University Taxation Law Case Study: Individual Taxpayer Assessment 2

VerifiedAdded on 2022/09/01

|13

|2937

|13

Case Study

AI Summary

This case study provides a comprehensive analysis of an individual taxpayer's tax obligations, covering various income sources, deductions, and tax offsets. The assignment examines income from employment, including gross wages, allowances, and fringe benefits, as well as income from business activities, such as receipts, trading stock, and private expenses. It also delves into income derived from rental properties, including rent, compensation, and deductible expenses like mortgage interest and travel. The assessment further explores the application of relevant tax legislation, including ITAA 1997 and FBTAA 1986, and the implications of specific deductions and offsets, such as those related to dependent spouses. The analysis incorporates case law to support the tax treatment of different income and expense items, providing a detailed understanding of the tax implications for the individual taxpayer.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Income and Expense Information:.............................................................................................2

Part A: Income from Employment:............................................................................................2

Part B: Income from business:...................................................................................................4

Part C: Income from Rental Property:.......................................................................................7

Dependent tax Offset:................................................................................................................9

References:...............................................................................................................................11

Table of Contents

Income and Expense Information:.............................................................................................2

Part A: Income from Employment:............................................................................................2

Part B: Income from business:...................................................................................................4

Part C: Income from Rental Property:.......................................................................................7

Dependent tax Offset:................................................................................................................9

References:...............................................................................................................................11

2TAXATION LAW

Income and Expense Information:

As per “sec 6-5 ITAA 1997” the ordinary income is an income that is in agreement

with the ordinary concepts. Interest is held as ordinary income and included in taxable

income. Eric has a joint term deposit account with his wife Linda in ANZ bank and earns an

income of $500 (Burman et al., 2016). The interest is an ordinary income under “sec 6-5

ITAA 1997” and included in taxable income of Eric.

Specific deduction is given in “sec 25-5 ITAA 1997” for outgoings incurred in

managing tax affairs. Eric has paid $400 to a tax agent for preparing his tax return. Therefore

it is allowable specific deduction under “sec 25-5 ITAA 1997”.

Part A: Income from Employment:

When a taxpayer gets a receipt from the employment and from delivering any sort of

personal services then it may be considered as the subject of tax for the employee or may be

held as fringe benefit tax for the employer. The receipt should be having nexus with the

personal service to constitute ordinary income. The example of “Dean v FCT (1997)” says

that retention payment given to employee for being employed was held as income in nature

(LeFevre, 2016). Similarly, Eric has received $7,800 as gross wages by working as employee

for Blue Merlin. The gross wages is a personal service income. Noting “Dean v FCT

(1997)” is a subject of tax for Eric and it is included for assessment as ordinary income under

“sec 6-5 ITA Act 97”.

Employees generally faces problem in understanding as what constitute allowance or

reimbursement. Allowances are salary and wages and it is simply excluded from being

considered as fringe benefit. It is treated taxable in the employees hand under the statutory

provision of “sec 15-2 ITAA 1997”. On the other hand, reimbursement is not a wages or

salary. The finding of court in Roads and Traffic Authority of “NSW v FCT (1993)” says

Income and Expense Information:

As per “sec 6-5 ITAA 1997” the ordinary income is an income that is in agreement

with the ordinary concepts. Interest is held as ordinary income and included in taxable

income. Eric has a joint term deposit account with his wife Linda in ANZ bank and earns an

income of $500 (Burman et al., 2016). The interest is an ordinary income under “sec 6-5

ITAA 1997” and included in taxable income of Eric.

Specific deduction is given in “sec 25-5 ITAA 1997” for outgoings incurred in

managing tax affairs. Eric has paid $400 to a tax agent for preparing his tax return. Therefore

it is allowable specific deduction under “sec 25-5 ITAA 1997”.

Part A: Income from Employment:

When a taxpayer gets a receipt from the employment and from delivering any sort of

personal services then it may be considered as the subject of tax for the employee or may be

held as fringe benefit tax for the employer. The receipt should be having nexus with the

personal service to constitute ordinary income. The example of “Dean v FCT (1997)” says

that retention payment given to employee for being employed was held as income in nature

(LeFevre, 2016). Similarly, Eric has received $7,800 as gross wages by working as employee

for Blue Merlin. The gross wages is a personal service income. Noting “Dean v FCT

(1997)” is a subject of tax for Eric and it is included for assessment as ordinary income under

“sec 6-5 ITA Act 97”.

Employees generally faces problem in understanding as what constitute allowance or

reimbursement. Allowances are salary and wages and it is simply excluded from being

considered as fringe benefit. It is treated taxable in the employees hand under the statutory

provision of “sec 15-2 ITAA 1997”. On the other hand, reimbursement is not a wages or

salary. The finding of court in Roads and Traffic Authority of “NSW v FCT (1993)” says

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

that a reimbursement is payment given for the actual outgoings that is occurred

(Braunerhjelm & Eklund, 2014).

Eric has got a shift allowance of $2,000. Within the provision of under the statutory

provision of “sec 15-2 ITAA 1997” the amount is treated taxable in the Eric’s hand. Whereas

the reimbursement of $800 is not a taxable salary or wage income for Eric. Noting “NSW v

FCT (1993)” reimbursement is payment given to Eric for the actual outgoings that is

occurred.

Under the “sec 7 (1) FBTAA 1986” when the employee is given a car for their private

usage by employee then it is a car fringe benefit. Similarly, a car is received by Eric during

the year by his employer (Arnold et al., 2019). The car is used for private purpose of Eric and

constitute a non-assessable fringe benefit under “sec 7 (1) FBTAA 1986”. The employer of

Eric is required to pay FBT since the benefit was given to Eric in relation to his direct

employer with the employment.

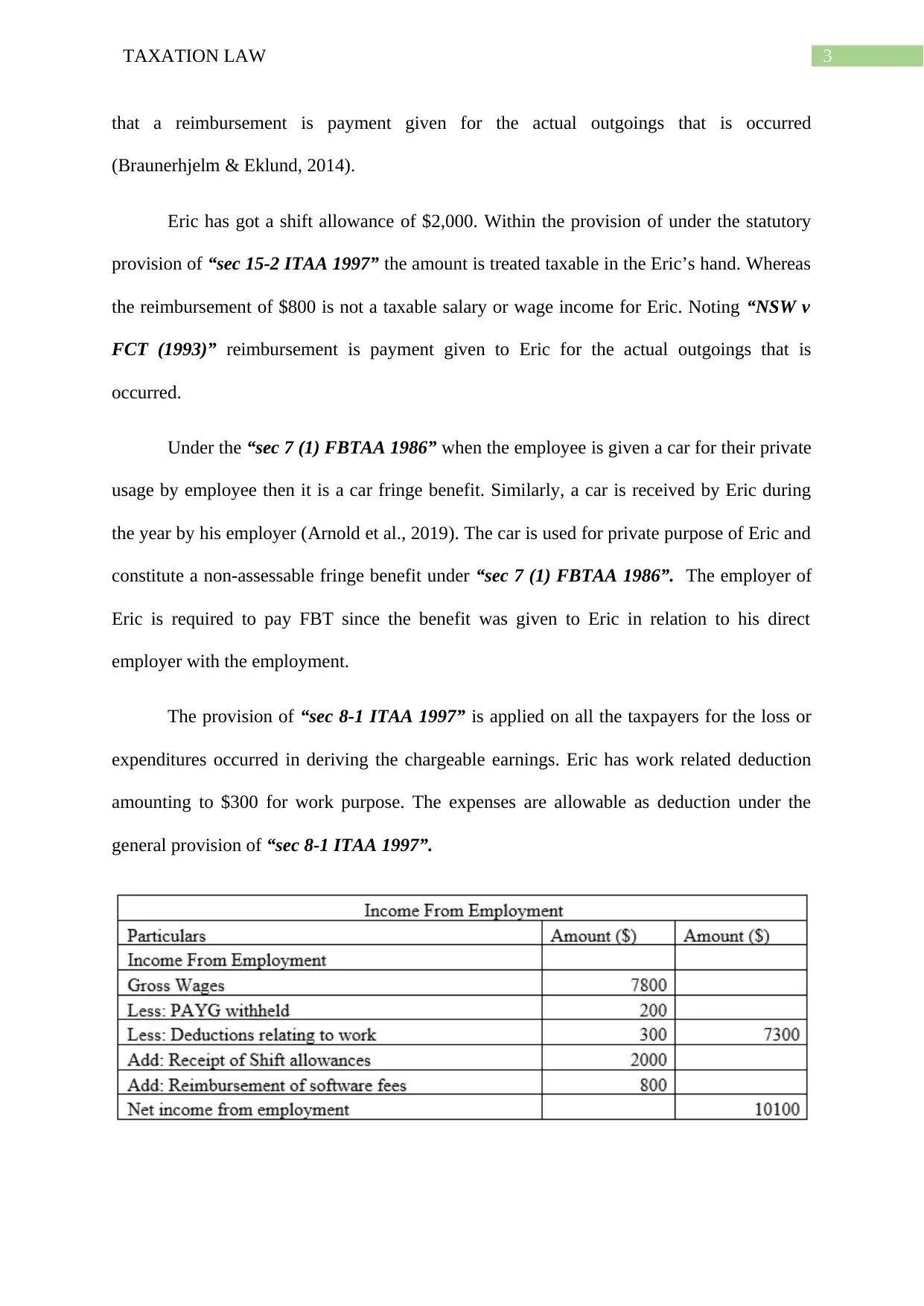

The provision of “sec 8-1 ITAA 1997” is applied on all the taxpayers for the loss or

expenditures occurred in deriving the chargeable earnings. Eric has work related deduction

amounting to $300 for work purpose. The expenses are allowable as deduction under the

general provision of “sec 8-1 ITAA 1997”.

that a reimbursement is payment given for the actual outgoings that is occurred

(Braunerhjelm & Eklund, 2014).

Eric has got a shift allowance of $2,000. Within the provision of under the statutory

provision of “sec 15-2 ITAA 1997” the amount is treated taxable in the Eric’s hand. Whereas

the reimbursement of $800 is not a taxable salary or wage income for Eric. Noting “NSW v

FCT (1993)” reimbursement is payment given to Eric for the actual outgoings that is

occurred.

Under the “sec 7 (1) FBTAA 1986” when the employee is given a car for their private

usage by employee then it is a car fringe benefit. Similarly, a car is received by Eric during

the year by his employer (Arnold et al., 2019). The car is used for private purpose of Eric and

constitute a non-assessable fringe benefit under “sec 7 (1) FBTAA 1986”. The employer of

Eric is required to pay FBT since the benefit was given to Eric in relation to his direct

employer with the employment.

The provision of “sec 8-1 ITAA 1997” is applied on all the taxpayers for the loss or

expenditures occurred in deriving the chargeable earnings. Eric has work related deduction

amounting to $300 for work purpose. The expenses are allowable as deduction under the

general provision of “sec 8-1 ITAA 1997”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Part B: Income from business:

When a taxpayer gets any proceeds from their business activity, it attracts income tax

liability for the income earned from business. The verdict noted in “GP International

Pipecoaters Pty Ltd v FCT (1990)” says that business incomes will be considered as ordinary

incidents of commercial activity and it is taxable within “sec 6-5 ITAA 1997” (Tran-Nam et

al., 2014). Accordingly, the taxpayer are also required to denote that they must account their

income under either cash method or accrual method.

The cash basis of tax accounting involves taking into account those receipts that are

received in cash. The accrual basis of tax accounting method says that all the income earned

which is yet to receive is also taken into the consideration. The federal court explained in

“Firstenberg v FCT (1976)” stated that the cash basis of accounting is the right method

because it is useful in showing the true income of the taxpayer.

The case facts obtained suggest that Eric has got a sum of $85,000 from the accounts

receivable. The judgement of “GP International Pipecoaters Pty Ltd v FCT (1990)” is

mentioned to take into account the receipts as taxable proceeds of business under under “sec

6-5 ITAA 1997” (Murphy, 2019). To account for the receipts, cash basis of tax accounting

method is followed. Referring “Firstenberg v FCT (1976)” the cash basis will help in

providing a right reflection of Eric’s taxable income.

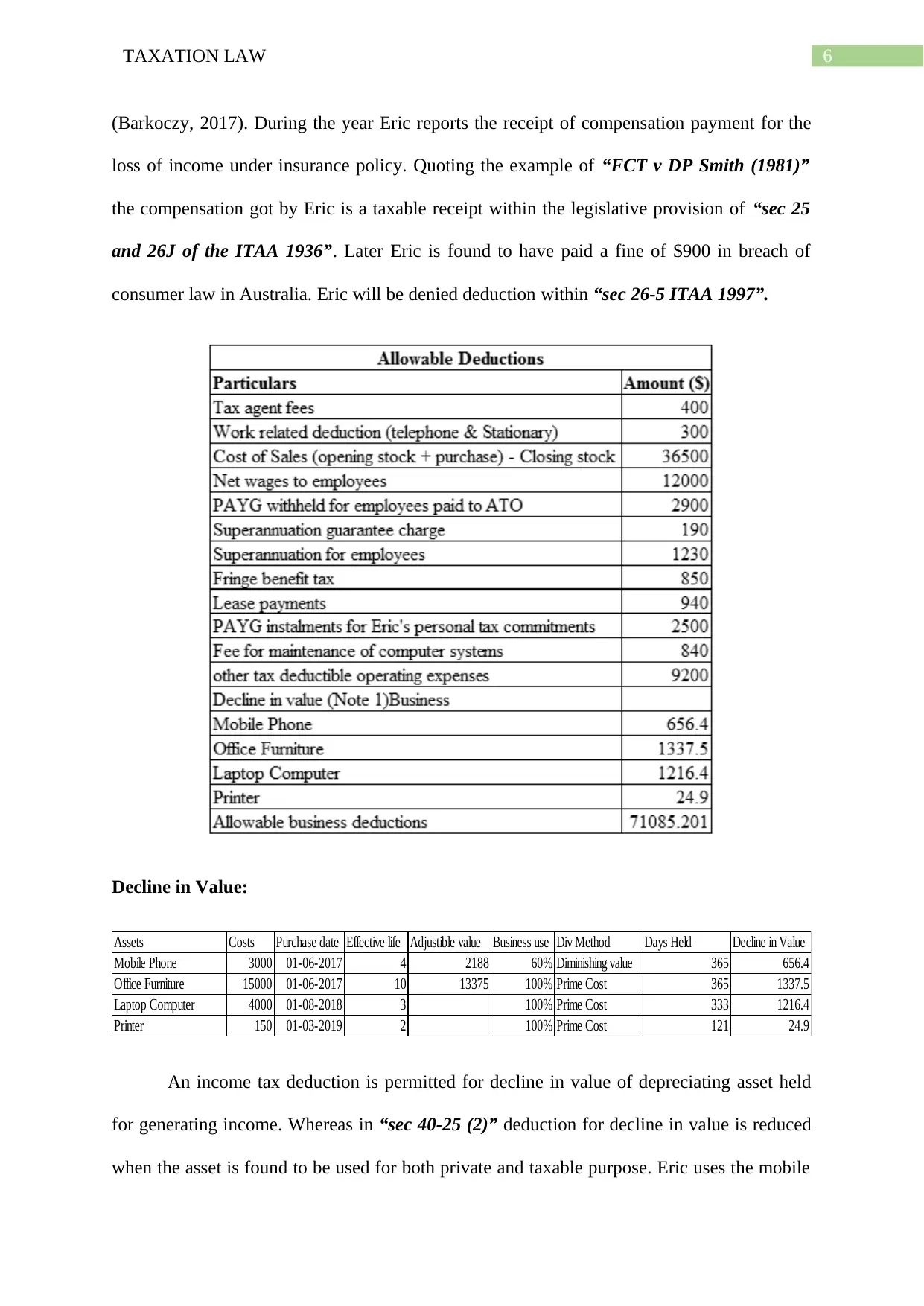

When a taxpayer purchases any trading stock then they are allowed for deduction

under “sec 70-15 ITAA 1997”. The payment which Eric has made for accounts payable will

permitted for deduction to Eric under “sec 70-15 ITAA 1997” (Smith, 2015). Furthermore,

within “sec 70-35 (3) ITAA 1997” a taxpayer is permitted to get deduction when the opening

stock value is greater than closing stock. The case facts of Eric provides that the value of

Part B: Income from business:

When a taxpayer gets any proceeds from their business activity, it attracts income tax

liability for the income earned from business. The verdict noted in “GP International

Pipecoaters Pty Ltd v FCT (1990)” says that business incomes will be considered as ordinary

incidents of commercial activity and it is taxable within “sec 6-5 ITAA 1997” (Tran-Nam et

al., 2014). Accordingly, the taxpayer are also required to denote that they must account their

income under either cash method or accrual method.

The cash basis of tax accounting involves taking into account those receipts that are

received in cash. The accrual basis of tax accounting method says that all the income earned

which is yet to receive is also taken into the consideration. The federal court explained in

“Firstenberg v FCT (1976)” stated that the cash basis of accounting is the right method

because it is useful in showing the true income of the taxpayer.

The case facts obtained suggest that Eric has got a sum of $85,000 from the accounts

receivable. The judgement of “GP International Pipecoaters Pty Ltd v FCT (1990)” is

mentioned to take into account the receipts as taxable proceeds of business under under “sec

6-5 ITAA 1997” (Murphy, 2019). To account for the receipts, cash basis of tax accounting

method is followed. Referring “Firstenberg v FCT (1976)” the cash basis will help in

providing a right reflection of Eric’s taxable income.

When a taxpayer purchases any trading stock then they are allowed for deduction

under “sec 70-15 ITAA 1997”. The payment which Eric has made for accounts payable will

permitted for deduction to Eric under “sec 70-15 ITAA 1997” (Smith, 2015). Furthermore,

within “sec 70-35 (3) ITAA 1997” a taxpayer is permitted to get deduction when the opening

stock value is greater than closing stock. The case facts of Eric provides that the value of

5TAXATION LAW

opening stock is in excess of the closing stock. As a result an income tax deduction for the

excess value is allowed as deduction within “sec 70-35 (3) ITAA 1997”.

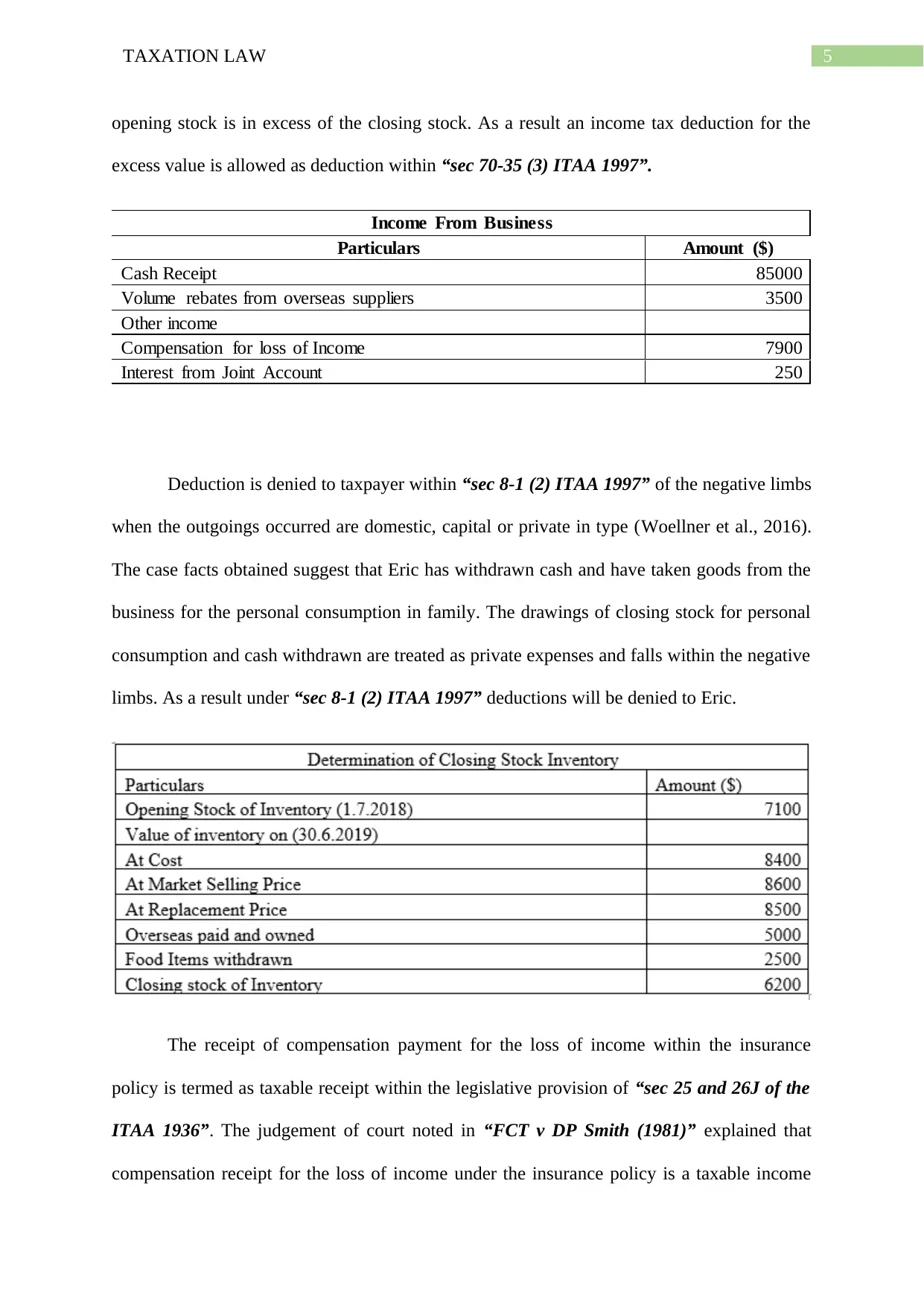

Income From Business

Particulars Amount ($)

Cash Receipt 85000

Volume rebates from overseas suppliers 3500

Other income

Compensation for loss of Income 7900

Interest from Joint Account 250

Deduction is denied to taxpayer within “sec 8-1 (2) ITAA 1997” of the negative limbs

when the outgoings occurred are domestic, capital or private in type (Woellner et al., 2016).

The case facts obtained suggest that Eric has withdrawn cash and have taken goods from the

business for the personal consumption in family. The drawings of closing stock for personal

consumption and cash withdrawn are treated as private expenses and falls within the negative

limbs. As a result under “sec 8-1 (2) ITAA 1997” deductions will be denied to Eric.

The receipt of compensation payment for the loss of income within the insurance

policy is termed as taxable receipt within the legislative provision of “sec 25 and 26J of the

ITAA 1936”. The judgement of court noted in “FCT v DP Smith (1981)” explained that

compensation receipt for the loss of income under the insurance policy is a taxable income

opening stock is in excess of the closing stock. As a result an income tax deduction for the

excess value is allowed as deduction within “sec 70-35 (3) ITAA 1997”.

Income From Business

Particulars Amount ($)

Cash Receipt 85000

Volume rebates from overseas suppliers 3500

Other income

Compensation for loss of Income 7900

Interest from Joint Account 250

Deduction is denied to taxpayer within “sec 8-1 (2) ITAA 1997” of the negative limbs

when the outgoings occurred are domestic, capital or private in type (Woellner et al., 2016).

The case facts obtained suggest that Eric has withdrawn cash and have taken goods from the

business for the personal consumption in family. The drawings of closing stock for personal

consumption and cash withdrawn are treated as private expenses and falls within the negative

limbs. As a result under “sec 8-1 (2) ITAA 1997” deductions will be denied to Eric.

The receipt of compensation payment for the loss of income within the insurance

policy is termed as taxable receipt within the legislative provision of “sec 25 and 26J of the

ITAA 1936”. The judgement of court noted in “FCT v DP Smith (1981)” explained that

compensation receipt for the loss of income under the insurance policy is a taxable income

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

(Barkoczy, 2017). During the year Eric reports the receipt of compensation payment for the

loss of income under insurance policy. Quoting the example of “FCT v DP Smith (1981)”

the compensation got by Eric is a taxable receipt within the legislative provision of “sec 25

and 26J of the ITAA 1936”. Later Eric is found to have paid a fine of $900 in breach of

consumer law in Australia. Eric will be denied deduction within “sec 26-5 ITAA 1997”.

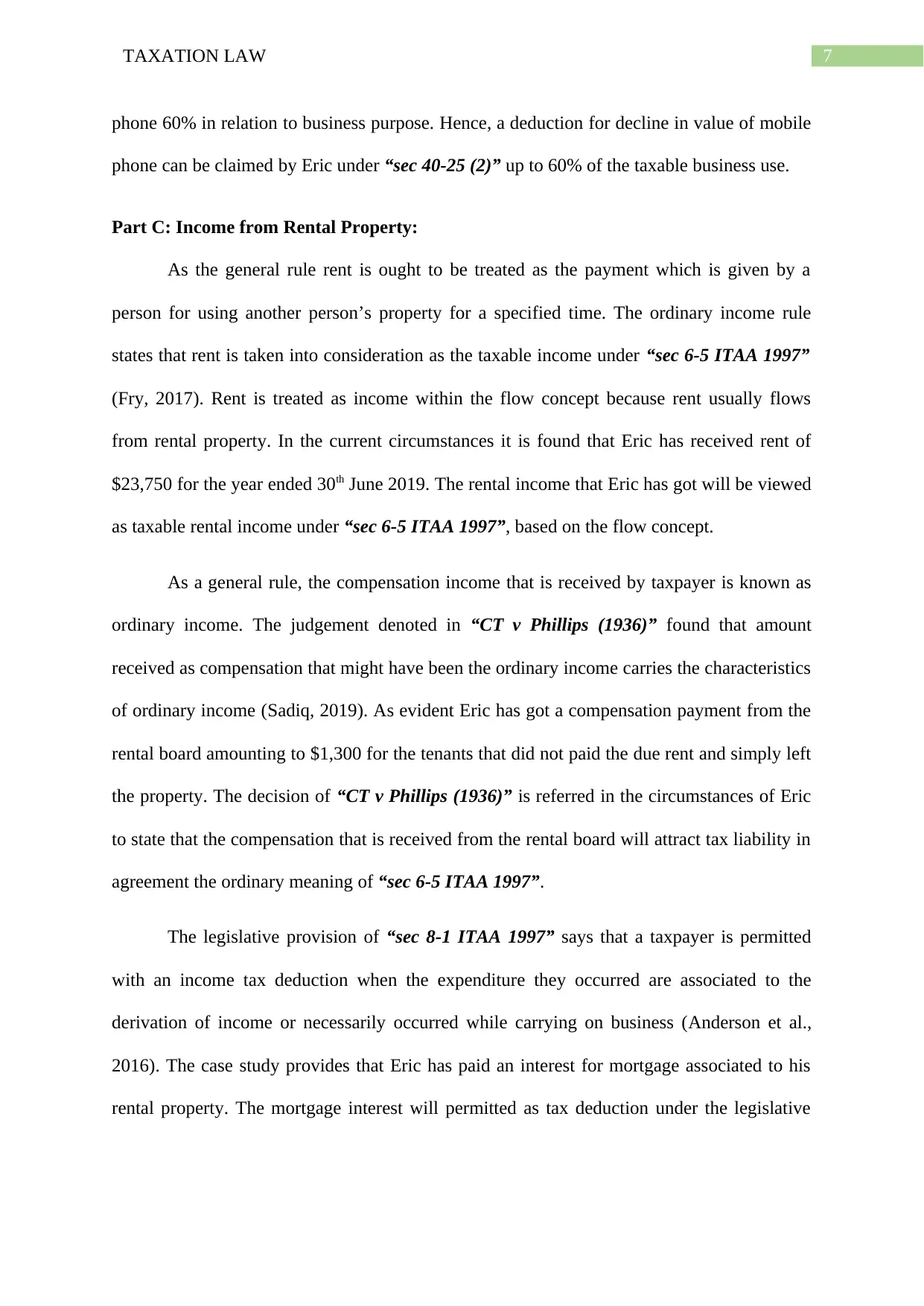

Decline in Value:

Assets Costs Purchase date Effective life Adjustible value Business use Div Method Days Held Decline in Value

Mobile Phone 3000 01-06-2017 4 2188 60% Diminishing value 365 656.4

Office Furniture 15000 01-06-2017 10 13375 100% Prime Cost 365 1337.5

Laptop Computer 4000 01-08-2018 3 100% Prime Cost 333 1216.4

Printer 150 01-03-2019 2 100% Prime Cost 121 24.9

An income tax deduction is permitted for decline in value of depreciating asset held

for generating income. Whereas in “sec 40-25 (2)” deduction for decline in value is reduced

when the asset is found to be used for both private and taxable purpose. Eric uses the mobile

(Barkoczy, 2017). During the year Eric reports the receipt of compensation payment for the

loss of income under insurance policy. Quoting the example of “FCT v DP Smith (1981)”

the compensation got by Eric is a taxable receipt within the legislative provision of “sec 25

and 26J of the ITAA 1936”. Later Eric is found to have paid a fine of $900 in breach of

consumer law in Australia. Eric will be denied deduction within “sec 26-5 ITAA 1997”.

Decline in Value:

Assets Costs Purchase date Effective life Adjustible value Business use Div Method Days Held Decline in Value

Mobile Phone 3000 01-06-2017 4 2188 60% Diminishing value 365 656.4

Office Furniture 15000 01-06-2017 10 13375 100% Prime Cost 365 1337.5

Laptop Computer 4000 01-08-2018 3 100% Prime Cost 333 1216.4

Printer 150 01-03-2019 2 100% Prime Cost 121 24.9

An income tax deduction is permitted for decline in value of depreciating asset held

for generating income. Whereas in “sec 40-25 (2)” deduction for decline in value is reduced

when the asset is found to be used for both private and taxable purpose. Eric uses the mobile

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

phone 60% in relation to business purpose. Hence, a deduction for decline in value of mobile

phone can be claimed by Eric under “sec 40-25 (2)” up to 60% of the taxable business use.

Part C: Income from Rental Property:

As the general rule rent is ought to be treated as the payment which is given by a

person for using another person’s property for a specified time. The ordinary income rule

states that rent is taken into consideration as the taxable income under “sec 6-5 ITAA 1997”

(Fry, 2017). Rent is treated as income within the flow concept because rent usually flows

from rental property. In the current circumstances it is found that Eric has received rent of

$23,750 for the year ended 30th June 2019. The rental income that Eric has got will be viewed

as taxable rental income under “sec 6-5 ITAA 1997”, based on the flow concept.

As a general rule, the compensation income that is received by taxpayer is known as

ordinary income. The judgement denoted in “CT v Phillips (1936)” found that amount

received as compensation that might have been the ordinary income carries the characteristics

of ordinary income (Sadiq, 2019). As evident Eric has got a compensation payment from the

rental board amounting to $1,300 for the tenants that did not paid the due rent and simply left

the property. The decision of “CT v Phillips (1936)” is referred in the circumstances of Eric

to state that the compensation that is received from the rental board will attract tax liability in

agreement the ordinary meaning of “sec 6-5 ITAA 1997”.

The legislative provision of “sec 8-1 ITAA 1997” says that a taxpayer is permitted

with an income tax deduction when the expenditure they occurred are associated to the

derivation of income or necessarily occurred while carrying on business (Anderson et al.,

2016). The case study provides that Eric has paid an interest for mortgage associated to his

rental property. The mortgage interest will permitted as tax deduction under the legislative

phone 60% in relation to business purpose. Hence, a deduction for decline in value of mobile

phone can be claimed by Eric under “sec 40-25 (2)” up to 60% of the taxable business use.

Part C: Income from Rental Property:

As the general rule rent is ought to be treated as the payment which is given by a

person for using another person’s property for a specified time. The ordinary income rule

states that rent is taken into consideration as the taxable income under “sec 6-5 ITAA 1997”

(Fry, 2017). Rent is treated as income within the flow concept because rent usually flows

from rental property. In the current circumstances it is found that Eric has received rent of

$23,750 for the year ended 30th June 2019. The rental income that Eric has got will be viewed

as taxable rental income under “sec 6-5 ITAA 1997”, based on the flow concept.

As a general rule, the compensation income that is received by taxpayer is known as

ordinary income. The judgement denoted in “CT v Phillips (1936)” found that amount

received as compensation that might have been the ordinary income carries the characteristics

of ordinary income (Sadiq, 2019). As evident Eric has got a compensation payment from the

rental board amounting to $1,300 for the tenants that did not paid the due rent and simply left

the property. The decision of “CT v Phillips (1936)” is referred in the circumstances of Eric

to state that the compensation that is received from the rental board will attract tax liability in

agreement the ordinary meaning of “sec 6-5 ITAA 1997”.

The legislative provision of “sec 8-1 ITAA 1997” says that a taxpayer is permitted

with an income tax deduction when the expenditure they occurred are associated to the

derivation of income or necessarily occurred while carrying on business (Anderson et al.,

2016). The case study provides that Eric has paid an interest for mortgage associated to his

rental property. The mortgage interest will permitted as tax deduction under the legislative

8TAXATION LAW

provision of “sec 8-1 ITAA 1997” because expenditure they occurred by Eric in the

derivation of rental income.

Further information furnished by Eric provides that he has incurred expenses on

painting the walls of the property. The explanation given in “sec 25-10 (3) ITAA 1997”

suggest that no deduction is allowed for repairs that amounts to capital in nature. A repair

may be held as capital in nature when the repair involves initial repair of an asset. The verdict

announced by the federal court in “Law Shipping Co Ltd v Inland Revenue Commissioners

(1923)” explained that where an outgoing has incurred in initial repair of ship following the

purchase will not be allowed as deduction because such repairs are treated as initial repair

(Barkoczy, 2016). Corresponding to the example cited above the paintings carried out by Eric

on the outside wall of house is an initial repair. The expenses are classified as capital in

nature and non-deductible under “sec 25-10 (3) ITAA 1997”.

Travel expense occurred on the rental property are permitted as tax deduction. The

travel expense include the outgoings that have happened in inspecting the property (Schenk,

2017). Eric reports a travel expense amounting to $830 for inspecting the rental property and

meeting with the agents. The expenditure is an allowable tax deduction within “sec 8-1 ITAA

1997”.

Borrowing fees of greater than $100 are deductible over several years. The borrowing

fees can be allowed for deduction for a period of five years or up to the loan period. Eric

during the year incurs a borrowing expenditure of $825 which he incurred while buying the

investment house. As the borrowing expenditure is greater than $100, Eric is recommended

to deduct the expenditure over the term of loan.

The description of “sec 40-25 (1) ITAA 1997” makes the taxpayer aware that they are

permitted to obtain an income tax deduction for the decline in value of a depreciating asset in

provision of “sec 8-1 ITAA 1997” because expenditure they occurred by Eric in the

derivation of rental income.

Further information furnished by Eric provides that he has incurred expenses on

painting the walls of the property. The explanation given in “sec 25-10 (3) ITAA 1997”

suggest that no deduction is allowed for repairs that amounts to capital in nature. A repair

may be held as capital in nature when the repair involves initial repair of an asset. The verdict

announced by the federal court in “Law Shipping Co Ltd v Inland Revenue Commissioners

(1923)” explained that where an outgoing has incurred in initial repair of ship following the

purchase will not be allowed as deduction because such repairs are treated as initial repair

(Barkoczy, 2016). Corresponding to the example cited above the paintings carried out by Eric

on the outside wall of house is an initial repair. The expenses are classified as capital in

nature and non-deductible under “sec 25-10 (3) ITAA 1997”.

Travel expense occurred on the rental property are permitted as tax deduction. The

travel expense include the outgoings that have happened in inspecting the property (Schenk,

2017). Eric reports a travel expense amounting to $830 for inspecting the rental property and

meeting with the agents. The expenditure is an allowable tax deduction within “sec 8-1 ITAA

1997”.

Borrowing fees of greater than $100 are deductible over several years. The borrowing

fees can be allowed for deduction for a period of five years or up to the loan period. Eric

during the year incurs a borrowing expenditure of $825 which he incurred while buying the

investment house. As the borrowing expenditure is greater than $100, Eric is recommended

to deduct the expenditure over the term of loan.

The description of “sec 40-25 (1) ITAA 1997” makes the taxpayer aware that they are

permitted to obtain an income tax deduction for the decline in value of a depreciating asset in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

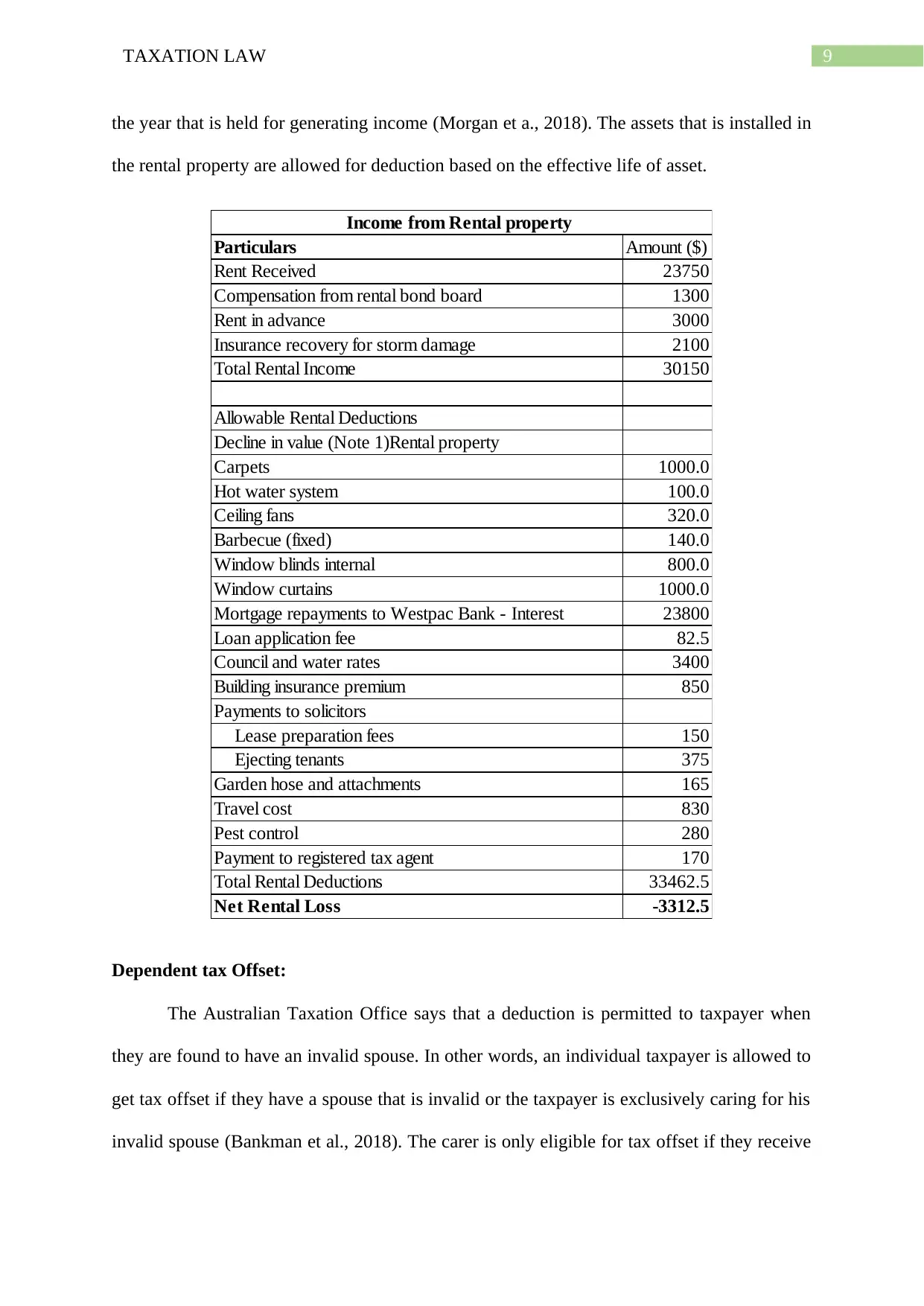

the year that is held for generating income (Morgan et a., 2018). The assets that is installed in

the rental property are allowed for deduction based on the effective life of asset.

Particulars Amount ($)

Rent Received 23750

Compensation from rental bond board 1300

Rent in advance 3000

Insurance recovery for storm damage 2100

Total Rental Income 30150

Allowable Rental Deductions

Decline in value (Note 1)Rental property

Carpets 1000.0

Hot water system 100.0

Ceiling fans 320.0

Barbecue (fixed) 140.0

Window blinds internal 800.0

Window curtains 1000.0

Mortgage repayments to Westpac Bank - Interest 23800

Loan application fee 82.5

Council and water rates 3400

Building insurance premium 850

Payments to solicitors

Lease preparation fees 150

Ejecting tenants 375

Garden hose and attachments 165

Travel cost 830

Pest control 280

Payment to registered tax agent 170

Total Rental Deductions 33462.5

Net Rental Loss -3312.5

Income from Rental property

Dependent tax Offset:

The Australian Taxation Office says that a deduction is permitted to taxpayer when

they are found to have an invalid spouse. In other words, an individual taxpayer is allowed to

get tax offset if they have a spouse that is invalid or the taxpayer is exclusively caring for his

invalid spouse (Bankman et al., 2018). The carer is only eligible for tax offset if they receive

the year that is held for generating income (Morgan et a., 2018). The assets that is installed in

the rental property are allowed for deduction based on the effective life of asset.

Particulars Amount ($)

Rent Received 23750

Compensation from rental bond board 1300

Rent in advance 3000

Insurance recovery for storm damage 2100

Total Rental Income 30150

Allowable Rental Deductions

Decline in value (Note 1)Rental property

Carpets 1000.0

Hot water system 100.0

Ceiling fans 320.0

Barbecue (fixed) 140.0

Window blinds internal 800.0

Window curtains 1000.0

Mortgage repayments to Westpac Bank - Interest 23800

Loan application fee 82.5

Council and water rates 3400

Building insurance premium 850

Payments to solicitors

Lease preparation fees 150

Ejecting tenants 375

Garden hose and attachments 165

Travel cost 830

Pest control 280

Payment to registered tax agent 170

Total Rental Deductions 33462.5

Net Rental Loss -3312.5

Income from Rental property

Dependent tax Offset:

The Australian Taxation Office says that a deduction is permitted to taxpayer when

they are found to have an invalid spouse. In other words, an individual taxpayer is allowed to

get tax offset if they have a spouse that is invalid or the taxpayer is exclusively caring for his

invalid spouse (Bankman et al., 2018). The carer is only eligible for tax offset if they receive

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

the carer payment or carer allowance within the “Social Security Act 1991” for the care they

give to that person or they are completely engaged in providing care to an individual that

receives disability support pension with “Social Security Act 1991”.

The case facts that is obtained from Eric furnishes that he has a spouse named Linda

that has lost her eye sight in a car accident. Eric exclusively takes care of Linda and she gets a

disability pension of $9,200 from the centre link during the year 2019. It can be stated that

Eric is eligible for obtaining a invalid and invalid carer tax offset because Eric spouse is an

invalid and receives a disability support pension under the “Social Security Act 1991”.

the carer payment or carer allowance within the “Social Security Act 1991” for the care they

give to that person or they are completely engaged in providing care to an individual that

receives disability support pension with “Social Security Act 1991”.

The case facts that is obtained from Eric furnishes that he has a spouse named Linda

that has lost her eye sight in a car accident. Eric exclusively takes care of Linda and she gets a

disability pension of $9,200 from the centre link during the year 2019. It can be stated that

Eric is eligible for obtaining a invalid and invalid carer tax offset because Eric spouse is an

invalid and receives a disability support pension under the “Social Security Act 1991”.

11TAXATION LAW

References:

Anderson, C., Dickfos, J., & Brown, C. (2016). The Australian Taxation Office–what role

does it play in anti-phoenix activity?. Insolvency Law Journal, 24(2), 127-140.

Arnold, B. J., Ault, H. J., & Cooper, G. (Eds.). (2019). Comparative income taxation: a

structural analysis. Kluwer Law International BV.

Bankman, J., Shaviro, D. N., Stark, K. J., & Kleinbard, E. D. (2018). Federal Income

Taxation. Aspen Publishers.

Barkoczy, S. (2016). Foundations of Taxation Law 2016. OUP Catalogue.

Barkoczy, S. (2017). Core tax legislation and study guide. OUP Catalogue.

Braunerhjelm, P., & Eklund, J. E. (2014). Taxes, tax administrative burdens and new firm

formation. Kyklos, 67(1), 1-11.

Burman, L. E., Gale, W. G., Gault, S., Kim, B., Nunns, J., & Rosenthal, S. (2016). Financial

transaction taxes in theory and practice. National Tax Journal, 69(1), 171-216.

Fry, M. (2017). Australian taxation of offshore hubs: an examination of the law on the ability

of Australia to tax economic activity in offshore hubs and the position of the

Australian Taxation Office. The APPEA Journal, 57(1), 49-63.

LeFevre, T. A. (2016). Justice in Taxation. Vt. L. Rev., 41, 763.

Morgan, A., Mortimer, C., & Pinto, D. (2018). A practical introduction to Australian

taxation law 2018. Oxford University Press.

Murphy, K. (2019). Procedural justice and the Australian Taxation Office: A study of scheme

investors. Centre for Tax System Integrity (CTSI), Research School of Social

Sciences, The Australian National University.

References:

Anderson, C., Dickfos, J., & Brown, C. (2016). The Australian Taxation Office–what role

does it play in anti-phoenix activity?. Insolvency Law Journal, 24(2), 127-140.

Arnold, B. J., Ault, H. J., & Cooper, G. (Eds.). (2019). Comparative income taxation: a

structural analysis. Kluwer Law International BV.

Bankman, J., Shaviro, D. N., Stark, K. J., & Kleinbard, E. D. (2018). Federal Income

Taxation. Aspen Publishers.

Barkoczy, S. (2016). Foundations of Taxation Law 2016. OUP Catalogue.

Barkoczy, S. (2017). Core tax legislation and study guide. OUP Catalogue.

Braunerhjelm, P., & Eklund, J. E. (2014). Taxes, tax administrative burdens and new firm

formation. Kyklos, 67(1), 1-11.

Burman, L. E., Gale, W. G., Gault, S., Kim, B., Nunns, J., & Rosenthal, S. (2016). Financial

transaction taxes in theory and practice. National Tax Journal, 69(1), 171-216.

Fry, M. (2017). Australian taxation of offshore hubs: an examination of the law on the ability

of Australia to tax economic activity in offshore hubs and the position of the

Australian Taxation Office. The APPEA Journal, 57(1), 49-63.

LeFevre, T. A. (2016). Justice in Taxation. Vt. L. Rev., 41, 763.

Morgan, A., Mortimer, C., & Pinto, D. (2018). A practical introduction to Australian

taxation law 2018. Oxford University Press.

Murphy, K. (2019). Procedural justice and the Australian Taxation Office: A study of scheme

investors. Centre for Tax System Integrity (CTSI), Research School of Social

Sciences, The Australian National University.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.