Taxation Law Assignment: CGT, Depreciation, and Tax Concessions

VerifiedAdded on 2022/10/17

|13

|2945

|19

Homework Assignment

AI Summary

This assignment provides a comprehensive analysis of taxation law, focusing on capital gains tax (CGT) and depreciation. The first part of the assignment analyzes different scenarios involving Jasmine, examining the tax implications of selling her main residence (pre-CGT asset), a car (personal use asset), her cleaning business (small business CGT concessions), furniture, and paintings (collectables). The second part of the assignment focuses on John and his CNC machine, exploring whether he can claim a deduction for the decline in the machine's value. The analysis includes relevant sections from the Income Tax Assessment Act 1997 (ITAA 1997), discussing active asset tests, small business concessions, personal use assets, and the cost base of depreciating assets. The assignment provides a detailed application of the law to each scenario, offering a clear understanding of the tax implications for each situation.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer A: Sale of main residence.........................................................................................2

Answer B: Sale of car:...........................................................................................................2

Answer C: Sale of her cleaning business...............................................................................3

Answer D: Sale of Furniture:.................................................................................................4

Answer E: Sale of paintings:..................................................................................................5

Answer to question 2:.................................................................................................................6

Issues:.....................................................................................................................................6

Laws:......................................................................................................................................6

Application:............................................................................................................................7

Conclusion:............................................................................................................................9

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer A: Sale of main residence.........................................................................................2

Answer B: Sale of car:...........................................................................................................2

Answer C: Sale of her cleaning business...............................................................................3

Answer D: Sale of Furniture:.................................................................................................4

Answer E: Sale of paintings:..................................................................................................5

Answer to question 2:.................................................................................................................6

Issues:.....................................................................................................................................6

Laws:......................................................................................................................................6

Application:............................................................................................................................7

Conclusion:............................................................................................................................9

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Answer A: Sale of main residence

The capital gains tax regime was started in the year 1985-86 in order to overcome the

deficiencies that is present in the current income tax system. Under the regime of CGT when

it is noticed that the net capital gains has been accrued to an individual taxpayer during the

specific income year, then such gains is included inside the taxpayer’s assessable income for

that year (Walrut 2017). As the CGT was introduced in 20/9/1985, taxes are only imposed on

the assets that is acquired following the events. For that reason, the word pre-CGT and post-

CGT is very commonly used by the taxpayer for referring the assets or events that happens

prior to that date.

The instances that has been obtained from the case details of Jasmine suggest that she

is the owner of family home which she has purchased in 1981 by paying a sum of $40,000.

Conversely, she has decided to sell it in in the present tax year for $650,000. As it is

understood that Jasmine is leaving Australia for a permanent basis to move UK, the sale of

property has yielded her capital gains (Gordon 2017). However, it must be noted that Jasmine

has purchased the property in 1981 which should be inferred as the pre-CGT asset. The

property was bought before the start of CGT regime. So in this situation the capital gains that

is made from selling her family is disregarded since it is exempted from the regime of CGT.

Answer B: Sale of car:

Within the “sub-div 108-C ITA Act 1997” guidance regarding the capital gains tax

treatment has been made for personal use assets (Sommer 2017). Mentioning “sec 108-20

(2)”, assets that is kept by taxpayer basically for making personal use and usage, it is termed

as personal use asset. Examples are boats, vehicles, furniture etc. are referred as personal use

Answer to question 1:

Answer A: Sale of main residence

The capital gains tax regime was started in the year 1985-86 in order to overcome the

deficiencies that is present in the current income tax system. Under the regime of CGT when

it is noticed that the net capital gains has been accrued to an individual taxpayer during the

specific income year, then such gains is included inside the taxpayer’s assessable income for

that year (Walrut 2017). As the CGT was introduced in 20/9/1985, taxes are only imposed on

the assets that is acquired following the events. For that reason, the word pre-CGT and post-

CGT is very commonly used by the taxpayer for referring the assets or events that happens

prior to that date.

The instances that has been obtained from the case details of Jasmine suggest that she

is the owner of family home which she has purchased in 1981 by paying a sum of $40,000.

Conversely, she has decided to sell it in in the present tax year for $650,000. As it is

understood that Jasmine is leaving Australia for a permanent basis to move UK, the sale of

property has yielded her capital gains (Gordon 2017). However, it must be noted that Jasmine

has purchased the property in 1981 which should be inferred as the pre-CGT asset. The

property was bought before the start of CGT regime. So in this situation the capital gains that

is made from selling her family is disregarded since it is exempted from the regime of CGT.

Answer B: Sale of car:

Within the “sub-div 108-C ITA Act 1997” guidance regarding the capital gains tax

treatment has been made for personal use assets (Sommer 2017). Mentioning “sec 108-20

(2)”, assets that is kept by taxpayer basically for making personal use and usage, it is termed

as personal use asset. Examples are boats, vehicles, furniture etc. are referred as personal use

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

asset. When a taxpayer makes any loss from the personal use asset then they are usually

disregarded under “sec 108-20 (1), ITA Act 1997” notwithstanding of its price.

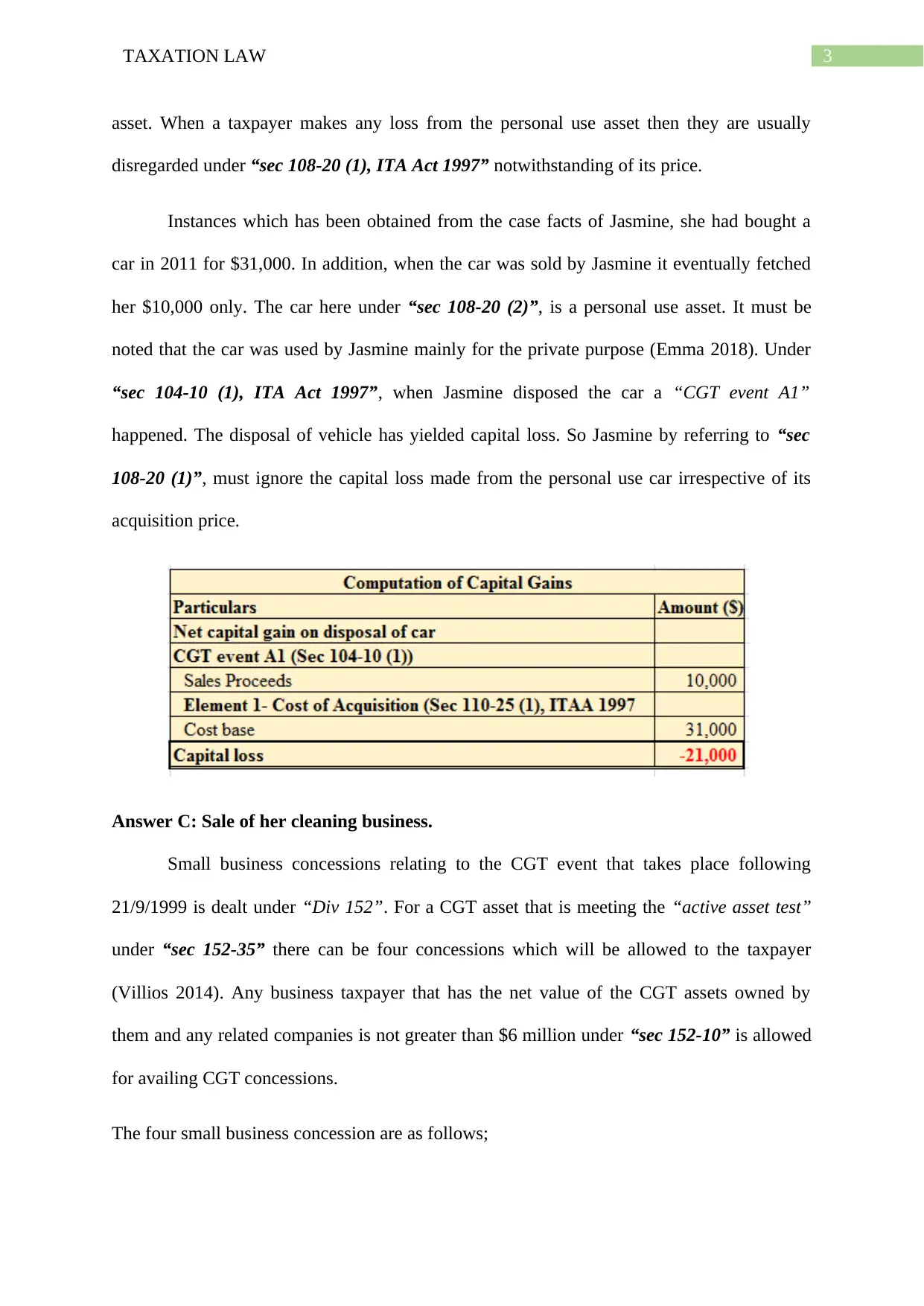

Instances which has been obtained from the case facts of Jasmine, she had bought a

car in 2011 for $31,000. In addition, when the car was sold by Jasmine it eventually fetched

her $10,000 only. The car here under “sec 108-20 (2)”, is a personal use asset. It must be

noted that the car was used by Jasmine mainly for the private purpose (Emma 2018). Under

“sec 104-10 (1), ITA Act 1997”, when Jasmine disposed the car a “CGT event A1”

happened. The disposal of vehicle has yielded capital loss. So Jasmine by referring to “sec

108-20 (1)”, must ignore the capital loss made from the personal use car irrespective of its

acquisition price.

Answer C: Sale of her cleaning business.

Small business concessions relating to the CGT event that takes place following

21/9/1999 is dealt under “Div 152”. For a CGT asset that is meeting the “active asset test”

under “sec 152-35” there can be four concessions which will be allowed to the taxpayer

(Villios 2014). Any business taxpayer that has the net value of the CGT assets owned by

them and any related companies is not greater than $6 million under “sec 152-10” is allowed

for availing CGT concessions.

The four small business concession are as follows;

asset. When a taxpayer makes any loss from the personal use asset then they are usually

disregarded under “sec 108-20 (1), ITA Act 1997” notwithstanding of its price.

Instances which has been obtained from the case facts of Jasmine, she had bought a

car in 2011 for $31,000. In addition, when the car was sold by Jasmine it eventually fetched

her $10,000 only. The car here under “sec 108-20 (2)”, is a personal use asset. It must be

noted that the car was used by Jasmine mainly for the private purpose (Emma 2018). Under

“sec 104-10 (1), ITA Act 1997”, when Jasmine disposed the car a “CGT event A1”

happened. The disposal of vehicle has yielded capital loss. So Jasmine by referring to “sec

108-20 (1)”, must ignore the capital loss made from the personal use car irrespective of its

acquisition price.

Answer C: Sale of her cleaning business.

Small business concessions relating to the CGT event that takes place following

21/9/1999 is dealt under “Div 152”. For a CGT asset that is meeting the “active asset test”

under “sec 152-35” there can be four concessions which will be allowed to the taxpayer

(Villios 2014). Any business taxpayer that has the net value of the CGT assets owned by

them and any related companies is not greater than $6 million under “sec 152-10” is allowed

for availing CGT concessions.

The four small business concession are as follows;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

a. Under “subdiv 152-B” a fifteen year exemption from capital gains is provided to the

small business.

b. As per “subdiv 152-C” a small business is permitted capital gain reduction by 50%.

c. With respect to “subdiv 152-D” a retirement capital gains exemption is permitted.

d. While under “subdiv 152-E” roll-over relief is provided to the taxpayer from capital

gains upon making asset replacement.

Jasmine is found to be selling her small cleaning business. At the time of sale,

Jasmine has yielded capital gains of $125,000 out of which $65,000 relates to business

equipment sale and $60,000 for goodwill. It can be stated that Jasmine is eligible for small

business CGT under “Div 152”. Additionally, under “sec 152-10, ITA Act 1997” the net

value of the CGT assets owned by Jasmine is within $6 million threshold limit (Sadiq and

Marsden 2014). The CGT asset under “sec 152-35, ITAA 1997” also meets the active asset

test. Therefore, Jasmine is eligible for claiming 15-year exemption from the disposal of her

CGT asset. Jasmine has owned the asset for a minimum of 15 years and she also ages more

than 55 years.

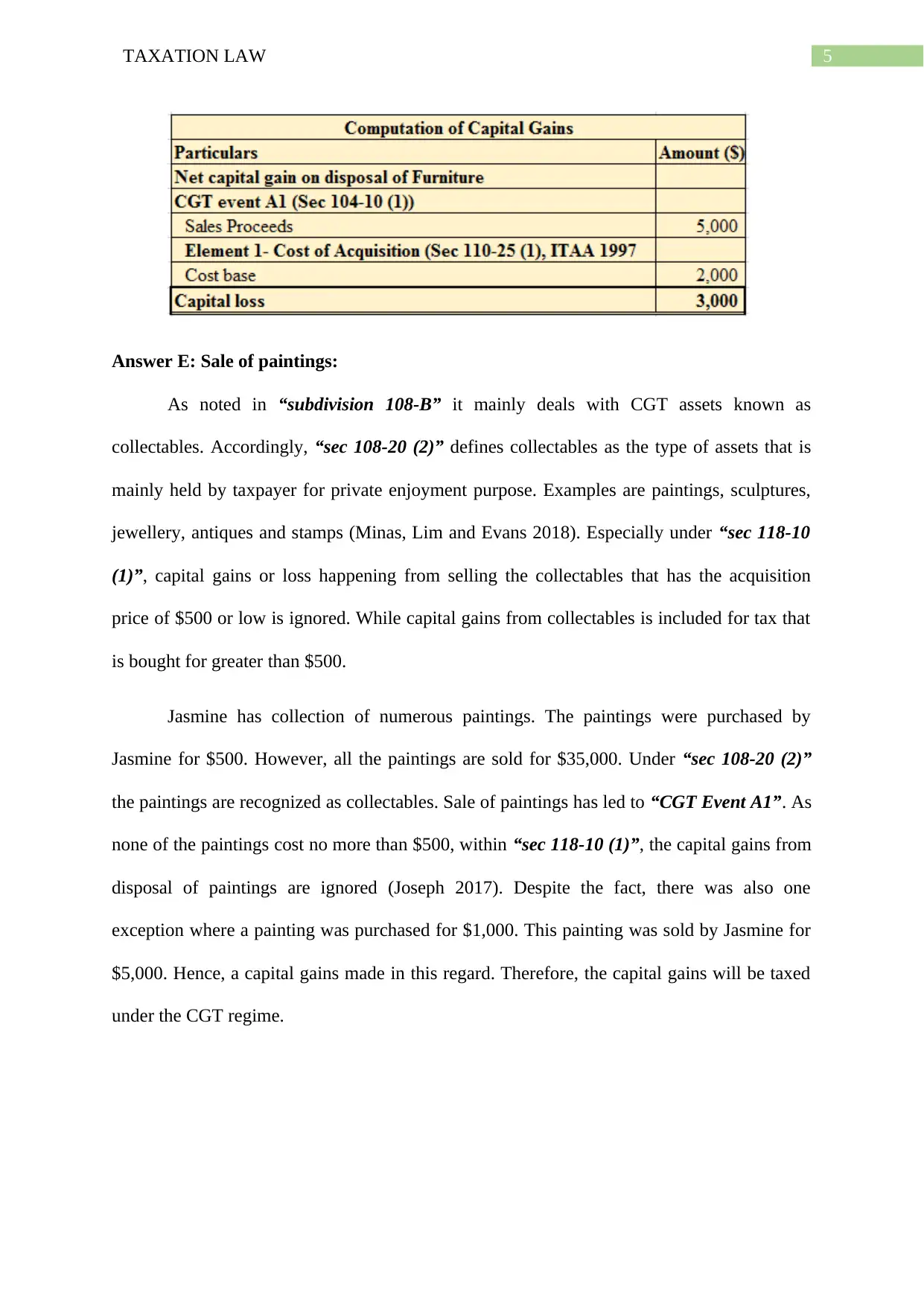

Answer D: Sale of Furniture:

It is essentially vital for the taxpayers to understand that under “sec 118-10, ITA Act

1997” capital gains that is realised from selling the personal use asset is simply disregarded

when the asset is purchased for lower $10,000 or low (Lam and Whitney 2016). The

evidences that is obtained here suggest that a furniture that cost $2000 was sold by Jasmine

for $5,000. On applying the special rules of “sec 118-10, ITA Act 1997” the capital gains

from furniture being a private use asset is disregarded in this situation.

a. Under “subdiv 152-B” a fifteen year exemption from capital gains is provided to the

small business.

b. As per “subdiv 152-C” a small business is permitted capital gain reduction by 50%.

c. With respect to “subdiv 152-D” a retirement capital gains exemption is permitted.

d. While under “subdiv 152-E” roll-over relief is provided to the taxpayer from capital

gains upon making asset replacement.

Jasmine is found to be selling her small cleaning business. At the time of sale,

Jasmine has yielded capital gains of $125,000 out of which $65,000 relates to business

equipment sale and $60,000 for goodwill. It can be stated that Jasmine is eligible for small

business CGT under “Div 152”. Additionally, under “sec 152-10, ITA Act 1997” the net

value of the CGT assets owned by Jasmine is within $6 million threshold limit (Sadiq and

Marsden 2014). The CGT asset under “sec 152-35, ITAA 1997” also meets the active asset

test. Therefore, Jasmine is eligible for claiming 15-year exemption from the disposal of her

CGT asset. Jasmine has owned the asset for a minimum of 15 years and she also ages more

than 55 years.

Answer D: Sale of Furniture:

It is essentially vital for the taxpayers to understand that under “sec 118-10, ITA Act

1997” capital gains that is realised from selling the personal use asset is simply disregarded

when the asset is purchased for lower $10,000 or low (Lam and Whitney 2016). The

evidences that is obtained here suggest that a furniture that cost $2000 was sold by Jasmine

for $5,000. On applying the special rules of “sec 118-10, ITA Act 1997” the capital gains

from furniture being a private use asset is disregarded in this situation.

5TAXATION LAW

Answer E: Sale of paintings:

As noted in “subdivision 108-B” it mainly deals with CGT assets known as

collectables. Accordingly, “sec 108-20 (2)” defines collectables as the type of assets that is

mainly held by taxpayer for private enjoyment purpose. Examples are paintings, sculptures,

jewellery, antiques and stamps (Minas, Lim and Evans 2018). Especially under “sec 118-10

(1)”, capital gains or loss happening from selling the collectables that has the acquisition

price of $500 or low is ignored. While capital gains from collectables is included for tax that

is bought for greater than $500.

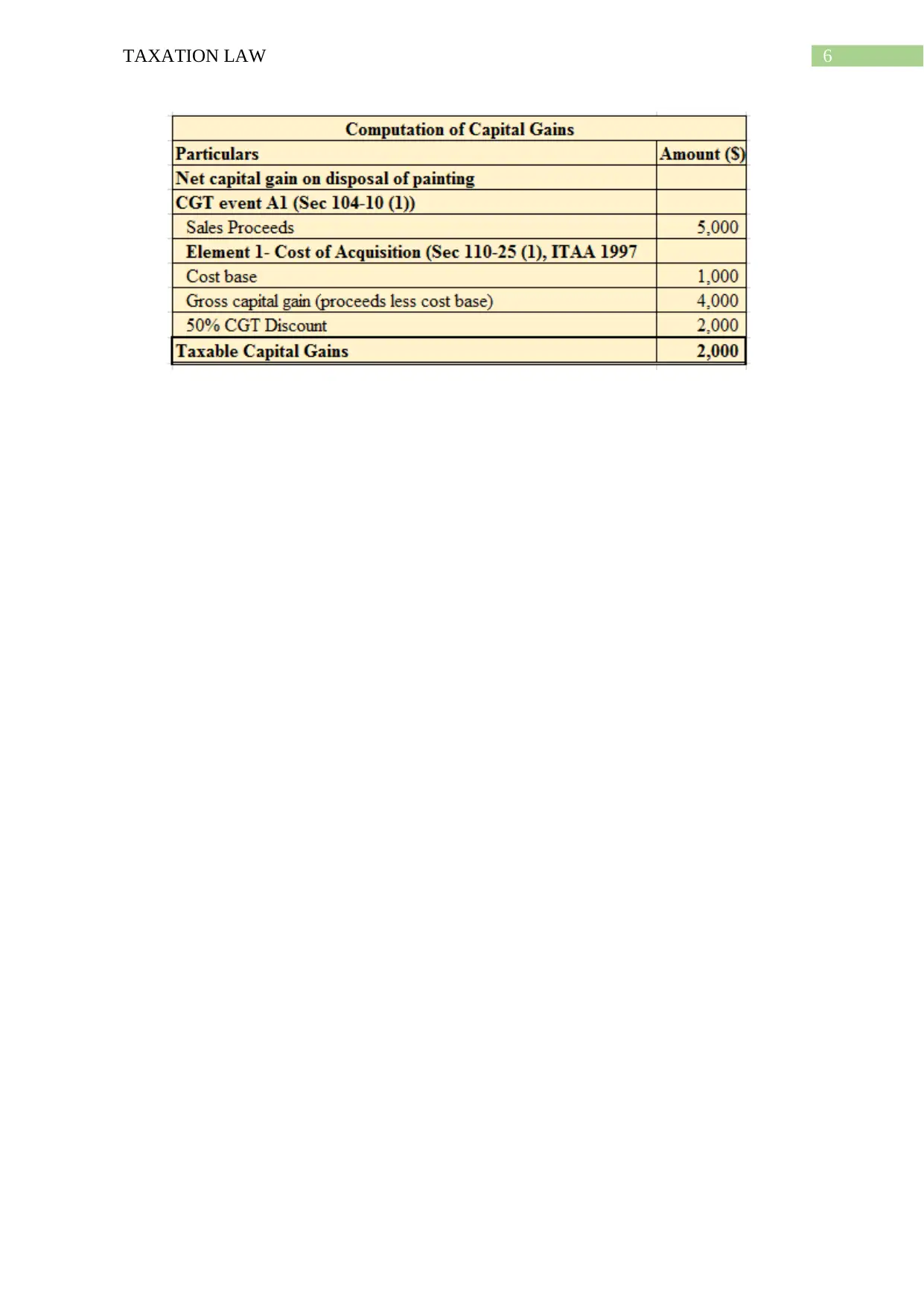

Jasmine has collection of numerous paintings. The paintings were purchased by

Jasmine for $500. However, all the paintings are sold for $35,000. Under “sec 108-20 (2)”

the paintings are recognized as collectables. Sale of paintings has led to “CGT Event A1”. As

none of the paintings cost no more than $500, within “sec 118-10 (1)”, the capital gains from

disposal of paintings are ignored (Joseph 2017). Despite the fact, there was also one

exception where a painting was purchased for $1,000. This painting was sold by Jasmine for

$5,000. Hence, a capital gains made in this regard. Therefore, the capital gains will be taxed

under the CGT regime.

Answer E: Sale of paintings:

As noted in “subdivision 108-B” it mainly deals with CGT assets known as

collectables. Accordingly, “sec 108-20 (2)” defines collectables as the type of assets that is

mainly held by taxpayer for private enjoyment purpose. Examples are paintings, sculptures,

jewellery, antiques and stamps (Minas, Lim and Evans 2018). Especially under “sec 118-10

(1)”, capital gains or loss happening from selling the collectables that has the acquisition

price of $500 or low is ignored. While capital gains from collectables is included for tax that

is bought for greater than $500.

Jasmine has collection of numerous paintings. The paintings were purchased by

Jasmine for $500. However, all the paintings are sold for $35,000. Under “sec 108-20 (2)”

the paintings are recognized as collectables. Sale of paintings has led to “CGT Event A1”. As

none of the paintings cost no more than $500, within “sec 118-10 (1)”, the capital gains from

disposal of paintings are ignored (Joseph 2017). Despite the fact, there was also one

exception where a painting was purchased for $1,000. This painting was sold by Jasmine for

$5,000. Hence, a capital gains made in this regard. Therefore, the capital gains will be taxed

under the CGT regime.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Answer to question 2:

Issues:

The issue considered in this factual situation of John is that whether he will be able to

get the access of “sec 40-25, ITA Act 1997” for claiming decline in value of the machine

bought during the year.

Laws:

A part of uniform capital allowances permits a taxpayer for deduction in respect of the

decline in value of depreciating asset in “Div 40, ITA Act 1997”. As a general note of

“Division 40, ITA Act 1997” the provision of capital allowance is commonly applicable on

the depreciating asset under “sec 40-30, ITA Act 97” which is not held as capital works. The

common provision of capital allowance under “Division 40” is not eligible for claim for all

the taxpayers (Phan 2016). The operative provision of “sec.40-25 (1), ITA Act 97”

pronounces that an individual taxpayer is permitted for claiming deduction equal to

depreciation amount for the income of a depreciating asset which the taxpayer has held it

during any part of the year.

As noted in “sec 40-30 (1)”, a depreciating asset is generally referred as the asset

which has the limited effective life and it is reasonably anticipated to fall in value with regard

to its usage. However, it must be noted that neither land nor trading stock has been

considered in this definition. Usually, assets are not defined and it should be assigned its

ordinary meaning based on the specific requirement of capital allowances (Pointon 2017).

The ordinary meaning of plant was considered by the federal court in the Australian case of

“FC of T v Wangaratta Woollen Mills Ltd [1969]”. The federal court stated that a structure

of dye-house was viewed as having the meaning of plant in contrast to the ordinary structure

Answer to question 2:

Issues:

The issue considered in this factual situation of John is that whether he will be able to

get the access of “sec 40-25, ITA Act 1997” for claiming decline in value of the machine

bought during the year.

Laws:

A part of uniform capital allowances permits a taxpayer for deduction in respect of the

decline in value of depreciating asset in “Div 40, ITA Act 1997”. As a general note of

“Division 40, ITA Act 1997” the provision of capital allowance is commonly applicable on

the depreciating asset under “sec 40-30, ITA Act 97” which is not held as capital works. The

common provision of capital allowance under “Division 40” is not eligible for claim for all

the taxpayers (Phan 2016). The operative provision of “sec.40-25 (1), ITA Act 97”

pronounces that an individual taxpayer is permitted for claiming deduction equal to

depreciation amount for the income of a depreciating asset which the taxpayer has held it

during any part of the year.

As noted in “sec 40-30 (1)”, a depreciating asset is generally referred as the asset

which has the limited effective life and it is reasonably anticipated to fall in value with regard

to its usage. However, it must be noted that neither land nor trading stock has been

considered in this definition. Usually, assets are not defined and it should be assigned its

ordinary meaning based on the specific requirement of capital allowances (Pointon 2017).

The ordinary meaning of plant was considered by the federal court in the Australian case of

“FC of T v Wangaratta Woollen Mills Ltd [1969]”. The federal court stated that a structure

of dye-house was viewed as having the meaning of plant in contrast to the ordinary structure

8TAXATION LAW

of a building. This is because the dye-house represented a tool in trade and plays a vital role

in the manufacturing procedure of the taxpayer.

“Division 40, ITA Act 1997” explains that a deduction for asset is allowed under the

capital allowance regime only when the asset is held for taxable purpose. For that reason,

under “sec 40-25 (7)”, the term taxable purpose represents the purpose of generating taxable

earnings (Armstrong 2016). The capital allowance regime of “Div 40, ITAA 1997” says that

a deduction the decline in value of the depreciating asset during the year of income is

permitted for claim by those that hold the asset all through the income year.

In calculating depreciation there are some relevant dates that should be considered

under the general capital allowance regime. With respect to “sec 40-60”, a depreciating asset

beings to depreciate when an individual taxpayer makes the first use of the asset or they have

installed the asset ready for assessable use purpose (Walrut 2013). While “sec 40-175” says

that depreciation is calculated based on the assets cost base. The cost base of the assets

usually contains two elements which are discussed below;

1st Element of Cost: The first element cost base includes the consideration that is

provided by the taxpayer for holding the asset. This commonly includes the

purchase price that is paid to purchase the asset.

2nd Element of Cost: The second element of cost base usually includes the

consideration that a taxpayer has provided to bring the asset in its present conditions

and location. This mostly takes account of cost involved in transportation, capital

improvements and installation expenses occurred to the asset.

Application:

The case study opens up with the scenario where it is noticed that John is the owner of

the manufacturing company which is largely involved in the production of BMW parts. In the

of a building. This is because the dye-house represented a tool in trade and plays a vital role

in the manufacturing procedure of the taxpayer.

“Division 40, ITA Act 1997” explains that a deduction for asset is allowed under the

capital allowance regime only when the asset is held for taxable purpose. For that reason,

under “sec 40-25 (7)”, the term taxable purpose represents the purpose of generating taxable

earnings (Armstrong 2016). The capital allowance regime of “Div 40, ITAA 1997” says that

a deduction the decline in value of the depreciating asset during the year of income is

permitted for claim by those that hold the asset all through the income year.

In calculating depreciation there are some relevant dates that should be considered

under the general capital allowance regime. With respect to “sec 40-60”, a depreciating asset

beings to depreciate when an individual taxpayer makes the first use of the asset or they have

installed the asset ready for assessable use purpose (Walrut 2013). While “sec 40-175” says

that depreciation is calculated based on the assets cost base. The cost base of the assets

usually contains two elements which are discussed below;

1st Element of Cost: The first element cost base includes the consideration that is

provided by the taxpayer for holding the asset. This commonly includes the

purchase price that is paid to purchase the asset.

2nd Element of Cost: The second element of cost base usually includes the

consideration that a taxpayer has provided to bring the asset in its present conditions

and location. This mostly takes account of cost involved in transportation, capital

improvements and installation expenses occurred to the asset.

Application:

The case study opens up with the scenario where it is noticed that John is the owner of

the manufacturing company which is largely involved in the production of BMW parts. In the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

meantime, the facts obtained from the case further contributes that John has bought a CNC

machine which he intends to use for his business. In regard to the operative provision of “sec

40-30 (1), ITA Act 97” the CNC machine is a depreciating asset (Mark and James 2016). By

referring to the factual situation of “FC of T v Wangaratta Woollen Mills Ltd [1969]”, the

depreciating asset has some degree of operational life and the CNC machine can reasonably

be anticipated to decrease in worth based on the time of its usage.

In the meantime, “sec 40-25 (7)”, contributes to the fact that the CNC machine was

bought by John wholly for taxable purpose. In other words, the CNC machine was bought for

producing taxable income. Under “Div 40, ITAA 1997” of the capital allowance regime, it is

necessary to determine the cost base of CNC machine (Mishra and Anwar 2017). As

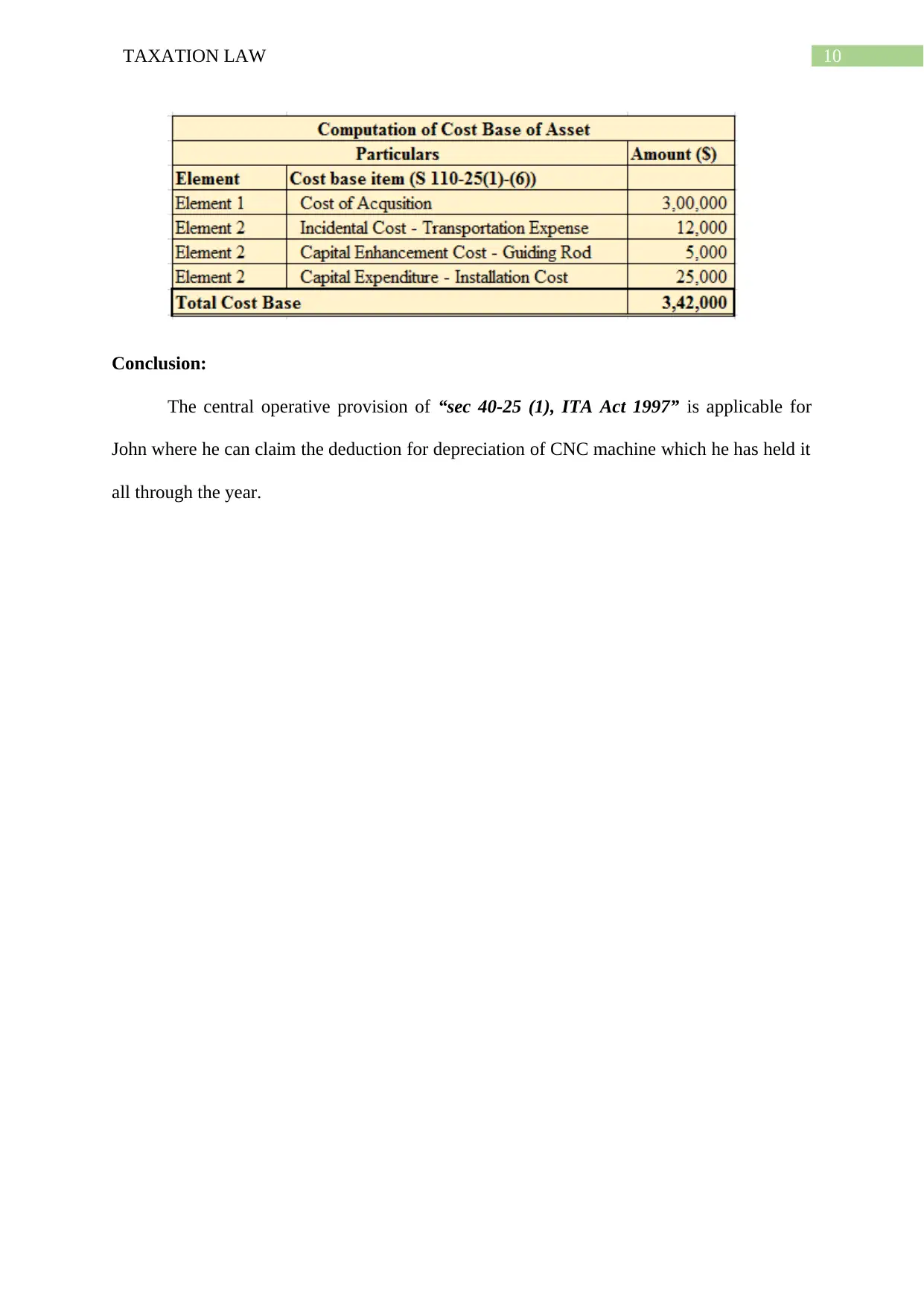

understood the machine was purchased by John by paying $300,000. With regard to “sec 40-

185”, the consideration paid by John to hold the CNC machine is included under the 1st

element of cost.

John further reports a cost of $25,000 incurred for installing the machine. He also

occurred an additional cost of $5,000 for adding a guiding rod in the CNC machine as this

will improve its performance. Denoting “sec 40-190, ITA Act 1997” the installation cost and

cost of adding a guiding rod will be included in the 2nd element cost of CNC machine.

To compute the decline of value of asset under “sec 40-25 (1), ITA Act 1997” the

start date of taxable use of CNC machine should be considered (Walrut 2013). As per the

case facts obtained, John completely installed the CNC machine on 15th January. Therefore,

under sec 40-60, the start date for decline in value of CNC machine is 15th January, for the

reason that John first used the machine from that day onwards for generating chargeable

business earnings.

meantime, the facts obtained from the case further contributes that John has bought a CNC

machine which he intends to use for his business. In regard to the operative provision of “sec

40-30 (1), ITA Act 97” the CNC machine is a depreciating asset (Mark and James 2016). By

referring to the factual situation of “FC of T v Wangaratta Woollen Mills Ltd [1969]”, the

depreciating asset has some degree of operational life and the CNC machine can reasonably

be anticipated to decrease in worth based on the time of its usage.

In the meantime, “sec 40-25 (7)”, contributes to the fact that the CNC machine was

bought by John wholly for taxable purpose. In other words, the CNC machine was bought for

producing taxable income. Under “Div 40, ITAA 1997” of the capital allowance regime, it is

necessary to determine the cost base of CNC machine (Mishra and Anwar 2017). As

understood the machine was purchased by John by paying $300,000. With regard to “sec 40-

185”, the consideration paid by John to hold the CNC machine is included under the 1st

element of cost.

John further reports a cost of $25,000 incurred for installing the machine. He also

occurred an additional cost of $5,000 for adding a guiding rod in the CNC machine as this

will improve its performance. Denoting “sec 40-190, ITA Act 1997” the installation cost and

cost of adding a guiding rod will be included in the 2nd element cost of CNC machine.

To compute the decline of value of asset under “sec 40-25 (1), ITA Act 1997” the

start date of taxable use of CNC machine should be considered (Walrut 2013). As per the

case facts obtained, John completely installed the CNC machine on 15th January. Therefore,

under sec 40-60, the start date for decline in value of CNC machine is 15th January, for the

reason that John first used the machine from that day onwards for generating chargeable

business earnings.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Conclusion:

The central operative provision of “sec 40-25 (1), ITA Act 1997” is applicable for

John where he can claim the deduction for depreciation of CNC machine which he has held it

all through the year.

Conclusion:

The central operative provision of “sec 40-25 (1), ITA Act 1997” is applicable for

John where he can claim the deduction for depreciation of CNC machine which he has held it

all through the year.

11TAXATION LAW

References:

Armstrong, M., 2016. CGT withholding on real estate transactions in Australia. Mondaq

Business Briefing, pp.Mondaq Business Briefing, March 11, 2016.

Emma L, 2018. CGT: changes to threshold and rate for foreign resident capital gains

withholding payments. Mondaq Business Briefing, pp.Mondaq Business Briefing, May 2,

2018.

Gordon, R., 2017. Proposed changes to CGT main residence exemption for foreign residents.

Mondaq Business Briefing, pp.Mondaq Business Briefing, August 22, 2017.

Joseph, M., 2017. Dissolving strata title and the potential for capital gains tax (CGT) liability.

Mondaq Business Briefing, pp.Mondaq Business Briefing, April 26, 2017.

Lam, D. and Whitney, A., 2016. Practical aspects of the new foreign resident CGT

withholding tax. LSJ: Law Society of NSW Journal, (21), p.84.

Mark, K and James, M, 2016. PM weighs higher capital gains tax. The Age (Melbourne,

Australia), p.4.

Minas, J, Lim, Y and Evans, C, 2018. The impact of tax rate changes on capital gains

realisations: Evidence from Australia. Australian Tax Forum, 33(4), pp.635–666.

Mishra, A.V. and Anwar, S., 2017. Foreign portfolio equity holdings and capital gains

taxation. International Review of Financial Analysis, 51, pp.54–68.

Phan, L., 2016. Australia's Foreign Resident Capital Gains Tax Withholding Regime.

Mondaq Business Briefing, pp.Mondaq Business Briefing, Sept 29, 2016.

Pointon, A., 2017. Separating business and personal property, and the application of the CGT

roll-overs. Mondaq Business Briefing, pp.Mondaq Business Briefing, June 25, 2017.

References:

Armstrong, M., 2016. CGT withholding on real estate transactions in Australia. Mondaq

Business Briefing, pp.Mondaq Business Briefing, March 11, 2016.

Emma L, 2018. CGT: changes to threshold and rate for foreign resident capital gains

withholding payments. Mondaq Business Briefing, pp.Mondaq Business Briefing, May 2,

2018.

Gordon, R., 2017. Proposed changes to CGT main residence exemption for foreign residents.

Mondaq Business Briefing, pp.Mondaq Business Briefing, August 22, 2017.

Joseph, M., 2017. Dissolving strata title and the potential for capital gains tax (CGT) liability.

Mondaq Business Briefing, pp.Mondaq Business Briefing, April 26, 2017.

Lam, D. and Whitney, A., 2016. Practical aspects of the new foreign resident CGT

withholding tax. LSJ: Law Society of NSW Journal, (21), p.84.

Mark, K and James, M, 2016. PM weighs higher capital gains tax. The Age (Melbourne,

Australia), p.4.

Minas, J, Lim, Y and Evans, C, 2018. The impact of tax rate changes on capital gains

realisations: Evidence from Australia. Australian Tax Forum, 33(4), pp.635–666.

Mishra, A.V. and Anwar, S., 2017. Foreign portfolio equity holdings and capital gains

taxation. International Review of Financial Analysis, 51, pp.54–68.

Phan, L., 2016. Australia's Foreign Resident Capital Gains Tax Withholding Regime.

Mondaq Business Briefing, pp.Mondaq Business Briefing, Sept 29, 2016.

Pointon, A., 2017. Separating business and personal property, and the application of the CGT

roll-overs. Mondaq Business Briefing, pp.Mondaq Business Briefing, June 25, 2017.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.