A Comprehensive Report on the UK Taxation Environment and Obligations

VerifiedAdded on 2020/06/05

|16

|4378

|42

Report

AI Summary

This report provides a comprehensive overview of the UK taxation system. It begins with an introduction to the tax environment in the UK, discussing the roles of central and local governments, and outlining the main types of taxes, including income tax, corporation tax, and capital gains tax. The report then delves into the duties of tax practitioners, emphasizing their role in understanding and applying tax regulations. It also covers tax obligations, including compliance and non-compliance penalties. The report includes examples of income, expenses, and allowance calculations, taxable amounts for self-employment, and details on documentation and tax returns. Finally, it examines chargeable profits, tax liability, income tax deductions, chargeable assets, capital gains and losses, and the calculation of capital gains tax payable, providing a detailed analysis of the UK's tax framework.

TAXATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Tax environment UK........................................................................................................1

1.2 Duties of tax practitioner..................................................................................................3

1.3 Tax obligations.................................................................................................................4

TASK 2............................................................................................................................................6

2.1 Income, expenses and allowances calculations................................................................6

2.2 Taxable amount and the self- employment income..........................................................7

2.3 Documentation and tax returns.........................................................................................8

TASK 3............................................................................................................................................9

3.1 Chargeable profit..............................................................................................................9

3.2 Tax liability....................................................................................................................10

3.3 Income tax deductions....................................................................................................11

4.1 Chargeable assets............................................................................................................11

4.2 Capital gains and losses..................................................................................................11

4.3 Capital gain tax payable.................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Tax environment UK........................................................................................................1

1.2 Duties of tax practitioner..................................................................................................3

1.3 Tax obligations.................................................................................................................4

TASK 2............................................................................................................................................6

2.1 Income, expenses and allowances calculations................................................................6

2.2 Taxable amount and the self- employment income..........................................................7

2.3 Documentation and tax returns.........................................................................................8

TASK 3............................................................................................................................................9

3.1 Chargeable profit..............................................................................................................9

3.2 Tax liability....................................................................................................................10

3.3 Income tax deductions....................................................................................................11

4.1 Chargeable assets............................................................................................................11

4.2 Capital gains and losses..................................................................................................11

4.3 Capital gain tax payable.................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Nations developed the certain policies and strategies to make the powerful economy in

competitive world. There can be various technique such as imposing taxes over income and

products or services. These can be good sources for generating funds or reserves for government,

and they utilise these funds in overcoming the monetary crisis over the country and also in the

development of economy. Educational sector, health and care sector and many essential sectors

of society can be benefited with this and thus they can have the favourable development. Every

nation tends to be developed, the history UK describes that it is a developed country there are

implication of various laws, taxes over citizens. There can be various rule and responsibilities of

tax practitioners, tax payers or agents. They have to make sure about proper payments of taxes

and proper information must be provided to legislatives like HMRC.

TASK 1

1.1 Tax environment UK

Developed and economically strong nation has the various taxation policies, which can

be helpful in maintain economic standard for them. UK is a best example of implicating taxation

policies in nation. There are 2 stages of government in which the taxation is ruling out:

Central Government: The central power UK is headed by Prime Minister and the

Crown (Her Majesty), government generate revenue from the sources which mainly includes

Income Tax, VAT, Corporation Tax, National Insurance and Duties over Fuel importing. The

main source of revenue is income tax levied on citizens (Ehrlich and Radulescu, 2017). Taxes

can be deducted directly from their salary accounts on whichso that they will not have to make

additional payments to government it can be beneficial in getting taxes on prompt process

without any fraudulent act occurred in taxation (Meier and et. al., 2016). The central government

makes several expenses in developing infrastructural facilities as well as economic development.

Local Government: The revenue generated by local government can be with the help of

central government, rates of business taxation at London and Wales, local fees and charges from

imposing penalties over non-parking zones and street parking like people park their vehicle

outside their house or on roads. And the council tax. These can be their sources of gaining

favourable amount of taxes (Basak, 2016). The local government at UK is powerful force with

1

Nations developed the certain policies and strategies to make the powerful economy in

competitive world. There can be various technique such as imposing taxes over income and

products or services. These can be good sources for generating funds or reserves for government,

and they utilise these funds in overcoming the monetary crisis over the country and also in the

development of economy. Educational sector, health and care sector and many essential sectors

of society can be benefited with this and thus they can have the favourable development. Every

nation tends to be developed, the history UK describes that it is a developed country there are

implication of various laws, taxes over citizens. There can be various rule and responsibilities of

tax practitioners, tax payers or agents. They have to make sure about proper payments of taxes

and proper information must be provided to legislatives like HMRC.

TASK 1

1.1 Tax environment UK

Developed and economically strong nation has the various taxation policies, which can

be helpful in maintain economic standard for them. UK is a best example of implicating taxation

policies in nation. There are 2 stages of government in which the taxation is ruling out:

Central Government: The central power UK is headed by Prime Minister and the

Crown (Her Majesty), government generate revenue from the sources which mainly includes

Income Tax, VAT, Corporation Tax, National Insurance and Duties over Fuel importing. The

main source of revenue is income tax levied on citizens (Ehrlich and Radulescu, 2017). Taxes

can be deducted directly from their salary accounts on whichso that they will not have to make

additional payments to government it can be beneficial in getting taxes on prompt process

without any fraudulent act occurred in taxation (Meier and et. al., 2016). The central government

makes several expenses in developing infrastructural facilities as well as economic development.

Local Government: The revenue generated by local government can be with the help of

central government, rates of business taxation at London and Wales, local fees and charges from

imposing penalties over non-parking zones and street parking like people park their vehicle

outside their house or on roads. And the council tax. These can be their sources of gaining

favourable amount of taxes (Basak, 2016). The local government at UK is powerful force with

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

help of them crime rate is lower down or reduced and there can be various developments in

locality of such rural and under- developed areas.

Tax legislation:

These two governmental bodies are involved in taxation of UK, the act of parliament has

made the laws and regulations over the statutory instruments of taxations. There can be three

kinds of main taxes which are levied by the central government these can be as follows:

Income tax: Tax can be levied over the income earned by an individual from the

sources like dividends, employment, self-governed business, rental income,

pension income and etc. these can be followed by various taxes relating to income

tax are ITEPA 2003, IITOIA 2005, CAA 2001 and ITA 2007 (TAX 1 Tiens,

2017).

Corporation tax: These taxes can be levied over the taxable profits or gains

earned by the private or limited organisations. There are fixed ratios over which

companies has to made tax payments, taxes can be levied by the following acts

CTA 2009, ICTA 1988 and the CAA 2001 (TAX 1 Tiens, 2017).

Capital gain tax: These Taxes are charged over the gains and profit earned by

selling or dispossessing an asset it can be the personal property of an individual,

shares and bonds. There may be allowable deduction as per conditions, these can

be followed by the various laws in TCGA 1992 (TAX 1 Tiens, 2017).

Improvements in Taxation system: UK government has implemented various changes into the

taxation process of the country. The earning and generation of governmental funds can mainly

through gains they have through taxes. Imposing taxes over individual as per their earning, it can

only be possible through making convenient process of paying taxes and imposing rates over

their income. HMRC has facilitated online payment of taxes with developing the PAYE scheme,

where a person can easily make payments online and it is a good or prompt way without any

influence of tax agents or any individual (Haffner and Winters, 2016). There can be several

changes made to the HMRC website that, the small business entity who pay salary to their

employees can be taxed free in making payments to their worker. They have to provide

necessary information to the HMRC regarding the details of employees and their pay-offs. There

must be follow of fair taxation policies which can be beneficial and fruitful for all sectors in

society like individuals, corporations, small business entity and also government.

2

locality of such rural and under- developed areas.

Tax legislation:

These two governmental bodies are involved in taxation of UK, the act of parliament has

made the laws and regulations over the statutory instruments of taxations. There can be three

kinds of main taxes which are levied by the central government these can be as follows:

Income tax: Tax can be levied over the income earned by an individual from the

sources like dividends, employment, self-governed business, rental income,

pension income and etc. these can be followed by various taxes relating to income

tax are ITEPA 2003, IITOIA 2005, CAA 2001 and ITA 2007 (TAX 1 Tiens,

2017).

Corporation tax: These taxes can be levied over the taxable profits or gains

earned by the private or limited organisations. There are fixed ratios over which

companies has to made tax payments, taxes can be levied by the following acts

CTA 2009, ICTA 1988 and the CAA 2001 (TAX 1 Tiens, 2017).

Capital gain tax: These Taxes are charged over the gains and profit earned by

selling or dispossessing an asset it can be the personal property of an individual,

shares and bonds. There may be allowable deduction as per conditions, these can

be followed by the various laws in TCGA 1992 (TAX 1 Tiens, 2017).

Improvements in Taxation system: UK government has implemented various changes into the

taxation process of the country. The earning and generation of governmental funds can mainly

through gains they have through taxes. Imposing taxes over individual as per their earning, it can

only be possible through making convenient process of paying taxes and imposing rates over

their income. HMRC has facilitated online payment of taxes with developing the PAYE scheme,

where a person can easily make payments online and it is a good or prompt way without any

influence of tax agents or any individual (Haffner and Winters, 2016). There can be several

changes made to the HMRC website that, the small business entity who pay salary to their

employees can be taxed free in making payments to their worker. They have to provide

necessary information to the HMRC regarding the details of employees and their pay-offs. There

must be follow of fair taxation policies which can be beneficial and fruitful for all sectors in

society like individuals, corporations, small business entity and also government.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.2 Duties of tax practitioner

Tax practitioners can be helpful for an organisation in helping with the various rules and

regulations imposed by UK government. Frequently changing taxation policies in UK market

over the transactions like import and export of the goods and services, manufacturing of the

various products, marketing of the item and etc. These can be understood and implied by the tax

practitioners in a business firm, to make them informed about the new policies to be followed

(Khan and Altaf, 2014). In a firm, there can be various transactions such as buying good quality

raw material at adequate prices, there can be taxation over importing raw material, but if

products are bought from domestic market than transportation charges have to be paid by firm

and there can be several taxes over transferring the product from one location to other. If

machinery is imported to produce or manufacture product the taxes can be levied on purchase,

import and the installation of machinery. There can be several rules and regulations that have to

be followed by the tax practitioners:

Supply and demand to be balanced: Tax practitioners can be liable to measure the costs

of the organisation spend over the production of the particular unit (Budd, 2016). Firm generates

the demand in market for their products and as to meet demands they started producing in excess

which will loss of resources and maximum time consumption. It can be essential for them to

know the better taxation policies as to compete in the UK market. It can be through applying the

laws and regulations in the effective manner that it can be benefit the organisation.

Quality standard: The essential part of knowing the rules for the tax practitioners is that

they have to meet the competition in the market and the substitute products, firms lower down

the value or prices of their products that can affect over their quality of such products. For the

manufacturing unit, this is necessary for them to follow the quality standards such as ISI mark

over the products. Regular inspection should be done over the products by the health and care

unit of the organisation. The raw material must be used in the products should be healthy and do

not generate the pollution (TAX 1 Tiens, 2017).

A part from these there can be further more responsibilities of a tax practitioner which are as

follows:

Tax practitioner must be informed and well known about the tax legislation and must

acquire the essential qualification to comply with common- laws rules as these are legal

responsibility of the practitioner.

3

Tax practitioners can be helpful for an organisation in helping with the various rules and

regulations imposed by UK government. Frequently changing taxation policies in UK market

over the transactions like import and export of the goods and services, manufacturing of the

various products, marketing of the item and etc. These can be understood and implied by the tax

practitioners in a business firm, to make them informed about the new policies to be followed

(Khan and Altaf, 2014). In a firm, there can be various transactions such as buying good quality

raw material at adequate prices, there can be taxation over importing raw material, but if

products are bought from domestic market than transportation charges have to be paid by firm

and there can be several taxes over transferring the product from one location to other. If

machinery is imported to produce or manufacture product the taxes can be levied on purchase,

import and the installation of machinery. There can be several rules and regulations that have to

be followed by the tax practitioners:

Supply and demand to be balanced: Tax practitioners can be liable to measure the costs

of the organisation spend over the production of the particular unit (Budd, 2016). Firm generates

the demand in market for their products and as to meet demands they started producing in excess

which will loss of resources and maximum time consumption. It can be essential for them to

know the better taxation policies as to compete in the UK market. It can be through applying the

laws and regulations in the effective manner that it can be benefit the organisation.

Quality standard: The essential part of knowing the rules for the tax practitioners is that

they have to meet the competition in the market and the substitute products, firms lower down

the value or prices of their products that can affect over their quality of such products. For the

manufacturing unit, this is necessary for them to follow the quality standards such as ISI mark

over the products. Regular inspection should be done over the products by the health and care

unit of the organisation. The raw material must be used in the products should be healthy and do

not generate the pollution (TAX 1 Tiens, 2017).

A part from these there can be further more responsibilities of a tax practitioner which are as

follows:

Tax practitioner must be informed and well known about the tax legislation and must

acquire the essential qualification to comply with common- laws rules as these are legal

responsibility of the practitioner.

3

Practitioners must know about the HMRC rule and regulations which will help them in

making the payments of the various taxations like income tax, CGT and Corporate tax.

There must be honesty in them while preparing the tax charge sheet and they must advice

their clients.

They must be up to date with their knowledge about taxation and regular changes in the

tax rates.

They will make sure that there must not be breach of any taxation law or they must

follow all the rule and regulations imposed by the government over various taxes.

Taxation must be done in an adequate manner as it must fulfil the requirements of all the

sectors like the government can earn the favourable amount in concern with making the

favourable rates over taxation (Budd, 2016). The main responsibility of the tax practitioners is to

gain the adequate knowledge about the current rate and rules in the taxation and they must

honestly advises individual about where they can reduce the taxes and where they can make the

adequate payments for the taxes.

1.3 Tax obligations

The tax practitioners can be agents or the other tax payers. There can be various

obligations over the taxes that has to be followed by them. These can be as follows:

Tax obligations: HMRC control of UK has obliged the tax payers to comply with the

taxation laws as they get completely sure regarding the taxes are to be made correct and legally

to various taxation method including VAT, Capital gain tax, PAYE1, Income Tax, Corporate

Taxes and may other taxes (Picciotto, 2015). They execute the whole taxation process which will

be beneficial in controlling the maximum number of crime rates in UK. Agents or tax payers

must make true payments of taxes, they must keep records of their all transactions like

appropriate payments of the taxes, rates imposed on amount and time and dates of taxes. There

must be punishment or penalties as per the breach of the rule and regulations by the agents or tax

practitioner.

Non-compliances: The breach of any tax rule or regulation than there are punishments

which are to be imposed over tax payers or agents. These is an technique to reduce crime and

lower down the risk of steeling the taxation revenue. There can be some penalties or punishments

over tax practitioners on the breach of any rules and regulations. Penalties can be made to the

1 Pay as you earn.

4

making the payments of the various taxations like income tax, CGT and Corporate tax.

There must be honesty in them while preparing the tax charge sheet and they must advice

their clients.

They must be up to date with their knowledge about taxation and regular changes in the

tax rates.

They will make sure that there must not be breach of any taxation law or they must

follow all the rule and regulations imposed by the government over various taxes.

Taxation must be done in an adequate manner as it must fulfil the requirements of all the

sectors like the government can earn the favourable amount in concern with making the

favourable rates over taxation (Budd, 2016). The main responsibility of the tax practitioners is to

gain the adequate knowledge about the current rate and rules in the taxation and they must

honestly advises individual about where they can reduce the taxes and where they can make the

adequate payments for the taxes.

1.3 Tax obligations

The tax practitioners can be agents or the other tax payers. There can be various

obligations over the taxes that has to be followed by them. These can be as follows:

Tax obligations: HMRC control of UK has obliged the tax payers to comply with the

taxation laws as they get completely sure regarding the taxes are to be made correct and legally

to various taxation method including VAT, Capital gain tax, PAYE1, Income Tax, Corporate

Taxes and may other taxes (Picciotto, 2015). They execute the whole taxation process which will

be beneficial in controlling the maximum number of crime rates in UK. Agents or tax payers

must make true payments of taxes, they must keep records of their all transactions like

appropriate payments of the taxes, rates imposed on amount and time and dates of taxes. There

must be punishment or penalties as per the breach of the rule and regulations by the agents or tax

practitioner.

Non-compliances: The breach of any tax rule or regulation than there are punishments

which are to be imposed over tax payers or agents. These is an technique to reduce crime and

lower down the risk of steeling the taxation revenue. There can be some penalties or punishments

over tax practitioners on the breach of any rules and regulations. Penalties can be made to the

1 Pay as you earn.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

individual if they did not make the payments for taxes or delayed in the payments than they will

be charged for punishments and penalties (Kemmerling, 2016). It will be totally void if there can

be breach of any laws or regulations because it will be illegal and the government of UK has to

bear all the losses occurred on the poor taxation made by their citizens. The punishment can be

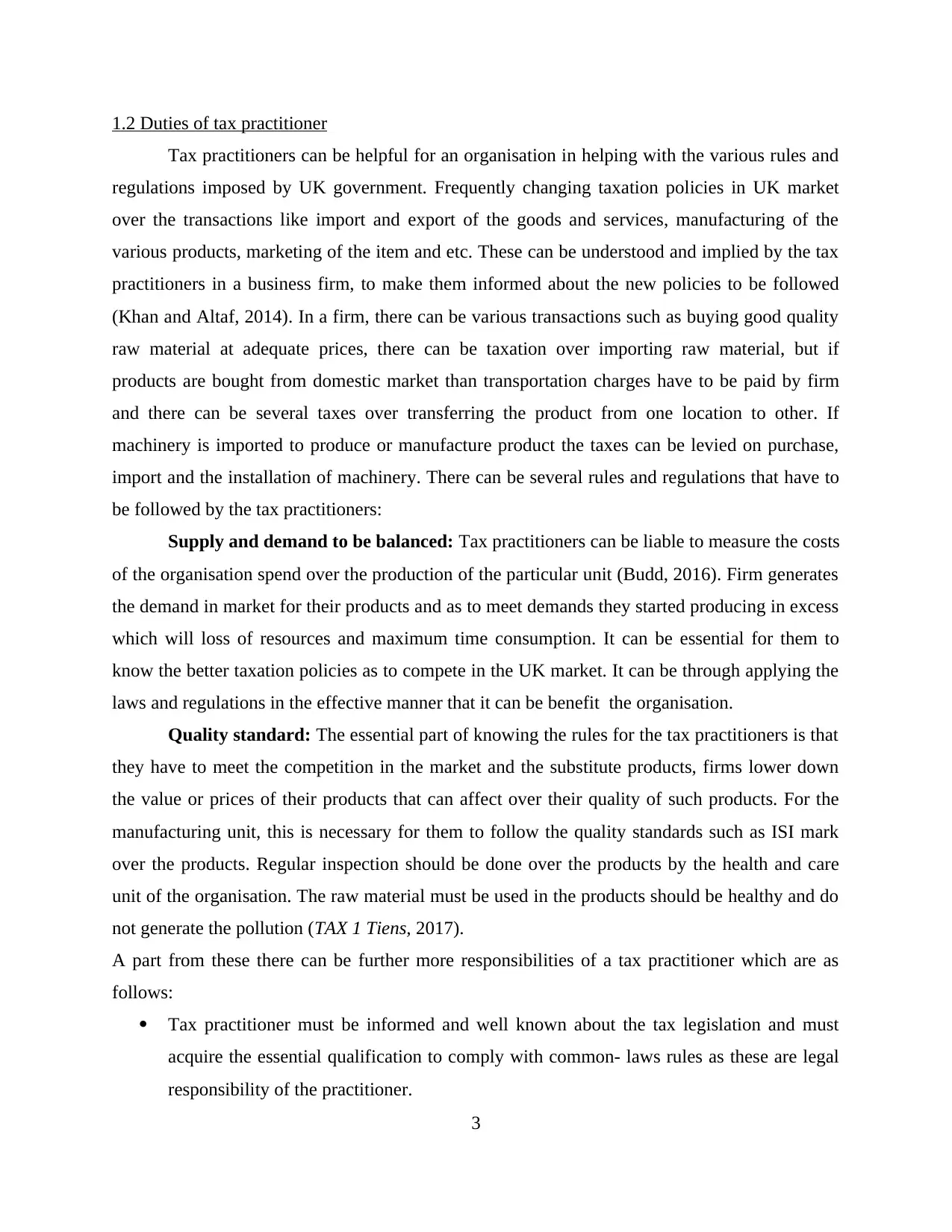

levied of them as if they do not notify HMRC2 about taxation transactions. The maximum

penalties can be levied on tax practitioner for the failures be shown in table:

Illustration 1: source: (Kemmerling, 2016)

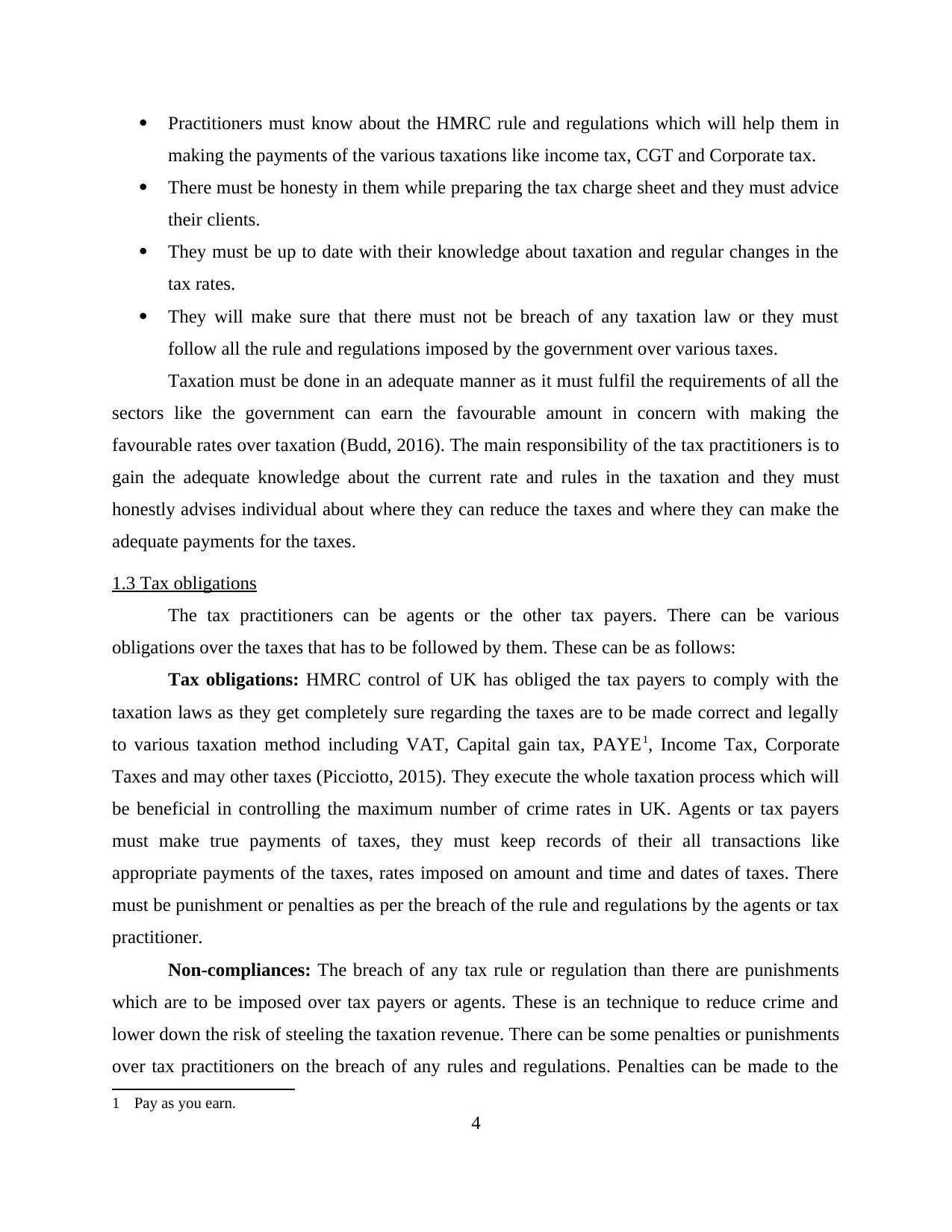

For the late payment of taxes made by the company can be automatically rated for 100 and it can

be more than the period of 3 month. If the documents provided by the tax payer are incorrect and

the not an adequate company tax can be made then there will be punishments such as charging

the extra tax and depends on the ranges of penalties as shown in the table below (Andrikopoulos,

A. and Kostaris, K, 2017). Penalty of more than 3000 can be charged over carrying or providing

the insufficient records to the legislation.

Illustration 2: source: (Andrikopoulos, A. and Kostaris, K,

2017)

2 Her Majesty revenue and customs, corporation tax penalty,2012

5

be charged for punishments and penalties (Kemmerling, 2016). It will be totally void if there can

be breach of any laws or regulations because it will be illegal and the government of UK has to

bear all the losses occurred on the poor taxation made by their citizens. The punishment can be

levied of them as if they do not notify HMRC2 about taxation transactions. The maximum

penalties can be levied on tax practitioner for the failures be shown in table:

Illustration 1: source: (Kemmerling, 2016)

For the late payment of taxes made by the company can be automatically rated for 100 and it can

be more than the period of 3 month. If the documents provided by the tax payer are incorrect and

the not an adequate company tax can be made then there will be punishments such as charging

the extra tax and depends on the ranges of penalties as shown in the table below (Andrikopoulos,

A. and Kostaris, K, 2017). Penalty of more than 3000 can be charged over carrying or providing

the insufficient records to the legislation.

Illustration 2: source: (Andrikopoulos, A. and Kostaris, K,

2017)

2 Her Majesty revenue and customs, corporation tax penalty,2012

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation: As per the above calculations there can be punishments to tax practitioner on

various mistakes made by them which can be by charging penalty, as per the ranges of

unprompted disclosure of the documents and records. Also, the penalty can be ranged for prompt

or quick disclosure of information or documents.

TASK 2

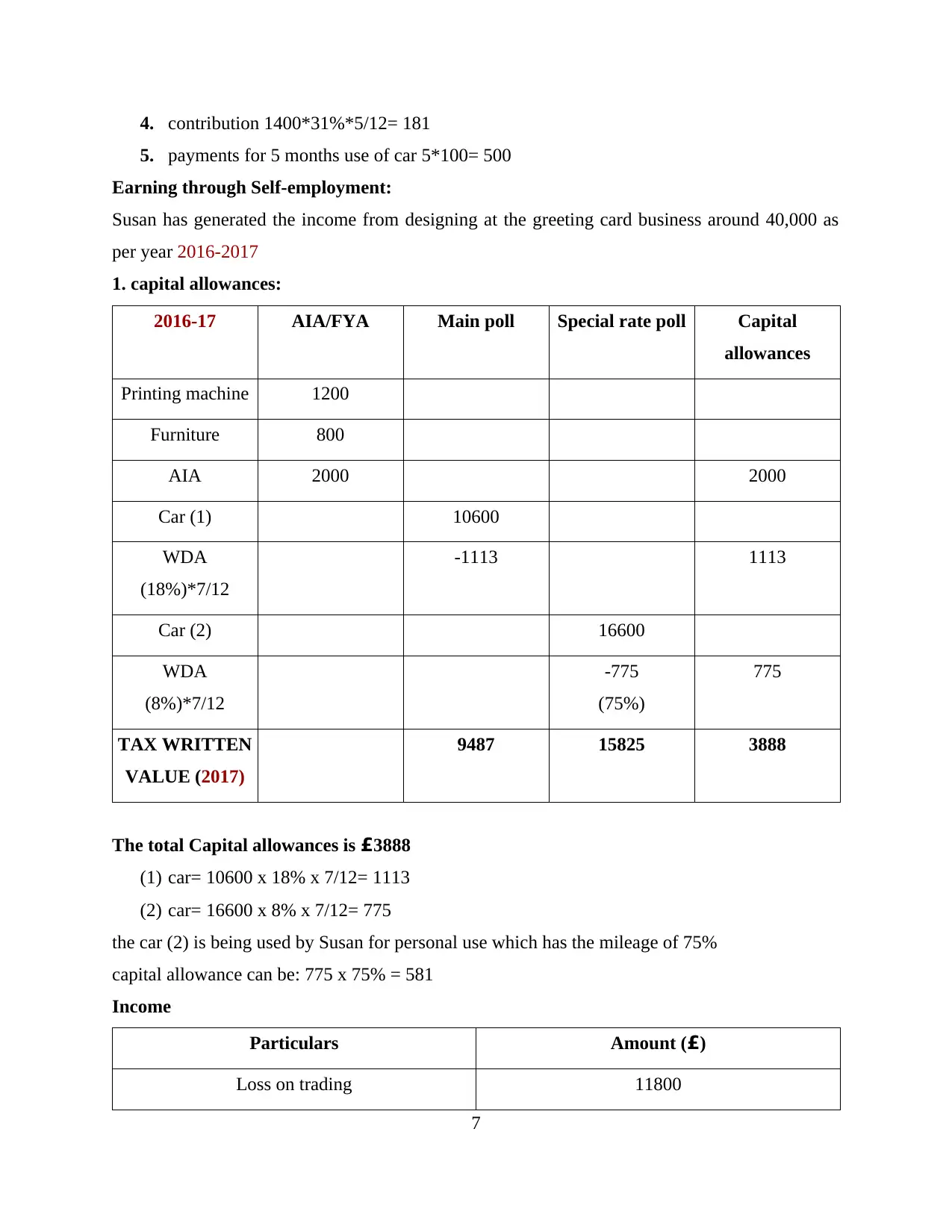

2.1 Income, expenses and allowances calculations

Earnings through Employment:

Income-

Particulars Amount (£)

Salary 28000

Benefits car 2067

Benefits fuel 2015

Less: use of car (contribution) -180

Less: use of car for 5 months -500

Total Income 31402

Allowances

Particulars Amount (£)

Personal allowances 8605

Interpretation:

1. Gross salary of Susan £28000

2. Benefits to Susan: (a) car can be facilitate by the till machine manager to Susan price at

the price of 16000 (petrol powered) with CO2 emission rate around 217 g/km. The round

of can be made at the nearest 5 than there can be percentage over car benefits is 215-

135(/)5% + fifteen % which equals to 31%. the use of car for 5 months than 16000 x 31%

x 5/12= 2067.

3. Fuel benefit can be 15600*31%*5/12= 2015

6

various mistakes made by them which can be by charging penalty, as per the ranges of

unprompted disclosure of the documents and records. Also, the penalty can be ranged for prompt

or quick disclosure of information or documents.

TASK 2

2.1 Income, expenses and allowances calculations

Earnings through Employment:

Income-

Particulars Amount (£)

Salary 28000

Benefits car 2067

Benefits fuel 2015

Less: use of car (contribution) -180

Less: use of car for 5 months -500

Total Income 31402

Allowances

Particulars Amount (£)

Personal allowances 8605

Interpretation:

1. Gross salary of Susan £28000

2. Benefits to Susan: (a) car can be facilitate by the till machine manager to Susan price at

the price of 16000 (petrol powered) with CO2 emission rate around 217 g/km. The round

of can be made at the nearest 5 than there can be percentage over car benefits is 215-

135(/)5% + fifteen % which equals to 31%. the use of car for 5 months than 16000 x 31%

x 5/12= 2067.

3. Fuel benefit can be 15600*31%*5/12= 2015

6

4. contribution 1400*31%*5/12= 181

5. payments for 5 months use of car 5*100= 500

Earning through Self-employment:

Susan has generated the income from designing at the greeting card business around 40,000 as

per year 2016-2017

1. capital allowances:

2016-17 AIA/FYA Main poll Special rate poll Capital

allowances

Printing machine 1200

Furniture 800

AIA 2000 2000

Car (1) 10600

WDA

(18%)*7/12

-1113 1113

Car (2) 16600

WDA

(8%)*7/12

-775

(75%)

775

TAX WRITTEN

VALUE (2017)

9487 15825 3888

The total Capital allowances is £3888

(1) car= 10600 x 18% x 7/12= 1113

(2) car= 16600 x 8% x 7/12= 775

the car (2) is being used by Susan for personal use which has the mileage of 75%

capital allowance can be: 775 x 75% = 581

Income

Particulars Amount (£)

Loss on trading 11800

7

5. payments for 5 months use of car 5*100= 500

Earning through Self-employment:

Susan has generated the income from designing at the greeting card business around 40,000 as

per year 2016-2017

1. capital allowances:

2016-17 AIA/FYA Main poll Special rate poll Capital

allowances

Printing machine 1200

Furniture 800

AIA 2000 2000

Car (1) 10600

WDA

(18%)*7/12

-1113 1113

Car (2) 16600

WDA

(8%)*7/12

-775

(75%)

775

TAX WRITTEN

VALUE (2017)

9487 15825 3888

The total Capital allowances is £3888

(1) car= 10600 x 18% x 7/12= 1113

(2) car= 16600 x 8% x 7/12= 775

the car (2) is being used by Susan for personal use which has the mileage of 75%

capital allowance can be: 775 x 75% = 581

Income

Particulars Amount (£)

Loss on trading 11800

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

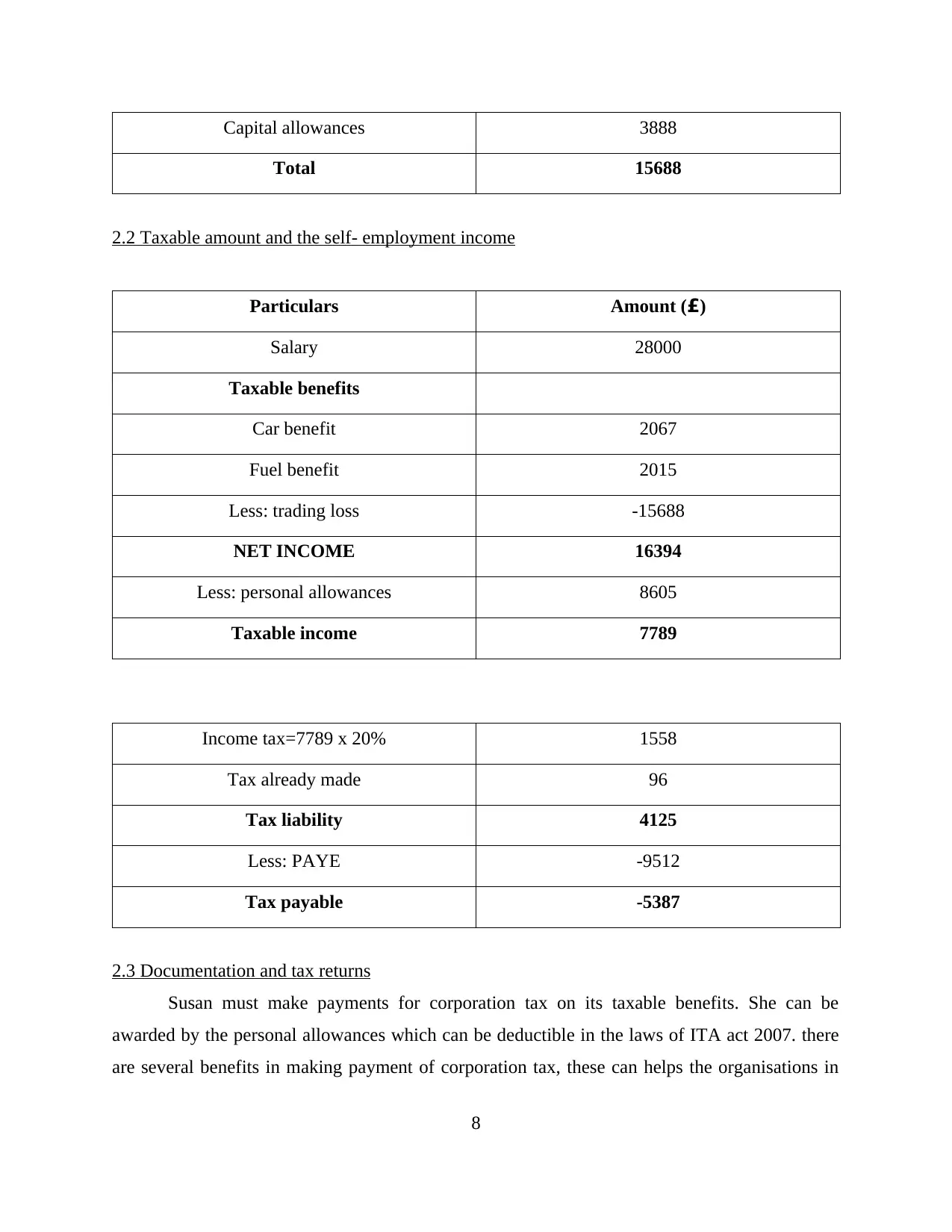

Capital allowances 3888

Total 15688

2.2 Taxable amount and the self- employment income

Particulars Amount (£)

Salary 28000

Taxable benefits

Car benefit 2067

Fuel benefit 2015

Less: trading loss -15688

NET INCOME 16394

Less: personal allowances 8605

Taxable income 7789

Income tax=7789 x 20% 1558

Tax already made 96

Tax liability 4125

Less: PAYE -9512

Tax payable -5387

2.3 Documentation and tax returns

Susan must make payments for corporation tax on its taxable benefits. She can be

awarded by the personal allowances which can be deductible in the laws of ITA act 2007. there

are several benefits in making payment of corporation tax, these can helps the organisations in

8

Total 15688

2.2 Taxable amount and the self- employment income

Particulars Amount (£)

Salary 28000

Taxable benefits

Car benefit 2067

Fuel benefit 2015

Less: trading loss -15688

NET INCOME 16394

Less: personal allowances 8605

Taxable income 7789

Income tax=7789 x 20% 1558

Tax already made 96

Tax liability 4125

Less: PAYE -9512

Tax payable -5387

2.3 Documentation and tax returns

Susan must make payments for corporation tax on its taxable benefits. She can be

awarded by the personal allowances which can be deductible in the laws of ITA act 2007. there

are several benefits in making payment of corporation tax, these can helps the organisations in

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

working together, more than the costs implied over resources can be offered and ventures that

will be helpful in providing cash to company (Ehrlich and Radulescu, 2017).

For setting up the new corporation the benefits can be gained by Susan in context with

that she have to first apply for registration under consideration of HMRC. After she can be able

to setup the organisational unit she must prepare system of regular report over income and

expenses occurred by her. There can be implementation of various rules and regulations as to

help her in the deductions over the income and expenses made throughout the operating year

(Understand your Self-Assessment tax bill. 2017). The deduction can be filed under various acts

like ICTA3 1988, CTA 20094, CAA, 20015.

TASK 3

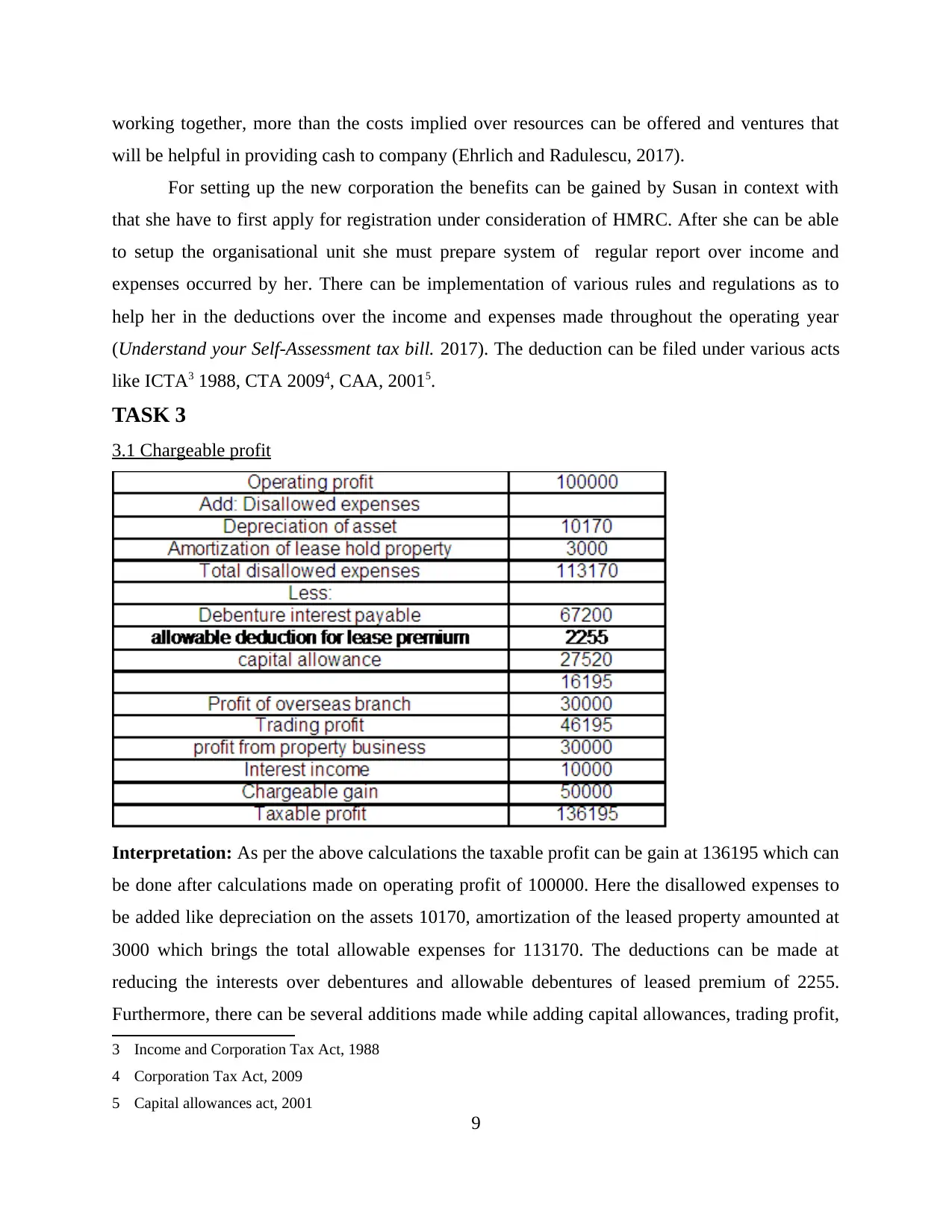

3.1 Chargeable profit

Interpretation: As per the above calculations the taxable profit can be gain at 136195 which can

be done after calculations made on operating profit of 100000. Here the disallowed expenses to

be added like depreciation on the assets 10170, amortization of the leased property amounted at

3000 which brings the total allowable expenses for 113170. The deductions can be made at

reducing the interests over debentures and allowable debentures of leased premium of 2255.

Furthermore, there can be several additions made while adding capital allowances, trading profit,

3 Income and Corporation Tax Act, 1988

4 Corporation Tax Act, 2009

5 Capital allowances act, 2001

9

will be helpful in providing cash to company (Ehrlich and Radulescu, 2017).

For setting up the new corporation the benefits can be gained by Susan in context with

that she have to first apply for registration under consideration of HMRC. After she can be able

to setup the organisational unit she must prepare system of regular report over income and

expenses occurred by her. There can be implementation of various rules and regulations as to

help her in the deductions over the income and expenses made throughout the operating year

(Understand your Self-Assessment tax bill. 2017). The deduction can be filed under various acts

like ICTA3 1988, CTA 20094, CAA, 20015.

TASK 3

3.1 Chargeable profit

Interpretation: As per the above calculations the taxable profit can be gain at 136195 which can

be done after calculations made on operating profit of 100000. Here the disallowed expenses to

be added like depreciation on the assets 10170, amortization of the leased property amounted at

3000 which brings the total allowable expenses for 113170. The deductions can be made at

reducing the interests over debentures and allowable debentures of leased premium of 2255.

Furthermore, there can be several additions made while adding capital allowances, trading profit,

3 Income and Corporation Tax Act, 1988

4 Corporation Tax Act, 2009

5 Capital allowances act, 2001

9

profit from overseas branch, interest income and the chargeable gains which all brings the total

profit (taxable).

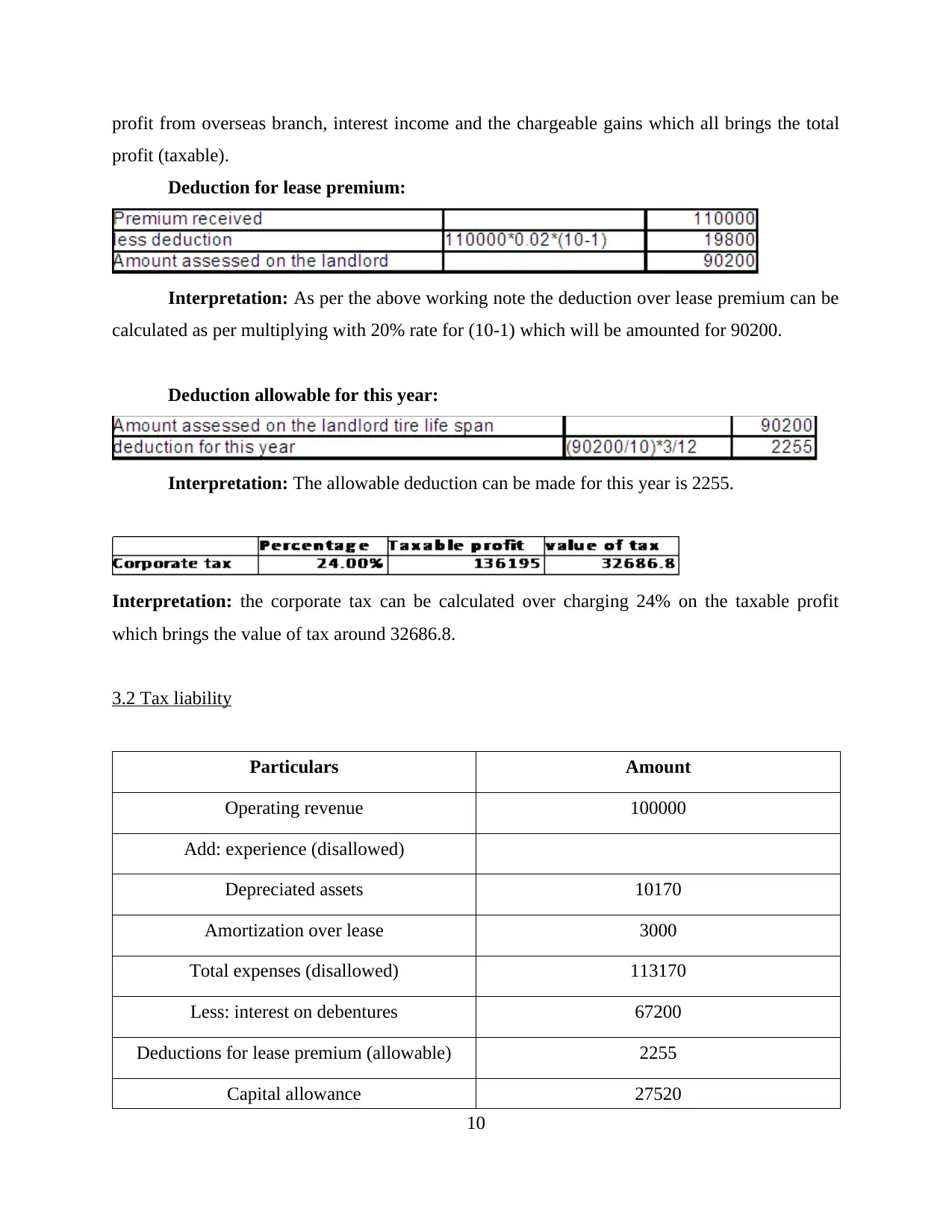

Deduction for lease premium:

Interpretation: As per the above working note the deduction over lease premium can be

calculated as per multiplying with 20% rate for (10-1) which will be amounted for 90200.

Deduction allowable for this year:

Interpretation: The allowable deduction can be made for this year is 2255.

Interpretation: the corporate tax can be calculated over charging 24% on the taxable profit

which brings the value of tax around 32686.8.

3.2 Tax liability

Particulars Amount

Operating revenue 100000

Add: experience (disallowed)

Depreciated assets 10170

Amortization over lease 3000

Total expenses (disallowed) 113170

Less: interest on debentures 67200

Deductions for lease premium (allowable) 2255

Capital allowance 27520

10

profit (taxable).

Deduction for lease premium:

Interpretation: As per the above working note the deduction over lease premium can be

calculated as per multiplying with 20% rate for (10-1) which will be amounted for 90200.

Deduction allowable for this year:

Interpretation: The allowable deduction can be made for this year is 2255.

Interpretation: the corporate tax can be calculated over charging 24% on the taxable profit

which brings the value of tax around 32686.8.

3.2 Tax liability

Particulars Amount

Operating revenue 100000

Add: experience (disallowed)

Depreciated assets 10170

Amortization over lease 3000

Total expenses (disallowed) 113170

Less: interest on debentures 67200

Deductions for lease premium (allowable) 2255

Capital allowance 27520

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.