Taxation Law Assignment: Income, Deductions, and Tax for 2018

VerifiedAdded on 2023/01/03

|7

|1131

|24

Homework Assignment

AI Summary

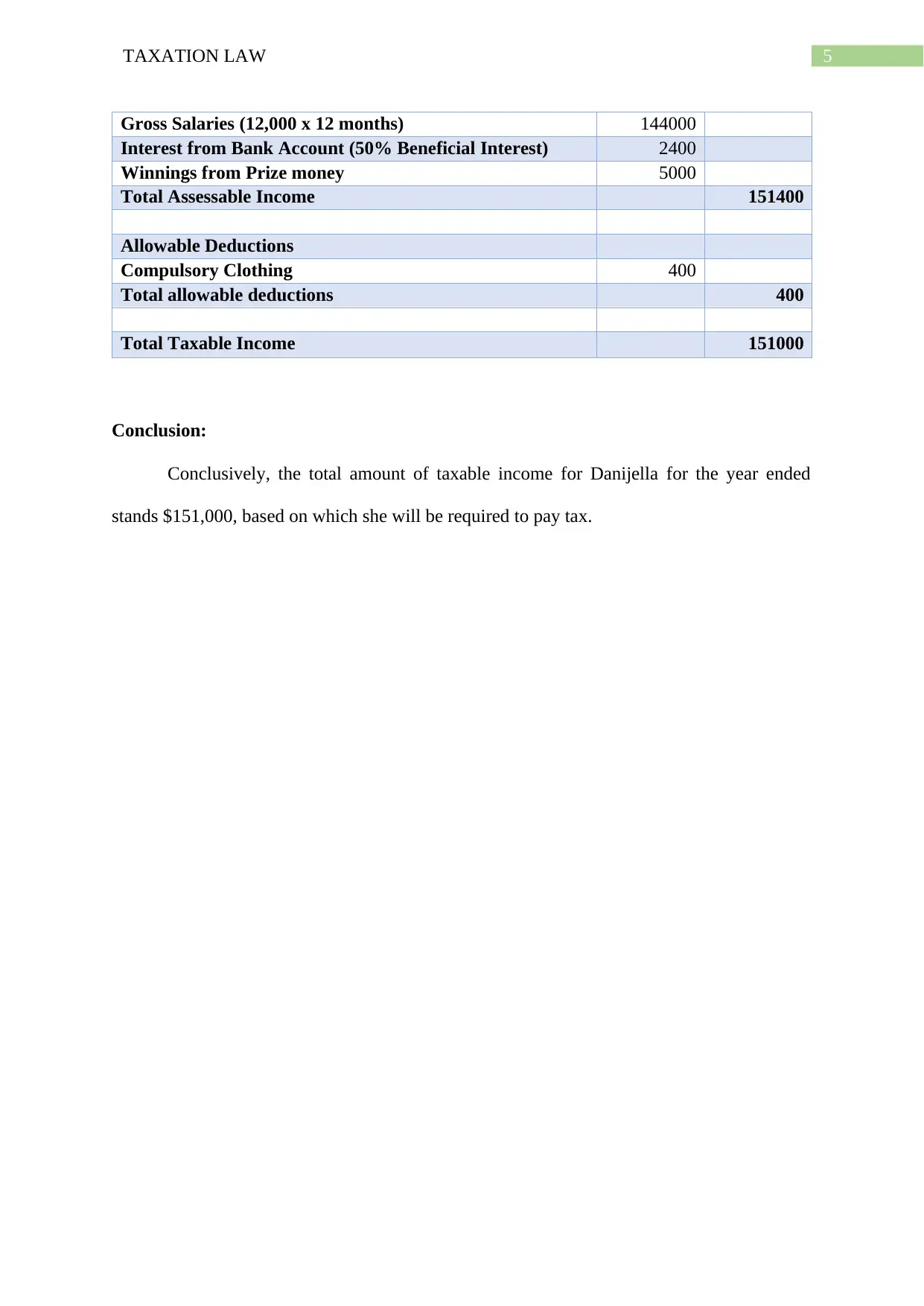

This assignment addresses the tax implications for Danijela, an IT manager, in the 2018 income tax year. It examines various sources of income, including salary, interest, and prize money, determining their assessability under relevant tax laws like ITAA 1997 and ITAA 1936. The solution analyzes allowable deductions, such as expenses for compulsory work clothing, while denying deductions for items like tax advice and self-education. It also covers capital gains and losses from the sale of personal-use assets. The assignment applies relevant case law, including Scott v CT, FCT v Stone, and FCT v Edwards, to support its conclusions and calculates Danijela's total taxable income for the year, providing a comprehensive overview of her tax liabilities.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.