Taxation Report: Taxation Implications of Capital Gains and Deductions

VerifiedAdded on 2019/11/26

|12

|2651

|161

Report

AI Summary

This report provides a comprehensive analysis of taxation principles, focusing on capital gains, deductions, and assessable income under the Income Tax Assessment Act 1997 (ITAA 1997). The report begins by explaining the concept of capital gains and losses, outlining how they are calculated and included in assessable income as statutory income. It then delves into the deductibility of expenses, differentiating between general and specific deductions, and highlighting the treatment of capital expenditures. The report applies these principles to three case studies: the capital gain tax consequences for Cassandra Pty Ltd, the deductibility of expenses for Oscar Pty Ltd, and the treatment of unpaid installments for Earnest Construction Pty Ltd. It includes detailed calculations and explanations to illustrate the tax implications of each scenario, providing practical insights into the application of tax laws in various business contexts. The report concludes by emphasizing the importance of accurate income assessment and the correct treatment of capital gains, deductions, and bad debts to determine taxable income.

Running Head: TAXATION

Taxation

Name of the Student:

Name of the University:

Authors Note:

Taxation

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

TAXATION

Table of Contents

Answer to part 1:.............................................................................................................................3

Answer to part 2:.............................................................................................................................7

Answer to part 3:.............................................................................................................................9

References:....................................................................................................................................12

TAXATION

Table of Contents

Answer to part 1:.............................................................................................................................3

Answer to part 2:.............................................................................................................................7

Answer to part 3:.............................................................................................................................9

References:....................................................................................................................................12

3

TAXATION

Answer to part 1:

The Division 100 of the Income tax Assessment Act 1997 provides a guide to the capital

or losses. The section 100-35 of the Income tax Assessment Act 1997 provides that a capital

gain is made if the amount received from the CGT event is more than the cost associated with

that CGT event and if it is vice versa then it is capital loss. That means on selling a capital asset,

real estate, shares or other such assets, a person, whether an individual or an organization with

separate legal identity, generally makes a gain or loss; these are termed as capital gain or capital

loss of such person. The difference between the cost of the asset that the person has incurred to

acquire it and the amount that the person has received from the disposal of such asset is either

capital gain or capital loss1. When the amount received from the disposal of a capital asset is

more than the cost incurred on acquiring such asset then the resultant will be capital gain.

However, in case the cost incurred in acquiring the asset is more than the amount received on

disposal of such asset then the resultant will be capital loss.

The Section 6-5 of Income Tax Assessment Act, 1997, provides the meaning of the

ordinary income. It states that income according to ordinary concept should be treated as

ordinary income. On the other hand, the section 6-10 of the Income Tax Assessment Act 1997

states that income that is not an ordinary income is a statutory income2. The section 6-25(2) of

the Income tax Assessment Act 1997 states that if an income is caught between ordinary and

statutory income then the specific provision shall apply. Therefore, in accordance with the

1 Barkoczy, Stephen. "Core Tax Legislation and Study Guide." OUP Catalogue (2017).

2 Chardon, Toni, Brett Freudenberg, and Mark Brimble. "Tax literacy in Australia: not knowing your deduction from

your offset." (2016).

TAXATION

Answer to part 1:

The Division 100 of the Income tax Assessment Act 1997 provides a guide to the capital

or losses. The section 100-35 of the Income tax Assessment Act 1997 provides that a capital

gain is made if the amount received from the CGT event is more than the cost associated with

that CGT event and if it is vice versa then it is capital loss. That means on selling a capital asset,

real estate, shares or other such assets, a person, whether an individual or an organization with

separate legal identity, generally makes a gain or loss; these are termed as capital gain or capital

loss of such person. The difference between the cost of the asset that the person has incurred to

acquire it and the amount that the person has received from the disposal of such asset is either

capital gain or capital loss1. When the amount received from the disposal of a capital asset is

more than the cost incurred on acquiring such asset then the resultant will be capital gain.

However, in case the cost incurred in acquiring the asset is more than the amount received on

disposal of such asset then the resultant will be capital loss.

The Section 6-5 of Income Tax Assessment Act, 1997, provides the meaning of the

ordinary income. It states that income according to ordinary concept should be treated as

ordinary income. On the other hand, the section 6-10 of the Income Tax Assessment Act 1997

states that income that is not an ordinary income is a statutory income2. The section 6-25(2) of

the Income tax Assessment Act 1997 states that if an income is caught between ordinary and

statutory income then the specific provision shall apply. Therefore, in accordance with the

1 Barkoczy, Stephen. "Core Tax Legislation and Study Guide." OUP Catalogue (2017).

2 Chardon, Toni, Brett Freudenberg, and Mark Brimble. "Tax literacy in Australia: not knowing your deduction from

your offset." (2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

TAXATION

section 102-5 of the Income tax Assessment Act 1997 it can be said that the capital gain should

be included in the assessable income as statutory income.

The Section 25-10 of ITAA provides that one can deduct expenditures incurred on repair

and maintenance on a depreciating asset only if such asset has sole been used to generate or to

produce assessable income. Thus, in case the sole purpose of the depreciating asset includes

anything else apart from using it for generation and production of assessable income then the

whole expenditures incurred on repair and maintenance of the asset would not be allowed as

deduction for computation of assessable income of the taxpayer concern3. According to sub-

section, 2 of this section (25-10 of ITAA) in case the property was party used for income

generation and party used for other purposes then proportionate amount of such expenditures

shall be allowed as deduction for computation of such assessable income. No capital expenditure

shall be allowed as deduction in computation of assessable income provided in sub section 3 of

section 25-10 of ITAA.

In determining the capital gain the concept of first element costs has to be worked out in

relation to a depreciating asset in accordance with the provision of section 40-180 of ITAA.

According to the provision of this section the first element is,

(a) The amount specified in an item; or

(b) The amount that has been paid by the existing owner to hold the asset4.

3 Mintrom, Michael, and Joannah Luetjens. "Design Thinking in Policymaking Processes: Opportunities and

Challenges." Australian Journal of Public Administration 75, no. 3 (2016): 391-402.

4 Kellow, Aynsley, and Marian Simms. "Policy change and industry associability: The Australian mining

sector." Australian Journal of Public Administration 72, no. 1 (2013): 41-54.

TAXATION

section 102-5 of the Income tax Assessment Act 1997 it can be said that the capital gain should

be included in the assessable income as statutory income.

The Section 25-10 of ITAA provides that one can deduct expenditures incurred on repair

and maintenance on a depreciating asset only if such asset has sole been used to generate or to

produce assessable income. Thus, in case the sole purpose of the depreciating asset includes

anything else apart from using it for generation and production of assessable income then the

whole expenditures incurred on repair and maintenance of the asset would not be allowed as

deduction for computation of assessable income of the taxpayer concern3. According to sub-

section, 2 of this section (25-10 of ITAA) in case the property was party used for income

generation and party used for other purposes then proportionate amount of such expenditures

shall be allowed as deduction for computation of such assessable income. No capital expenditure

shall be allowed as deduction in computation of assessable income provided in sub section 3 of

section 25-10 of ITAA.

In determining the capital gain the concept of first element costs has to be worked out in

relation to a depreciating asset in accordance with the provision of section 40-180 of ITAA.

According to the provision of this section the first element is,

(a) The amount specified in an item; or

(b) The amount that has been paid by the existing owner to hold the asset4.

3 Mintrom, Michael, and Joannah Luetjens. "Design Thinking in Policymaking Processes: Opportunities and

Challenges." Australian Journal of Public Administration 75, no. 3 (2016): 391-402.

4 Kellow, Aynsley, and Marian Simms. "Policy change and industry associability: The Australian mining

sector." Australian Journal of Public Administration 72, no. 1 (2013): 41-54.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

TAXATION

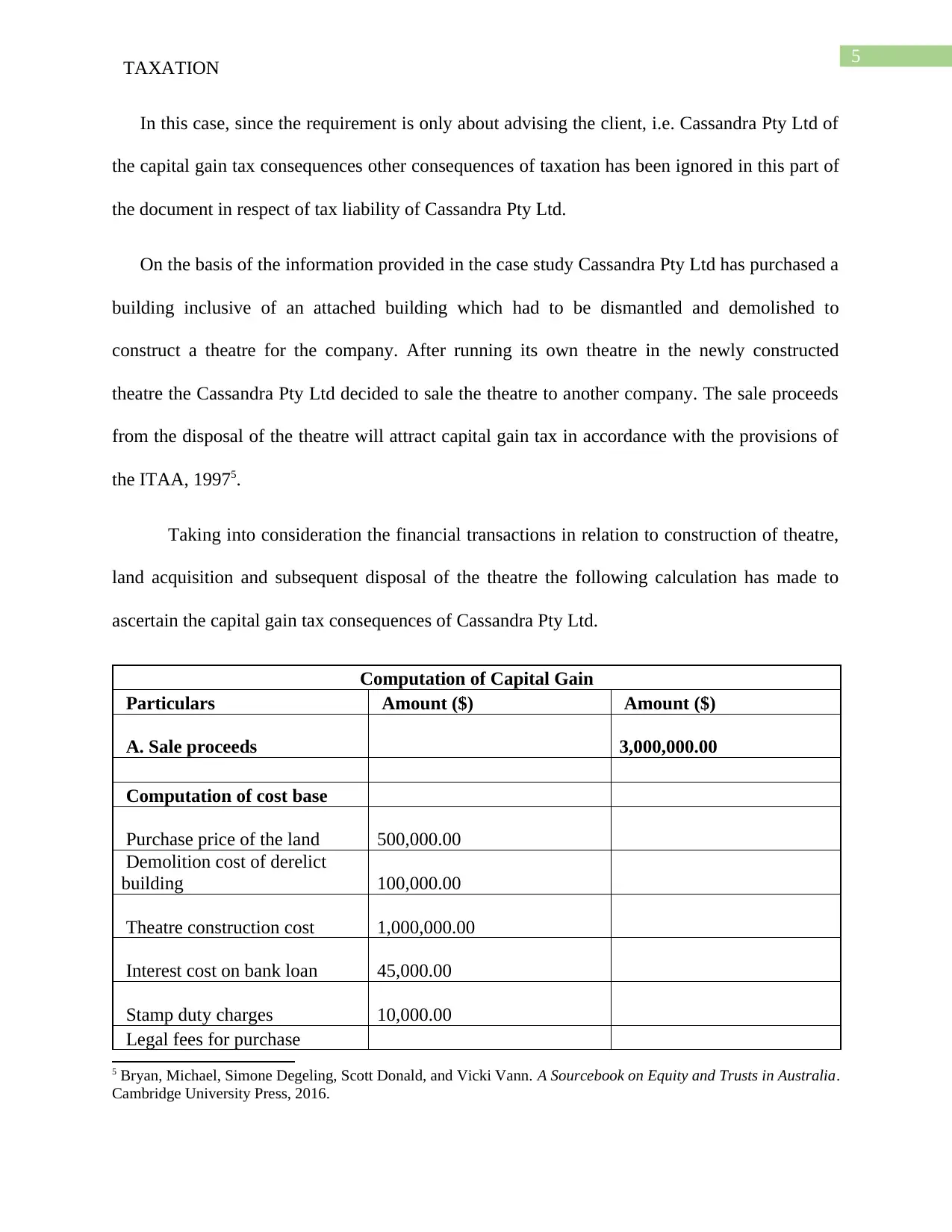

In this case, since the requirement is only about advising the client, i.e. Cassandra Pty Ltd of

the capital gain tax consequences other consequences of taxation has been ignored in this part of

the document in respect of tax liability of Cassandra Pty Ltd.

On the basis of the information provided in the case study Cassandra Pty Ltd has purchased a

building inclusive of an attached building which had to be dismantled and demolished to

construct a theatre for the company. After running its own theatre in the newly constructed

theatre the Cassandra Pty Ltd decided to sale the theatre to another company. The sale proceeds

from the disposal of the theatre will attract capital gain tax in accordance with the provisions of

the ITAA, 19975.

Taking into consideration the financial transactions in relation to construction of theatre,

land acquisition and subsequent disposal of the theatre the following calculation has made to

ascertain the capital gain tax consequences of Cassandra Pty Ltd.

Computation of Capital Gain

Particulars Amount ($) Amount ($)

A. Sale proceeds 3,000,000.00

Computation of cost base

Purchase price of the land 500,000.00

Demolition cost of derelict

building 100,000.00

Theatre construction cost 1,000,000.00

Interest cost on bank loan 45,000.00

Stamp duty charges 10,000.00

Legal fees for purchase

5 Bryan, Michael, Simone Degeling, Scott Donald, and Vicki Vann. A Sourcebook on Equity and Trusts in Australia.

Cambridge University Press, 2016.

TAXATION

In this case, since the requirement is only about advising the client, i.e. Cassandra Pty Ltd of

the capital gain tax consequences other consequences of taxation has been ignored in this part of

the document in respect of tax liability of Cassandra Pty Ltd.

On the basis of the information provided in the case study Cassandra Pty Ltd has purchased a

building inclusive of an attached building which had to be dismantled and demolished to

construct a theatre for the company. After running its own theatre in the newly constructed

theatre the Cassandra Pty Ltd decided to sale the theatre to another company. The sale proceeds

from the disposal of the theatre will attract capital gain tax in accordance with the provisions of

the ITAA, 19975.

Taking into consideration the financial transactions in relation to construction of theatre,

land acquisition and subsequent disposal of the theatre the following calculation has made to

ascertain the capital gain tax consequences of Cassandra Pty Ltd.

Computation of Capital Gain

Particulars Amount ($) Amount ($)

A. Sale proceeds 3,000,000.00

Computation of cost base

Purchase price of the land 500,000.00

Demolition cost of derelict

building 100,000.00

Theatre construction cost 1,000,000.00

Interest cost on bank loan 45,000.00

Stamp duty charges 10,000.00

Legal fees for purchase

5 Bryan, Michael, Simone Degeling, Scott Donald, and Vicki Vann. A Sourcebook on Equity and Trusts in Australia.

Cambridge University Press, 2016.

6

TAXATION

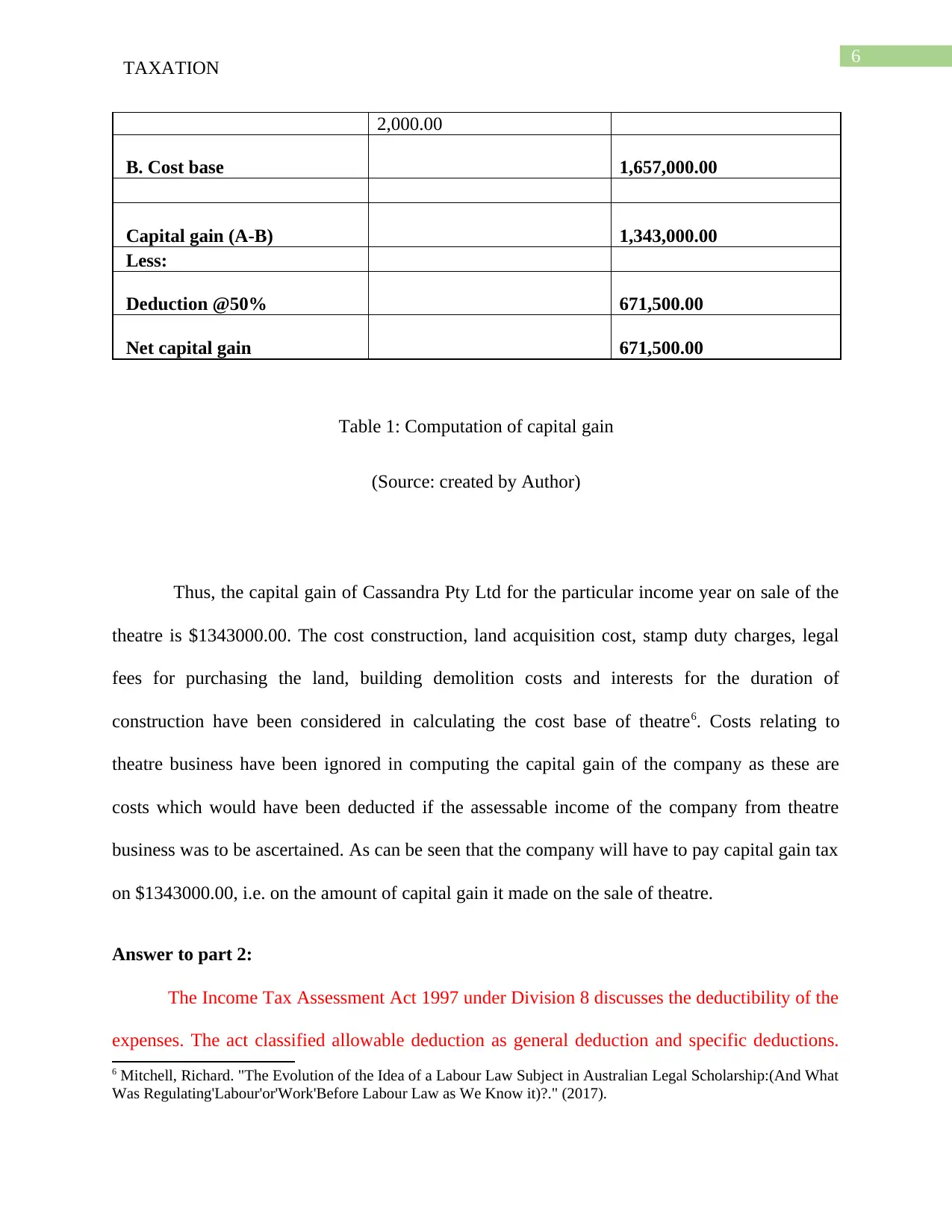

2,000.00

B. Cost base 1,657,000.00

Capital gain (A-B) 1,343,000.00

Less:

Deduction @50% 671,500.00

Net capital gain 671,500.00

Table 1: Computation of capital gain

(Source: created by Author)

Thus, the capital gain of Cassandra Pty Ltd for the particular income year on sale of the

theatre is $1343000.00. The cost construction, land acquisition cost, stamp duty charges, legal

fees for purchasing the land, building demolition costs and interests for the duration of

construction have been considered in calculating the cost base of theatre6. Costs relating to

theatre business have been ignored in computing the capital gain of the company as these are

costs which would have been deducted if the assessable income of the company from theatre

business was to be ascertained. As can be seen that the company will have to pay capital gain tax

on $1343000.00, i.e. on the amount of capital gain it made on the sale of theatre.

Answer to part 2:

The Income Tax Assessment Act 1997 under Division 8 discusses the deductibility of the

expenses. The act classified allowable deduction as general deduction and specific deductions.

6 Mitchell, Richard. "The Evolution of the Idea of a Labour Law Subject in Australian Legal Scholarship:(And What

Was Regulating'Labour'or'Work'Before Labour Law as We Know it)?." (2017).

TAXATION

2,000.00

B. Cost base 1,657,000.00

Capital gain (A-B) 1,343,000.00

Less:

Deduction @50% 671,500.00

Net capital gain 671,500.00

Table 1: Computation of capital gain

(Source: created by Author)

Thus, the capital gain of Cassandra Pty Ltd for the particular income year on sale of the

theatre is $1343000.00. The cost construction, land acquisition cost, stamp duty charges, legal

fees for purchasing the land, building demolition costs and interests for the duration of

construction have been considered in calculating the cost base of theatre6. Costs relating to

theatre business have been ignored in computing the capital gain of the company as these are

costs which would have been deducted if the assessable income of the company from theatre

business was to be ascertained. As can be seen that the company will have to pay capital gain tax

on $1343000.00, i.e. on the amount of capital gain it made on the sale of theatre.

Answer to part 2:

The Income Tax Assessment Act 1997 under Division 8 discusses the deductibility of the

expenses. The act classified allowable deduction as general deduction and specific deductions.

6 Mitchell, Richard. "The Evolution of the Idea of a Labour Law Subject in Australian Legal Scholarship:(And What

Was Regulating'Labour'or'Work'Before Labour Law as We Know it)?." (2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

TAXATION

The section 8-1 of the ITAA 97 states that a taxpayer is allowed to deduct the expenses from the

assessable income to the extent the expenses is used for producing the assessable income or is

incurred for carrying out the business. The section 8-1(2) also mentions the expenses that are of

capital, private or domestic nature are not allowed as deduction7. There are certain deductions

that are allowed under specific provisions of the act. This type of deduction is termed as specific

deduction as per section 8-5 of the ITAA 97. The section 8-1 of the ITAA97 contains two limbs

that allows the taxpayer to deduct the loss or outgoing from the assessable income. The first limb

is the positive limb it is the expenses that is incurred for producing the assessable income by the

taxpayer8. The second limb is the negative limb that states the loss or outgoings is not allowed as

deduction if it falls under any of the negative limb. In this case, the expenses that are allowed

under these sections are discussed by referring to the provisions of the act.

The amount of $500000.00 incurred by Oscar, the payment of which was decided to be

made in four equal installments over a period of 16 months of which though the company failed

to pay last two installments will not be allowed as deduction in computation of assessable

income of Oscar Pty Ltd as the expenditure is capital expenditure in nature9. Thus, the

expenditure will be added to the cost of theatre on which the company can claim depreciation.

This depreciation would have been allowed as deduction in computation of the assessable

income of the company from its theatre business. However, apart from that all the expenses

incurred by the company for and only for the business of the theatre will be allowed as deduction

7 Khanh Hung, Tran, and Nguyen Duc Hung. "State Financial Transfers in Environmental Protection: The Case of

Vietnam." Journal of Economics and Development 16, no. 2 (2014): 93.

8 Kang, Chuen Tat. Full Legal Report in Victoria of Australia: Chuen-Tat Kang V Swinburne University of

Technology Australia. Kang Chuen Tat, 2015.

9 Brigham, Eugene F., and Michael C. Ehrhardt. Financial management: Theory & practice. Cengage Learning,

2013.

TAXATION

The section 8-1 of the ITAA 97 states that a taxpayer is allowed to deduct the expenses from the

assessable income to the extent the expenses is used for producing the assessable income or is

incurred for carrying out the business. The section 8-1(2) also mentions the expenses that are of

capital, private or domestic nature are not allowed as deduction7. There are certain deductions

that are allowed under specific provisions of the act. This type of deduction is termed as specific

deduction as per section 8-5 of the ITAA 97. The section 8-1 of the ITAA97 contains two limbs

that allows the taxpayer to deduct the loss or outgoing from the assessable income. The first limb

is the positive limb it is the expenses that is incurred for producing the assessable income by the

taxpayer8. The second limb is the negative limb that states the loss or outgoings is not allowed as

deduction if it falls under any of the negative limb. In this case, the expenses that are allowed

under these sections are discussed by referring to the provisions of the act.

The amount of $500000.00 incurred by Oscar, the payment of which was decided to be

made in four equal installments over a period of 16 months of which though the company failed

to pay last two installments will not be allowed as deduction in computation of assessable

income of Oscar Pty Ltd as the expenditure is capital expenditure in nature9. Thus, the

expenditure will be added to the cost of theatre on which the company can claim depreciation.

This depreciation would have been allowed as deduction in computation of the assessable

income of the company from its theatre business. However, apart from that all the expenses

incurred by the company for and only for the business of the theatre will be allowed as deduction

7 Khanh Hung, Tran, and Nguyen Duc Hung. "State Financial Transfers in Environmental Protection: The Case of

Vietnam." Journal of Economics and Development 16, no. 2 (2014): 93.

8 Kang, Chuen Tat. Full Legal Report in Victoria of Australia: Chuen-Tat Kang V Swinburne University of

Technology Australia. Kang Chuen Tat, 2015.

9 Brigham, Eugene F., and Michael C. Ehrhardt. Financial management: Theory & practice. Cengage Learning,

2013.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

TAXATION

in computation of assessable income of the company from its theatre business10. Accordingly, the

salary costs of $15000 per week to employees which include carpenter, stage and lighting

technicians, finance manager and a marketing manager. The material expenses of $50000 to be

used for construction of stage requiring for the play; and all the payments to be made to actors

i.e. $500 per rehearsal and $1000 per performance will be allowed as deduction in computing the

assessable income / loss from the theatre business of the company for the particular income year

to which these relate.

Oscar Pty Ltd is an organization that is in the business of theatre and thus, all expenses

incurred by the company in relation to the stage play and theatre will be allowed as deduction in

computation of taxable income from theatre business provided these are expenditures revenue in

nature11. In case of capital expenditure such as construction or strengthening of the theatre

building to protect from earthquake shall be added to the cost of building since the expenditure

has strengthen the existing building and enhanced its life period by a certain margin and will

protect the building from future earthquake like the one took place in Christchurch, New

Zealand12. Accordingly, the expenses incurred as discussed above for creating and developing

plays to be performed in theatre will be allowed as deduction to compute the taxable income of

the company from theatre business.

Expenditures Amount ($) Allow ability /

non-allow ability

Reason

Strengthening 500,000.00 not allowed Capital expenditure in

10 Mumford, Ann. Taxing culture: towards a theory of tax collection law. Routledge, 2017.

11 Kurtz, Jennifer A., Roland J. Cole, and Isabel A. Cole. "Citizens and E-Government Service Delivery: Techniques

to Increase Citizen Participation." In Digital Literacy: Concepts, Methodologies, Tools, and Applications, pp. 910-

931. IGI Global, 2013.

12 Berk, Jonathon, Peter DeMarzo, Jarrod Harford, Guy Ford, Vito Mollica, and Nigel Finch. Fundamentals of

corporate finance. Pearson Higher Education AU, 2013.

TAXATION

in computation of assessable income of the company from its theatre business10. Accordingly, the

salary costs of $15000 per week to employees which include carpenter, stage and lighting

technicians, finance manager and a marketing manager. The material expenses of $50000 to be

used for construction of stage requiring for the play; and all the payments to be made to actors

i.e. $500 per rehearsal and $1000 per performance will be allowed as deduction in computing the

assessable income / loss from the theatre business of the company for the particular income year

to which these relate.

Oscar Pty Ltd is an organization that is in the business of theatre and thus, all expenses

incurred by the company in relation to the stage play and theatre will be allowed as deduction in

computation of taxable income from theatre business provided these are expenditures revenue in

nature11. In case of capital expenditure such as construction or strengthening of the theatre

building to protect from earthquake shall be added to the cost of building since the expenditure

has strengthen the existing building and enhanced its life period by a certain margin and will

protect the building from future earthquake like the one took place in Christchurch, New

Zealand12. Accordingly, the expenses incurred as discussed above for creating and developing

plays to be performed in theatre will be allowed as deduction to compute the taxable income of

the company from theatre business.

Expenditures Amount ($) Allow ability /

non-allow ability

Reason

Strengthening 500,000.00 not allowed Capital expenditure in

10 Mumford, Ann. Taxing culture: towards a theory of tax collection law. Routledge, 2017.

11 Kurtz, Jennifer A., Roland J. Cole, and Isabel A. Cole. "Citizens and E-Government Service Delivery: Techniques

to Increase Citizen Participation." In Digital Literacy: Concepts, Methodologies, Tools, and Applications, pp. 910-

931. IGI Global, 2013.

12 Berk, Jonathon, Peter DeMarzo, Jarrod Harford, Guy Ford, Vito Mollica, and Nigel Finch. Fundamentals of

corporate finance. Pearson Higher Education AU, 2013.

9

TAXATION

work in building nature

Salary costs of

employees

$15000 Per week Allowed Exclusively incurred for the

purpose of business.

Material cost

necessary for stage

$50,000 Allowed Exclusively incurred for the

purpose of business.

Rehearsal

expenses

$500 Per rehearsal Allowed Exclusively incurred for the

purpose of business.

Performance

expenses

$1000 to $1500

Per performance

Allowed Exclusively incurred for the

purpose of business.

Table 2: Expenditure

(Source: created by Author)

Answer to part 3:

The section 4-1 of the Income Tax Assessment Act 1997 provides that every individual,

business or other entity is required to pay tax on their taxable income. The taxable income is

calculated by deducting allowable deductions from the assessable income13. The assessable

income is classified into ordinary income and statutory income. The income according to the

ordinary concept is treated as the ordinary income as per section 6-5 of the ITAA 97. The

income that is not an ordinary concept should be treated as statutory income as per section 6-10

of the act. The individual is required to pay tax on the income that is accrued or received. In

accordance with the concept of ordinary income as provided in section 6-5 of ITAA 1997-failed

installment by customers will not be considered as an ordinary income until unless the customers

have paid the installments at a later stage14. Thus, in this case the contact between Ernest

13 Berk, Jonathon, Peter DeMarzo, Jarrod Harford, Guy Ford, Vito Mollica, and Nigel Finch. Fundamentals of

corporate finance. Pearson Higher Education AU, 2013.

14 Kumar, Rajesh. Strategic Financial Management Casebook. Academic Press, 2017.

TAXATION

work in building nature

Salary costs of

employees

$15000 Per week Allowed Exclusively incurred for the

purpose of business.

Material cost

necessary for stage

$50,000 Allowed Exclusively incurred for the

purpose of business.

Rehearsal

expenses

$500 Per rehearsal Allowed Exclusively incurred for the

purpose of business.

Performance

expenses

$1000 to $1500

Per performance

Allowed Exclusively incurred for the

purpose of business.

Table 2: Expenditure

(Source: created by Author)

Answer to part 3:

The section 4-1 of the Income Tax Assessment Act 1997 provides that every individual,

business or other entity is required to pay tax on their taxable income. The taxable income is

calculated by deducting allowable deductions from the assessable income13. The assessable

income is classified into ordinary income and statutory income. The income according to the

ordinary concept is treated as the ordinary income as per section 6-5 of the ITAA 97. The

income that is not an ordinary concept should be treated as statutory income as per section 6-10

of the act. The individual is required to pay tax on the income that is accrued or received. In

accordance with the concept of ordinary income as provided in section 6-5 of ITAA 1997-failed

installment by customers will not be considered as an ordinary income until unless the customers

have paid the installments at a later stage14. Thus, in this case the contact between Ernest

13 Berk, Jonathon, Peter DeMarzo, Jarrod Harford, Guy Ford, Vito Mollica, and Nigel Finch. Fundamentals of

corporate finance. Pearson Higher Education AU, 2013.

14 Kumar, Rajesh. Strategic Financial Management Casebook. Academic Press, 2017.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

TAXATION

Construction Pty Ltd and Oscar Pty Ltd provided that the later will made four equal installment

of $125000 within a period of 16 months to the former. The former, i.e. Earnest Construction Pty

Ltd will only be under an obligation to include the installments received from Oscar if the same

has actually been received as provided in section 6-5 of ITAA 1997. Since in this case Oscar Pty

Ltd has failed to make payment of the last two installments of $125000 to Earnest Construction

Pty Ltd the later will obviously not include the installment in its revenue to ascertain its

assessable income. The failed installments in-fact should be disclosed as bad debts in the books

of accounts and shall be deducted from revenue, if already included, as bad debts to reduce its

assessable income from business15.

However, if at a later date, in case the Oscar Pty Ltd made good of its failed installments

by making payment in the future to Earnest Construction Pty Ltd. Then, the later shall include

the installments received as revenue of the business to ascertain its assessable income form

business for the income year in which the installments were to be paid16.

Based on the above it is clear that only if at a future date Earnest Construction Pty Ltd

gets to receive the installments of $125000.00 that Oscar Pty Ltd failed to pay during the income

year to be ended on 30 June, 2018 then the same shall be included in assessable income of

Earnest Construction Pty Ltd for the year in which the installments shall be received by the

company.

15 Kang, Chuen Tat. Full Legal Report in Victoria of Australia: Chuen-Tat Kang V Swinburne University of

Technology Australia. Kang Chuen Tat, 2015.

16 Sjostrom Jr, William K. Business Organizations: A Transactional Approach. Wolters Kluwer Law & Business,

2015.

TAXATION

Construction Pty Ltd and Oscar Pty Ltd provided that the later will made four equal installment

of $125000 within a period of 16 months to the former. The former, i.e. Earnest Construction Pty

Ltd will only be under an obligation to include the installments received from Oscar if the same

has actually been received as provided in section 6-5 of ITAA 1997. Since in this case Oscar Pty

Ltd has failed to make payment of the last two installments of $125000 to Earnest Construction

Pty Ltd the later will obviously not include the installment in its revenue to ascertain its

assessable income. The failed installments in-fact should be disclosed as bad debts in the books

of accounts and shall be deducted from revenue, if already included, as bad debts to reduce its

assessable income from business15.

However, if at a later date, in case the Oscar Pty Ltd made good of its failed installments

by making payment in the future to Earnest Construction Pty Ltd. Then, the later shall include

the installments received as revenue of the business to ascertain its assessable income form

business for the income year in which the installments were to be paid16.

Based on the above it is clear that only if at a future date Earnest Construction Pty Ltd

gets to receive the installments of $125000.00 that Oscar Pty Ltd failed to pay during the income

year to be ended on 30 June, 2018 then the same shall be included in assessable income of

Earnest Construction Pty Ltd for the year in which the installments shall be received by the

company.

15 Kang, Chuen Tat. Full Legal Report in Victoria of Australia: Chuen-Tat Kang V Swinburne University of

Technology Australia. Kang Chuen Tat, 2015.

16 Sjostrom Jr, William K. Business Organizations: A Transactional Approach. Wolters Kluwer Law & Business,

2015.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

TAXATION

References:

Barkoczy, Stephen. "Core Tax Legislation and Study Guide." OUP Catalogue (2017).

Berk, Jonathon, Peter DeMarzo, Jarrod Harford, Guy Ford, Vito Mollica, and Nigel

Finch. Fundamentals of corporate finance. Pearson Higher Education AU, 2013.

Brigham, Eugene F., and Michael C. Ehrhardt. Financial management: Theory & practice.

Cengage Learning, 2013.

Bryan, Michael, Simone Degeling, Scott Donald, and Vicki Vann. A Sourcebook on Equity and

Trusts in Australia. Cambridge University Press, 2016.

Chardon, Toni, Brett Freudenberg, and Mark Brimble. "Tax literacy in Australia: not knowing

your deduction from your offset." (2016).

Kang, Chuen Tat. Full Legal Report in Victoria of Australia: Chuen-Tat Kang V Swinburne

University of Technology Australia. Kang Chuen Tat, 2015.

Kang, Chuen Tat. Full Legal Report in Victoria of Australia: Chuen-Tat Kang V Swinburne

University of Technology Australia. Kang Chuen Tat, 2015.

Kellow, Aynsley, and Marian Simms. "Policy change and industry associability: The Australian

mining sector." Australian Journal of Public Administration 72, no. 1 (2013): 41-54.

Khanh Hung, Tran, and Nguyen Duc Hung. "State Financial Transfers in Environmental

Protection: The Case of Vietnam." Journal of Economics and Development 16, no. 2 (2014): 93.

Kumar, Rajesh. Strategic Financial Management Casebook. Academic Press, 2017.

TAXATION

References:

Barkoczy, Stephen. "Core Tax Legislation and Study Guide." OUP Catalogue (2017).

Berk, Jonathon, Peter DeMarzo, Jarrod Harford, Guy Ford, Vito Mollica, and Nigel

Finch. Fundamentals of corporate finance. Pearson Higher Education AU, 2013.

Brigham, Eugene F., and Michael C. Ehrhardt. Financial management: Theory & practice.

Cengage Learning, 2013.

Bryan, Michael, Simone Degeling, Scott Donald, and Vicki Vann. A Sourcebook on Equity and

Trusts in Australia. Cambridge University Press, 2016.

Chardon, Toni, Brett Freudenberg, and Mark Brimble. "Tax literacy in Australia: not knowing

your deduction from your offset." (2016).

Kang, Chuen Tat. Full Legal Report in Victoria of Australia: Chuen-Tat Kang V Swinburne

University of Technology Australia. Kang Chuen Tat, 2015.

Kang, Chuen Tat. Full Legal Report in Victoria of Australia: Chuen-Tat Kang V Swinburne

University of Technology Australia. Kang Chuen Tat, 2015.

Kellow, Aynsley, and Marian Simms. "Policy change and industry associability: The Australian

mining sector." Australian Journal of Public Administration 72, no. 1 (2013): 41-54.

Khanh Hung, Tran, and Nguyen Duc Hung. "State Financial Transfers in Environmental

Protection: The Case of Vietnam." Journal of Economics and Development 16, no. 2 (2014): 93.

Kumar, Rajesh. Strategic Financial Management Casebook. Academic Press, 2017.

12

TAXATION

Kurtz, Jennifer A., Roland J. Cole, and Isabel A. Cole. "Citizens and E-Government Service

Delivery: Techniques to Increase Citizen Participation." In Digital Literacy: Concepts,

Methodologies, Tools, and Applications, pp. 910-931. IGI Global, 2013.

Mintrom, Michael, and Joannah Luetjens. "Design Thinking in Policymaking Processes:

Opportunities and Challenges." Australian Journal of Public Administration 75, no. 3 (2016):

391-402.

Mitchell, Richard. "The Evolution of the Idea of a Labour Law Subject in Australian Legal

Scholarship:(And What Was Regulating'Labour'or'Work'Before Labour Law as We Know it)?."

(2017).

Mumford, Ann. Taxing culture: towards a theory of tax collection law. Routledge, 2017.

Sjostrom Jr, William K. Business Organizations: A Transactional Approach. Wolters Kluwer

Law & Business, 2015.

Zagaris, Bruce. International white collar crime: cases and materials. Cambridge University

Press, 2015.

TAXATION

Kurtz, Jennifer A., Roland J. Cole, and Isabel A. Cole. "Citizens and E-Government Service

Delivery: Techniques to Increase Citizen Participation." In Digital Literacy: Concepts,

Methodologies, Tools, and Applications, pp. 910-931. IGI Global, 2013.

Mintrom, Michael, and Joannah Luetjens. "Design Thinking in Policymaking Processes:

Opportunities and Challenges." Australian Journal of Public Administration 75, no. 3 (2016):

391-402.

Mitchell, Richard. "The Evolution of the Idea of a Labour Law Subject in Australian Legal

Scholarship:(And What Was Regulating'Labour'or'Work'Before Labour Law as We Know it)?."

(2017).

Mumford, Ann. Taxing culture: towards a theory of tax collection law. Routledge, 2017.

Sjostrom Jr, William K. Business Organizations: A Transactional Approach. Wolters Kluwer

Law & Business, 2015.

Zagaris, Bruce. International white collar crime: cases and materials. Cambridge University

Press, 2015.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.