Taxation Assignment: Capital Gains, Fringe Benefits, and Tax Law

VerifiedAdded on 2020/03/23

|9

|3175

|32

Homework Assignment

AI Summary

This assignment solution for HI6028 Taxation Theory, Practice & Law, analyzes various aspects of taxation. It begins with the calculation of Eric's net capital gain or loss, differentiating between assets for personal use and collectibles, and determining the tax implications. The solution then calculates Brian's taxable value of fringe benefits, considering a loan with a reduced interest rate and statutory interest rates. The assignment also addresses the allocation of property loss between Jack and Jill based on their profit-sharing agreement, and the implications for tax purposes. Finally, the solution explores the principle established in IRC v Duke of Westminster [1936] AC 1, emphasizing the legality of tax minimization through legitimate means. The assignment covers capital gains, fringe benefits, property loss allocation, and the Duke of Westminster case, demonstrating an understanding of tax principles and calculations.

1

HI6028 Taxation Theory, Practice & Law

<Student ID>

<Student Name>

<University Name>

HI6028 Taxation Theory, Practice & Law

<Student ID>

<Student Name>

<University Name>

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Contents

1. Calculation of Eric’s net capital gain or net capital loss for the year:...................................3

2. Calculation of Brian’s taxable value of the fringe benefits for the 2016/17 FBT year:.........4

3. Allocation of loss on property for tax purposes.....................................................................5

4. Principle established in IRC v Duke of Westminster [1936] AC 1.......................................6

5. Logging company scenario....................................................................................................7

References..................................................................................................................................8

Contents

1. Calculation of Eric’s net capital gain or net capital loss for the year:...................................3

2. Calculation of Brian’s taxable value of the fringe benefits for the 2016/17 FBT year:.........4

3. Allocation of loss on property for tax purposes.....................................................................5

4. Principle established in IRC v Duke of Westminster [1936] AC 1.......................................6

5. Logging company scenario....................................................................................................7

References..................................................................................................................................8

3

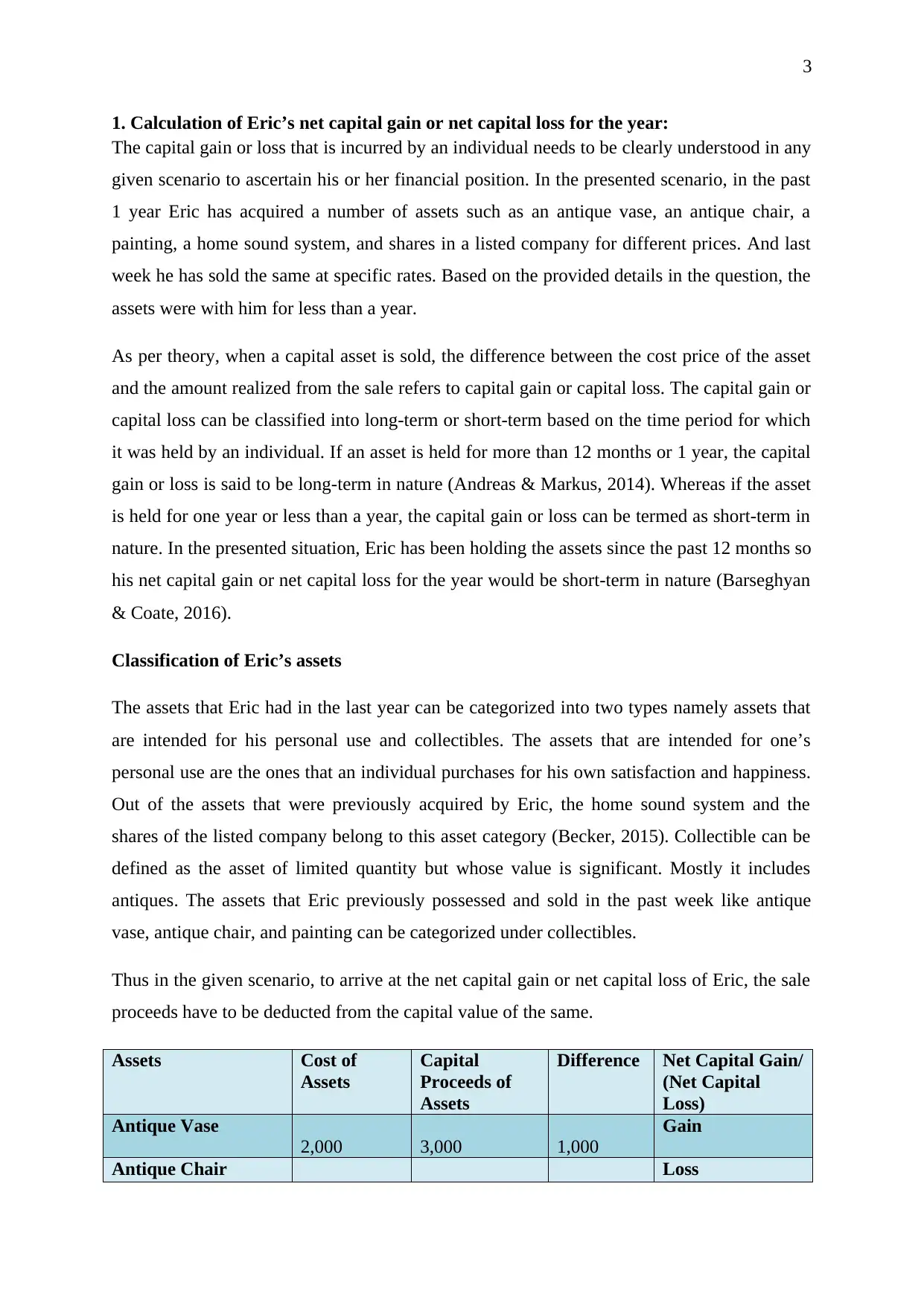

1. Calculation of Eric’s net capital gain or net capital loss for the year:

The capital gain or loss that is incurred by an individual needs to be clearly understood in any

given scenario to ascertain his or her financial position. In the presented scenario, in the past

1 year Eric has acquired a number of assets such as an antique vase, an antique chair, a

painting, a home sound system, and shares in a listed company for different prices. And last

week he has sold the same at specific rates. Based on the provided details in the question, the

assets were with him for less than a year.

As per theory, when a capital asset is sold, the difference between the cost price of the asset

and the amount realized from the sale refers to capital gain or capital loss. The capital gain or

capital loss can be classified into long-term or short-term based on the time period for which

it was held by an individual. If an asset is held for more than 12 months or 1 year, the capital

gain or loss is said to be long-term in nature (Andreas & Markus, 2014). Whereas if the asset

is held for one year or less than a year, the capital gain or loss can be termed as short-term in

nature. In the presented situation, Eric has been holding the assets since the past 12 months so

his net capital gain or net capital loss for the year would be short-term in nature (Barseghyan

& Coate, 2016).

Classification of Eric’s assets

The assets that Eric had in the last year can be categorized into two types namely assets that

are intended for his personal use and collectibles. The assets that are intended for one’s

personal use are the ones that an individual purchases for his own satisfaction and happiness.

Out of the assets that were previously acquired by Eric, the home sound system and the

shares of the listed company belong to this asset category (Becker, 2015). Collectible can be

defined as the asset of limited quantity but whose value is significant. Mostly it includes

antiques. The assets that Eric previously possessed and sold in the past week like antique

vase, antique chair, and painting can be categorized under collectibles.

Thus in the given scenario, to arrive at the net capital gain or net capital loss of Eric, the sale

proceeds have to be deducted from the capital value of the same.

Assets Cost of

Assets

Capital

Proceeds of

Assets

Difference Net Capital Gain/

(Net Capital

Loss)

Antique Vase

2,000 3,000 1,000

Gain

Antique Chair Loss

1. Calculation of Eric’s net capital gain or net capital loss for the year:

The capital gain or loss that is incurred by an individual needs to be clearly understood in any

given scenario to ascertain his or her financial position. In the presented scenario, in the past

1 year Eric has acquired a number of assets such as an antique vase, an antique chair, a

painting, a home sound system, and shares in a listed company for different prices. And last

week he has sold the same at specific rates. Based on the provided details in the question, the

assets were with him for less than a year.

As per theory, when a capital asset is sold, the difference between the cost price of the asset

and the amount realized from the sale refers to capital gain or capital loss. The capital gain or

capital loss can be classified into long-term or short-term based on the time period for which

it was held by an individual. If an asset is held for more than 12 months or 1 year, the capital

gain or loss is said to be long-term in nature (Andreas & Markus, 2014). Whereas if the asset

is held for one year or less than a year, the capital gain or loss can be termed as short-term in

nature. In the presented situation, Eric has been holding the assets since the past 12 months so

his net capital gain or net capital loss for the year would be short-term in nature (Barseghyan

& Coate, 2016).

Classification of Eric’s assets

The assets that Eric had in the last year can be categorized into two types namely assets that

are intended for his personal use and collectibles. The assets that are intended for one’s

personal use are the ones that an individual purchases for his own satisfaction and happiness.

Out of the assets that were previously acquired by Eric, the home sound system and the

shares of the listed company belong to this asset category (Becker, 2015). Collectible can be

defined as the asset of limited quantity but whose value is significant. Mostly it includes

antiques. The assets that Eric previously possessed and sold in the past week like antique

vase, antique chair, and painting can be categorized under collectibles.

Thus in the given scenario, to arrive at the net capital gain or net capital loss of Eric, the sale

proceeds have to be deducted from the capital value of the same.

Assets Cost of

Assets

Capital

Proceeds of

Assets

Difference Net Capital Gain/

(Net Capital

Loss)

Antique Vase

2,000 3,000 1,000

Gain

Antique Chair Loss

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

3,000 1,000 -2,000

Painting

9,000 1,000 -8,000

Loss

Home Sound System

12,000 11,000 -1,000

Loss

Shares in listed

company 5,000 20,000 15,000

Gain

Total 31,000 36,000

Net Capital

Gain/Loss

5,000 Total Net Capital

Gain

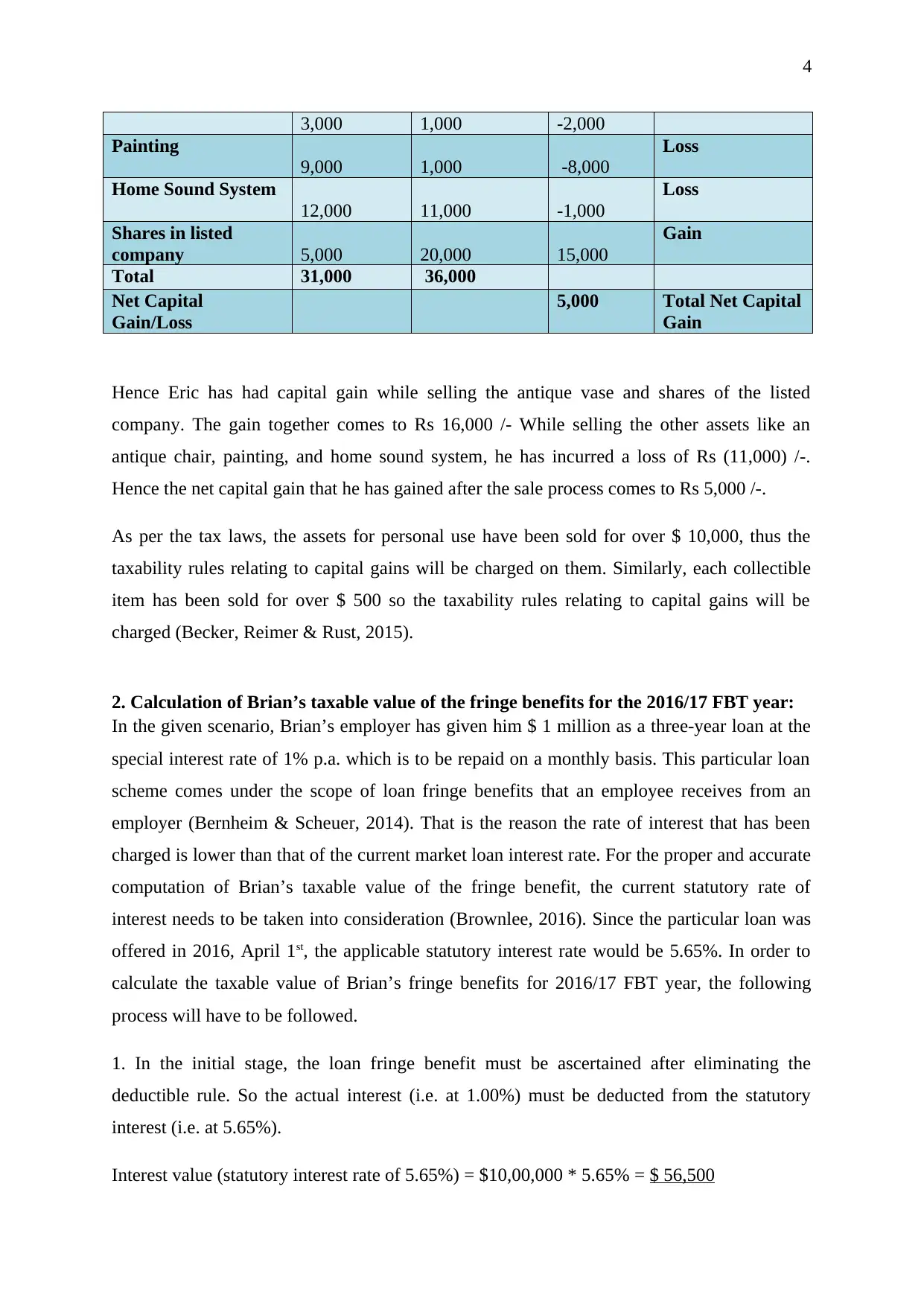

Hence Eric has had capital gain while selling the antique vase and shares of the listed

company. The gain together comes to Rs 16,000 /- While selling the other assets like an

antique chair, painting, and home sound system, he has incurred a loss of Rs (11,000) /-.

Hence the net capital gain that he has gained after the sale process comes to Rs 5,000 /-.

As per the tax laws, the assets for personal use have been sold for over $ 10,000, thus the

taxability rules relating to capital gains will be charged on them. Similarly, each collectible

item has been sold for over $ 500 so the taxability rules relating to capital gains will be

charged (Becker, Reimer & Rust, 2015).

2. Calculation of Brian’s taxable value of the fringe benefits for the 2016/17 FBT year:

In the given scenario, Brian’s employer has given him $ 1 million as a three-year loan at the

special interest rate of 1% p.a. which is to be repaid on a monthly basis. This particular loan

scheme comes under the scope of loan fringe benefits that an employee receives from an

employer (Bernheim & Scheuer, 2014). That is the reason the rate of interest that has been

charged is lower than that of the current market loan interest rate. For the proper and accurate

computation of Brian’s taxable value of the fringe benefit, the current statutory rate of

interest needs to be taken into consideration (Brownlee, 2016). Since the particular loan was

offered in 2016, April 1st, the applicable statutory interest rate would be 5.65%. In order to

calculate the taxable value of Brian’s fringe benefits for 2016/17 FBT year, the following

process will have to be followed.

1. In the initial stage, the loan fringe benefit must be ascertained after eliminating the

deductible rule. So the actual interest (i.e. at 1.00%) must be deducted from the statutory

interest (i.e. at 5.65%).

Interest value (statutory interest rate of 5.65%) = $10,00,000 * 5.65% = $ 56,500

3,000 1,000 -2,000

Painting

9,000 1,000 -8,000

Loss

Home Sound System

12,000 11,000 -1,000

Loss

Shares in listed

company 5,000 20,000 15,000

Gain

Total 31,000 36,000

Net Capital

Gain/Loss

5,000 Total Net Capital

Gain

Hence Eric has had capital gain while selling the antique vase and shares of the listed

company. The gain together comes to Rs 16,000 /- While selling the other assets like an

antique chair, painting, and home sound system, he has incurred a loss of Rs (11,000) /-.

Hence the net capital gain that he has gained after the sale process comes to Rs 5,000 /-.

As per the tax laws, the assets for personal use have been sold for over $ 10,000, thus the

taxability rules relating to capital gains will be charged on them. Similarly, each collectible

item has been sold for over $ 500 so the taxability rules relating to capital gains will be

charged (Becker, Reimer & Rust, 2015).

2. Calculation of Brian’s taxable value of the fringe benefits for the 2016/17 FBT year:

In the given scenario, Brian’s employer has given him $ 1 million as a three-year loan at the

special interest rate of 1% p.a. which is to be repaid on a monthly basis. This particular loan

scheme comes under the scope of loan fringe benefits that an employee receives from an

employer (Bernheim & Scheuer, 2014). That is the reason the rate of interest that has been

charged is lower than that of the current market loan interest rate. For the proper and accurate

computation of Brian’s taxable value of the fringe benefit, the current statutory rate of

interest needs to be taken into consideration (Brownlee, 2016). Since the particular loan was

offered in 2016, April 1st, the applicable statutory interest rate would be 5.65%. In order to

calculate the taxable value of Brian’s fringe benefits for 2016/17 FBT year, the following

process will have to be followed.

1. In the initial stage, the loan fringe benefit must be ascertained after eliminating the

deductible rule. So the actual interest (i.e. at 1.00%) must be deducted from the statutory

interest (i.e. at 5.65%).

Interest value (statutory interest rate of 5.65%) = $10,00,000 * 5.65% = $ 56,500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

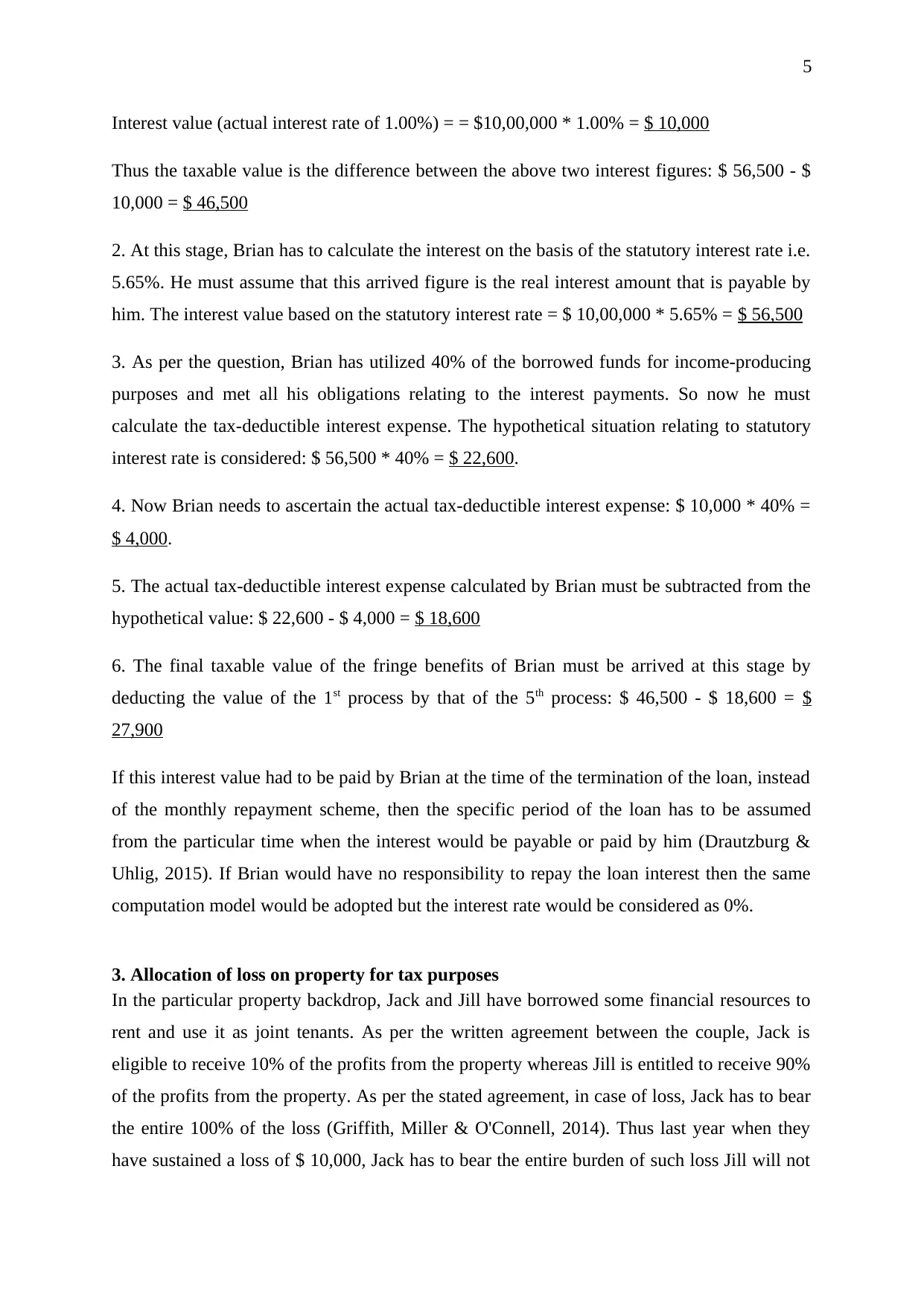

Interest value (actual interest rate of 1.00%) = = $10,00,000 * 1.00% = $ 10,000

Thus the taxable value is the difference between the above two interest figures: $ 56,500 - $

10,000 = $ 46,500

2. At this stage, Brian has to calculate the interest on the basis of the statutory interest rate i.e.

5.65%. He must assume that this arrived figure is the real interest amount that is payable by

him. The interest value based on the statutory interest rate = $ 10,00,000 * 5.65% = $ 56,500

3. As per the question, Brian has utilized 40% of the borrowed funds for income-producing

purposes and met all his obligations relating to the interest payments. So now he must

calculate the tax-deductible interest expense. The hypothetical situation relating to statutory

interest rate is considered: $ 56,500 * 40% = $ 22,600.

4. Now Brian needs to ascertain the actual tax-deductible interest expense: $ 10,000 * 40% =

$ 4,000.

5. The actual tax-deductible interest expense calculated by Brian must be subtracted from the

hypothetical value: $ 22,600 - $ 4,000 = $ 18,600

6. The final taxable value of the fringe benefits of Brian must be arrived at this stage by

deducting the value of the 1st process by that of the 5th process: $ 46,500 - $ 18,600 = $

27,900

If this interest value had to be paid by Brian at the time of the termination of the loan, instead

of the monthly repayment scheme, then the specific period of the loan has to be assumed

from the particular time when the interest would be payable or paid by him (Drautzburg &

Uhlig, 2015). If Brian would have no responsibility to repay the loan interest then the same

computation model would be adopted but the interest rate would be considered as 0%.

3. Allocation of loss on property for tax purposes

In the particular property backdrop, Jack and Jill have borrowed some financial resources to

rent and use it as joint tenants. As per the written agreement between the couple, Jack is

eligible to receive 10% of the profits from the property whereas Jill is entitled to receive 90%

of the profits from the property. As per the stated agreement, in case of loss, Jack has to bear

the entire 100% of the loss (Griffith, Miller & O'Connell, 2014). Thus last year when they

have sustained a loss of $ 10,000, Jack has to bear the entire burden of such loss Jill will not

Interest value (actual interest rate of 1.00%) = = $10,00,000 * 1.00% = $ 10,000

Thus the taxable value is the difference between the above two interest figures: $ 56,500 - $

10,000 = $ 46,500

2. At this stage, Brian has to calculate the interest on the basis of the statutory interest rate i.e.

5.65%. He must assume that this arrived figure is the real interest amount that is payable by

him. The interest value based on the statutory interest rate = $ 10,00,000 * 5.65% = $ 56,500

3. As per the question, Brian has utilized 40% of the borrowed funds for income-producing

purposes and met all his obligations relating to the interest payments. So now he must

calculate the tax-deductible interest expense. The hypothetical situation relating to statutory

interest rate is considered: $ 56,500 * 40% = $ 22,600.

4. Now Brian needs to ascertain the actual tax-deductible interest expense: $ 10,000 * 40% =

$ 4,000.

5. The actual tax-deductible interest expense calculated by Brian must be subtracted from the

hypothetical value: $ 22,600 - $ 4,000 = $ 18,600

6. The final taxable value of the fringe benefits of Brian must be arrived at this stage by

deducting the value of the 1st process by that of the 5th process: $ 46,500 - $ 18,600 = $

27,900

If this interest value had to be paid by Brian at the time of the termination of the loan, instead

of the monthly repayment scheme, then the specific period of the loan has to be assumed

from the particular time when the interest would be payable or paid by him (Drautzburg &

Uhlig, 2015). If Brian would have no responsibility to repay the loan interest then the same

computation model would be adopted but the interest rate would be considered as 0%.

3. Allocation of loss on property for tax purposes

In the particular property backdrop, Jack and Jill have borrowed some financial resources to

rent and use it as joint tenants. As per the written agreement between the couple, Jack is

eligible to receive 10% of the profits from the property whereas Jill is entitled to receive 90%

of the profits from the property. As per the stated agreement, in case of loss, Jack has to bear

the entire 100% of the loss (Griffith, Miller & O'Connell, 2014). Thus last year when they

have sustained a loss of $ 10,000, Jack has to bear the entire burden of such loss Jill will not

6

be having any financial obligation towards this loss. This loss of Jack can be set off with the

other forms of income of Jack so that he can determine his net profit or loss of the year. He

has one more option in hand i.e. to carry forward the loss for the following years (Henneman,

2015).

If the couple decides to sell off the property, the subsequent gain or loss from it would be

available for them. In case there is a loss from the specific transaction, the same has to be

incurred by Jack and he has the entire right to carry it forward in the future years or use it in

the very year to ascertain his total net profit or loss. Similarly, in case of gain, the particular

amount must be distributed between Jack and Jill in the exact proportion that has been stated

in the written agreement (Jaimovich & Rebelo, 2017). The ratio decided by the couple for

sharing of profits is 1:9 where Jack receives one portion of the profits and Jill receives nine

portions of the profit. Jack has the complete right and authority to set off the particular loss

against the gain that they would earn by selling of the property.

Thus it can be concluded that Jack is in a position where he has the authority to treat the loss

from the property as per his convenience and need. He could set of this loss from the property

if he would gain from selling the same (Piketty, Saez & Stantcheva, 2014). If Jack has no

gains in the current year then the loss must be borne by him while his wife would not have

any obligation towards the loss from the property. The treatment of tax would be insignificant

for Jill whereas Jack would have to record such loss in his books of accounts.

4. Principle established in IRC v Duke of Westminster [1936] AC 1

The particular case relating to IRC v Duke of Westminster [1936] is a popular case that has

come under limelight due to the particular tax avoidance situation. After referring the case, it

can be clearly stated that every individual is righteously entitled to utilize his or her legal

rights and benefits to help him minimize his tax that is attached to his total income earned

during the year. In layman’s language, it can be stated that if a person adopts fair and legal

methods to reduce his total income value and thus reduce his tax value, the Commissioners of

Inland Revenue have no power and authority to compel a taxpayer to pay a higher tax amount

(Pomeranz, 2015). This particular model is applicable only when a taxpayer uses the fair and

honest methods to reduce the amount of tax that is supposed to be paid by him. Fair tools and

techniques must be adopted by him in order to reduce his gross income at the end of the year

with the purpose to decrease his tax payable amount.

be having any financial obligation towards this loss. This loss of Jack can be set off with the

other forms of income of Jack so that he can determine his net profit or loss of the year. He

has one more option in hand i.e. to carry forward the loss for the following years (Henneman,

2015).

If the couple decides to sell off the property, the subsequent gain or loss from it would be

available for them. In case there is a loss from the specific transaction, the same has to be

incurred by Jack and he has the entire right to carry it forward in the future years or use it in

the very year to ascertain his total net profit or loss. Similarly, in case of gain, the particular

amount must be distributed between Jack and Jill in the exact proportion that has been stated

in the written agreement (Jaimovich & Rebelo, 2017). The ratio decided by the couple for

sharing of profits is 1:9 where Jack receives one portion of the profits and Jill receives nine

portions of the profit. Jack has the complete right and authority to set off the particular loss

against the gain that they would earn by selling of the property.

Thus it can be concluded that Jack is in a position where he has the authority to treat the loss

from the property as per his convenience and need. He could set of this loss from the property

if he would gain from selling the same (Piketty, Saez & Stantcheva, 2014). If Jack has no

gains in the current year then the loss must be borne by him while his wife would not have

any obligation towards the loss from the property. The treatment of tax would be insignificant

for Jill whereas Jack would have to record such loss in his books of accounts.

4. Principle established in IRC v Duke of Westminster [1936] AC 1

The particular case relating to IRC v Duke of Westminster [1936] is a popular case that has

come under limelight due to the particular tax avoidance situation. After referring the case, it

can be clearly stated that every individual is righteously entitled to utilize his or her legal

rights and benefits to help him minimize his tax that is attached to his total income earned

during the year. In layman’s language, it can be stated that if a person adopts fair and legal

methods to reduce his total income value and thus reduce his tax value, the Commissioners of

Inland Revenue have no power and authority to compel a taxpayer to pay a higher tax amount

(Pomeranz, 2015). This particular model is applicable only when a taxpayer uses the fair and

honest methods to reduce the amount of tax that is supposed to be paid by him. Fair tools and

techniques must be adopted by him in order to reduce his gross income at the end of the year

with the purpose to decrease his tax payable amount.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

The case is one of the best examples that add value to the taxation model and acts like a

breath of fresh air for honest taxpayers. The particular legal case covers various areas

including every person who adopts fair strategic methods to manage his books of accounts

has the right to take legal assistance to decrease his total income value (Scheuer & Werning,

2017). If the ethical and moral principals are in place and they have not been altered, the

person cannot be forced to pay further tax in the process. The use of legal mode by the person

strengthens his position in the eyes of the law. So no authority can question the validity of the

person’s method since he has the legal backing.

When the particular case was stated in front of the judge, he stated that the effective use of

the legal model by an individual to lower his income is a fair technique. The law should stand

by it since no ethical aspects have been hampered in the process. This particular rule holds

immense relevance in the current times in Australia. It discourages business undertakings to

manipulate their books of accounts to have an additional advantage. It even provides the legal

right to function a business activity in a truthful manner (Schmitt, 2015). It encourages

businesses to use ethical means to strengthen their financial performance instead of altering

their books of accounts. Since this principle encourages individuals as well as businesses to

operate efficiently it is a valuable case that makes the contribution to the taxation system of

Australia.

5. Logging company scenario

In the presented situation, Bill has a large parcel of land on which there are numerous tall

pine trees. He intends to use it for grazing sheep and so he wants to have it cleared. A

particular logging firm is showing its willingness to pay him $1,000 for every 100 meters of

the timber that they can take from the land. The first and foremost question that arises in the

situation is whether the tax laws are applicable or not for Bill for the money that he would be

receiving from the logging business (Thomson, 2015). The given circumstances in the

question do not throw light on the fact that whether the receipts that he would receive from

the firm could be considered as revenue receipts or not. This high degree of uncertainty

shows that the rules relating to the capital gains taxes do not apply to Bill’s specific situation.

If Bill would receive a significant amount of money of $ 50,000 from the logging business to

remove the pine trees from his yard, the same amount would be considered as a capital

receipt for Bill. The very reason for such treatment is the large value of the finance and the

lack of recurring receipts in the situation. In this situation, relevant tax rules would apply to

The case is one of the best examples that add value to the taxation model and acts like a

breath of fresh air for honest taxpayers. The particular legal case covers various areas

including every person who adopts fair strategic methods to manage his books of accounts

has the right to take legal assistance to decrease his total income value (Scheuer & Werning,

2017). If the ethical and moral principals are in place and they have not been altered, the

person cannot be forced to pay further tax in the process. The use of legal mode by the person

strengthens his position in the eyes of the law. So no authority can question the validity of the

person’s method since he has the legal backing.

When the particular case was stated in front of the judge, he stated that the effective use of

the legal model by an individual to lower his income is a fair technique. The law should stand

by it since no ethical aspects have been hampered in the process. This particular rule holds

immense relevance in the current times in Australia. It discourages business undertakings to

manipulate their books of accounts to have an additional advantage. It even provides the legal

right to function a business activity in a truthful manner (Schmitt, 2015). It encourages

businesses to use ethical means to strengthen their financial performance instead of altering

their books of accounts. Since this principle encourages individuals as well as businesses to

operate efficiently it is a valuable case that makes the contribution to the taxation system of

Australia.

5. Logging company scenario

In the presented situation, Bill has a large parcel of land on which there are numerous tall

pine trees. He intends to use it for grazing sheep and so he wants to have it cleared. A

particular logging firm is showing its willingness to pay him $1,000 for every 100 meters of

the timber that they can take from the land. The first and foremost question that arises in the

situation is whether the tax laws are applicable or not for Bill for the money that he would be

receiving from the logging business (Thomson, 2015). The given circumstances in the

question do not throw light on the fact that whether the receipts that he would receive from

the firm could be considered as revenue receipts or not. This high degree of uncertainty

shows that the rules relating to the capital gains taxes do not apply to Bill’s specific situation.

If Bill would receive a significant amount of money of $ 50,000 from the logging business to

remove the pine trees from his yard, the same amount would be considered as a capital

receipt for Bill. The very reason for such treatment is the large value of the finance and the

lack of recurring receipts in the situation. In this situation, relevant tax rules would apply to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Bill. Thus the nature of the financial transaction between parties has a significant impact on

the applicable taxation laws (Wallace, 2015).

So in the mentioned scenarios, the value of the finance involved has a significant impact on

the application of taxation law. In the former instance, Bill would be receiving smaller and

repeated payments from the logging firm while in the latter situation; he would be receiving a

financial figure in bulk and the receipt would be one-time in nature (Scheuer & Werning,

2017). As per the taxation law, when one party is involved in a sales transaction for a specific

consideration, the receipt received in the situation is considered to be a capital one and thus it

is taxable in the eyes of law. In the first scenario, the taxation would be charged at normal tax

rates and they would not be treated as capital gains for Bill.

References

Andreas, O. and Markus, H., 2014. Taxation of income from domestic and cross-border

collective investment.

Barseghyan, L. and Coate, S., 2016. Property Taxation, Zoning, and Efficiency in a Dynamic

Tiebout Model. American Economic Journal: Economic Policy, 8(3), pp.1-38.

Becker, J., 2015. The Relation of Article 9 Paragraph 1 German Double Taxation Treaties to

Domestic Tax Law and the Consequences for Current Value Depreciation under Section 1

Paragraph 1: Foreign Tax Act. Intertax, 43(10), pp.589-594.

Becker, J., Reimer, E. and Rust, A., 2015. Klaus Vogel on Double Taxation Conventions.

Kluwer Law International.

Bernheim, B.D. and Scheuer, F., 2014. ECON 242: PUBLIC FINANCE AND TAXATION

II.

Brownlee, W.E., 2016. Federal Taxation in America. Cambridge University Press.

Drautzburg, T. and Uhlig, H., 2015. Fiscal stimulus and distortionary taxation. Review of

Economic Dynamics, 18(4), pp.894-920.

Griffith, R., Miller, H. and O'Connell, M., 2014. Ownership of intellectual property and

corporate taxation. Journal of Public Economics, 112, pp.12-23.

Bill. Thus the nature of the financial transaction between parties has a significant impact on

the applicable taxation laws (Wallace, 2015).

So in the mentioned scenarios, the value of the finance involved has a significant impact on

the application of taxation law. In the former instance, Bill would be receiving smaller and

repeated payments from the logging firm while in the latter situation; he would be receiving a

financial figure in bulk and the receipt would be one-time in nature (Scheuer & Werning,

2017). As per the taxation law, when one party is involved in a sales transaction for a specific

consideration, the receipt received in the situation is considered to be a capital one and thus it

is taxable in the eyes of law. In the first scenario, the taxation would be charged at normal tax

rates and they would not be treated as capital gains for Bill.

References

Andreas, O. and Markus, H., 2014. Taxation of income from domestic and cross-border

collective investment.

Barseghyan, L. and Coate, S., 2016. Property Taxation, Zoning, and Efficiency in a Dynamic

Tiebout Model. American Economic Journal: Economic Policy, 8(3), pp.1-38.

Becker, J., 2015. The Relation of Article 9 Paragraph 1 German Double Taxation Treaties to

Domestic Tax Law and the Consequences for Current Value Depreciation under Section 1

Paragraph 1: Foreign Tax Act. Intertax, 43(10), pp.589-594.

Becker, J., Reimer, E. and Rust, A., 2015. Klaus Vogel on Double Taxation Conventions.

Kluwer Law International.

Bernheim, B.D. and Scheuer, F., 2014. ECON 242: PUBLIC FINANCE AND TAXATION

II.

Brownlee, W.E., 2016. Federal Taxation in America. Cambridge University Press.

Drautzburg, T. and Uhlig, H., 2015. Fiscal stimulus and distortionary taxation. Review of

Economic Dynamics, 18(4), pp.894-920.

Griffith, R., Miller, H. and O'Connell, M., 2014. Ownership of intellectual property and

corporate taxation. Journal of Public Economics, 112, pp.12-23.

9

Henneman, J.B., 2015. Royal Taxation in Fourteenth-Century France: The Development of

War Financing, 1322-1359. Princeton University Press.

Jaimovich, N. and Rebelo, S., 2017. Nonlinear effects of taxation on growth. Journal of

Political Economy, 125(1), pp.265-291.

Piketty, T., Saez, E. and Stantcheva, S., 2014. Optimal taxation of top labor incomes: A tale

of three elasticities. American economic journal: economic policy, 6(1), pp.230-271.

Pomeranz, D., 2015. No taxation without information: Deterrence and self-enforcement in the

value added tax. The American economic review, 105(8), pp.2539-2569.

Scheuer, F. and Werning, I., 2017. The taxation of superstars. The Quarterly Journal of

Economics, 132(1), pp.211-270.

Schmitt, N., 2015. Social Norms or Income Taxation–What drives a Couple‘s Labor Supply?

Experimental Evidence. Norma, (2/13).

Thomson, W., 2015. Axiomatic and game-theoretic analysis of bankruptcy and taxation

problems: an update. Mathematical Social Sciences, 74, pp.41-59.

Wallace, S.L., 2015. Taxation in Egypt from Augustus to Diocletian. Princeton University

Press.

Henneman, J.B., 2015. Royal Taxation in Fourteenth-Century France: The Development of

War Financing, 1322-1359. Princeton University Press.

Jaimovich, N. and Rebelo, S., 2017. Nonlinear effects of taxation on growth. Journal of

Political Economy, 125(1), pp.265-291.

Piketty, T., Saez, E. and Stantcheva, S., 2014. Optimal taxation of top labor incomes: A tale

of three elasticities. American economic journal: economic policy, 6(1), pp.230-271.

Pomeranz, D., 2015. No taxation without information: Deterrence and self-enforcement in the

value added tax. The American economic review, 105(8), pp.2539-2569.

Scheuer, F. and Werning, I., 2017. The taxation of superstars. The Quarterly Journal of

Economics, 132(1), pp.211-270.

Schmitt, N., 2015. Social Norms or Income Taxation–What drives a Couple‘s Labor Supply?

Experimental Evidence. Norma, (2/13).

Thomson, W., 2015. Axiomatic and game-theoretic analysis of bankruptcy and taxation

problems: an update. Mathematical Social Sciences, 74, pp.41-59.

Wallace, S.L., 2015. Taxation in Egypt from Augustus to Diocletian. Princeton University

Press.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.