Taxation Law Assignment: Income Tax, Capital Gains, and Case Analysis

VerifiedAdded on 2021/06/17

|11

|2182

|39

Homework Assignment

AI Summary

This taxation law assignment solution addresses several key issues related to income tax and capital gains tax (CGT) in Australia. It examines the taxability of income derived from services, including media interviews and book publications, referencing relevant legislation such as the ITAA 1997 and case law like FCT v Scott and FCT v Brent. The assignment also explores the tax treatment of interest income from loans and the implications of selling assets, including land and buildings, under CGT rules. Furthermore, the solution analyzes scenarios involving property sales, providing calculations for capital gains and losses, and considers the tax implications for both individuals and companies. The document incorporates references to supporting legal principles and case precedents to justify its conclusions.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Answer to question 1:

Issue:

It is noteworthy to take into the consideration the issue that is associated with the

derivation of the money from the reward for service?

Laws:

a. “Section 6-1 of the ITAA 1997”

b. “Section 6-5 of the ITAA 1997”

c. “Scott v Commissioner of Taxation (1935)”

d. “section 15-2 of the ITAA 1997”

e. “Brent v Federal Commissioner of Taxation ATC 4195 (1971)”

f. “Housden (Inspector of Taxes) v Marshall (1958)”

g. “Hobbs v Hussey (1942) 24 TC 153”

Applications:

The private exertion income has been defined in the “S-1 of the ITA Act 1936”. It is

worth mentioning that when a taxpayer is earning income through the help of salaries or

wages or earning any kind of the payment through the business which a taxpayer executes

either alone or through the partners is classified as the private exertion income (Ostry, Berg

and Tsangarides 2014). Ordinary income is those income that is earned majorly earned by a

person with the help of ordinary concepts. The conceptual meaning of the ordinary income is

explained in “S-6-5 of the ITA Act 1997”. An important consideration should be paid

towards the law court decision in “FCT v Scott (1935)” (Anderson, Dickfos and Brown

2016). The explanation that has been made express that a person that earns income through

the help or ordinary means is an ordinary income under “S-6-5 of the ITA Act 1997”.

Answer to question 1:

Issue:

It is noteworthy to take into the consideration the issue that is associated with the

derivation of the money from the reward for service?

Laws:

a. “Section 6-1 of the ITAA 1997”

b. “Section 6-5 of the ITAA 1997”

c. “Scott v Commissioner of Taxation (1935)”

d. “section 15-2 of the ITAA 1997”

e. “Brent v Federal Commissioner of Taxation ATC 4195 (1971)”

f. “Housden (Inspector of Taxes) v Marshall (1958)”

g. “Hobbs v Hussey (1942) 24 TC 153”

Applications:

The private exertion income has been defined in the “S-1 of the ITA Act 1936”. It is

worth mentioning that when a taxpayer is earning income through the help of salaries or

wages or earning any kind of the payment through the business which a taxpayer executes

either alone or through the partners is classified as the private exertion income (Ostry, Berg

and Tsangarides 2014). Ordinary income is those income that is earned majorly earned by a

person with the help of ordinary concepts. The conceptual meaning of the ordinary income is

explained in “S-6-5 of the ITA Act 1997”. An important consideration should be paid

towards the law court decision in “FCT v Scott (1935)” (Anderson, Dickfos and Brown

2016). The explanation that has been made express that a person that earns income through

the help or ordinary means is an ordinary income under “S-6-5 of the ITA Act 1997”.

2TAXATION LAW

It is noteworthy to denote that “S-6-1 of the ITA Act 1936” provides an explanation

that private exertion earnings should be classified as statutory or the ordinary earnings (Vann

2016). It is very much important to consider that “S-15-2 of the ITA Act 1997” explains that

earnings will be held classified as chargeable earnings for the money that is obtained through

rendering of services of employment.

Apparently material evidences that is gained exclusively explains that Hilary was very

much a famous climber of mountain. As a result the Daily Terror Newspaper decided to give

Hilary $10,000 and required her to write the book by incorporating the story of her life.

Signifying the explanation of “S-6-5 of the ITA Act 1997” media interview money is a

chargeable income. It is noteworthy to give an important consideration that taxpayers are

only liable for taxation purpose if the money is paid for rendering the service (Australian

Taxation Office 2016). The explanation that has been provided by the law court in “FCT v

Brent (1971)” is related to the determination of the chargeable income for the services that is

provided to the media television where the wife of robber was liable for taxation for

obtaining the reward for service (Berg and Davidson 2016). Representing the elucidation of

“S-6-5 of the ITA Act 1997” media interview money that is received by the taxpayer is

chargeable income.

The case study provides the media publications of books and receiving the money for

such kind of publications by Hilary is a chargeable income. The explanation “FCT v Brent

(1971)” can be relevantly cited in Hilary’s case and a conclusive evidence can be drawn by

explaining that $10,000 for writing the books is taxable under the “S-6-5 of the ITA Act

1997” (Phillips and McKeown 2016). Referring to “S-1 of the ITA Act 1936” the sum of

$10,000 is a private exertion income for Hilary.

It is noteworthy to denote that “S-6-1 of the ITA Act 1936” provides an explanation

that private exertion earnings should be classified as statutory or the ordinary earnings (Vann

2016). It is very much important to consider that “S-15-2 of the ITA Act 1997” explains that

earnings will be held classified as chargeable earnings for the money that is obtained through

rendering of services of employment.

Apparently material evidences that is gained exclusively explains that Hilary was very

much a famous climber of mountain. As a result the Daily Terror Newspaper decided to give

Hilary $10,000 and required her to write the book by incorporating the story of her life.

Signifying the explanation of “S-6-5 of the ITA Act 1997” media interview money is a

chargeable income. It is noteworthy to give an important consideration that taxpayers are

only liable for taxation purpose if the money is paid for rendering the service (Australian

Taxation Office 2016). The explanation that has been provided by the law court in “FCT v

Brent (1971)” is related to the determination of the chargeable income for the services that is

provided to the media television where the wife of robber was liable for taxation for

obtaining the reward for service (Berg and Davidson 2016). Representing the elucidation of

“S-6-5 of the ITA Act 1997” media interview money that is received by the taxpayer is

chargeable income.

The case study provides the media publications of books and receiving the money for

such kind of publications by Hilary is a chargeable income. The explanation “FCT v Brent

(1971)” can be relevantly cited in Hilary’s case and a conclusive evidence can be drawn by

explaining that $10,000 for writing the books is taxable under the “S-6-5 of the ITA Act

1997” (Phillips and McKeown 2016). Referring to “S-1 of the ITA Act 1936” the sum of

$10,000 is a private exertion income for Hilary.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Hilary on the second instances was found to have sold the manuscripts of the books

and the photographs that was taken by her in the event of climbing the mountain. The

elucidation that was made by the law court in “Marshall v Housden (Inspector or

Taxation) (1958)” provides the taxability of the income when the taxpayer made the

photographs and the cuttings of newspaper available for sale (Bajada 2017). Therefore, the

court remained relied on the explanation of “S-6-5 of the ITA Act 1997” to stated that

money that is received from such sale is taxable based on ordinary perceptions.

Taking into the considerations the instances where an imaginary situation of assuming

that if the books was written by Hilary for her own private purpose then the outcome of such

sale of books would have accounted as the Royalty income. Relying on the reference of the

“Hussey v Hobbs (1942)” the taxpayer was held for assessment because the taxpayer sold

the rights of autobiographies for the publications purpose (Braithwaite 2017). The money that

was gained by the taxpayer from selling the books is a chargeable income based on the

ordinary perceptions of “S-6-5 of the ITA Act 1997” (Doidge and Dyck 2015). Equally, for

Hilary these income from the autobiography sale is taxable as the Royalty. The amount

should be viewed as the assessable based on ordinary perceptions of “S-6-5 of the ITA Act

1997”.

Conclusion:

A conclusion can be drawn by explaining that the three receipts that is earned by

Hilary is a private effort or private exertion income. This income would be classified as

chargeable based on the ordinary perceptions of “S-6-5 of the ITA Act 1997”. Alternatively

if she chooses to write the book herself then the sale of book would result in royalties for

Hilary that would be held taxable.

Hilary on the second instances was found to have sold the manuscripts of the books

and the photographs that was taken by her in the event of climbing the mountain. The

elucidation that was made by the law court in “Marshall v Housden (Inspector or

Taxation) (1958)” provides the taxability of the income when the taxpayer made the

photographs and the cuttings of newspaper available for sale (Bajada 2017). Therefore, the

court remained relied on the explanation of “S-6-5 of the ITA Act 1997” to stated that

money that is received from such sale is taxable based on ordinary perceptions.

Taking into the considerations the instances where an imaginary situation of assuming

that if the books was written by Hilary for her own private purpose then the outcome of such

sale of books would have accounted as the Royalty income. Relying on the reference of the

“Hussey v Hobbs (1942)” the taxpayer was held for assessment because the taxpayer sold

the rights of autobiographies for the publications purpose (Braithwaite 2017). The money that

was gained by the taxpayer from selling the books is a chargeable income based on the

ordinary perceptions of “S-6-5 of the ITA Act 1997” (Doidge and Dyck 2015). Equally, for

Hilary these income from the autobiography sale is taxable as the Royalty. The amount

should be viewed as the assessable based on ordinary perceptions of “S-6-5 of the ITA Act

1997”.

Conclusion:

A conclusion can be drawn by explaining that the three receipts that is earned by

Hilary is a private effort or private exertion income. This income would be classified as

chargeable based on the ordinary perceptions of “S-6-5 of the ITA Act 1997”. Alternatively

if she chooses to write the book herself then the sale of book would result in royalties for

Hilary that would be held taxable.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

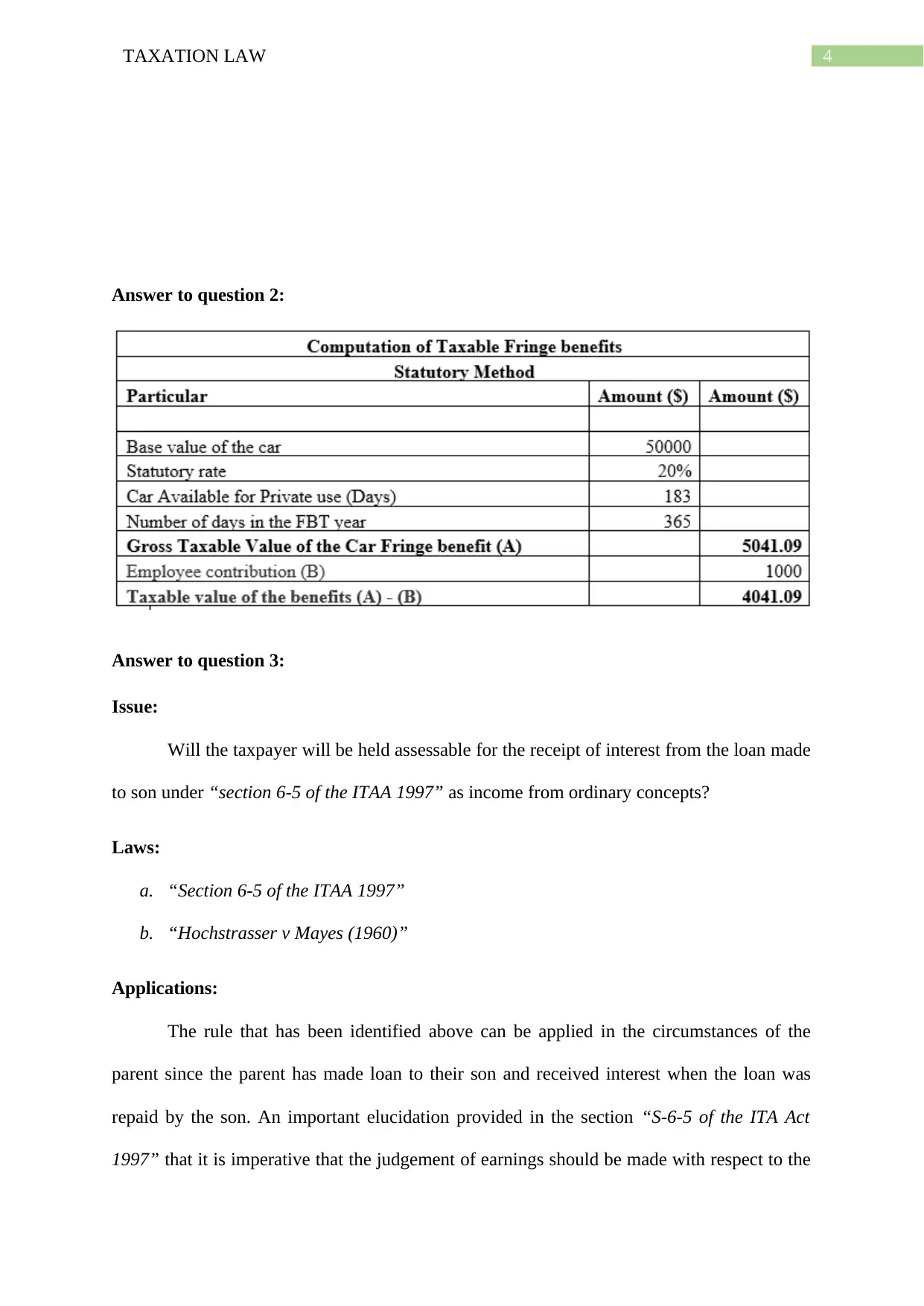

Answer to question 2:

Answer to question 3:

Issue:

Will the taxpayer will be held assessable for the receipt of interest from the loan made

to son under “section 6-5 of the ITAA 1997” as income from ordinary concepts?

Laws:

a. “Section 6-5 of the ITAA 1997”

b. “Hochstrasser v Mayes (1960)”

Applications:

The rule that has been identified above can be applied in the circumstances of the

parent since the parent has made loan to their son and received interest when the loan was

repaid by the son. An important elucidation provided in the section “S-6-5 of the ITA Act

1997” that it is imperative that the judgement of earnings should be made with respect to the

Answer to question 2:

Answer to question 3:

Issue:

Will the taxpayer will be held assessable for the receipt of interest from the loan made

to son under “section 6-5 of the ITAA 1997” as income from ordinary concepts?

Laws:

a. “Section 6-5 of the ITAA 1997”

b. “Hochstrasser v Mayes (1960)”

Applications:

The rule that has been identified above can be applied in the circumstances of the

parent since the parent has made loan to their son and received interest when the loan was

repaid by the son. An important elucidation provided in the section “S-6-5 of the ITA Act

1997” that it is imperative that the judgement of earnings should be made with respect to the

5TAXATION LAW

surroundings of derivation (Tran-Nam and Walpole 2016). The law court has relied on the

principles that was explained in “Mayes v Hochstrasser (1960)” that to hold the income

character it should be classified as gain.

As evident in the current situation a loan was provided by the parent to the son as the

short term housing loan based on the agreement that the son would be paying the principle

amount following the end of the five years. Though the parents of son did not charged any

interest from the son but the sum was paid by son inside two years along with the interest

payment (Scholes 2015). By remaining reliant on the principles of the “S-6-5 of the ITA Act

1997” the homecoming of income carries the element of the income based on the notion of

ordinary concepts. An individual is considered to have received the amount as soon as the

sum is received or dealt in on behalf of the individual that directs it.

Preceding the explanation of the “S-6-5 of the ITA Act 1997” the parents have

received the interest income for the loans made to son and the interest amount is a chargeable

income (Heider and Ljungqvist 2015). This is because the receipt of interest possessed the

character of income and constituted a gain by the taxpayer. However, the repayment of

principle loan amount is not assessable since it constituted capital for the parents. By

remaining reliant on the principles of the “S-6-5 of the ITA Act 1997” the interest must be

classified as income which would attract tax liability (Slemrod and Bakija 2017). Citing the

reference of the “Hochstrasser v Mayes (1960)” the interest income had the character of

income and should be held as the element of gain for the taxpayer.

Conclusion:

On a conclusive note, the receipt of interest constituted an element of gain which is

considered as the taxable income under “section 6-5 of the ITAA 1997”. The amount was

surroundings of derivation (Tran-Nam and Walpole 2016). The law court has relied on the

principles that was explained in “Mayes v Hochstrasser (1960)” that to hold the income

character it should be classified as gain.

As evident in the current situation a loan was provided by the parent to the son as the

short term housing loan based on the agreement that the son would be paying the principle

amount following the end of the five years. Though the parents of son did not charged any

interest from the son but the sum was paid by son inside two years along with the interest

payment (Scholes 2015). By remaining reliant on the principles of the “S-6-5 of the ITA Act

1997” the homecoming of income carries the element of the income based on the notion of

ordinary concepts. An individual is considered to have received the amount as soon as the

sum is received or dealt in on behalf of the individual that directs it.

Preceding the explanation of the “S-6-5 of the ITA Act 1997” the parents have

received the interest income for the loans made to son and the interest amount is a chargeable

income (Heider and Ljungqvist 2015). This is because the receipt of interest possessed the

character of income and constituted a gain by the taxpayer. However, the repayment of

principle loan amount is not assessable since it constituted capital for the parents. By

remaining reliant on the principles of the “S-6-5 of the ITA Act 1997” the interest must be

classified as income which would attract tax liability (Slemrod and Bakija 2017). Citing the

reference of the “Hochstrasser v Mayes (1960)” the interest income had the character of

income and should be held as the element of gain for the taxpayer.

Conclusion:

On a conclusive note, the receipt of interest constituted an element of gain which is

considered as the taxable income under “section 6-5 of the ITAA 1997”. The amount was

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

paid by the son to the parents three years before the prescribed time with an additional 5 per

cent for the sum that was borrowed.

Answer to question 4:

Answer to A:

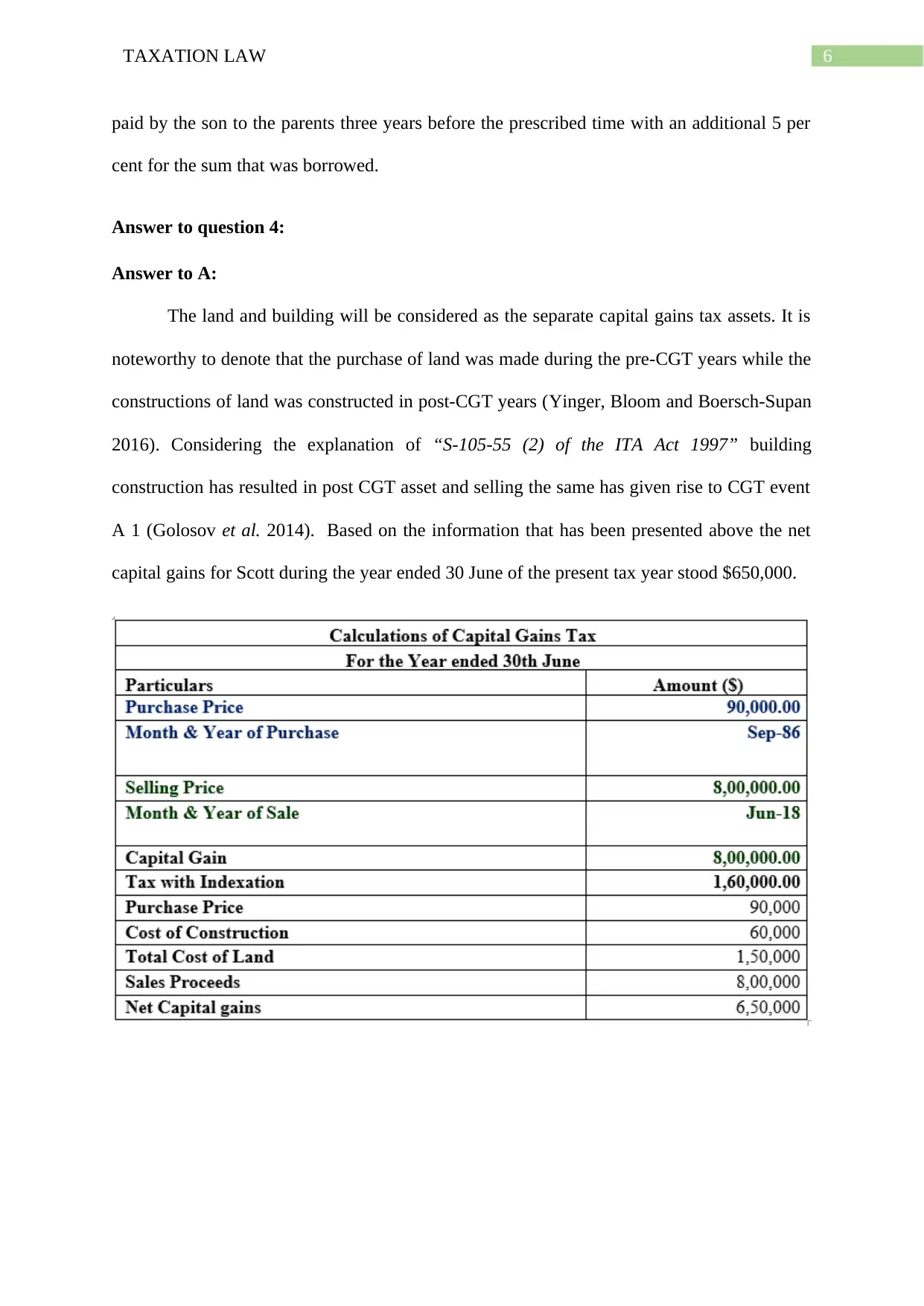

The land and building will be considered as the separate capital gains tax assets. It is

noteworthy to denote that the purchase of land was made during the pre-CGT years while the

constructions of land was constructed in post-CGT years (Yinger, Bloom and Boersch-Supan

2016). Considering the explanation of “S-105-55 (2) of the ITA Act 1997” building

construction has resulted in post CGT asset and selling the same has given rise to CGT event

A 1 (Golosov et al. 2014). Based on the information that has been presented above the net

capital gains for Scott during the year ended 30 June of the present tax year stood $650,000.

paid by the son to the parents three years before the prescribed time with an additional 5 per

cent for the sum that was borrowed.

Answer to question 4:

Answer to A:

The land and building will be considered as the separate capital gains tax assets. It is

noteworthy to denote that the purchase of land was made during the pre-CGT years while the

constructions of land was constructed in post-CGT years (Yinger, Bloom and Boersch-Supan

2016). Considering the explanation of “S-105-55 (2) of the ITA Act 1997” building

construction has resulted in post CGT asset and selling the same has given rise to CGT event

A 1 (Golosov et al. 2014). Based on the information that has been presented above the net

capital gains for Scott during the year ended 30 June of the present tax year stood $650,000.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

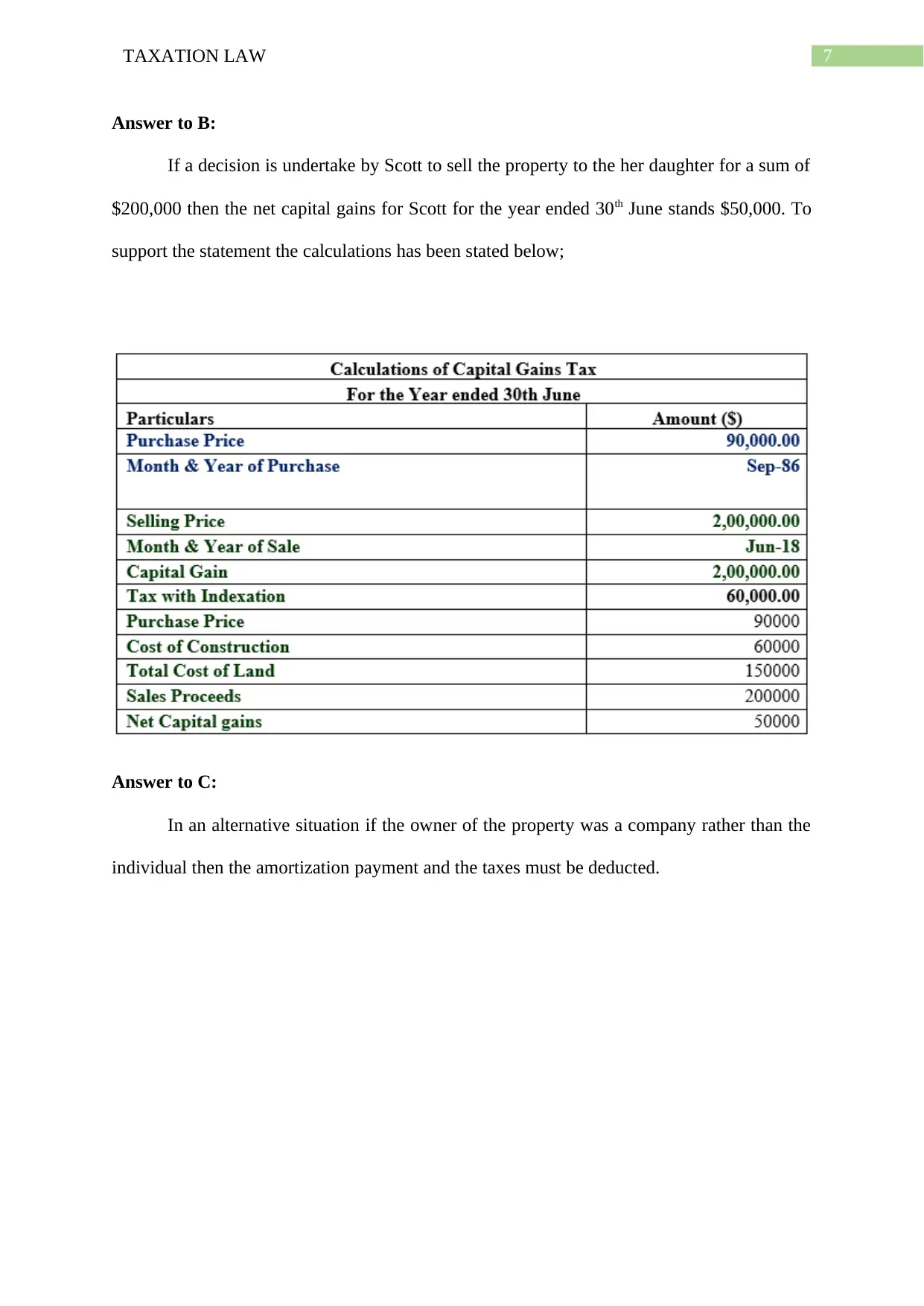

Answer to B:

If a decision is undertake by Scott to sell the property to the her daughter for a sum of

$200,000 then the net capital gains for Scott for the year ended 30th June stands $50,000. To

support the statement the calculations has been stated below;

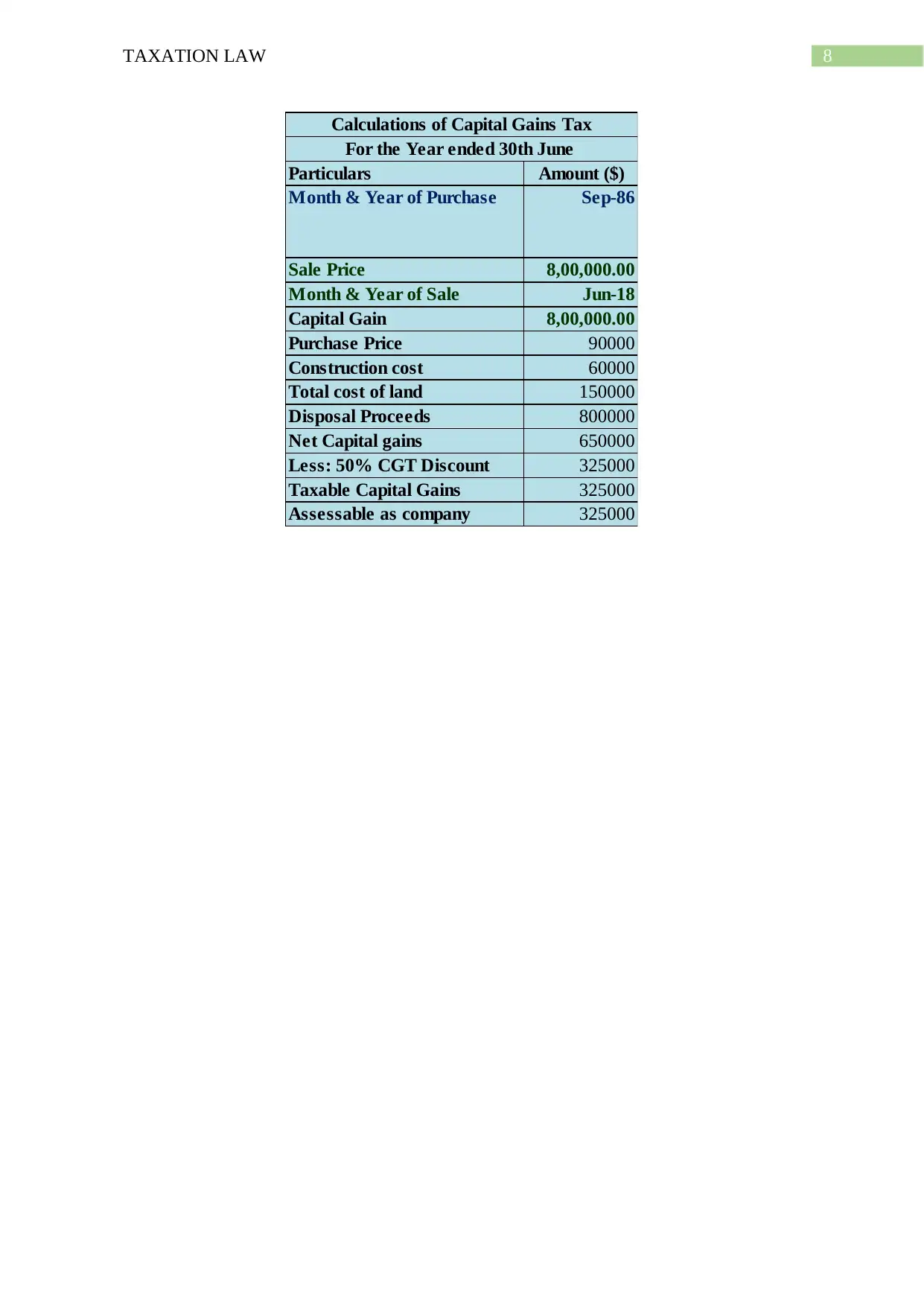

Answer to C:

In an alternative situation if the owner of the property was a company rather than the

individual then the amortization payment and the taxes must be deducted.

Answer to B:

If a decision is undertake by Scott to sell the property to the her daughter for a sum of

$200,000 then the net capital gains for Scott for the year ended 30th June stands $50,000. To

support the statement the calculations has been stated below;

Answer to C:

In an alternative situation if the owner of the property was a company rather than the

individual then the amortization payment and the taxes must be deducted.

8TAXATION LAW

Particulars Amount ($)

Month & Year of Purchase Sep-86

Sale Price 8,00,000.00

Month & Year of Sale Jun-18

Capital Gain 8,00,000.00

Purchase Price 90000

Construction cost 60000

Total cost of land 150000

Disposal Proceeds 800000

Net Capital gains 650000

Less: 50% CGT Discount 325000

Taxable Capital Gains 325000

Assessable as company 325000

Calculations of Capital Gains Tax

For the Year ended 30th June

Particulars Amount ($)

Month & Year of Purchase Sep-86

Sale Price 8,00,000.00

Month & Year of Sale Jun-18

Capital Gain 8,00,000.00

Purchase Price 90000

Construction cost 60000

Total cost of land 150000

Disposal Proceeds 800000

Net Capital gains 650000

Less: 50% CGT Discount 325000

Taxable Capital Gains 325000

Assessable as company 325000

Calculations of Capital Gains Tax

For the Year ended 30th June

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Reference List:

Anderson, C., Dickfos, J. and Brown, C., 2016. The Australian Taxation Office-what role

does it play in anti-phoenix activity?. Insolvency Law Journal, 24(2), pp.127-140.

Australian Taxation Office (ATO), 2016. Self-Managed Super Fund Statistical Report.

(March 2016).

Bajada, C., 2017. Australia's Cash Economy: A Troubling Issue for Policymakers: A

Troubling Issue for Policymakers.

Berg, C. and Davidson, S., 2016. Submission to the House of Representatives Standing

Committee on Tax and Revenue Inquiry into the External Scrutiny of the Australian Taxation

Office.

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Doidge, C. and Dyck, A., 2015. Taxes and corporate policies: Evidence from a quasi natural

experiment. The Journal of Finance, 70(1), pp.45-89.

Golosov, M., Hassler, J., Krusell, P. and Tsyvinski, A., 2014. Optimal taxes on fossil fuel in

general equilibrium. Econometrica, 82(1), pp.41-88.

Heider, F. and Ljungqvist, A., 2015. As certain as debt and taxes: Estimating the tax

sensitivity of leverage from state tax changes. Journal of Financial Economics, 118(3),

pp.684-712.

Ostry, M.J.D., Berg, M.A. and Tsangarides, M.C.G., 2014. Redistribution, inequality, and

growth. International Monetary Fund.

Reference List:

Anderson, C., Dickfos, J. and Brown, C., 2016. The Australian Taxation Office-what role

does it play in anti-phoenix activity?. Insolvency Law Journal, 24(2), pp.127-140.

Australian Taxation Office (ATO), 2016. Self-Managed Super Fund Statistical Report.

(March 2016).

Bajada, C., 2017. Australia's Cash Economy: A Troubling Issue for Policymakers: A

Troubling Issue for Policymakers.

Berg, C. and Davidson, S., 2016. Submission to the House of Representatives Standing

Committee on Tax and Revenue Inquiry into the External Scrutiny of the Australian Taxation

Office.

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Doidge, C. and Dyck, A., 2015. Taxes and corporate policies: Evidence from a quasi natural

experiment. The Journal of Finance, 70(1), pp.45-89.

Golosov, M., Hassler, J., Krusell, P. and Tsyvinski, A., 2014. Optimal taxes on fossil fuel in

general equilibrium. Econometrica, 82(1), pp.41-88.

Heider, F. and Ljungqvist, A., 2015. As certain as debt and taxes: Estimating the tax

sensitivity of leverage from state tax changes. Journal of Financial Economics, 118(3),

pp.684-712.

Ostry, M.J.D., Berg, M.A. and Tsangarides, M.C.G., 2014. Redistribution, inequality, and

growth. International Monetary Fund.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Phillips, K. and McKeown, T., 2016. Understanding Self-Employment: The Opportunities

and the Challenges for Good Policy. Government, SMEs and Entrepreneurship Development:

Policy, Practice and Challenges, p.157.

Scholes, M.S., 2015. Taxes and business strategy. Prentice Hall.

Slemrod, J. and Bakija, J., 2017. Taxing ourselves: a citizen's guide to the debate over taxes.

MIt Press.

Tran-Nam, B. and Walpole, M., 2016. Tax disputes, litigation costs and access to tax

justice. eJournal of Tax Research, 14(2), p.319.

Vann, R., 2016. Hybrid Entities in Australia: Resource Capital Fund III LP Case.

Yinger, J., Bloom, H.S. and Boersch-Supan, A., 2016. Property taxes and house values: The

theory and estimation of intrajurisdictional property tax capitalization. Elsevier.

Phillips, K. and McKeown, T., 2016. Understanding Self-Employment: The Opportunities

and the Challenges for Good Policy. Government, SMEs and Entrepreneurship Development:

Policy, Practice and Challenges, p.157.

Scholes, M.S., 2015. Taxes and business strategy. Prentice Hall.

Slemrod, J. and Bakija, J., 2017. Taxing ourselves: a citizen's guide to the debate over taxes.

MIt Press.

Tran-Nam, B. and Walpole, M., 2016. Tax disputes, litigation costs and access to tax

justice. eJournal of Tax Research, 14(2), p.319.

Vann, R., 2016. Hybrid Entities in Australia: Resource Capital Fund III LP Case.

Yinger, J., Bloom, H.S. and Boersch-Supan, A., 2016. Property taxes and house values: The

theory and estimation of intrajurisdictional property tax capitalization. Elsevier.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.