Taxation Assignment: Deductions, GST, Foreign Tax Offset Analysis

VerifiedAdded on 2020/07/23

|11

|2528

|38

Homework Assignment

AI Summary

This taxation assignment delves into various aspects of income tax, GST, and foreign tax offsets, providing detailed calculations and explanations. It begins with an examination of deductible expenses under section 8-1 of ITAA 1997, differentiating between capital and revenue expenses. The assignment then assesses Big Bank's ability to claim advertising expenses, including GST implications for their new insurance product and traditional loan services. Furthermore, it determines Angelo's foreign tax offset through a three-step process, calculating taxable income, tax liability, and the final offset amount. Finally, the assignment concludes by calculating the net income for a partnership, considering various income sources, deductible expenses, and partner salaries, providing a comprehensive overview of taxation principles and their practical application.

Taxation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 1..................................................................................................................................1

(A)................................................................................................................................................1

(B)................................................................................................................................................2

(C)................................................................................................................................................2

(D)................................................................................................................................................2

QUESTION 2..................................................................................................................................3

Assessing Big Bank’s ability to claim in relation to advertising expenses.................................3

QUESTION 3..................................................................................................................................4

Determining foreign tax offset.....................................................................................................4

QUESTION 4..................................................................................................................................6

Calculating net income for the partnership..................................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

QUESTION 1..................................................................................................................................1

(A)................................................................................................................................................1

(B)................................................................................................................................................2

(C)................................................................................................................................................2

(D)................................................................................................................................................2

QUESTION 2..................................................................................................................................3

Assessing Big Bank’s ability to claim in relation to advertising expenses.................................3

QUESTION 3..................................................................................................................................4

Determining foreign tax offset.....................................................................................................4

QUESTION 4..................................................................................................................................6

Calculating net income for the partnership..................................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

INTRODUCTION

Section 8-1 of ITAA 1997 consists various deductions from the assessable income of

assesses. Furthermore, expenses which are incurred by person can be deduct from their income

tax amount and they are not able to pay them at the time of payment of tax. Income tax has been

imposed on every person or firm as well and they are responsible to pay amount equal to the

mentioned under law (Mete, Dick and Moerman, 2010). Present report based on payment of

compulsory amount which is mentioned under law. In case company established in order to

provide services to people then it have to pay GST up to the rate imposed on them. Foreign tax

offset has been calculated of any person according to his income, expenses and rate of tax as

well. Also two partners name called Johnny and Leon who run partnership firm. So that, their net

income needs to be calculated on the basis of their income and expenses also they are bound to

pay the same.

QUESTION 1

(A)

According to rules of section 8-1 of ITAA 1997 it has been stated that machinery

considered as fixed assets for the company. If it moved from one site to another than expenses

should be considered as capital expenses. Various types of rules and procedures mentioned under

this section which is imposed on assesses and bound them to follow the same also try to comply

with them as well (Tran-Nam and Evans, 2011). The expenses of moving of fixed assets from

one site to another no deduction will be provided because it is considered as expenses of capital

nature. These are able to increase cost of the goods and services for the purpose of depreciation.

This expenses has not been paid in case but it can reduce cost of fixed assets every year. But this

is not the reason for provide deduction amount. Tax liabilities must be imposed on person whose

income higher then limited amount of income which is mentioned under. Profit which is earn by

Section 8-1 of ITAA 1997 consists various deductions from the assessable income of

assesses. Furthermore, expenses which are incurred by person can be deduct from their income

tax amount and they are not able to pay them at the time of payment of tax. Income tax has been

imposed on every person or firm as well and they are responsible to pay amount equal to the

mentioned under law (Mete, Dick and Moerman, 2010). Present report based on payment of

compulsory amount which is mentioned under law. In case company established in order to

provide services to people then it have to pay GST up to the rate imposed on them. Foreign tax

offset has been calculated of any person according to his income, expenses and rate of tax as

well. Also two partners name called Johnny and Leon who run partnership firm. So that, their net

income needs to be calculated on the basis of their income and expenses also they are bound to

pay the same.

QUESTION 1

(A)

According to rules of section 8-1 of ITAA 1997 it has been stated that machinery

considered as fixed assets for the company. If it moved from one site to another than expenses

should be considered as capital expenses. Various types of rules and procedures mentioned under

this section which is imposed on assesses and bound them to follow the same also try to comply

with them as well (Tran-Nam and Evans, 2011). The expenses of moving of fixed assets from

one site to another no deduction will be provided because it is considered as expenses of capital

nature. These are able to increase cost of the goods and services for the purpose of depreciation.

This expenses has not been paid in case but it can reduce cost of fixed assets every year. But this

is not the reason for provide deduction amount. Tax liabilities must be imposed on person whose

income higher then limited amount of income which is mentioned under. Profit which is earn by

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

companies in through fixed assets are considered as capital profit on which no firm can receive

deduction (Butler and Skandakumar, 2014).

(B)

Cost of asset revaluation is the process which incurred expenses related to fixed assets.

So that, as per the rules of law, such expenses can be deduct from assessable income of assesses.

As they are bound to pay remaining amount which is imposed on them. It is deductable item as

per the rule of law (Joseph, 2014). If expenses are related to fixed it should be considered that it

must be deductabe in nature which is beneficial for people because it is able to enhance income

earning capacity of them which can be protect as well as preserve it. If the expenses should be

recurring in nature than should be deductible according to rules of law. Expenses which are

incurred upon asset revaluation than it should be deemed to be recurring in nature. Certain rules

mentioned under this rules which is imposed on people and they are bound to fulfil the same in

order to comply with law.

(C)

If the legal expenses incurred by a organization in order to opposing a petition for the

purpose of winding up then amount should be deductible in nature (Harrison and Keating, 2010).

As per this scenario, deductibility of expenses is totally depends on the structure which is given

as related to structure or it can depend on the income generation capacity of above mentioned

company. Or expenses can be related to with operational activities of the organization. In case

uncertain outcomes on the petition is able to reduce ability of firm and through which it is not

able to enhance their level on income then expenses are considered as capital expense. If the

cases related to the operation functions of the company then it should be related with the revenue

which is covered under section 8-1 of ITAA 1997. Expenses related to process of operation of

business has been considered as revenue in nature. Furthermore, such amount is able to

deductible in nature. On the basis of that capital expenses can be deduct from amount of payment

of tax.

(D)

Legal expenses which are incurred for the purpose of providing services of solicitor

which is related to several numbers of matters involving legal advice to various client related to

their business operation, conveyancing and much more. In this scenario, the account of solicitor

deduction (Butler and Skandakumar, 2014).

(B)

Cost of asset revaluation is the process which incurred expenses related to fixed assets.

So that, as per the rules of law, such expenses can be deduct from assessable income of assesses.

As they are bound to pay remaining amount which is imposed on them. It is deductable item as

per the rule of law (Joseph, 2014). If expenses are related to fixed it should be considered that it

must be deductabe in nature which is beneficial for people because it is able to enhance income

earning capacity of them which can be protect as well as preserve it. If the expenses should be

recurring in nature than should be deductible according to rules of law. Expenses which are

incurred upon asset revaluation than it should be deemed to be recurring in nature. Certain rules

mentioned under this rules which is imposed on people and they are bound to fulfil the same in

order to comply with law.

(C)

If the legal expenses incurred by a organization in order to opposing a petition for the

purpose of winding up then amount should be deductible in nature (Harrison and Keating, 2010).

As per this scenario, deductibility of expenses is totally depends on the structure which is given

as related to structure or it can depend on the income generation capacity of above mentioned

company. Or expenses can be related to with operational activities of the organization. In case

uncertain outcomes on the petition is able to reduce ability of firm and through which it is not

able to enhance their level on income then expenses are considered as capital expense. If the

cases related to the operation functions of the company then it should be related with the revenue

which is covered under section 8-1 of ITAA 1997. Expenses related to process of operation of

business has been considered as revenue in nature. Furthermore, such amount is able to

deductible in nature. On the basis of that capital expenses can be deduct from amount of payment

of tax.

(D)

Legal expenses which are incurred for the purpose of providing services of solicitor

which is related to several numbers of matters involving legal advice to various client related to

their business operation, conveyancing and much more. In this scenario, the account of solicitor

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

is not able to separate from costs of different matter (Passant, McLaren and Silaen, 2014). As per

the rule expenses which are incurred in this scenario are not able to charge amount of deduction.

Such amount should not be deductible in nature. Amount of dividend and interest has been

considered as income of the person which are added in income.

QUESTION 2

Assessing Big Bank’s ability to claim in relation to advertising expenses

Issues

Given case situation entails that Big Bank is offering loan and deposit facilities from

several years. In addition to this, in the previous year, Big Bank introduced new product namely

Big Bank home and contents insurance policies. Cited case presents that Big Bank home is

registered for GST purpose. Hence, as per the taxation rules and regulations GST will be

applicable on the new product of Big Bank Ltd such as insurance policies. From the given

scenario, it has been found that expenditure budget in relation to the promotional aspect of

services such as loan and insurance accounted for $1650000. Further, it is mentioned in the case

situation insurance business accounts for 2% of the entire operations. On the other side, 98%

amount of advertisement expense was related to the traditional loan and deposit facilities

business. In this, advertising consultant issued tax invoice related to the amount of $1650000

respectively.

Law

Goods and services tax called as GST it should be imposed on most of the items approx.

10% or more which needs to paid by assesses. It must be registered by them if-

Companies having annual turnover of 75,000 dollars or more, Non profit making firm annual turnover 1,50,000 dollars or more (Income Tax

Assessment Act 1997, 2009)

Application

the rule expenses which are incurred in this scenario are not able to charge amount of deduction.

Such amount should not be deductible in nature. Amount of dividend and interest has been

considered as income of the person which are added in income.

QUESTION 2

Assessing Big Bank’s ability to claim in relation to advertising expenses

Issues

Given case situation entails that Big Bank is offering loan and deposit facilities from

several years. In addition to this, in the previous year, Big Bank introduced new product namely

Big Bank home and contents insurance policies. Cited case presents that Big Bank home is

registered for GST purpose. Hence, as per the taxation rules and regulations GST will be

applicable on the new product of Big Bank Ltd such as insurance policies. From the given

scenario, it has been found that expenditure budget in relation to the promotional aspect of

services such as loan and insurance accounted for $1650000. Further, it is mentioned in the case

situation insurance business accounts for 2% of the entire operations. On the other side, 98%

amount of advertisement expense was related to the traditional loan and deposit facilities

business. In this, advertising consultant issued tax invoice related to the amount of $1650000

respectively.

Law

Goods and services tax called as GST it should be imposed on most of the items approx.

10% or more which needs to paid by assesses. It must be registered by them if-

Companies having annual turnover of 75,000 dollars or more, Non profit making firm annual turnover 1,50,000 dollars or more (Income Tax

Assessment Act 1997, 2009)

Application

From assessment, it has been identified that in Australia, 10% GST is charged on most of

the goods or services. On the basis of legislation, it is highly required for Big Bank ltd to charge

GST from customers. In addition to this, firm has also right to claim for the business expenses

and other inputs. As per the aspects of Income Tax credit at the time fulfilling obligations in

relation to output business unit has authority to reduce the liability to the amount that have

already paid on inputs. On the basis of such aspect, tax is paid by the firm on balance figure. In

accordance with such aspect, 10% of $550000 comes under the category of input tax credit.

Thus, Big Bank can claim for input tax credit amounted to AUD $55000. Along with this, in the

remaining expenses such as $1100000, 2% are related to advertisements. Hence, in relation to

insurance business additional input tax credit accounted for $2200 respectively. On the other

side, advertisement expenses pertaining to loan and deposit facilities offers by Big Bank Ltd

account for AUD $1078000. Thus, it can be said that input tax credit for the business of Big

Bank such as loan and deposit accounts for $107800 significantly.

Conclusion

From the cited case and as per ITAA (1997) it has been concluded that input tax credit

for Big Bank Home and content insurance policies related to the amount of AUD $57200

respectively. In contrast to this, tax liability pertaining to the business of loan and deposit is

$107800. Thus, it can be stated that Big bank can claim regarding input tax credit for each

business as per GST rules of ITAA, 1997.

QUESTION 3

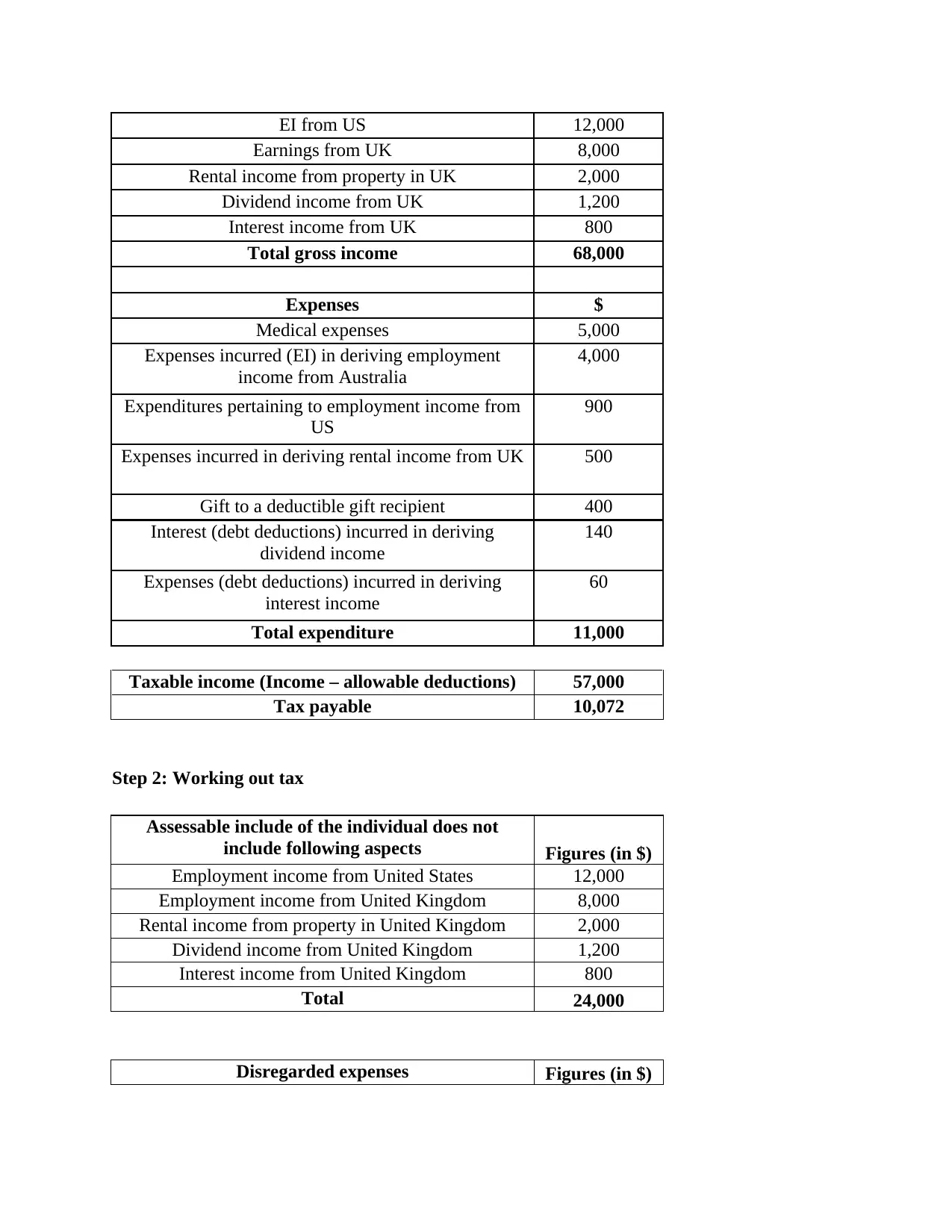

Determining foreign tax offset

For the determination of Angelo’s foreign tax offset three step process is considered such

as:

Step 1: Calculation of taxable income and associated liability

Particulars Amount (in

AUD $)

Gross income

Employment income (EI) from Australia 44,000

the goods or services. On the basis of legislation, it is highly required for Big Bank ltd to charge

GST from customers. In addition to this, firm has also right to claim for the business expenses

and other inputs. As per the aspects of Income Tax credit at the time fulfilling obligations in

relation to output business unit has authority to reduce the liability to the amount that have

already paid on inputs. On the basis of such aspect, tax is paid by the firm on balance figure. In

accordance with such aspect, 10% of $550000 comes under the category of input tax credit.

Thus, Big Bank can claim for input tax credit amounted to AUD $55000. Along with this, in the

remaining expenses such as $1100000, 2% are related to advertisements. Hence, in relation to

insurance business additional input tax credit accounted for $2200 respectively. On the other

side, advertisement expenses pertaining to loan and deposit facilities offers by Big Bank Ltd

account for AUD $1078000. Thus, it can be said that input tax credit for the business of Big

Bank such as loan and deposit accounts for $107800 significantly.

Conclusion

From the cited case and as per ITAA (1997) it has been concluded that input tax credit

for Big Bank Home and content insurance policies related to the amount of AUD $57200

respectively. In contrast to this, tax liability pertaining to the business of loan and deposit is

$107800. Thus, it can be stated that Big bank can claim regarding input tax credit for each

business as per GST rules of ITAA, 1997.

QUESTION 3

Determining foreign tax offset

For the determination of Angelo’s foreign tax offset three step process is considered such

as:

Step 1: Calculation of taxable income and associated liability

Particulars Amount (in

AUD $)

Gross income

Employment income (EI) from Australia 44,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

EI from US 12,000

Earnings from UK 8,000

Rental income from property in UK 2,000

Dividend income from UK 1,200

Interest income from UK 800

Total gross income 68,000

Expenses $

Medical expenses 5,000

Expenses incurred (EI) in deriving employment

income from Australia

4,000

Expenditures pertaining to employment income from

US

900

Expenses incurred in deriving rental income from UK 500

Gift to a deductible gift recipient 400

Interest (debt deductions) incurred in deriving

dividend income

140

Expenses (debt deductions) incurred in deriving

interest income

60

Total expenditure 11,000

Taxable income (Income – allowable deductions) 57,000

Tax payable 10,072

Step 2: Working out tax

Assessable include of the individual does not

include following aspects Figures (in $)

Employment income from United States 12,000

Employment income from United Kingdom 8,000

Rental income from property in United Kingdom 2,000

Dividend income from United Kingdom 1,200

Interest income from United Kingdom 800

Total 24,000

Disregarded expenses Figures (in $)

Earnings from UK 8,000

Rental income from property in UK 2,000

Dividend income from UK 1,200

Interest income from UK 800

Total gross income 68,000

Expenses $

Medical expenses 5,000

Expenses incurred (EI) in deriving employment

income from Australia

4,000

Expenditures pertaining to employment income from

US

900

Expenses incurred in deriving rental income from UK 500

Gift to a deductible gift recipient 400

Interest (debt deductions) incurred in deriving

dividend income

140

Expenses (debt deductions) incurred in deriving

interest income

60

Total expenditure 11,000

Taxable income (Income – allowable deductions) 57,000

Tax payable 10,072

Step 2: Working out tax

Assessable include of the individual does not

include following aspects Figures (in $)

Employment income from United States 12,000

Employment income from United Kingdom 8,000

Rental income from property in United Kingdom 2,000

Dividend income from United Kingdom 1,200

Interest income from United Kingdom 800

Total 24,000

Disregarded expenses Figures (in $)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

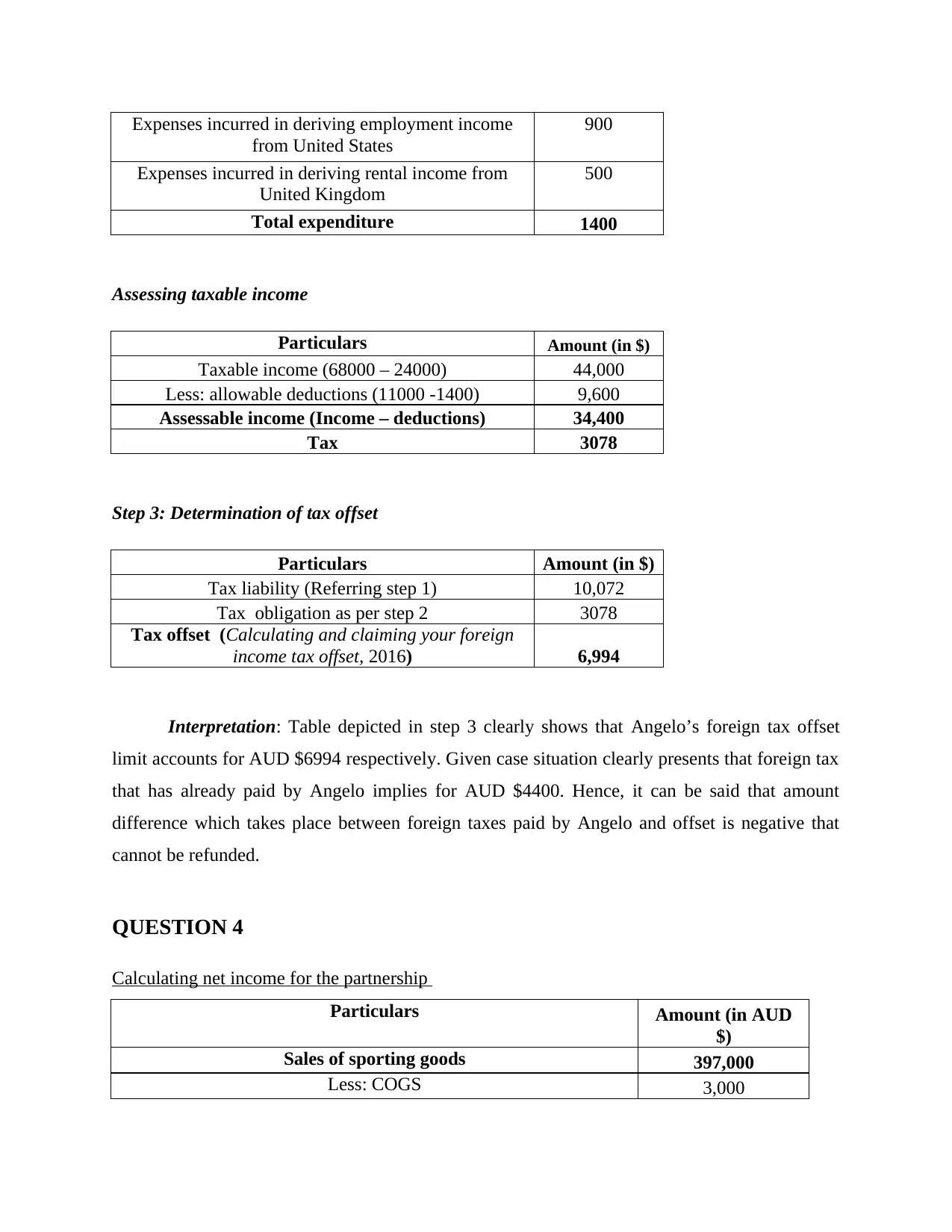

Expenses incurred in deriving employment income

from United States

900

Expenses incurred in deriving rental income from

United Kingdom

500

Total expenditure 1400

Assessing taxable income

Particulars Amount (in $)

Taxable income (68000 – 24000) 44,000

Less: allowable deductions (11000 -1400) 9,600

Assessable income (Income – deductions) 34,400

Tax 3078

Step 3: Determination of tax offset

Particulars Amount (in $)

Tax liability (Referring step 1) 10,072

Tax obligation as per step 2 3078

Tax offset (Calculating and claiming your foreign

income tax offset, 2016) 6,994

Interpretation: Table depicted in step 3 clearly shows that Angelo’s foreign tax offset

limit accounts for AUD $6994 respectively. Given case situation clearly presents that foreign tax

that has already paid by Angelo implies for AUD $4400. Hence, it can be said that amount

difference which takes place between foreign taxes paid by Angelo and offset is negative that

cannot be refunded.

QUESTION 4

Calculating net income for the partnership

Particulars Amount (in AUD

$)

Sales of sporting goods 397,000

Less: COGS 3,000

from United States

900

Expenses incurred in deriving rental income from

United Kingdom

500

Total expenditure 1400

Assessing taxable income

Particulars Amount (in $)

Taxable income (68000 – 24000) 44,000

Less: allowable deductions (11000 -1400) 9,600

Assessable income (Income – deductions) 34,400

Tax 3078

Step 3: Determination of tax offset

Particulars Amount (in $)

Tax liability (Referring step 1) 10,072

Tax obligation as per step 2 3078

Tax offset (Calculating and claiming your foreign

income tax offset, 2016) 6,994

Interpretation: Table depicted in step 3 clearly shows that Angelo’s foreign tax offset

limit accounts for AUD $6994 respectively. Given case situation clearly presents that foreign tax

that has already paid by Angelo implies for AUD $4400. Hence, it can be said that amount

difference which takes place between foreign taxes paid by Angelo and offset is negative that

cannot be refunded.

QUESTION 4

Calculating net income for the partnership

Particulars Amount (in AUD

$)

Sales of sporting goods 397,000

Less: COGS 3,000

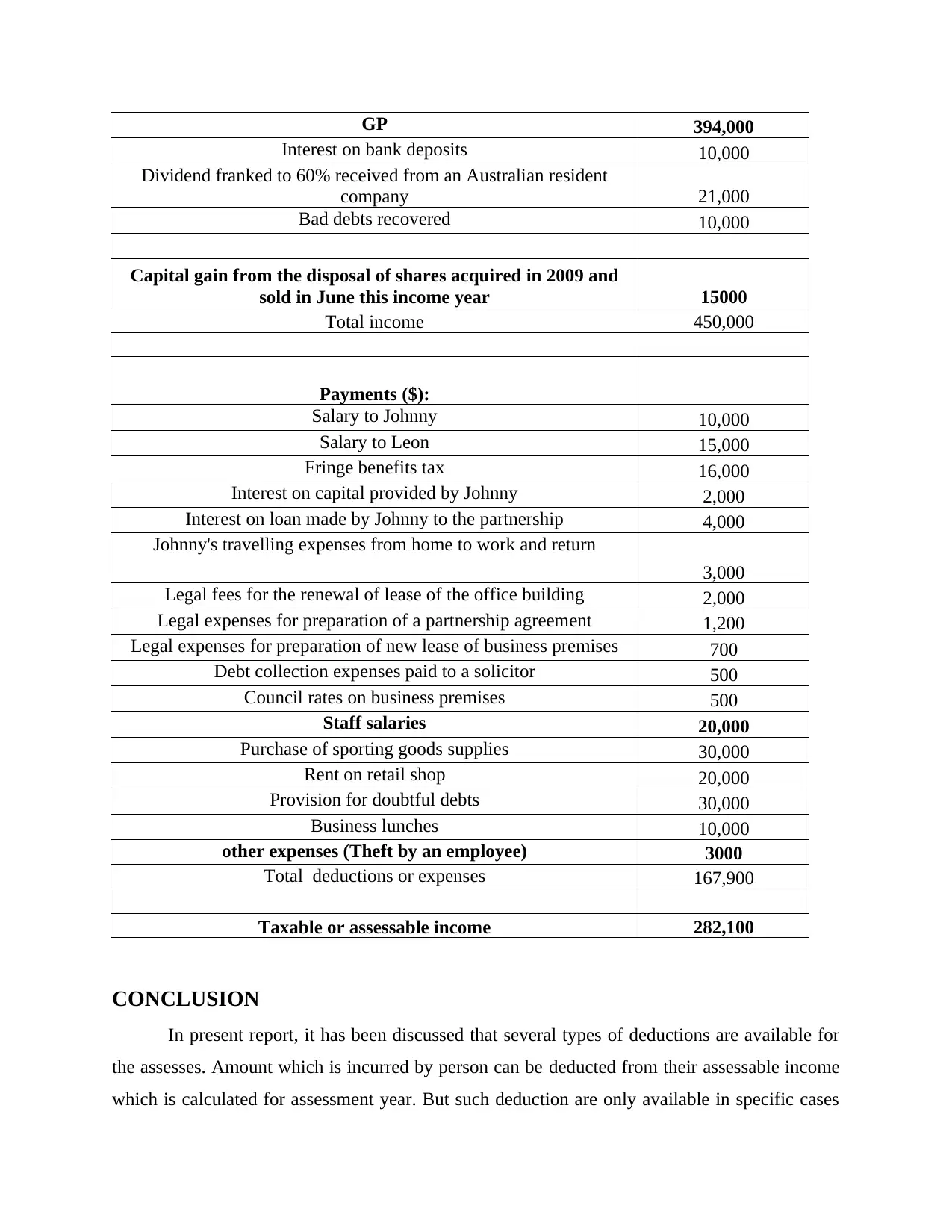

GP 394,000

Interest on bank deposits 10,000

Dividend franked to 60% received from an Australian resident

company 21,000

Bad debts recovered 10,000

Capital gain from the disposal of shares acquired in 2009 and

sold in June this income year 15000

Total income 450,000

Payments ($):

Salary to Johnny 10,000

Salary to Leon 15,000

Fringe benefits tax 16,000

Interest on capital provided by Johnny 2,000

Interest on loan made by Johnny to the partnership 4,000

Johnny's travelling expenses from home to work and return

3,000

Legal fees for the renewal of lease of the office building 2,000

Legal expenses for preparation of a partnership agreement 1,200

Legal expenses for preparation of new lease of business premises 700

Debt collection expenses paid to a solicitor 500

Council rates on business premises 500

Staff salaries 20,000

Purchase of sporting goods supplies 30,000

Rent on retail shop 20,000

Provision for doubtful debts 30,000

Business lunches 10,000

other expenses (Theft by an employee) 3000

Total deductions or expenses 167,900

Taxable or assessable income 282,100

CONCLUSION

In present report, it has been discussed that several types of deductions are available for

the assesses. Amount which is incurred by person can be deducted from their assessable income

which is calculated for assessment year. But such deduction are only available in specific cases

Interest on bank deposits 10,000

Dividend franked to 60% received from an Australian resident

company 21,000

Bad debts recovered 10,000

Capital gain from the disposal of shares acquired in 2009 and

sold in June this income year 15000

Total income 450,000

Payments ($):

Salary to Johnny 10,000

Salary to Leon 15,000

Fringe benefits tax 16,000

Interest on capital provided by Johnny 2,000

Interest on loan made by Johnny to the partnership 4,000

Johnny's travelling expenses from home to work and return

3,000

Legal fees for the renewal of lease of the office building 2,000

Legal expenses for preparation of a partnership agreement 1,200

Legal expenses for preparation of new lease of business premises 700

Debt collection expenses paid to a solicitor 500

Council rates on business premises 500

Staff salaries 20,000

Purchase of sporting goods supplies 30,000

Rent on retail shop 20,000

Provision for doubtful debts 30,000

Business lunches 10,000

other expenses (Theft by an employee) 3000

Total deductions or expenses 167,900

Taxable or assessable income 282,100

CONCLUSION

In present report, it has been discussed that several types of deductions are available for

the assesses. Amount which is incurred by person can be deducted from their assessable income

which is calculated for assessment year. But such deduction are only available in specific cases

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

only like no deduction available for capital expenses related to fixed assets but it should be

provide in revenue expenses. Organization which are incorporated and providing its services to

people than it should be responsible to pay amount of GST or income tax which are imposed on

them. In present report Angelo’s foreign tax offset has been calculated on the basis of his

income, expenses and foreign tax paid by him. Also two partners collectively selling sporting

goods and services. So that, their income has been calculated on the basis of information about

their further income and expenses which are available excluding GST.

provide in revenue expenses. Organization which are incorporated and providing its services to

people than it should be responsible to pay amount of GST or income tax which are imposed on

them. In present report Angelo’s foreign tax offset has been calculated on the basis of his

income, expenses and foreign tax paid by him. Also two partners collectively selling sporting

goods and services. So that, their income has been calculated on the basis of information about

their further income and expenses which are available excluding GST.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Butler, D. and Skandakumar, K., 2014. TR 2013/D7-apportioning SMSF expenses. Taxation in

Australia. 48(8). p.455.

Harrison, J. and Keating, M., 2014. The deductibility of Sarbanes-Oxley costs incurred by

Australasian companies. Accounting Research Journal. 27(1). pp.52-70.

Joseph, S.A., 2014. The polluter pays principle and land remediation: A comparison of the

United Kingdom and Australian approaches. AJEL. 1. p.24.

Mete, P., Dick, C. and Moerman, L., 2010. Creating institutional meaning: Accounting and

taxation law perspectives of carbon permits. Critical Perspectives on Accounting. 21(7).

pp.619-630.

Passant, J., McLaren, J.A. and Silaen, P., 2014. Are returns received by householders from

electricity generated by solar panels assessable income?.

Tran-Nam, B. and Evans, C., 2011. Tax policy simplification: An evaluation of the proposal for

a standard deduction for work related expenses. Austl. Tax F.. 26. p.719.

Online

Calculating and claiming your foreign income tax offset, 2016. [Online]. Available through:

<https://www.ato.gov.au/individuals/tax-return/2016/in-detail/publications/guide-to-

foreign-income-tax-offset-rules-2016/?

anchor=Calculating_your_offset_limit#Calculating_your_offset_limit> [Accessed on 14th

September 2017].

Income Tax Assessment Act 1997, 2009. [Pdf]. Available through:

<https://lawlex.com.au/tempstore/consolidated/5495.pdf> [Accessed on 14th September

2017].

Books and Journals

Butler, D. and Skandakumar, K., 2014. TR 2013/D7-apportioning SMSF expenses. Taxation in

Australia. 48(8). p.455.

Harrison, J. and Keating, M., 2014. The deductibility of Sarbanes-Oxley costs incurred by

Australasian companies. Accounting Research Journal. 27(1). pp.52-70.

Joseph, S.A., 2014. The polluter pays principle and land remediation: A comparison of the

United Kingdom and Australian approaches. AJEL. 1. p.24.

Mete, P., Dick, C. and Moerman, L., 2010. Creating institutional meaning: Accounting and

taxation law perspectives of carbon permits. Critical Perspectives on Accounting. 21(7).

pp.619-630.

Passant, J., McLaren, J.A. and Silaen, P., 2014. Are returns received by householders from

electricity generated by solar panels assessable income?.

Tran-Nam, B. and Evans, C., 2011. Tax policy simplification: An evaluation of the proposal for

a standard deduction for work related expenses. Austl. Tax F.. 26. p.719.

Online

Calculating and claiming your foreign income tax offset, 2016. [Online]. Available through:

<https://www.ato.gov.au/individuals/tax-return/2016/in-detail/publications/guide-to-

foreign-income-tax-offset-rules-2016/?

anchor=Calculating_your_offset_limit#Calculating_your_offset_limit> [Accessed on 14th

September 2017].

Income Tax Assessment Act 1997, 2009. [Pdf]. Available through:

<https://lawlex.com.au/tempstore/consolidated/5495.pdf> [Accessed on 14th September

2017].

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.