HI6028 Taxation Theory, Practice, and Law: Assessment Solution

VerifiedAdded on 2023/01/09

|6

|1915

|48

Homework Assignment

AI Summary

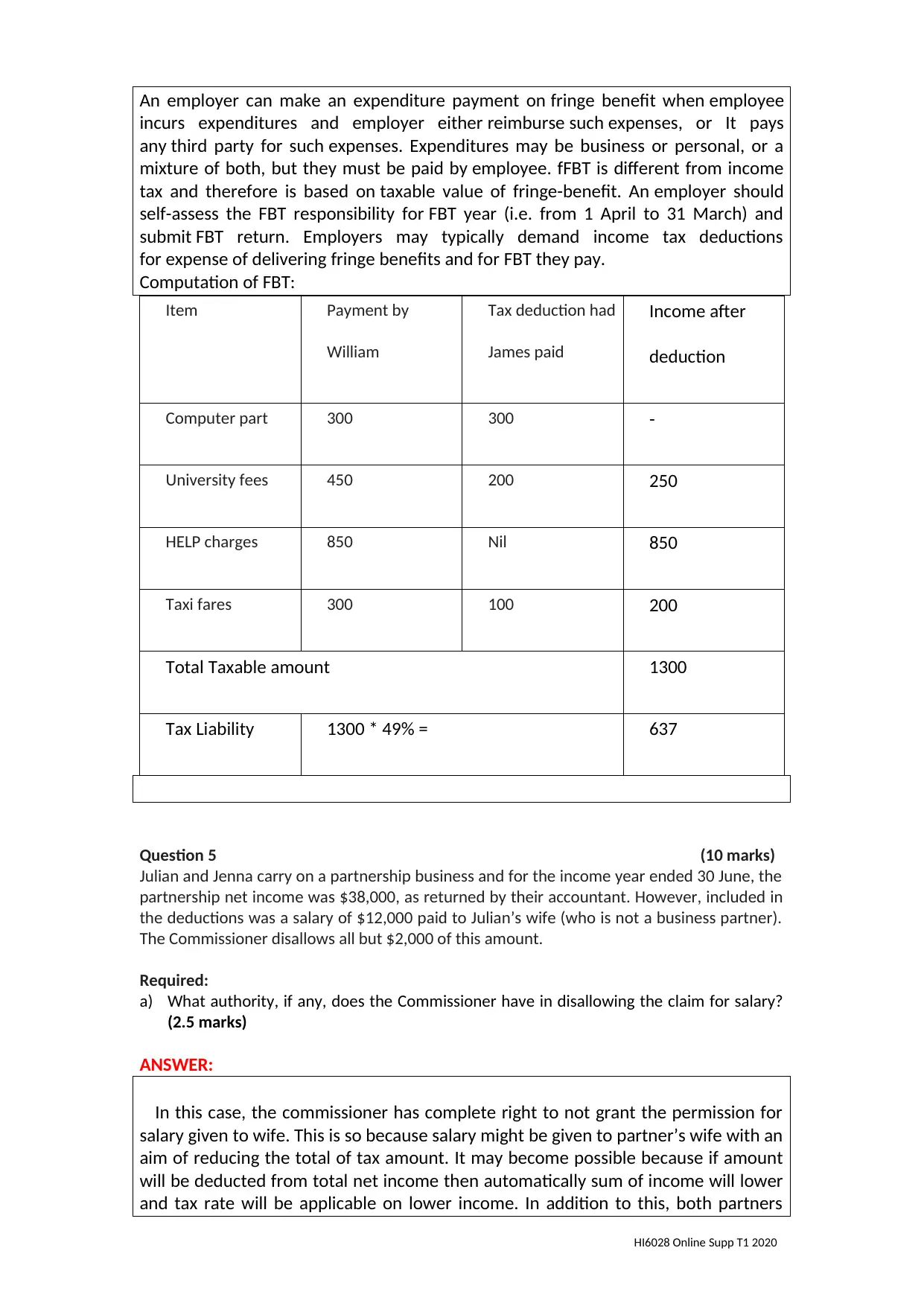

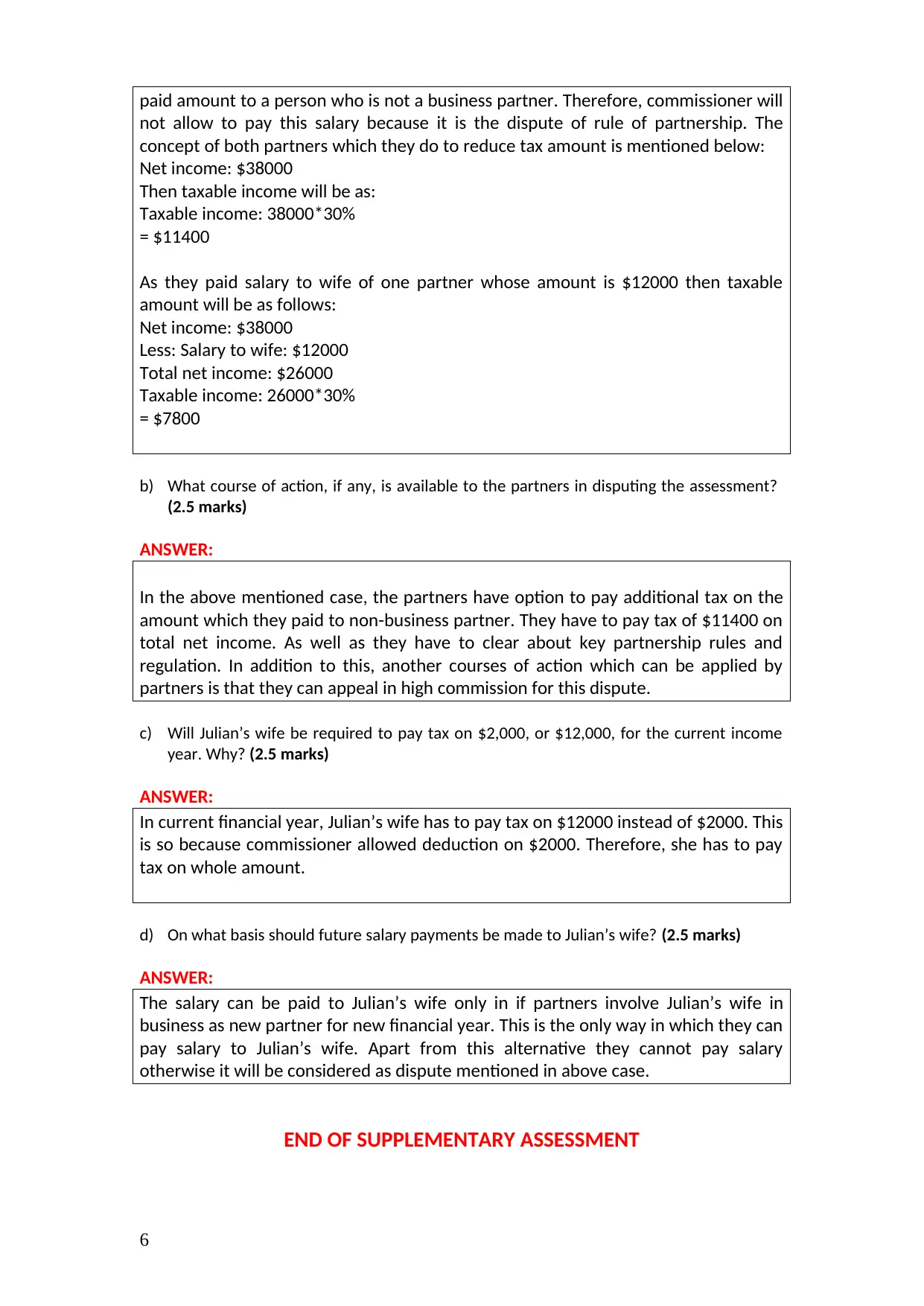

This document contains a comprehensive solution to the HI6028 Taxation Theory, Practice, and Law assignment for Trimester 1, 2020. The assignment assesses the student's understanding of Australian taxation principles through five questions. Question 1 analyzes whether various scenarios, including barter transactions and the exchange of services for goods, give rise to taxable income, referencing relevant legislation and case law. Question 2 explores the assessability or exemption of income from scholarships and part-time army reserve remuneration. Question 3 involves calculating deductible expenses for a teacher working from home, considering expenses like rent, utilities, and phone bills. Question 4 focuses on calculating the taxable value for Fringe Benefits Tax (FBT) purposes, concerning payments made by an employer. Finally, Question 5 examines partnership taxation, addressing the commissioner's authority to disallow salary claims, the available courses of action for partners, the tax implications for a partner's wife, and the basis for future salary payments. The solution provides detailed explanations and calculations, referencing relevant tax laws and regulations.

1 out of 6

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.