Taxation Law Assignment: Analysis of Tax Issues, HI6028, T2 2019

VerifiedAdded on 2022/10/12

|8

|2693

|14

Homework Assignment

AI Summary

This taxation law assignment addresses key aspects of Australian taxation law, focusing on GST and Capital Gains Tax (CGT). The assignment analyzes a case study involving a company's claim for input tax credit on land and legal services, citing relevant legislation and case law to determine eligibility. The analysis concludes that the company is ineligible for input tax credit on the land but eligible for legal services. The assignment further explores CGT implications, examining scenarios involving the sale of land, shares, and a stamp collection, detailing cost base calculations and tax implications for each. The document also includes a discussion of pre-CGT assets and the treatment of collectibles. The assignment demonstrates the application of taxation principles to real-life problems, providing comprehensive solutions to complex tax issues.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:...................................................................................................2

Answer to Question 2...................................................................................................3

References:..................................................................................................................7

Table of Contents

Answer to question 1:...................................................................................................2

Answer to Question 2...................................................................................................3

References:..................................................................................................................7

2TAXATION LAW

Answer to question 1:

Issues:

The question will be dealing with the matters related to the claim of input tax

credit for the transactions that are occurred during the year.

Laws:

The “GSTR ruling of 2008/1” puts forward that to claim the input tax credit

there should be a creditable acquisition or importation. For the taxpayers, if they are

make the creditable purchase then it should be exclusively or to some extent for the

commercial activities of business (James, Sawyer and Wallschutzky 2015). The

explanation that has been given in the ruling explains that there are some important

factors that are required to be considered while making in purchase or importation

for the creditable purpose. The ruling mainly addresses whether the purchase or the

import has been made at the time of carrying the enterprise or whether it is of private

or domestic in nature. It also includes whether the taxpayer has purchased anything

which is associated to making the supplies which would be input taxed.

The ruling generally accounts for input tax credit chiefly with companies that are

carrying the enterprise which results in making of supplies. Entities which are

registered under the GST are usually entitled to making input tax credit only from the

creditable purchase and imports. The creditable purchase has been dealt under the

“division 11” while the creditable imports has been dealt under the “division 15” (May

2016). As a general note, under “sec 11-5”, an entity that is registered for GST

makes creditable purchase when the purchase anything completely for use in

business. It also includes that the supply of thing to the entity amounts to a taxable

supply.

On the other hand, the creditable purpose has been dealt in “sec 11-15”. According

to the central provision of “sec 11-15” an entity generally purchases a thing for

creditable purpose only when the entity is carrying the enterprise activity (Krever and

Teoh 2017). The GST in Australia is regarded as the multi-stage valued added tax.

This tax is commonly borne at the time of final consumption of goods and services.

One of the fundamental aspect of the value added tax is that taxes are imposed at

every point based on which the value is added before the final consumption.

The law court in “HP Mercantile Pty Ltd v CT (2005)” stated that in case a taxpayer

that makes the input tax supplies, then in such situation no output tax will be liable

on the supplies made by the taxpayer that meets the description of input tax supplies

(Thistleton 2016). The taxpayer in such a situation will be left without any input tax

credit relating to taxes payable on the purchase where any necessary relationship is

existent. As a common rule, the main intention of the input tax credit is that it aims in

offsetting the GST that is included in the price the taxpayers have paid for an

acquisition provided that the purchase made is for the use of company’s business

activities.

It must be noted by the taxpayers at times there will be few situations where

purchases pay the GST. This is known as reverse charge. The taxpayers must

denote that reverse charge is usually required for some offshore purchase, in spite of

the fact that they are the purchaser and even after the fact that the sale would

commonly attract GST liability (Seiden and Apkarian 2017). The taxpayer might

choose to pay the GST for the purchase made despite the fact that they are

purchaser. There may be things apart from the real property or goods which attracts

GST when it is purchased by the Australian business and things are done out of

Australia or made with the help of business which is performed by the sellers out of

Answer to question 1:

Issues:

The question will be dealing with the matters related to the claim of input tax

credit for the transactions that are occurred during the year.

Laws:

The “GSTR ruling of 2008/1” puts forward that to claim the input tax credit

there should be a creditable acquisition or importation. For the taxpayers, if they are

make the creditable purchase then it should be exclusively or to some extent for the

commercial activities of business (James, Sawyer and Wallschutzky 2015). The

explanation that has been given in the ruling explains that there are some important

factors that are required to be considered while making in purchase or importation

for the creditable purpose. The ruling mainly addresses whether the purchase or the

import has been made at the time of carrying the enterprise or whether it is of private

or domestic in nature. It also includes whether the taxpayer has purchased anything

which is associated to making the supplies which would be input taxed.

The ruling generally accounts for input tax credit chiefly with companies that are

carrying the enterprise which results in making of supplies. Entities which are

registered under the GST are usually entitled to making input tax credit only from the

creditable purchase and imports. The creditable purchase has been dealt under the

“division 11” while the creditable imports has been dealt under the “division 15” (May

2016). As a general note, under “sec 11-5”, an entity that is registered for GST

makes creditable purchase when the purchase anything completely for use in

business. It also includes that the supply of thing to the entity amounts to a taxable

supply.

On the other hand, the creditable purpose has been dealt in “sec 11-15”. According

to the central provision of “sec 11-15” an entity generally purchases a thing for

creditable purpose only when the entity is carrying the enterprise activity (Krever and

Teoh 2017). The GST in Australia is regarded as the multi-stage valued added tax.

This tax is commonly borne at the time of final consumption of goods and services.

One of the fundamental aspect of the value added tax is that taxes are imposed at

every point based on which the value is added before the final consumption.

The law court in “HP Mercantile Pty Ltd v CT (2005)” stated that in case a taxpayer

that makes the input tax supplies, then in such situation no output tax will be liable

on the supplies made by the taxpayer that meets the description of input tax supplies

(Thistleton 2016). The taxpayer in such a situation will be left without any input tax

credit relating to taxes payable on the purchase where any necessary relationship is

existent. As a common rule, the main intention of the input tax credit is that it aims in

offsetting the GST that is included in the price the taxpayers have paid for an

acquisition provided that the purchase made is for the use of company’s business

activities.

It must be noted by the taxpayers at times there will be few situations where

purchases pay the GST. This is known as reverse charge. The taxpayers must

denote that reverse charge is usually required for some offshore purchase, in spite of

the fact that they are the purchaser and even after the fact that the sale would

commonly attract GST liability (Seiden and Apkarian 2017). The taxpayer might

choose to pay the GST for the purchase made despite the fact that they are

purchaser. There may be things apart from the real property or goods which attracts

GST when it is purchased by the Australian business and things are done out of

Australia or made with the help of business which is performed by the sellers out of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Australia. Under such kind of situation, the taxpayers are under obligation of paying

GST despite the fact that they are purchaser and sellers does not have to pay GST

on the sales made.

Application:

On applying the above given laws in the factual case of City Sky Co which is

registered under GST and also eligible for claiming input tax credit as and when

applicable. It is noticed that the company has bought a vacant land and looks to

construct 15 flats to sell. Commonly, land must be considered as property which is

not movable by City Sky Co. The purchase of land by City Sky Co is not eligible for

GST (Krever and Teoh 2017). Consequently, no such GST is required to paid on

land by the purchaser in the current case. As the case progresses, it is noticed that

City Sky Co is looking to build apartments on the vacant land.

The City Sky Co must denote that the vacant land is falling inside the

provision of black credit. This represents that purchase of products or services by a

taxable entity for enabling construction on the immovable property as the bid to

progress the business further is not considered eligible for claiming input tax credit.

City Sky Co cannot claim any input tax credit for acquiring the vacant land.

The case study also contributes that Maurice Blackburn provided legal service to

City Sky Co. The legal services sought were mainly for the land developmental

purpose and incurred an expense of $33,000. The services that is taken by City Sky

Co is falling inside the mechanism of reverse charge. As per this mechanism the

liability of paying GST is falling on the City Sky Co being the service receiver.

Reference to “sec 11-5, of the GST Act 1999” can also be made to treat the

service as the creditable acquisition (Hanegbi and Obst 2015). The services were

sought by City Sky Co solely for the creditable business purpose. Citing “HP

Mercantile Pty Ltd v CT (2005)” City Sky Co will be considered eligible for claiming

input tax credit for the legal services received from Maurice Blackburn.

Conclusion:

The above given analysis contributes to the fact that City Sky Co is not

permitted for claiming the input tax credit on the vacant land. While the company is

eligible for claiming input tax credit on the legal services received.

Answer to Question 2

Sale of Land

In case of capital gain taxation, the most common occurrence in terms of an

event is the “CGT event A1” which attracts capital gains taxes on sale of an asset.

A “CGT event A1” occurs within the meaning stated in “Section 104(10) of ITAA

1997” when a CGT asset is sold off for a gain or when there is a change in the

ownership of the asset covered under “Section 104(10)(2) of ITAA 1997”. In such a

situation, the taxpayer needs to have a contract of sale for the asset as the same

would be signifying if there was sale of asset or just a transfer of ownership covered

within the meaning of “Section 104(10) of ITAA 1997”. Further, it is also important

for the taxpayer to ascertain the cost base of the asset for the purpose of computing

the capital gains arising from the same. As per the provisions of “Section 110(25) of

ITAA 1997” there are total of five element which must be considered for the cost

base of the asset considered for capital gains.

The first element recognised in the cost base of the asset is the acquisition

value or cost of the asset and the same is covered in subsection 2 of Section

110(25) which reflects the amount at which the asset was actually acquired. In other

Australia. Under such kind of situation, the taxpayers are under obligation of paying

GST despite the fact that they are purchaser and sellers does not have to pay GST

on the sales made.

Application:

On applying the above given laws in the factual case of City Sky Co which is

registered under GST and also eligible for claiming input tax credit as and when

applicable. It is noticed that the company has bought a vacant land and looks to

construct 15 flats to sell. Commonly, land must be considered as property which is

not movable by City Sky Co. The purchase of land by City Sky Co is not eligible for

GST (Krever and Teoh 2017). Consequently, no such GST is required to paid on

land by the purchaser in the current case. As the case progresses, it is noticed that

City Sky Co is looking to build apartments on the vacant land.

The City Sky Co must denote that the vacant land is falling inside the

provision of black credit. This represents that purchase of products or services by a

taxable entity for enabling construction on the immovable property as the bid to

progress the business further is not considered eligible for claiming input tax credit.

City Sky Co cannot claim any input tax credit for acquiring the vacant land.

The case study also contributes that Maurice Blackburn provided legal service to

City Sky Co. The legal services sought were mainly for the land developmental

purpose and incurred an expense of $33,000. The services that is taken by City Sky

Co is falling inside the mechanism of reverse charge. As per this mechanism the

liability of paying GST is falling on the City Sky Co being the service receiver.

Reference to “sec 11-5, of the GST Act 1999” can also be made to treat the

service as the creditable acquisition (Hanegbi and Obst 2015). The services were

sought by City Sky Co solely for the creditable business purpose. Citing “HP

Mercantile Pty Ltd v CT (2005)” City Sky Co will be considered eligible for claiming

input tax credit for the legal services received from Maurice Blackburn.

Conclusion:

The above given analysis contributes to the fact that City Sky Co is not

permitted for claiming the input tax credit on the vacant land. While the company is

eligible for claiming input tax credit on the legal services received.

Answer to Question 2

Sale of Land

In case of capital gain taxation, the most common occurrence in terms of an

event is the “CGT event A1” which attracts capital gains taxes on sale of an asset.

A “CGT event A1” occurs within the meaning stated in “Section 104(10) of ITAA

1997” when a CGT asset is sold off for a gain or when there is a change in the

ownership of the asset covered under “Section 104(10)(2) of ITAA 1997”. In such a

situation, the taxpayer needs to have a contract of sale for the asset as the same

would be signifying if there was sale of asset or just a transfer of ownership covered

within the meaning of “Section 104(10) of ITAA 1997”. Further, it is also important

for the taxpayer to ascertain the cost base of the asset for the purpose of computing

the capital gains arising from the same. As per the provisions of “Section 110(25) of

ITAA 1997” there are total of five element which must be considered for the cost

base of the asset considered for capital gains.

The first element recognised in the cost base of the asset is the acquisition

value or cost of the asset and the same is covered in subsection 2 of Section

110(25) which reflects the amount at which the asset was actually acquired. In other

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

words, the same would also be including market value for the asset and any extra

payments which is made by the taxpayer (Barkoczy 2016). The second principle

covered within the cost base of an asset is the incidental costs incurred for acquiring

the asset. These types of costs are extra and includes transfer fee, legal costs,

stamp duty and similar other costs.

The third element which is included in the cost base is provided in

subsection 4 of Section 110(25) and the same deals with the cost of ownership of

the asset. Such a cost refers to the cost of maintenance which the taxpayer needs to

bear and the same involves repairing expenses, interest payments, rates or any form

of capital expenses undertaken by the business (Faccio and Xu 2015). The fourth

element involves the improvement costs which is undertaken to make improvements

to the asset. Any improvement in the value of the asset or the efficiency of the asset

is considered to be an improvement in the asset. The fifth expense which forms a

cost base of the asset is the capital expenses or establishing title of ownership of the

asset or defending the same.

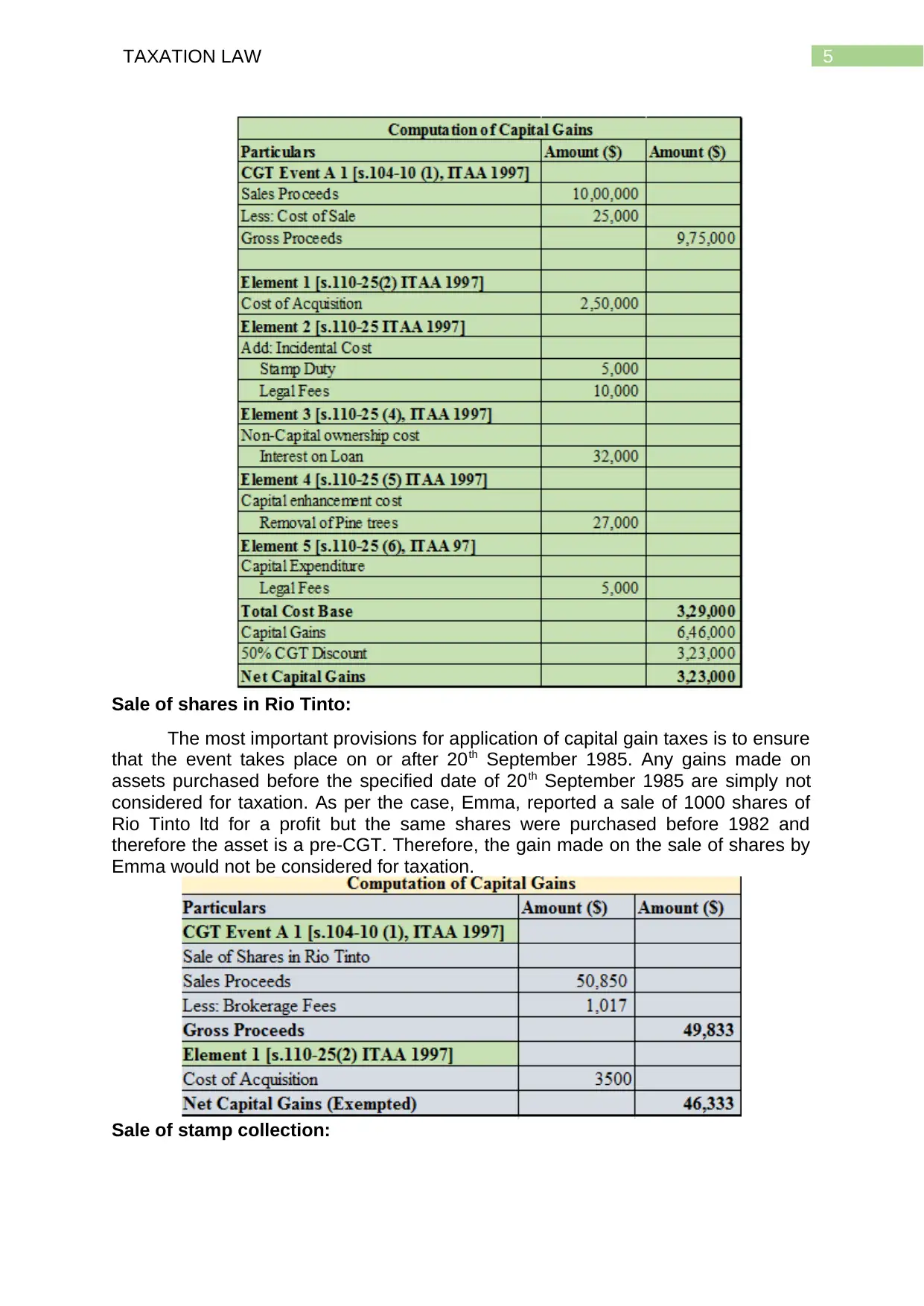

As per the case shown. Emma owns a land which was originally purchased in

1991 for a sum of $ 250,000 and Emma sold the same for $ 1,000,000. This would

be attracting “CGT event A1” as per the regulations of “Section 104(10) of ITAA

1997”. Emma further incurred expenses for stamp duty and legal fees for $ 5,000

and $ 10,000 respectively. These costs would be considered as incidental costs and

would be considered within the second element of cost base (Eccleston and Woolley

2014). Further expenses were also incurred such as interest on loan, water rates,

insurance and council rates. All these costs would be considered within the cost

base of the asset within the meaning of subsection 4 of Section 110(25) of ITTA

1997.

Emma also incurred legal expenses for $ 5,000 for settling a dispute over the

land and use of the neighbour of the land. The legal fees would be covered under

the title costs and would be considered under the fifth element of cost base. In

addition to this, an expense of $ 27,000 was paid to remove pine trees from the

property which can be treated as an enhancement made to the property which is a

part of the fourth element of the cost base of the asset. The cost base of the asset is

computed below:

words, the same would also be including market value for the asset and any extra

payments which is made by the taxpayer (Barkoczy 2016). The second principle

covered within the cost base of an asset is the incidental costs incurred for acquiring

the asset. These types of costs are extra and includes transfer fee, legal costs,

stamp duty and similar other costs.

The third element which is included in the cost base is provided in

subsection 4 of Section 110(25) and the same deals with the cost of ownership of

the asset. Such a cost refers to the cost of maintenance which the taxpayer needs to

bear and the same involves repairing expenses, interest payments, rates or any form

of capital expenses undertaken by the business (Faccio and Xu 2015). The fourth

element involves the improvement costs which is undertaken to make improvements

to the asset. Any improvement in the value of the asset or the efficiency of the asset

is considered to be an improvement in the asset. The fifth expense which forms a

cost base of the asset is the capital expenses or establishing title of ownership of the

asset or defending the same.

As per the case shown. Emma owns a land which was originally purchased in

1991 for a sum of $ 250,000 and Emma sold the same for $ 1,000,000. This would

be attracting “CGT event A1” as per the regulations of “Section 104(10) of ITAA

1997”. Emma further incurred expenses for stamp duty and legal fees for $ 5,000

and $ 10,000 respectively. These costs would be considered as incidental costs and

would be considered within the second element of cost base (Eccleston and Woolley

2014). Further expenses were also incurred such as interest on loan, water rates,

insurance and council rates. All these costs would be considered within the cost

base of the asset within the meaning of subsection 4 of Section 110(25) of ITTA

1997.

Emma also incurred legal expenses for $ 5,000 for settling a dispute over the

land and use of the neighbour of the land. The legal fees would be covered under

the title costs and would be considered under the fifth element of cost base. In

addition to this, an expense of $ 27,000 was paid to remove pine trees from the

property which can be treated as an enhancement made to the property which is a

part of the fourth element of the cost base of the asset. The cost base of the asset is

computed below:

5TAXATION LAW

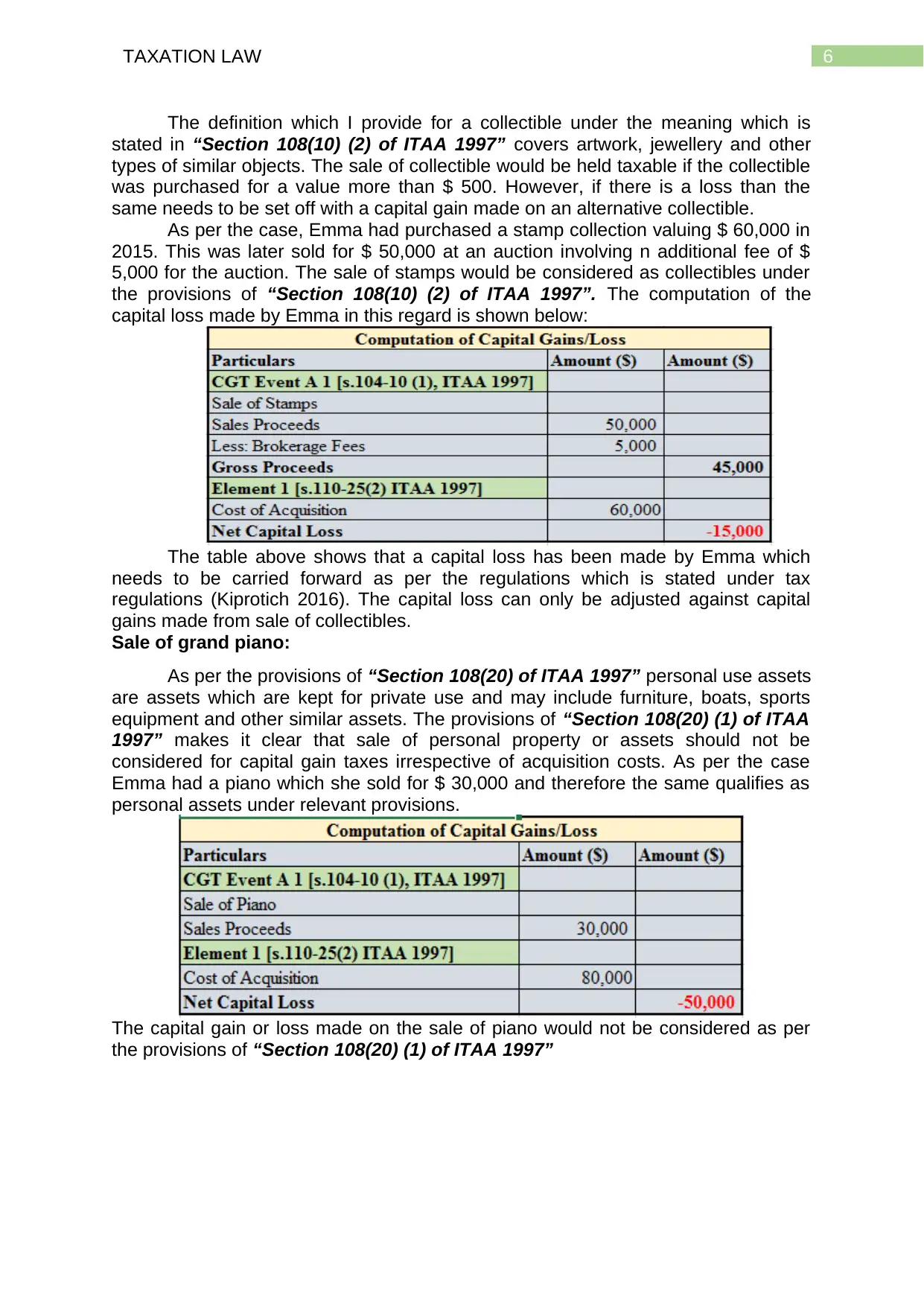

Sale of shares in Rio Tinto:

The most important provisions for application of capital gain taxes is to ensure

that the event takes place on or after 20th September 1985. Any gains made on

assets purchased before the specified date of 20th September 1985 are simply not

considered for taxation. As per the case, Emma, reported a sale of 1000 shares of

Rio Tinto ltd for a profit but the same shares were purchased before 1982 and

therefore the asset is a pre-CGT. Therefore, the gain made on the sale of shares by

Emma would not be considered for taxation.

Sale of stamp collection:

Sale of shares in Rio Tinto:

The most important provisions for application of capital gain taxes is to ensure

that the event takes place on or after 20th September 1985. Any gains made on

assets purchased before the specified date of 20th September 1985 are simply not

considered for taxation. As per the case, Emma, reported a sale of 1000 shares of

Rio Tinto ltd for a profit but the same shares were purchased before 1982 and

therefore the asset is a pre-CGT. Therefore, the gain made on the sale of shares by

Emma would not be considered for taxation.

Sale of stamp collection:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

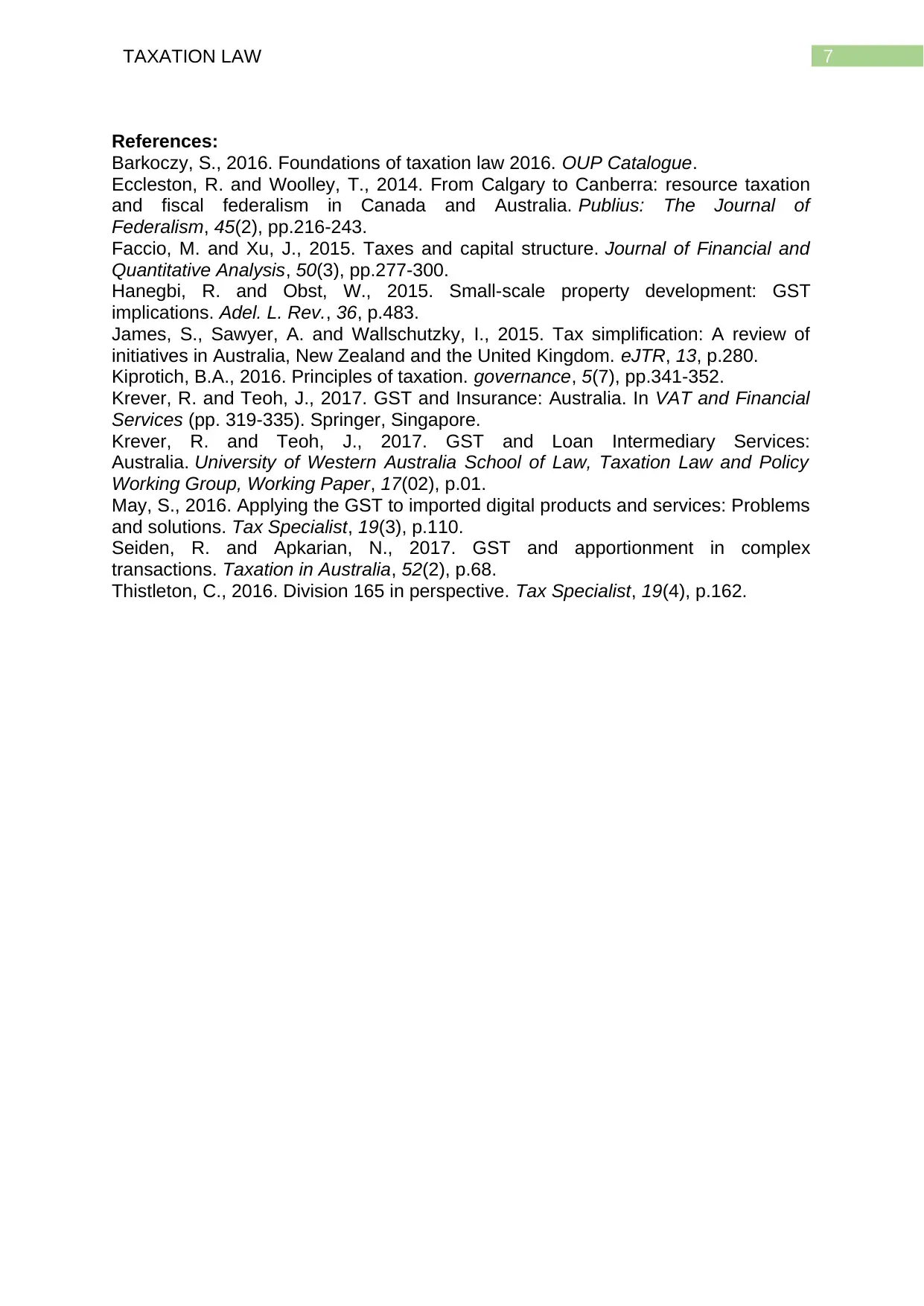

The definition which I provide for a collectible under the meaning which is

stated in “Section 108(10) (2) of ITAA 1997” covers artwork, jewellery and other

types of similar objects. The sale of collectible would be held taxable if the collectible

was purchased for a value more than $ 500. However, if there is a loss than the

same needs to be set off with a capital gain made on an alternative collectible.

As per the case, Emma had purchased a stamp collection valuing $ 60,000 in

2015. This was later sold for $ 50,000 at an auction involving n additional fee of $

5,000 for the auction. The sale of stamps would be considered as collectibles under

the provisions of “Section 108(10) (2) of ITAA 1997”. The computation of the

capital loss made by Emma in this regard is shown below:

The table above shows that a capital loss has been made by Emma which

needs to be carried forward as per the regulations which is stated under tax

regulations (Kiprotich 2016). The capital loss can only be adjusted against capital

gains made from sale of collectibles.

Sale of grand piano:

As per the provisions of “Section 108(20) of ITAA 1997” personal use assets

are assets which are kept for private use and may include furniture, boats, sports

equipment and other similar assets. The provisions of “Section 108(20) (1) of ITAA

1997” makes it clear that sale of personal property or assets should not be

considered for capital gain taxes irrespective of acquisition costs. As per the case

Emma had a piano which she sold for $ 30,000 and therefore the same qualifies as

personal assets under relevant provisions.

The capital gain or loss made on the sale of piano would not be considered as per

the provisions of “Section 108(20) (1) of ITAA 1997”

The definition which I provide for a collectible under the meaning which is

stated in “Section 108(10) (2) of ITAA 1997” covers artwork, jewellery and other

types of similar objects. The sale of collectible would be held taxable if the collectible

was purchased for a value more than $ 500. However, if there is a loss than the

same needs to be set off with a capital gain made on an alternative collectible.

As per the case, Emma had purchased a stamp collection valuing $ 60,000 in

2015. This was later sold for $ 50,000 at an auction involving n additional fee of $

5,000 for the auction. The sale of stamps would be considered as collectibles under

the provisions of “Section 108(10) (2) of ITAA 1997”. The computation of the

capital loss made by Emma in this regard is shown below:

The table above shows that a capital loss has been made by Emma which

needs to be carried forward as per the regulations which is stated under tax

regulations (Kiprotich 2016). The capital loss can only be adjusted against capital

gains made from sale of collectibles.

Sale of grand piano:

As per the provisions of “Section 108(20) of ITAA 1997” personal use assets

are assets which are kept for private use and may include furniture, boats, sports

equipment and other similar assets. The provisions of “Section 108(20) (1) of ITAA

1997” makes it clear that sale of personal property or assets should not be

considered for capital gain taxes irrespective of acquisition costs. As per the case

Emma had a piano which she sold for $ 30,000 and therefore the same qualifies as

personal assets under relevant provisions.

The capital gain or loss made on the sale of piano would not be considered as per

the provisions of “Section 108(20) (1) of ITAA 1997”

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

References:

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Eccleston, R. and Woolley, T., 2014. From Calgary to Canberra: resource taxation

and fiscal federalism in Canada and Australia. Publius: The Journal of

Federalism, 45(2), pp.216-243.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and

Quantitative Analysis, 50(3), pp.277-300.

Hanegbi, R. and Obst, W., 2015. Small-scale property development: GST

implications. Adel. L. Rev., 36, p.483.

James, S., Sawyer, A. and Wallschutzky, I., 2015. Tax simplification: A review of

initiatives in Australia, New Zealand and the United Kingdom. eJTR, 13, p.280.

Kiprotich, B.A., 2016. Principles of taxation. governance, 5(7), pp.341-352.

Krever, R. and Teoh, J., 2017. GST and Insurance: Australia. In VAT and Financial

Services (pp. 319-335). Springer, Singapore.

Krever, R. and Teoh, J., 2017. GST and Loan Intermediary Services:

Australia. University of Western Australia School of Law, Taxation Law and Policy

Working Group, Working Paper, 17(02), p.01.

May, S., 2016. Applying the GST to imported digital products and services: Problems

and solutions. Tax Specialist, 19(3), p.110.

Seiden, R. and Apkarian, N., 2017. GST and apportionment in complex

transactions. Taxation in Australia, 52(2), p.68.

Thistleton, C., 2016. Division 165 in perspective. Tax Specialist, 19(4), p.162.

References:

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Eccleston, R. and Woolley, T., 2014. From Calgary to Canberra: resource taxation

and fiscal federalism in Canada and Australia. Publius: The Journal of

Federalism, 45(2), pp.216-243.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and

Quantitative Analysis, 50(3), pp.277-300.

Hanegbi, R. and Obst, W., 2015. Small-scale property development: GST

implications. Adel. L. Rev., 36, p.483.

James, S., Sawyer, A. and Wallschutzky, I., 2015. Tax simplification: A review of

initiatives in Australia, New Zealand and the United Kingdom. eJTR, 13, p.280.

Kiprotich, B.A., 2016. Principles of taxation. governance, 5(7), pp.341-352.

Krever, R. and Teoh, J., 2017. GST and Insurance: Australia. In VAT and Financial

Services (pp. 319-335). Springer, Singapore.

Krever, R. and Teoh, J., 2017. GST and Loan Intermediary Services:

Australia. University of Western Australia School of Law, Taxation Law and Policy

Working Group, Working Paper, 17(02), p.01.

May, S., 2016. Applying the GST to imported digital products and services: Problems

and solutions. Tax Specialist, 19(3), p.110.

Seiden, R. and Apkarian, N., 2017. GST and apportionment in complex

transactions. Taxation in Australia, 52(2), p.68.

Thistleton, C., 2016. Division 165 in perspective. Tax Specialist, 19(4), p.162.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.