Holmes Institute HI6028 Taxation Assignment: Analysis of Tax Law

VerifiedAdded on 2022/11/14

|17

|2806

|125

Homework Assignment

AI Summary

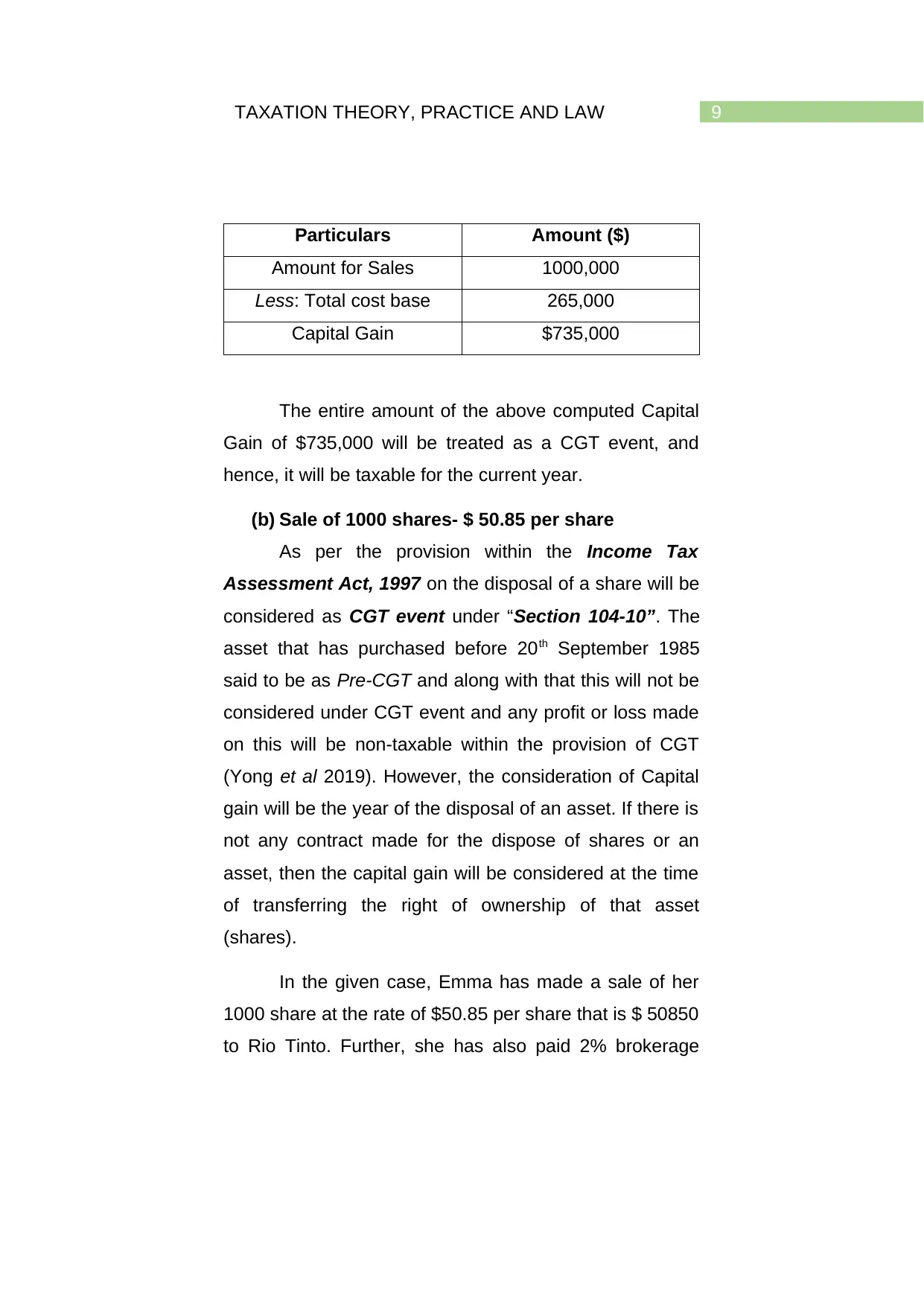

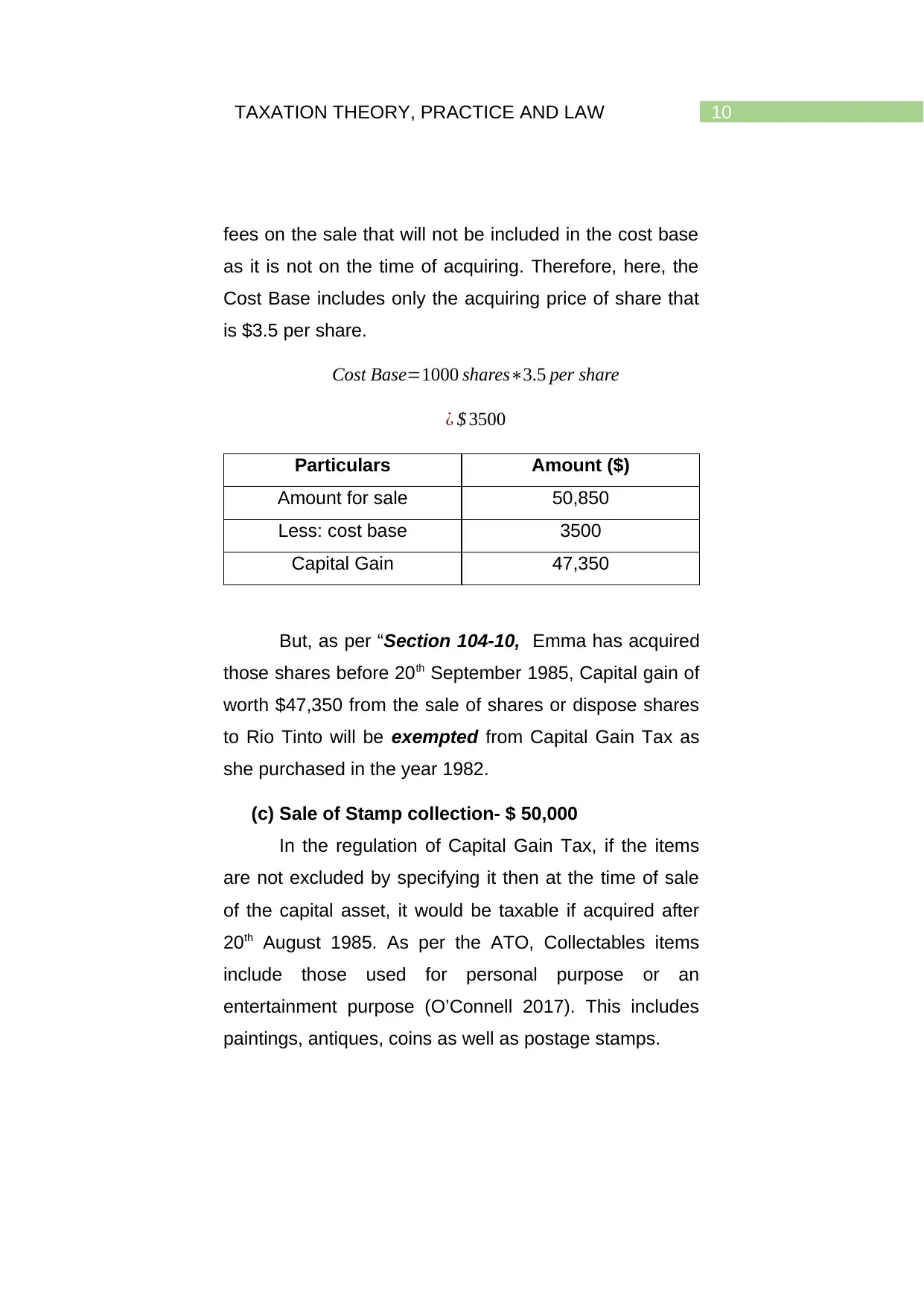

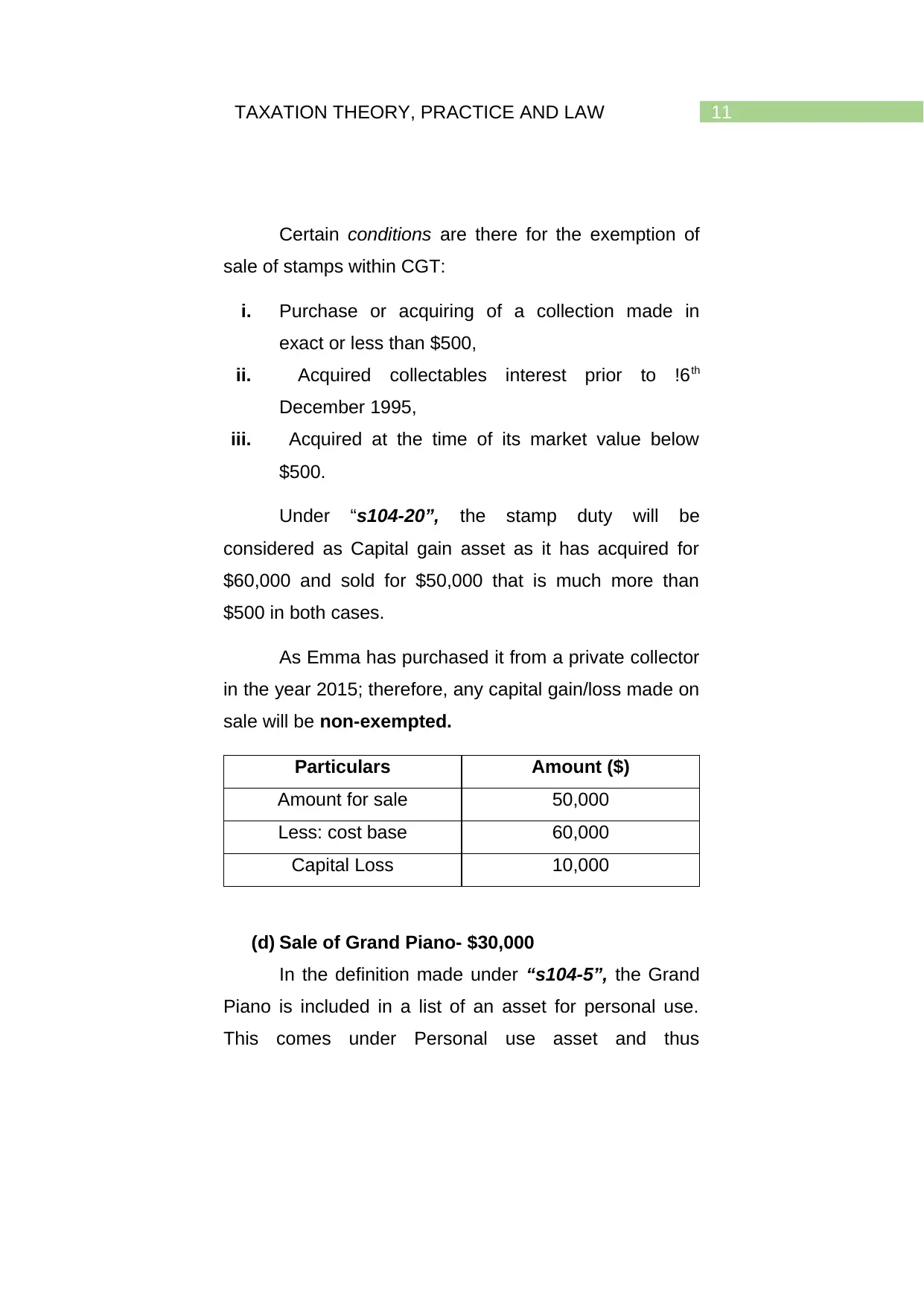

This assignment solution for HI6028 Taxation Theory, Practice & Law analyzes two key areas of Australian taxation: Goods and Services Tax (GST) and Capital Gains Tax (CGT). The solution begins with an examination of GST, specifically its application to property transactions, including the purchase of vacant land and the legal services provided to a development company, and whether the company is eligible for input tax credit. The second part of the assignment focuses on Capital Gains Tax (CGT), assessing the tax implications of various asset sales, including a block of land, shares, and a stamp collection. The analysis considers relevant legislation, cost base calculations, and exemptions, providing a comprehensive understanding of CGT principles. The assignment demonstrates an understanding of the Australian income tax system, identifies and analyzes taxation issues, interprets relevant legislation, and applies taxation principles to real-life problems. The document includes a detailed breakdown of each scenario, relevant calculations, and citations from the Australian Taxation Office (ATO).

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.