Taxation Law Assignment: Bruce Lee's Tax Liability Calculation

VerifiedAdded on 2023/06/08

|12

|2700

|303

Homework Assignment

AI Summary

This assignment provides a comprehensive analysis of Bruce Lee's tax liability for the year ended June 30, 2018, as a lawyer with his own legal practice. The assignment meticulously examines various sources of income, including professional legal fees, rental income, dividends, and interest, determining their assessability under the ITAA 1997. It also details the calculation of taxable income, considering allowable deductions such as office rent, salary payments, and tax agent fees. The assignment also covers specific tax implications related to capital gains from the sale of office equipment, and the treatment of expenses related to his investment property, like rates and interest payments, as well as the impact of carry-forward losses and franking credits. The solution provides a detailed computation of tax liability, culminating in the calculation of total tax payable, offering a practical application of taxation law principles.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

The ordinary income represents the income under the ordinary concepts and hence it

is considered taxable under “section 6-5 of the ITAA 1997”. The taxation official in “Scott v

CT (1935)” held that income should be ascertained in compliance with the normal

perceptions and use of mankind (Woellner et al. 2016). “Section 6-5” states that gains

originating from performing of business activities is held as ordinary income. The present

case study is based on determining the income tax liability for Bruce and determining

allowable deductions to lower the income tax liability. To characterize receipts as the

ordinary income from the commercial action consist of determining whether the taxpayers is

carrying on the activities of business or whether the considerations of earnings are treated as

ordinary incomes from that commercial activity.

As per “section 6-1 of the ITAA 1997” deriving proceeds from the personal effort

represents revenue comprising of salaries, pays and wages (Braithwaite 2017). “Section 6-1

of the ITAA 1997” also includes proceeds that a taxpayer obtains from the business that is

conducted alone or as partners. The case facts reveal the transaction reported by Bruce

originating from the receipt of professional legal fees. The professional legal fees constitute

receipts from the normal proceeds of the business activity. The professional receipts would be

characterized as ordinary income from the business carried on.

Agreeing to the “section 6-5 of the ITAA 1997” any revenues originating from the

person service of the taxpayer does not represents ordinary income (Blakelock and King

2017). As held in “FCT v Brent (1971)” receipt of lump-sum or the one-off receipts for the

performance of specific tax is held as normal revenue. Quoting the reference of “section 6-5

of the ITAA 1997” receipts from the property is held as income (Edmonds 2018). The receipt

Answer to question 1:

The ordinary income represents the income under the ordinary concepts and hence it

is considered taxable under “section 6-5 of the ITAA 1997”. The taxation official in “Scott v

CT (1935)” held that income should be ascertained in compliance with the normal

perceptions and use of mankind (Woellner et al. 2016). “Section 6-5” states that gains

originating from performing of business activities is held as ordinary income. The present

case study is based on determining the income tax liability for Bruce and determining

allowable deductions to lower the income tax liability. To characterize receipts as the

ordinary income from the commercial action consist of determining whether the taxpayers is

carrying on the activities of business or whether the considerations of earnings are treated as

ordinary incomes from that commercial activity.

As per “section 6-1 of the ITAA 1997” deriving proceeds from the personal effort

represents revenue comprising of salaries, pays and wages (Braithwaite 2017). “Section 6-1

of the ITAA 1997” also includes proceeds that a taxpayer obtains from the business that is

conducted alone or as partners. The case facts reveal the transaction reported by Bruce

originating from the receipt of professional legal fees. The professional legal fees constitute

receipts from the normal proceeds of the business activity. The professional receipts would be

characterized as ordinary income from the business carried on.

Agreeing to the “section 6-5 of the ITAA 1997” any revenues originating from the

person service of the taxpayer does not represents ordinary income (Blakelock and King

2017). As held in “FCT v Brent (1971)” receipt of lump-sum or the one-off receipts for the

performance of specific tax is held as normal revenue. Quoting the reference of “section 6-5

of the ITAA 1997” receipts from the property is held as income (Edmonds 2018). The receipt

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

of $25,000 from the 10-year lease constitute a one-off receipt. Therefore, the one-off lease

receipts would be treated as ordinary proceeds and forms the part of taxable proceeds.

According to the Australian Taxation Office irrespective of a person has a single or

more employment or working as full time or part-time, the individual taxpayer is obligatorily

required to declare such income from employment while filing tax return. As held in “FCT v

Dean (1997)” receipts from employment is held as chargeable wages (Neil et al. 2015).

Receipts of salary by Bruce from the part time lecture in university constitute income from

employment. The receipts would be held taxable under ordinary concepts of “section 6-5”.

According to “section 44 (1) of the ITAA 1997” taxpayers are required to declare

dividend income in their tax return. Dividends are usually received from the investment in

listed entities, trust that trades publicly and corporate unit trust (McLaren and Cormick 2018).

Certain dividends have franking credits enclosed in it and a taxpayer can claim set-off from

their tax return. Dividends received by Bruce from the Australian sourced investment forms

the part of chargeable earnings and the franking credit can be set-off to reduce the tax

liability.

The federal court in “Dixon v FCT (1952)” held that periodic receipts represents an

income stream i.e., amount paid periodically (Davies and Wheelahan 2018). Any form of

gain which is period is probably held as ordinary income. In “Blake v FCT (1984)” regular

receipt is categorized as earnings in nature. Rental income from investment property received

by Bruce would be held as assessable income because it carries adequate nexus with the

income making activity.

An Australian resident that receives interest from the financial bank account or term

deposits would be considered as income. Receipts of interest from the bank account or term

deposits is held as taxable earnings (Swan 2018). The tax liability originates when a taxpayer

of $25,000 from the 10-year lease constitute a one-off receipt. Therefore, the one-off lease

receipts would be treated as ordinary proceeds and forms the part of taxable proceeds.

According to the Australian Taxation Office irrespective of a person has a single or

more employment or working as full time or part-time, the individual taxpayer is obligatorily

required to declare such income from employment while filing tax return. As held in “FCT v

Dean (1997)” receipts from employment is held as chargeable wages (Neil et al. 2015).

Receipts of salary by Bruce from the part time lecture in university constitute income from

employment. The receipts would be held taxable under ordinary concepts of “section 6-5”.

According to “section 44 (1) of the ITAA 1997” taxpayers are required to declare

dividend income in their tax return. Dividends are usually received from the investment in

listed entities, trust that trades publicly and corporate unit trust (McLaren and Cormick 2018).

Certain dividends have franking credits enclosed in it and a taxpayer can claim set-off from

their tax return. Dividends received by Bruce from the Australian sourced investment forms

the part of chargeable earnings and the franking credit can be set-off to reduce the tax

liability.

The federal court in “Dixon v FCT (1952)” held that periodic receipts represents an

income stream i.e., amount paid periodically (Davies and Wheelahan 2018). Any form of

gain which is period is probably held as ordinary income. In “Blake v FCT (1984)” regular

receipt is categorized as earnings in nature. Rental income from investment property received

by Bruce would be held as assessable income because it carries adequate nexus with the

income making activity.

An Australian resident that receives interest from the financial bank account or term

deposits would be considered as income. Receipts of interest from the bank account or term

deposits is held as taxable earnings (Swan 2018). The tax liability originates when a taxpayer

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

is required to include the interest income in their taxable return. Similarly, the receipt of

interest from bank by Bruce would be treated as the assessable income and are liable for

taxation.

As explained in “section 108-5 of the ITAA 1997”, CGT asset signifies any form of

property. The sale of office equipment lead to capital gain and the profits from such sale

would be treated as capital gains tax (Burton 2018). The profit forms the part of taxable

return and would be treated as ordinary earnings under “section 6-5 of the ITAA 1997”.

“Section 8-1” carries the potential of being applied to any taxpayer. A losses or

outgoings might be held deductible under the general provision of “section 8-1” (Miller and

Oats 2016). The two positive limbs of “section 8-1”explain that a person can subtract from

their taxable proceeds any loss or expenditures that is occurred in making the taxpayer’s

earnings. However, a taxpayer is prohibited to deduct any losses under the negative limbs of

“section 8-1 (2)” if the expenses are capital, domestic or private in nature.

Bruce reports outgoings related to office rent, cleaning contractor and payment of

salary to employee. As held in “FCT v Amalgamated Zinc Ltd (1935)” expenses incurred in

producing or gaining taxable income is considered deductible under the positive limbs of

“section 8-1 of the ITAA 1997” (James and Nobes 2016). Similarly, the expenses on office

rent, cleaning contractor and staff salary payment are expenses incurred in producing or

gaining taxable income and deductible within the positive limbs of “section 8-1”.

The Australian taxation office states that expenses incurred in purchase of equipment,

tools and any other assets that directly forms the part of earning income, the taxpayer is

allowed to claim deductions for the cost as a whole or in parts of such equipment (Cao,

Chapple and Sadiq 2014). An item of equipment costing less than $300 can be immediately

is required to include the interest income in their taxable return. Similarly, the receipt of

interest from bank by Bruce would be treated as the assessable income and are liable for

taxation.

As explained in “section 108-5 of the ITAA 1997”, CGT asset signifies any form of

property. The sale of office equipment lead to capital gain and the profits from such sale

would be treated as capital gains tax (Burton 2018). The profit forms the part of taxable

return and would be treated as ordinary earnings under “section 6-5 of the ITAA 1997”.

“Section 8-1” carries the potential of being applied to any taxpayer. A losses or

outgoings might be held deductible under the general provision of “section 8-1” (Miller and

Oats 2016). The two positive limbs of “section 8-1”explain that a person can subtract from

their taxable proceeds any loss or expenditures that is occurred in making the taxpayer’s

earnings. However, a taxpayer is prohibited to deduct any losses under the negative limbs of

“section 8-1 (2)” if the expenses are capital, domestic or private in nature.

Bruce reports outgoings related to office rent, cleaning contractor and payment of

salary to employee. As held in “FCT v Amalgamated Zinc Ltd (1935)” expenses incurred in

producing or gaining taxable income is considered deductible under the positive limbs of

“section 8-1 of the ITAA 1997” (James and Nobes 2016). Similarly, the expenses on office

rent, cleaning contractor and staff salary payment are expenses incurred in producing or

gaining taxable income and deductible within the positive limbs of “section 8-1”.

The Australian taxation office states that expenses incurred in purchase of equipment,

tools and any other assets that directly forms the part of earning income, the taxpayer is

allowed to claim deductions for the cost as a whole or in parts of such equipment (Cao,

Chapple and Sadiq 2014). An item of equipment costing less than $300 can be immediately

5TAXATION LAW

claimed as deductions. The purchase of calculator for business use purpose can be claimed

for deductions immediately since its cost base is lower than $300.

As defined by ATO meals to clients are treated as business entertainment expenses.

Similarly, the expenses incurred by Bruce for entertaining the client with food would be

treated as allowable business deductions (Pinto, Kendall and Sadiq 2015). However, the meal

expenses incurred by Bruce upon himself does not qualifies as deductions under “section 8-

1” since it is a private expenditure.

The general rule in “FCT v Lunney” states that expenditure that is incurred by the

taxpayer for travelling between the taxpayer’s home and regular place of work is non-

deductible expenditure (White and Townsend 2018). The statutory provision of “section 25-

100” provides interpretation that deductions is allowed to the taxpayer for the purpose of

travelling directly between two places of work where the taxpayer is engaged in producing

income. The common law in “Payne v FCT (2001)” states that travel between unconnected

places of work is not permitted for deductions under “section 8-1”. As obvious Bruce reports

expenses for travel between home and workplace. Therefore, based on common law Bruce

would not be allowed to claim deductions for travel between home and workplace as it is a

private expense.

Expenditure incurred by the taxpayer is not considered permissible deductions given

the expenses meets any one of the negative limbs. As stated under “section 8-1 (2) (b) of the

ITAA 1997” costs that are entirely domestic or private in character is non-allowable

deductions because these expenses do not meet any of the positive limbs criteria (Woellner et

al. 2016). Expenses reported by Bruce on rates, electricity for their family home does not

qualify the deductible conditions of either one of positive limbs. Therefore, Bruce would not

be permitted to claim for an allowable deduction under “section 8-1 of the ITAA 1997”.

claimed as deductions. The purchase of calculator for business use purpose can be claimed

for deductions immediately since its cost base is lower than $300.

As defined by ATO meals to clients are treated as business entertainment expenses.

Similarly, the expenses incurred by Bruce for entertaining the client with food would be

treated as allowable business deductions (Pinto, Kendall and Sadiq 2015). However, the meal

expenses incurred by Bruce upon himself does not qualifies as deductions under “section 8-

1” since it is a private expenditure.

The general rule in “FCT v Lunney” states that expenditure that is incurred by the

taxpayer for travelling between the taxpayer’s home and regular place of work is non-

deductible expenditure (White and Townsend 2018). The statutory provision of “section 25-

100” provides interpretation that deductions is allowed to the taxpayer for the purpose of

travelling directly between two places of work where the taxpayer is engaged in producing

income. The common law in “Payne v FCT (2001)” states that travel between unconnected

places of work is not permitted for deductions under “section 8-1”. As obvious Bruce reports

expenses for travel between home and workplace. Therefore, based on common law Bruce

would not be allowed to claim deductions for travel between home and workplace as it is a

private expense.

Expenditure incurred by the taxpayer is not considered permissible deductions given

the expenses meets any one of the negative limbs. As stated under “section 8-1 (2) (b) of the

ITAA 1997” costs that are entirely domestic or private in character is non-allowable

deductions because these expenses do not meet any of the positive limbs criteria (Woellner et

al. 2016). Expenses reported by Bruce on rates, electricity for their family home does not

qualify the deductible conditions of either one of positive limbs. Therefore, Bruce would not

be permitted to claim for an allowable deduction under “section 8-1 of the ITAA 1997”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

“Section 8-5 of the ITAA 1997” defines that specific deductions originates when

there is a specific provision in the income tax legislation offers deductions to the taxpayers

(Edmonds 2018). As stated under “section 25-5” a taxpayer is permitted to an allowable

deduction for certain costs including the expenses incurred in managing the tax affairs. The

tax agent fees incurred by Bruce for preparing the tax return qualifies for the specific

deductions under “section 25-5 of the ITAA 1997”.

A taxpayer is permitted to claim deductions for expenses that is occurred when the

rental property is available for rent or it is rented out. Bruce reports expenditure on rates

incurred in rental property and also reported interest on loan incurred in acquiring the rental

property (Pinto, Kendall and Sadiq 2015). Mentioning the decision in “Amalgamated Zinc

Ltd v FCT (1935)” Bruce can claim deductions under “section 8-1 of the ITAA 1997” on

rates and interest incurred on the rental property since these expenses are incurred in

producing the assessable rental income.

“Section 25-10 of the ITAA 1997” prohibits a taxpayer from claiming deductions

relating to cost incurred on notional repair. As held in “Inland Revenue Commissioners v

Shipping Co Ltd (1923)” a taxpayer that undertakes the initial repair to correct the defects

that was present while acquiring the property is treated as expenses of capital in nature and no

deductions is allowed. Bruce reports cost for repainting the investment property (James and

Nobes 2016). These costs can be treated as capital expenses which is occurred to remedy the

defects present in the property prior to subletting. These expenses do not arise from Bruce

own use of property to obtain the rental earnings. Hence, no deductions are allowed in this

circumstances.

As per “Section 25-10” a taxpayer is allowed to an entitlement of permissible

deduction for spending that is happened in replacing a portion of investment property that is

“Section 8-5 of the ITAA 1997” defines that specific deductions originates when

there is a specific provision in the income tax legislation offers deductions to the taxpayers

(Edmonds 2018). As stated under “section 25-5” a taxpayer is permitted to an allowable

deduction for certain costs including the expenses incurred in managing the tax affairs. The

tax agent fees incurred by Bruce for preparing the tax return qualifies for the specific

deductions under “section 25-5 of the ITAA 1997”.

A taxpayer is permitted to claim deductions for expenses that is occurred when the

rental property is available for rent or it is rented out. Bruce reports expenditure on rates

incurred in rental property and also reported interest on loan incurred in acquiring the rental

property (Pinto, Kendall and Sadiq 2015). Mentioning the decision in “Amalgamated Zinc

Ltd v FCT (1935)” Bruce can claim deductions under “section 8-1 of the ITAA 1997” on

rates and interest incurred on the rental property since these expenses are incurred in

producing the assessable rental income.

“Section 25-10 of the ITAA 1997” prohibits a taxpayer from claiming deductions

relating to cost incurred on notional repair. As held in “Inland Revenue Commissioners v

Shipping Co Ltd (1923)” a taxpayer that undertakes the initial repair to correct the defects

that was present while acquiring the property is treated as expenses of capital in nature and no

deductions is allowed. Bruce reports cost for repainting the investment property (James and

Nobes 2016). These costs can be treated as capital expenses which is occurred to remedy the

defects present in the property prior to subletting. These expenses do not arise from Bruce

own use of property to obtain the rental earnings. Hence, no deductions are allowed in this

circumstances.

As per “Section 25-10” a taxpayer is allowed to an entitlement of permissible

deduction for spending that is happened in replacing a portion of investment property that is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

damaged during storm (Swan 2018). As understood Bruce reported an expense on replacing

the tiles of roof that is damaged in storm. Since the investment property was held for

generating taxable income therefore a deduction is allowable to Bruce under “Section 25-

10”.

An individual taxpayer is prohibited from claiming any deductions when an

improvement made to the investment property surpasses the meaning of repair as it alters the

original character of the item. A taxpayer in this circumstances is not allowed to claim

deduction (White and Townsend 2018). On noticing that the work lead to substantial

improvement, any form of addition or alterations is not treated as repair and no allowable

deductions is permitted under “section 25-10”. Expenses reported by Bruce for extension of

bathroom on the rental property constitutes substantial improvement. Therefore, no

permissible deductions are permitted under “section 25-10”.

damaged during storm (Swan 2018). As understood Bruce reported an expense on replacing

the tiles of roof that is damaged in storm. Since the investment property was held for

generating taxable income therefore a deduction is allowable to Bruce under “Section 25-

10”.

An individual taxpayer is prohibited from claiming any deductions when an

improvement made to the investment property surpasses the meaning of repair as it alters the

original character of the item. A taxpayer in this circumstances is not allowed to claim

deduction (White and Townsend 2018). On noticing that the work lead to substantial

improvement, any form of addition or alterations is not treated as repair and no allowable

deductions is permitted under “section 25-10”. Expenses reported by Bruce for extension of

bathroom on the rental property constitutes substantial improvement. Therefore, no

permissible deductions are permitted under “section 25-10”.

8TAXATION LAW

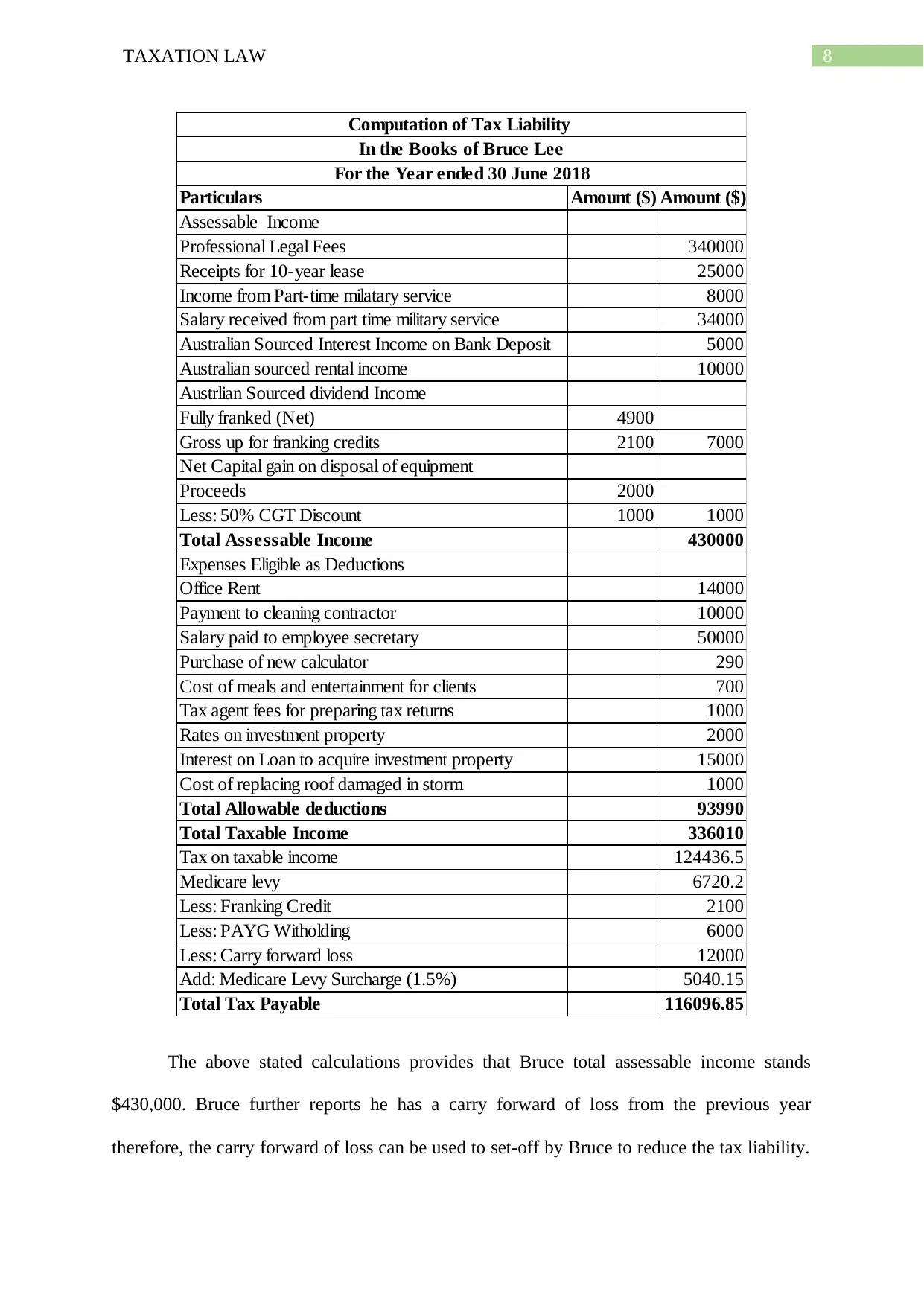

Particulars Amount ($) Amount ($)

Assessable Income

Professional Legal Fees 340000

Receipts for 10-year lease 25000

Income from Part-time milatary service 8000

Salary received from part time military service 34000

Australian Sourced Interest Income on Bank Deposit 5000

Australian sourced rental income 10000

Austrlian Sourced dividend Income

Fully franked (Net) 4900

Gross up for franking credits 2100 7000

Net Capital gain on disposal of equipment

Proceeds 2000

Less: 50% CGT Discount 1000 1000

Total Assessable Income 430000

Expenses Eligible as Deductions

Office Rent 14000

Payment to cleaning contractor 10000

Salary paid to employee secretary 50000

Purchase of new calculator 290

Cost of meals and entertainment for clients 700

Tax agent fees for preparing tax returns 1000

Rates on investment property 2000

Interest on Loan to acquire investment property 15000

Cost of replacing roof damaged in storm 1000

Total Allowable deductions 93990

Total Taxable Income 336010

Tax on taxable income 124436.5

Medicare levy 6720.2

Less: Franking Credit 2100

Less: PAYG Witholding 6000

Less: Carry forward loss 12000

Add: Medicare Levy Surcharge (1.5%) 5040.15

Total Tax Payable 116096.85

Computation of Tax Liability

In the Books of Bruce Lee

For the Year ended 30 June 2018

The above stated calculations provides that Bruce total assessable income stands

$430,000. Bruce further reports he has a carry forward of loss from the previous year

therefore, the carry forward of loss can be used to set-off by Bruce to reduce the tax liability.

Particulars Amount ($) Amount ($)

Assessable Income

Professional Legal Fees 340000

Receipts for 10-year lease 25000

Income from Part-time milatary service 8000

Salary received from part time military service 34000

Australian Sourced Interest Income on Bank Deposit 5000

Australian sourced rental income 10000

Austrlian Sourced dividend Income

Fully franked (Net) 4900

Gross up for franking credits 2100 7000

Net Capital gain on disposal of equipment

Proceeds 2000

Less: 50% CGT Discount 1000 1000

Total Assessable Income 430000

Expenses Eligible as Deductions

Office Rent 14000

Payment to cleaning contractor 10000

Salary paid to employee secretary 50000

Purchase of new calculator 290

Cost of meals and entertainment for clients 700

Tax agent fees for preparing tax returns 1000

Rates on investment property 2000

Interest on Loan to acquire investment property 15000

Cost of replacing roof damaged in storm 1000

Total Allowable deductions 93990

Total Taxable Income 336010

Tax on taxable income 124436.5

Medicare levy 6720.2

Less: Franking Credit 2100

Less: PAYG Witholding 6000

Less: Carry forward loss 12000

Add: Medicare Levy Surcharge (1.5%) 5040.15

Total Tax Payable 116096.85

Computation of Tax Liability

In the Books of Bruce Lee

For the Year ended 30 June 2018

The above stated calculations provides that Bruce total assessable income stands

$430,000. Bruce further reports he has a carry forward of loss from the previous year

therefore, the carry forward of loss can be used to set-off by Bruce to reduce the tax liability.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Additionally, Bruce has no private hospital insurance and would be liable for Medicare levy

surcharge of 1.5% on the overall taxable income. The total tax liability stands $116,096.85.

Additionally, Bruce has no private hospital insurance and would be liable for Medicare levy

surcharge of 1.5% on the overall taxable income. The total tax liability stands $116,096.85.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Blakelock, S. and King, P., 2017. Taxation law: The advance of ATO data

matching. Proctor, The, 37(6), p.18.

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Burton, M., 2018. Extending the tax expenditure concept in Australia.

Cao, R., Chapple, L.J. and Sadiq, K., 2014. Taxation determinations as de facto regulation:

private equity exits in Australia. Australian Tax Review, 43(2), pp.118-141.

Davies, G. and Wheelahan, E., 2018. The application of Pt IVA to stapled structures. Tax

Specialist, 21(5), p.195.

Edmonds, R., 2018. Resource Capital Fund IV LP: The issues on appeal?. Taxation in

Australia, 53(1), p.22.

James, S.R. and Nobes, C., 2016. Economics of Taxation: Principles, Policy and Practice.

Fiscal Publications.

McLaren, J. and Cormick, R., 2018. Dividend imputation: a critical review of the future of

the system. In Australian Tax Forum (Vol. 33, No. 1, p. 141). Tax Institute.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Neil Brydges, C.T.A., Counsel, S., Yuen, K. and Lawyer, S.L., 2015. Trusts, income tax,

CGT and foreign residents.

Pinto, D., Kendall, K. and Sadiq, K., 2015. Fundamental Tax Legislation. Thomson Reuters.

Swan, P.L., 2018. Investment, the Corporate Tax Rate, and the Pricing of Franking Credits.

References:

Blakelock, S. and King, P., 2017. Taxation law: The advance of ATO data

matching. Proctor, The, 37(6), p.18.

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Burton, M., 2018. Extending the tax expenditure concept in Australia.

Cao, R., Chapple, L.J. and Sadiq, K., 2014. Taxation determinations as de facto regulation:

private equity exits in Australia. Australian Tax Review, 43(2), pp.118-141.

Davies, G. and Wheelahan, E., 2018. The application of Pt IVA to stapled structures. Tax

Specialist, 21(5), p.195.

Edmonds, R., 2018. Resource Capital Fund IV LP: The issues on appeal?. Taxation in

Australia, 53(1), p.22.

James, S.R. and Nobes, C., 2016. Economics of Taxation: Principles, Policy and Practice.

Fiscal Publications.

McLaren, J. and Cormick, R., 2018. Dividend imputation: a critical review of the future of

the system. In Australian Tax Forum (Vol. 33, No. 1, p. 141). Tax Institute.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Neil Brydges, C.T.A., Counsel, S., Yuen, K. and Lawyer, S.L., 2015. Trusts, income tax,

CGT and foreign residents.

Pinto, D., Kendall, K. and Sadiq, K., 2015. Fundamental Tax Legislation. Thomson Reuters.

Swan, P.L., 2018. Investment, the Corporate Tax Rate, and the Pricing of Franking Credits.

11TAXATION LAW

White, J. and Townsend, A., 2018. Deductibility of employee travel expenses: The ATO's

guidance. Taxation in Australia, 52(11), p.608.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

White, J. and Townsend, A., 2018. Deductibility of employee travel expenses: The ATO's

guidance. Taxation in Australia, 52(11), p.608.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.