HI6028 Taxation Law T3 2018: Partnership Income & Fringe Benefits

VerifiedAdded on 2023/04/21

|13

|2240

|85

Report

AI Summary

This report provides a detailed analysis of taxation law, focusing on the calculation of net partnership income and the implications of fringe benefit tax. It examines a case study involving a partnership between Olivia and Daniel, calculating their net income for the 2017 income year based on reported receipts and expenses, referencing relevant sections of the ITAA 1936 and ITAA 1997. Additionally, the report addresses fringe benefit tax consequences for an employer, considering scenarios such as school fee payments for an employee's child and housing accommodations provided to the employee, referencing the FBTAA 1986. The analysis includes applications of relevant legal principles and concludes with a determination of taxable amounts and deductible expenses.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Calculation of Net Income from Partnership:............................................................................4

Working Papers:.........................................................................................................................5

Answer to question 2:.................................................................................................................7

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Calculation of Net Income from Partnership:............................................................................4

Working Papers:.........................................................................................................................5

Answer to question 2:.................................................................................................................7

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Issues:

The case study brings forward the issues relating to the determination of the net

partnership income based on the expenses and receipts reported in the income year.

Rule:

As per the discussion in “division 5 of the ITAA 1936” partnership is not recognized

as an unique legal aspect falling under the general law and also it is not included in paying

tax. In a partnership business the partners decide their tax payables according to the profits

earned as well as distributed. As per the “section 91” partnership is an important aspect while

lodging the income tax for showing the profit shared between the shareholders (McKee,

Nelson and Whitmire 2017). “Section 92 of the ITAA 1997” highlights all the profits are

distributed among the shareholders and they are responsible for paying tax on that gained

profits. As per the “section 995-1(1)” partnership can be understood in a better way if the

objectives of gaining profit are carried forward throughout business lifecycle (Graetz et al.

2015). In this section one thing is made clear that partnership is nothing but the objective of

gaining ordinary income or statutory bonus while doing sharing the business idea with some

shareholder.

As per the explanation given in “section 6-5 of ITAA 1997” the taxpayers pay

majority of their income as the ordinary income (Oishi, Kushlev and Schimmack 2018).

According to “Commissioner of Taxation v Scott (1935)” the income is not considered as an

artistic term and the application of important principles are used to make the objective of

ordinary concepts successful for the mankind.

Answer to question 1:

Issues:

The case study brings forward the issues relating to the determination of the net

partnership income based on the expenses and receipts reported in the income year.

Rule:

As per the discussion in “division 5 of the ITAA 1936” partnership is not recognized

as an unique legal aspect falling under the general law and also it is not included in paying

tax. In a partnership business the partners decide their tax payables according to the profits

earned as well as distributed. As per the “section 91” partnership is an important aspect while

lodging the income tax for showing the profit shared between the shareholders (McKee,

Nelson and Whitmire 2017). “Section 92 of the ITAA 1997” highlights all the profits are

distributed among the shareholders and they are responsible for paying tax on that gained

profits. As per the “section 995-1(1)” partnership can be understood in a better way if the

objectives of gaining profit are carried forward throughout business lifecycle (Graetz et al.

2015). In this section one thing is made clear that partnership is nothing but the objective of

gaining ordinary income or statutory bonus while doing sharing the business idea with some

shareholder.

As per the explanation given in “section 6-5 of ITAA 1997” the taxpayers pay

majority of their income as the ordinary income (Oishi, Kushlev and Schimmack 2018).

According to “Commissioner of Taxation v Scott (1935)” the income is not considered as an

artistic term and the application of important principles are used to make the objective of

ordinary concepts successful for the mankind.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

According to “section 8-1 of the ITAA 1997” there are two important extremities.

Taxpayer can include their claims for deductions from their taxable incomes if the income or

loss is occurred when they are about to fulfil the business objectives for gaining taxable

profits (Bankman et al. 2018). Conversely, according to “section 8-1 (2) of the ITAA 1997”

the taxpayer is not allowed to claim expense those are domestic, private or capital in nature.

Hence, partnership policies don’t allow any deductions.

According to the Australian Taxation Office the taxpayer with an instant write-off can

claim the deductions those are less than 20,000. Agreeing to the “taxation ruling of TR

97/23”, repair are also allowed to the taxpayer under “section 25-10 of the ITAA 1997”

(Schenk 2017). The taxpayers can get a deducted amount if the repairs are done for the

damage or corrosion of the property. Conditions to be applicable in these kind of repair is, if

the repairs are including a expense amount as capital then the deductions are not allowed to

the taxpayer. According to “Western Suburbs Cinemas v FC of T (1952)” the court does not

allow the taxpayer to get the deductions for notional deductions (Murphy and Higgins 2016).

Applications:

The considered case study is all about the partnership of Olivia and Daniel who are

continuing a collaborative business. During the income year the partnership has reported

receipts and the expenses are incurred during throughout the business functionalities. The

business gained from profit from the business sales encountered and payments from the

debtors (Schmalbeck, Zelenak and Lawsky 2015).

According to the event “sect 6-5 of the ITAA 1997” ordinary income is gained by

Olivia and Daniel through the partnership business sales and debtors payments. According to

the concepts declared the ordinary income gained from business sales and debtor’s payment

According to “section 8-1 of the ITAA 1997” there are two important extremities.

Taxpayer can include their claims for deductions from their taxable incomes if the income or

loss is occurred when they are about to fulfil the business objectives for gaining taxable

profits (Bankman et al. 2018). Conversely, according to “section 8-1 (2) of the ITAA 1997”

the taxpayer is not allowed to claim expense those are domestic, private or capital in nature.

Hence, partnership policies don’t allow any deductions.

According to the Australian Taxation Office the taxpayer with an instant write-off can

claim the deductions those are less than 20,000. Agreeing to the “taxation ruling of TR

97/23”, repair are also allowed to the taxpayer under “section 25-10 of the ITAA 1997”

(Schenk 2017). The taxpayers can get a deducted amount if the repairs are done for the

damage or corrosion of the property. Conditions to be applicable in these kind of repair is, if

the repairs are including a expense amount as capital then the deductions are not allowed to

the taxpayer. According to “Western Suburbs Cinemas v FC of T (1952)” the court does not

allow the taxpayer to get the deductions for notional deductions (Murphy and Higgins 2016).

Applications:

The considered case study is all about the partnership of Olivia and Daniel who are

continuing a collaborative business. During the income year the partnership has reported

receipts and the expenses are incurred during throughout the business functionalities. The

business gained from profit from the business sales encountered and payments from the

debtors (Schmalbeck, Zelenak and Lawsky 2015).

According to the event “sect 6-5 of the ITAA 1997” ordinary income is gained by

Olivia and Daniel through the partnership business sales and debtors payments. According to

the concepts declared the ordinary income gained from business sales and debtor’s payment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

will constitute the ordinary proceeds following the ordinary concepts of “section 6-5 of the

ITAA 1997”.

In the income year of 2017 the price of air conditioner was $1,200, which was less

than 20,000. Hence this can be allowed to the taxpayer with the help of a written off as

deduction.

In the concerned discussion about the partnership of Daniel and Olivia, the expenses are

applicable on shop painting and refrigerator. Hence, referring to “Western Suburbs Cinemas

v FCT (1952)” these are notional and the expense was in capital so no deductions will be

allowed to Daniel and Olivia according to “section 25-10 of the ITAA 1997”. The net

income was elaborated in the bellow table-

will constitute the ordinary proceeds following the ordinary concepts of “section 6-5 of the

ITAA 1997”.

In the income year of 2017 the price of air conditioner was $1,200, which was less

than 20,000. Hence this can be allowed to the taxpayer with the help of a written off as

deduction.

In the concerned discussion about the partnership of Daniel and Olivia, the expenses are

applicable on shop painting and refrigerator. Hence, referring to “Western Suburbs Cinemas

v FCT (1952)” these are notional and the expense was in capital so no deductions will be

allowed to Daniel and Olivia according to “section 25-10 of the ITAA 1997”. The net

income was elaborated in the bellow table-

5TAXATION LAW

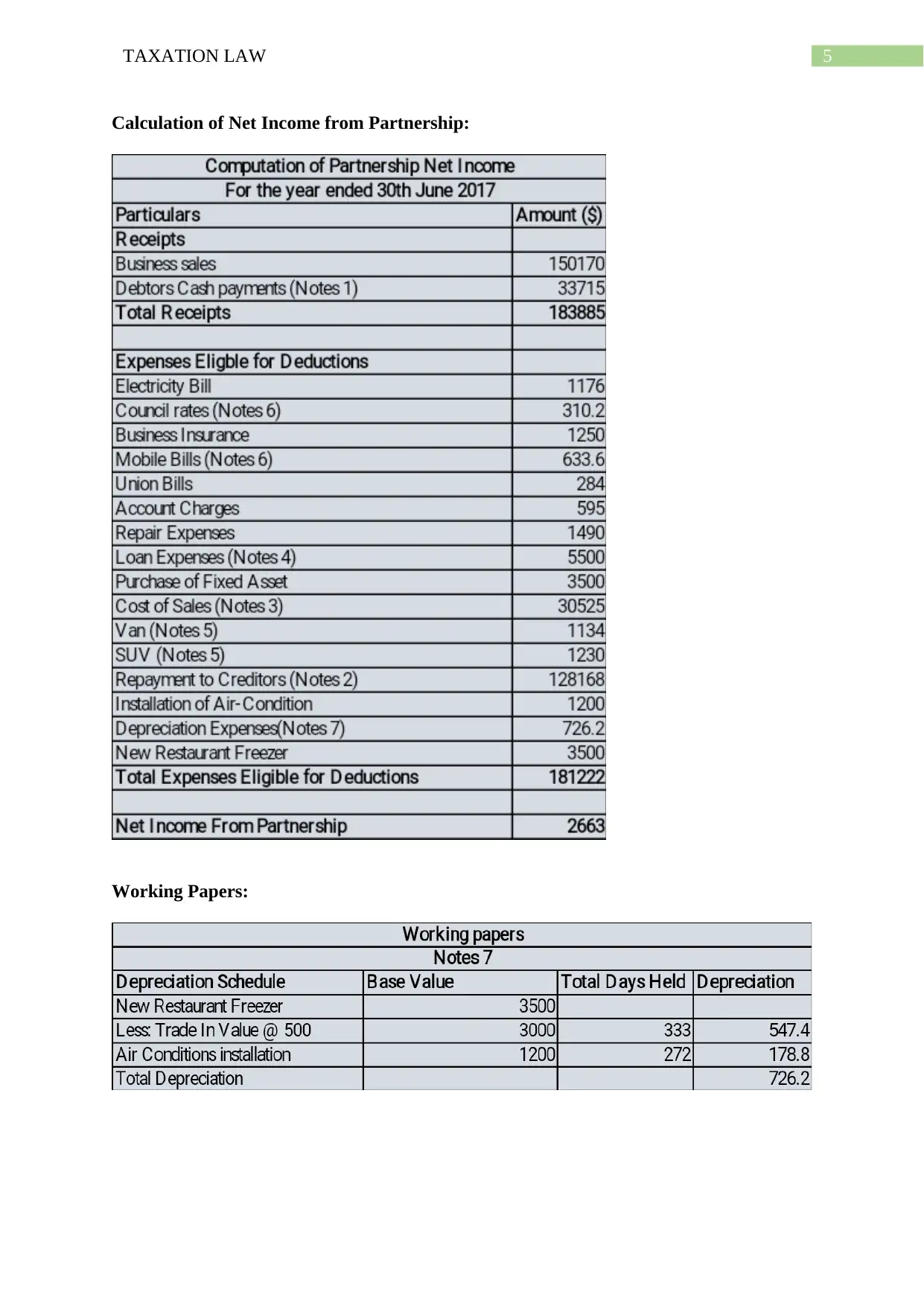

Calculation of Net Income from Partnership:

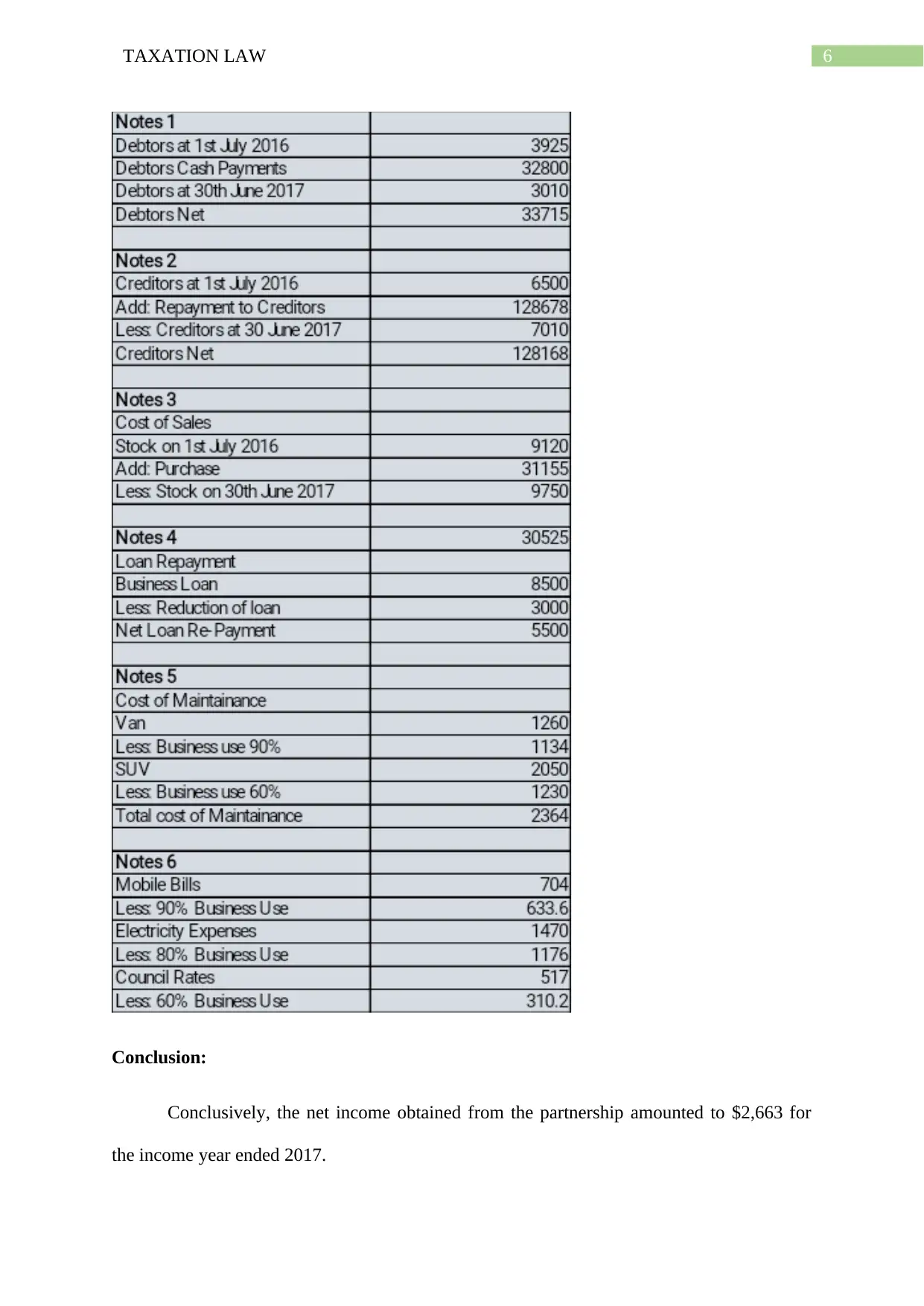

Working Papers:

Calculation of Net Income from Partnership:

Working Papers:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Conclusion:

Conclusively, the net income obtained from the partnership amounted to $2,663 for

the income year ended 2017.

Conclusion:

Conclusively, the net income obtained from the partnership amounted to $2,663 for

the income year ended 2017.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Answer to question 2:

Issue:

The case introduces the issues based on the fringe benefit tax consequences for the

employer based on the fringe benefit provided for child’s school fees payment and housing

accommodation provided to employee.

Rule:

Fringe benefit can be elaborated as the payment which the employee get and is not the

same as salary or wages. The employees get fringe benefit as the benefit of being employed

with the company (Simmons et al. 2017). All the employees get these benefits from the

company. In contrast with this, the employer is liable to pay the fringe benefit tax which they

are paying to their employee, director or office holder. Depending on the situations, the

employer can do reductions in the fringe benefit tax that they provide to their employees.

Sometimes the employers provide the fringe benefits in terms of lieu of payments. This

payment is known as the employee contribution. These amounts are paid to the person who is

providing the fringe benefits to their employees.

In accordance with the taxation commissioner of “FC of T v J & G Knowles (2000)”,

the recipients should ensure that they are having a materialistic or sufficient relation with the

expense and their occupation (Seto 2015). According to “sub-paragraph 65A (ii) of the

FBTAA 1986” if the child of the recipient is perusing a full time education then the recipient

is allowed to get the deductions which will be calculated as the reduction from the assessable

charge of the fringe benefit.

According to the “section 25 of the FBTAA 1986” housing fringe benefits are taken

into the account when an employee is using the lease or license for the part of the house or

the property as the regular residence (Raabe et al. 2015). All the rights of the employer for

Answer to question 2:

Issue:

The case introduces the issues based on the fringe benefit tax consequences for the

employer based on the fringe benefit provided for child’s school fees payment and housing

accommodation provided to employee.

Rule:

Fringe benefit can be elaborated as the payment which the employee get and is not the

same as salary or wages. The employees get fringe benefit as the benefit of being employed

with the company (Simmons et al. 2017). All the employees get these benefits from the

company. In contrast with this, the employer is liable to pay the fringe benefit tax which they

are paying to their employee, director or office holder. Depending on the situations, the

employer can do reductions in the fringe benefit tax that they provide to their employees.

Sometimes the employers provide the fringe benefits in terms of lieu of payments. This

payment is known as the employee contribution. These amounts are paid to the person who is

providing the fringe benefits to their employees.

In accordance with the taxation commissioner of “FC of T v J & G Knowles (2000)”,

the recipients should ensure that they are having a materialistic or sufficient relation with the

expense and their occupation (Seto 2015). According to “sub-paragraph 65A (ii) of the

FBTAA 1986” if the child of the recipient is perusing a full time education then the recipient

is allowed to get the deductions which will be calculated as the reduction from the assessable

charge of the fringe benefit.

According to the “section 25 of the FBTAA 1986” housing fringe benefits are taken

into the account when an employee is using the lease or license for the part of the house or

the property as the regular residence (Raabe et al. 2015). All the rights of the employer for

8TAXATION LAW

that particular part of house are replicated for the employee as he uses that house for his

formal residence. The part of accommodation might be a flat or house itself. These

accommodation details are also including the house or flat those are provided to the

employees directly as residence (Burns and Ziliak 2017). The charges are calculated for these

houses or flats according to the market value of those properties. These providences are also

in relation with the rental property and the rental charges are relevant to these rental houses or

flats.

Application:

According to the understanding gained from the situation of John who is working as a

senior executive in a printing company, here the employer is liable to pay for the kid of John.

The fee is $15,000. Now according to “section 20 of FBTAA 1986” here the concept of

fringe benefit is taken into consideration as the John’s employer is paying the expense of his

Kid’s school.

Consequently, in case of the present situation of John, the employer pays for school

expense for his kid. The expense for the school of John kid is considered as a full time

education. Along with this this is encountered that this is in materialistic relation with his

occupation. Hence, the employer of john will be allowing the deductions in fringe benefit tax,

because the expense was considered for the full time education of John’s kid. According to

“sub-paragraph 65A (ii) of the FBTAA 1986” the employer here can reduce the taxable

amount through deductions from the fringe benefits to John as the full time education is

related to the fringe benefits provided by his employer.

In the later part, it is understood from the current situation of John, he has been

provided with the part of accommodation from his employer. Hence, John is liable to provide

$100 per week to the employer in relation with the rental property. In contrast with this, the

that particular part of house are replicated for the employee as he uses that house for his

formal residence. The part of accommodation might be a flat or house itself. These

accommodation details are also including the house or flat those are provided to the

employees directly as residence (Burns and Ziliak 2017). The charges are calculated for these

houses or flats according to the market value of those properties. These providences are also

in relation with the rental property and the rental charges are relevant to these rental houses or

flats.

Application:

According to the understanding gained from the situation of John who is working as a

senior executive in a printing company, here the employer is liable to pay for the kid of John.

The fee is $15,000. Now according to “section 20 of FBTAA 1986” here the concept of

fringe benefit is taken into consideration as the John’s employer is paying the expense of his

Kid’s school.

Consequently, in case of the present situation of John, the employer pays for school

expense for his kid. The expense for the school of John kid is considered as a full time

education. Along with this this is encountered that this is in materialistic relation with his

occupation. Hence, the employer of john will be allowing the deductions in fringe benefit tax,

because the expense was considered for the full time education of John’s kid. According to

“sub-paragraph 65A (ii) of the FBTAA 1986” the employer here can reduce the taxable

amount through deductions from the fringe benefits to John as the full time education is

related to the fringe benefits provided by his employer.

In the later part, it is understood from the current situation of John, he has been

provided with the part of accommodation from his employer. Hence, John is liable to provide

$100 per week to the employer in relation with the rental property. In contrast with this, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

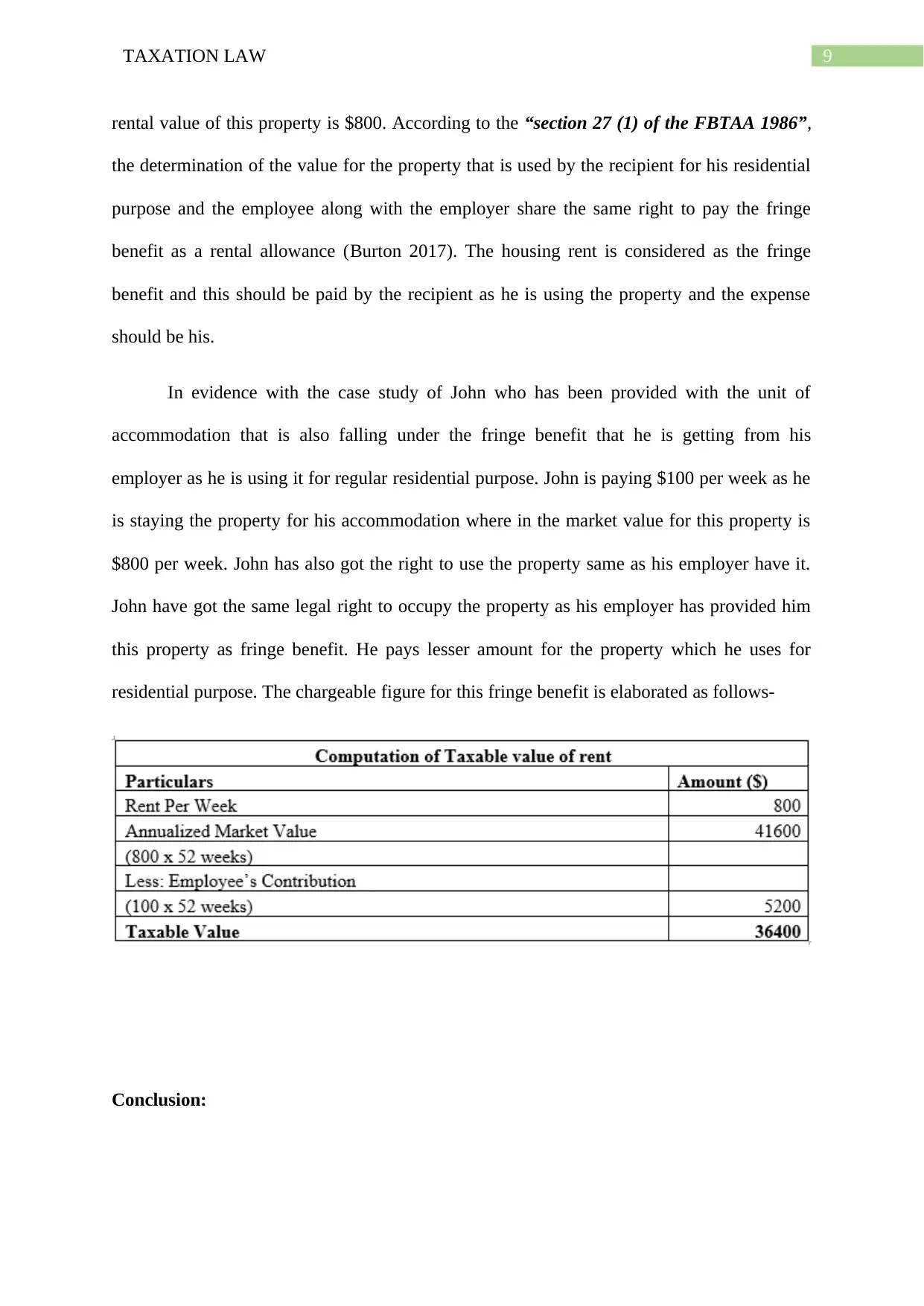

rental value of this property is $800. According to the “section 27 (1) of the FBTAA 1986”,

the determination of the value for the property that is used by the recipient for his residential

purpose and the employee along with the employer share the same right to pay the fringe

benefit as a rental allowance (Burton 2017). The housing rent is considered as the fringe

benefit and this should be paid by the recipient as he is using the property and the expense

should be his.

In evidence with the case study of John who has been provided with the unit of

accommodation that is also falling under the fringe benefit that he is getting from his

employer as he is using it for regular residential purpose. John is paying $100 per week as he

is staying the property for his accommodation where in the market value for this property is

$800 per week. John has also got the right to use the property same as his employer have it.

John have got the same legal right to occupy the property as his employer has provided him

this property as fringe benefit. He pays lesser amount for the property which he uses for

residential purpose. The chargeable figure for this fringe benefit is elaborated as follows-

Conclusion:

rental value of this property is $800. According to the “section 27 (1) of the FBTAA 1986”,

the determination of the value for the property that is used by the recipient for his residential

purpose and the employee along with the employer share the same right to pay the fringe

benefit as a rental allowance (Burton 2017). The housing rent is considered as the fringe

benefit and this should be paid by the recipient as he is using the property and the expense

should be his.

In evidence with the case study of John who has been provided with the unit of

accommodation that is also falling under the fringe benefit that he is getting from his

employer as he is using it for regular residential purpose. John is paying $100 per week as he

is staying the property for his accommodation where in the market value for this property is

$800 per week. John has also got the right to use the property same as his employer have it.

John have got the same legal right to occupy the property as his employer has provided him

this property as fringe benefit. He pays lesser amount for the property which he uses for

residential purpose. The chargeable figure for this fringe benefit is elaborated as follows-

Conclusion:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

On a conclusive note the employer here can lower the taxable value of the fringe

benefit afterward subtracting the contributions that is made by the employee here. The

employer here will be taxable for expense payment fringe benefit and housing benefit.

On a conclusive note the employer here can lower the taxable value of the fringe

benefit afterward subtracting the contributions that is made by the employee here. The

employer here will be taxable for expense payment fringe benefit and housing benefit.

11TAXATION LAW

References:

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2018. Federal Income Taxation.

Aspen Casebook.

Burns, S.K. and Ziliak, J.P., 2017. Identifying the elasticity of taxable income. The Economic

Journal, 127(600), pp.297-329.

Burton, D.R., 2017. Tax Reform: Eliminating the Double Taxation of Corporate Income.

Graetz, M., Schenk, D., Freeland, J., Lathrope, D., Lind, S., Stephens, R., Burke, K., Brealey,

R., Myers, S., Allen, F. and Keyes, K., 2015. Federal Income Taxation, Principles and

Policies (University Casebook Series). Foundation Press/West Academic.

McKee, W.S., Nelson, W.F. and Whitmire, R.L., 2017. Federal taxation of partnerships and

partners (Vol. 1). Warren, Gorham & Lamont.

Murphy, K.E. and Higgins, M., 2016. Concepts in Federal Taxation 2017. Cengage

Learning.

Oishi, S., Kushlev, K. and Schimmack, U., 2018. Progressive taxation, income inequality,

and happiness. American Psychologist, 73(2), p.157.

Raabe, W.A., Maloney, D.M., Young, J.C., Smith, J.E. and Nellen, A., 2015. South-Western

Federal Taxation 2016: Essentials of Taxation: Individuals and Business Entities. Nelson

Education.

Schenk, D.H., 2017. Federal Taxation of S Corporations. Law Journal Press.

Schmalbeck, R., Zelenak, L. and Lawsky, S.B., 2015. Federal Income Taxation. Wolters

Kluwer Law & Business.

References:

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2018. Federal Income Taxation.

Aspen Casebook.

Burns, S.K. and Ziliak, J.P., 2017. Identifying the elasticity of taxable income. The Economic

Journal, 127(600), pp.297-329.

Burton, D.R., 2017. Tax Reform: Eliminating the Double Taxation of Corporate Income.

Graetz, M., Schenk, D., Freeland, J., Lathrope, D., Lind, S., Stephens, R., Burke, K., Brealey,

R., Myers, S., Allen, F. and Keyes, K., 2015. Federal Income Taxation, Principles and

Policies (University Casebook Series). Foundation Press/West Academic.

McKee, W.S., Nelson, W.F. and Whitmire, R.L., 2017. Federal taxation of partnerships and

partners (Vol. 1). Warren, Gorham & Lamont.

Murphy, K.E. and Higgins, M., 2016. Concepts in Federal Taxation 2017. Cengage

Learning.

Oishi, S., Kushlev, K. and Schimmack, U., 2018. Progressive taxation, income inequality,

and happiness. American Psychologist, 73(2), p.157.

Raabe, W.A., Maloney, D.M., Young, J.C., Smith, J.E. and Nellen, A., 2015. South-Western

Federal Taxation 2016: Essentials of Taxation: Individuals and Business Entities. Nelson

Education.

Schenk, D.H., 2017. Federal Taxation of S Corporations. Law Journal Press.

Schmalbeck, R., Zelenak, L. and Lawsky, S.B., 2015. Federal Income Taxation. Wolters

Kluwer Law & Business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.