University Taxation Law Assignment: Payroll, GST, and Income Tax

VerifiedAdded on 2021/12/28

|9

|1108

|26

Homework Assignment

AI Summary

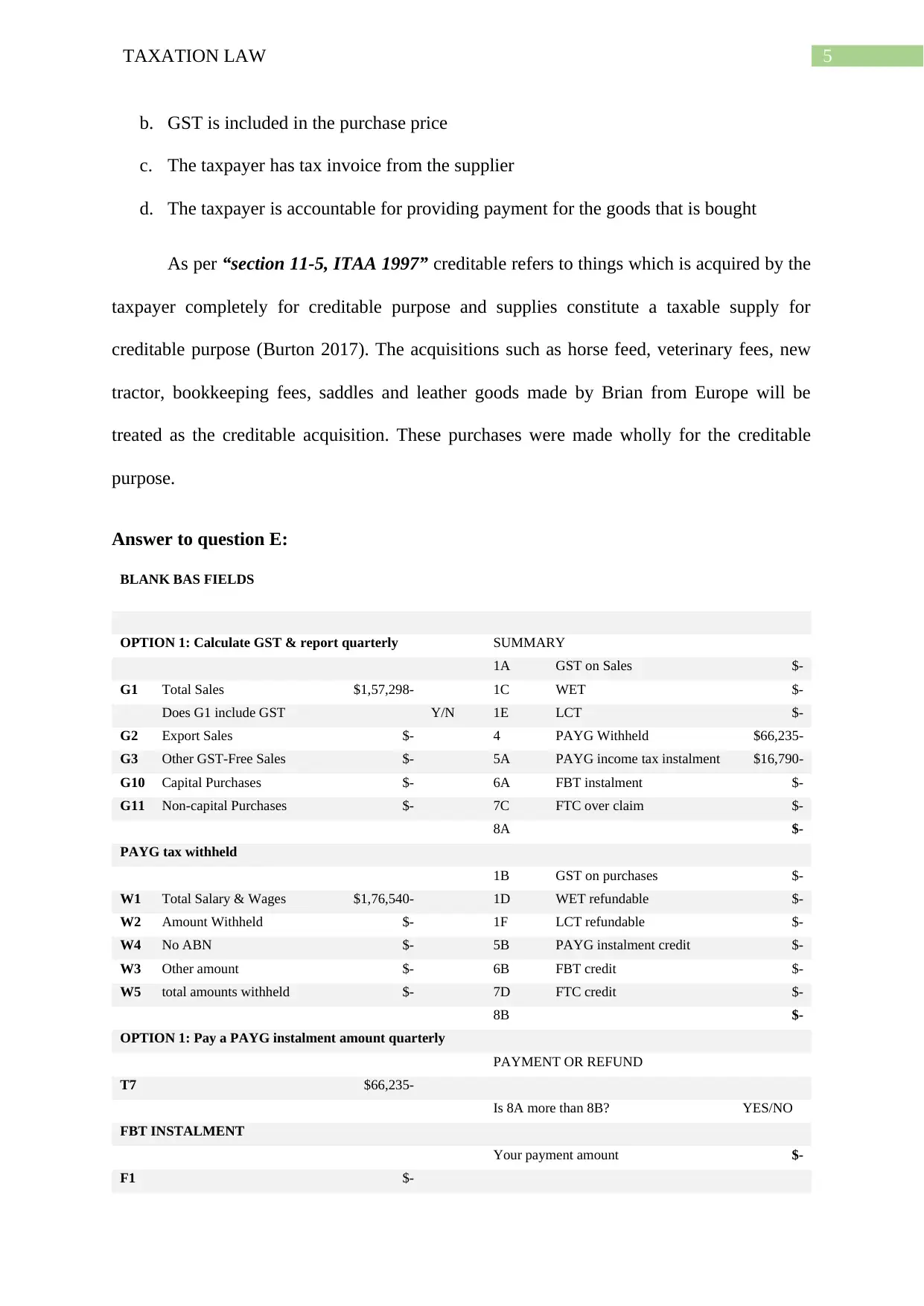

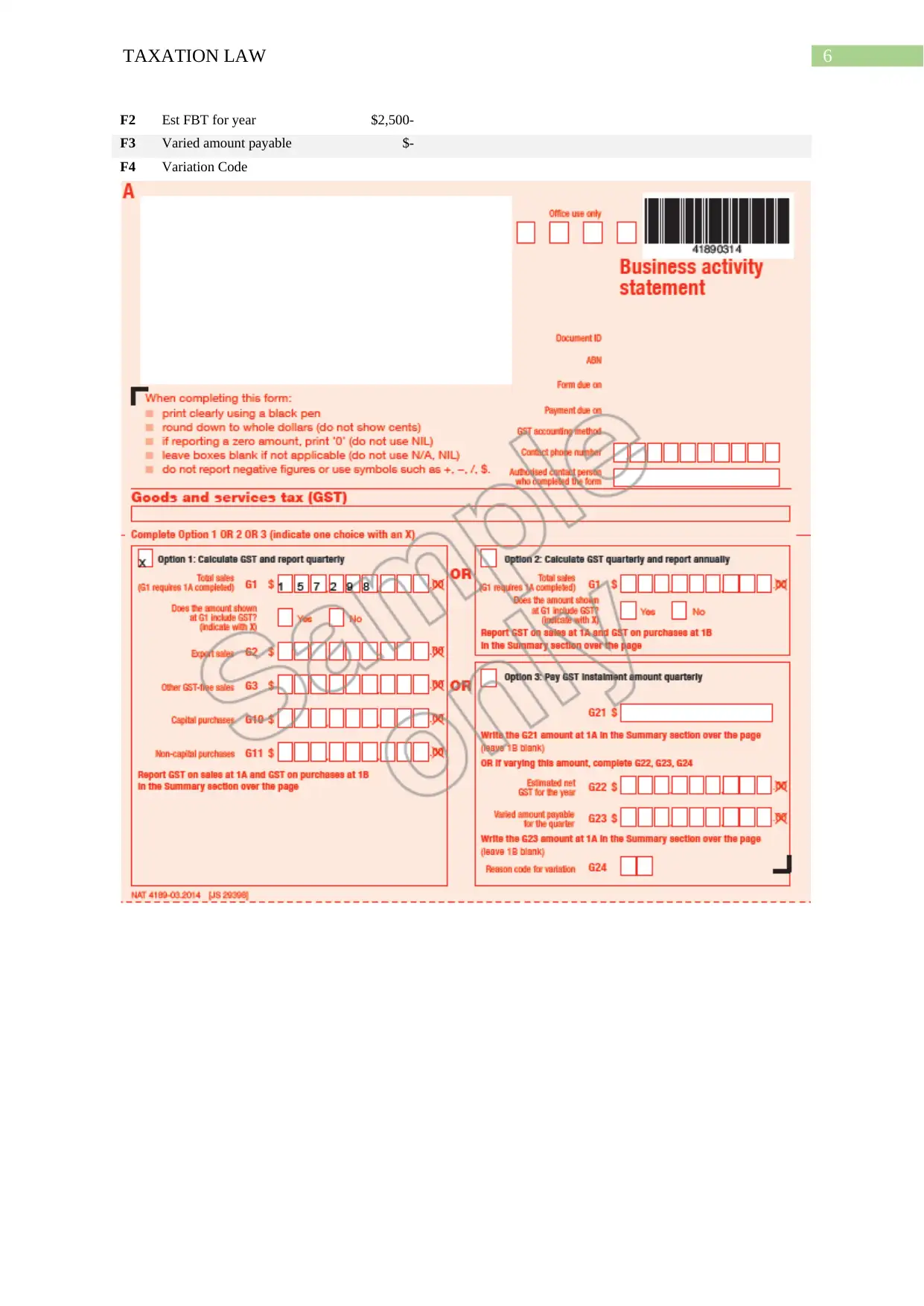

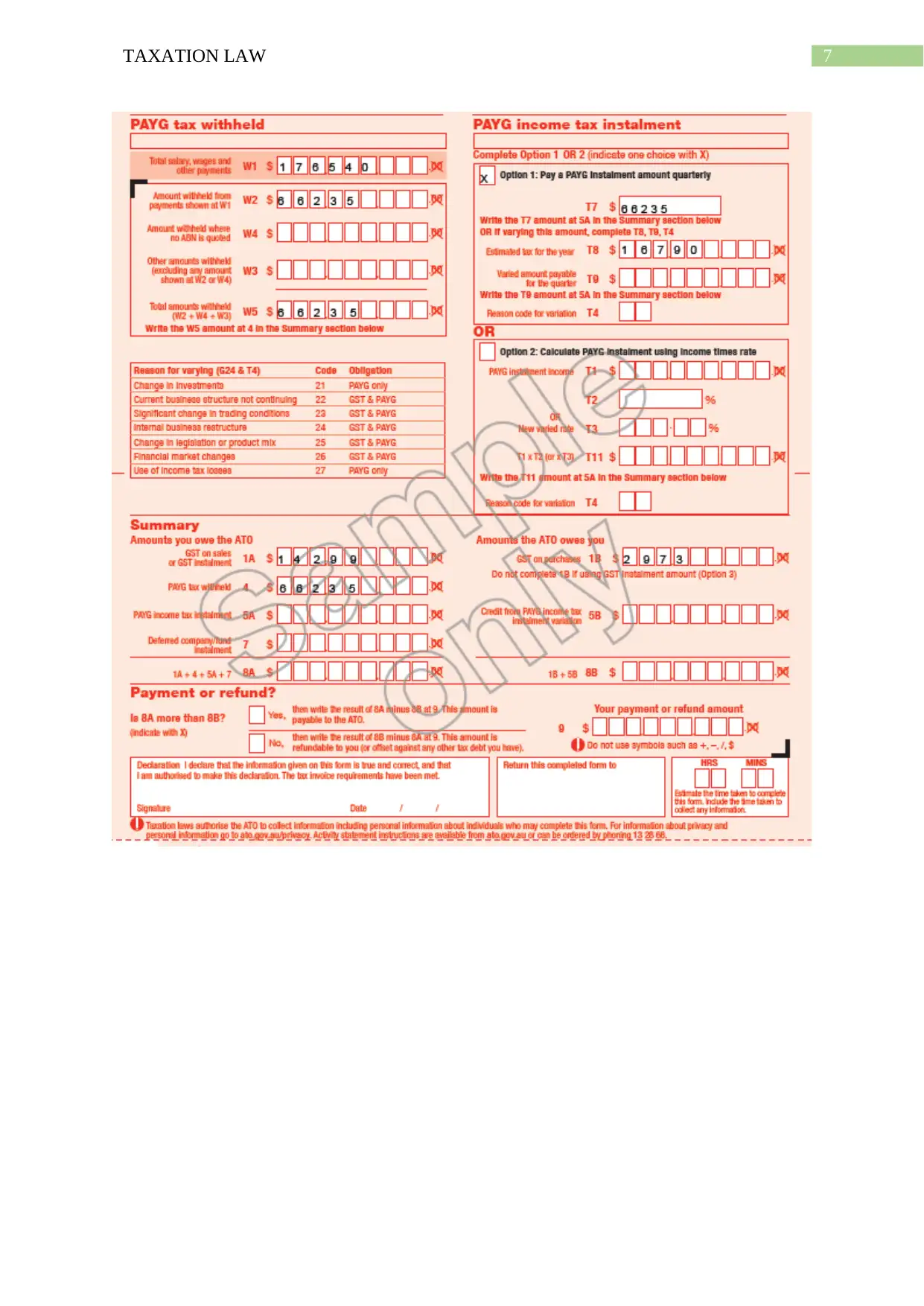

This Taxation Law assignment addresses several key areas of Australian taxation. It begins with the computation of a payroll schedule and the calculation of an employer's statutory Superannuation Guarantee obligations. The assignment then delves into the classification of income, distinguishing between ordinary and assessable income, citing relevant sections of the ITAA 1997 and legal precedents like Scott v Commissioner of Taxation (1935). The analysis includes income from training payments, customer share of prizes on horses, and the trade-in of a tractor. Furthermore, the assignment covers permissible deductions for expenses such as horse feed, veterinary fees, and accommodation costs, referencing Ronpibon Nil NL v FCT (1949). The document also discusses GST credits and creditable acquisitions, as defined by section 11-5 of the ITAA 1997. Finally, the assignment concludes with a BLANK BAS FIELDS OPTION 1, outlining the calculation and reporting of GST on sales and purchases, PAYG, and other relevant financial figures, as well as the FBT instalment. The solution provides a detailed breakdown of each aspect, including the application of relevant tax laws and case precedents.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.