Finance Taxation Assignment: Capital Gains, Loans, and Property

VerifiedAdded on 2019/11/12

|9

|2594

|161

Homework Assignment

AI Summary

This assignment provides comprehensive solutions to various taxation problems. The first solution addresses capital gains tax, determining its applicability based on asset holding periods and personal utilization. The second solution focuses on concessional loans, calculating the tax implications of fringe benefits arising from below-market interest rates. The third solution examines property rental, outlining the tax treatment of profits, losses, and the division of responsibilities between partners. The fourth solution delves into tax minimization strategies, referencing legal precedents and the right of individuals to manage their accounts to reduce tax burdens, provided it is within the legal framework. Finally, the fifth solution analyzes the tax implications of a timber sale, differentiating between revenue and capital receipts based on the nature of the transaction.

TAXATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation

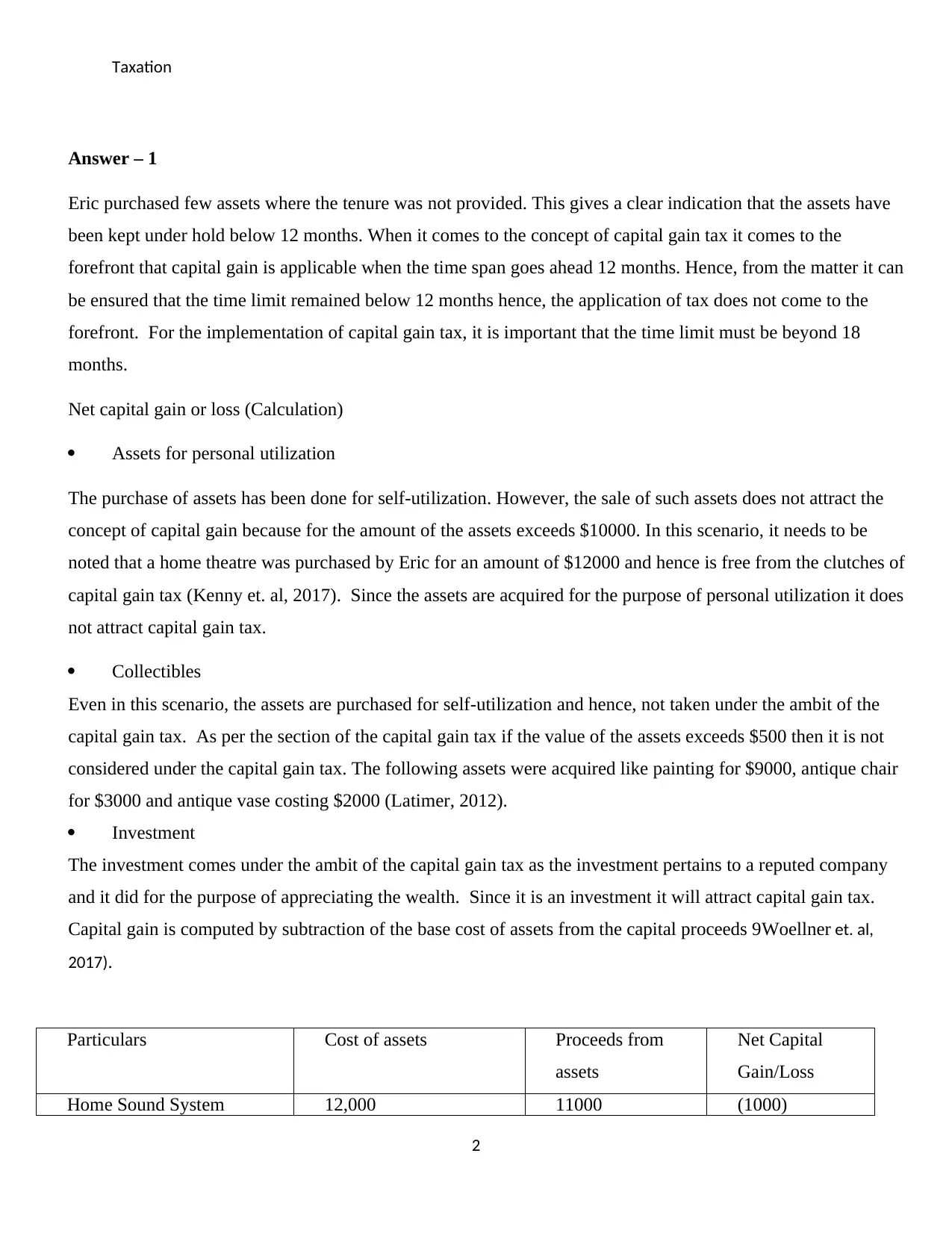

Answer – 1

Eric purchased few assets where the tenure was not provided. This gives a clear indication that the assets have

been kept under hold below 12 months. When it comes to the concept of capital gain tax it comes to the

forefront that capital gain is applicable when the time span goes ahead 12 months. Hence, from the matter it can

be ensured that the time limit remained below 12 months hence, the application of tax does not come to the

forefront. For the implementation of capital gain tax, it is important that the time limit must be beyond 18

months.

Net capital gain or loss (Calculation)

Assets for personal utilization

The purchase of assets has been done for self-utilization. However, the sale of such assets does not attract the

concept of capital gain because for the amount of the assets exceeds $10000. In this scenario, it needs to be

noted that a home theatre was purchased by Eric for an amount of $12000 and hence is free from the clutches of

capital gain tax (Kenny et. al, 2017). Since the assets are acquired for the purpose of personal utilization it does

not attract capital gain tax.

Collectibles

Even in this scenario, the assets are purchased for self-utilization and hence, not taken under the ambit of the

capital gain tax. As per the section of the capital gain tax if the value of the assets exceeds $500 then it is not

considered under the capital gain tax. The following assets were acquired like painting for $9000, antique chair

for $3000 and antique vase costing $2000 (Latimer, 2012).

Investment

The investment comes under the ambit of the capital gain tax as the investment pertains to a reputed company

and it did for the purpose of appreciating the wealth. Since it is an investment it will attract capital gain tax.

Capital gain is computed by subtraction of the base cost of assets from the capital proceeds 9Woellner et. al,

2017).

Particulars Cost of assets Proceeds from

assets

Net Capital

Gain/Loss

Home Sound System 12,000 11000 (1000)

2

Answer – 1

Eric purchased few assets where the tenure was not provided. This gives a clear indication that the assets have

been kept under hold below 12 months. When it comes to the concept of capital gain tax it comes to the

forefront that capital gain is applicable when the time span goes ahead 12 months. Hence, from the matter it can

be ensured that the time limit remained below 12 months hence, the application of tax does not come to the

forefront. For the implementation of capital gain tax, it is important that the time limit must be beyond 18

months.

Net capital gain or loss (Calculation)

Assets for personal utilization

The purchase of assets has been done for self-utilization. However, the sale of such assets does not attract the

concept of capital gain because for the amount of the assets exceeds $10000. In this scenario, it needs to be

noted that a home theatre was purchased by Eric for an amount of $12000 and hence is free from the clutches of

capital gain tax (Kenny et. al, 2017). Since the assets are acquired for the purpose of personal utilization it does

not attract capital gain tax.

Collectibles

Even in this scenario, the assets are purchased for self-utilization and hence, not taken under the ambit of the

capital gain tax. As per the section of the capital gain tax if the value of the assets exceeds $500 then it is not

considered under the capital gain tax. The following assets were acquired like painting for $9000, antique chair

for $3000 and antique vase costing $2000 (Latimer, 2012).

Investment

The investment comes under the ambit of the capital gain tax as the investment pertains to a reputed company

and it did for the purpose of appreciating the wealth. Since it is an investment it will attract capital gain tax.

Capital gain is computed by subtraction of the base cost of assets from the capital proceeds 9Woellner et. al,

2017).

Particulars Cost of assets Proceeds from

assets

Net Capital

Gain/Loss

Home Sound System 12,000 11000 (1000)

2

Taxation

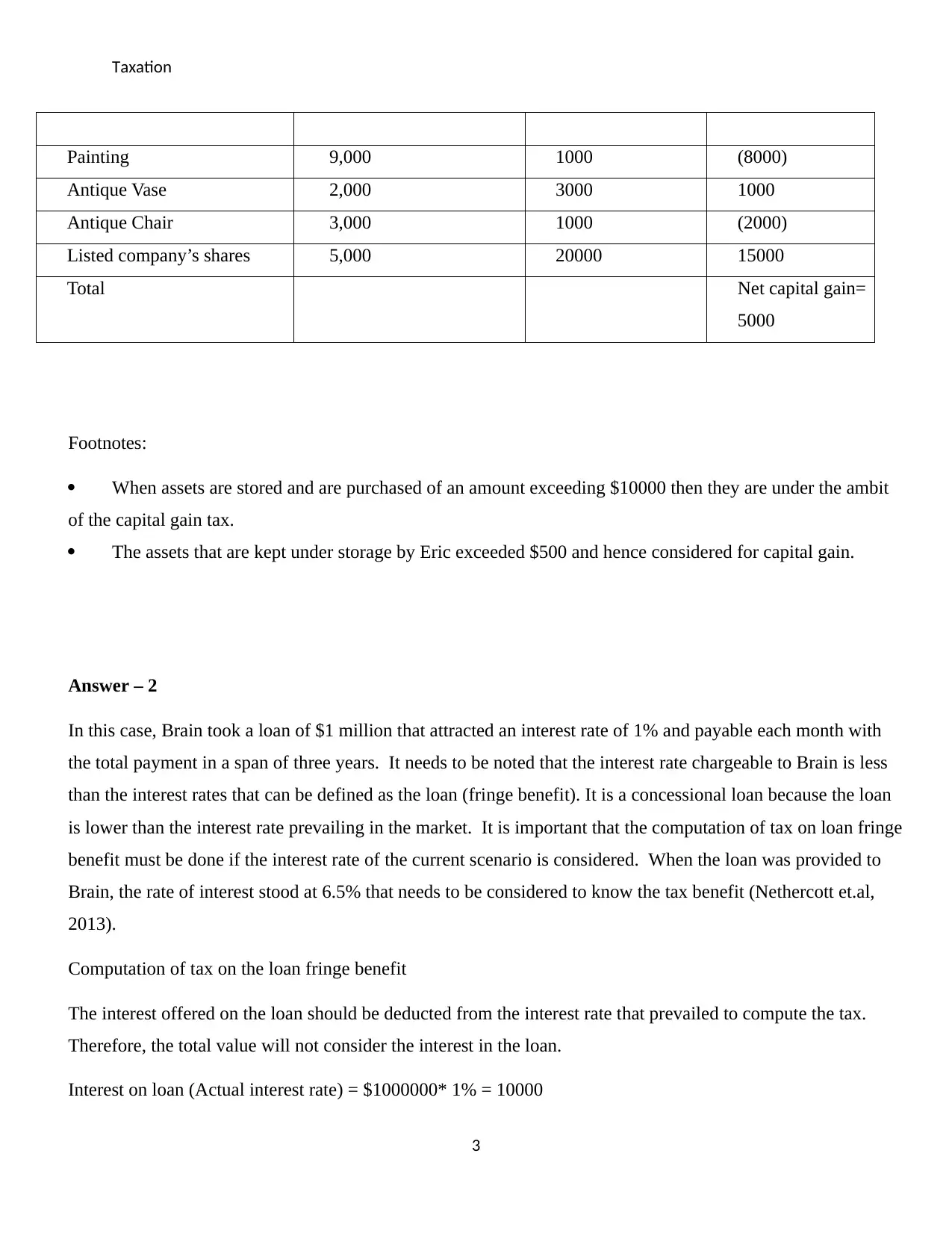

Painting 9,000 1000 (8000)

Antique Vase 2,000 3000 1000

Antique Chair 3,000 1000 (2000)

Listed company’s shares 5,000 20000 15000

Total Net capital gain=

5000

Footnotes:

When assets are stored and are purchased of an amount exceeding $10000 then they are under the ambit

of the capital gain tax.

The assets that are kept under storage by Eric exceeded $500 and hence considered for capital gain.

Answer – 2

In this case, Brain took a loan of $1 million that attracted an interest rate of 1% and payable each month with

the total payment in a span of three years. It needs to be noted that the interest rate chargeable to Brain is less

than the interest rates that can be defined as the loan (fringe benefit). It is a concessional loan because the loan

is lower than the interest rate prevailing in the market. It is important that the computation of tax on loan fringe

benefit must be done if the interest rate of the current scenario is considered. When the loan was provided to

Brain, the rate of interest stood at 6.5% that needs to be considered to know the tax benefit (Nethercott et.al,

2013).

Computation of tax on the loan fringe benefit

The interest offered on the loan should be deducted from the interest rate that prevailed to compute the tax.

Therefore, the total value will not consider the interest in the loan.

Interest on loan (Actual interest rate) = $1000000* 1% = 10000

3

Painting 9,000 1000 (8000)

Antique Vase 2,000 3000 1000

Antique Chair 3,000 1000 (2000)

Listed company’s shares 5,000 20000 15000

Total Net capital gain=

5000

Footnotes:

When assets are stored and are purchased of an amount exceeding $10000 then they are under the ambit

of the capital gain tax.

The assets that are kept under storage by Eric exceeded $500 and hence considered for capital gain.

Answer – 2

In this case, Brain took a loan of $1 million that attracted an interest rate of 1% and payable each month with

the total payment in a span of three years. It needs to be noted that the interest rate chargeable to Brain is less

than the interest rates that can be defined as the loan (fringe benefit). It is a concessional loan because the loan

is lower than the interest rate prevailing in the market. It is important that the computation of tax on loan fringe

benefit must be done if the interest rate of the current scenario is considered. When the loan was provided to

Brain, the rate of interest stood at 6.5% that needs to be considered to know the tax benefit (Nethercott et.al,

2013).

Computation of tax on the loan fringe benefit

The interest offered on the loan should be deducted from the interest rate that prevailed to compute the tax.

Therefore, the total value will not consider the interest in the loan.

Interest on loan (Actual interest rate) = $1000000* 1% = 10000

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation

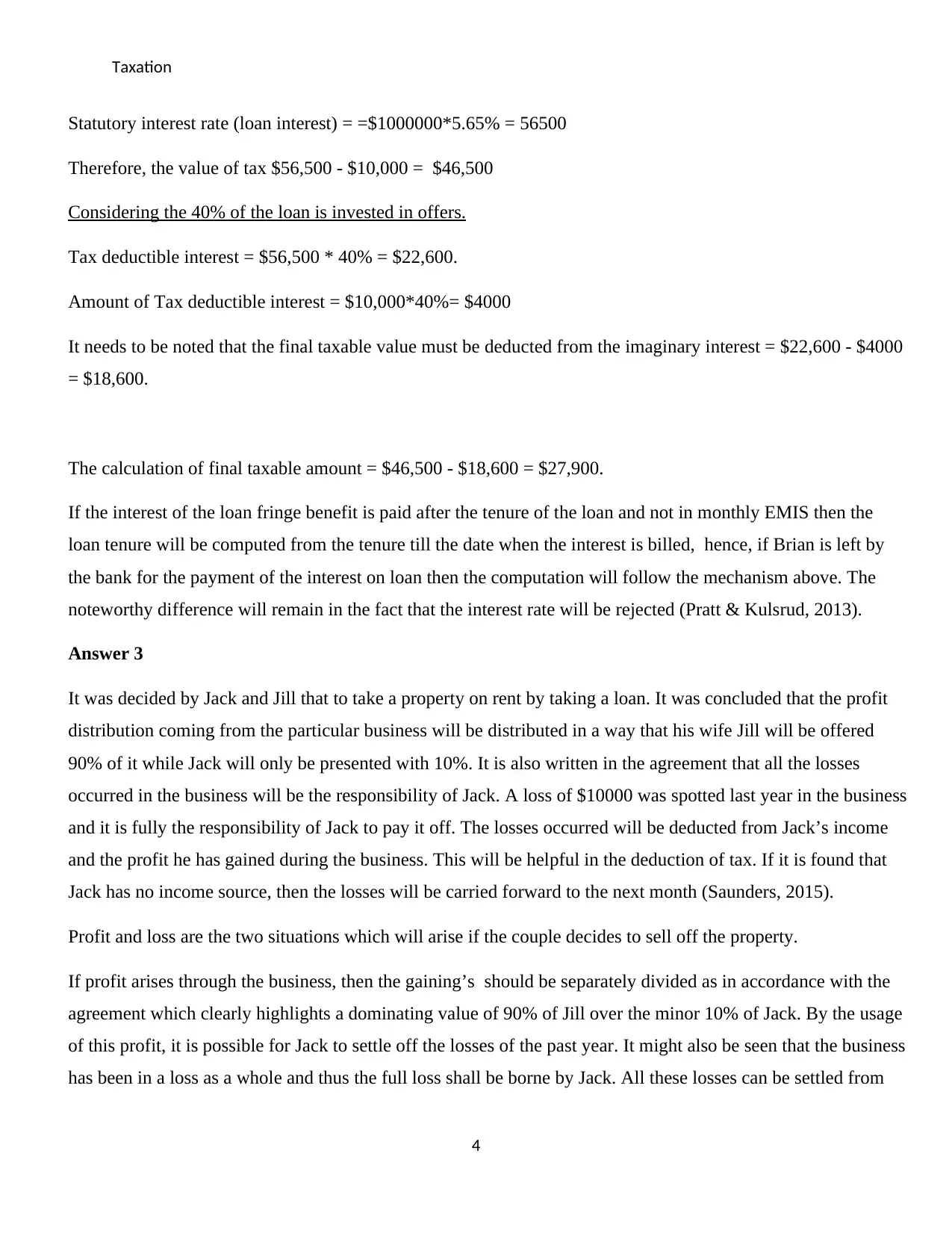

Statutory interest rate (loan interest) = =$1000000*5.65% = 56500

Therefore, the value of tax $56,500 - $10,000 = $46,500

Considering the 40% of the loan is invested in offers.

Tax deductible interest = $56,500 * 40% = $22,600.

Amount of Tax deductible interest = $10,000*40%= $4000

It needs to be noted that the final taxable value must be deducted from the imaginary interest = $22,600 - $4000

= $18,600.

The calculation of final taxable amount = $46,500 - $18,600 = $27,900.

If the interest of the loan fringe benefit is paid after the tenure of the loan and not in monthly EMIS then the

loan tenure will be computed from the tenure till the date when the interest is billed, hence, if Brian is left by

the bank for the payment of the interest on loan then the computation will follow the mechanism above. The

noteworthy difference will remain in the fact that the interest rate will be rejected (Pratt & Kulsrud, 2013).

Answer 3

It was decided by Jack and Jill that to take a property on rent by taking a loan. It was concluded that the profit

distribution coming from the particular business will be distributed in a way that his wife Jill will be offered

90% of it while Jack will only be presented with 10%. It is also written in the agreement that all the losses

occurred in the business will be the responsibility of Jack. A loss of $10000 was spotted last year in the business

and it is fully the responsibility of Jack to pay it off. The losses occurred will be deducted from Jack’s income

and the profit he has gained during the business. This will be helpful in the deduction of tax. If it is found that

Jack has no income source, then the losses will be carried forward to the next month (Saunders, 2015).

Profit and loss are the two situations which will arise if the couple decides to sell off the property.

If profit arises through the business, then the gaining’s should be separately divided as in accordance with the

agreement which clearly highlights a dominating value of 90% of Jill over the minor 10% of Jack. By the usage

of this profit, it is possible for Jack to settle off the losses of the past year. It might also be seen that the business

has been in a loss as a whole and thus the full loss shall be borne by Jack. All these losses can be settled from

4

Statutory interest rate (loan interest) = =$1000000*5.65% = 56500

Therefore, the value of tax $56,500 - $10,000 = $46,500

Considering the 40% of the loan is invested in offers.

Tax deductible interest = $56,500 * 40% = $22,600.

Amount of Tax deductible interest = $10,000*40%= $4000

It needs to be noted that the final taxable value must be deducted from the imaginary interest = $22,600 - $4000

= $18,600.

The calculation of final taxable amount = $46,500 - $18,600 = $27,900.

If the interest of the loan fringe benefit is paid after the tenure of the loan and not in monthly EMIS then the

loan tenure will be computed from the tenure till the date when the interest is billed, hence, if Brian is left by

the bank for the payment of the interest on loan then the computation will follow the mechanism above. The

noteworthy difference will remain in the fact that the interest rate will be rejected (Pratt & Kulsrud, 2013).

Answer 3

It was decided by Jack and Jill that to take a property on rent by taking a loan. It was concluded that the profit

distribution coming from the particular business will be distributed in a way that his wife Jill will be offered

90% of it while Jack will only be presented with 10%. It is also written in the agreement that all the losses

occurred in the business will be the responsibility of Jack. A loss of $10000 was spotted last year in the business

and it is fully the responsibility of Jack to pay it off. The losses occurred will be deducted from Jack’s income

and the profit he has gained during the business. This will be helpful in the deduction of tax. If it is found that

Jack has no income source, then the losses will be carried forward to the next month (Saunders, 2015).

Profit and loss are the two situations which will arise if the couple decides to sell off the property.

If profit arises through the business, then the gaining’s should be separately divided as in accordance with the

agreement which clearly highlights a dominating value of 90% of Jill over the minor 10% of Jack. By the usage

of this profit, it is possible for Jack to settle off the losses of the past year. It might also be seen that the business

has been in a loss as a whole and thus the full loss shall be borne by Jack. All these losses can be settled from

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation

Jack’s income and if he’s not having ones then the losses can be carried forward to the next year to be deducted

from some supplementary sources.

All this explains that Jack can have a possibility to settle all the losses of the past year by the gain arisen from

selling the property. But if the above statement fails and profit changes to loss then Jack will have to bear the

full loss aroused. Jill has no relation to the payment of losses of the company. All this states that Jill cannot be

affected by the tax valid on the loss while it will surely affect Jack as he has to record the same in his book of

accounts.

Answer-4

All entities or individual possess a fundamental and legal right to manage his business account in a manner to

an extent to minimize the tax on their total income. Tax Authorities in the state revenue department is not

necessarily obliged to increase the tax payable by the assessee even if he finds some provisioning so long as it

has been done within the framework of legal provisions. The proposition was well-established in the judgment

of case IRC v Duke of Westminster (1936) AC 1. The proposition will be applied so long as the taxpayer or an

entity manage his books of accounts in accordance with the rules and regulations laid down in the income tax

rules and can be established in the court of law (Kobestky, 2005). The principle set up by the rivalry between

IRC and Duke of Westminster [1936] AC 1 was as follows:

It is the right of every person to intelligently decrease the tax amount payable in such a way that it is minimum

in value and this all can be done by deliberately altering the accounting data and the investments carried out.

Till date the procedures carried out by the person is legal, the procedures are valid and no question can be asked

in accordance with the steps followed not by the Commissioners of Inland Revenue also. But a major uphold of

this right is that the steps followed by a person should be legally aligned with the laws and rules put up in

accordance with the income tax rules made by the higher courts (Hopewell, 2012).

So long as the books of accounts are compiled and the documents in relation to detail entries in the books are

furnished by the taxpayer are genuine in nature, then the judiciary shall not consider every document based on

concealed evidence on the following propositions:

5

Jack’s income and if he’s not having ones then the losses can be carried forward to the next year to be deducted

from some supplementary sources.

All this explains that Jack can have a possibility to settle all the losses of the past year by the gain arisen from

selling the property. But if the above statement fails and profit changes to loss then Jack will have to bear the

full loss aroused. Jill has no relation to the payment of losses of the company. All this states that Jill cannot be

affected by the tax valid on the loss while it will surely affect Jack as he has to record the same in his book of

accounts.

Answer-4

All entities or individual possess a fundamental and legal right to manage his business account in a manner to

an extent to minimize the tax on their total income. Tax Authorities in the state revenue department is not

necessarily obliged to increase the tax payable by the assessee even if he finds some provisioning so long as it

has been done within the framework of legal provisions. The proposition was well-established in the judgment

of case IRC v Duke of Westminster (1936) AC 1. The proposition will be applied so long as the taxpayer or an

entity manage his books of accounts in accordance with the rules and regulations laid down in the income tax

rules and can be established in the court of law (Kobestky, 2005). The principle set up by the rivalry between

IRC and Duke of Westminster [1936] AC 1 was as follows:

It is the right of every person to intelligently decrease the tax amount payable in such a way that it is minimum

in value and this all can be done by deliberately altering the accounting data and the investments carried out.

Till date the procedures carried out by the person is legal, the procedures are valid and no question can be asked

in accordance with the steps followed not by the Commissioners of Inland Revenue also. But a major uphold of

this right is that the steps followed by a person should be legally aligned with the laws and rules put up in

accordance with the income tax rules made by the higher courts (Hopewell, 2012).

So long as the books of accounts are compiled and the documents in relation to detail entries in the books are

furnished by the taxpayer are genuine in nature, then the judiciary shall not consider every document based on

concealed evidence on the following propositions:

5

Taxation

a. All the entities or the individual possess the right to keep his books of accounts, in

accordance with the law, to maintain in such a manner to reduce the burden of the tax

payable to the government (Kenny, 2016).

b. When the authorities found no mistakes in the books of accounts and there is no deviation

in keeping the records in an authentic manner, then no additional tax liability will be

imposed (Kenny, 2016).

c. So long as the transactions are within the framework of law and established in the system

no one can challenge that the significance of the transaction contrasts with as described

by the taxpayer in his submission (Fullerton et. al, 2017)

Although this regulation was not altered over the years new laws had come into existence, the

significance of the said law has lost its merit in current juncture, as because the approach of

scrutinizing the boos of accounts are been differentiated.

Still, the regulation has some importance in the current scenario. Any transaction in the books of

accounts which is in the interest in helping in running the business smoothly in accordance with the

law without avoiding any taxes than it is precisely impeccable in doing so. The rule holds merit so long

as it restricts the entities from manipulating the figures and allows the entities or individual to carry out

the business within the framework of law (Fullerton et. al, 2017). Take the example, when a business

entity is suffering from huge losses and is unable to pay off its debt, it can take steps to write off its

fixed assets at the current value in the balance sheet, even if the entity does not hold any authentic

document to prove the transaction. But in case of the entity involved in manipulation and suppress vital

information’s from the stakeholders, then the law will take its own course and bar the entity from

manipulating with the facts (Sadiq et. al, 2017).

Answer-5

Bill in his possession owns a big parcel of land having lots of long pine trees, he wants to utilize the

land for sheep farming, so he must remove the whole lot of pine trees from the land. For every 100

meters of timber from the trees, he shall receive $1000 from a timber company. Here the question

arises that whether any tax on receipt arises in the deal as the quantum of the amount in the deal is not

ascertained in the selling of the timber. Therefore, the money received can be considered as revenue

receipt derived from the sale of timber by Bill from Timber Company. Accordingly, by treating the

6

a. All the entities or the individual possess the right to keep his books of accounts, in

accordance with the law, to maintain in such a manner to reduce the burden of the tax

payable to the government (Kenny, 2016).

b. When the authorities found no mistakes in the books of accounts and there is no deviation

in keeping the records in an authentic manner, then no additional tax liability will be

imposed (Kenny, 2016).

c. So long as the transactions are within the framework of law and established in the system

no one can challenge that the significance of the transaction contrasts with as described

by the taxpayer in his submission (Fullerton et. al, 2017)

Although this regulation was not altered over the years new laws had come into existence, the

significance of the said law has lost its merit in current juncture, as because the approach of

scrutinizing the boos of accounts are been differentiated.

Still, the regulation has some importance in the current scenario. Any transaction in the books of

accounts which is in the interest in helping in running the business smoothly in accordance with the

law without avoiding any taxes than it is precisely impeccable in doing so. The rule holds merit so long

as it restricts the entities from manipulating the figures and allows the entities or individual to carry out

the business within the framework of law (Fullerton et. al, 2017). Take the example, when a business

entity is suffering from huge losses and is unable to pay off its debt, it can take steps to write off its

fixed assets at the current value in the balance sheet, even if the entity does not hold any authentic

document to prove the transaction. But in case of the entity involved in manipulation and suppress vital

information’s from the stakeholders, then the law will take its own course and bar the entity from

manipulating with the facts (Sadiq et. al, 2017).

Answer-5

Bill in his possession owns a big parcel of land having lots of long pine trees, he wants to utilize the

land for sheep farming, so he must remove the whole lot of pine trees from the land. For every 100

meters of timber from the trees, he shall receive $1000 from a timber company. Here the question

arises that whether any tax on receipt arises in the deal as the quantum of the amount in the deal is not

ascertained in the selling of the timber. Therefore, the money received can be considered as revenue

receipt derived from the sale of timber by Bill from Timber Company. Accordingly, by treating the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation

amount as revenue receipt in the accounts by Bill, there shall be no capital gain tax is applicable in this

transaction (Woellner et. al, 2017).

In another scenario, when Bill agrees to sell its rights to a timber company to cut the trees and remove

the timber from the land for a lump sum amount of $ 50000, then this transaction shall be treated as

capital receipt because firstly he had agreed to sell his right to cut the trees from his land and secondly

the deal is on a fixed onetime payment from the company. Therefore, it shall be considered as capital

receipt and accordingly liable to pay capital gain taxes (Woellner et. al, 2017).

In conclusion, in both the scenario, Bill shall get the money. Firstly, by selling his trees in trenches,

where he gets small but regular payment which comes under revenue receipt attracts a normal rate of

taxes. Whereas, in the second case he agrees to give to give away his rights for a fixed amount of

$50000, which may be treated as the selling of an asset leading to attract capital gain tax.

7

amount as revenue receipt in the accounts by Bill, there shall be no capital gain tax is applicable in this

transaction (Woellner et. al, 2017).

In another scenario, when Bill agrees to sell its rights to a timber company to cut the trees and remove

the timber from the land for a lump sum amount of $ 50000, then this transaction shall be treated as

capital receipt because firstly he had agreed to sell his right to cut the trees from his land and secondly

the deal is on a fixed onetime payment from the company. Therefore, it shall be considered as capital

receipt and accordingly liable to pay capital gain taxes (Woellner et. al, 2017).

In conclusion, in both the scenario, Bill shall get the money. Firstly, by selling his trees in trenches,

where he gets small but regular payment which comes under revenue receipt attracts a normal rate of

taxes. Whereas, in the second case he agrees to give to give away his rights for a fixed amount of

$50000, which may be treated as the selling of an asset leading to attract capital gain tax.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation

References

Fullerton, I.G, Deutsch, R, Friezer, M.L, Hanley,P & Snape, T 2017, The Australian Tax Handbook

Tax Return Edition 2017, Thomson Reuters: Australia

Kenny, B. V 2016, Australian Tax 2016, Thomson Reuters (Professional) Australia Limited

Kenny, P, Blissenden, M, & Villios, S 2017, Australian Tax 2017, Thomson Reuters: Australia

Kobestky, M 2005, Income Tax: Text, Materials and Essential Cases, Sydney: The Federation Press

Latimer, P 2012, Australian Business Law 2012, 31st ed, Sydney, NSW: CCH Australia Limited.

Hopewell, L 2012, Australia tax inquiry opens submissions, viewed 17 September 2017,

www.zdnet.com.au.

Nethercott, L, Richardson, G & Devos,K. 2013, Australian Taxation Study Manual, Sydney.

Pratt, J. W & Kulsrud, W N 2013, Federal Taxation, Oxford university press.

Sadiq, K, Coleman, C , Hanegbi, R, Jogarajan,S, Krever, R, Obst, R, Teoh, J & Ting, A 2017,

Principles of Taxation Law 2017, Law book Australia

Saunders, C 2015, The Australian Constitution, Carlton: Constitutional Centenary Foundation

Woellner, R, Barkoczy, S, Murphy, S, Evans, C & Pinto, D 2017, Australian taxation law 2017,

Oxford University Press Australia

8

References

Fullerton, I.G, Deutsch, R, Friezer, M.L, Hanley,P & Snape, T 2017, The Australian Tax Handbook

Tax Return Edition 2017, Thomson Reuters: Australia

Kenny, B. V 2016, Australian Tax 2016, Thomson Reuters (Professional) Australia Limited

Kenny, P, Blissenden, M, & Villios, S 2017, Australian Tax 2017, Thomson Reuters: Australia

Kobestky, M 2005, Income Tax: Text, Materials and Essential Cases, Sydney: The Federation Press

Latimer, P 2012, Australian Business Law 2012, 31st ed, Sydney, NSW: CCH Australia Limited.

Hopewell, L 2012, Australia tax inquiry opens submissions, viewed 17 September 2017,

www.zdnet.com.au.

Nethercott, L, Richardson, G & Devos,K. 2013, Australian Taxation Study Manual, Sydney.

Pratt, J. W & Kulsrud, W N 2013, Federal Taxation, Oxford university press.

Sadiq, K, Coleman, C , Hanegbi, R, Jogarajan,S, Krever, R, Obst, R, Teoh, J & Ting, A 2017,

Principles of Taxation Law 2017, Law book Australia

Saunders, C 2015, The Australian Constitution, Carlton: Constitutional Centenary Foundation

Woellner, R, Barkoczy, S, Murphy, S, Evans, C & Pinto, D 2017, Australian taxation law 2017,

Oxford University Press Australia

8

Taxation

9

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.