Taxation Law Report: Analysis of ITAA 1997 for Britney's Income

VerifiedAdded on 2023/06/10

|10

|2669

|274

Report

AI Summary

This report provides an analysis of taxation law, focusing on the Income Tax Assessment Act 1997 (ITAA 1997). It examines various income scenarios and their tax implications for an individual named Britney. The report covers key aspects such as assessable income, including ordinary and statutory income, and exempt income like scholarships. It analyzes different situations, including salary, superannuation, work-related expenses (clothing), license fees, capital expenditure (copyright), gifts, and rental income. The report also discusses tax deductions related to legal fees and commission expenses. The conclusion summarizes the assessable income, deductions, and calculates Britney's taxable income and tax liability, including the HELP debt repayment. The analysis demonstrates how different sections of the ITAA 1997 apply to specific situations, providing a comprehensive overview of tax calculations and compliance.

Taxation Law LAWS3222

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

1...................................................................................................................................................3

2...................................................................................................................................................3

3...................................................................................................................................................4

4...................................................................................................................................................5

5...................................................................................................................................................5

6...................................................................................................................................................6

7...................................................................................................................................................7

8. CONCLUSION............................................................................................................................7

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

1...................................................................................................................................................3

2...................................................................................................................................................3

3...................................................................................................................................................4

4...................................................................................................................................................5

5...................................................................................................................................................5

6...................................................................................................................................................6

7...................................................................................................................................................7

8. CONCLUSION............................................................................................................................7

REFERENCES................................................................................................................................1

INTRODUCTION

The income tax assessment act 1997 is the act which outlines all the laws relating to the taxation

of the individual and the business. this is necessary for the reason that this act provides all the

guidance that how the different element is being treated in order to calculate the tax and try to

meet all the tax related obligations. The division 4 and 6 of this act relates with ‘how to work out

the income tax payable on the taxable income of the person’ and ‘assessable income and exempt

income respectively’. Hence, the knowledge of both these divisions will be leading to better

treatment of the different situation being provided. The current study will outline the different

situations and how in every situation the event will be treated with respect to the tax guidelines

and the ITAA 1997. This compliance is very necessary because in case it will not be there the it

will be affecting the tax calculation and will be improving the efficiency as well.

1.

As per Section 6-5 of ITAA 1997, the amount of $5000 received by Britney as a scholarship is

an exempt income. It is because the section 6-5 state that the scholarship granted by the

University to meet the cost of education is exempt from Income Tax purpose in Australia.

Hence, in the given question the $5000 received by Britney is an exempt income and thus

excluded from the assessable income of Britney1. The assessable income basically includes

ordinary income plus statutory income.

2.

As per Section 6-5 of ITAA 1997, assessable income includes both ordinary as well as statutory

income and exclude exempt income and non-assessable non-exempt income. Further, as per

section 6(1) of ITAA 1997, ordinary income means the income consisting of earnings, salaries,

wages, commission, fees, bonuses, pensions, superannuation allowances, renting allowances,

retiring gratuity and gratuity received in relation to any service rendered etc. Thus, the gross

salary and superannuation contribution of Britney of $60000 plus 9.5% is considered as ordinary

1 Christians, Allison, and Laurens van Apeldoorn. "Taxing income where value is created." Fla.

Tax Rev. 22 (2018): 1.

The income tax assessment act 1997 is the act which outlines all the laws relating to the taxation

of the individual and the business. this is necessary for the reason that this act provides all the

guidance that how the different element is being treated in order to calculate the tax and try to

meet all the tax related obligations. The division 4 and 6 of this act relates with ‘how to work out

the income tax payable on the taxable income of the person’ and ‘assessable income and exempt

income respectively’. Hence, the knowledge of both these divisions will be leading to better

treatment of the different situation being provided. The current study will outline the different

situations and how in every situation the event will be treated with respect to the tax guidelines

and the ITAA 1997. This compliance is very necessary because in case it will not be there the it

will be affecting the tax calculation and will be improving the efficiency as well.

1.

As per Section 6-5 of ITAA 1997, the amount of $5000 received by Britney as a scholarship is

an exempt income. It is because the section 6-5 state that the scholarship granted by the

University to meet the cost of education is exempt from Income Tax purpose in Australia.

Hence, in the given question the $5000 received by Britney is an exempt income and thus

excluded from the assessable income of Britney1. The assessable income basically includes

ordinary income plus statutory income.

2.

As per Section 6-5 of ITAA 1997, assessable income includes both ordinary as well as statutory

income and exclude exempt income and non-assessable non-exempt income. Further, as per

section 6(1) of ITAA 1997, ordinary income means the income consisting of earnings, salaries,

wages, commission, fees, bonuses, pensions, superannuation allowances, renting allowances,

retiring gratuity and gratuity received in relation to any service rendered etc. Thus, the gross

salary and superannuation contribution of Britney of $60000 plus 9.5% is considered as ordinary

1 Christians, Allison, and Laurens van Apeldoorn. "Taxing income where value is created." Fla.

Tax Rev. 22 (2018): 1.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

income and assessable income. Thus, the amount of $65700 [$60000 + ($60000 * 9.5%)] is an

assessable income for Britney 2.

Also in this case, Britney is an Australian resident and because of this the assessable income

always includes the ordinary income being derived directly or even indirectly from the other

different sources as well. Also, this fact includes the income in or out of Australia as well and is

not restricted only to Australia.

3.

Along with the salary, Britney’s company has also decided to pay for $1000 for assisting

her in buying work clothes. Also the company is having strict policy relating to the clothes which

have relating to the quality. In addition to this the clothes also includes the very limited colours

and style and Britney spend $1000 for buying the clothes. But because of her good selection she

was able to wear those clothes for attending her personal event as well. thus, this will be included

in the deduction because it is being provided by the company and it will be deducted while

calculating the assessable income3. In accordance to ATO for all the work related expenses the

person can claim the deduction. But this is only with respect to when the employee themselves

buy the clothes or amount being spent on it and the cleaning cost. But in case the employer pays

for this clothing then the individual cannot claim.

But in the present case, Britney is also using the clothing for personal event as well which is not

correct. Hence, in this case this will not be a deduction as she is already using the dress in

personal use as well. also some part of this amount will not be a deduction but other will be. The

10 % of the clothes are worn and this implies that for $1000, $900 will be part of deduction as it

is used in workplace and $100 will not be because it is being used for the personal events of

Britney. Further in accordance to the section 34 C of ITAA 97 it is clear that the employee must

have the registration relating to the design for getting the uniform and also must take the written

notice of decision and even when the uniform is being registered on the name of the person.

2 Bucci, Valeria. "Presumptive taxation methods: A review of the empirical literature." Journal

of Economic Surveys 34, no. 2 (2020): 372-397.

3 Income Tax Assessment Act 1997. 2022. [Online]. Available through:

<https://www.legislation.gov.au/Details/C2021C00112>

assessable income for Britney 2.

Also in this case, Britney is an Australian resident and because of this the assessable income

always includes the ordinary income being derived directly or even indirectly from the other

different sources as well. Also, this fact includes the income in or out of Australia as well and is

not restricted only to Australia.

3.

Along with the salary, Britney’s company has also decided to pay for $1000 for assisting

her in buying work clothes. Also the company is having strict policy relating to the clothes which

have relating to the quality. In addition to this the clothes also includes the very limited colours

and style and Britney spend $1000 for buying the clothes. But because of her good selection she

was able to wear those clothes for attending her personal event as well. thus, this will be included

in the deduction because it is being provided by the company and it will be deducted while

calculating the assessable income3. In accordance to ATO for all the work related expenses the

person can claim the deduction. But this is only with respect to when the employee themselves

buy the clothes or amount being spent on it and the cleaning cost. But in case the employer pays

for this clothing then the individual cannot claim.

But in the present case, Britney is also using the clothing for personal event as well which is not

correct. Hence, in this case this will not be a deduction as she is already using the dress in

personal use as well. also some part of this amount will not be a deduction but other will be. The

10 % of the clothes are worn and this implies that for $1000, $900 will be part of deduction as it

is used in workplace and $100 will not be because it is being used for the personal events of

Britney. Further in accordance to the section 34 C of ITAA 97 it is clear that the employee must

have the registration relating to the design for getting the uniform and also must take the written

notice of decision and even when the uniform is being registered on the name of the person.

2 Bucci, Valeria. "Presumptive taxation methods: A review of the empirical literature." Journal

of Economic Surveys 34, no. 2 (2020): 372-397.

3 Income Tax Assessment Act 1997. 2022. [Online]. Available through:

<https://www.legislation.gov.au/Details/C2021C00112>

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4.

As per section 6-5 of ITAA 1997, the ordinary income is an income which is received by

individual for their employment such as wages, bonuses, rents etc. and also the income from

rendering personal services, income from property and income from carrying on trading

activities. The amount of license fees received by Britney is basically against its personal service

i.e., copyright to use their new band songs discovering. Hence, in the given scenario, the amount

of license fees i.e., $50000 + $2000 ($1000 * 2 months) = $52000 is consider as ordinary income

of Britney as per the section 6-5 of the income tax assessment act 1997. This is an ordinary

income of the Britney thus it is included in the assessable income of the taxpayer name Britney 4.

On the other hand, the expenditure of $10000 in buying copyright on their new bands

song is basically a capital expenditure. It is also falls under the negative limb. Hence, the

deduction on total amount of $10000 is not deductible as per section 8-1 of ITAA 1997. While

on the other hand, Britney can deduct under section 40-25 of income tax assessment act 1997,

the decline in the value of capital assets. Basically, copyright is an intangible asset which are

consider as capital assets but are not allowable for declining value deduction. Hence, the

expenditure on copyright is a non-deductible tax and Britney are not liable to claim deduction on

the same.

5.

Further in the present situation Britney is providing extra help to Tame Antelope in order

to line up the music performances. For this Britney is being provided with a $1000 for arranging

the performances for the band. In order to thank Britney, the lead singer of Tame Antelope sent a

cheque of $1000 and with that there was enclosed gold necklace worth $5000. This will be

treated as the deduction because in accordance to the CGT that is capital gain tax certain gifts are

being exempted from tax5. Hence, this will not be part of assessable income and will be treated

4 Hoynes, Hilary. "The earned income tax credit." The Annals of the American Academy of

Political and Social Science 686, no. 1 (2019): 180-203.

5 Boccabella, Dale, and Michael Blissenden. "No full FITO on US gains as CGT discount"

excludes" part of gain: taxpayer in Burton has a case. Part 1." Weekly Tax Bulletin (2019):

12-17.

As per section 6-5 of ITAA 1997, the ordinary income is an income which is received by

individual for their employment such as wages, bonuses, rents etc. and also the income from

rendering personal services, income from property and income from carrying on trading

activities. The amount of license fees received by Britney is basically against its personal service

i.e., copyright to use their new band songs discovering. Hence, in the given scenario, the amount

of license fees i.e., $50000 + $2000 ($1000 * 2 months) = $52000 is consider as ordinary income

of Britney as per the section 6-5 of the income tax assessment act 1997. This is an ordinary

income of the Britney thus it is included in the assessable income of the taxpayer name Britney 4.

On the other hand, the expenditure of $10000 in buying copyright on their new bands

song is basically a capital expenditure. It is also falls under the negative limb. Hence, the

deduction on total amount of $10000 is not deductible as per section 8-1 of ITAA 1997. While

on the other hand, Britney can deduct under section 40-25 of income tax assessment act 1997,

the decline in the value of capital assets. Basically, copyright is an intangible asset which are

consider as capital assets but are not allowable for declining value deduction. Hence, the

expenditure on copyright is a non-deductible tax and Britney are not liable to claim deduction on

the same.

5.

Further in the present situation Britney is providing extra help to Tame Antelope in order

to line up the music performances. For this Britney is being provided with a $1000 for arranging

the performances for the band. In order to thank Britney, the lead singer of Tame Antelope sent a

cheque of $1000 and with that there was enclosed gold necklace worth $5000. This will be

treated as the deduction because in accordance to the CGT that is capital gain tax certain gifts are

being exempted from tax5. Hence, this will not be part of assessable income and will be treated

4 Hoynes, Hilary. "The earned income tax credit." The Annals of the American Academy of

Political and Social Science 686, no. 1 (2019): 180-203.

5 Boccabella, Dale, and Michael Blissenden. "No full FITO on US gains as CGT discount"

excludes" part of gain: taxpayer in Burton has a case. Part 1." Weekly Tax Bulletin (2019):

12-17.

as the deduction. Also, the amount of $1000 will be treated as the part of statutory income

because this has not been earned from the ordinary course of activity. This is necessary for the

fact that when the income is generated from the sources other than ordinary employment is being

treated as the deduction and it will not be included in assessable income.

Also, this will be affecting the calculation of the assessable income in case the deduction

will be treated in wrong manner and this will be affecting the total income being taxable. In

accordance to the section 6- 10 of ITAA 1997 the amount which is not included in the ordinary

income is being included within the statutory income6. Also, in case the person is an Australian

resident then assessable income will be including all the statutory income from other sources as

well.

6.

As per section 8-1 (1) of Income Tax Assessment Act 1997, the tax payer can deduct any loss or

expenses they incur in order to either gain or produce assessable income and incurred in carrying

on the business for the purpose of gaining or producing assessable income. Basically, the income

they received from Sony Music against their copyright for the songs are assessable income and

they are considering as part of ordinary income 7. Thus, in the given question the amount of

$10000 as a legal fees paid by Britney for defending the copyright infringement action to the

lawyer is consider as tax deductible. It is basically a tax deductible under category general

deduction as per section 8-1 (1) of the ITAA 1997.

Also with respect to the section 8- 2 the person can also deduct the specific deduction in order to

reach to the correct assessable income. This is pertaining to the fact that some of the provision of

this act involves preventing the person from deducting an amount which can be deducted

otherwise as well8. Thus any amount which is being deducted under the provision of the act that

6 Australia Individual - Income determination. 2022. [Online]. Available through:

<https://taxsummaries.pwc.com/australia/individual/income-determination>

7 Arnold, Brian J., Hugh J. Ault, and Graeme Cooper, eds. Comparative income taxation: a

structural analysis. Kluwer Law International BV, 2019.

8 Brydges, Neil, and Kelvin Yuen. "A matter of trusts: Trusts, income tax, CGT and foreign

residents." Taxation in Australia 53, no. 2 (2018): 80-82.

because this has not been earned from the ordinary course of activity. This is necessary for the

fact that when the income is generated from the sources other than ordinary employment is being

treated as the deduction and it will not be included in assessable income.

Also, this will be affecting the calculation of the assessable income in case the deduction

will be treated in wrong manner and this will be affecting the total income being taxable. In

accordance to the section 6- 10 of ITAA 1997 the amount which is not included in the ordinary

income is being included within the statutory income6. Also, in case the person is an Australian

resident then assessable income will be including all the statutory income from other sources as

well.

6.

As per section 8-1 (1) of Income Tax Assessment Act 1997, the tax payer can deduct any loss or

expenses they incur in order to either gain or produce assessable income and incurred in carrying

on the business for the purpose of gaining or producing assessable income. Basically, the income

they received from Sony Music against their copyright for the songs are assessable income and

they are considering as part of ordinary income 7. Thus, in the given question the amount of

$10000 as a legal fees paid by Britney for defending the copyright infringement action to the

lawyer is consider as tax deductible. It is basically a tax deductible under category general

deduction as per section 8-1 (1) of the ITAA 1997.

Also with respect to the section 8- 2 the person can also deduct the specific deduction in order to

reach to the correct assessable income. This is pertaining to the fact that some of the provision of

this act involves preventing the person from deducting an amount which can be deducted

otherwise as well8. Thus any amount which is being deducted under the provision of the act that

6 Australia Individual - Income determination. 2022. [Online]. Available through:

<https://taxsummaries.pwc.com/australia/individual/income-determination>

7 Arnold, Brian J., Hugh J. Ault, and Graeme Cooper, eds. Comparative income taxation: a

structural analysis. Kluwer Law International BV, 2019.

8 Brydges, Neil, and Kelvin Yuen. "A matter of trusts: Trusts, income tax, CGT and foreign

residents." Taxation in Australia 53, no. 2 (2018): 80-82.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

outside the division is being called as the specific deduction. Hence, the current case of copyright

against the songs is being part of infringement and is deductible.

7.

As per section 6 sub section 1 of the ITAA 1936, the rental income received from the

property is consider as ordinary income of the individual. Hence, the amount of $1000 which

Britney has received from its main residence via renting out it on Airbnb is consider as an

ordinary income and recorded as an assessable income. Further, Britney pays $200 commission

to Airbnb which is basically incur by the Britney in producing $1000 by renting out their

apartment through Airbnb. Thus, the amount of $200 commission is deductible under section 8-1

of ITAA 1997. It means Britney are allowable to take deduction of $200 because the amount is

apportioned properly so that Britney claim deduction only for the part of gaining income not

personal use. Generally, they do not fall under any specific deduction provision 9.

Thus, in accordance to the section 8- 1 of the ITAA 1997 the commission of the $200 is being

deducted as per this section, the person can deduct from the assessable income any loss or the

expenses being incurred in order to earn an income. Thus in this present case Britney has

incurred expense of $200 in order to earn $1000 from rent. Hence, because of this reason it will

be treated as the deduction from the assessable income.

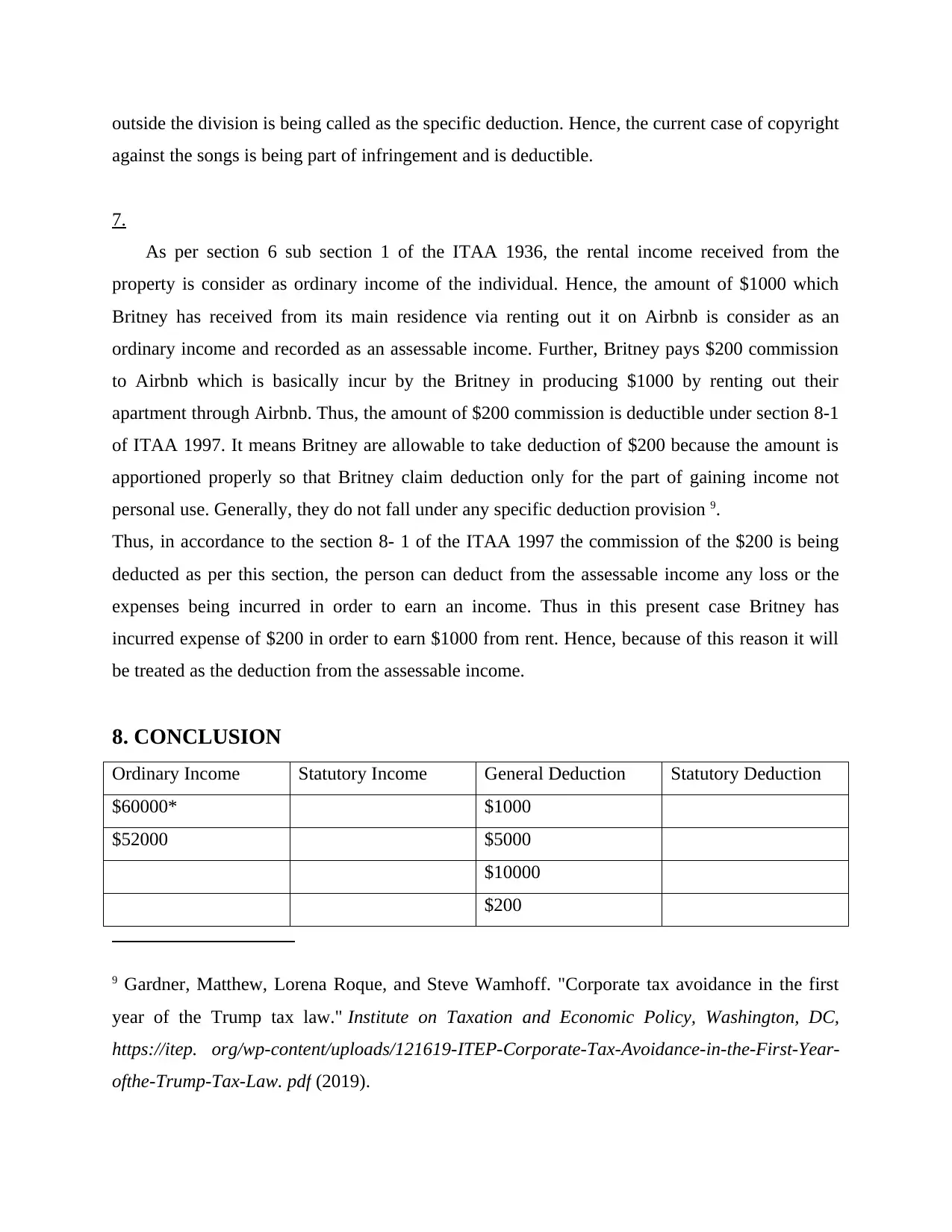

8. CONCLUSION

Ordinary Income Statutory Income General Deduction Statutory Deduction

$60000* $1000

$52000 $5000

$10000

$200

9 Gardner, Matthew, Lorena Roque, and Steve Wamhoff. "Corporate tax avoidance in the first

year of the Trump tax law." Institute on Taxation and Economic Policy, Washington, DC,

https://itep. org/wp-content/uploads/121619-ITEP-Corporate-Tax-Avoidance-in-the-First-Year-

ofthe-Trump-Tax-Law. pdf (2019).

against the songs is being part of infringement and is deductible.

7.

As per section 6 sub section 1 of the ITAA 1936, the rental income received from the

property is consider as ordinary income of the individual. Hence, the amount of $1000 which

Britney has received from its main residence via renting out it on Airbnb is consider as an

ordinary income and recorded as an assessable income. Further, Britney pays $200 commission

to Airbnb which is basically incur by the Britney in producing $1000 by renting out their

apartment through Airbnb. Thus, the amount of $200 commission is deductible under section 8-1

of ITAA 1997. It means Britney are allowable to take deduction of $200 because the amount is

apportioned properly so that Britney claim deduction only for the part of gaining income not

personal use. Generally, they do not fall under any specific deduction provision 9.

Thus, in accordance to the section 8- 1 of the ITAA 1997 the commission of the $200 is being

deducted as per this section, the person can deduct from the assessable income any loss or the

expenses being incurred in order to earn an income. Thus in this present case Britney has

incurred expense of $200 in order to earn $1000 from rent. Hence, because of this reason it will

be treated as the deduction from the assessable income.

8. CONCLUSION

Ordinary Income Statutory Income General Deduction Statutory Deduction

$60000* $1000

$52000 $5000

$10000

$200

9 Gardner, Matthew, Lorena Roque, and Steve Wamhoff. "Corporate tax avoidance in the first

year of the Trump tax law." Institute on Taxation and Economic Policy, Washington, DC,

https://itep. org/wp-content/uploads/121619-ITEP-Corporate-Tax-Avoidance-in-the-First-Year-

ofthe-Trump-Tax-Law. pdf (2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

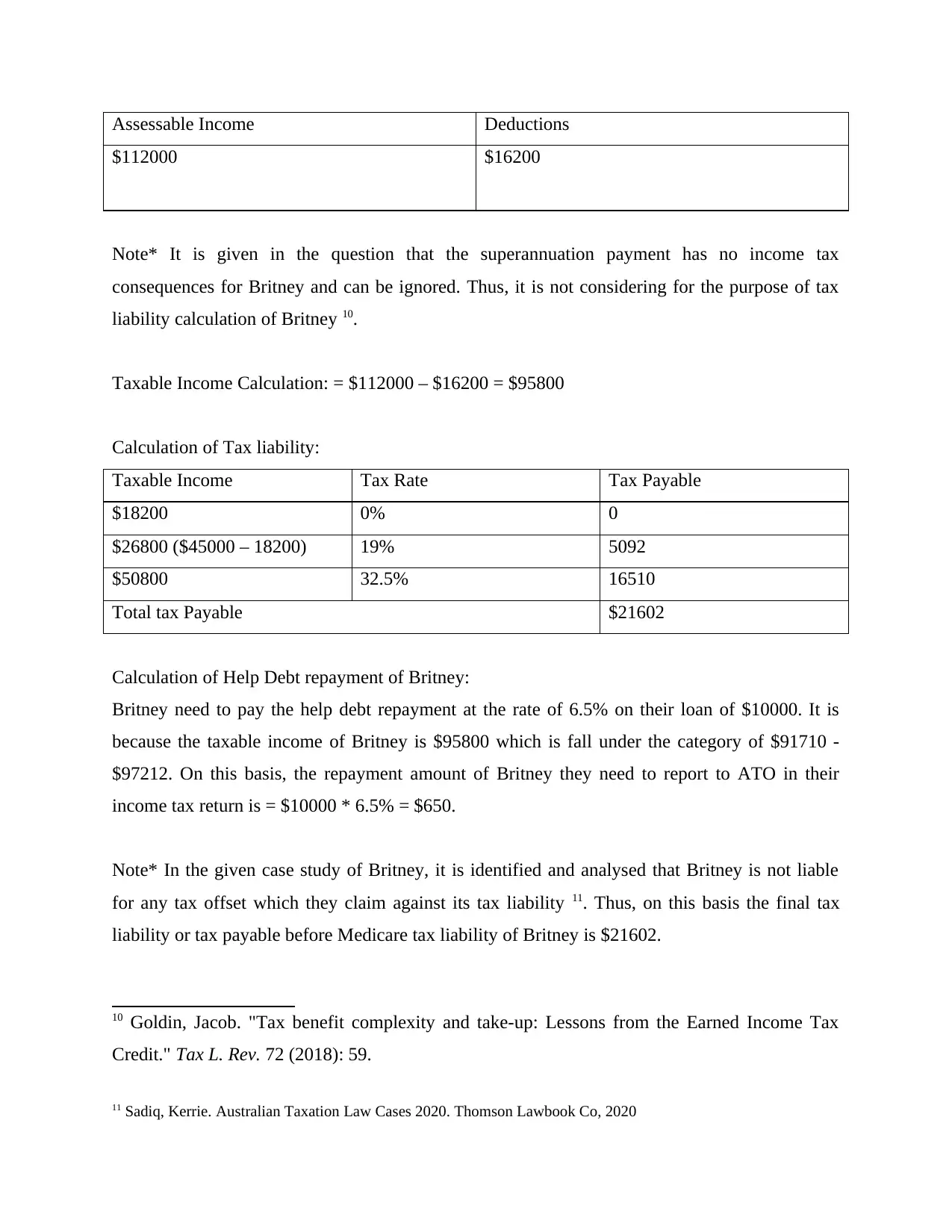

Assessable Income Deductions

$112000 $16200

Note* It is given in the question that the superannuation payment has no income tax

consequences for Britney and can be ignored. Thus, it is not considering for the purpose of tax

liability calculation of Britney 10.

Taxable Income Calculation: = $112000 – $16200 = $95800

Calculation of Tax liability:

Taxable Income Tax Rate Tax Payable

$18200 0% 0

$26800 ($45000 – 18200) 19% 5092

$50800 32.5% 16510

Total tax Payable $21602

Calculation of Help Debt repayment of Britney:

Britney need to pay the help debt repayment at the rate of 6.5% on their loan of $10000. It is

because the taxable income of Britney is $95800 which is fall under the category of $91710 -

$97212. On this basis, the repayment amount of Britney they need to report to ATO in their

income tax return is = $10000 * 6.5% = $650.

Note* In the given case study of Britney, it is identified and analysed that Britney is not liable

for any tax offset which they claim against its tax liability 11. Thus, on this basis the final tax

liability or tax payable before Medicare tax liability of Britney is $21602.

10 Goldin, Jacob. "Tax benefit complexity and take-up: Lessons from the Earned Income Tax

Credit." Tax L. Rev. 72 (2018): 59.

11 Sadiq, Kerrie. Australian Taxation Law Cases 2020. Thomson Lawbook Co, 2020

$112000 $16200

Note* It is given in the question that the superannuation payment has no income tax

consequences for Britney and can be ignored. Thus, it is not considering for the purpose of tax

liability calculation of Britney 10.

Taxable Income Calculation: = $112000 – $16200 = $95800

Calculation of Tax liability:

Taxable Income Tax Rate Tax Payable

$18200 0% 0

$26800 ($45000 – 18200) 19% 5092

$50800 32.5% 16510

Total tax Payable $21602

Calculation of Help Debt repayment of Britney:

Britney need to pay the help debt repayment at the rate of 6.5% on their loan of $10000. It is

because the taxable income of Britney is $95800 which is fall under the category of $91710 -

$97212. On this basis, the repayment amount of Britney they need to report to ATO in their

income tax return is = $10000 * 6.5% = $650.

Note* In the given case study of Britney, it is identified and analysed that Britney is not liable

for any tax offset which they claim against its tax liability 11. Thus, on this basis the final tax

liability or tax payable before Medicare tax liability of Britney is $21602.

10 Goldin, Jacob. "Tax benefit complexity and take-up: Lessons from the Earned Income Tax

Credit." Tax L. Rev. 72 (2018): 59.

11 Sadiq, Kerrie. Australian Taxation Law Cases 2020. Thomson Lawbook Co, 2020

On the other hand, other levies also added to Britney income tax bill. For example, Britney in the

given case is liable to pay Medicare levy at the rate 2% and also need to pay Medicare levy

surcharge at the rate of 1%. It is because Britney is fall under the MLS income Threshold of Tier

1 $90001 to $105000. Also, as the Britney is obliged to pay Medicare levy surcharge of because

Britney does not hold private health insurance 12.

Calculation of Britney Medicare Levy:

= $95800 * 2% = $1916

Calculation of Britney Medicare levy surcharge:

= $95800 * 1% = $958

Calculation of Total or overall tax liability that need to be paid by Britney to ATO for the year

ended 30th June 2022 are as follows:

= Total Tax payable + Medicare levy + Medicare levy surcharge

= $21602 + $1916 + $958 = $24476

12 Medicare Levy Act 1986 (Cth) ss5, 6(1).

given case is liable to pay Medicare levy at the rate 2% and also need to pay Medicare levy

surcharge at the rate of 1%. It is because Britney is fall under the MLS income Threshold of Tier

1 $90001 to $105000. Also, as the Britney is obliged to pay Medicare levy surcharge of because

Britney does not hold private health insurance 12.

Calculation of Britney Medicare Levy:

= $95800 * 2% = $1916

Calculation of Britney Medicare levy surcharge:

= $95800 * 1% = $958

Calculation of Total or overall tax liability that need to be paid by Britney to ATO for the year

ended 30th June 2022 are as follows:

= Total Tax payable + Medicare levy + Medicare levy surcharge

= $21602 + $1916 + $958 = $24476

12 Medicare Levy Act 1986 (Cth) ss5, 6(1).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and journals

1

Books and journals

1

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.