Taxation Law: Emily Buff's Tax Liability and Recommendations

VerifiedAdded on 2021/06/18

|7

|953

|59

Homework Assignment

AI Summary

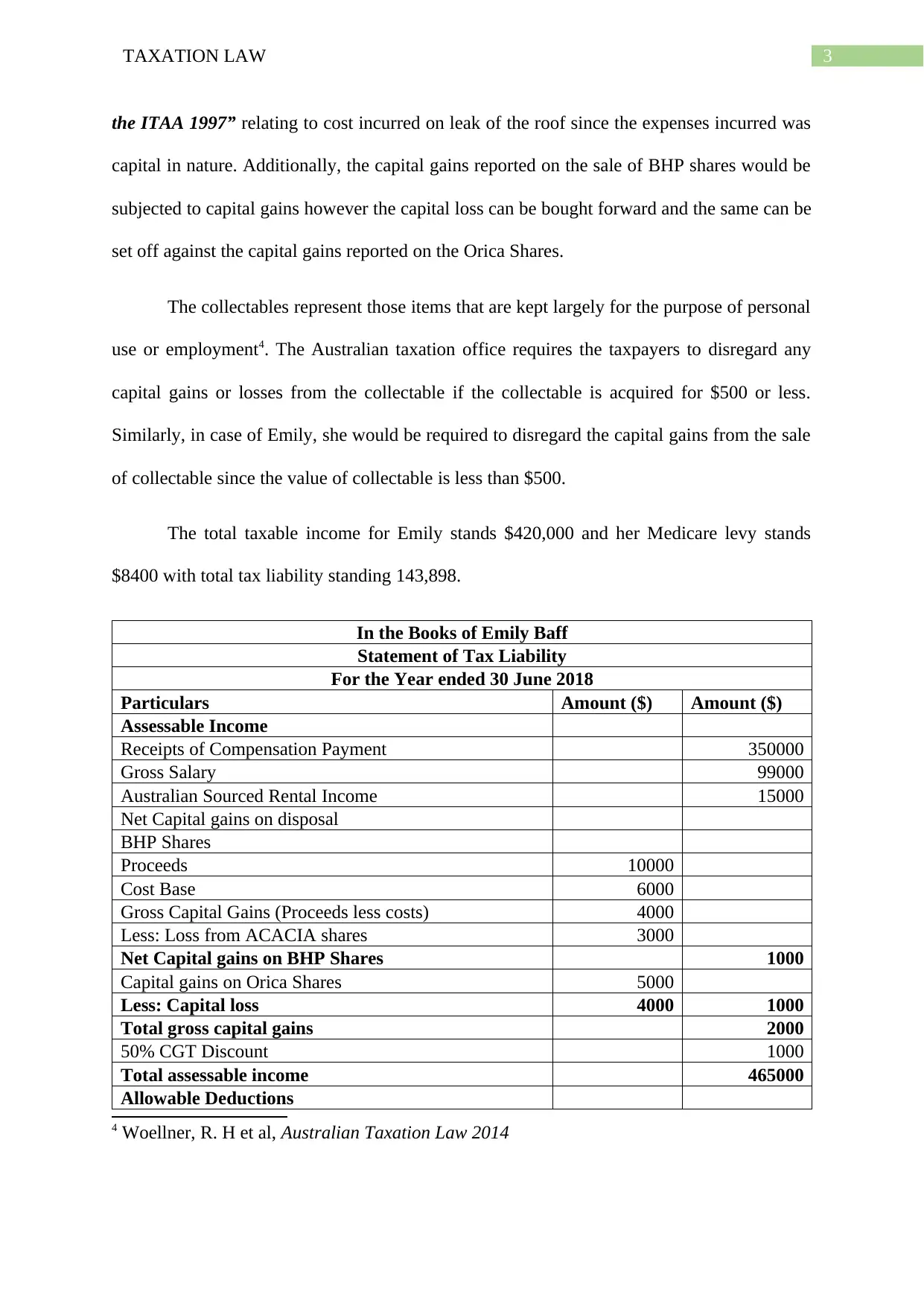

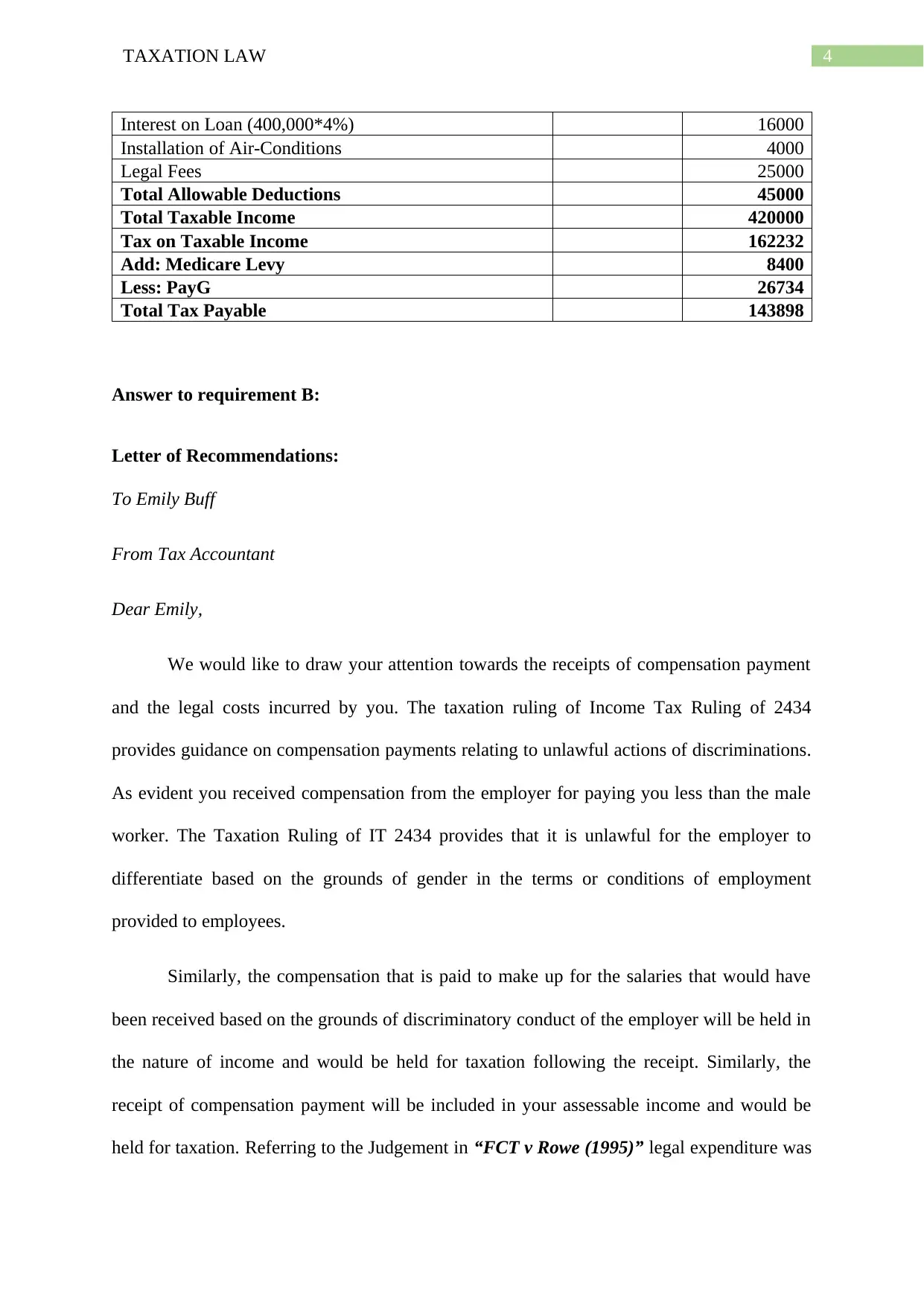

This assignment solution analyzes Emily Buff's tax liability, encompassing assessable income, allowable deductions, and tax payable for the year ending June 30, 2018. The solution addresses various aspects of taxation law, including deductions related to investment properties (interest, air conditioner installation, legal fees), capital gains tax on the sale of BHP and Orica shares, and the treatment of collectables. It also examines the tax implications of a compensation payment received by Emily, referencing relevant taxation rulings and legal precedents. The assignment provides a detailed breakdown of Emily's tax calculation, including her taxable income, Medicare levy, and total tax liability. Furthermore, it includes a letter of recommendation from a tax accountant offering guidance on the compensation payment and legal expenses, citing relevant sections of the ITAA 1997 and case law. The solution concludes with a comprehensive reference list of taxation law resources.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.