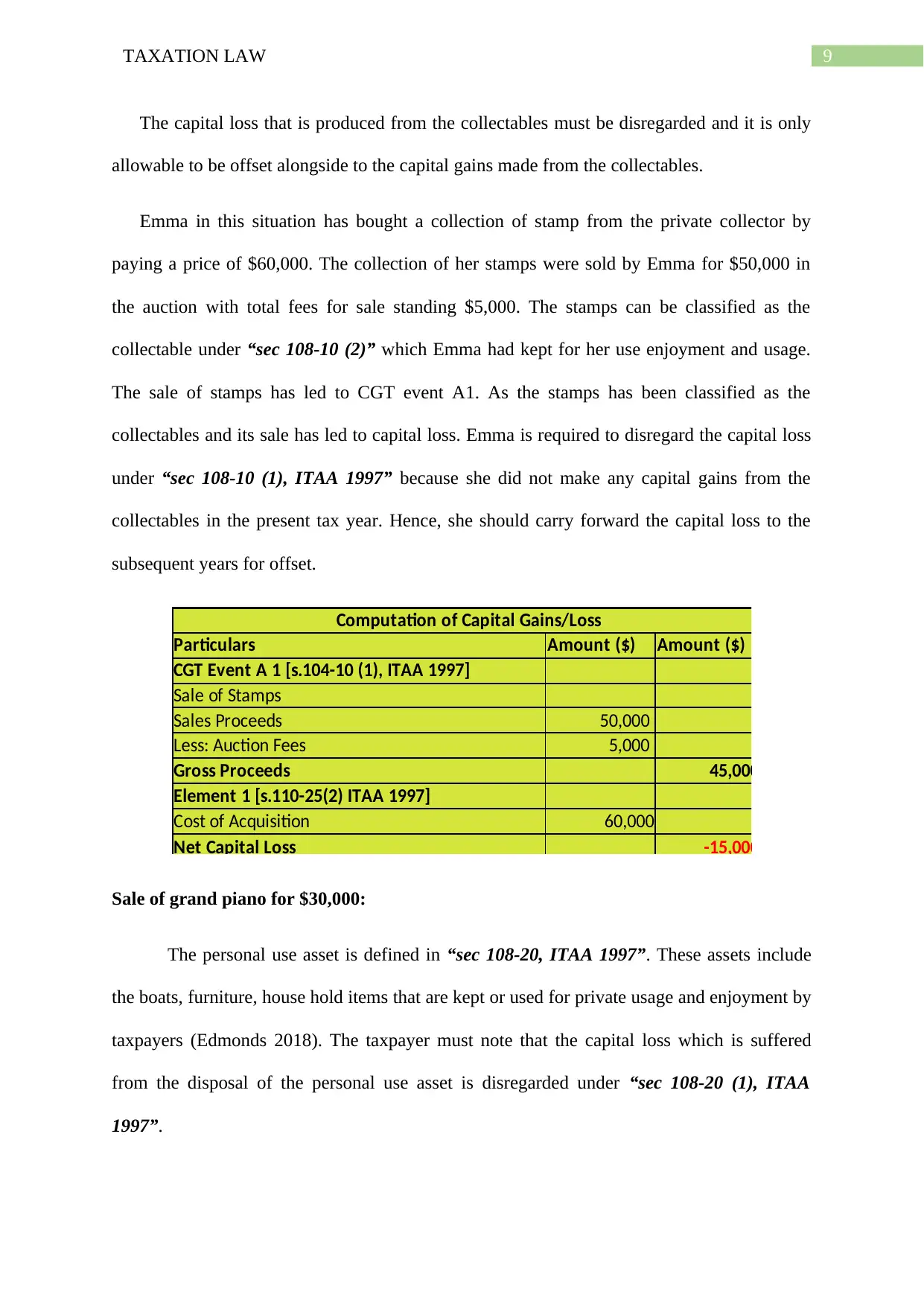

Emma in this situation has bought a collection of stamp from the private collector by

paying a price of $60,000. The collection of her stamps were sold by Emma for $50,000 in

the auction with total fees for sale standing $5,000. The stamps can be classified as the

collectable under “sec 108-10 (2)” which Emma had kept for her use enjoyment and usage.

The sale of stamps has led to CGT event A1. As the stamps has been classified as the

collectables and its sale has led to capital loss. Emma is required to disregard the capital loss

under “sec 108-10 (1), ITAA 1997” because she did not make any capital gains from the

collectables in the present tax year. Hence, she should carry forward the capital loss to the

subsequent years for offset.

Computation of Capital Gains/Loss

Particulars Amount ($) Amount ($)

CGT Event A 1 [s.104-10 (1), ITAA 1997]

Sale of Stamps

Sales Proceeds 50,000

Less: Auction Fees 5,000

Gross Proceeds 45,000

Element 1 [s.110-25(2) ITAA 1997]

Cost of Acquisition 60,000

Net Capital Loss -15,000

Sale of grand piano for $30,000:

The personal use asset is defined in “sec 108-20, ITAA 1997”. These assets include

the boats, furniture, house hold items that are kept or used for private usage and enjoyment by

taxpayers (Edmonds 2018). The taxpayer must note that the capital loss which is suffered

from the disposal of the personal use asset is disregarded under “sec 108-20 (1), ITAA

1997”.

The capital loss that is produced from the collectables must be disregarded and it is only

allowable to be offset alongside to the capital gains made from the collectables.

Emma in this situation has bought a collection of stamp from the private collector by

paying a price of $60,000. The collection of her stamps were sold by Emma for $50,000 in

the auction with total fees for sale standing $5,000. The stamps can be classified as the

collectable under “sec 108-10 (2)” which Emma had kept for her use enjoyment and usage.

The sale of stamps has led to CGT event A1. As the stamps has been classified as the

collectables and its sale has led to capital loss. Emma is required to disregard the capital loss

under “sec 108-10 (1), ITAA 1997” because she did not make any capital gains from the

collectables in the present tax year. Hence, she should carry forward the capital loss to the

subsequent years for offset.

Computation of Capital Gains/Loss

Particulars Amount ($) Amount ($)

CGT Event A 1 [s.104-10 (1), ITAA 1997]

Sale of Stamps

Sales Proceeds 50,000

Less: Auction Fees 5,000

Gross Proceeds 45,000

Element 1 [s.110-25(2) ITAA 1997]

Cost of Acquisition 60,000

Net Capital Loss -15,000

Sale of grand piano for $30,000:

The personal use asset is defined in “sec 108-20, ITAA 1997”. These assets include

the boats, furniture, house hold items that are kept or used for private usage and enjoyment by

taxpayers (Edmonds 2018). The taxpayer must note that the capital loss which is suffered

from the disposal of the personal use asset is disregarded under “sec 108-20 (1), ITAA

1997”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

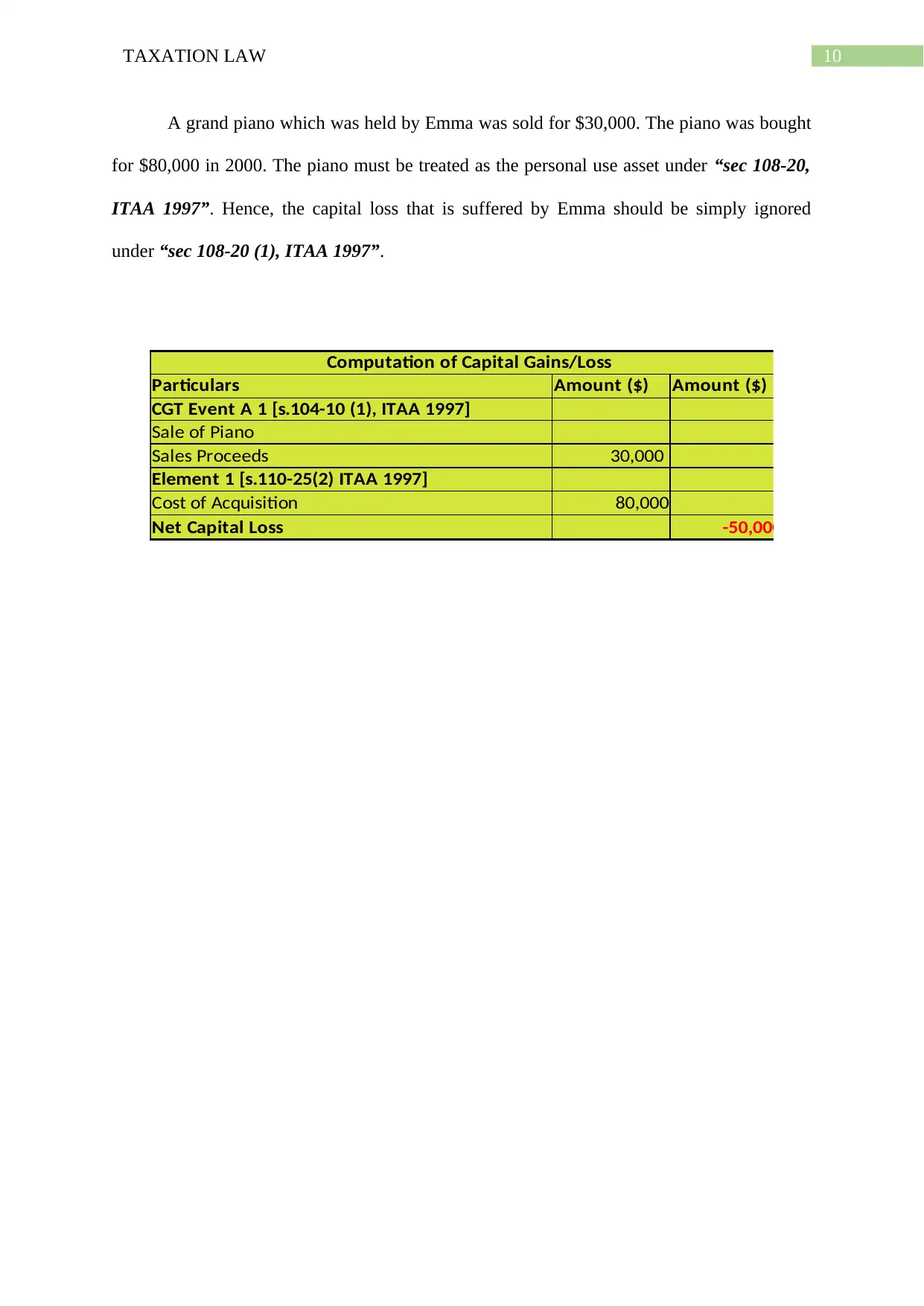

A grand piano which was held by Emma was sold for $30,000. The piano was bought

for $80,000 in 2000. The piano must be treated as the personal use asset under “sec 108-20,

ITAA 1997”. Hence, the capital loss that is suffered by Emma should be simply ignored

under “sec 108-20 (1), ITAA 1997”.

Computation of Capital Gains/Loss

Particulars Amount ($) Amount ($)

CGT Event A 1 [s.104-10 (1), ITAA 1997]

Sale of Piano

Sales Proceeds 30,000

Element 1 [s.110-25(2) ITAA 1997]

Cost of Acquisition 80,000

Net Capital Loss -50,000

A grand piano which was held by Emma was sold for $30,000. The piano was bought

for $80,000 in 2000. The piano must be treated as the personal use asset under “sec 108-20,

ITAA 1997”. Hence, the capital loss that is suffered by Emma should be simply ignored

under “sec 108-20 (1), ITAA 1997”.

Computation of Capital Gains/Loss

Particulars Amount ($) Amount ($)

CGT Event A 1 [s.104-10 (1), ITAA 1997]

Sale of Piano

Sales Proceeds 30,000

Element 1 [s.110-25(2) ITAA 1997]

Cost of Acquisition 80,000

Net Capital Loss -50,000

11TAXATION LAW

References:

Bentley, D., 2019. Does A Capital Gains Tax Work? The Australian Experience Eleven

Years On. Journal of Malaysian and Comparative Law, 23, pp.13-36.

Edmonds, R., 2018. Resource Capital Fund IV LP: the issues on appeal?. Taxation in

Australia, 53(1), p.22.

He, E., Jacob, M., Vashishtha, R. and Venkatachalam, M., 2019. The effect of capital gains

tax policy changes on long-term investments. Available at SSRN 3383649.

Hickman, K., 2018. From capital gains to tax administration, and everything in between: in

honour of Professor Chris Evans. eJTR, 16, p.269.

Kraal, D. and Kasipillai, J., 2016. Finally, a goods and services tax for Malaysia: A

comparison to Australia's GST experience. Austl. Tax F., 31, p.257.

Krever, R. and Sadiq, K., 2019. Non-residents and capital gains tax in Australia. Canadian

Tax Journal/Revue fiscale canadienne, 67(1).

Ramli, R., Palil, M.R., Hassan, N.S.A. and Mustapha, A.F., 2015. Compliance costs of Goods

and Services Tax (GST) among small and medium enterprises. Jurnal Pengurusan (UKM

Journal of Management), 45.

Ranjan, R., 2018. Goods and Services Tax (GST): An Overview. Journal Homepage:

http://www. ijmra. us, 8(8).

Schenk, A., Thuronyi, V. and Cui, W., 2016. Value added tax: a comparative approach.

Steyn, T., Smulders, S., Stark, K. and Penning, I., 2018. Capital gains tax research: an initial

synthesis of the literature. eJTR, 16, p.278.

References:

Bentley, D., 2019. Does A Capital Gains Tax Work? The Australian Experience Eleven

Years On. Journal of Malaysian and Comparative Law, 23, pp.13-36.

Edmonds, R., 2018. Resource Capital Fund IV LP: the issues on appeal?. Taxation in

Australia, 53(1), p.22.

He, E., Jacob, M., Vashishtha, R. and Venkatachalam, M., 2019. The effect of capital gains

tax policy changes on long-term investments. Available at SSRN 3383649.

Hickman, K., 2018. From capital gains to tax administration, and everything in between: in

honour of Professor Chris Evans. eJTR, 16, p.269.

Kraal, D. and Kasipillai, J., 2016. Finally, a goods and services tax for Malaysia: A

comparison to Australia's GST experience. Austl. Tax F., 31, p.257.

Krever, R. and Sadiq, K., 2019. Non-residents and capital gains tax in Australia. Canadian

Tax Journal/Revue fiscale canadienne, 67(1).

Ramli, R., Palil, M.R., Hassan, N.S.A. and Mustapha, A.F., 2015. Compliance costs of Goods

and Services Tax (GST) among small and medium enterprises. Jurnal Pengurusan (UKM

Journal of Management), 45.

Ranjan, R., 2018. Goods and Services Tax (GST): An Overview. Journal Homepage:

http://www. ijmra. us, 8(8).

Schenk, A., Thuronyi, V. and Cui, W., 2016. Value added tax: a comparative approach.

Steyn, T., Smulders, S., Stark, K. and Penning, I., 2018. Capital gains tax research: an initial

synthesis of the literature. eJTR, 16, p.278.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.