Taxation 16 (Finance): Income, National Insurance, Capital Gains, IHT

VerifiedAdded on 2022/08/29

|16

|2179

|37

Homework Assignment

AI Summary

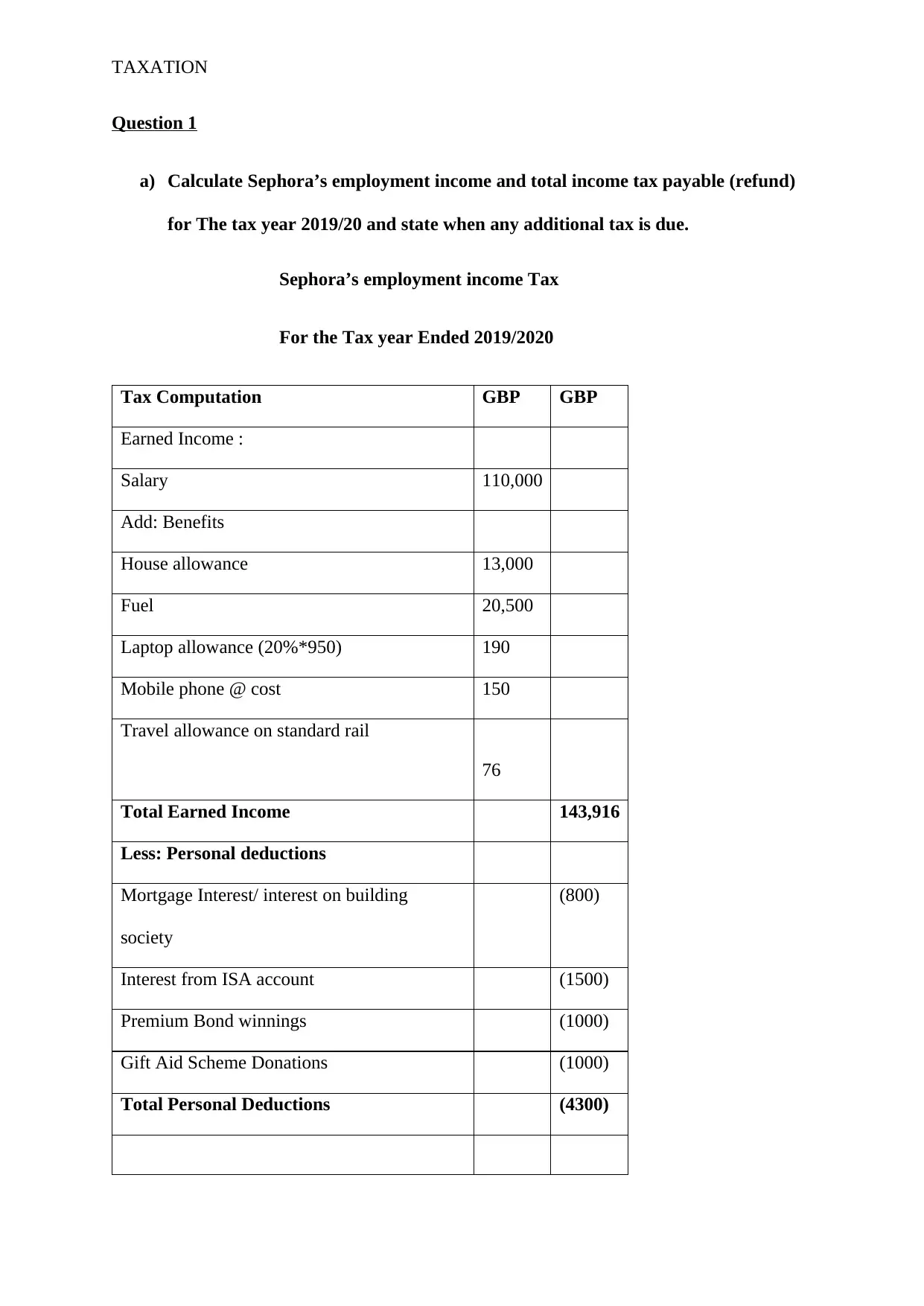

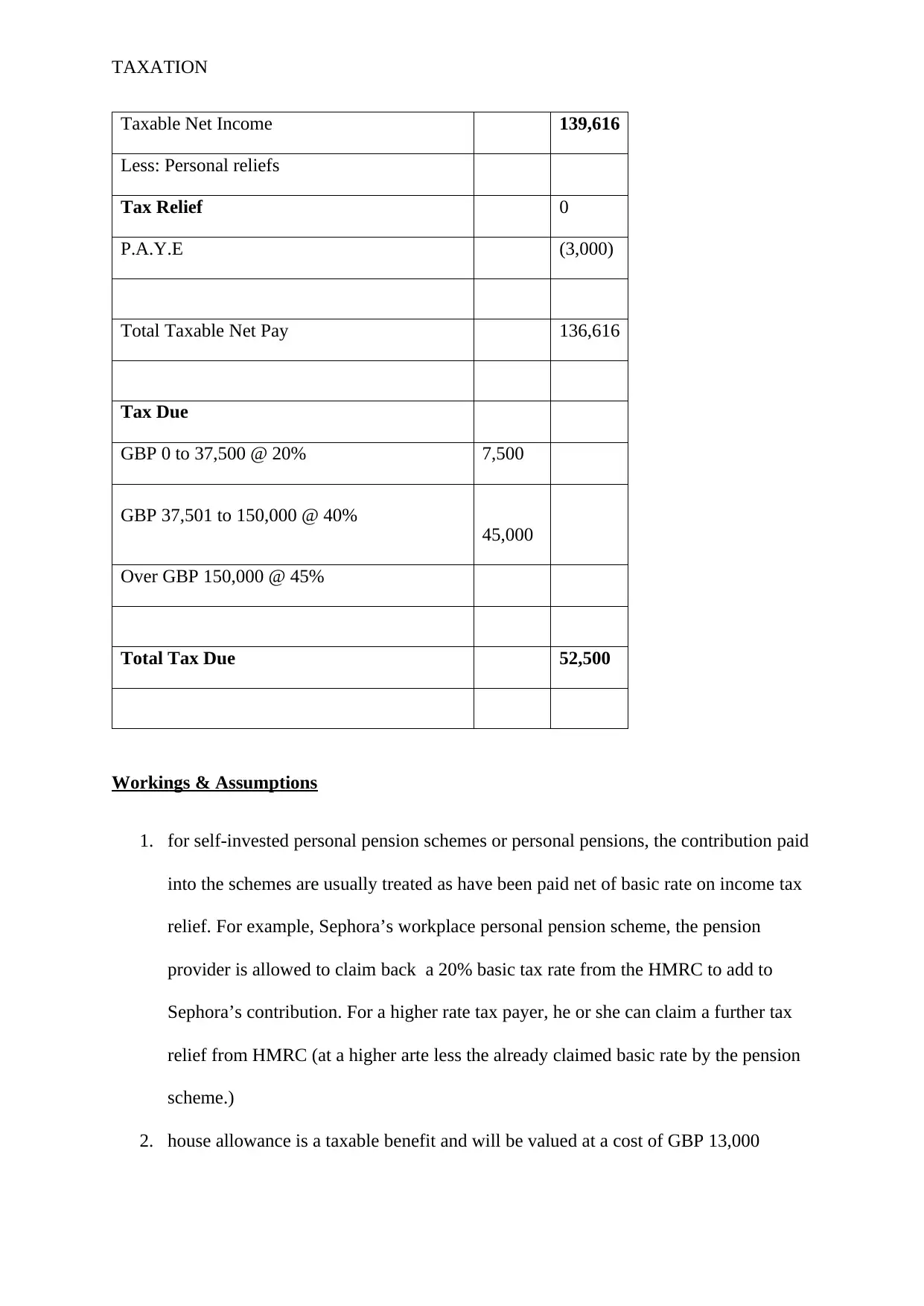

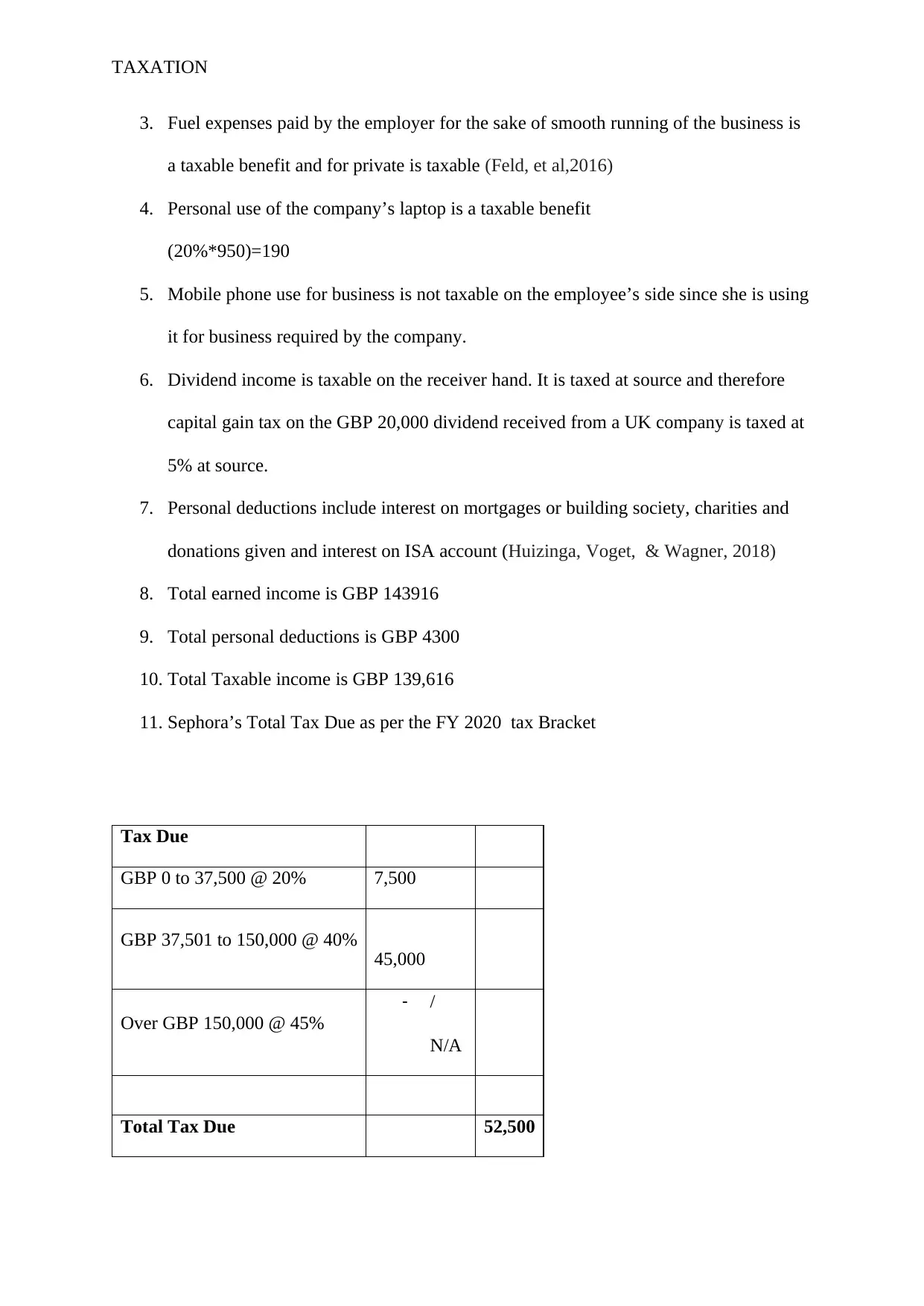

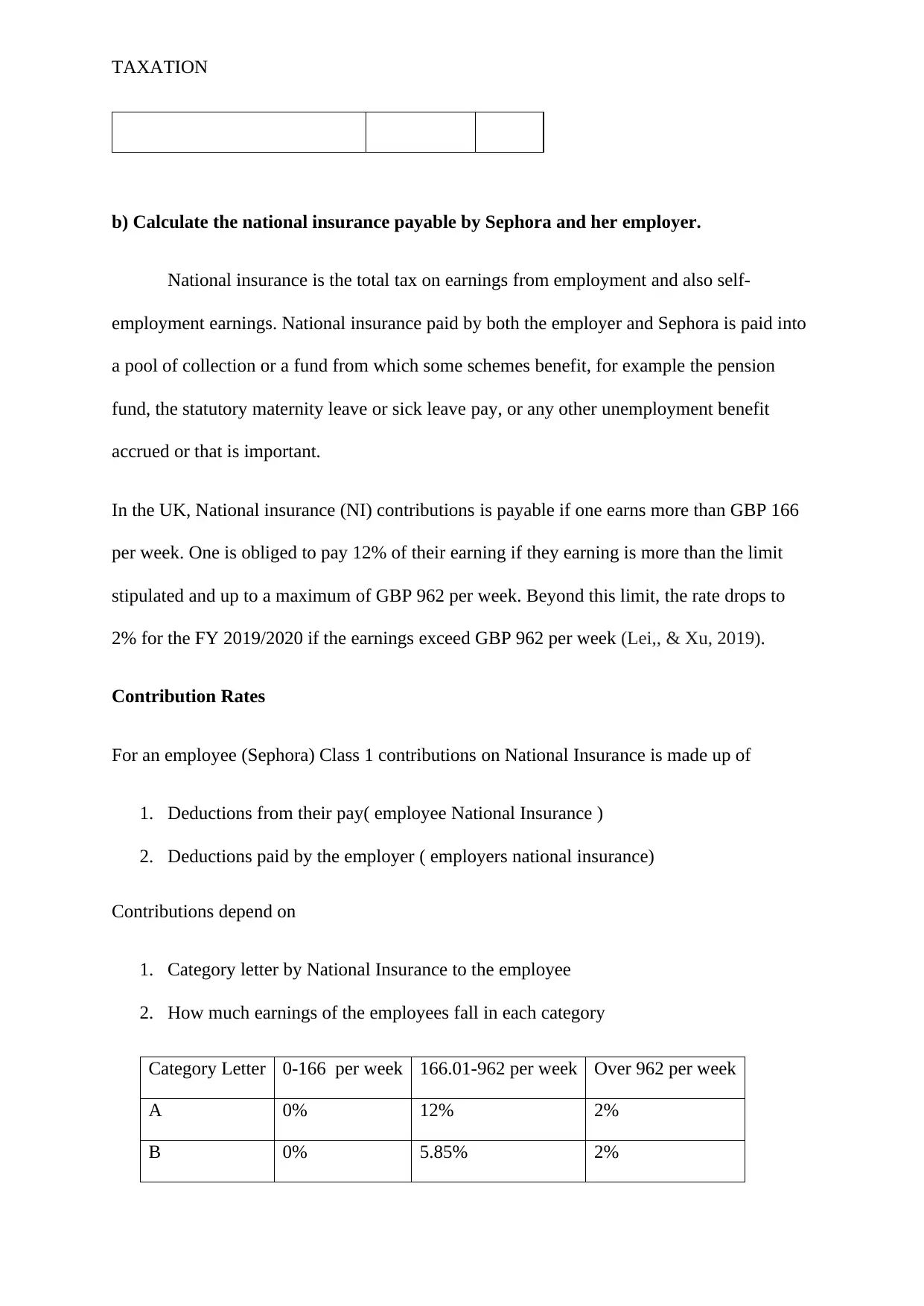

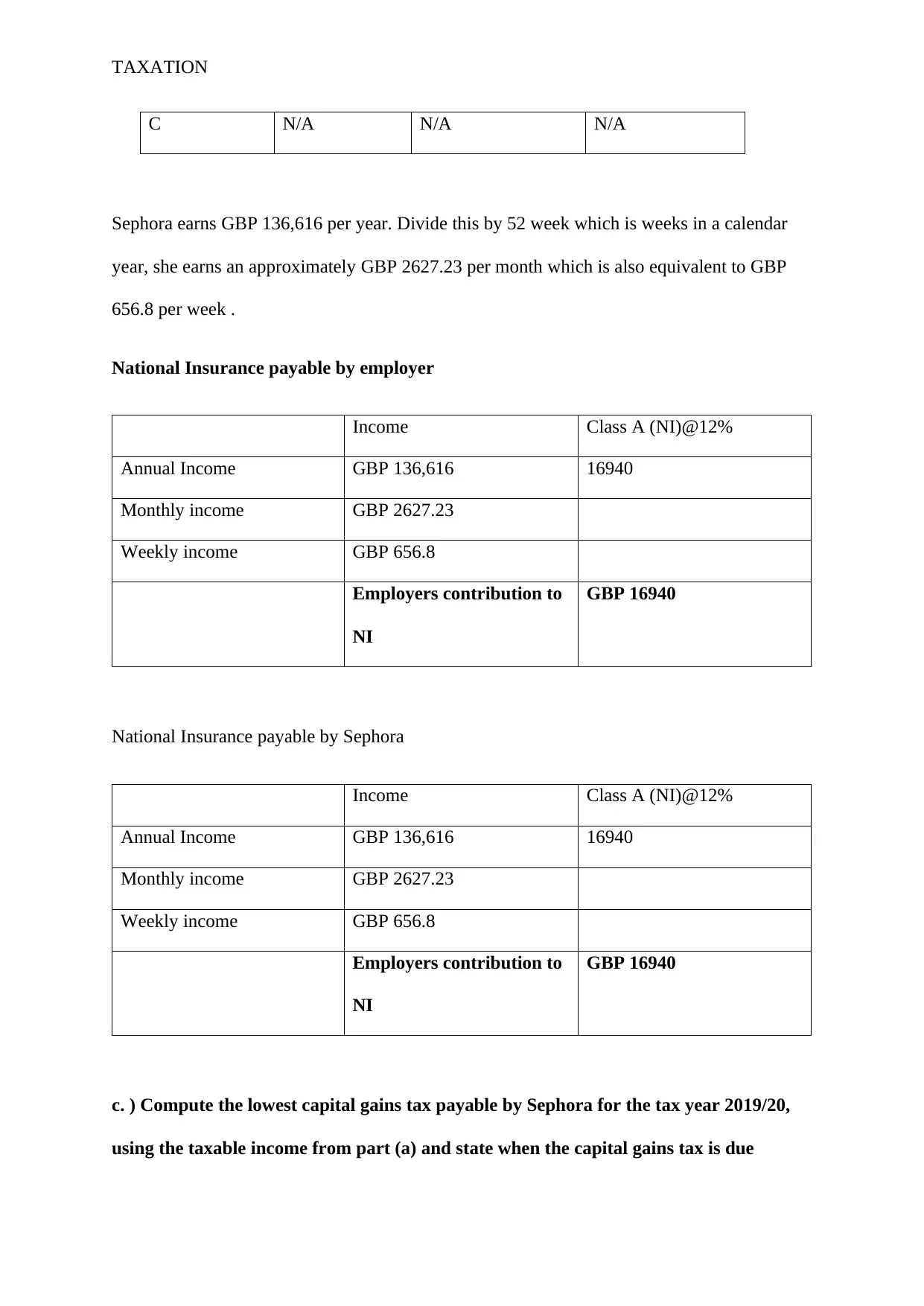

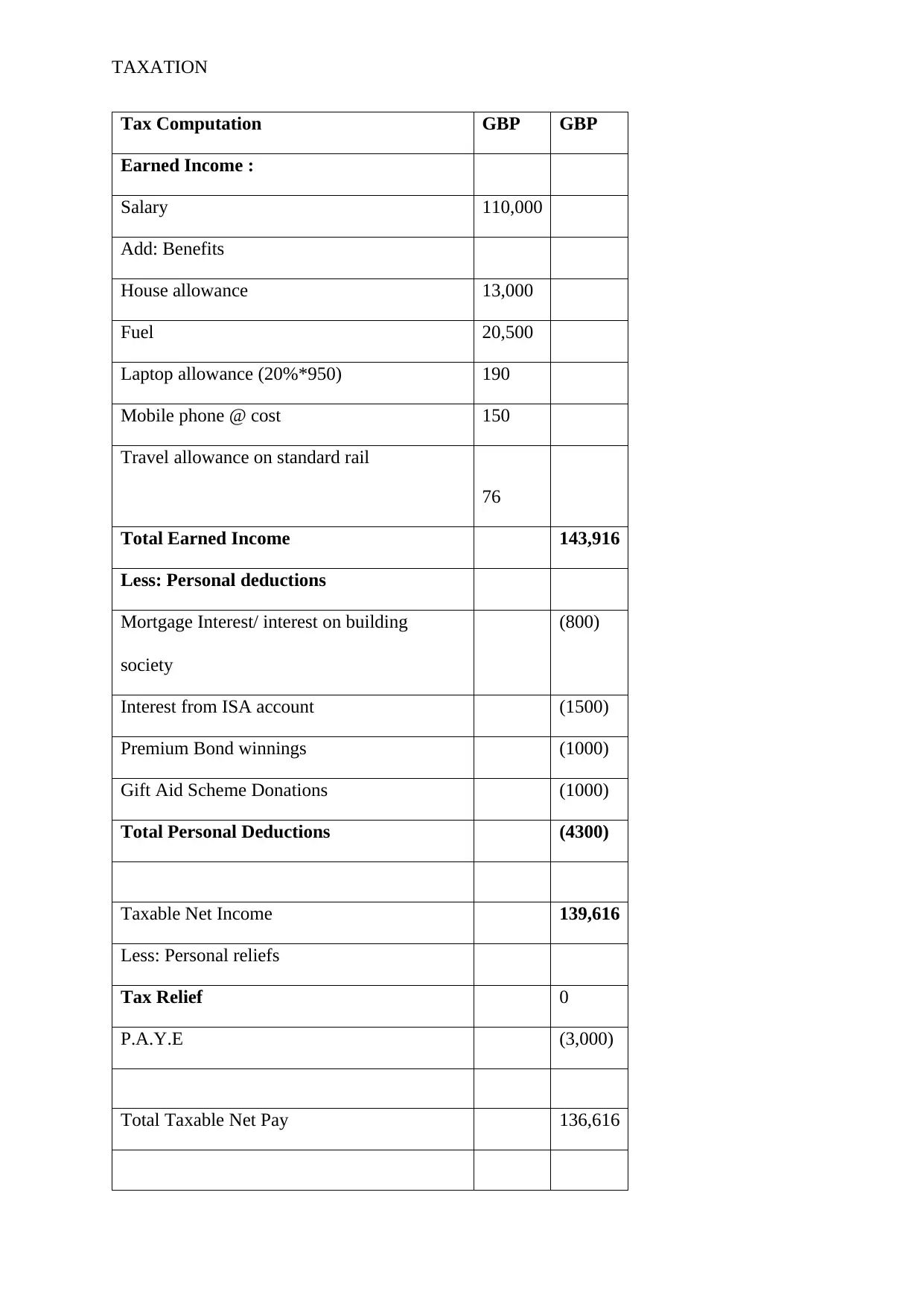

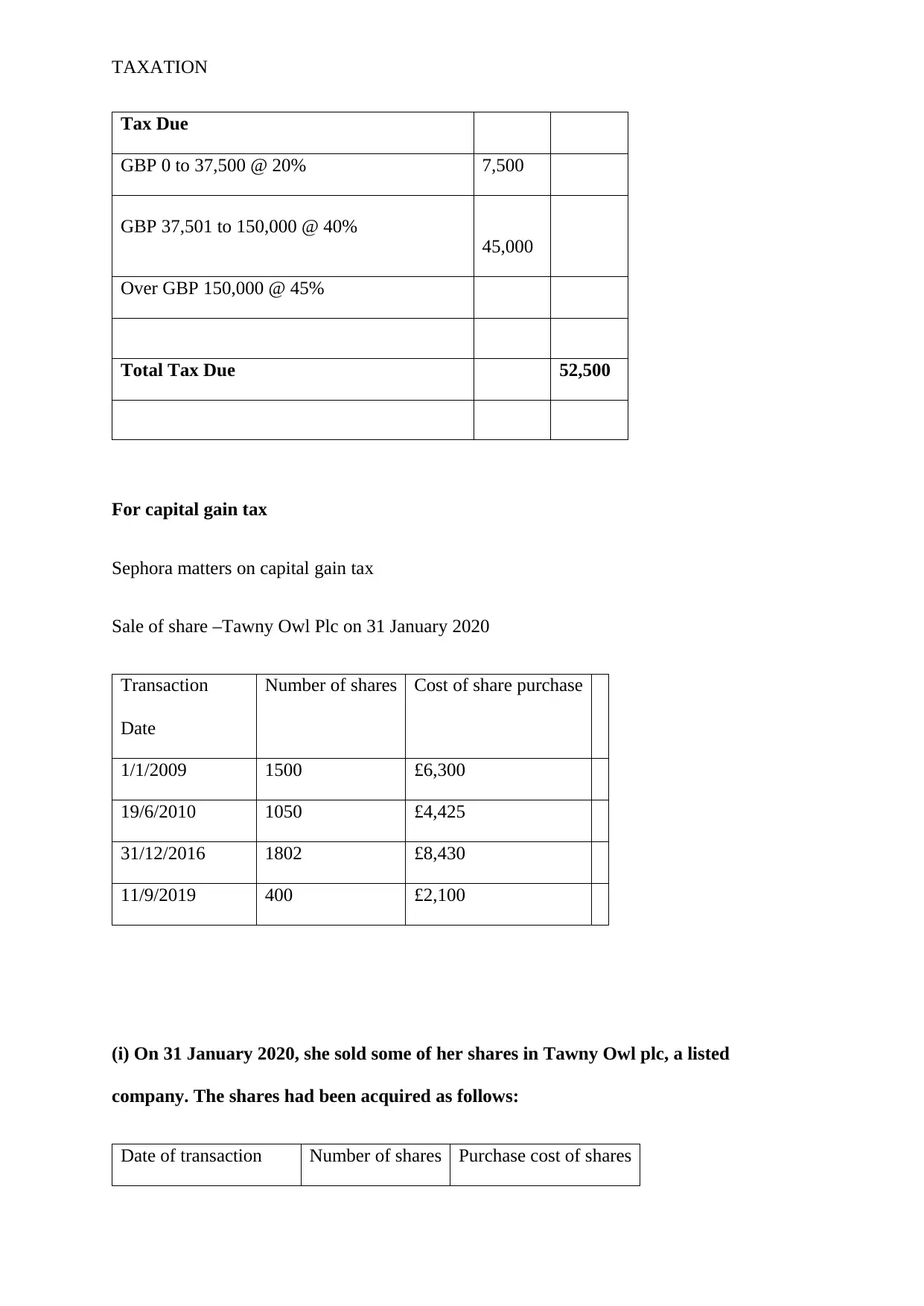

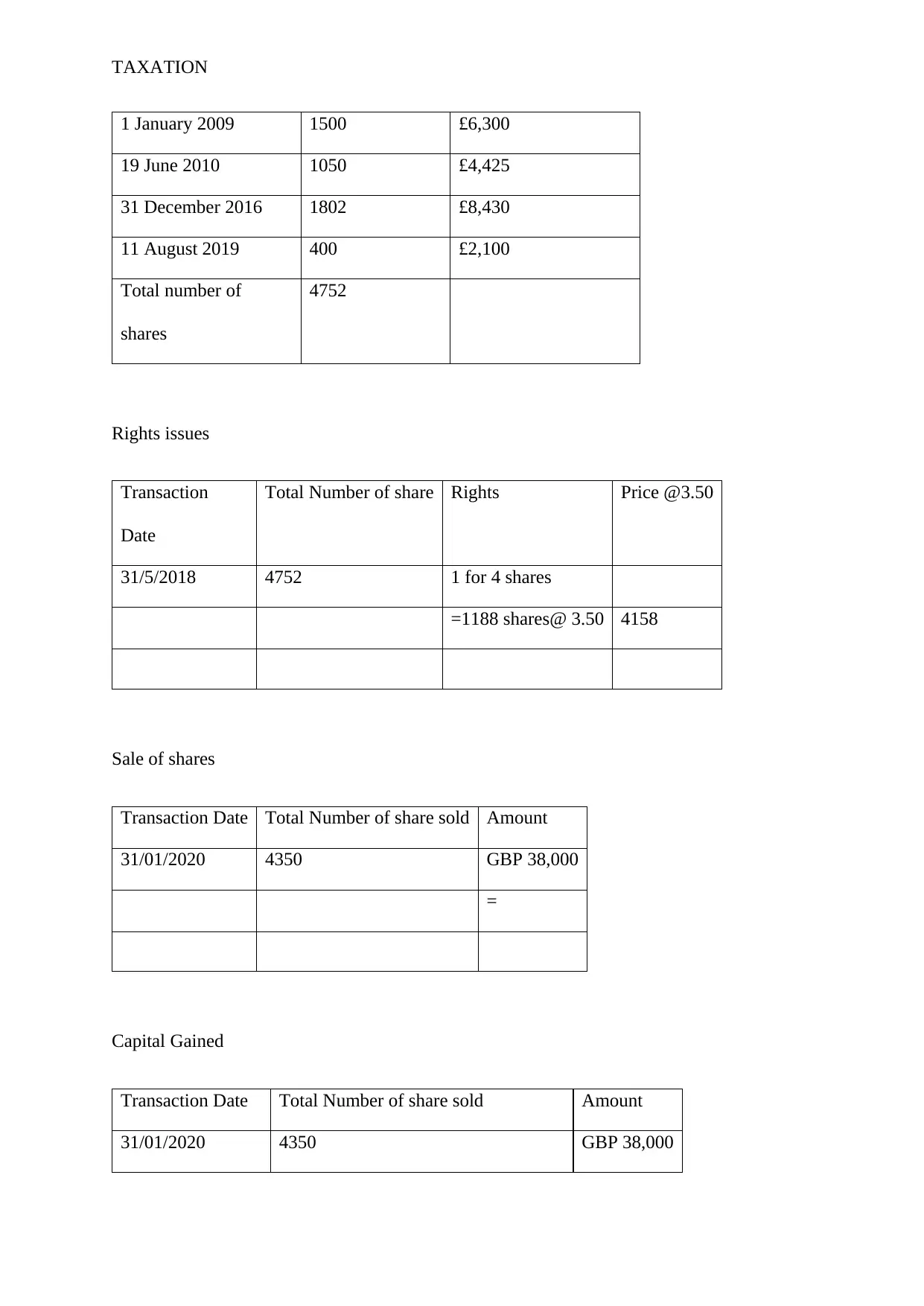

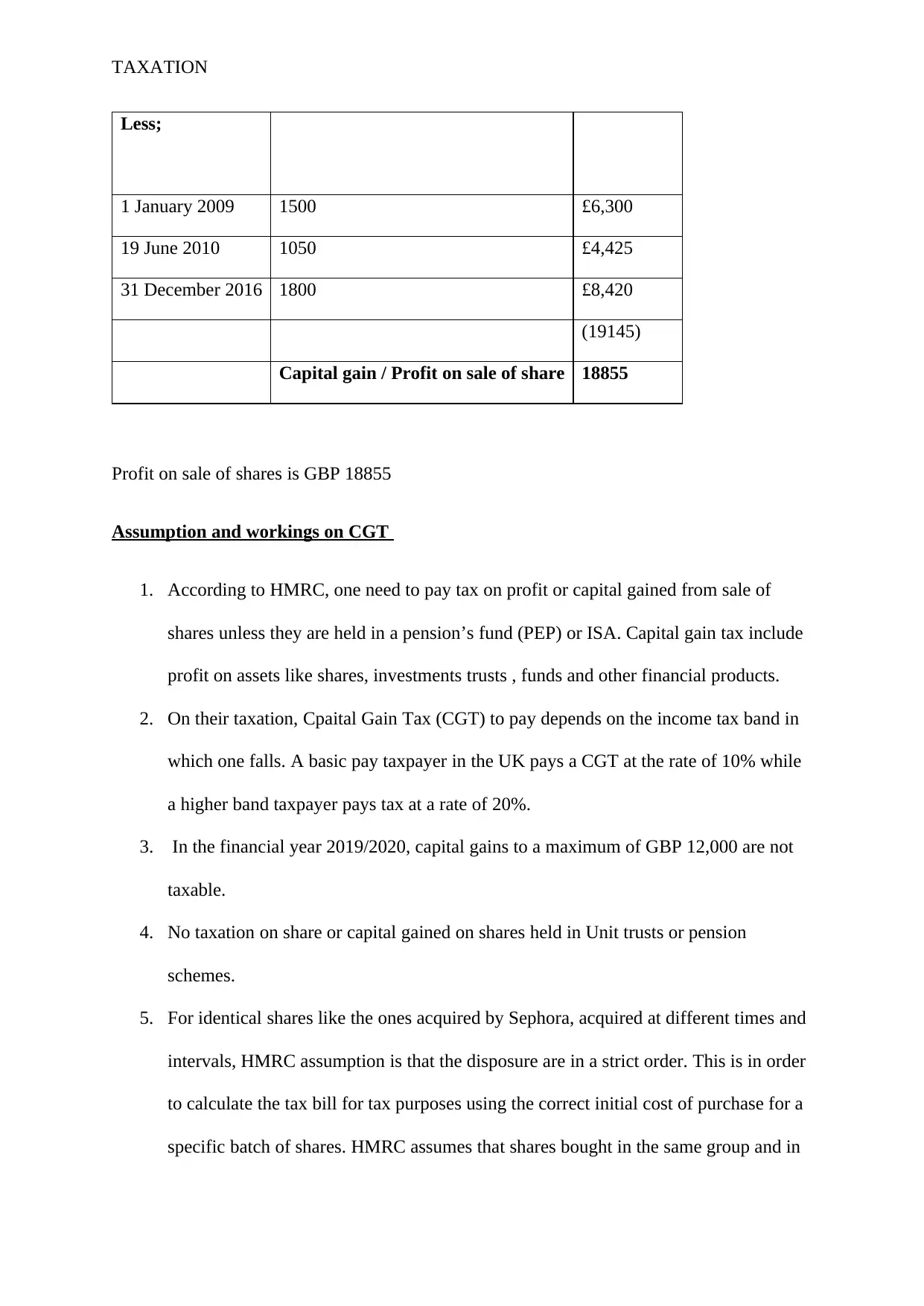

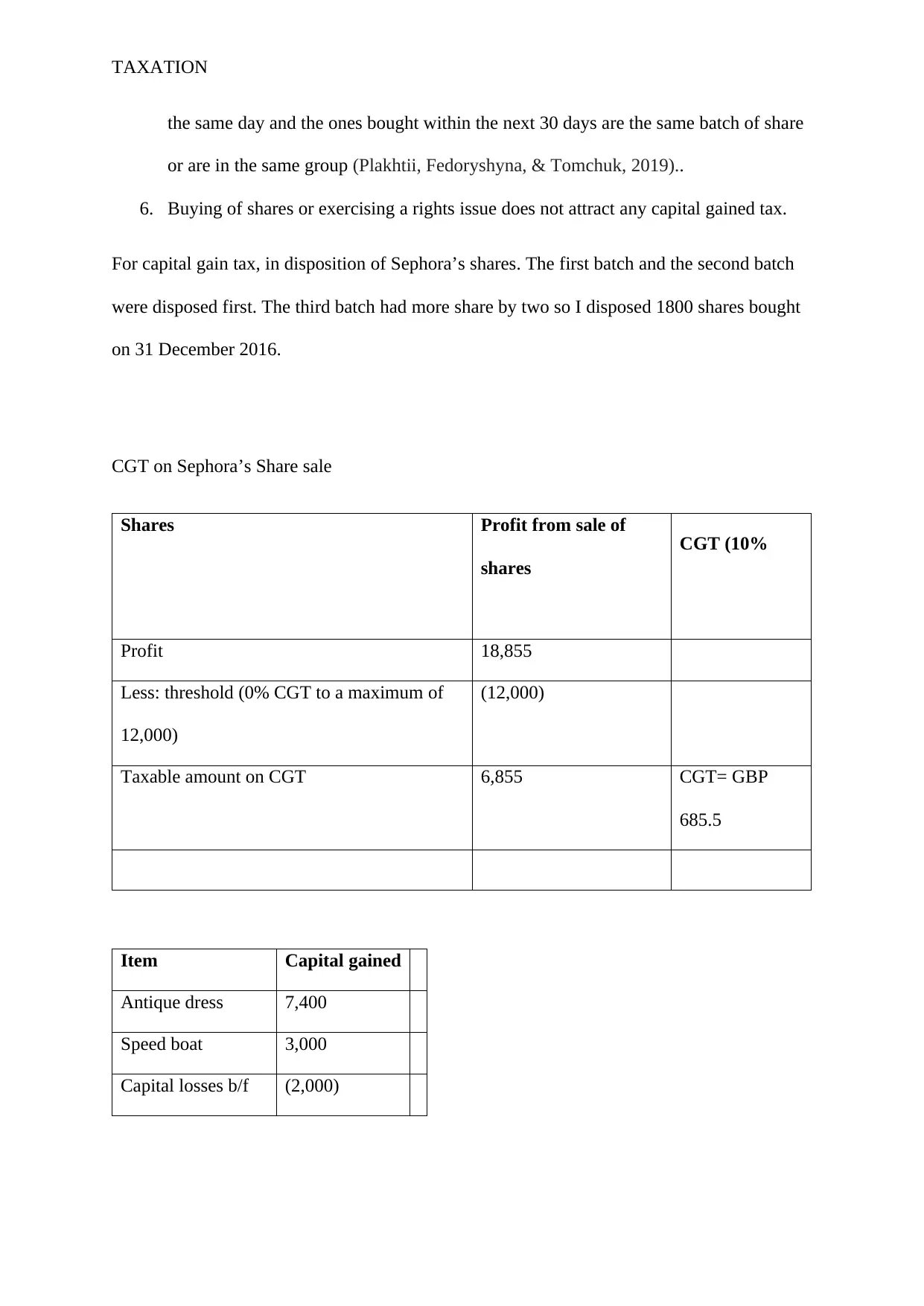

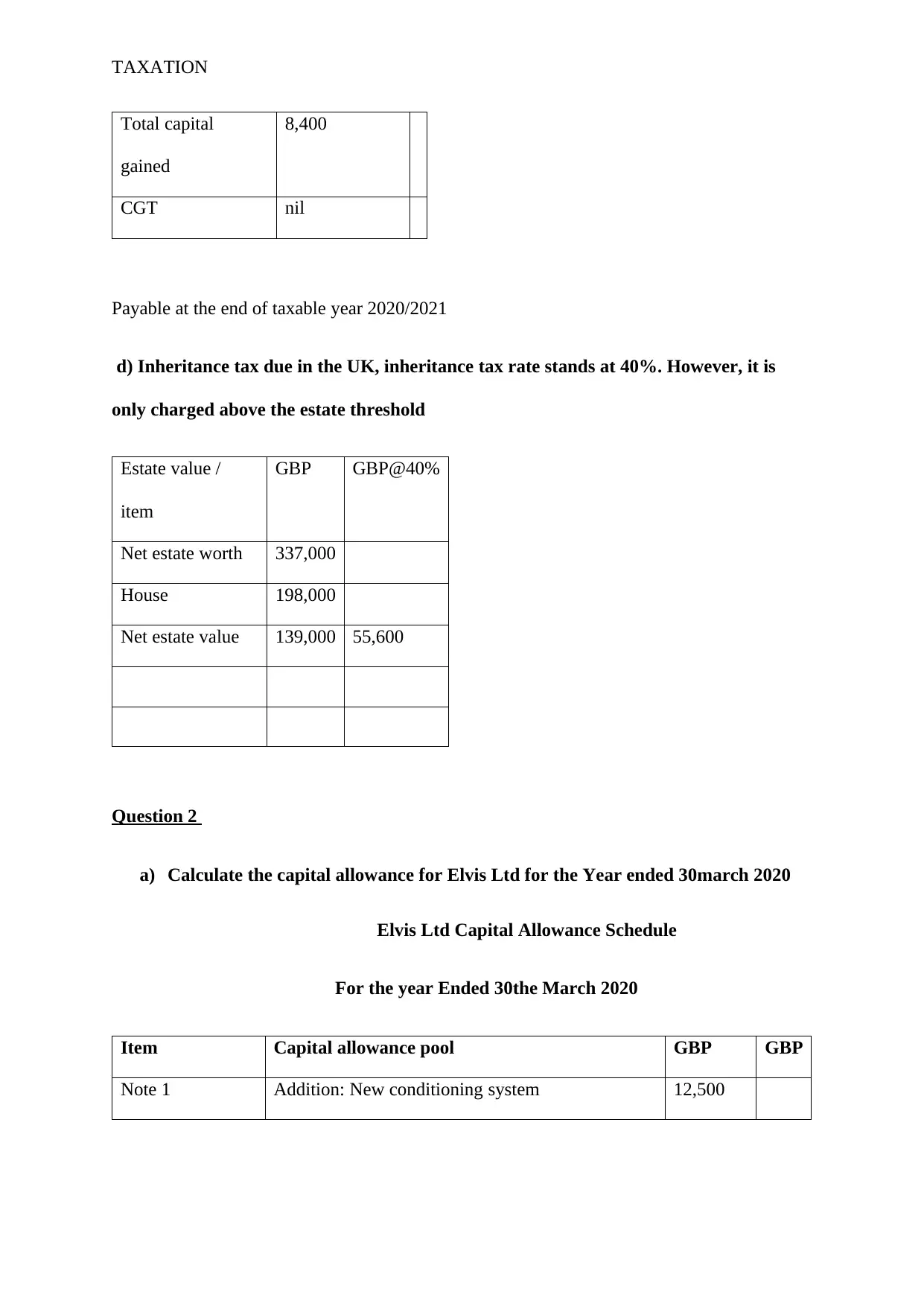

This assignment analyzes the tax liabilities of Sephora, a finance director, and Elvis Ltd for the tax year 2019/20. It calculates Sephora's employment income, total income tax payable (including benefits like house allowance, fuel, and laptop allowance), national insurance contributions (employee and employer), and capital gains tax from share sales. The analysis includes detailed workings, assumptions, and references to relevant tax regulations. Furthermore, the assignment calculates the inheritance tax due based on the estate value. For Elvis Ltd, the assignment calculates capital allowances, net adjusted trading profit, and corporation tax liability, including depreciation, expenses, and tax computations. The assignment also covers the computation of the corporation tax and the assumptions made for tax purposes. Finally, it provides the calculation of the tax liability of the company.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.