HI6028 Taxation: Capital Gains and Fringe Benefits

VerifiedAdded on 2020/04/07

|8

|2059

|73

Homework Assignment

AI Summary

This assignment solution analyzes various taxation aspects, including capital gains tax on collectibles, personal use assets, and share sales. It also delves into fringe benefits tax, specifically loan fringe benefits, and calculates the taxable value in different scenarios. Furthermore, the solution examines partnership arrangements, determining loss allocation based on the existence of a partnership. Finally, it discusses the principle of tax avoidance, as highlighted in the IRC v Duke of Westminster case, and its relevance in Australia, along with the treatment of proceeds from pine tree removal as royalty income under ITAA 1936.

Taxation Theory, Practice and the Law

HI6028

STUDENT ID

[Pick the date]

HI6028

STUDENT ID

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation

Question 1

Issue

Eric has made a host of transactions in the given financial year and the objective is to highlight

the capital gains impact of the same.

Rule

Considering the differing rules to compute capital gains, the relevant discussion in this matter is

indicated as follows.

Collectibles

Defined by s. 108-10(2) and consists of antique items besides painting, rare books etc.

Capital losses if any on these articles cannot offset gains made in other asset classes but

have to be adjusted only against capital gains on collectibles sale only (s. 108-1)

(Barkoczy, 2017).

Capital gain recognition would be enabled only the underlying article has been bought for

a price which surpasses $ 500 (Deutsch et. al., 2016).

Can be rolled over perpetually till the time the capital gains from collectibles are realised

for adjustment (Sadiq et. al., 2017).

Items of Personal Use

Capital losses are never realised and instead ignored and non-existent for CGT

computation (s. 108-10(3)) (Gilders et. al., 2016).

Realisation of capital gains is accomplished only if the underlying asset has been bought

for a price that surpasses $10,000 (CCH, 2013).

Disposal of Shares

Capital gains or losses on share sale as per s. 104-5 would lead to taxable capital gains.

Respite available to individual taxpayers whereby as per s. 115-25, long term capital

gains can be discounted and thus only the remaining half would attract CGT (Woellner,

2014).

Application

The various transactions enacted by Eric need to be analysed in the light of the rules outlined

above.

Collectible

1

Question 1

Issue

Eric has made a host of transactions in the given financial year and the objective is to highlight

the capital gains impact of the same.

Rule

Considering the differing rules to compute capital gains, the relevant discussion in this matter is

indicated as follows.

Collectibles

Defined by s. 108-10(2) and consists of antique items besides painting, rare books etc.

Capital losses if any on these articles cannot offset gains made in other asset classes but

have to be adjusted only against capital gains on collectibles sale only (s. 108-1)

(Barkoczy, 2017).

Capital gain recognition would be enabled only the underlying article has been bought for

a price which surpasses $ 500 (Deutsch et. al., 2016).

Can be rolled over perpetually till the time the capital gains from collectibles are realised

for adjustment (Sadiq et. al., 2017).

Items of Personal Use

Capital losses are never realised and instead ignored and non-existent for CGT

computation (s. 108-10(3)) (Gilders et. al., 2016).

Realisation of capital gains is accomplished only if the underlying asset has been bought

for a price that surpasses $10,000 (CCH, 2013).

Disposal of Shares

Capital gains or losses on share sale as per s. 104-5 would lead to taxable capital gains.

Respite available to individual taxpayers whereby as per s. 115-25, long term capital

gains can be discounted and thus only the remaining half would attract CGT (Woellner,

2014).

Application

The various transactions enacted by Eric need to be analysed in the light of the rules outlined

above.

Collectible

1

Taxation

Antiques (Chair & Vase) and painting to be recognised as collectible items for CGT

purposes.

The price at which each of these items have been procured is greater than $ 500 and

hence these items are not exempt from CGT implications.

Antique chair sale (Capital gains realised) = 1000-3000 = -$ 2,000

Antique vase sale (Capital gains realised) = 3000-2000 = $ 1,000

Painting sale (Capital gains realised) =1000-9000 = -$8,000

Net capital gains from collectible sale = -2000+ 1000 -8000 = -$ 9,000

The above losses would be carried forwarded by Eric in the future years so that it can be sued to

neutralise any future collectible capital gains.

Personal Use Assets

The buying cost of the sound system which is for personal use is over $ 10,000 and

therefore the CGT implications would arise in case of any gains made.

Sound System sale (Capital gains realised) = 11,000- 12,000 = -$ 1,000

The capital losses do not contribute to the capital gains computation and hence this is ignored.

Shares

Buying price of shares is given as $ 5,000 while the corresponding sale price is $ 20,000.

Also, it is noticeable that holding period is less than 12 months.

Share sale (Capital gains realised) = 20,000 – 5,000 = $ 15,000

Conclusion

Eric would need to pay capital gains tax on capital gains of $ 15,000 for the given year.

Question 2

Issue

Certain fringe benefits in the form of cheap loan have been extended to Brian by his employer in

wake of which the taxable value needs to be computed.

Rule

2

Antiques (Chair & Vase) and painting to be recognised as collectible items for CGT

purposes.

The price at which each of these items have been procured is greater than $ 500 and

hence these items are not exempt from CGT implications.

Antique chair sale (Capital gains realised) = 1000-3000 = -$ 2,000

Antique vase sale (Capital gains realised) = 3000-2000 = $ 1,000

Painting sale (Capital gains realised) =1000-9000 = -$8,000

Net capital gains from collectible sale = -2000+ 1000 -8000 = -$ 9,000

The above losses would be carried forwarded by Eric in the future years so that it can be sued to

neutralise any future collectible capital gains.

Personal Use Assets

The buying cost of the sound system which is for personal use is over $ 10,000 and

therefore the CGT implications would arise in case of any gains made.

Sound System sale (Capital gains realised) = 11,000- 12,000 = -$ 1,000

The capital losses do not contribute to the capital gains computation and hence this is ignored.

Shares

Buying price of shares is given as $ 5,000 while the corresponding sale price is $ 20,000.

Also, it is noticeable that holding period is less than 12 months.

Share sale (Capital gains realised) = 20,000 – 5,000 = $ 15,000

Conclusion

Eric would need to pay capital gains tax on capital gains of $ 15,000 for the given year.

Question 2

Issue

Certain fringe benefits in the form of cheap loan have been extended to Brian by his employer in

wake of which the taxable value needs to be computed.

Rule

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation

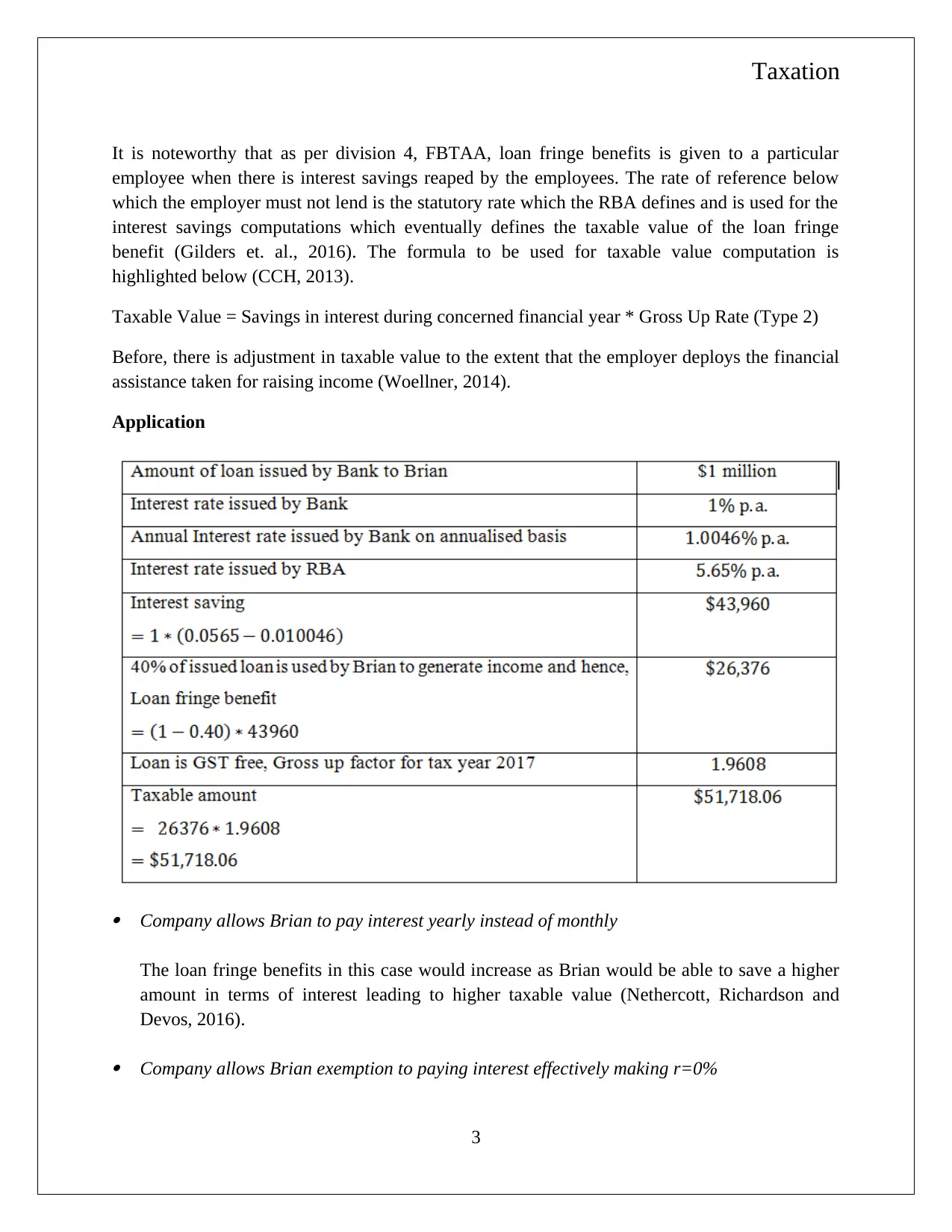

It is noteworthy that as per division 4, FBTAA, loan fringe benefits is given to a particular

employee when there is interest savings reaped by the employees. The rate of reference below

which the employer must not lend is the statutory rate which the RBA defines and is used for the

interest savings computations which eventually defines the taxable value of the loan fringe

benefit (Gilders et. al., 2016). The formula to be used for taxable value computation is

highlighted below (CCH, 2013).

Taxable Value = Savings in interest during concerned financial year * Gross Up Rate (Type 2)

Before, there is adjustment in taxable value to the extent that the employer deploys the financial

assistance taken for raising income (Woellner, 2014).

Application

Company allows Brian to pay interest yearly instead of monthly

The loan fringe benefits in this case would increase as Brian would be able to save a higher

amount in terms of interest leading to higher taxable value (Nethercott, Richardson and

Devos, 2016).

Company allows Brian exemption to paying interest effectively making r=0%

3

It is noteworthy that as per division 4, FBTAA, loan fringe benefits is given to a particular

employee when there is interest savings reaped by the employees. The rate of reference below

which the employer must not lend is the statutory rate which the RBA defines and is used for the

interest savings computations which eventually defines the taxable value of the loan fringe

benefit (Gilders et. al., 2016). The formula to be used for taxable value computation is

highlighted below (CCH, 2013).

Taxable Value = Savings in interest during concerned financial year * Gross Up Rate (Type 2)

Before, there is adjustment in taxable value to the extent that the employer deploys the financial

assistance taken for raising income (Woellner, 2014).

Application

Company allows Brian to pay interest yearly instead of monthly

The loan fringe benefits in this case would increase as Brian would be able to save a higher

amount in terms of interest leading to higher taxable value (Nethercott, Richardson and

Devos, 2016).

Company allows Brian exemption to paying interest effectively making r=0%

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation

The loan fringe benefits in this case would increase as Brian would be able to save a higher

amount in terms of interest leading to higher taxable value. Infact the loan fringe benefit

would assume the maximum possible value in this case as no interest cost levied (Sadiq et.

al., 2016).

Conclusion

On the basis of the current situation, the loan fringe benefit will have a net taxable value of

$51,718.06.

Question 3

Issue

The central issue is to highlight the arrangement for loss allocation and Jack and his wife Jill.

Relevant law

The key concern is to determine if the given transaction gives rise to a partnership relation or not.

This requires the fulfilment of three pivotal conditions (Woellner, 2014).

1) “Carrying on of the business activity”

2) Carrying on “in common”

3) Profit motive should be present for the activities.

Few critical points which are relevant are outlined below (Nethercott, Richardson and Devos,

2016).

It would be unfair to compare carrying on with repetition and isolated transactions driven

by circumstances can be partnership (Playfair Development Corporation Pty Ltd v Ryan

(1969) 90 WN (NSW))

In common not only implies collective rights and obligations but same extends to profit

and loss sharing. Hence, no partner can limit exposure to loss unless the underlying

partner is limited (Re Ruddock (1879) 5 VLR (IP & M) 51).

Application

The first objective is to ascertain whether there is existence of partnership relationship in the

given case. The key facets in this regards are indicated below.

Business owing to buying and selling of property

In common as the property purchase has been done jointly.

4

The loan fringe benefits in this case would increase as Brian would be able to save a higher

amount in terms of interest leading to higher taxable value. Infact the loan fringe benefit

would assume the maximum possible value in this case as no interest cost levied (Sadiq et.

al., 2016).

Conclusion

On the basis of the current situation, the loan fringe benefit will have a net taxable value of

$51,718.06.

Question 3

Issue

The central issue is to highlight the arrangement for loss allocation and Jack and his wife Jill.

Relevant law

The key concern is to determine if the given transaction gives rise to a partnership relation or not.

This requires the fulfilment of three pivotal conditions (Woellner, 2014).

1) “Carrying on of the business activity”

2) Carrying on “in common”

3) Profit motive should be present for the activities.

Few critical points which are relevant are outlined below (Nethercott, Richardson and Devos,

2016).

It would be unfair to compare carrying on with repetition and isolated transactions driven

by circumstances can be partnership (Playfair Development Corporation Pty Ltd v Ryan

(1969) 90 WN (NSW))

In common not only implies collective rights and obligations but same extends to profit

and loss sharing. Hence, no partner can limit exposure to loss unless the underlying

partner is limited (Re Ruddock (1879) 5 VLR (IP & M) 51).

Application

The first objective is to ascertain whether there is existence of partnership relationship in the

given case. The key facets in this regards are indicated below.

Business owing to buying and selling of property

In common as the property purchase has been done jointly.

4

Taxation

Further, purchase of property has been done so as to make gains by selling the same.

From the above, existence of partnership is concerned. Hence, if loss arises on account of

business, then irrespective of the agreement, the partners (Jack & Jill) will have to divide losses

in the ratio 10(Jack) : 90(Jill). Also, in case of capital losses, the relevant losses would be

available to the individual partners who can then offset the same against any capital gains or can

roll these over.

Conclusion

The loss division would be in the same ratio as profit as partnership exists and the executed

agreement does not matter.

Question 4

Issue

The principle which the IRC v Duke of Westminster case highlighted needs to be listed down and

the relevance of the same in Australia needs to be outlined.

Relevant law and Application

The key principle that this landmark case brought into light was in relation to tax avoidance. This

case entitled every taxpayer with the legally approved right of minimising the liability associated

with tax outflow (Barkoczy, 2017). The net result was that there was no provision related to anti-

avoidance that was inserted in the ITAA 1936 and relevant changes were prompted only after

four decades when the income levels grew and also the misuse also increased. The various steps

in Australian context are outlined as follows (CCH, 2013).

The judicial system through the court endorsed the choice principle as per which the

taxpayer are not supposed to get creative in their tax arrangements and rather utilise the

concessions provided in the statute in the manner prescribed to lower tax liability.

Anti –avoidance provisions were incorporated in ITAA 1936 (Part IVA) in 1981

Before 2006, the clauses only targeted taxpayers but not the promoters offering such

schemes to them. However, this was rectified with promoter penalty provisions with

wider powers available to Tax Commissioner (Gilders et. al., 2016).

Conclusion

5

Further, purchase of property has been done so as to make gains by selling the same.

From the above, existence of partnership is concerned. Hence, if loss arises on account of

business, then irrespective of the agreement, the partners (Jack & Jill) will have to divide losses

in the ratio 10(Jack) : 90(Jill). Also, in case of capital losses, the relevant losses would be

available to the individual partners who can then offset the same against any capital gains or can

roll these over.

Conclusion

The loss division would be in the same ratio as profit as partnership exists and the executed

agreement does not matter.

Question 4

Issue

The principle which the IRC v Duke of Westminster case highlighted needs to be listed down and

the relevance of the same in Australia needs to be outlined.

Relevant law and Application

The key principle that this landmark case brought into light was in relation to tax avoidance. This

case entitled every taxpayer with the legally approved right of minimising the liability associated

with tax outflow (Barkoczy, 2017). The net result was that there was no provision related to anti-

avoidance that was inserted in the ITAA 1936 and relevant changes were prompted only after

four decades when the income levels grew and also the misuse also increased. The various steps

in Australian context are outlined as follows (CCH, 2013).

The judicial system through the court endorsed the choice principle as per which the

taxpayer are not supposed to get creative in their tax arrangements and rather utilise the

concessions provided in the statute in the manner prescribed to lower tax liability.

Anti –avoidance provisions were incorporated in ITAA 1936 (Part IVA) in 1981

Before 2006, the clauses only targeted taxpayers but not the promoters offering such

schemes to them. However, this was rectified with promoter penalty provisions with

wider powers available to Tax Commissioner (Gilders et. al., 2016).

Conclusion

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation

As a result of the measures undertaken above, the right to manage tax affairs for lowering tax

still exists but steps have been taken to prevent the abuse of the same (Barkoczy, 2017).

Question 5

Issue

In wake of the relevant provisions of ITAA 1936 along with case law, the relevant treatment of

the proceeds received from pine tree removal needs to be outlined.

Rule

Any income that arises from passing the “right to fell timber” would be treated as royalty as

highlighted by s. 26(f), ITAA 1936. This recognition is independent of the taxpayer conduction

forest operations or not. A leading case which provides evidence about the same is McCauley

v The Federal Commissioner of Taxation (1944) 69 CLR 235 case (Deutsch et. al., 2016).

The royalty mechanism can be enacted in the following two formats (Sadiq et. al., 2016).

A sum lump payment being forwarded by contractor to land owner with no regards to

actual timber extracted. For such a case, a leading case is Stanton v The Federal

Commissioner of Taxation (1955) 92 CLR 630 in accordance with which payments

received are non-assessable.

Royalty linked with the amount of timber extracted in which cases the receipts are

assessable in the hands of the land owner.

Application

It is apparent that Bill did not grow the pine trees and now wanted to get rid of these for

establishing a business. The compensation provided by the contractor (i.e. logging company) is

given as $1,000 for every meter of pine timber extracted. Since, there is a link between proceeds

obtained and the timber taken, hence the proceeds would be taxable at Bill’s end. However, if the

right was given to the contractor for $50,000, then the proceeds would not be taxable considering

the discussion and case law cited above.

Conclusion

Hence, the proceeds received from pine timber would be assessable for Bill only when the

royalty is linked to wood extracted while lump sum payment is not taxed.

6

As a result of the measures undertaken above, the right to manage tax affairs for lowering tax

still exists but steps have been taken to prevent the abuse of the same (Barkoczy, 2017).

Question 5

Issue

In wake of the relevant provisions of ITAA 1936 along with case law, the relevant treatment of

the proceeds received from pine tree removal needs to be outlined.

Rule

Any income that arises from passing the “right to fell timber” would be treated as royalty as

highlighted by s. 26(f), ITAA 1936. This recognition is independent of the taxpayer conduction

forest operations or not. A leading case which provides evidence about the same is McCauley

v The Federal Commissioner of Taxation (1944) 69 CLR 235 case (Deutsch et. al., 2016).

The royalty mechanism can be enacted in the following two formats (Sadiq et. al., 2016).

A sum lump payment being forwarded by contractor to land owner with no regards to

actual timber extracted. For such a case, a leading case is Stanton v The Federal

Commissioner of Taxation (1955) 92 CLR 630 in accordance with which payments

received are non-assessable.

Royalty linked with the amount of timber extracted in which cases the receipts are

assessable in the hands of the land owner.

Application

It is apparent that Bill did not grow the pine trees and now wanted to get rid of these for

establishing a business. The compensation provided by the contractor (i.e. logging company) is

given as $1,000 for every meter of pine timber extracted. Since, there is a link between proceeds

obtained and the timber taken, hence the proceeds would be taxable at Bill’s end. However, if the

right was given to the contractor for $50,000, then the proceeds would not be taxable considering

the discussion and case law cited above.

Conclusion

Hence, the proceeds received from pine timber would be assessable for Bill only when the

royalty is linked to wood extracted while lump sum payment is not taxed.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation

References

Barkoczy, S. (2017), Foundation of Taxation Law 2017, 9thed., North Ryde: CCH Publications

CCH (2013), Australian Master Tax Guide 2013, 51st ed., Sydney: Wolters Kluwer

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2016), Australian tax handbook

8th ed., Pymont: Thomson Reuters,

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016), Understanding taxation law

2016, 9th ed., Sydney: LexisNexis/Butterworths.

Nethercott, L., Richardson, G. and Devos, K. (2016), Australian Taxation Study Manual 2016,

4th ed., Sydney: Oxford University Press

Sadiq, K, Coleman, C, Hanegbi, R, Jogarajan, S, Krever, R, Obst, W, and Ting, A

(2016) , Principles of Taxation Law 2016, 8th ed., Pymont:Thomson Reuters

Woellner, R (2014), Australian taxation law 2014, 7th ed., North Ryde: CCH Australia

7

References

Barkoczy, S. (2017), Foundation of Taxation Law 2017, 9thed., North Ryde: CCH Publications

CCH (2013), Australian Master Tax Guide 2013, 51st ed., Sydney: Wolters Kluwer

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2016), Australian tax handbook

8th ed., Pymont: Thomson Reuters,

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016), Understanding taxation law

2016, 9th ed., Sydney: LexisNexis/Butterworths.

Nethercott, L., Richardson, G. and Devos, K. (2016), Australian Taxation Study Manual 2016,

4th ed., Sydney: Oxford University Press

Sadiq, K, Coleman, C, Hanegbi, R, Jogarajan, S, Krever, R, Obst, W, and Ting, A

(2016) , Principles of Taxation Law 2016, 8th ed., Pymont:Thomson Reuters

Woellner, R (2014), Australian taxation law 2014, 7th ed., North Ryde: CCH Australia

7

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.