Analysis of Taxation, Capital Gains, and Income Report

VerifiedAdded on 2020/10/04

|9

|2526

|36

Report

AI Summary

This report provides a comprehensive analysis of taxation, covering capital gains, personal exertion income, and their implications. It begins with an introduction to taxation and its importance, followed by an examination of capital gains tax, including tax rates and examples. The report analyzes how capital gains taxes apply to various assets like paintings, sculptures, and jewelry. It then delves into income from personal exertion, defining it and providing examples such as income from book publications, manuscripts, and interviews. The report concludes with a case study involving a loan between a father and son and how it impacts their taxable income, including a discussion of dividends. The report references various tax regulations and case laws to support its analysis.

Taxation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Question 1....................................................................................................................................1

Question 2....................................................................................................................................3

Question 3....................................................................................................................................5

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Question 1....................................................................................................................................1

Question 2....................................................................................................................................3

Question 3....................................................................................................................................5

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Taxation is an amount which is required to be paid by individuals as well as corporation

on the incomes which is received by them from different sources. Governmental bodies

implement regulations related to tax and for all the tax payers it is very important to comply with

them. There are different types of taxes such as direct and indirect which are needed to be paid

by organisations and people. All the countries have their own taxation rules which is required to

be followed by individuals and organisations operating business in that nation.

MAIN BODY

Question 1

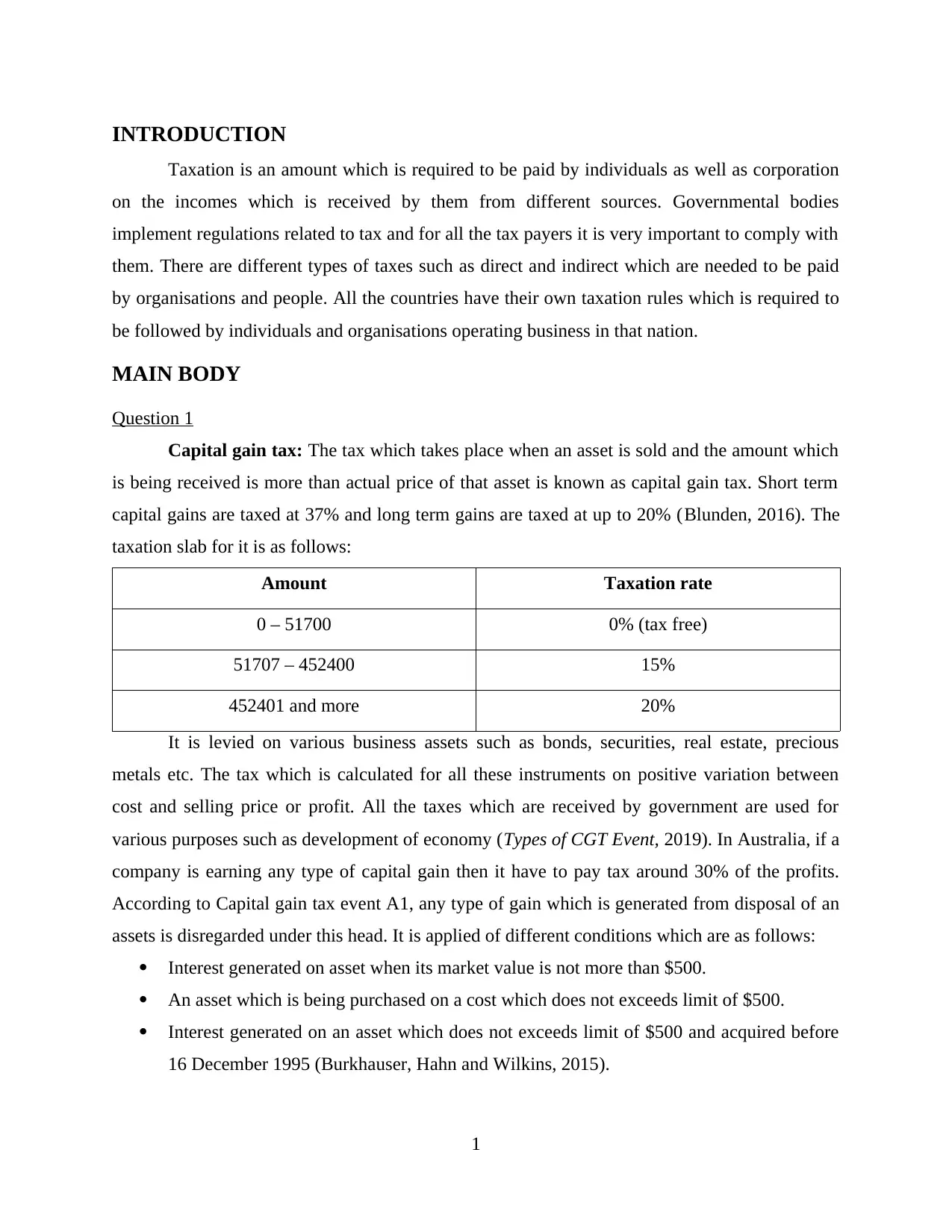

Capital gain tax: The tax which takes place when an asset is sold and the amount which

is being received is more than actual price of that asset is known as capital gain tax. Short term

capital gains are taxed at 37% and long term gains are taxed at up to 20% (Blunden, 2016). The

taxation slab for it is as follows:

Amount Taxation rate

0 – 51700 0% (tax free)

51707 – 452400 15%

452401 and more 20%

It is levied on various business assets such as bonds, securities, real estate, precious

metals etc. The tax which is calculated for all these instruments on positive variation between

cost and selling price or profit. All the taxes which are received by government are used for

various purposes such as development of economy (Types of CGT Event, 2019). In Australia, if a

company is earning any type of capital gain then it have to pay tax around 30% of the profits.

According to Capital gain tax event A1, any type of gain which is generated from disposal of an

assets is disregarded under this head. It is applied of different conditions which are as follows:

Interest generated on asset when its market value is not more than $500.

An asset which is being purchased on a cost which does not exceeds limit of $500.

Interest generated on an asset which does not exceeds limit of $500 and acquired before

16 December 1995 (Burkhauser, Hahn and Wilkins, 2015).

1

Taxation is an amount which is required to be paid by individuals as well as corporation

on the incomes which is received by them from different sources. Governmental bodies

implement regulations related to tax and for all the tax payers it is very important to comply with

them. There are different types of taxes such as direct and indirect which are needed to be paid

by organisations and people. All the countries have their own taxation rules which is required to

be followed by individuals and organisations operating business in that nation.

MAIN BODY

Question 1

Capital gain tax: The tax which takes place when an asset is sold and the amount which

is being received is more than actual price of that asset is known as capital gain tax. Short term

capital gains are taxed at 37% and long term gains are taxed at up to 20% (Blunden, 2016). The

taxation slab for it is as follows:

Amount Taxation rate

0 – 51700 0% (tax free)

51707 – 452400 15%

452401 and more 20%

It is levied on various business assets such as bonds, securities, real estate, precious

metals etc. The tax which is calculated for all these instruments on positive variation between

cost and selling price or profit. All the taxes which are received by government are used for

various purposes such as development of economy (Types of CGT Event, 2019). In Australia, if a

company is earning any type of capital gain then it have to pay tax around 30% of the profits.

According to Capital gain tax event A1, any type of gain which is generated from disposal of an

assets is disregarded under this head. It is applied of different conditions which are as follows:

Interest generated on asset when its market value is not more than $500.

An asset which is being purchased on a cost which does not exceeds limit of $500.

Interest generated on an asset which does not exceeds limit of $500 and acquired before

16 December 1995 (Burkhauser, Hahn and Wilkins, 2015).

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

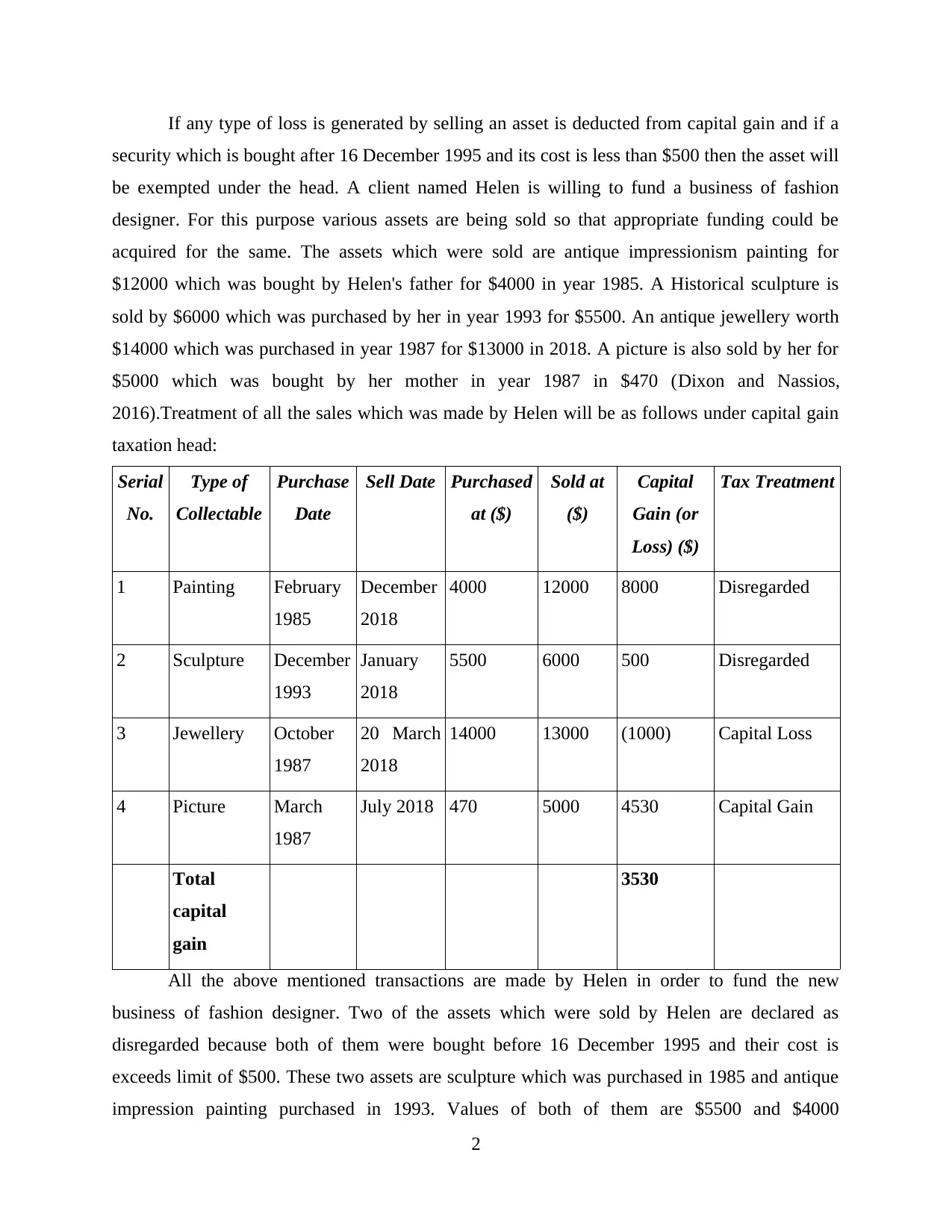

If any type of loss is generated by selling an asset is deducted from capital gain and if a

security which is bought after 16 December 1995 and its cost is less than $500 then the asset will

be exempted under the head. A client named Helen is willing to fund a business of fashion

designer. For this purpose various assets are being sold so that appropriate funding could be

acquired for the same. The assets which were sold are antique impressionism painting for

$12000 which was bought by Helen's father for $4000 in year 1985. A Historical sculpture is

sold by $6000 which was purchased by her in year 1993 for $5500. An antique jewellery worth

$14000 which was purchased in year 1987 for $13000 in 2018. A picture is also sold by her for

$5000 which was bought by her mother in year 1987 in $470 (Dixon and Nassios,

2016).Treatment of all the sales which was made by Helen will be as follows under capital gain

taxation head:

Serial

No.

Type of

Collectable

Purchase

Date

Sell Date Purchased

at ($)

Sold at

($)

Capital

Gain (or

Loss) ($)

Tax Treatment

1 Painting February

1985

December

2018

4000 12000 8000 Disregarded

2 Sculpture December

1993

January

2018

5500 6000 500 Disregarded

3 Jewellery October

1987

20 March

2018

14000 13000 (1000) Capital Loss

4 Picture March

1987

July 2018 470 5000 4530 Capital Gain

Total

capital

gain

3530

All the above mentioned transactions are made by Helen in order to fund the new

business of fashion designer. Two of the assets which were sold by Helen are declared as

disregarded because both of them were bought before 16 December 1995 and their cost is

exceeds limit of $500. These two assets are sculpture which was purchased in 1985 and antique

impression painting purchased in 1993. Values of both of them are $5500 and $4000

2

security which is bought after 16 December 1995 and its cost is less than $500 then the asset will

be exempted under the head. A client named Helen is willing to fund a business of fashion

designer. For this purpose various assets are being sold so that appropriate funding could be

acquired for the same. The assets which were sold are antique impressionism painting for

$12000 which was bought by Helen's father for $4000 in year 1985. A Historical sculpture is

sold by $6000 which was purchased by her in year 1993 for $5500. An antique jewellery worth

$14000 which was purchased in year 1987 for $13000 in 2018. A picture is also sold by her for

$5000 which was bought by her mother in year 1987 in $470 (Dixon and Nassios,

2016).Treatment of all the sales which was made by Helen will be as follows under capital gain

taxation head:

Serial

No.

Type of

Collectable

Purchase

Date

Sell Date Purchased

at ($)

Sold at

($)

Capital

Gain (or

Loss) ($)

Tax Treatment

1 Painting February

1985

December

2018

4000 12000 8000 Disregarded

2 Sculpture December

1993

January

2018

5500 6000 500 Disregarded

3 Jewellery October

1987

20 March

2018

14000 13000 (1000) Capital Loss

4 Picture March

1987

July 2018 470 5000 4530 Capital Gain

Total

capital

gain

3530

All the above mentioned transactions are made by Helen in order to fund the new

business of fashion designer. Two of the assets which were sold by Helen are declared as

disregarded because both of them were bought before 16 December 1995 and their cost is

exceeds limit of $500. These two assets are sculpture which was purchased in 1985 and antique

impression painting purchased in 1993. Values of both of them are $5500 and $4000

2

respectively. Antique jewellery which was sold by Helen for $13000 acquired in year 1987 is

showing capital loss of $1000 as it was purchased for $14000. This $1000 which is a long term

capital gain will be reduced from total income of capital gain head (Richardson, Taylor and

Lanis, 2015). The picture which was bought in year 1987 and sold in 2018 is showing capital

gain of $4530 as it was sold for $5000 and acquired for $470. Total capital gain of Helen is

$3530 ($4530-$1000).

Question 2

Income from personal exertion refers to the gains which are acquired by individuals by

earning ordinary income directly with the help of their own skills or knowledge. Barbara is an

economist researcher and commentator. She has got an offer from Eco books Limited to write a

book regarding economic principles for $13000. It will be the first time when Barbara is going to

write a book in her career and she accepts the offer and writes a book on principles of

Economics. The copyrights of the books wrote by Barbara were assigned to Eco Books Limited

for $13400. The books were published and she is being paid by the book publisher. Manuscripts

of books are also sold by Barbara to the library of Eco Books Ltd. for $4350 and she has also

collected $3200 for the interviews which were related to writing of the book (Hockridge, 2018).

In order to calculate income generated from personal exertion following steps are going to be

undertaken:

First of all appropriate transaction are identified which could be considered as the part of

income from personal exertion.

Afterwards it is analysed that the income is actually related to the head or not.

Identification of transactions which were generated from personal exertion:

Transaction Amount ($) Personal Exertion

Income received from publication of

books

13400 Yes

Manuscripts which were sold in the

library

4530 Yes

Income generated from interviews

related to book publishing

3200 Yes

3

showing capital loss of $1000 as it was purchased for $14000. This $1000 which is a long term

capital gain will be reduced from total income of capital gain head (Richardson, Taylor and

Lanis, 2015). The picture which was bought in year 1987 and sold in 2018 is showing capital

gain of $4530 as it was sold for $5000 and acquired for $470. Total capital gain of Helen is

$3530 ($4530-$1000).

Question 2

Income from personal exertion refers to the gains which are acquired by individuals by

earning ordinary income directly with the help of their own skills or knowledge. Barbara is an

economist researcher and commentator. She has got an offer from Eco books Limited to write a

book regarding economic principles for $13000. It will be the first time when Barbara is going to

write a book in her career and she accepts the offer and writes a book on principles of

Economics. The copyrights of the books wrote by Barbara were assigned to Eco Books Limited

for $13400. The books were published and she is being paid by the book publisher. Manuscripts

of books are also sold by Barbara to the library of Eco Books Ltd. for $4350 and she has also

collected $3200 for the interviews which were related to writing of the book (Hockridge, 2018).

In order to calculate income generated from personal exertion following steps are going to be

undertaken:

First of all appropriate transaction are identified which could be considered as the part of

income from personal exertion.

Afterwards it is analysed that the income is actually related to the head or not.

Identification of transactions which were generated from personal exertion:

Transaction Amount ($) Personal Exertion

Income received from publication of

books

13400 Yes

Manuscripts which were sold in the

library

4530 Yes

Income generated from interviews

related to book publishing

3200 Yes

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total income generated from

personal exertion

21130

The above table shows all the transaction which could be considered as the part of

income generated from self exerted sources. Detailed analysis of all of them are as follows:

Income received from publication of books: Amount of $13000 was offered by Eco

Books Limited to Barbara to write a book on Principles of Economics. The offer was accepted

by her and a book was wrote by her. Total amount which was provided by the publishing

company was around $13400. It is considered as income which is being acquired from personal

exertion. According to a case s6-5, Hochstrasser v Mayes [1960] of ITAA 1997, it is vital to if,

benefits from a contract are received, then it does not lave impact upon the time when the

activity is being completed. All the incomes which are received from such activities which were

conducted with the help of personal skills and knowledge then it will be treated as income

acquired from personal exertion. This law also states that income which is being generated by

Barbara by selling copyrights to Eco Books Limited (McGuire, Seib and Anderson, 2016).

Manuscripts which were sold in the library: This transaction is also considered as

Barbara's income which is being generated by her by selling manuscripts in library of Eco Books

Limited. Main reason behind taking this income under this head is that manuscripts are the drafts

of final published books so the income is also related to books. Barbara has received $4530 for

manuscripts which were considered as the part of her personal exertion income. Another reason

for considering it as personal income is that efforts which were made by writer while writing

manuscripts are part of the book writing activities. According to s6-5, Kelly v FCT [1985] of

ITAA 1997, if any type of benefit is received by a person for an activity which is related to main

task is considered as income generated from personal exertion whether it is received from third

party. In this case Barbara received $4530 from external parties by selling manuscripts to them

which was a part of final book so it is treated as income from personal exertion (Personal

Exertion, 2019).

Income generated from interviews related to book publishing: When Barbara was

writing the book named Principles of Economics various interviews conducted by her which

were related to the book publishing. From this activity Barbara received $3200. this amount is

also considered as the part of income from personal exertion as it was the part of the activity

which is being mentioned in offer which is provided by Eco Books Limited to her. According to

4

personal exertion

21130

The above table shows all the transaction which could be considered as the part of

income generated from self exerted sources. Detailed analysis of all of them are as follows:

Income received from publication of books: Amount of $13000 was offered by Eco

Books Limited to Barbara to write a book on Principles of Economics. The offer was accepted

by her and a book was wrote by her. Total amount which was provided by the publishing

company was around $13400. It is considered as income which is being acquired from personal

exertion. According to a case s6-5, Hochstrasser v Mayes [1960] of ITAA 1997, it is vital to if,

benefits from a contract are received, then it does not lave impact upon the time when the

activity is being completed. All the incomes which are received from such activities which were

conducted with the help of personal skills and knowledge then it will be treated as income

acquired from personal exertion. This law also states that income which is being generated by

Barbara by selling copyrights to Eco Books Limited (McGuire, Seib and Anderson, 2016).

Manuscripts which were sold in the library: This transaction is also considered as

Barbara's income which is being generated by her by selling manuscripts in library of Eco Books

Limited. Main reason behind taking this income under this head is that manuscripts are the drafts

of final published books so the income is also related to books. Barbara has received $4530 for

manuscripts which were considered as the part of her personal exertion income. Another reason

for considering it as personal income is that efforts which were made by writer while writing

manuscripts are part of the book writing activities. According to s6-5, Kelly v FCT [1985] of

ITAA 1997, if any type of benefit is received by a person for an activity which is related to main

task is considered as income generated from personal exertion whether it is received from third

party. In this case Barbara received $4530 from external parties by selling manuscripts to them

which was a part of final book so it is treated as income from personal exertion (Personal

Exertion, 2019).

Income generated from interviews related to book publishing: When Barbara was

writing the book named Principles of Economics various interviews conducted by her which

were related to the book publishing. From this activity Barbara received $3200. this amount is

also considered as the part of income from personal exertion as it was the part of the activity

which is being mentioned in offer which is provided by Eco Books Limited to her. According to

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

s6-5 of ITAA 1997, if an interview is conducted which is related to launching of a new book in

the market will be considered as a part of income from personal exertion. Hence the amount of

$3200 is also treated as personal income of Barbara (Smith, 2015).

By considering all the incomes in personal exertion income of Barbara total income of

her will be around $21130.

Treatment of rewards if Barbara has written books otherwise: If the book was

written by Barbara otherwise then it could be considered as business income rather than personal

one. Reason behind treating it as business income is that books would have been wrote for the

purpose of selling them later. The income which will be received from writing them otherwise

will be taxable in that accounting year in which it will be generated.

Question 3

David who is son of Patrick received $52000 from his father on a condition that this

amount will be refunded after 5 years as $58000. This amount is considered as a loan which was

provided by Patrick without any formal agreement or security deposit. According to Patrick,

David is not required to pay any type of interest (Rimmer, Smith and Wende, 2014). David

repaid total amount with 5% addition after two years will be to Patrick. So the amount which was

be repaid by David is ($52000+5%) $54600. this income will leave impact upon total incomes of

Patrick because there will e no direct tax for Patrick due to no agreement between them. As the

business will grow in upcoming years and start to generated profits so Patrick will be considered

as main investor of David's business. According to this clause Patrick will be the shareholder of

the business. The additional amount which is being paid by David to Patrick will be considered

as dividend. The additional amount is $2600 (54600 – 52000). This dividend will be the part of

income from other sources for Patrick. Due to this taxable income will be increased and Patrick

have to pay additional tax on income from other sources (Wilkins, 2015).

CONCLUSION

From the above project report it has been concluded that all the individuals and

corporations are required to pay appropriate amount of taxation on their incomes according to

governmental rules and regulations. If they are not able to pay amount according to legal

requirements then it may result in strict action of legal authorities against them. There are various

types of taxations such as capital gain, personal exertion, other sources etc. Australian Tax

5

the market will be considered as a part of income from personal exertion. Hence the amount of

$3200 is also treated as personal income of Barbara (Smith, 2015).

By considering all the incomes in personal exertion income of Barbara total income of

her will be around $21130.

Treatment of rewards if Barbara has written books otherwise: If the book was

written by Barbara otherwise then it could be considered as business income rather than personal

one. Reason behind treating it as business income is that books would have been wrote for the

purpose of selling them later. The income which will be received from writing them otherwise

will be taxable in that accounting year in which it will be generated.

Question 3

David who is son of Patrick received $52000 from his father on a condition that this

amount will be refunded after 5 years as $58000. This amount is considered as a loan which was

provided by Patrick without any formal agreement or security deposit. According to Patrick,

David is not required to pay any type of interest (Rimmer, Smith and Wende, 2014). David

repaid total amount with 5% addition after two years will be to Patrick. So the amount which was

be repaid by David is ($52000+5%) $54600. this income will leave impact upon total incomes of

Patrick because there will e no direct tax for Patrick due to no agreement between them. As the

business will grow in upcoming years and start to generated profits so Patrick will be considered

as main investor of David's business. According to this clause Patrick will be the shareholder of

the business. The additional amount which is being paid by David to Patrick will be considered

as dividend. The additional amount is $2600 (54600 – 52000). This dividend will be the part of

income from other sources for Patrick. Due to this taxable income will be increased and Patrick

have to pay additional tax on income from other sources (Wilkins, 2015).

CONCLUSION

From the above project report it has been concluded that all the individuals and

corporations are required to pay appropriate amount of taxation on their incomes according to

governmental rules and regulations. If they are not able to pay amount according to legal

requirements then it may result in strict action of legal authorities against them. There are various

types of taxations such as capital gain, personal exertion, other sources etc. Australian Tax

5

authority have imposed different types of rules for all these incomes and individuals who are

generating all of them have to follow the legislation. It can help them to reduce possibilities of

interferences of government in this business or personal activities.

6

generating all of them have to follow the legislation. It can help them to reduce possibilities of

interferences of government in this business or personal activities.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.