HI6028 Taxation Law Assignment: CGT, Income from Personal Exertion

VerifiedAdded on 2022/11/26

|6

|2428

|157

Homework Assignment

AI Summary

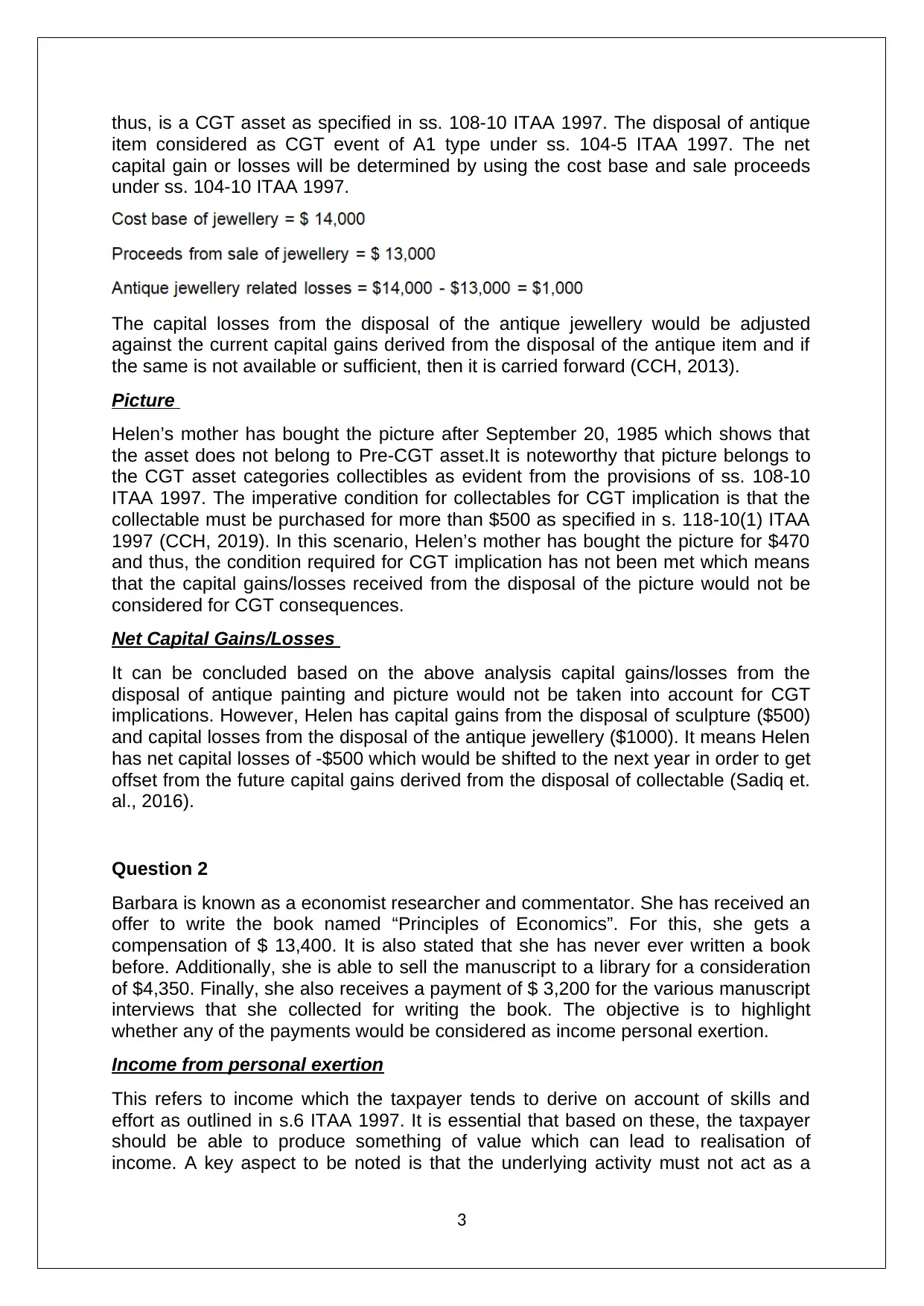

This assignment addresses key aspects of Australian taxation law, as applied to various scenarios. Question 1 focuses on Capital Gains Tax (CGT), analyzing the tax implications of selling different assets, including an antique painting, sculpture, and jewellery, as well as a picture, considering pre-CGT assets and the $500 threshold for collectables. Question 2 delves into income from personal exertion, examining whether payments received by an economist researcher for writing a book, selling the manuscript, and conducting manuscript interviews constitute assessable income. Question 3 explores the tax treatment of a loan provided by a father to his son for business purposes, specifically concerning the principal repayment and an additional payment, determining whether these amounts are considered assessable income or non-assessable income, such as a gift. The assignment demonstrates an understanding of the Australian income tax system, applying taxation principles to real-life problems, and interpreting relevant taxation legislations.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.