Taxation Law: Assessment of Assessable Income and Tax Liability

VerifiedAdded on 2020/12/29

|6

|1366

|295

Homework Assignment

AI Summary

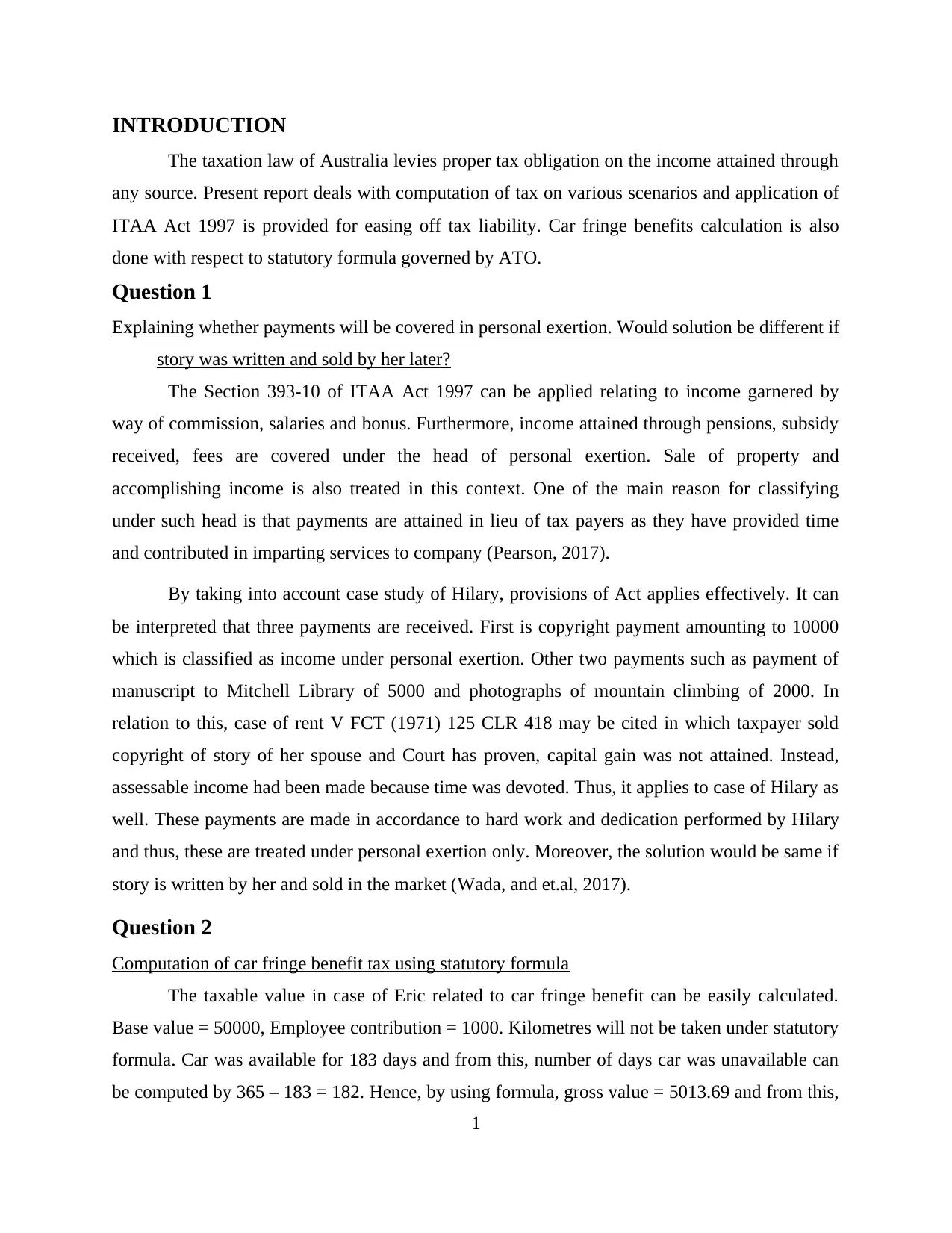

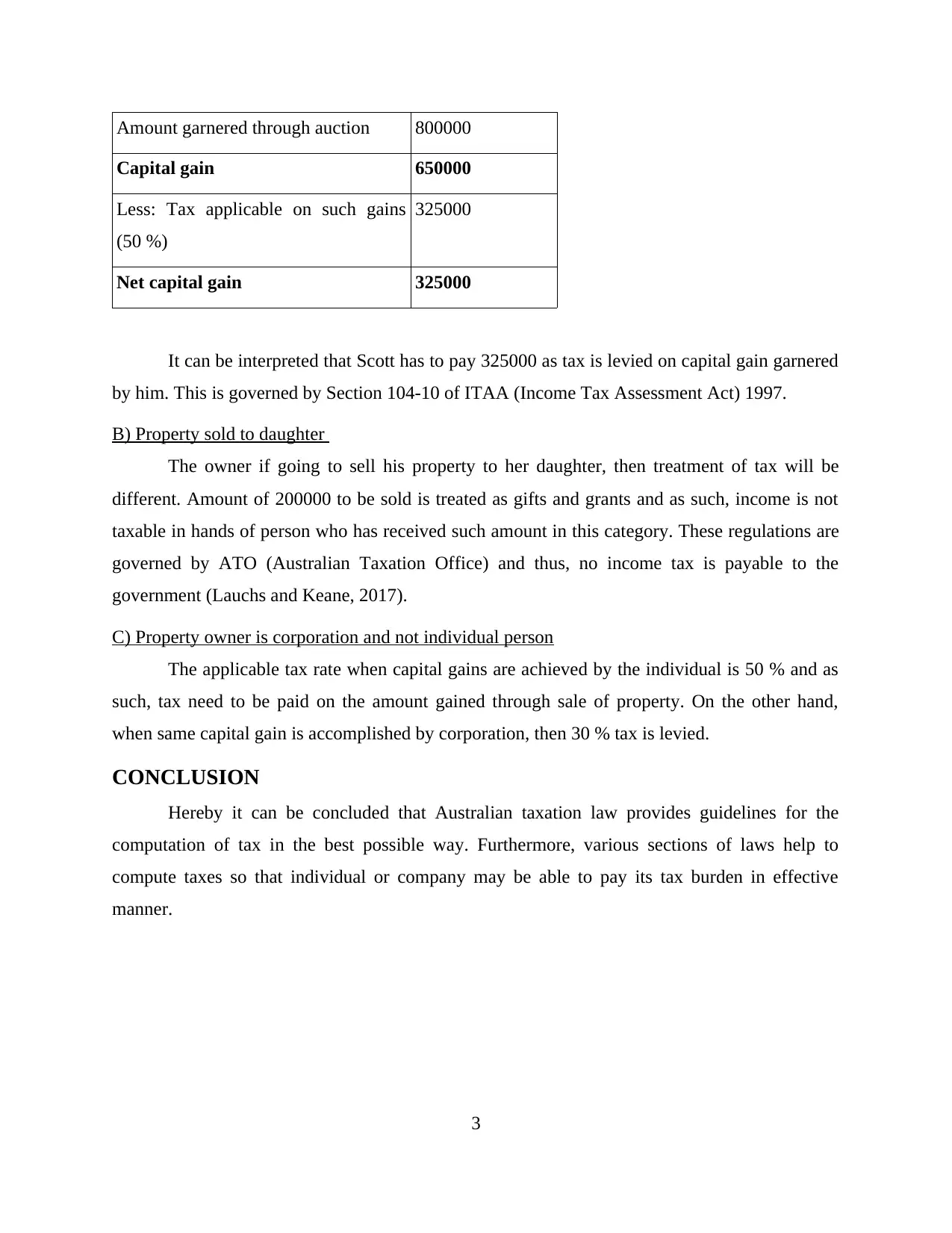

This taxation law assignment analyzes several scenarios related to Australian taxation. It begins with a discussion of personal exertion income, including copyright payments and the sale of stories, referencing relevant case law and the ITAA 1997. The assignment then calculates car fringe benefit tax using the statutory formula. Next, it examines the tax implications of a parent lending money to a son, including interest payments and gift tax regulations. Finally, the assignment calculates capital gains and losses from the sale of property, considering different scenarios based on whether the property owner is an individual or a corporation, and discusses the tax implications of selling property to a daughter. The conclusion summarizes the application of Australian taxation law to these various situations.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.