TAXATION 16 Assignment: Analyzing Deductions and GST in Taxation Law

VerifiedAdded on 2020/03/23

|18

|3140

|145

Homework Assignment

AI Summary

This assignment analyzes various aspects of taxation, focusing on permissible deductions and Goods and Services Tax (GST) credits under Australian tax law. The paper addresses several scenarios, including the deductibility of costs associated with moving equipment, revaluation of assets for insurance purposes, legal expenses related to business closure, and solicitor fees. It examines relevant legislation, particularly section 8-1 of the ITAA 1997, and provides detailed applications of the law to each scenario, referencing case law like British Insulated & Helsby Cables and FC of T v Snowden and Wilson Pty Ltd. The assignment also explores GST credits for advertising expenses, referencing the GST Act 1999 and rulings like GSTR 2006/3, and the application of the "extent" principle. The paper concludes with a discussion of whether the expenses are treated as income tax permissible deductions or not, and how the legal framework applies to various business expenses. It provides a comprehensive overview of the legal and practical aspects of taxation, with a focus on the implications for businesses and taxpayers.

Running Head: TAXATION 1

TAXATION

(Name)

(Institutional Affiliation)

TAXATION

(Name)

(Institutional Affiliation)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAXATION 2

Table of Contents

Question 1:.................................................................................................................................2

Requirement 1:...........................................................................................................................2

Issue:..........................................................................................................................................2

Legislations:...............................................................................................................................2

Applications:..............................................................................................................................2

Conclusion:................................................................................................................................3

Requirement 2:...........................................................................................................................3

Issue:..........................................................................................................................................3

Legislation:.................................................................................................................................4

Application:................................................................................................................................4

Conclusion:................................................................................................................................4

Requirement 3:...........................................................................................................................4

Issue:..........................................................................................................................................4

Legislation:.................................................................................................................................5

Application:................................................................................................................................5

Conclusion:................................................................................................................................6

Requirement 4:..........................................................................................................................6

Issue:..........................................................................................................................................6

Legislation:.................................................................................................................................6

Table of Contents

Question 1:.................................................................................................................................2

Requirement 1:...........................................................................................................................2

Issue:..........................................................................................................................................2

Legislations:...............................................................................................................................2

Applications:..............................................................................................................................2

Conclusion:................................................................................................................................3

Requirement 2:...........................................................................................................................3

Issue:..........................................................................................................................................3

Legislation:.................................................................................................................................4

Application:................................................................................................................................4

Conclusion:................................................................................................................................4

Requirement 3:...........................................................................................................................4

Issue:..........................................................................................................................................4

Legislation:.................................................................................................................................5

Application:................................................................................................................................5

Conclusion:................................................................................................................................6

Requirement 4:..........................................................................................................................6

Issue:..........................................................................................................................................6

Legislation:.................................................................................................................................6

TAXATION 3

Application:................................................................................................................................6

Conclusion:................................................................................................................................7

Question 2:.................................................................................................................................7

Issue:..........................................................................................................................................7

Legislation:.................................................................................................................................7

Application:................................................................................................................................8

Conclusion:..............................................................................................................................10

Question 3:...............................................................................................................................11

Question 4:...............................................................................................................................13

References................................................................................................................................14

Application:................................................................................................................................6

Conclusion:................................................................................................................................7

Question 2:.................................................................................................................................7

Issue:..........................................................................................................................................7

Legislation:.................................................................................................................................7

Application:................................................................................................................................8

Conclusion:..............................................................................................................................10

Question 3:...............................................................................................................................11

Question 4:...............................................................................................................................13

References................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TAXATION 4

Question 1

Requirement 1

Issue:

The issue to be discussed in this case is the manner in which deductions are permitted.

The discussion will be anchored on “section 8-1 of the ITAA 1997”. The permission is always

given in relation to the costs that are incurred in the transactions done to acquire the shifting

machine.

Legislations:

Two types of legislations will be used in the analysis of this question. The first one has

been mentioned before as “section 8-1of the ITAA 1997” and secondly is the “British Insulated

and Helsby Cables.”

Applications:

The cost that has emanated from moving the device to a fresh area which depicts capital

expenditure as well as deductions is not permissible within the law section of “8-1 of the Income

Tax Assessment Act 1997” . The issue of depreciation has adversely affected the movement of

assets and the records indicate that the cost would really increase. The cost which has come up

for relocating the device to the other places indicate a cost that precedes from trivial adjustments

and means that can be admissible like similar deductions in “section 8-1 of the ITAA 1997”. The

main rationale for considering the expenses for admissible deductions is due to the outlay which

is deemed as the section of the enterprise charges emanating from the daily business activities.

(Bammens, 2013)

Question 1

Requirement 1

Issue:

The issue to be discussed in this case is the manner in which deductions are permitted.

The discussion will be anchored on “section 8-1 of the ITAA 1997”. The permission is always

given in relation to the costs that are incurred in the transactions done to acquire the shifting

machine.

Legislations:

Two types of legislations will be used in the analysis of this question. The first one has

been mentioned before as “section 8-1of the ITAA 1997” and secondly is the “British Insulated

and Helsby Cables.”

Applications:

The cost that has emanated from moving the device to a fresh area which depicts capital

expenditure as well as deductions is not permissible within the law section of “8-1 of the Income

Tax Assessment Act 1997” . The issue of depreciation has adversely affected the movement of

assets and the records indicate that the cost would really increase. The cost which has come up

for relocating the device to the other places indicate a cost that precedes from trivial adjustments

and means that can be admissible like similar deductions in “section 8-1 of the ITAA 1997”. The

main rationale for considering the expenses for admissible deductions is due to the outlay which

is deemed as the section of the enterprise charges emanating from the daily business activities.

(Bammens, 2013)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAXATION 5

In reference to the results given in the scenario of “British Insulated &Helsby Cables”,

the cost that comes up from the bearing defines a continuous benefit on the trade-associated

areas by identifying assets that can undergo depreciation. In accordance with the “Taxation

Ruling of TD 93/126” about the fixing of the devices and beginning of its functionality, the

amount of value to bring the machine to total operation will always be recorded as revenue. It

has been considered under the current state of affairs that the incidence of cost in identifying the

device to the new site defines an environment of cost of capital and will be handled like

permissible deductions. (Arnold, 2011)

Conclusions:

It can be inferred from the above discussion that the movement of the machine from one

place to another is not permissible. This is aimed at avoiding various deductions which are

treated as capital cost. Section 8-1 of the ITAA 1997 of the law gives all the provisions that guide

the manner in which the costs are handled and the resulting deductions.

Requirement 2:

Issue:

The present scenario is accustomed to if the reassessment of assets to influence the

insurance policy would be taken as permissible deductions or not. These are also provisions of

“section 8-1 ITAA 1997”.

Legislation

The only form of legislation in this case would be the provisions of the “section 8-1 ITAA

1997”.

In reference to the results given in the scenario of “British Insulated &Helsby Cables”,

the cost that comes up from the bearing defines a continuous benefit on the trade-associated

areas by identifying assets that can undergo depreciation. In accordance with the “Taxation

Ruling of TD 93/126” about the fixing of the devices and beginning of its functionality, the

amount of value to bring the machine to total operation will always be recorded as revenue. It

has been considered under the current state of affairs that the incidence of cost in identifying the

device to the new site defines an environment of cost of capital and will be handled like

permissible deductions. (Arnold, 2011)

Conclusions:

It can be inferred from the above discussion that the movement of the machine from one

place to another is not permissible. This is aimed at avoiding various deductions which are

treated as capital cost. Section 8-1 of the ITAA 1997 of the law gives all the provisions that guide

the manner in which the costs are handled and the resulting deductions.

Requirement 2:

Issue:

The present scenario is accustomed to if the reassessment of assets to influence the

insurance policy would be taken as permissible deductions or not. These are also provisions of

“section 8-1 ITAA 1997”.

Legislation

The only form of legislation in this case would be the provisions of the “section 8-1 ITAA

1997”.

TAXATION 6

Application:

As it can be seen from the current scenario, it can be deduced that the expenses have a

union with the non current asset, thus in computing the deductions it is prudent to ascertain

whether such expenditure has happened in revaluation which is acquired in improving the

production capacity of revenue or it is merely done in safeguarding the property (Ault, 2010). If

the other application results in the outline of earnings of temporary being, maybe given the state

that expenditure is probably a repetition in nature, then it would be taken care of as permissible

deductions according to “section 8-1 of ITAA”. A realistic confirmation obtained from the

current state occurrence of cost in revaluation of the asset as a result of the f insurance policy

will be admitted as income taxable deductions. Section 8-1 gives further clarification for this

issue from the period when the steady flow that has occurred is most probably undergoing

repetition. (Lodin, 2011)

Conclusion:

As a result of the assessment that has been done over the cost of revaluation, it can be

conclude that insurance policy costs are treated as income tax permissible deductions.

Subsequently the charge is treated as sporadic and it should be treated as the as allowable

deductions upon income as it is the provisions of section 8-1 of the ITAA 1997.

Requirement 3:

Issue:

The declaration initiates the occurrences that enhance the question of whether the lawful

expenditure which has been sustained by a taxpayer with the reason of objecting the need for

Application:

As it can be seen from the current scenario, it can be deduced that the expenses have a

union with the non current asset, thus in computing the deductions it is prudent to ascertain

whether such expenditure has happened in revaluation which is acquired in improving the

production capacity of revenue or it is merely done in safeguarding the property (Ault, 2010). If

the other application results in the outline of earnings of temporary being, maybe given the state

that expenditure is probably a repetition in nature, then it would be taken care of as permissible

deductions according to “section 8-1 of ITAA”. A realistic confirmation obtained from the

current state occurrence of cost in revaluation of the asset as a result of the f insurance policy

will be admitted as income taxable deductions. Section 8-1 gives further clarification for this

issue from the period when the steady flow that has occurred is most probably undergoing

repetition. (Lodin, 2011)

Conclusion:

As a result of the assessment that has been done over the cost of revaluation, it can be

conclude that insurance policy costs are treated as income tax permissible deductions.

Subsequently the charge is treated as sporadic and it should be treated as the as allowable

deductions upon income as it is the provisions of section 8-1 of the ITAA 1997.

Requirement 3:

Issue:

The declaration initiates the occurrences that enhance the question of whether the lawful

expenditure which has been sustained by a taxpayer with the reason of objecting the need for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TAXATION 7

closing up the entity would be considered for tax which has admissible deductions but within the

provisions of section 8-1 of the ITAA 1997.

Legislations:

The forms of laws that will be used in the analysis of the issue above would include “Section 8-1

of ITAA” and “FC of T v Snowden and Wilson Pty Ltd (1958)”

Application:

With reference to the aforementioned issue and within the provisions of “section 8-1 of

the ITAA 1997”, the costs that have been incurred in closing up the enterprise have not been

determined as admissible deductions on income. The taxation ruling of ID 2004/367 stands in for

the lawful expenditure which will be sought for deductions if the charges are for executing the

enterprise activities where an individual gives out the records of the taxable income. (HJI, 2015)

Basing on the suit of FC of T v Snowden and Wilson Pty Ltd (1958) expenditure which is

not common to the taxpayer in later occasion are necessary to begin the legal process as in no

occurrences does it hinder the application of expenses needed to meet the threshold as expenses

that are liable for the normal deductions. (Milne, 2012)

The incident of authorized expenditure for overlapping in closing down the request will

not be admitted as deductions since they stand in for the definition of capital. This expenditure is

associated with the activities of the enterprise. (In Avi-Yonah, 2016)

Conclusion

In relation to the assessment that has been carried out regarding the charges that occured

in the objection efforts to close down the enterprise will be treated according to the

closing up the entity would be considered for tax which has admissible deductions but within the

provisions of section 8-1 of the ITAA 1997.

Legislations:

The forms of laws that will be used in the analysis of the issue above would include “Section 8-1

of ITAA” and “FC of T v Snowden and Wilson Pty Ltd (1958)”

Application:

With reference to the aforementioned issue and within the provisions of “section 8-1 of

the ITAA 1997”, the costs that have been incurred in closing up the enterprise have not been

determined as admissible deductions on income. The taxation ruling of ID 2004/367 stands in for

the lawful expenditure which will be sought for deductions if the charges are for executing the

enterprise activities where an individual gives out the records of the taxable income. (HJI, 2015)

Basing on the suit of FC of T v Snowden and Wilson Pty Ltd (1958) expenditure which is

not common to the taxpayer in later occasion are necessary to begin the legal process as in no

occurrences does it hinder the application of expenses needed to meet the threshold as expenses

that are liable for the normal deductions. (Milne, 2012)

The incident of authorized expenditure for overlapping in closing down the request will

not be admitted as deductions since they stand in for the definition of capital. This expenditure is

associated with the activities of the enterprise. (In Avi-Yonah, 2016)

Conclusion

In relation to the assessment that has been carried out regarding the charges that occured

in the objection efforts to close down the enterprise will be treated according to the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAXATION 8

considerations as not permissible income tax deductions in regard to the provisions of section 8-1

of the ITAA 1997.

Requirement 4

Issue:

The declaration in the subject extends the matter of ascertaining if or not the official

payout for sourcing the services of solicitor so that they can execute various business activities of

those who pay taxes will be regarded as the allowable income tax deductions according to the

provisions envisaged in section 8-1 of the ITAA 1997.

Legislation

The type of legislation that would be referred to would border on the “section 8-1 of ITAA

1997”. Notably, this form of legislation has been quoted extensively in this discussion.

Apparently, it is a rich case which has set precedence for other referrals in terms of the taxation

subject matter. It would still form a strong basis under which the above quoted issue would be

examined.

Application

The introduction of this statement that has been carefully done in reference to the

background of section 8-1 of the Income Tax Assessment Act 1997, every time the taxpayer is

subjected to a permissible expense with the aim of executing several commercial activities so

that they can obtain maximum yields in terms of profitability. However, there exist certain types

of exemption to the provisions of “section 8-1 of the ITAA” where the occasion of authorized

considerations as not permissible income tax deductions in regard to the provisions of section 8-1

of the ITAA 1997.

Requirement 4

Issue:

The declaration in the subject extends the matter of ascertaining if or not the official

payout for sourcing the services of solicitor so that they can execute various business activities of

those who pay taxes will be regarded as the allowable income tax deductions according to the

provisions envisaged in section 8-1 of the ITAA 1997.

Legislation

The type of legislation that would be referred to would border on the “section 8-1 of ITAA

1997”. Notably, this form of legislation has been quoted extensively in this discussion.

Apparently, it is a rich case which has set precedence for other referrals in terms of the taxation

subject matter. It would still form a strong basis under which the above quoted issue would be

examined.

Application

The introduction of this statement that has been carefully done in reference to the

background of section 8-1 of the Income Tax Assessment Act 1997, every time the taxpayer is

subjected to a permissible expense with the aim of executing several commercial activities so

that they can obtain maximum yields in terms of profitability. However, there exist certain types

of exemption to the provisions of “section 8-1 of the ITAA” where the occasion of authorized

TAXATION 9

expenditure that has occurred show the quality of capital, local and personal expense or the

expenditure is undertaken in admitting the excluded and free proceeds. (Morrison, 2015)

In regard to the above discussion, for a person to incur an authorized fee, that may not be

taken as permissible deductions given that there is no type of union has been reached in coming

up with the taxable revenue. In the perspective of the current state of affairs that has been

presented in the present matter, it is determined that authorized expenses are directly associated

with the taxpayers enterprise with the aim of creating the taxable returns and ways to be admitted

as deductions upon income. This too is well covered under “section 8-1 of the ITAA 1997.”

(Dourado, 2013)

Conclusion

According to the above argument authorized costs took place in regard to the enterprise activities

to create the taxable revenue should be handled as deductions that have been allowed while

alluding to “section 8-1 of the ITAA 1997.”

Question 2

Issue

The current situation of Big Bank is related with determining the contribution to tax

credit for the announcing expenses that Big Bank has had to bear while paying attention to the

provisions of “GSTR Act 1999.”

Legislation:

expenditure that has occurred show the quality of capital, local and personal expense or the

expenditure is undertaken in admitting the excluded and free proceeds. (Morrison, 2015)

In regard to the above discussion, for a person to incur an authorized fee, that may not be

taken as permissible deductions given that there is no type of union has been reached in coming

up with the taxable revenue. In the perspective of the current state of affairs that has been

presented in the present matter, it is determined that authorized expenses are directly associated

with the taxpayers enterprise with the aim of creating the taxable returns and ways to be admitted

as deductions upon income. This too is well covered under “section 8-1 of the ITAA 1997.”

(Dourado, 2013)

Conclusion

According to the above argument authorized costs took place in regard to the enterprise activities

to create the taxable revenue should be handled as deductions that have been allowed while

alluding to “section 8-1 of the ITAA 1997.”

Question 2

Issue

The current situation of Big Bank is related with determining the contribution to tax

credit for the announcing expenses that Big Bank has had to bear while paying attention to the

provisions of “GSTR Act 1999.”

Legislation:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TAXATION

10

Just like other issues, this one will be addressed with reference to other sets of law which include

GST Act 1999, “Goods and Service taxation ruling of GSTR 2006/3” and Ronpibon Tin NL v.

FC of T.

Application:

As it has been rightly quoted under the “Goods and Service taxation ruling of GSTR 2006/3”it

gives the personal taxpayers the requisite management involving the ways of executing the

judgment to settle on the items concerning tax costs. Away from this the judgment also gives the

solution through which the payers of tax can advocate for change that is used for the financial

supplies inside the structure of fresh structure of tax “GST Act 1999”. It also takes stock of the

enormity of the laudable principle and the real purpose for the use of the “Goods and Service

taxation ruling of GSTR 2006/3” under “division 11-15 and 129 of the GST Act 1999”. (Evans,

2011)

As witnessed in the modern situation of Big Bank, it lays a basis that the bank has bred

the notion to an expenditure of about $1,650,000, which also has the sum required for

promotions in the previous year. As exhibited in the current conditions of Big Bank, the taxation

judgment of Goods as well as Service taxation verdict of “GSTR 2006/3” is appropriate for the

corporation since the firm is eligible and suitable for input tax credit or reduced input tax credit

(Woellner,2014). According to the judgment, if an organization has been formalized and is

expected to acquire registration, GST shall bear the liability of implementing the supplies

amounting from taxation. The arrangement of GST guidelines holds that a taxable organization

under the critical situations is expected to claim rights of input tax credit for the supply of goods

that comprise of the sum of the GST that is obtained through the business organization. As

10

Just like other issues, this one will be addressed with reference to other sets of law which include

GST Act 1999, “Goods and Service taxation ruling of GSTR 2006/3” and Ronpibon Tin NL v.

FC of T.

Application:

As it has been rightly quoted under the “Goods and Service taxation ruling of GSTR 2006/3”it

gives the personal taxpayers the requisite management involving the ways of executing the

judgment to settle on the items concerning tax costs. Away from this the judgment also gives the

solution through which the payers of tax can advocate for change that is used for the financial

supplies inside the structure of fresh structure of tax “GST Act 1999”. It also takes stock of the

enormity of the laudable principle and the real purpose for the use of the “Goods and Service

taxation ruling of GSTR 2006/3” under “division 11-15 and 129 of the GST Act 1999”. (Evans,

2011)

As witnessed in the modern situation of Big Bank, it lays a basis that the bank has bred

the notion to an expenditure of about $1,650,000, which also has the sum required for

promotions in the previous year. As exhibited in the current conditions of Big Bank, the taxation

judgment of Goods as well as Service taxation verdict of “GSTR 2006/3” is appropriate for the

corporation since the firm is eligible and suitable for input tax credit or reduced input tax credit

(Woellner,2014). According to the judgment, if an organization has been formalized and is

expected to acquire registration, GST shall bear the liability of implementing the supplies

amounting from taxation. The arrangement of GST guidelines holds that a taxable organization

under the critical situations is expected to claim rights of input tax credit for the supply of goods

that comprise of the sum of the GST that is obtained through the business organization. As

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAXATION

11

highlighted in the GSTR judgment, a business entity that undertakes a business supplies activity

and extends the business acquirement threshold, such brand of business organization will not

possess any rights to restore the total GST demanded. Nonetheless, such a move would amount

to a section of the GST which could be restored by the firm. (Barkoczy, 2017)

Referring to the inference in “Ronpibon Tin NL v. FC of T” the principle of “extent” and

“to the extent” is realistically executed in the interrogation of the legislations of GST. This

makes up the duty under which the technique of allocation which is adopted must be fair and

realistic in scenarios of the definite venture. As seen in “paragraph 11-5 and 15-5” to meet the

necessities of a possession as the worthy acquirement the business unit has to be laudable either

in totality or in segments.( Abdulrazaq, 2015)

As highlighted and discussed in regard of “paragraph 11-5 (a) and 15-5 (a)”, for any

entity to come up with a fiscal attainment to meet the expectations of “GSTR 2006/6” for

meeting the threshold as the laudable import, it is quite sensible that the acquirement which has

been initiated by the entity should be totally worthy. In the scenario where it is realized that the

attainment is partially for the laudable reason, then it is quite sensible again to ensure that the

sureness and credibility of the process is guaranteed. As it has been highlighted within the

“subsection 15-25 of the GSTR 2006/6”, any import will only be viewed as creditable if the

business organization makes monetary supplies with the aim of laying claim to the right of input

tax credit. It is arguable that this can be extended so that the announcements concerning the

expenses and concerning the Big Bank in the current situation undergo the required threshold.

Furthermore, the proof of purchase that has been offered will be considered for the reason of

input tax credit relating to the supplies of the GST that is incurred by the Big Bank. (Sangkuhl,

2015)

11

highlighted in the GSTR judgment, a business entity that undertakes a business supplies activity

and extends the business acquirement threshold, such brand of business organization will not

possess any rights to restore the total GST demanded. Nonetheless, such a move would amount

to a section of the GST which could be restored by the firm. (Barkoczy, 2017)

Referring to the inference in “Ronpibon Tin NL v. FC of T” the principle of “extent” and

“to the extent” is realistically executed in the interrogation of the legislations of GST. This

makes up the duty under which the technique of allocation which is adopted must be fair and

realistic in scenarios of the definite venture. As seen in “paragraph 11-5 and 15-5” to meet the

necessities of a possession as the worthy acquirement the business unit has to be laudable either

in totality or in segments.( Abdulrazaq, 2015)

As highlighted and discussed in regard of “paragraph 11-5 (a) and 15-5 (a)”, for any

entity to come up with a fiscal attainment to meet the expectations of “GSTR 2006/6” for

meeting the threshold as the laudable import, it is quite sensible that the acquirement which has

been initiated by the entity should be totally worthy. In the scenario where it is realized that the

attainment is partially for the laudable reason, then it is quite sensible again to ensure that the

sureness and credibility of the process is guaranteed. As it has been highlighted within the

“subsection 15-25 of the GSTR 2006/6”, any import will only be viewed as creditable if the

business organization makes monetary supplies with the aim of laying claim to the right of input

tax credit. It is arguable that this can be extended so that the announcements concerning the

expenses and concerning the Big Bank in the current situation undergo the required threshold.

Furthermore, the proof of purchase that has been offered will be considered for the reason of

input tax credit relating to the supplies of the GST that is incurred by the Big Bank. (Sangkuhl,

2015)

TAXATION

12

Conclusion:

It has been observed in the above definition that the assessment of the case study can be

inferred that Big Bank Ltd meets the threshold to lay claim on the input tax credit which has

been envisaged and adequately described in the “GSTR 2006/13” for the amount that is

continuous on the issue of announcing the status of the expenses.

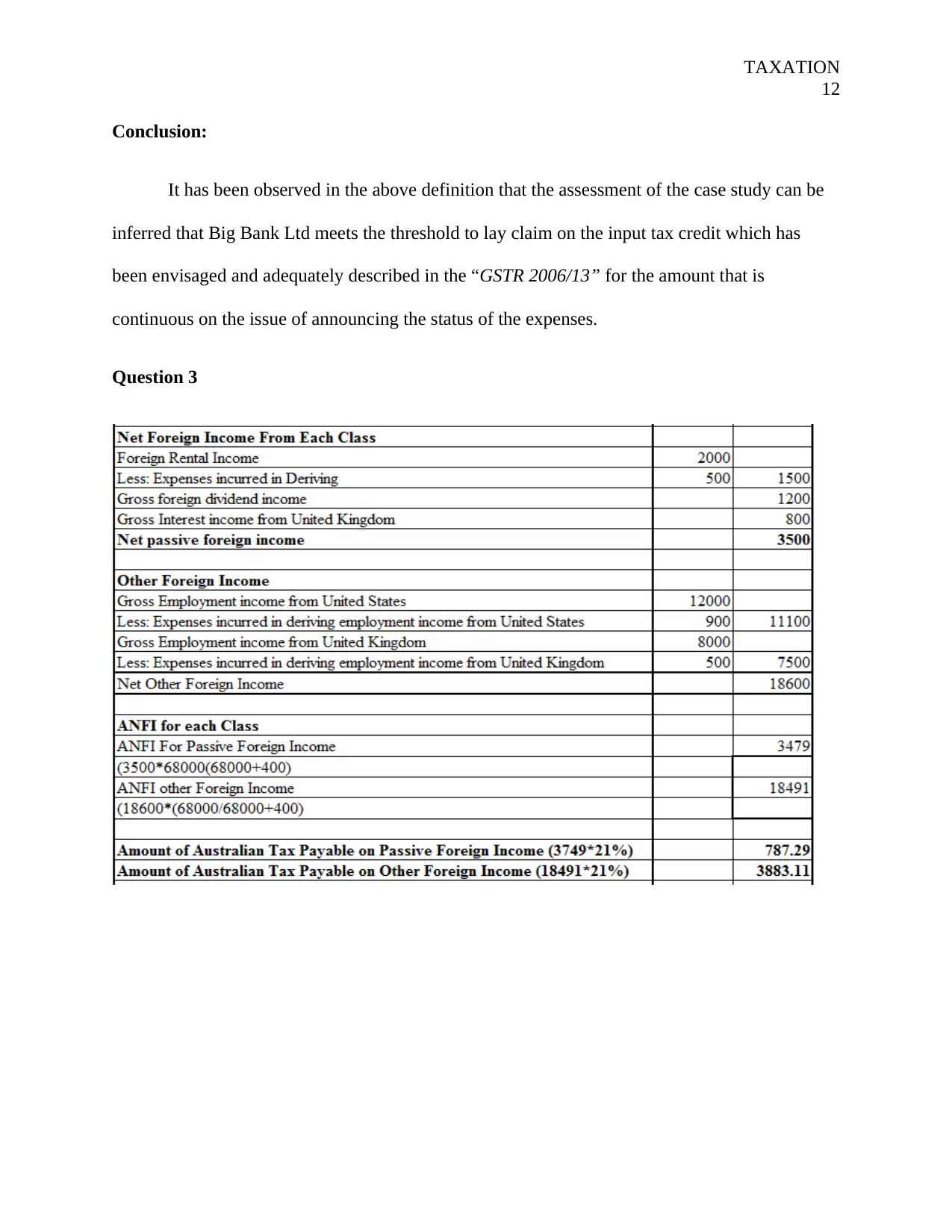

Question 3

12

Conclusion:

It has been observed in the above definition that the assessment of the case study can be

inferred that Big Bank Ltd meets the threshold to lay claim on the input tax credit which has

been envisaged and adequately described in the “GSTR 2006/13” for the amount that is

continuous on the issue of announcing the status of the expenses.

Question 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.