HI6028 Taxation Theory, Practice & Law Assignment: GST and CGT

VerifiedAdded on 2022/12/01

|11

|2742

|321

Homework Assignment

AI Summary

This assignment analyzes two key aspects of Australian taxation law: Goods and Services Tax (GST) and Capital Gains Tax (CGT). The GST section examines the City Sky Co. case study, assessing the applicability of GST credits for construction inputs and legal services, considering relevant tax laws and material facts. It determines whether GST credit is applicable in the case of wage payments to a lawyer. The CGT portion focuses on Emma's financial transactions, including the sale of land, shares, a stamp collection, and a piano. It calculates capital gains and losses, applying relevant tax laws to determine the tax implications of each transaction, including ownership costs, discounts, and taxable income, providing a detailed breakdown of each scenario.

Taxation Theory, Practice & Law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1: The goods and services tax (GST).................................................................3

Introduction...........................................................................................................................3

Description of GST credit:..................................................................................................3

Identification of legal issues and relevant taxation laws:..............................................4

Succinct application of tax law to material facts:............................................................4

Conclusions:.........................................................................................................................5

Question 2: Capital gains tax (CGT)....................................................................................6

Introduction...........................................................................................................................6

Description of Capital gains tax (CGT):................................................................................6

Identification of legal issues and succinct application of relevant tax law to material

facts:......................................................................................................................................7

Sale of a block of land for $1,000,000:............................................................................7

Sale of Emma’s 1000 shares in Rio Tinto for $50.85 per share:.................................8

Sale of a stamp collection Emma had purchased, from a private collector, in

January 2015 for $60,000:.................................................................................................9

Sale of a grand piano for $30,000:...................................................................................9

Conclusion:.........................................................................................................................10

Reference:..............................................................................................................................11

Question 1: The goods and services tax (GST).................................................................3

Introduction...........................................................................................................................3

Description of GST credit:..................................................................................................3

Identification of legal issues and relevant taxation laws:..............................................4

Succinct application of tax law to material facts:............................................................4

Conclusions:.........................................................................................................................5

Question 2: Capital gains tax (CGT)....................................................................................6

Introduction...........................................................................................................................6

Description of Capital gains tax (CGT):................................................................................6

Identification of legal issues and succinct application of relevant tax law to material

facts:......................................................................................................................................7

Sale of a block of land for $1,000,000:............................................................................7

Sale of Emma’s 1000 shares in Rio Tinto for $50.85 per share:.................................8

Sale of a stamp collection Emma had purchased, from a private collector, in

January 2015 for $60,000:.................................................................................................9

Sale of a grand piano for $30,000:...................................................................................9

Conclusion:.........................................................................................................................10

Reference:..............................................................................................................................11

Question 1: The goods and services tax (GST)

Introduction

The first part deals with the consequences of goods and service tax (GST) in the

context of the case study of The City Sky co. It focus on the legal issues relevant to

taxation law and GST credit, identification of material facts with respect to GST

aspect along with the application of tax laws to material facts succinctly. It also

covers if GST credit applicable in case of wage payment made to lawyer.

Description of GST credit:

An input tax credit or GST credit can be claimed by a business organization when

the GST is included in the price of goods & services or the inputs that are being

bought for utilizing those inputs for business purposes only.

The GST credit refers to the fact that if a business organization makes some

purchase of goods and services that are to be utilised for business purpose only and

if the business has acquired those goods and services at a GST inclusive price

where the total monetary value of the GST inclusive price is higher than A$82.50,

then the business is entitled to claim credit or exemption for the GST included in the

price of those inputs being purchased ("Claiming GST credits", 2019).

Identification of material facts regarding The City Sky Co goods and services

taxation aspects:

In the present scenario the business organization City Sky Co which is GST

registered is looking for building 15 apartments on a vacant piece of land south of

Brisbane. The apartments are being built for selling them out in future.

As City Sky Co is GST registered then the business is entitled to claim GST credit on

the supply price of inputs or goods & services that are to be purchased for business

purpose provided that the supply price of inputs or goods & services are including

the GST and the inputs are being supplied by a supplier who is also registered for

GST.

In addition to that it is being assumed that City Sky Co is keeping the invoices of

purchases of inputs that are being purchased from a GST registered supplier who is

Introduction

The first part deals with the consequences of goods and service tax (GST) in the

context of the case study of The City Sky co. It focus on the legal issues relevant to

taxation law and GST credit, identification of material facts with respect to GST

aspect along with the application of tax laws to material facts succinctly. It also

covers if GST credit applicable in case of wage payment made to lawyer.

Description of GST credit:

An input tax credit or GST credit can be claimed by a business organization when

the GST is included in the price of goods & services or the inputs that are being

bought for utilizing those inputs for business purposes only.

The GST credit refers to the fact that if a business organization makes some

purchase of goods and services that are to be utilised for business purpose only and

if the business has acquired those goods and services at a GST inclusive price

where the total monetary value of the GST inclusive price is higher than A$82.50,

then the business is entitled to claim credit or exemption for the GST included in the

price of those inputs being purchased ("Claiming GST credits", 2019).

Identification of material facts regarding The City Sky Co goods and services

taxation aspects:

In the present scenario the business organization City Sky Co which is GST

registered is looking for building 15 apartments on a vacant piece of land south of

Brisbane. The apartments are being built for selling them out in future.

As City Sky Co is GST registered then the business is entitled to claim GST credit on

the supply price of inputs or goods & services that are to be purchased for business

purpose provided that the supply price of inputs or goods & services are including

the GST and the inputs are being supplied by a supplier who is also registered for

GST.

In addition to that it is being assumed that City Sky Co is keeping the invoices of

purchases of inputs that are being purchased from a GST registered supplier who is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

supplying the inputs at a GST inclusive price("Wondering what an input tax credit

is?",2019).

Identification of legal issues and relevant taxation laws:

A business organization can claim for GST credit on purchase of goods and services

or inputs that are going to be solely used for business purpose provided both the

purchaser of input as well as supplier of inputs are GST registered and the invoice

containing GST inclusive price of inputs is higher than A$82.50.

However the business will not be able to claim GST credit on GST inclusive

purchase price of goods and services provided the inputs are to be used in some

private purpose and either purchaser or both the purchaser or the supplier are not

registered for GST.

The purchaser for goods and services will not be entitled to GST provided the input

price of GST free (like the ingredients of basic food) and if the input purchased is

input taxed.

Input tax credit or ITC cannot be claimed in case of the purchase of the following

items;

On purchase of vehicles used for transportation

On purchase of Food, beverages& club membership services

On purchase of insurance, repair and maintenance services

On hiring of work contract services

On purchase of inputs to be used for construction of immovable properties where the

constructions are to be done in own account of the ‘purchaser of inputs

On Wages paid to the staff ("When you cannot claim a GST credit", 2019)

Succinct application of tax law to material facts:

But here the organization City Sky Co is purchasing the inputs at a GST inclusive

price where the inputs are to be used for manufacturing building apartments which

can be categorised as immovable property to be prepared in the own account of the

is?",2019).

Identification of legal issues and relevant taxation laws:

A business organization can claim for GST credit on purchase of goods and services

or inputs that are going to be solely used for business purpose provided both the

purchaser of input as well as supplier of inputs are GST registered and the invoice

containing GST inclusive price of inputs is higher than A$82.50.

However the business will not be able to claim GST credit on GST inclusive

purchase price of goods and services provided the inputs are to be used in some

private purpose and either purchaser or both the purchaser or the supplier are not

registered for GST.

The purchaser for goods and services will not be entitled to GST provided the input

price of GST free (like the ingredients of basic food) and if the input purchased is

input taxed.

Input tax credit or ITC cannot be claimed in case of the purchase of the following

items;

On purchase of vehicles used for transportation

On purchase of Food, beverages& club membership services

On purchase of insurance, repair and maintenance services

On hiring of work contract services

On purchase of inputs to be used for construction of immovable properties where the

constructions are to be done in own account of the ‘purchaser of inputs

On Wages paid to the staff ("When you cannot claim a GST credit", 2019)

Succinct application of tax law to material facts:

But here the organization City Sky Co is purchasing the inputs at a GST inclusive

price where the inputs are to be used for manufacturing building apartments which

can be categorised as immovable property to be prepared in the own account of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business which will be later sold by the business("When you cannot claim a GST

credit", 2019).

Thus it can be seen that City Sky Co is going to build this apartments in their own

account only with an intention for selling them out latter and thus the building

apartments that are going to be prepared by the business is not going to be used for

manufacturing purpose unlike plant and machineries. In such a situation City SKY

Co is not supposed to entitle for the GST credit ("Cases Where Input Tax Credit

under GST Cannot Be Availed", 2019).

But if the City Sky Co was going to purchase those inputs for developing plant and

machineries then the company could have claimed for a GST credit at the rate of

10%(as the GST tax rate in Australia is 10%) over the purchase price (inclusive of

GST) of inputs that would have been used for building the plant and machineries that

are going to be used for developing the plant and machineries ("GST", 2019).

The other factor that must be taken under consideration is that the City Sky Co has

hired a local lawyer Maurice Blackburn for providing the legal services as well as

legal issues that will arise while holding the development process. The hiring cost of

the lawyer Maurice Blackburn is $33,000 which City Sky Co is paying out to the

lawyer as wage. As the amount $33,000 is paid out as wage, therefore City Sky Co

will not be able to claim for any GST credit with respect to this service being

purchased. The legislation of input tax credit requires that GST credit cannot be

claimed on wage being paid to a staff (Maurice Blackburn) who is being hired under

a contract ("GST", 2019).

Conclusions:

From the above discussion of the case study incidence following the relevant tax law

it can be seen that the chosen organization of City Sky Co is not entitled to claim for

a GST credit on purchase of inputs to be used for construction of apartments where

the construction of these immovable properties are primarily going to be done in the

account of the company and the immovable property is not going to be used for

manufacturing purchase.

credit", 2019).

Thus it can be seen that City Sky Co is going to build this apartments in their own

account only with an intention for selling them out latter and thus the building

apartments that are going to be prepared by the business is not going to be used for

manufacturing purpose unlike plant and machineries. In such a situation City SKY

Co is not supposed to entitle for the GST credit ("Cases Where Input Tax Credit

under GST Cannot Be Availed", 2019).

But if the City Sky Co was going to purchase those inputs for developing plant and

machineries then the company could have claimed for a GST credit at the rate of

10%(as the GST tax rate in Australia is 10%) over the purchase price (inclusive of

GST) of inputs that would have been used for building the plant and machineries that

are going to be used for developing the plant and machineries ("GST", 2019).

The other factor that must be taken under consideration is that the City Sky Co has

hired a local lawyer Maurice Blackburn for providing the legal services as well as

legal issues that will arise while holding the development process. The hiring cost of

the lawyer Maurice Blackburn is $33,000 which City Sky Co is paying out to the

lawyer as wage. As the amount $33,000 is paid out as wage, therefore City Sky Co

will not be able to claim for any GST credit with respect to this service being

purchased. The legislation of input tax credit requires that GST credit cannot be

claimed on wage being paid to a staff (Maurice Blackburn) who is being hired under

a contract ("GST", 2019).

Conclusions:

From the above discussion of the case study incidence following the relevant tax law

it can be seen that the chosen organization of City Sky Co is not entitled to claim for

a GST credit on purchase of inputs to be used for construction of apartments where

the construction of these immovable properties are primarily going to be done in the

account of the company and the immovable property is not going to be used for

manufacturing purchase.

Secondly the City Sky Co is not also entitled to claim GST credit on purchase of the

service of the lawyer Maurice Blackburn where the company is paying out an amount

of 33000 as wage to the lawyer for his service of legal advice as GST credit is not

applicable over wage payment.

Question 2: Capital gains tax (CGT)

Introduction

This section deals with the tax application pertaining to capital gains tax (GST) for

Emma who conducts different transaction of sales namely block land, shares, stamp

collectible and piano. It evaluates the legal issues and financial implication on the

sale transaction She incurs a profit in the first three and a loss in the sale of Piano

and how it impacts her taxable income is explained with calculation and justification.

Description of Capital gains tax (CGT):

The capital gain taxation in Australia refers to the taxation to be imposed on gain or

profit earned on the sale of asset. The assets that are taxed are properties, real

estate and shares.

The capital gain taxation is being imposed on in the year in which the contract of

asset disposal has been undertaken and not in the year in which the asset is being

disposed and final settlement is being received.

If a property is held for more than one year after the purchase of the asset till the

initiation of the disposal contract, then an individual is eligible for a 50% discount

over the gain attained from sale of asset and a company is only eligible for a 33.3%

discount ("Capital gains tax", 2019).

In case of an individual the taxable capital gain amount is being added to the total

income and the taxation is being done as per the income tax rate being defined with

respect to the income slabs being specified in a particular year. Whereas, in case of

a company a flat rate of 30% taxation to be imposed on the amount of capital gain.

Both individual as well as company will not have to pay any kind of capital gain

taxation over capital loss. However the capital loss cannot be used for tax

service of the lawyer Maurice Blackburn where the company is paying out an amount

of 33000 as wage to the lawyer for his service of legal advice as GST credit is not

applicable over wage payment.

Question 2: Capital gains tax (CGT)

Introduction

This section deals with the tax application pertaining to capital gains tax (GST) for

Emma who conducts different transaction of sales namely block land, shares, stamp

collectible and piano. It evaluates the legal issues and financial implication on the

sale transaction She incurs a profit in the first three and a loss in the sale of Piano

and how it impacts her taxable income is explained with calculation and justification.

Description of Capital gains tax (CGT):

The capital gain taxation in Australia refers to the taxation to be imposed on gain or

profit earned on the sale of asset. The assets that are taxed are properties, real

estate and shares.

The capital gain taxation is being imposed on in the year in which the contract of

asset disposal has been undertaken and not in the year in which the asset is being

disposed and final settlement is being received.

If a property is held for more than one year after the purchase of the asset till the

initiation of the disposal contract, then an individual is eligible for a 50% discount

over the gain attained from sale of asset and a company is only eligible for a 33.3%

discount ("Capital gains tax", 2019).

In case of an individual the taxable capital gain amount is being added to the total

income and the taxation is being done as per the income tax rate being defined with

respect to the income slabs being specified in a particular year. Whereas, in case of

a company a flat rate of 30% taxation to be imposed on the amount of capital gain.

Both individual as well as company will not have to pay any kind of capital gain

taxation over capital loss. However the capital loss cannot be used for tax

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

deductions with respect to the other income that are chargeable to tax (eChoice Ltd,

2019)

Identification of legal issues and succinct application of relevant tax law

to material facts:

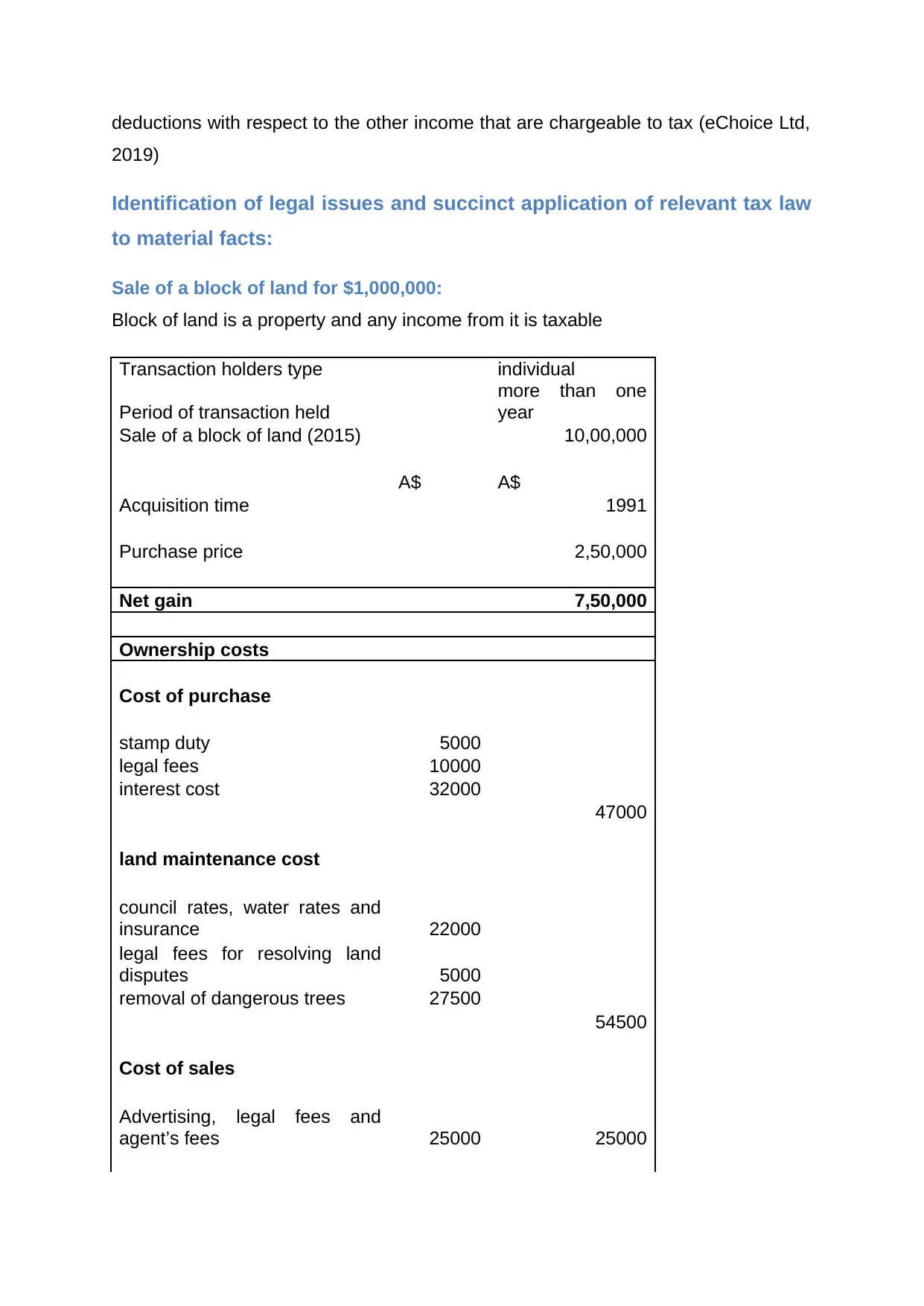

Sale of a block of land for $1,000,000:

Block of land is a property and any income from it is taxable

Transaction holders type individual

Period of transaction held

more than one

year

Sale of a block of land (2015) 10,00,000

A$ A$

Acquisition time 1991

Purchase price 2,50,000

Net gain 7,50,000

Ownership costs

Cost of purchase

stamp duty 5000

legal fees 10000

interest cost 32000

47000

land maintenance cost

council rates, water rates and

insurance 22000

legal fees for resolving land

disputes 5000

removal of dangerous trees 27500

54500

Cost of sales

Advertising, legal fees and

agent’s fees 25000 25000

2019)

Identification of legal issues and succinct application of relevant tax law

to material facts:

Sale of a block of land for $1,000,000:

Block of land is a property and any income from it is taxable

Transaction holders type individual

Period of transaction held

more than one

year

Sale of a block of land (2015) 10,00,000

A$ A$

Acquisition time 1991

Purchase price 2,50,000

Net gain 7,50,000

Ownership costs

Cost of purchase

stamp duty 5000

legal fees 10000

interest cost 32000

47000

land maintenance cost

council rates, water rates and

insurance 22000

legal fees for resolving land

disputes 5000

removal of dangerous trees 27500

54500

Cost of sales

Advertising, legal fees and

agent’s fees 25000 25000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total ownership cost on the

land 3,76,500

Net Capital gain or loss 3,73,500

As Emma is an individual so she is eligible for a 50% discount on net capital gain

and therefore only 50% of $ 373500 or $ 186750 will be added to the total taxable

income of Emma. Additionally as the property was being purchased after September

20, 1985 and before September 21, 1999, therefore the indexation method (marginal

tax rate*indexation factor*capital gain amount) will be applied for calculating the

actual tax liability.

For the purpose of calculating the capital gain taxation first of all the gain from the

disposal of asset is being calculated, then the ownership costs [cost of purchase,

cost of land maintenance and finally cost of sales] are being deducted from the

calculated capital gain for deriving the net capital gain on which 50% discount is

being applied and then the discounted amount will be added to the total taxable

income of Emma.

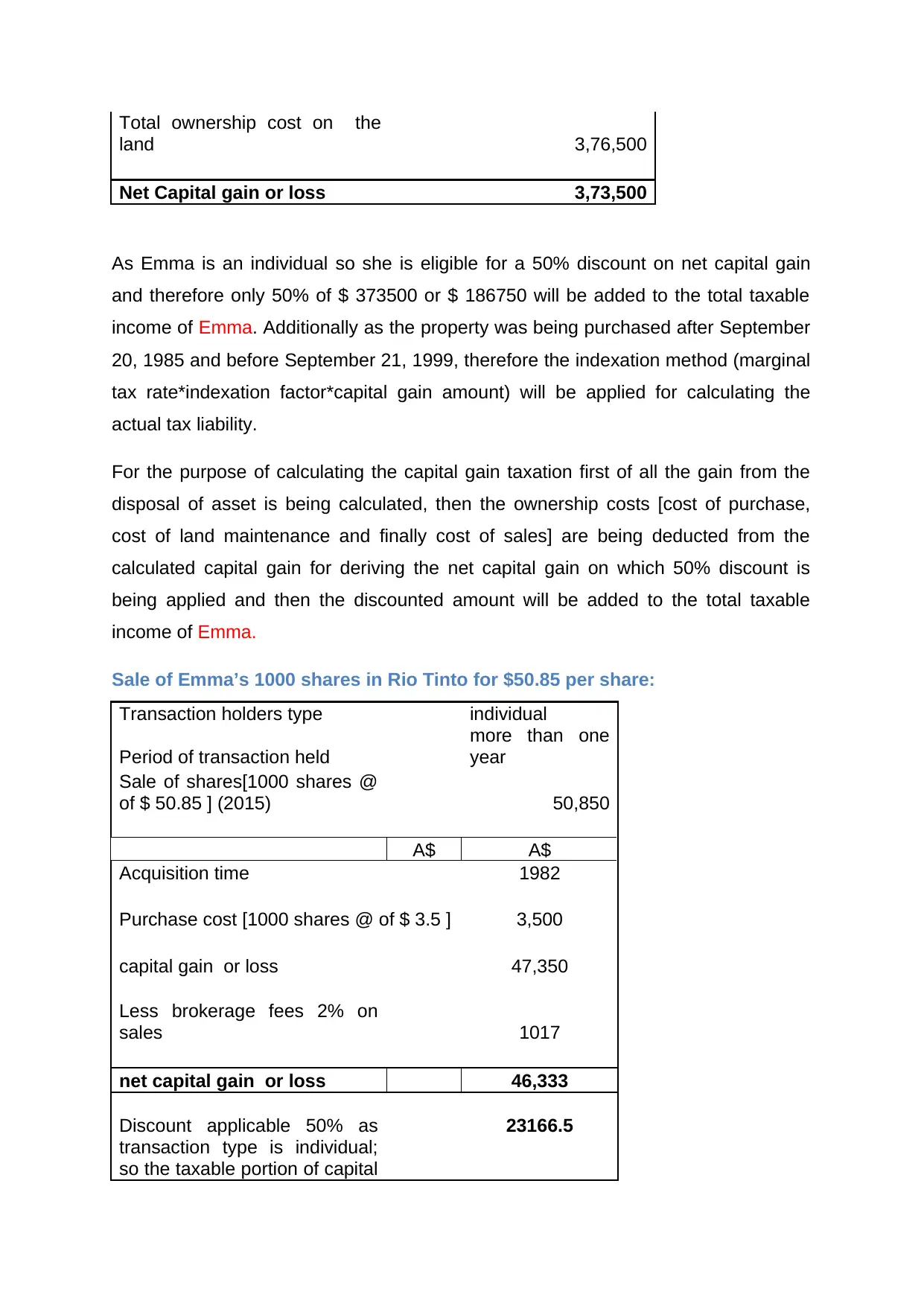

Sale of Emma’s 1000 shares in Rio Tinto for $50.85 per share:

Transaction holders type individual

Period of transaction held

more than one

year

Sale of shares[1000 shares @

of $ 50.85 ] (2015) 50,850

A$ A$

Acquisition time 1982

Purchase cost [1000 shares @ of $ 3.5 ] 3,500

capital gain or loss 47,350

Less brokerage fees 2% on

sales 1017

net capital gain or loss 46,333

Discount applicable 50% as

transaction type is individual;

so the taxable portion of capital

23166.5

land 3,76,500

Net Capital gain or loss 3,73,500

As Emma is an individual so she is eligible for a 50% discount on net capital gain

and therefore only 50% of $ 373500 or $ 186750 will be added to the total taxable

income of Emma. Additionally as the property was being purchased after September

20, 1985 and before September 21, 1999, therefore the indexation method (marginal

tax rate*indexation factor*capital gain amount) will be applied for calculating the

actual tax liability.

For the purpose of calculating the capital gain taxation first of all the gain from the

disposal of asset is being calculated, then the ownership costs [cost of purchase,

cost of land maintenance and finally cost of sales] are being deducted from the

calculated capital gain for deriving the net capital gain on which 50% discount is

being applied and then the discounted amount will be added to the total taxable

income of Emma.

Sale of Emma’s 1000 shares in Rio Tinto for $50.85 per share:

Transaction holders type individual

Period of transaction held

more than one

year

Sale of shares[1000 shares @

of $ 50.85 ] (2015) 50,850

A$ A$

Acquisition time 1982

Purchase cost [1000 shares @ of $ 3.5 ] 3,500

capital gain or loss 47,350

Less brokerage fees 2% on

sales 1017

net capital gain or loss 46,333

Discount applicable 50% as

transaction type is individual;

so the taxable portion of capital

23166.5

profit is

Thus it can be seen that out of the taxable capital gain generated from sale of shares

is $23166.5 and this amount will be added to the total taxable income of Emma and

the indexation method will not be applied in the taxation process as the property is

being acquired before September 20, 1985 and the discount rate of 50% will be

applied as the shares are being held for more than 1 year (Nab.com.au, 2019)..

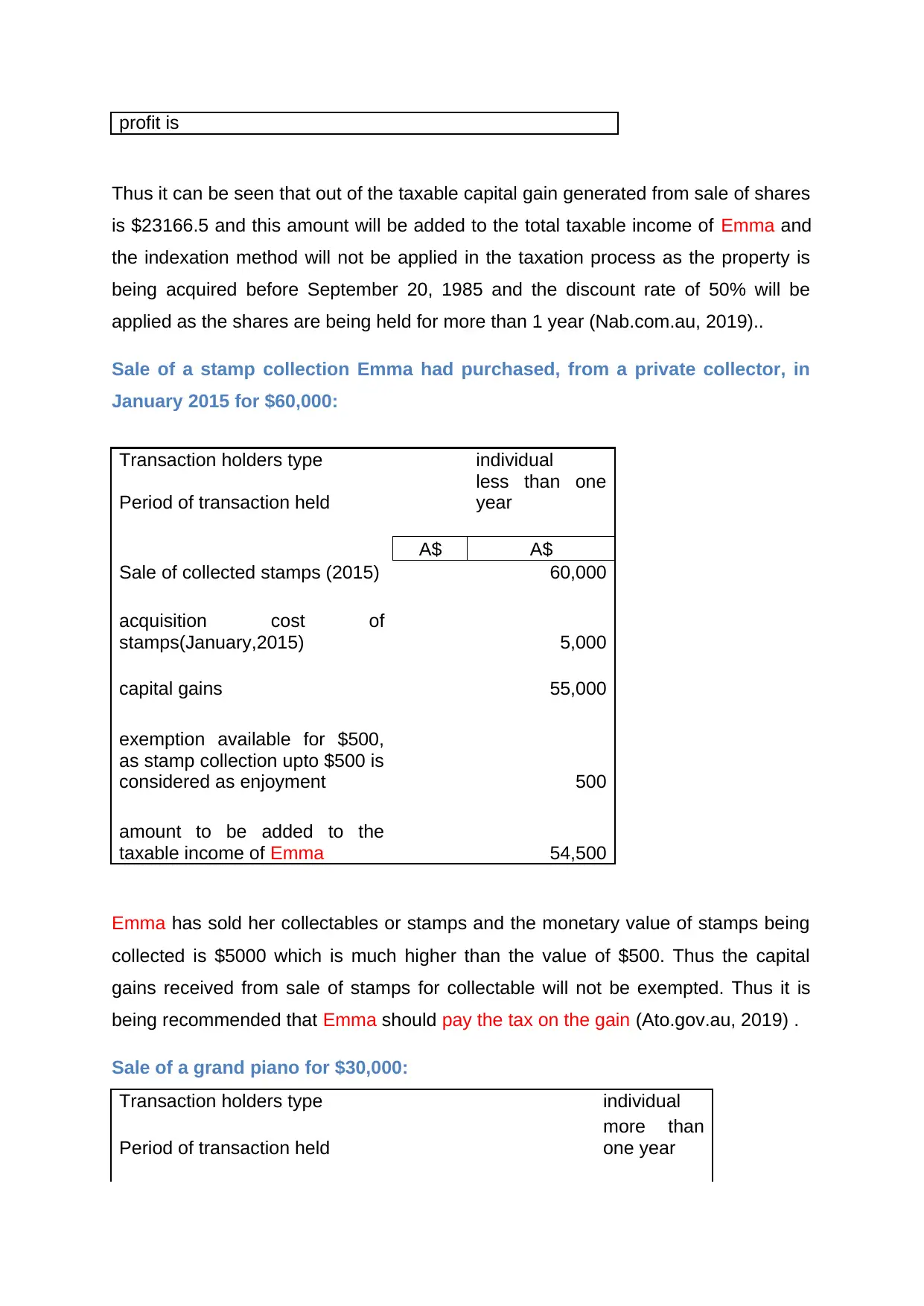

Sale of a stamp collection Emma had purchased, from a private collector, in

January 2015 for $60,000:

Transaction holders type individual

Period of transaction held

less than one

year

A$ A$

Sale of collected stamps (2015) 60,000

acquisition cost of

stamps(January,2015) 5,000

capital gains 55,000

exemption available for $500,

as stamp collection upto $500 is

considered as enjoyment 500

amount to be added to the

taxable income of Emma 54,500

Emma has sold her collectables or stamps and the monetary value of stamps being

collected is $5000 which is much higher than the value of $500. Thus the capital

gains received from sale of stamps for collectable will not be exempted. Thus it is

being recommended that Emma should pay the tax on the gain (Ato.gov.au, 2019) .

Sale of a grand piano for $30,000:

Transaction holders type individual

Period of transaction held

more than

one year

Thus it can be seen that out of the taxable capital gain generated from sale of shares

is $23166.5 and this amount will be added to the total taxable income of Emma and

the indexation method will not be applied in the taxation process as the property is

being acquired before September 20, 1985 and the discount rate of 50% will be

applied as the shares are being held for more than 1 year (Nab.com.au, 2019)..

Sale of a stamp collection Emma had purchased, from a private collector, in

January 2015 for $60,000:

Transaction holders type individual

Period of transaction held

less than one

year

A$ A$

Sale of collected stamps (2015) 60,000

acquisition cost of

stamps(January,2015) 5,000

capital gains 55,000

exemption available for $500,

as stamp collection upto $500 is

considered as enjoyment 500

amount to be added to the

taxable income of Emma 54,500

Emma has sold her collectables or stamps and the monetary value of stamps being

collected is $5000 which is much higher than the value of $500. Thus the capital

gains received from sale of stamps for collectable will not be exempted. Thus it is

being recommended that Emma should pay the tax on the gain (Ato.gov.au, 2019) .

Sale of a grand piano for $30,000:

Transaction holders type individual

Period of transaction held

more than

one year

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

A$ A$

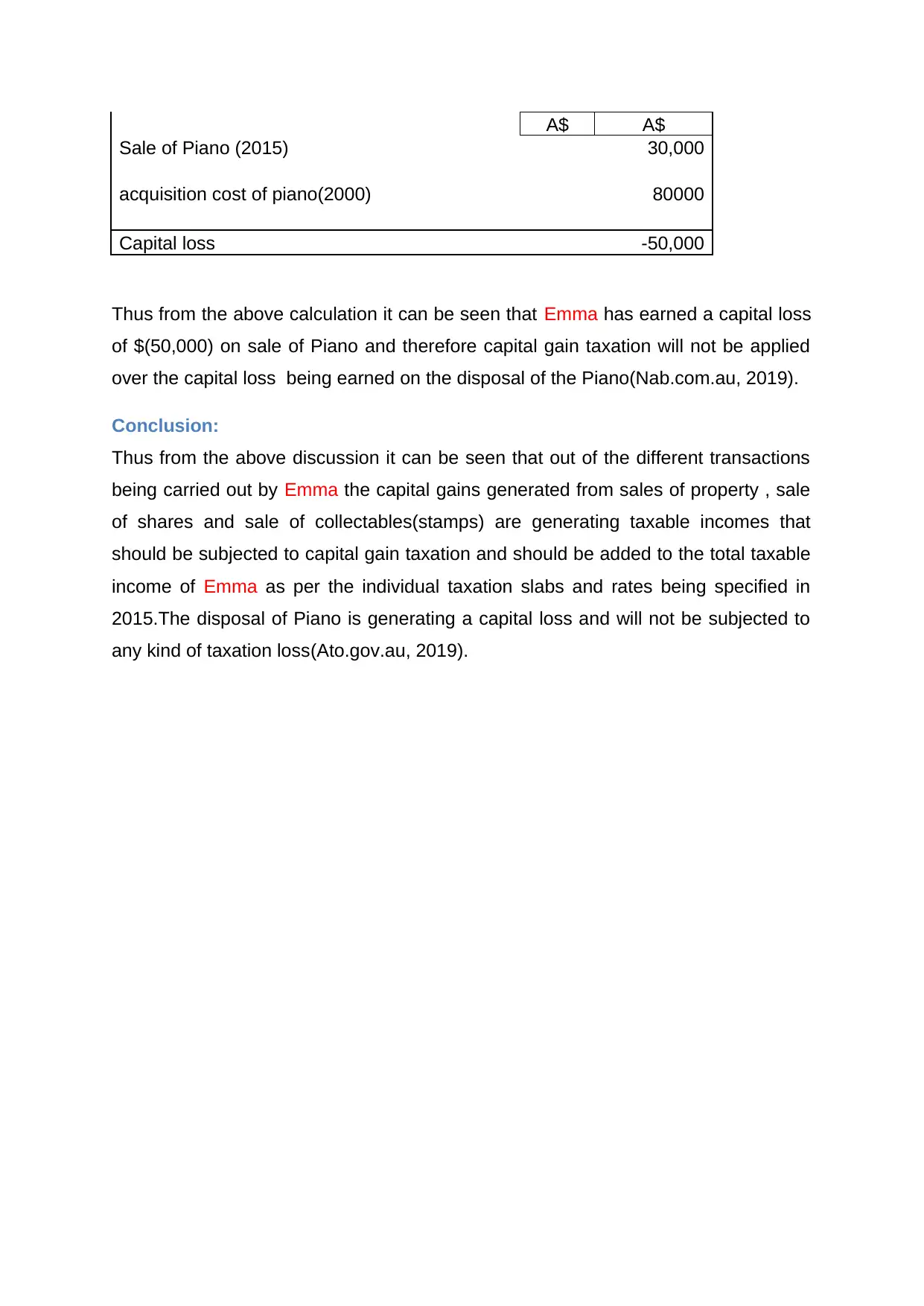

Sale of Piano (2015) 30,000

acquisition cost of piano(2000) 80000

Capital loss -50,000

Thus from the above calculation it can be seen that Emma has earned a capital loss

of $(50,000) on sale of Piano and therefore capital gain taxation will not be applied

over the capital loss being earned on the disposal of the Piano(Nab.com.au, 2019).

Conclusion:

Thus from the above discussion it can be seen that out of the different transactions

being carried out by Emma the capital gains generated from sales of property , sale

of shares and sale of collectables(stamps) are generating taxable incomes that

should be subjected to capital gain taxation and should be added to the total taxable

income of Emma as per the individual taxation slabs and rates being specified in

2015.The disposal of Piano is generating a capital loss and will not be subjected to

any kind of taxation loss(Ato.gov.au, 2019).

Sale of Piano (2015) 30,000

acquisition cost of piano(2000) 80000

Capital loss -50,000

Thus from the above calculation it can be seen that Emma has earned a capital loss

of $(50,000) on sale of Piano and therefore capital gain taxation will not be applied

over the capital loss being earned on the disposal of the Piano(Nab.com.au, 2019).

Conclusion:

Thus from the above discussion it can be seen that out of the different transactions

being carried out by Emma the capital gains generated from sales of property , sale

of shares and sale of collectables(stamps) are generating taxable incomes that

should be subjected to capital gain taxation and should be added to the total taxable

income of Emma as per the individual taxation slabs and rates being specified in

2015.The disposal of Piano is generating a capital loss and will not be subjected to

any kind of taxation loss(Ato.gov.au, 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Reference:

Ato.gov.au. (2019). Capital gains tax. Retrieved 21 September 2019, from

https://www.ato.gov.au/General/Capital-gains-tax/

Ato.gov.au. (2019). CGT assets and exemptions. Retrieved 21 September 2019,

from https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-

exemptions/

Capital gains tax. (2019). Retrieved 21 September 2019, from

https://www.ato.gov.au/General/Capital-gains-tax/

Cases Where Input Tax Credit under GST Cannot Be Availed. (2019). Retrieved 21

September 2019, from https://cleartax.in/s/gst-cases-where-input-tax-credit-is-

unavailable

Claiming GST credits. (2019). Retrieved 21 September 2019, from

https://www.ato.gov.au/Business/GST/Claiming-GST-credits/

eChoice Ltd. (2019). What is Capital Gains Tax? How is it Calculated?. Retrieved 21

September 2019, from https://www.echoice.com.au/guides/capital-gains-tax-

calculated/

GST. (2019). Retrieved 21 September 2019, from

https://www.ato.gov.au/Business/GST/

Nab.com.au. (2019). Calculating and paying capital gains tax. Retrieved 21

September 2019, from https://www.nab.com.au/personal/life-moments/manage-

money/money-basics/capital-gains-tax

When you cannot claim a GST credit. (2019). Retrieved 21 September 2019, from

https://www.ato.gov.au/business/gst/claiming-gst-credits/when-you-cannot-

claim-a-gst-credit/

Wondering what an input tax credit is?. (2019). Retrieved 21 September 2019, from

https://www.ato.gov.au/Newsroom/smallbusiness/GST-and-excise/Wondering-

what-an-input-tax-credit-is-/

Ato.gov.au. (2019). Capital gains tax. Retrieved 21 September 2019, from

https://www.ato.gov.au/General/Capital-gains-tax/

Ato.gov.au. (2019). CGT assets and exemptions. Retrieved 21 September 2019,

from https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-

exemptions/

Capital gains tax. (2019). Retrieved 21 September 2019, from

https://www.ato.gov.au/General/Capital-gains-tax/

Cases Where Input Tax Credit under GST Cannot Be Availed. (2019). Retrieved 21

September 2019, from https://cleartax.in/s/gst-cases-where-input-tax-credit-is-

unavailable

Claiming GST credits. (2019). Retrieved 21 September 2019, from

https://www.ato.gov.au/Business/GST/Claiming-GST-credits/

eChoice Ltd. (2019). What is Capital Gains Tax? How is it Calculated?. Retrieved 21

September 2019, from https://www.echoice.com.au/guides/capital-gains-tax-

calculated/

GST. (2019). Retrieved 21 September 2019, from

https://www.ato.gov.au/Business/GST/

Nab.com.au. (2019). Calculating and paying capital gains tax. Retrieved 21

September 2019, from https://www.nab.com.au/personal/life-moments/manage-

money/money-basics/capital-gains-tax

When you cannot claim a GST credit. (2019). Retrieved 21 September 2019, from

https://www.ato.gov.au/business/gst/claiming-gst-credits/when-you-cannot-

claim-a-gst-credit/

Wondering what an input tax credit is?. (2019). Retrieved 21 September 2019, from

https://www.ato.gov.au/Newsroom/smallbusiness/GST-and-excise/Wondering-

what-an-input-tax-credit-is-/

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.