T2 2017 HI6028 Taxation Theory, Practice & Law Individual Assignment

VerifiedAdded on 2019/10/30

|10

|2362

|194

Homework Assignment

AI Summary

This document presents a comprehensive solution to a HI6028 Taxation Theory, Practice & Law individual assignment from T2 2017. The assignment addresses five key issues: tax implications of asset sales, taxability of fringe benefits (loans), tax consequences of rental property ownership, the concept of tax evasion vs. tax planning (IRC v. Duke of Westminster), and the tax implications of timber sales. Each question includes an issue statement, relevant tax regulations, applicability analysis, and a conclusion. The solution references various books and journals to support the analysis, offering a detailed understanding of Australian taxation law concerning capital gains, fringe benefits, property, and business income. The assignment covers CGT, FBT, partnership, and income from timber sales, providing a thorough overview of taxation principles and their practical application.

HI6028 Taxation Theory, Practice

& Law

T2 2017 Individual Assignment

& Law

T2 2017 Individual Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Question 1..................................................................................................................................3

Issue........................................................................................................................................3

Regulations.............................................................................................................................3

Applicability...........................................................................................................................3

Conclusion..............................................................................................................................3

Question 2..................................................................................................................................3

Issue........................................................................................................................................3

Regulations.............................................................................................................................3

Applicability...........................................................................................................................4

Conclusion..............................................................................................................................4

Question 3..................................................................................................................................4

Issue........................................................................................................................................4

Regulations.............................................................................................................................4

Applicability...........................................................................................................................5

Conclusion..............................................................................................................................5

Question 4..................................................................................................................................5

Issue........................................................................................................................................5

Regulations.............................................................................................................................5

Applicability...........................................................................................................................6

Conclusion..............................................................................................................................6

Question 5..................................................................................................................................6

Issue........................................................................................................................................6

Regulations.............................................................................................................................6

Applicability and Conclusion.................................................................................................7

References..................................................................................................................................8

Question 1..................................................................................................................................3

Issue........................................................................................................................................3

Regulations.............................................................................................................................3

Applicability...........................................................................................................................3

Conclusion..............................................................................................................................3

Question 2..................................................................................................................................3

Issue........................................................................................................................................3

Regulations.............................................................................................................................3

Applicability...........................................................................................................................4

Conclusion..............................................................................................................................4

Question 3..................................................................................................................................4

Issue........................................................................................................................................4

Regulations.............................................................................................................................4

Applicability...........................................................................................................................5

Conclusion..............................................................................................................................5

Question 4..................................................................................................................................5

Issue........................................................................................................................................5

Regulations.............................................................................................................................5

Applicability...........................................................................................................................6

Conclusion..............................................................................................................................6

Question 5..................................................................................................................................6

Issue........................................................................................................................................6

Regulations.............................................................................................................................6

Applicability and Conclusion.................................................................................................7

References..................................................................................................................................8

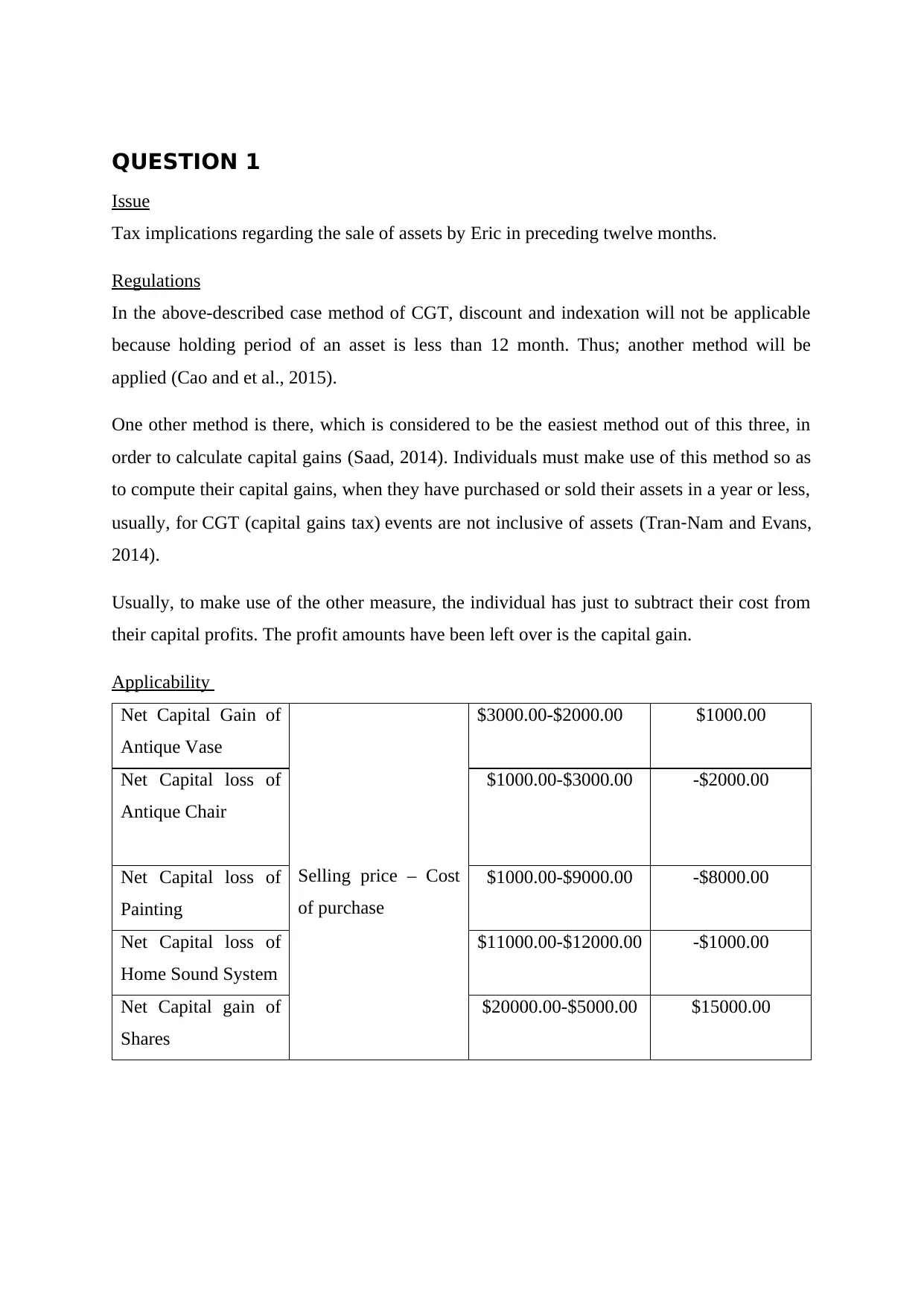

QUESTION 1

Issue

Tax implications regarding the sale of assets by Eric in preceding twelve months.

Regulations

In the above-described case method of CGT, discount and indexation will not be applicable

because holding period of an asset is less than 12 month. Thus; another method will be

applied (Cao and et al., 2015).

One other method is there, which is considered to be the easiest method out of this three, in

order to calculate capital gains (Saad, 2014). Individuals must make use of this method so as

to compute their capital gains, when they have purchased or sold their assets in a year or less,

usually, for CGT (capital gains tax) events are not inclusive of assets (Tran‐Nam and Evans,

2014).

Usually, to make use of the other measure, the individual has just to subtract their cost from

their capital profits. The profit amounts have been left over is the capital gain.

Applicability

Net Capital Gain of

Antique Vase

Selling price – Cost

of purchase

$3000.00-$2000.00 $1000.00

Net Capital loss of

Antique Chair

$1000.00-$3000.00 -$2000.00

Net Capital loss of

Painting

$1000.00-$9000.00 -$8000.00

Net Capital loss of

Home Sound System

$11000.00-$12000.00 -$1000.00

Net Capital gain of

Shares

$20000.00-$5000.00 $15000.00

Issue

Tax implications regarding the sale of assets by Eric in preceding twelve months.

Regulations

In the above-described case method of CGT, discount and indexation will not be applicable

because holding period of an asset is less than 12 month. Thus; another method will be

applied (Cao and et al., 2015).

One other method is there, which is considered to be the easiest method out of this three, in

order to calculate capital gains (Saad, 2014). Individuals must make use of this method so as

to compute their capital gains, when they have purchased or sold their assets in a year or less,

usually, for CGT (capital gains tax) events are not inclusive of assets (Tran‐Nam and Evans,

2014).

Usually, to make use of the other measure, the individual has just to subtract their cost from

their capital profits. The profit amounts have been left over is the capital gain.

Applicability

Net Capital Gain of

Antique Vase

Selling price – Cost

of purchase

$3000.00-$2000.00 $1000.00

Net Capital loss of

Antique Chair

$1000.00-$3000.00 -$2000.00

Net Capital loss of

Painting

$1000.00-$9000.00 -$8000.00

Net Capital loss of

Home Sound System

$11000.00-$12000.00 -$1000.00

Net Capital gain of

Shares

$20000.00-$5000.00 $15000.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Conclusion

As per above calculations, $6000 capital gain will be taxable. Due to lack of

information regarding other income, it is assumed capital gains are sole income and tax rate

will be 10%, so the tax will be $600.

QUESTION 2

Issue

Taxability regarding Fringe benefit, i.e. loan provided at a special rate.

Regulations

Fringe benefits tax is the amount paid on some of the benefits which employers offer

to employees instead of wages or salaries (Mishra and Ratti, 2014). All the FBT along with

the value of taxes according to the Fringe Benefits Tax Assessment Act 1986, excluding

fringe benefits of tax-exempt body entertainment, are solely responsible for the payroll tax

(Burkhauser, Hahn, and Wilkins, 2015).

In case the benefit is not liable, excluding of the Superannuation Holding Accounts

Special Account deposits, or contains zero value will not be responsible for the payroll tax

(Mishra, 2014). The individual needs to state the real value of the entire fringe benefits for

every month. However, individual can make use of estimate method for every month, if they

have payments of fringe benefits for 15 months or more than this (Bond and Wright, 2017).

If not, then the individual should provide the real amounts of fringe benefits. It can be

performed on a monthly basis by adding up all the benefits further multiplying the total Type

1 and Type 2 by the appropriate Type 2 rate of gross for the particular year (Woellner and et

al., 2016). The interest rate of the benchmark can be used in order to estimate the taxable

value of the following:FBT provided in the way of loan, FBT of a car, when employees want

to measure the benefit by making use of operating cost method.

Statutory Rate

FBT year Benchmark rate Reference

1 April 2016 to 31 March 2017 5.65% TD 2016/5

As per above calculations, $6000 capital gain will be taxable. Due to lack of

information regarding other income, it is assumed capital gains are sole income and tax rate

will be 10%, so the tax will be $600.

QUESTION 2

Issue

Taxability regarding Fringe benefit, i.e. loan provided at a special rate.

Regulations

Fringe benefits tax is the amount paid on some of the benefits which employers offer

to employees instead of wages or salaries (Mishra and Ratti, 2014). All the FBT along with

the value of taxes according to the Fringe Benefits Tax Assessment Act 1986, excluding

fringe benefits of tax-exempt body entertainment, are solely responsible for the payroll tax

(Burkhauser, Hahn, and Wilkins, 2015).

In case the benefit is not liable, excluding of the Superannuation Holding Accounts

Special Account deposits, or contains zero value will not be responsible for the payroll tax

(Mishra, 2014). The individual needs to state the real value of the entire fringe benefits for

every month. However, individual can make use of estimate method for every month, if they

have payments of fringe benefits for 15 months or more than this (Bond and Wright, 2017).

If not, then the individual should provide the real amounts of fringe benefits. It can be

performed on a monthly basis by adding up all the benefits further multiplying the total Type

1 and Type 2 by the appropriate Type 2 rate of gross for the particular year (Woellner and et

al., 2016). The interest rate of the benchmark can be used in order to estimate the taxable

value of the following:FBT provided in the way of loan, FBT of a car, when employees want

to measure the benefit by making use of operating cost method.

Statutory Rate

FBT year Benchmark rate Reference

1 April 2016 to 31 March 2017 5.65% TD 2016/5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Applicability

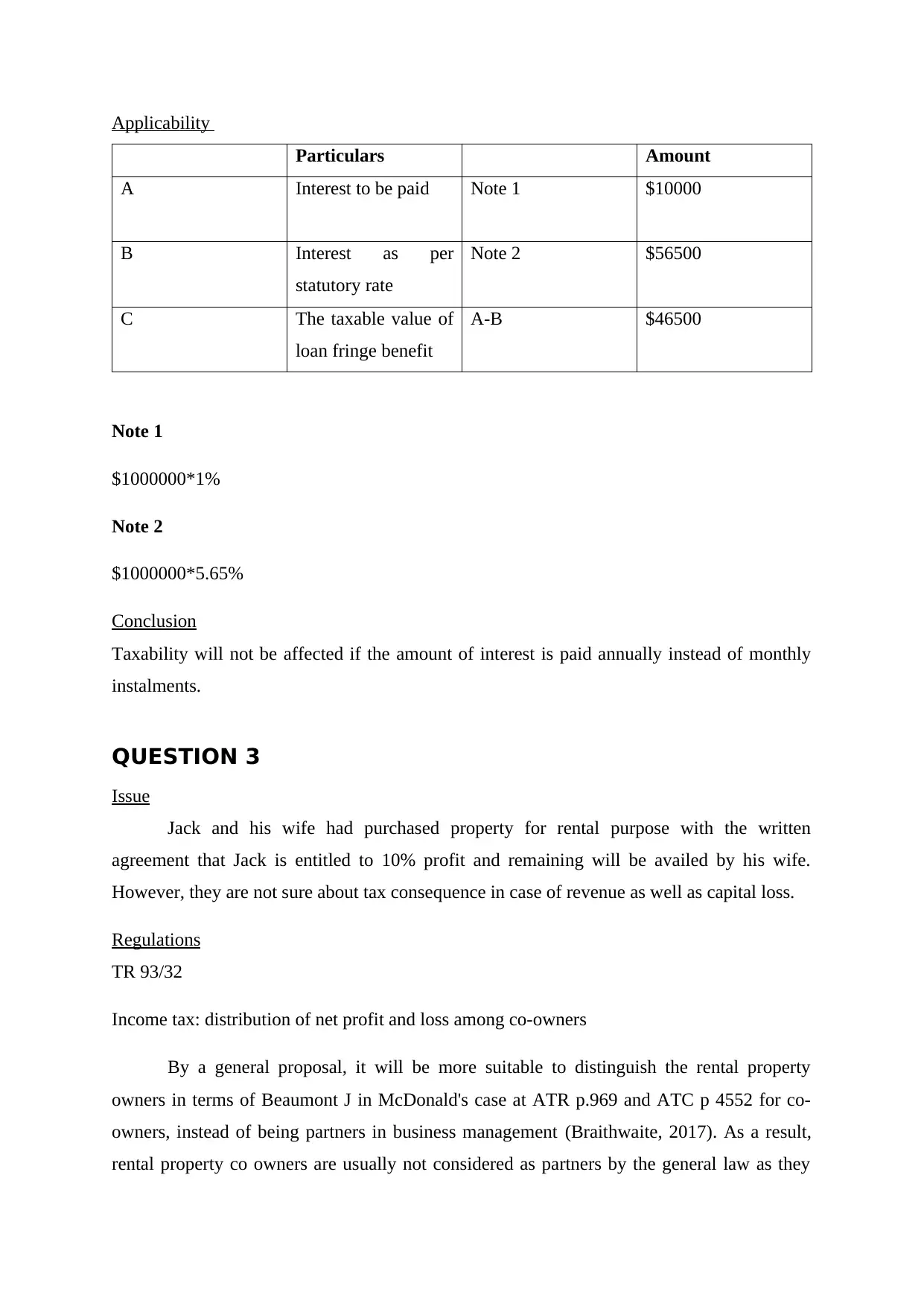

Particulars Amount

A Interest to be paid Note 1 $10000

B Interest as per

statutory rate

Note 2 $56500

C The taxable value of

loan fringe benefit

A-B $46500

Note 1

$1000000*1%

Note 2

$1000000*5.65%

Conclusion

Taxability will not be affected if the amount of interest is paid annually instead of monthly

instalments.

QUESTION 3

Issue

Jack and his wife had purchased property for rental purpose with the written

agreement that Jack is entitled to 10% profit and remaining will be availed by his wife.

However, they are not sure about tax consequence in case of revenue as well as capital loss.

Regulations

TR 93/32

Income tax: distribution of net profit and loss among co-owners

By a general proposal, it will be more suitable to distinguish the rental property

owners in terms of Beaumont J in McDonald's case at ATR p.969 and ATC p 4552 for co-

owners, instead of being partners in business management (Braithwaite, 2017). As a result,

rental property co owners are usually not considered as partners by the general law as they

Particulars Amount

A Interest to be paid Note 1 $10000

B Interest as per

statutory rate

Note 2 $56500

C The taxable value of

loan fringe benefit

A-B $46500

Note 1

$1000000*1%

Note 2

$1000000*5.65%

Conclusion

Taxability will not be affected if the amount of interest is paid annually instead of monthly

instalments.

QUESTION 3

Issue

Jack and his wife had purchased property for rental purpose with the written

agreement that Jack is entitled to 10% profit and remaining will be availed by his wife.

However, they are not sure about tax consequence in case of revenue as well as capital loss.

Regulations

TR 93/32

Income tax: distribution of net profit and loss among co-owners

By a general proposal, it will be more suitable to distinguish the rental property

owners in terms of Beaumont J in McDonald's case at ATR p.969 and ATC p 4552 for co-

owners, instead of being partners in business management (Braithwaite, 2017). As a result,

rental property co owners are usually not considered as partners by the general law as they

are not based not the applicable general law to a partnership comprising the distribution of

gains and losses from the rental property.

Applicability

In accordance with the cited provisions, there is no existence of partnership according

to the general law among the respondent and their spouse. The relationship among them was

said to be of co ownership, and if they agree to partnership under subsection 6(1), this

situation will be stated as irrelevant, as their unreal partnership will carry such consequences

that they have to treat each other as a pure partner for some specific purposes (Long,

Campbell and Kelshaw, 2016). It will not practise the deduction responded will make on the

loss of business. They can only subtract the interest of the individual in the loss of partnership

(Arnold and et al., 2014). The individual interest is that interest which is allowed entirely to

the partner, be compared with their joint interest in the property as a whole: in this aspect

case of FCT v Whiting (1943), 68 CLR 199 at 204; 2 AITR 421 at 425-6 can be referred.

Conclusion

Thus, it is essential to identify either both the respondent and his wife are just only

notional partners for the intention of the Act or are pure partners according to the general law.

By considering their deed partners will be liable for proportionate loss and can claim for the

same.

QUESTION 4

Issue

IRC v. Duke of Westminster carried out an agreement of covalent with his associates

inclusive of household helpers, servants, gardeners etc. In the particular agreement, Duke

obliged to pay his fellow some money in exchange for their work. A letter was submitted to

the fellows declaring that Duke will pay wages on extra sums, if there is any, for their

services. Still, the servants received the same wage as before, however Duke was benefitted

from this as he earned tax benefit under the law that applied at that time period, and the deed

decreased Duke's liability to additional charges.

Regulations

For this case, handed over to the House of Lords, the judge Lord Tomlin said that;

gains and losses from the rental property.

Applicability

In accordance with the cited provisions, there is no existence of partnership according

to the general law among the respondent and their spouse. The relationship among them was

said to be of co ownership, and if they agree to partnership under subsection 6(1), this

situation will be stated as irrelevant, as their unreal partnership will carry such consequences

that they have to treat each other as a pure partner for some specific purposes (Long,

Campbell and Kelshaw, 2016). It will not practise the deduction responded will make on the

loss of business. They can only subtract the interest of the individual in the loss of partnership

(Arnold and et al., 2014). The individual interest is that interest which is allowed entirely to

the partner, be compared with their joint interest in the property as a whole: in this aspect

case of FCT v Whiting (1943), 68 CLR 199 at 204; 2 AITR 421 at 425-6 can be referred.

Conclusion

Thus, it is essential to identify either both the respondent and his wife are just only

notional partners for the intention of the Act or are pure partners according to the general law.

By considering their deed partners will be liable for proportionate loss and can claim for the

same.

QUESTION 4

Issue

IRC v. Duke of Westminster carried out an agreement of covalent with his associates

inclusive of household helpers, servants, gardeners etc. In the particular agreement, Duke

obliged to pay his fellow some money in exchange for their work. A letter was submitted to

the fellows declaring that Duke will pay wages on extra sums, if there is any, for their

services. Still, the servants received the same wage as before, however Duke was benefitted

from this as he earned tax benefit under the law that applied at that time period, and the deed

decreased Duke's liability to additional charges.

Regulations

For this case, handed over to the House of Lords, the judge Lord Tomlin said that;

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Each and every person is allowed, if they arrange their own affairs so that the tax been

attached according to the suitable action would be less than it should be (AO, M.D.A., 2015).

If they get success in arranging them then they can safeguard the outcome, however, then no

appreciation by the fellows or Inland Revenue Commissioners might be of their initiatives,

and are not bound to pay surplus taxes (Barkoczy, 2017).

Applicability

This case cited that the tax evasion will only be accepted if it practices initiated statue

law or act that will reduce the liability of Duke, if it is allowed and do deed in accordance

with the yearly payment. It is declared that if any company adopts such tools will be

responsible for tax profit reductions, or else will not be allowable. Further, the court must

look upon the broad economic jurisprudence and states in order to keep it up, in context with

tax planning which will be introduced for tax evasions. Hence, the court must declare this

principle as invalid.

Conclusion

This case provides clear guidance regarding drawing difference better tax evasion and

fair tax practices to ensure viable regulatory compliance.

QUESTION 5

Issue

In this case, Bill is the owner of a large parcel of land in which there are various tall

pine trees. He has been offered to get paid $1,000 for every 100 metres of timber on this land

by a logging company. Now he wants to know about tax implications of receipt and

consequence if lump sum amount is paid for granting the right to the logging company.

Regulations

Rule of taxation

TR 95/6

Standing timber’s disposal, but not in regular business course

If a taxpayer owns a disposal of timber, which is planted for the reason of sale might

lead to the value of those trees inclusive in the assessable income of the taxpayer, according

to the subsection 36(1), during the period when disposal will take place (Blakelock and King,

attached according to the suitable action would be less than it should be (AO, M.D.A., 2015).

If they get success in arranging them then they can safeguard the outcome, however, then no

appreciation by the fellows or Inland Revenue Commissioners might be of their initiatives,

and are not bound to pay surplus taxes (Barkoczy, 2017).

Applicability

This case cited that the tax evasion will only be accepted if it practices initiated statue

law or act that will reduce the liability of Duke, if it is allowed and do deed in accordance

with the yearly payment. It is declared that if any company adopts such tools will be

responsible for tax profit reductions, or else will not be allowable. Further, the court must

look upon the broad economic jurisprudence and states in order to keep it up, in context with

tax planning which will be introduced for tax evasions. Hence, the court must declare this

principle as invalid.

Conclusion

This case provides clear guidance regarding drawing difference better tax evasion and

fair tax practices to ensure viable regulatory compliance.

QUESTION 5

Issue

In this case, Bill is the owner of a large parcel of land in which there are various tall

pine trees. He has been offered to get paid $1,000 for every 100 metres of timber on this land

by a logging company. Now he wants to know about tax implications of receipt and

consequence if lump sum amount is paid for granting the right to the logging company.

Regulations

Rule of taxation

TR 95/6

Standing timber’s disposal, but not in regular business course

If a taxpayer owns a disposal of timber, which is planted for the reason of sale might

lead to the value of those trees inclusive in the assessable income of the taxpayer, according

to the subsection 36(1), during the period when disposal will take place (Blakelock and King,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2017). This might be either the taxpayer is running the business of forest operation or not,

since the taxpayer is running the business and there is no disposal in the regular business

course. The main thing being required is the trees comprise the total asset of business as a

whole.

Either or nor a specific deed results in a tress disposal, been said by the distinct, from

the sale of a land’s interest, rely on the basis of interpretation of that deed. The Subsection

36(1) will not be applicable if the trees are planted on leased land and if the lessee doesn’t

contain entire ownership on trees were planted on the leased land (Lam and Whitney, 2016).

Rights disposal to standing timber

A tax payer running a business of forest operation might sell its standing timber via giving a

right to any individual to remove or cut the standing timber, if there will be right or not to cut

the timber is practised (Barkoczy. 2016). The profits earned from that sale are assessable in

accordance with subsection 25(1).

Applicability and Conclusion

By considering regulatory provisions, if Bill get a receipt of $1000 then income will

be assessed as per provisions of 36(1) and if lump sum amount is paid then taxability will be

as per subsection 25(1).

since the taxpayer is running the business and there is no disposal in the regular business

course. The main thing being required is the trees comprise the total asset of business as a

whole.

Either or nor a specific deed results in a tress disposal, been said by the distinct, from

the sale of a land’s interest, rely on the basis of interpretation of that deed. The Subsection

36(1) will not be applicable if the trees are planted on leased land and if the lessee doesn’t

contain entire ownership on trees were planted on the leased land (Lam and Whitney, 2016).

Rights disposal to standing timber

A tax payer running a business of forest operation might sell its standing timber via giving a

right to any individual to remove or cut the standing timber, if there will be right or not to cut

the timber is practised (Barkoczy. 2016). The profits earned from that sale are assessable in

accordance with subsection 25(1).

Applicability and Conclusion

By considering regulatory provisions, if Bill get a receipt of $1000 then income will

be assessed as per provisions of 36(1) and if lump sum amount is paid then taxability will be

as per subsection 25(1).

REFERENCES

Books and journals

AO, M.D.A., 2015. Modernising the Australian Taxation Office: Vision, people, systems and

values. eJournal of Tax Research, 13(1), p.1.

Arnold, B.R., Bateman, H., Ferguson, A. and Raftery, A., 2014. The size, cost and asset

allocation of Australian self-managed superannuation funds.

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Barkoczy, S., 2017. Core Tax Legislation and Study Guide. OUP Catalogue.

Blakelock, S. and King, P., 2017. Taxation law: The advance of ATO data matching. Proctor,

The, 37(6), p.18.

Bond, D. and Wright, A., 2017. A Snapshot of the Australian Taxpayer.

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax

record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2),

pp.181-205.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and

Wende, S., 2015. Understanding the economy-wide efficiency and incidence of major

Australian taxes. Treasury WP, 1.

Lam, D. and Whitney, A., 2016. Taxation and property: Practical aspects of the new foreign

resident CGT witholding tax. LSJ: Law Society of NSW Journal, (21), p.84.

Long, B., Campbell, J. and Kelshaw, C., 2016. The justice lens on taxation policy in

Australia. St Mark's Review, (235), p.94.

Mishra, A.V. and Ratti, R.A., 2014. Taxation of domestic dividend income and foreign

investment holdings. International Review of Economics & Finance,31, pp.218-231.

Books and journals

AO, M.D.A., 2015. Modernising the Australian Taxation Office: Vision, people, systems and

values. eJournal of Tax Research, 13(1), p.1.

Arnold, B.R., Bateman, H., Ferguson, A. and Raftery, A., 2014. The size, cost and asset

allocation of Australian self-managed superannuation funds.

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Barkoczy, S., 2017. Core Tax Legislation and Study Guide. OUP Catalogue.

Blakelock, S. and King, P., 2017. Taxation law: The advance of ATO data matching. Proctor,

The, 37(6), p.18.

Bond, D. and Wright, A., 2017. A Snapshot of the Australian Taxpayer.

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax

record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2),

pp.181-205.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and

Wende, S., 2015. Understanding the economy-wide efficiency and incidence of major

Australian taxes. Treasury WP, 1.

Lam, D. and Whitney, A., 2016. Taxation and property: Practical aspects of the new foreign

resident CGT witholding tax. LSJ: Law Society of NSW Journal, (21), p.84.

Long, B., Campbell, J. and Kelshaw, C., 2016. The justice lens on taxation policy in

Australia. St Mark's Review, (235), p.94.

Mishra, A.V. and Ratti, R.A., 2014. Taxation of domestic dividend income and foreign

investment holdings. International Review of Economics & Finance,31, pp.218-231.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Mishra, A.V., 2014. Australia's home bias and cross border taxation. Global Finance

Journal, 25(2), pp.108-123.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Tran‐Nam, B. and Evans, C., 2014. Towards the development of a tax system complexity

index. Fiscal Studies, 35(3), pp.341-370.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Journal, 25(2), pp.108-123.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Tran‐Nam, B. and Evans, C., 2014. Towards the development of a tax system complexity

index. Fiscal Studies, 35(3), pp.341-370.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.